Cognition Supplements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

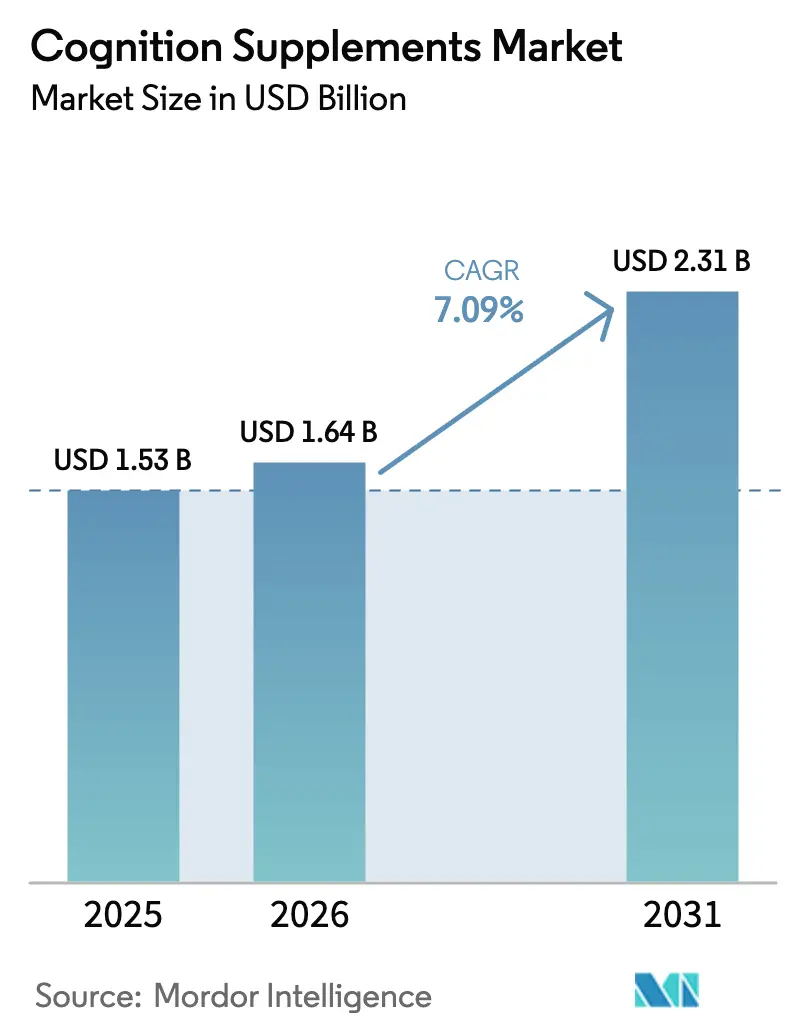

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 2.31 Billion |

| Growth Rate (2026 - 2031) | 7.09% CAGR |

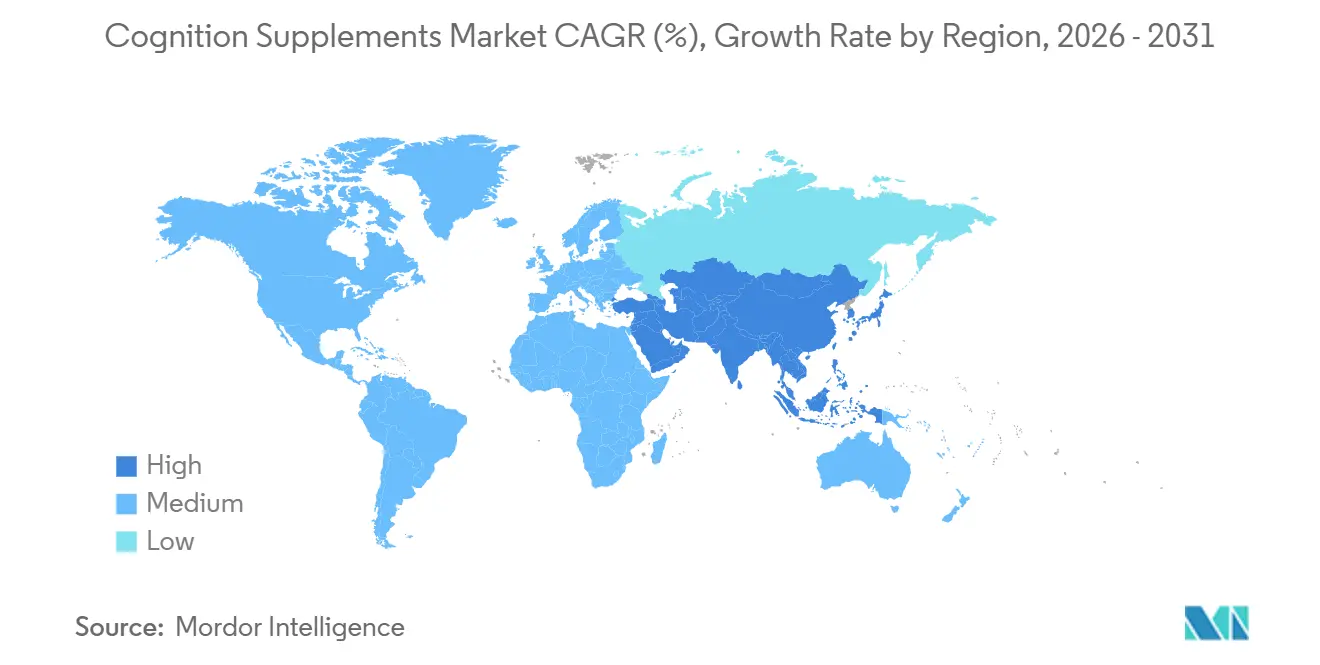

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cognition Supplements Market Analysis by Mordor Intelligence

The Cognition Supplements Market size is expected to increase from USD 1.53 billion in 2025 to USD 1.64 billion in 2026 and reach USD 2.31 billion by 2031, growing at a CAGR of 7.09% over 2026-2031. Increasing life expectancy has led neurological disorders to surpass cardiovascular diseases in disability-adjusted life years, driving the demand for preventive brain-health products. Ingredient science is transitioning from single herbs to micronutrient combinations supported by evidence. Advancements such as nano-encapsulation and liposomal delivery are improving bioavailability without adding to the pill burden. Online subscription models are mitigating price sensitivity by offering personalized and convenient bundles, although recent FDA warning letters have raised compliance standards for disease claims. In the Asia-Pacific region, regulatory harmonization is creating high-growth opportunities for both botanical and synthetic nootropics, enabling first-movers to scale their formulations across borders.

Key Report Takeaways

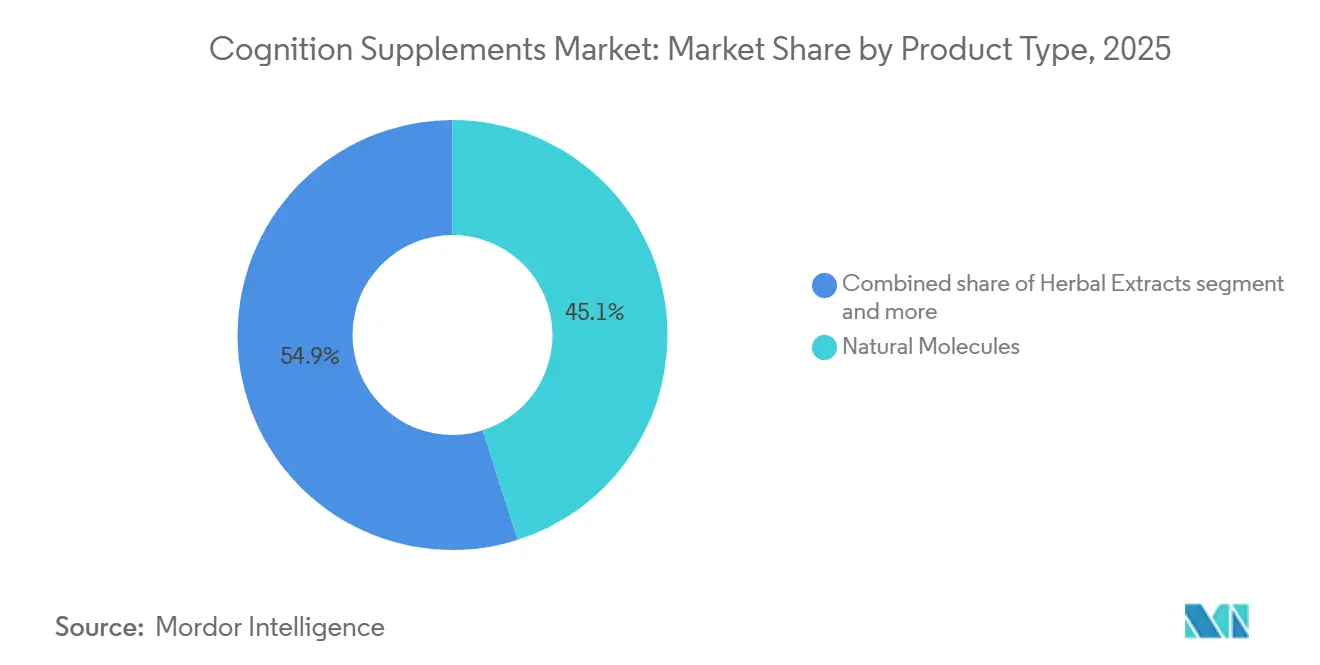

- By product type, Natural Molecules captured 45.09% of the cognition supplement market share in 2025, while Vitamins and Minerals are advancing at an 8.15% CAGR through 2031.

- By form, Capsules and Tablets held 51.85% of the cognition supplement market size in 2025 and Gummies and Chewables are expanding at a 7.65% CAGR over 2026-2031.

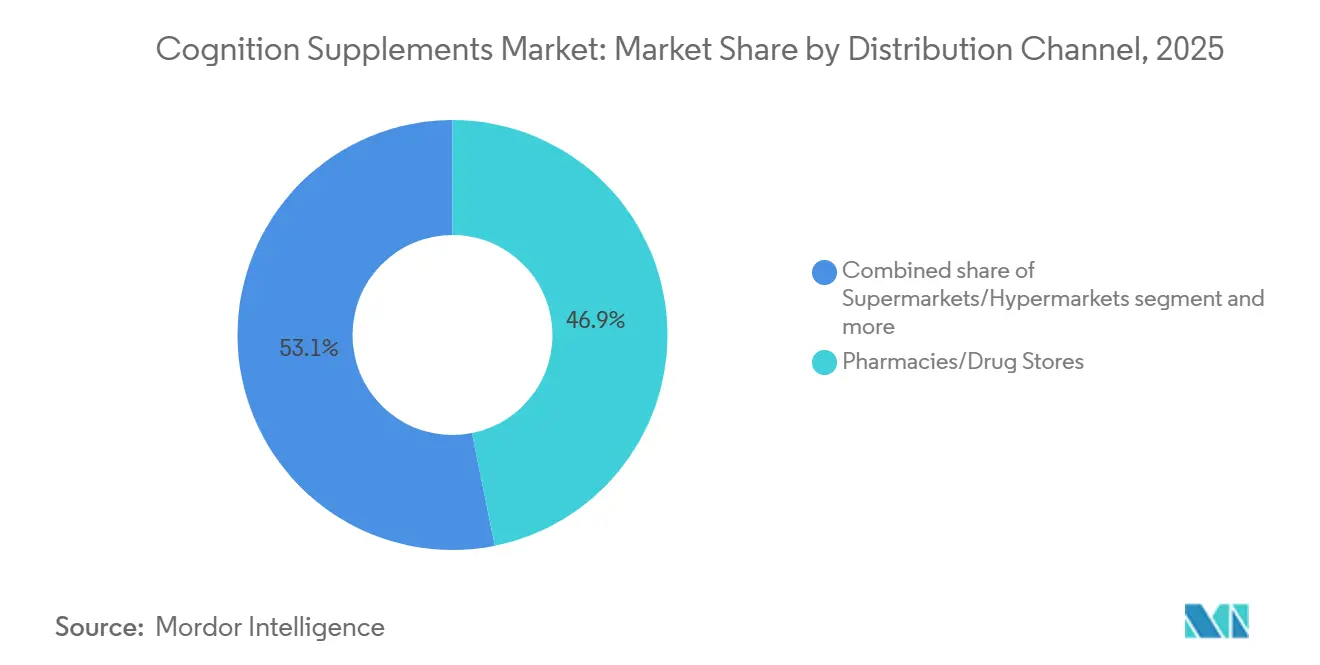

- By distribution channel, Pharmacies and Drug Stores controlled 46.85% of the cognition supplement market share in 2025, whereas Online Retail Stores are forecast to grow at an 8.25% CAGR to 2031.

- By geography, North America retained 31.74% of the cognition supplement market size in 2025, and Asia-Pacific is projected to post an 8.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cognition Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising aging population and cognitive decline awareness | +1.2% | Global, with concentration in Japan, Germany, Italy, South Korea | Long term (≥ 4 years) |

| Preventive-health and wellness trend | +0.9% | North America, Western Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Growing consumer interest in natural and plant-based solutions | +0.8% | North America, Europe, India | Medium term (2-4 years) |

| Growing prevalence of neurological disorders | +1.1% | Global, particularly high-income aging economies | Long term (≥ 4 years) |

| Integration with sports and e-sports nutrition | +0.6% | North America, South Korea, China, Brazil | Short term (≤ 2 years) |

| Scientific research and product innovation | +0.7% | Global, led by North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising aging population and cognitive decline awareness

In 2024, 10% of the world's population was aged 65 and older, according to the World Bank[1]Source: World Bank, "Population ages 65 and above", worldbank.org . This aging population trend is further emphasized by findings from the Lancet Commission on Dementia Prevention, which identified 12 modifiable risk factors, including hypertension, diabetes, and air pollution, that collectively contribute to approximately 40% of dementia cases. These insights highlight the growing importance of cognitive supplements as complementary tools to support lifestyle interventions aimed at mitigating these risks. In response to this demand, brands are increasingly developing multi-ingredient formulations designed to address both neurotransmitter support and vascular health. This approach is effectively bridging the gap between cardiovascular and cognitive product categories. Furthermore, regulatory frameworks in high-income markets are evolving to accommodate structure-function claims related to aging. However, manufacturers must substantiate these claims with credible evidence, such as biomarkers like brain-derived neurotrophic factor or cerebral blood flow, to ensure compliance and consumer trust.

Preventive-health and wellness trend

Preventive health expenditure is undergoing a significant transformation, shifting focus from reactive disease management to proactive health optimization. This trend has gained momentum due to the rise of employer wellness programs and the increasing adoption of direct-to-consumer telehealth platforms. Subscription-based business models are effectively leveraging this shift. For example, companies like Care/of and Ritual utilize algorithm-driven quizzes to create personalized nootropic regimens for their customers. These companies then secure customer loyalty through recurring shipment models, which enhance their lifetime value metrics. Additionally, the emphasis on wellness is becoming increasingly intertwined with workplace productivity. Corporate buyers are exploring cognitive-supplement programs as part of broader initiatives that include ergonomic improvements and mental health benefits. These efforts highlight the growing recognition of brain health as a critical factor in improving employee retention and performance. Although the employer channel for such programs is still in its early stages, it presents a promising opportunity to establish bulk purchasing agreements that could bypass traditional retail margins, offering a more cost-effective and scalable solution.

Growing consumer interest in natural and plant-based solutions

Consumer preference surveys indicate a growing shift towards plant-based and adaptogenic ingredients, which are increasingly replacing synthetic nootropics. This trend is primarily driven by the perception of these ingredients as safer alternatives and their alignment with holistic wellness philosophies. Ayurvedic staples such as Bacopa monnieri, ashwagandha, and Gotu kola are no longer confined to niche health-food stores but are now making their way into mainstream pharmacy shelves. This transition is supported by clinical trials published in reputable peer-reviewed journals, including Phytotherapy Research and the Journal of Ethnopharmacology, which highlight the efficacy and benefits of these ingredients. Lion's Mane mushroom, known for its high content of hericenones and erinacines, has garnered significant attention from venture capitalists, leading to increased funding for its cultivation. Growers in the United States and the Netherlands are investing heavily in controlled-environment agriculture to ensure consistent beta-glucan content, which is a key quality parameter for this mushroom. In 2025, the Food Safety and Standards Authority of India introduced draft guidelines permitting the use of Ayurvedic extracts in nutraceutical products. These guidelines mandate compliance with strict heavy-metal limits and require manufacturers to include disclaimers about traditional use on product labels. This regulatory approval is expected to act as a catalyst for the export of standardized Bacopa and ashwagandha extracts to Western markets. In these markets, formulators place a high value on traceability and certificate-of-analysis documentation, further driving demand for these Ayurvedic ingredients.

Growing prevalence of neurological disorders

The Global Burden of Disease study by the Institute for Health Metrics and Evaluation identifies neurological conditions as the leading cause of disability-adjusted life years, surpassing ischemic heart disease and stroke. In 2024, the WHO's Global Status Report on Neurology emphasized the growing burden of neurological diseases, such as stroke, dementia, migraine, epilepsy, and developmental disorders. The report reveals that these conditions impact over one-third of the global population[2]Source: World Federation of Neurology, "Promoting global neurological education and training", wfneurology.org. This scenario is driving payers and health systems to adopt non-pharmacological interventions. For example, in 2024, the U.S. Centers for Medicare and Medicaid Services launched a demonstration project reimbursing cognitive-training software paired with omega-3 and B-vitamin supplements for mild cognitive impairment. Simultaneously, pharmaceutical companies are strengthening their Alzheimer's drug pipelines by partnering with or acquiring supplement brands, positioning them as complementary therapies or interim solutions during extended drug development timelines. This integration of pharmaceutical rigor with nutraceutical accessibility is fostering hybrid business models that operate across both over-the-counter and prescription markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse-effect and drug-interaction concerns | -0.5% | Global, particularly North America and Europe with high polypharmacy rates | Medium term (2-4 years) |

| Fragmented global regulatory frameworks | -0.4% | Global, acute in cross-border e-commerce | Long term (≥ 4 years) |

| High risk of misinformation, mislabeling and online counterfeit | -0.6% | Global, concentrated in online retail channels | Short term (≤ 2 years) |

| Supply-chain adulteration of exotic botanicals | -0.5% | Global, sourcing risk in India, China, Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse-effect and drug-interaction concerns

Older adults, who are the primary users of cognitive supplements, face increased risks of herb-drug interactions due to polypharmacy. These interactions can reduce a supplement's effectiveness or cause adverse side effects. The U.S. National Institutes of Health's Office of Dietary Supplements has documented significant interactions, including Ginkgo biloba with anticoagulants, St. John's Wort with selective serotonin reuptake inhibitors, and high-dose B vitamins with metformin. Physicians often hesitate to recommend supplements because of insufficient pharmacokinetic data, which hinders their broader adoption. In 2024, the FDA's adverse-event reporting system recorded 1,847 serious incidents associated with dietary supplements, though determining causality is challenging, especially with overlapping medication use. Brands that conduct drug-interaction studies and publish their findings in reputable journals can establish a competitive edge in safety. However, these studies require years to complete and demand significant financial resources, often beyond the capacity of smaller brands. The Dietary Supplement Health and Education Act does not mandate pre-market approvals, placing the responsibility on post-market surveillance to ensure safety, which increases reputational risks if major adverse events attract media attention.

Fragmented global regulatory frameworks

Regulatory differences across jurisdictions create significant challenges for multinational brands striving for economies of scale in product development and market entry. For example, China's National Medical Products Administration mandates pre-market registration for health foods, requiring toxicology dossiers and clinical trials. In the United States, market entry is permitted under the Dietary Supplement Health and Education Act with only a notification for new dietary ingredients. Japan's Foods with Function Claims system requires scientific evidence but does not mandate pre-approval, while India's Food Safety and Standards Authority is working to harmonize Ayurvedic and allopathic frameworks. These regulatory inconsistencies force brands to develop region-specific formulations, labeling, and claim substantiation, increasing compliance costs and delaying time-to-market. E-commerce platforms add to the complexity by enabling cross-border sales that bypass local registration requirements, prompting regulators to focus enforcement efforts on online marketplaces. Additionally, the lack of mutual recognition agreements between major markets prevents products approved in the European Union from automatically entering Asian markets, fragmenting research and development investments and limiting portfolio optimization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Micronutrient Stacks Gain Clinical Traction

In 2025, Natural Molecules held a 45.09% share of the cognition supplement market, highlighting the robust clinical evidence supporting omega-3 and phosphatidylserine. At the same time, Vitamins and Minerals are experiencing an 8.15% CAGR, driven by formulators emphasizing B-complex vitamins and magnesium threonate for their ability to manage homocysteine levels and improve synaptic density. This shift not only strengthens medical endorsements but also aligns with dietary reference intakes monitored by physicians. On the innovation front, herbal extracts such as Bacopa and Lion’s Mane leverage adaptogenic narratives, though dosage inconsistencies continue to complicate meta-analyses. Furthermore, as commodity pressures reduce margins on fish-oil concentrates, brands are turning to value-added options like krill oil enriched with astaxanthin.

Micronutrient stacks attract biohackers seeking measurable biomarker changes, while standardized herbal extracts appeal to natural-product enthusiasts. Proprietary citicoline commands a premium due to its clinical backing, but generic choline poses a threat to its market share. Recent USP monograph updates have standardized potency bands for Bacopa and ashwagandha, enabling more consistent efficacy comparisons. Ingredient suppliers investing in head-to-head trials could influence the growth of the cognition supplement market in favor of their branded actives. Additionally, amino acids like L-theanine are gaining traction as they transition from energy drinks to capsules and powders, expanding their demand across various consumer groups.

By Form: Gummies Capture Compliance-Averse Consumers

In 2025, Capsules and Tablets accounted for 51.85% of the cognition supplement market, driven by their precise dosing and affordability. Enteric-coated vegetarian capsules appeal to plant-based consumers and protect sensitive probiotics, supporting the gut-brain axis. Tablets benefit from economies of scale but require granulation improvements for high-bulk botanicals. Powders, while niche, hold significant appeal among athletes and DIY formulators due to their customizable dosing and rapid absorption.

Gummies and Chewables are expected to grow faster than all other formats, with a projected CAGR of 7.65%. Clinical studies revealed that liposomal curcumin embedded in pectin matrices increased plasma uptake by 34%, demonstrating the effectiveness of functional candies in delivering bioactives. Pediatric and geriatric consumers, who often face swallowing difficulties, show higher repeat purchase rates for gummies, resulting in a 20-30% increase in gross margins compared to capsules. Although regulators monitor sugar content and child-resistant packaging, advancements in taste-masking using monk fruit sweeteners address these concerns. As a result, the cognition supplement market is increasingly shifting toward experiential formats that also serve as lifestyle products.

By Distribution Channel: E-Commerce Rewrites Pharmacy Playbook

In 2025, pharmacies and drug stores held a dominant 46.85% share of the cognition supplement market. This strong position was primarily driven by the role of pharmacist counseling, which effectively addressed consumer concerns about potential drug interactions. Chain private-label brands capitalized on shelf economics by optimizing product placement and curating assortments based on verified supply chains, ensuring product reliability and trust. However, the increasing shift toward mail-order prescriptions has led to a decline in foot traffic, creating challenges for front-of-store sales growth.

Online retail stores are set to lead the pack, boasting an impressive 8.25% CAGR. Techniques like serialized authentication, algorithmic bundling, and auto-ship features are successfully transforming casual buyers into loyal subscribers. The surge in online sales can be largely credited to the expanding global internet penetration. Data from the International Telecommunication Union highlights this trend: in 2025, 74% of the world was online, up from 71% the year prior[3]Source: International Telecommunication Union, "Key Figure", itu.int. Furthermore, direct-to-consumer platforms are harnessing first-party data to refine their upselling strategies. iHerb, on the other hand, is making significant strides in South America and Southeast Asia, thanks to its adept cross-border logistics. While the FDA's intensified scrutiny on influencer health claims has moderated messaging, it has also purged the market of less credible entities. Additionally, specialty health-food stores and multi-level marketing channels are catering to consumers who value personal demonstrations and community-centric sales approaches.

Geography Analysis

In 2025, North America held a 31.74 percent market share, driven by high per-capita spending on supplements, a robust distribution network, and a regulatory framework under the Dietary Supplement Health and Education Act that enables rapid product launches without requiring pre-market approval. The U.S. leads in innovation, with venture-backed startups like HVMN and Neurohacker Collective introducing advanced nootropic stacks and ketone esters that appeal to biohacking communities. However, the FDA's enforcement actions in 2024 and 2025, targeting unapproved disease claims and good manufacturing practice violations, have increased compliance risks, favoring larger brands with dedicated regulatory teams. In Canada, the Natural and Non-prescription Health Products Directorate requires pre-market notifications and product licensing, creating a higher entry barrier compared to the U.S., while signaling quality that appeals to risk-averse consumers. Meanwhile, Mexico's expanding middle class and proximity to U.S. supply chains are attracting cross-border e-commerce players, though inconsistent regulatory enforcement and the prevalence of counterfeit products in informal retail remain challenges.

Asia-Pacific is projected to be the fastest-growing region, with an 8.01 percent expansion forecast from 2026 to 2031. This growth is driven by aging populations in Japan and South Korea, coupled with increasing health awareness in China and India. In 2025, Japan's Ministry of Health, Labour and Welfare reported that one in four citizens is over 65, fueling demand for Foods with Function Claims that target memory and concentration without requiring pre-market approval. In 2024, China's National Medical Products Administration tightened health food registration requirements, mandating toxicology dossiers and clinical trials, which benefit multinational corporations with regulatory expertise over local startups. In 2025, India's Food Safety and Standards Authority of India introduced draft guidelines allowing Ayurvedic extracts in nutraceuticals, unlocking export opportunities for standardized Bacopa and ashwagandha while enabling domestic brands to formalize traditional-use claims. Southeast Asian countries like Thailand, Indonesia, and Singapore are attracting multinational brands seeking first-mover advantages in e-commerce and modern retail, though fragmented regulations and import tariffs complicate regional strategies. Australia and New Zealand, governed by the Therapeutic Goods Administration's complementary-medicines framework, offer mature markets with high consumer trust in third-party certifications, positioning them as ideal testing grounds for premium formulations before broader Asia-Pacific rollouts.

Europe's cognitive-supplement market benefits from the European Food Safety Authority's health-claims regulation, which requires pre-approval of structure-function claims based on peer-reviewed evidence. While this enhances credibility, it also raises entry barriers for smaller brands. The U.K., Germany, and France lead in per-capita consumption, driven by aging populations and strong pharmacy channels that provide pharmacist-led counseling on supplement use. The European Union's Novel Foods Regulation mandates pre-market safety assessments for ingredients without significant consumption history before 1997. This has slowed the introduction of emerging nootropics like Lion's Mane mushroom, prompting brands to rely on established botanicals such as Ginkgo biloba. Eastern European markets like Poland and Russia are experiencing growth as rising incomes and urbanization drive demand for preventive health products, though distribution remains concentrated in pharmacies and hypermarkets, with limited e-commerce penetration. In South America, Brazil and Argentina are seeing increased interest in traditional botanicals like Guarana and Maca, though incomplete regulatory harmonization under Mercosur and import tariffs on finished goods favor local manufacturing. The Middle East and Africa, led by the United Arab Emirates and South Africa, are emerging markets where expatriate populations and medical tourism drive demand for premium imported brands. However, the region faces challenges with limited local manufacturing capacity and evolving regulatory frameworks.

Competitive Landscape

The cognition supplement market exhibits moderate fragmentation, with multinational consumer-health conglomerates. Key market players include Amway Corp., NOW Foods, Herbalife Nutrition Ltd., Bayer AG, and Reckitt Benckiser Group PLC. No single player commands more than significant global share, creating white space for brands that can navigate regulatory heterogeneity and build direct-to-consumer relationships. Larger companies, such as Lonza Group, benefit from vertical integration. Their planned capsule-capacity expansion by 2025 and ingredient-development partnerships enable them to serve both branded and private-label clients, capturing value across the supply chain. Venture-backed newcomers like HVMN and Neurohacker Collective differentiate themselves through clinical validation and community engagement. They invest in randomized controlled trials and publish findings in peer-reviewed journals, enhancing their credibility with biohacking audiences. Multi-level marketing leaders, including Amway and Herbalife, utilize distributor networks to access emerging markets with underdeveloped retail infrastructures. However, these companies face increasing regulatory scrutiny regarding income claims and product efficacy, particularly in the U.S. and China.

Technological advancements are significantly altering the competitive dynamics of the market. Brands are increasingly adopting algorithmic personalization to recommend tailored ingredient combinations based on genetic testing, microbiome analysis, or cognitive assessments. However, the clinical validity of these approaches remains a topic of ongoing debate. For online distribution, programs like Amazon's Transparency and certifications from organizations such as NSF International and USP are becoming critical requirements. This trend places pressure on smaller brands to either absorb the costs of verification or risk being delisted from major platforms. Additionally, brands are intensifying their efforts to secure intellectual property by filing patents for innovative delivery systems, including liposomal encapsulation, sublingual strips, and time-release matrices. These advancements aim to enhance bioavailability and create competitive moats around their products.

Emerging disruptors in the market include ingredient suppliers that are bypassing traditional finished-goods brands by selling directly to consumers through e-commerce platforms. This approach compresses margins and accelerates the commoditization of formulations, challenging the traditional market structure. The evolving competitive landscape increasingly favors companies that can effectively balance scientific rigor, regulatory compliance, and consumer trust-building. Consumer trust is now more reliant on transparent supply chains and third-party verifications than on traditional marketing expenditures, reflecting a shift in consumer priorities and expectations.

Cognition Supplements Industry Leaders

-

Amway Corp.

-

NOW Foods

-

Herbalife Nutrition Ltd.

-

Bayer AG

-

Reckitt Benckiser Group PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: MemoTril has launched a cognitive health dietary supplement, targeting the growing cognitive wellness market. Positioned as a memory support and natural nootropic product, MemoTril aims to establish itself as a prominent player in the brain health supplement segment.

- September 2025: Reckitt Benckiser Group's brand Neuriva introduced Memory 3D Formula, which contains two clinically tested ingredients - Cognicell and Neurofactor - to support memory function.

- July 2025: MemoCore Drops, a new cognitive support supplement, aims to enhance brain health, boost memory retention, and sharpen mental clarity. Key ingredients include Bacopa Monnieri, Ginkgo Biloba, Phosphatidylserine, and a Vitamin B Complex.

- November 2024: Bayer launched Berocca Mind, which contains Spanish Sage to support memory function. The effervescent tablets contain 12 essential vitamins and minerals, including all eight B vitamins, magnesium to reduce tiredness and fatigue, and zinc and iron to support normal cognitive function.

Global Cognition Supplements Market Report Scope

Cognition supplements are dietary supplements designed to boost cognitive functions, including memory, focus, attention, and mental clarity. By product type, the market is segmented into natural molecules, herbal extracts, vitamins and minerals, and others. By form, the market is segmented into capsules and tablets, powders, gummies and chewables. By distribution channel, the market is segmented into supermarkets/hypermarkets, pharmacies/drug stores, online retail stores, and others. By Geography, the market is segmented into North America, South America, Europe, Asia-Pacific, the Middle East and Africa. For each segment, the market forecasts are provided in terms of value (USD) and volume (tons).

| Natural Molecules |

| Herbal Extracts |

| Vitamins and Minerals |

| Others |

| Capsules and Tablets |

| Powders |

| Gummies and Chewables |

| Supermarkets/Hypermarkets |

| Pharmacies/Drug Stores |

| Online Retail Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Natural Molecules | |

| Herbal Extracts | ||

| Vitamins and Minerals | ||

| Others | ||

| By Form | Capsules and Tablets | |

| Powders | ||

| Gummies and Chewables | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies/Drug Stores | ||

| Online Retail Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast value of the cognition supplement market in 2031?

It is expected to reach USD 2.31 billion by 2031, reflecting a 7.09% CAGR from 2026.

Which region will grow fastest through 2031?

Asia-Pacific is projected to expand at an 8.01% CAGR as regulatory harmonization and aging demographics converge.

Which product type is growing quickest?

Vitamins & Minerals lead expansion at an 8.15% CAGR, driven by evidence-backed micronutrient stacks.

Why are gummies gaining popularity?

Nano-encapsulation and pectin matrices boost bioavailability and taste, lifting gummies to a 7.65% CAGR.

Page last updated on: