Cold Plasma In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

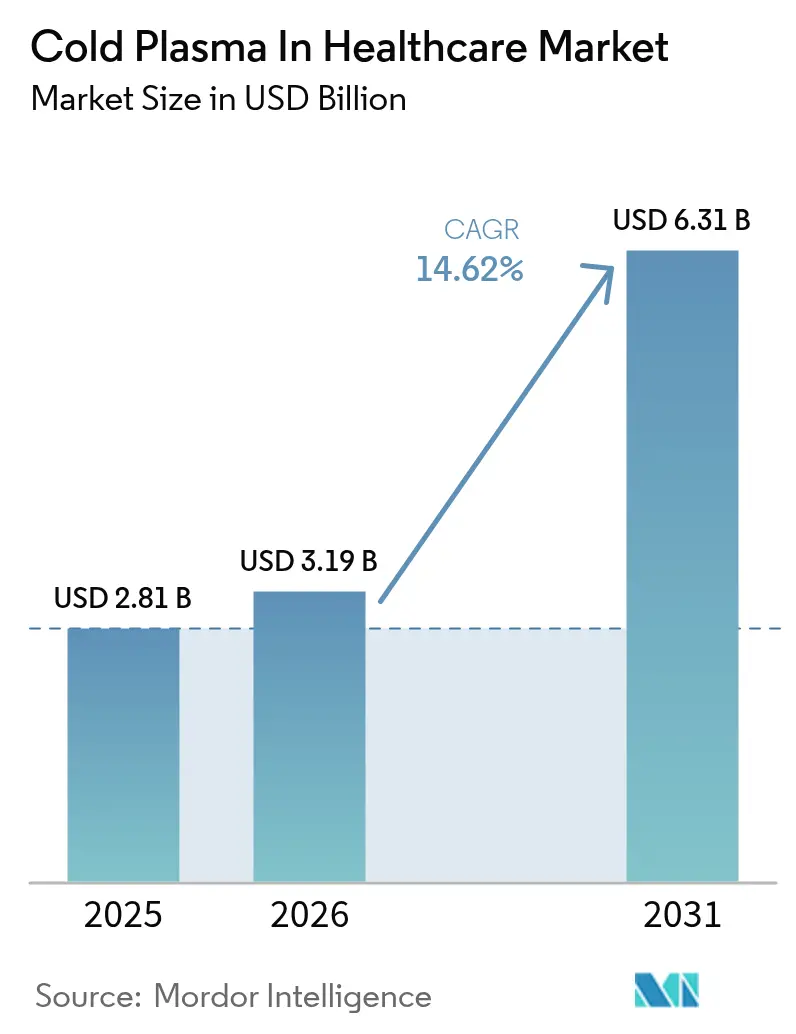

| Market Size (2026) | USD 3.19 Billion |

| Market Size (2031) | USD 6.31 Billion |

| Growth Rate (2026 - 2031) | 14.62% CAGR |

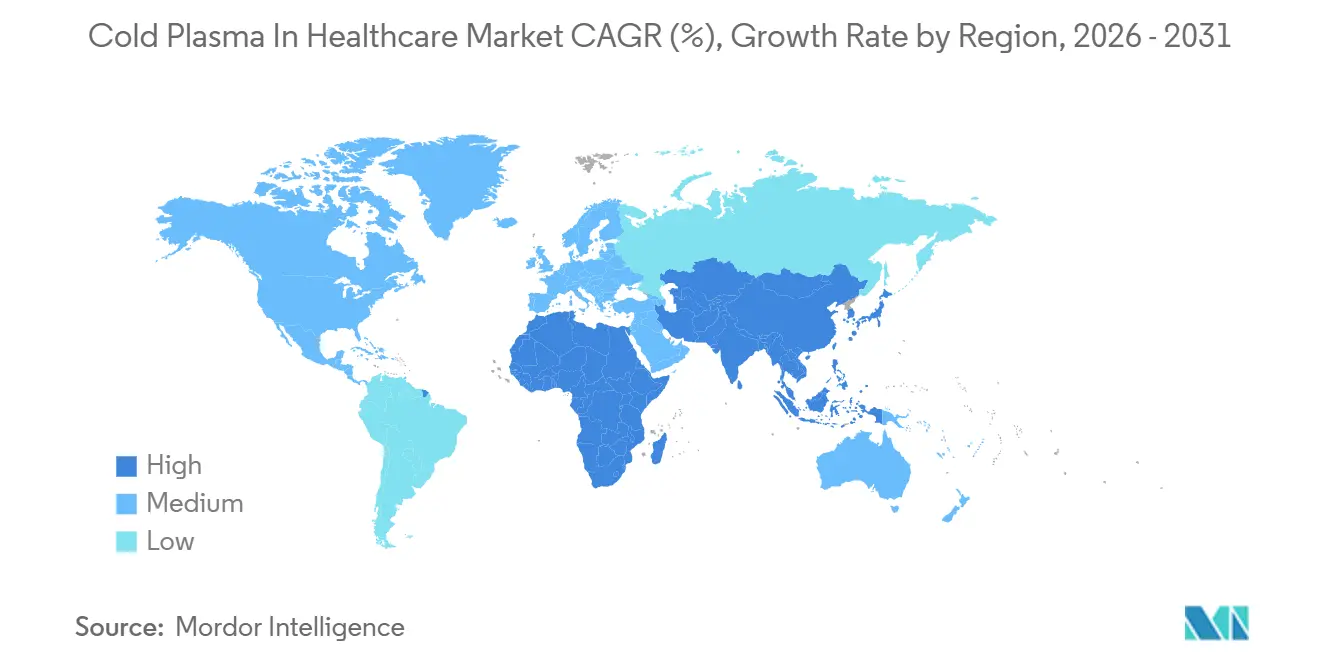

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

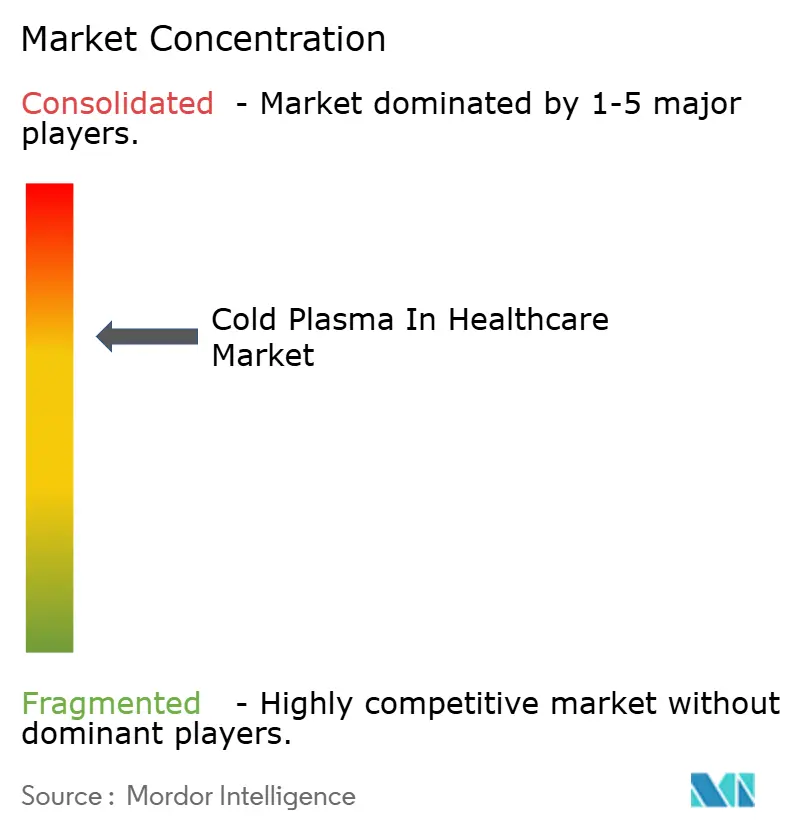

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cold Plasma In Healthcare Market Analysis by Mordor Intelligence

The Cold Plasma In Healthcare Market size is expected to increase from USD 2.81 billion in 2025 to USD 3.19 billion in 2026 and reach USD 6.31 billion by 2031, growing at a CAGR of 14.62% over 2026-2031.

Mounting clinical urgency around chronic wounds, surging antibiotic resistance, and the rollout of reimbursement codes for atmospheric systems in Germany and Japan are accelerating adoption. Device sales dominated early growth, yet recurring software subscriptions and procedure-linked services are now reshaping lifetime value economics. Helium scarcity is tilting engineering choices toward radio-frequency platforms that run on ambient air, while fast-track regulatory pathways in Japan and the United States are shortening commercialization cycles. Competitive intensity remains moderate because no vendor holds double-digit global share, leaving room for new entrants that can scale manufacturing and clinical evidence simultaneously.

Key Report Takeaways

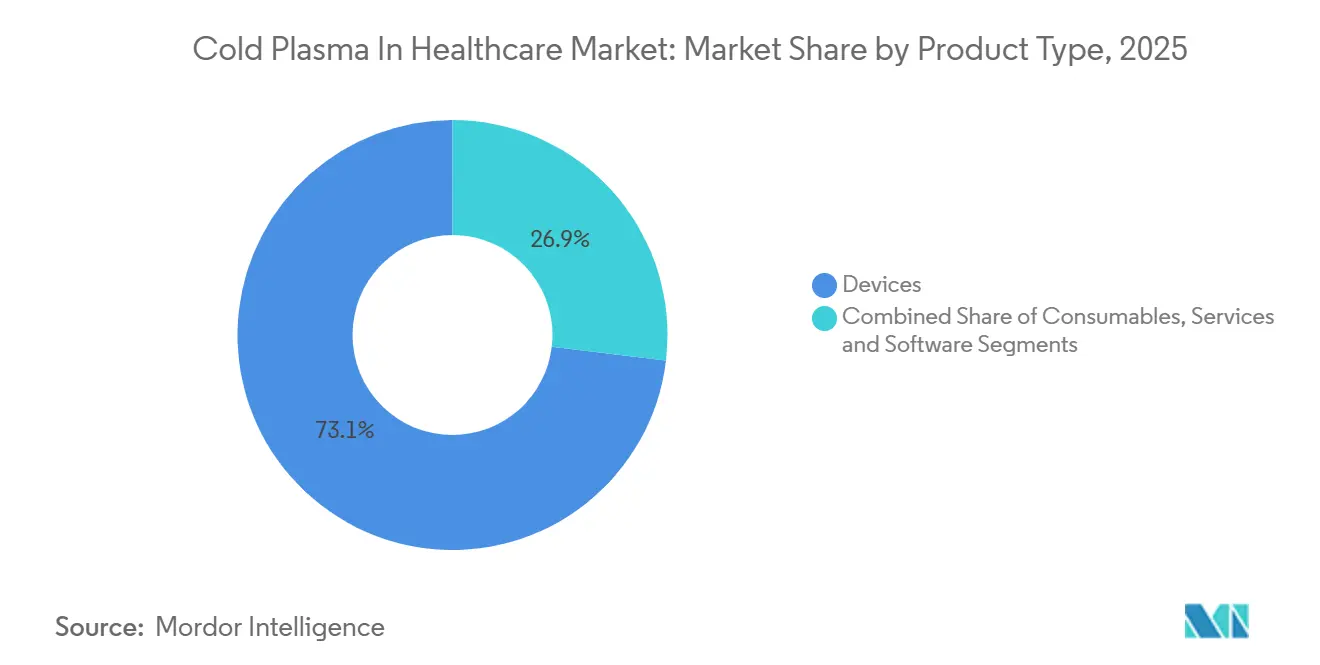

- By product type, devices led with 73.11% of the cold plasma in healthcare market share in 2025, while services and software are forecast to post the fastest growth at an 18.57% CAGR through 2031.

- By device technology, plasma jet generators held 41.57% revenue share of the cold plasma in healthcare market size in 2025 and radio-frequency CAP systems are expected to expand at a 17.35% CAGR between 2026 and 2031.

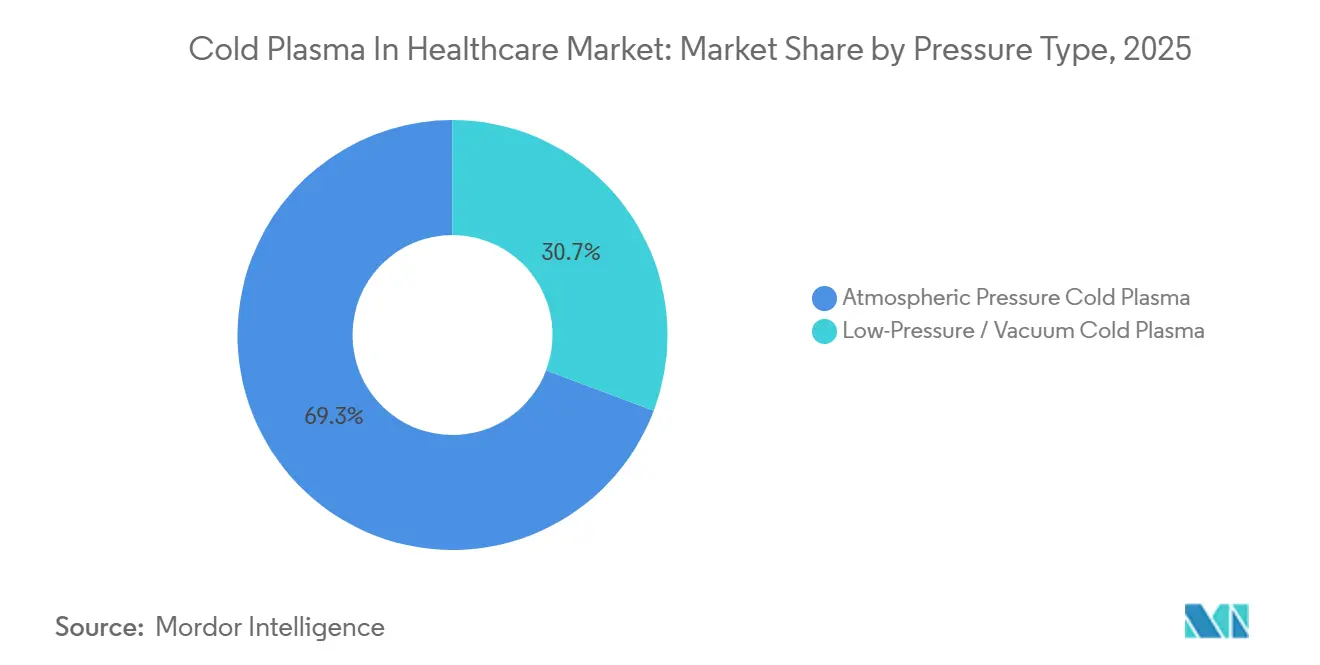

- By pressure type, atmospheric systems accounted for 69.26% of the cold plasma in healthcare market size in 2025, while low-pressure chambers are projected to register a 17.93% CAGR to 2031.

- By application, chronic wound healing held 30.74% of the cold plasma in healthcare market share in 2025 and surgical oncology ablation is anticipated to grow at an 18.55% CAGR through 2031.

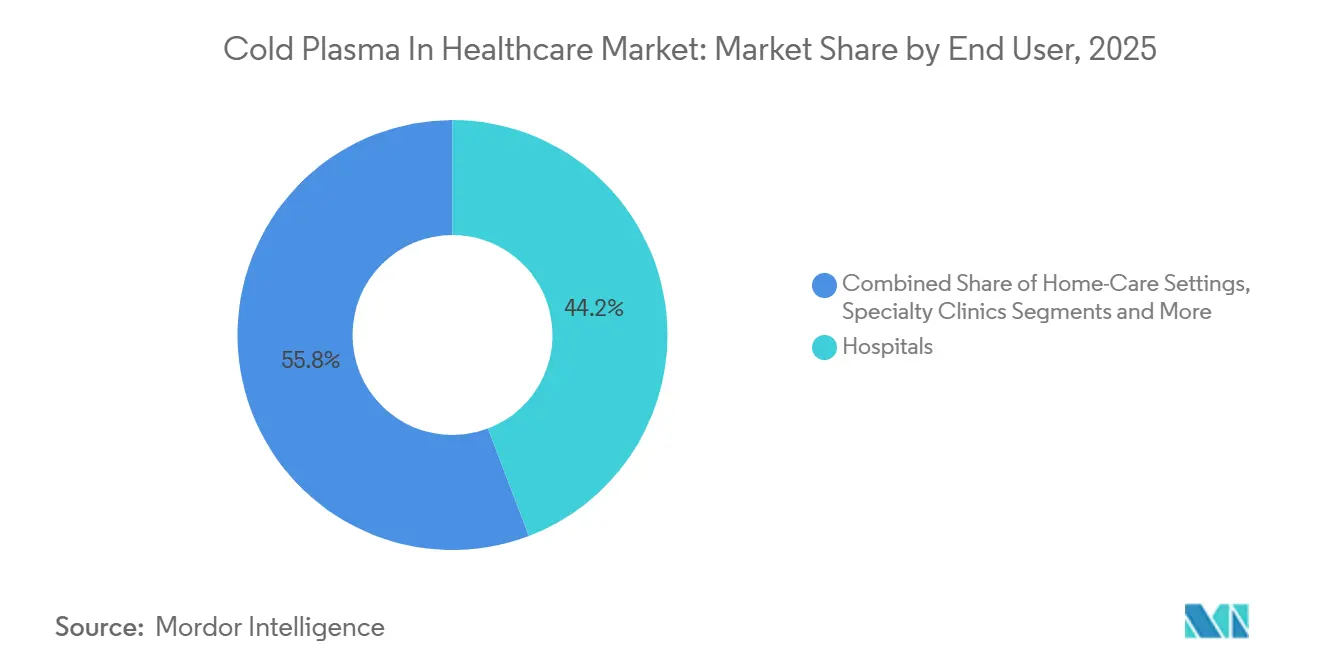

- By end user, hospitals generated 44.22% of revenue in 2025; ambulatory surgical centers are on track for a 19.63% CAGR to 2031.

- By geography, North America led with 39.62% revenue share in 2025, whereas Asia-Pacific is forecast to be the fastest-growing region with a 16.83% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cold Plasma In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of chronic wounds & diabetic ulcers | +2.5% | Global, concentrated in North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Antibiotic-resistant infections raise demand for non-thermal sterilization | +2.3% | Global, acute in North America and EU hospitals | Short term (≤ 2 years) |

| Hospital uptake of atmospheric CAP for infection control | +2.0% | North America and Europe; emerging in GCC and South Korea | Medium term (2-4 years) |

| Favorable approvals and reimbursement pilots | +1.8% | Germany, France, UK; pilots in Canada, Australia | Short term (≤ 2 years) |

| Plasma-activated hydrogel dressings for sustained ROS delivery | +1.5% | North America and EU research hubs; early trials in Japan | Long term (≥ 4 years) |

| AI-driven dose-control modules | +1.2% | North America, Germany, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Wounds & Diabetic Ulcers

Diabetic foot ulcers affect 4%–25% of people with diabetes and recur in 65% of cases within five years, creating a weekly caseload of 60,000–75,000 treatments in England alone.[1]Samuel Ugwueze, “Diabetic Foot Ulcers: A Comprehensive Review,” National Center for Biotechnology Information, ncbi.nlm.nih.gov These hard-to-heal wounds precede 80% of non-traumatic amputations and cost USD 8,600–13,500 per patient each year. Cold plasma generates reactive oxygen and nitrogen species at skin-safe temperatures, accelerating granulation while lowering antibiotic use from 23% to 4% in the POWER trial. Academic groups in Sheffield and Adelaide confirmed in 2024 that plasma-activated hydrogels eradicate biofilms within 24 hours while maintaining moisture balance.[2]Tom Jenkins, “Plasma-Activated Hydrogel Therapy Could Revolutionise Chronic Wound Treatment,” University of Sheffield, sheffield.ac.uk As diabetes prevalence rises, hospitals are embedding plasma protocols into multidisciplinary foot clinics.

Increasing Antibiotic-Resistant Infections Spur Demand for Non-Thermal Sterilization

The World Health Organization attributes 1.27 million deaths to bacterial resistance each year, with 42% of Escherichia coli isolates now defying third-generation cephalosporins. Cold plasma offers a drug-free pathway by rupturing bacterial membranes and DNA in under a minute. A 2024 study showed 3- to 5-log reductions in multidrug-resistant Pseudomonas and Acinetobacter on hospital surfaces, outperforming chemical disinfectants that need 10 minutes.[3]IEEE, “Cold Atmospheric Plasma for Surface Decontamination,” IEEE Xplore, ieeexplore.ieee.org Japan’s health ministry approved Plasma Care for room decontamination the same year, validating the technology as an adjunct to chemical wipes. Infection-control committees now bundle plasma units with UV-C and HEPA measures in intensive-care settings.

Growing Adoption of Atmospheric CAP in Hospital Infection-Control Protocols

Atmospheric devices avoid costly vacuum chambers, letting staff wheel systems into operating theaters or isolation suites without construction work. In 2025 the Robert Koch Institute recommended CAP as a supplement for terminal cleaning after outbreaks of carbapenem-resistant organisms, citing 99.9% sporicidal efficacy in 90 seconds. South Korea certified two models for surgical instrument sterilization in 2024, extending usage beyond research labs. Because CAP is gentle on heat-sensitive scopes and robotic devices, hospitals see it as an alternative to ethylene oxide and hydrogen peroxide methods that face safety and material-compatibility limits. Gulf hospitals are piloting CAP for airborne pathogen control, though ozone-exposure limits are under ISO review.

Favorable Regulatory Approvals & Reimbursement Pilots

Germany’s G-BA added cold plasma to its EBM fee schedule in Q4 2024, granting codes—PlasmaDerm Flex (EUR 35.21), Plasma Care (EUR 20.29), and kINPen MED (EUR 29.83)—subject to real-world evidence collection. The U.S. FDA cleared the MIRARI system for dermal wounds in 2024, creating a predicate device that eases future 510(k) filings. Canada and Australia are piloting similar reimbursement frameworks, while Japan shortened Class III reviews to ten months for handheld jets. These moves shift adoption from discretionary capital budgets to payer-funded procedural revenue, accelerating hospital procurement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost of equipment and noble-gas consumables | −1.8% | Global; acute in India, Brazil, South Africa | Short term (≤ 2 years) |

| Lack of standardized clinical protocols and large RCTs | −1.5% | Global; limits payer adoption in North America, EU | Medium term (2-4 years) |

| Multi-disciplinary, lengthy regulatory pathways | −1.2% | North America, EU, Asia-Pacific | Medium term (2-4 years) |

| Helium supply volatility inflates jet-device operating costs | −1.0% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Cold-Plasma Systems & Noble-Gas Consumables

Entry-level atmospheric units cost USD 12,000–25,000, and low-pressure chambers exceed USD 150,000, out-pricing many public hospitals. Helium now runs USD 80–120 per cylinder after the U.S. reserve sale, lifting per-procedure consumables to USD 15–25. Argon mixes are cheaper but require higher voltage and yield narrower antimicrobial spectra. Leasing and pay-per-use contracts in Germany and the UK are emerging to convert capex into opex, yet uptake in price-sensitive markets still lags.

Lack of Standardized Clinical Protocols & Limited Large-Scale RCTs

The POWER trial proved efficacy but used varied exposure times and excluded ischemic ulcers, making meta-analysis difficul. CMS withheld national coverage in 2024, citing short follow-up periods and insufficient cost-effectiveness data. IQWiG requested head-to-head trials against silver foams, delaying broader German reimbursement. The International Society for Plasma Medicine has draft guidelines, yet no ISO committee has finalized performance benchmarks, leaving manufacturers to self-certify settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Outpace Hardware as AI Platforms Monetize

Devices captured 73.11% of the cold plasma in healthcare market in 2025 as hospitals expanded installed bases for wound-care and sterilization. Consumables such as disposable electrodes and gas cartridges drove 18% of revenue, locking customers into proprietary supply chains. Services and software owned just 9% but are scaling at an 18.57% CAGR because predictive-analytics modules sell for USD 500–1,200 per month. This shift lifts recurring revenue and cushions hardware price erosion.

The cold plasma in healthcare market size linked to services will expand further once plasma-activated dressings reach commercial volumes after 2027. Electrode replacement every 200–500 cycles and gas canisters per 30–40 procedures add stable aftermarket streams. Cloud dashboards that document RONS exposure, tissue impedance, and healing curves satisfy MDR traceability rules and underpin outcome-based reimbursement contracts.

By Device Technology: RF CAP Gains as Helium Costs Erode Jet Economics

Plasma jets commanded 41.57% revenue in 2025 thanks to handheld ergonomics, yet helium shortages are pushing operators toward radio-frequency units that need only ambient air. RF systems are forecast to grow at 17.35% CAGR, helped by RKI guidelines that cite 99.9% sporicidal kill in 90 seconds. Microwave CAP occupies a 12% niche for bulk instrument loads but requires electromagnetic shielding.

Piezoelectric jets usher battery-driven portability, fast-tracked by Japan’s regulator in 2024. DBD roll-to-roll arrays remain pre-commercial but could transform manufacturing of plasma-activated dressings. As gas-free top-line gains offset higher capex, RF vendors are closing the performance-price gap and taking share from jet incumbents.

By Pressure Type: Atmospheric Dominance Masks Low-Pressure Niche Surge

Atmospheric systems held 69.26% revenue share in 2025 because they wheel straight to the bedside and qualify for new German reimbursement codes. They will keep the volume lead, yet low-pressure chambers are set for a 17.93% CAGR as implant manufacturers seek sub-Torr uniformity that boosts osseointegration.

Low-pressure units achieve 6-log bacterial kill in five minutes on titanium hardware, meeting ISO 5832 surface-energy targets. While chambers cost more and need dedicated rooms, orthopedic OEMs are integrating them inline to raise implant pull-out strength by up to 40%. Hospitals remain wedded to atmospheric portability, especially in ambulatory centers that lack space for vacuum pumps.

By Application: Oncology Ablation Emerges as High-Growth Frontier

Chronic wound healing ruled with 30.74% share in 2025 because diabetic ulcers remain endemic. Surgical oncology ablation, though only 8% then, is poised for an 18.55% CAGR as trials confirm selective apoptosis without collateral heat damage. Early work shows plasma can cut chemotherapy dosing by one-third when combined with doxorubicin.

Hemostasis applications use CAP to cross-link fibrin within 20 seconds, outperforming topical thrombin in laparoscopy. Dental and dermatology niches together add another 20% slice, benefiting from plasma’s ability to disrupt biofilms and modulate sebaceous glands. Plasma-activated liquids are still in pilot phases but promise home-care convenience once roll-to-roll arrays supply dressings at scale.

By End User: ASCs Capitalize on Portability and Lower Overhead

Hospitals held 44.22% of spending in 2025 yet face margin pressure as payers steer chronic-care episodes to lower-acuity venues. Ambulatory surgical centers are forecast to log a 19.63% CAGR because hand-piece models under USD 15,000 fit ASC budgets and dermatology caseloads.

Dedicated wound-care centers captured 16% of the cold plasma in healthcare market size in 2025 by processing 50–100 patients a week, making device payback swift. Specialty oncology clinics use plasma for investigational glioblastoma therapy under hospital exemptions. Home-care remains nascent at 3%, but CE-marked consumer devices like PlasmaDerm @home signal future direct-to-patient channels once regulators craft remote-use rules.

Geography Analysis

North America controlled 39.62% revenue in 2025, anchored by FDA clearances. Yet absent Medicare-wide coverage tempers hospital rollouts, shifting emphasis toward private-payer pilots and software subscriptions. Helium rationing is nudging buyers to ambient-air RF models, and margins for jet suppliers are thinning.

Europe generated 32% share, underpinned by Germany’s new codes and RKI guidelines. Funding from Niterra Ventures is scaling device capacity, while at-home pilots test recurrence reduction in diabetic ulcers. The UK’s NICE is drafting guidance for 2026, and Spain and Italy run research protocols until payer positions mature.

Asia-Pacific is the growth engine at a 16.83% CAGR to 2031. Japan’s PMDA fast-tracked handheld jets and sanctioned Plasma Care for room disinfection, while China finalizes Class III oncology rules. India’s public sector struggles with capex, but private-chain hospitals in tier-1 cities are adopting atmospheric units. South Korea approved two sterilization models, and Australia is trialing reimbursement in New South Wales wound clinics.

Competitive Landscape

The cold plasma in healthcare market a mid-range fragmentation profile. Vertically integrated players such as Apyx Medical and Relyon Plasma sell hardware, disposables, and service bundles, whereas component specialists license plasma modules to implant and pharmaceutical OEMs. Neoplas Med’s USD 18 million infusion funds kINPen MED scale-up, and CINOGY targets the home segment with sub-USD 1,100 kits.

AI software is emerging as a differentiator. Vendors that log dose metrics and healing curves satisfy MDR traceability and win outcome-based contracts. Patent filings concentrate on roll-to-roll arrays and piezoelectric minis, reflecting a pivot away from helium-intensive jets. Helium inflation squeezed Renuvion margins by six points last year, prompting Apyx to explore nitrogen chemistries despite a 20% efficacy trade-off.

Rising service subscriptions stabilize cash flow and lift valuations, while hardware price competition intensifies as ambient-air RF units commoditize. Market-entry barriers remain in regulatory dossiers and clinical-evidence funding, areas where well-capitalized firms can still widen the moat.

Cold Plasma In Healthcare Industry Leaders

Neoplas med GmbH

terraplasma medical GmbH

Apyx Medical

US Medical Innovations

ADTEC Plasma Technology Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Iran opened its largest cold-plasma wound clinic at Al-Zahra Medical Center, signaling national support for non-invasive therapies.

- January 2026: Neoplas Med unveiled an argon jet platform that promises steadier healing and fewer complications in routine practice.

- January 2026: The Leipzig Veterinary Congress showcased EquCellpen and PetCellpen devices, illustrating plasma’s crossover into veterinary medicine.

Global Cold Plasma In Healthcare Market Report Scope

As per the scope of the report, cold plasma, or Cold Atmospheric Plasma (CAP), is a non-thermal, ionized gas generated at near-room temperature, enabling safe, non-invasive interaction with biological tissues while serving as a sterilizing agent and aiding wound healing.

The Cold Plasma in Healthcare Market Report is segmented by Product Type, Device Technology, Pressure Type, Application, End User, and Geography. By Product Type, the market is segmented into Devices, Consumables, and Services & Software. By Device Technology, the market is segmented into Radio‑Frequency CAP, Microwave CAP, Piezoelectric Handheld Jet, and DBD Roll‑to‑Roll Arrays. By Pressure Type, the market is segmented into Atmospheric and Low‑Pressure systems. By Application, the market is segmented into Chronic Wound Healing, Surgical Oncology Ablation, Hemostasis, Dentistry, Dermatology, Sterilization, Plasma‑Activated Liquids, and Implant Functionalization. By End User, the market is segmented into Hospitals, ASCs, Wound‑Care Centers, Specialty Clinics, Research Institutes, and Home‑Care. By Geography, the market is segmented into North America, Europe, Asia‑Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Devices | Plasma Jet Generators |

| Dielectric Barrier Discharge Units | |

| Microwave CAP Systems | |

| Low-Pressure RF Chambers | |

| Consumables | Disposable Gas Cartridges |

| Plasma-Activated Dressings / Patches | |

| Replacement Electrodes & Nozzles | |

| Services & Software | AI-Driven Dose-Control Platforms |

| Installation & Maintenance Contracts |

| Radio-Frequency CAP |

| Microwave CAP |

| Piezoelectric Handheld Jet |

| DBD Roll-to-Roll Arrays |

| Atmospheric Pressure Cold Plasma |

| Low-Pressure / Vacuum Cold Plasma |

| Chronic Wound Healing |

| Surgical Oncology Ablation |

| Hemostasis & Blood Coagulation |

| Dentistry & Oral Care |

| Dermatology & Aesthetics |

| Sterilization & Disinfection of Instruments & Surfaces |

| Plasma-Activated Liquids & Hydrogels |

| Implant Surface Functionalization |

| Hospitals (Inpatient) |

| Ambulatory Surgical Centers |

| Dedicated Wound-Care Centers |

| Specialty Clinics (Dermatology / Oncology) |

| Research & Academic Institutes |

| Home-Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Devices | Plasma Jet Generators |

| Dielectric Barrier Discharge Units | ||

| Microwave CAP Systems | ||

| Low-Pressure RF Chambers | ||

| Consumables | Disposable Gas Cartridges | |

| Plasma-Activated Dressings / Patches | ||

| Replacement Electrodes & Nozzles | ||

| Services & Software | AI-Driven Dose-Control Platforms | |

| Installation & Maintenance Contracts | ||

| By Device Technology | Radio-Frequency CAP | |

| Microwave CAP | ||

| Piezoelectric Handheld Jet | ||

| DBD Roll-to-Roll Arrays | ||

| By Pressure Type | Atmospheric Pressure Cold Plasma | |

| Low-Pressure / Vacuum Cold Plasma | ||

| By Application | Chronic Wound Healing | |

| Surgical Oncology Ablation | ||

| Hemostasis & Blood Coagulation | ||

| Dentistry & Oral Care | ||

| Dermatology & Aesthetics | ||

| Sterilization & Disinfection of Instruments & Surfaces | ||

| Plasma-Activated Liquids & Hydrogels | ||

| Implant Surface Functionalization | ||

| By End User | Hospitals (Inpatient) | |

| Ambulatory Surgical Centers | ||

| Dedicated Wound-Care Centers | ||

| Specialty Clinics (Dermatology / Oncology) | ||

| Research & Academic Institutes | ||

| Home-Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the cold plasma in healthcare market in 2031?

The market is forecast to reach USD 6.31 billion by 2031, advancing at a 14.62% CAGR from 2026.

Which segment is growing fastest within the global cold plasma space?

Services and software are set to expand at an 18.57% CAGR as hospitals adopt AI-driven dose-control platforms.

How is helium scarcity influencing technology choices?

Escalating helium costs are pushing providers toward radio-frequency devices that ionize ambient air, despite higher upfront prices.

Why is Asia-Pacific the most attractive growth region?

Japan’s fast-track approvals and China’s oncology pathways, combined with an expanding diabetic population, underpin a 16.83% regional CAGR.

What clinical evidence supports plasma-based wound care?

The POWER randomized trial and follow-up studies showed faster closure rates and reduced antibiotic usage in diabetic foot ulcers.

Page last updated on: