Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

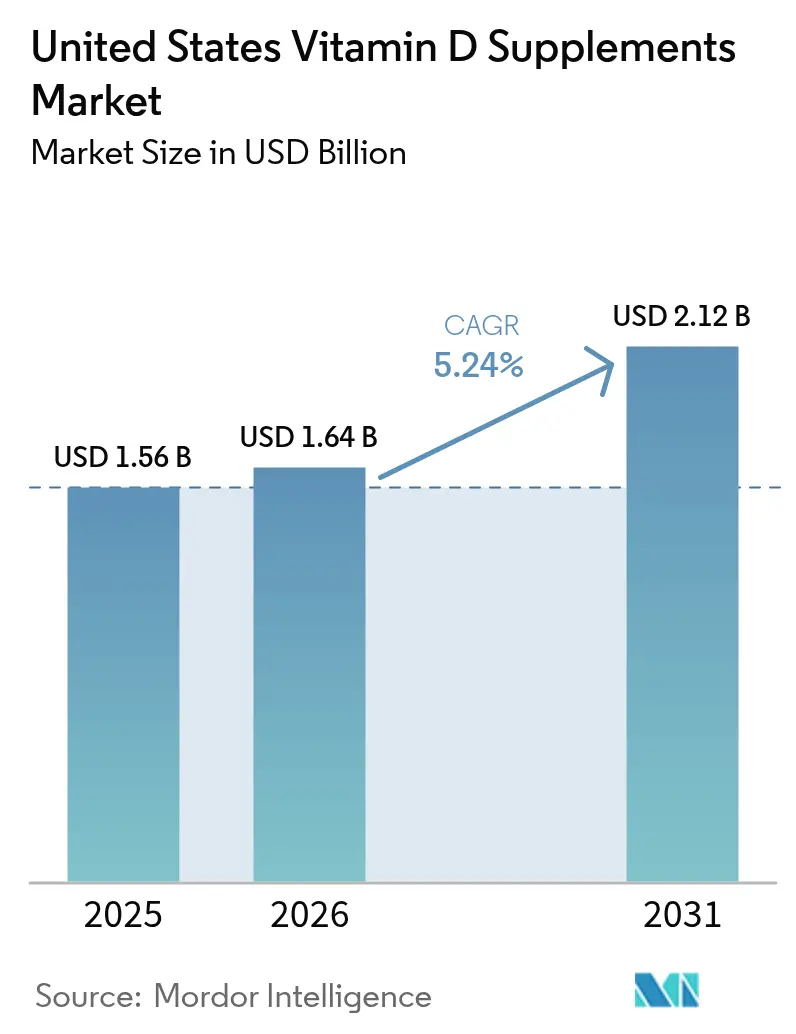

| Base Year Market Size (2025) | USD 1.56 Billion |

| Market Size (2026) | USD 1.64 Billion |

| Market Size (2031) | USD 2.12 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

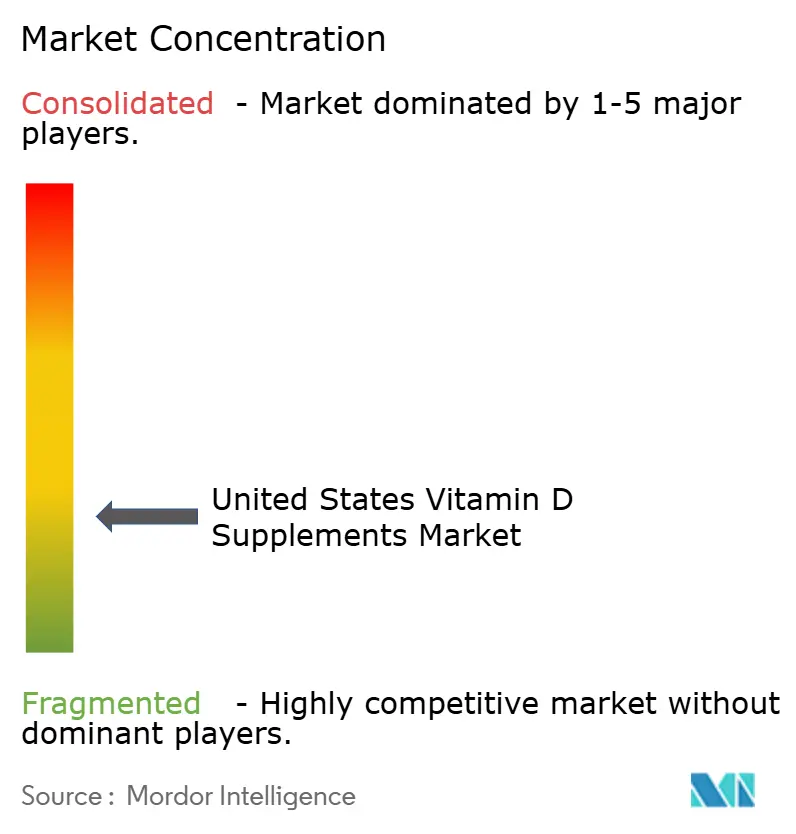

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Vitamin D Supplements Market Analysis by Mordor Intelligence

The United States vitamin D supplements market size was valued at USD 1.56 billion in 2025 and estimated to grow from USD 1.64 billion in 2026 to reach USD 2.12 billion by 2031, at a CAGR of 5.24% during the forecast period (2026-2031). The market growth is driven by three key factors: increasing vitamin D deficiency across ethnic groups, an aging population seeking supplements for osteoporosis management, and updated clinical guidelines targeting specific risk groups. The market is experiencing product innovation through diverse delivery formats, including gummies and high-bioavailability calcifediol, while e-commerce platforms enhance accessibility and price transparency. Moreover, the Western region shows strong growth due to health-conscious consumers and digital adoption, while the South maintains the largest market share due to its population size and prevalence of bone-related conditions.

Key Report Takeaways

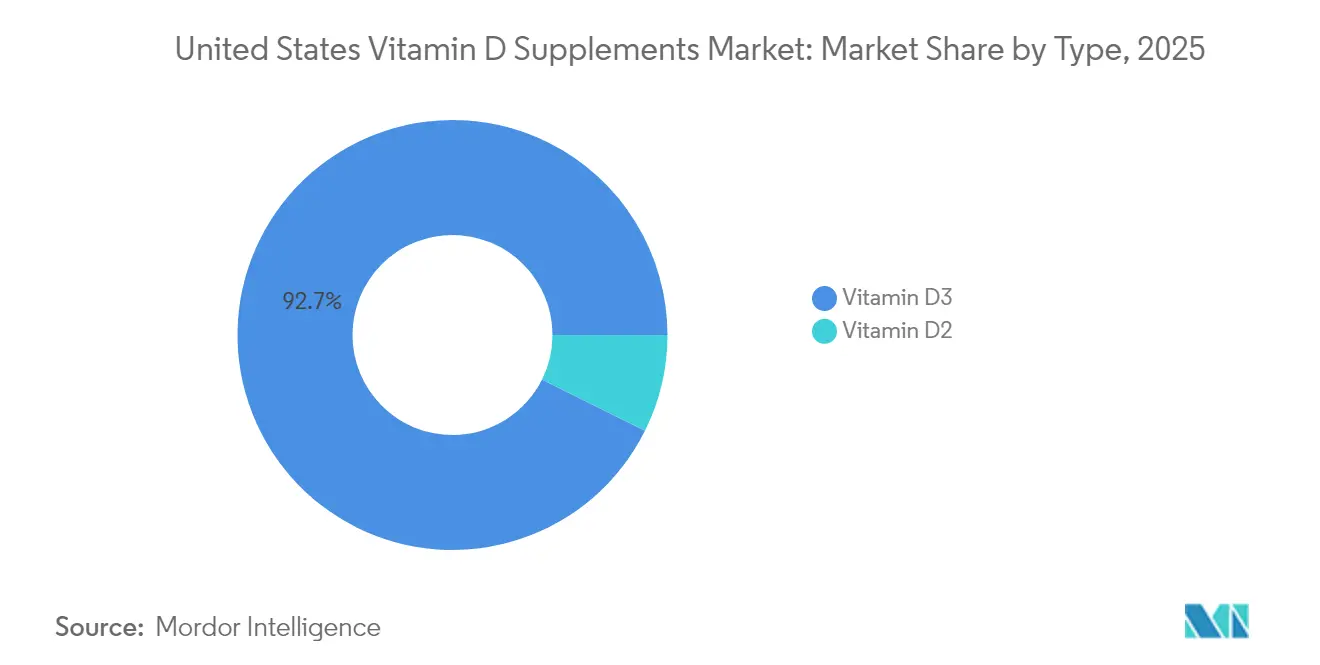

- By type, vitamin D3 dominated with 92.65% of the United States vitamin D supplements market share in 2025 and is growing at a 6.02% CAGR through 2031.

- By form, capsules and soft gels maintained the largest revenue share at 34.12% in 2025, while gummies demonstrate strong growth potential with a projected 6.62% CAGR to 2031.

- By source, animal-based ingredients maintained a substantial 70.58% share in 2025, with plant-based/vegan alternatives showing the highest growth rate at 7.01% CAGR during 2026-2031.

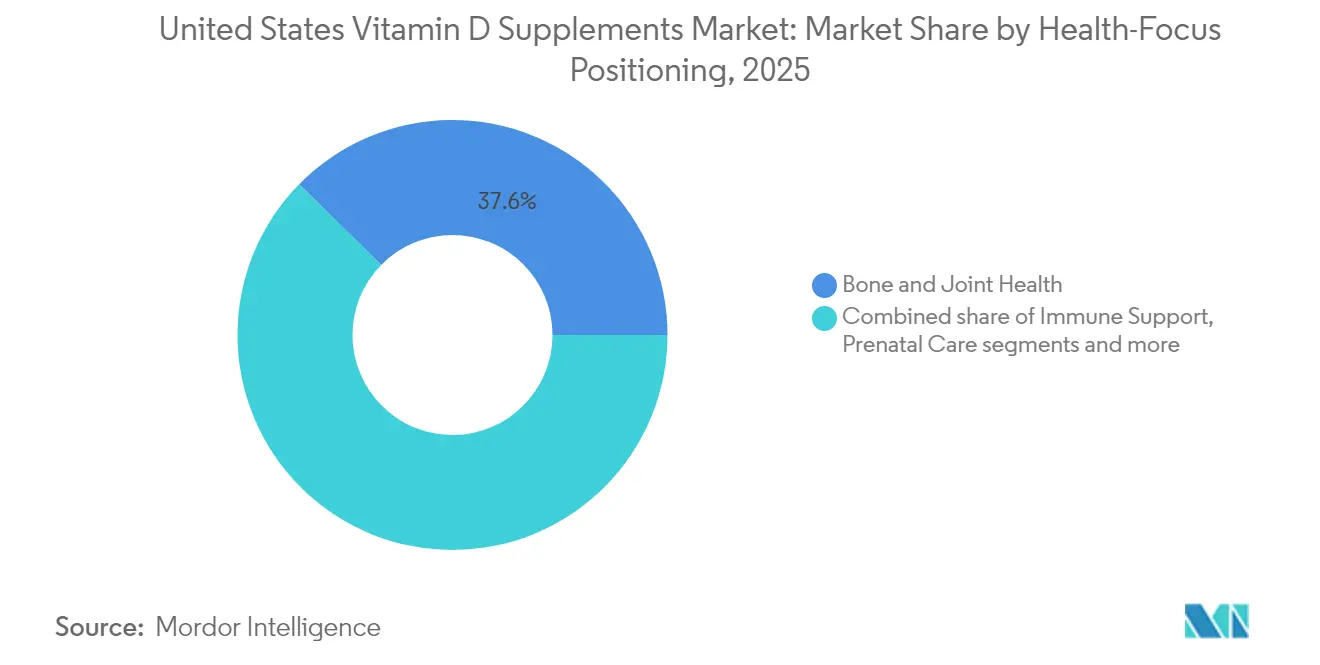

- By health-focused positioning, bone and joint health represented 37.64% of the market share in 2025, while immune support segments are growing at a 5.69% CAGR.

- By distribution channels, specialty, and health stores dominated with 40.79% market share in 2025, though online retailers are experiencing rapid growth with a 6.55% CAGR.

- By geography, the Southern region held 34.21% of market shares in 2025, while the Western region is experiencing the fastest growth at 7.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Vitamin D Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of vitamin D Deficiency among U.S. adults | +1.2% | National, with higher impact in Northeast and Midwest | Long term (≥ 4 years) |

| Aging population seeks vitamin D supplements for osteoporosis | +0.9% | National, with concentration in South and West | Medium term (2-4 years) |

| Expansion of e-commerce and DTC channels | +0.8% | National, with early gains in West and Northeast | Short term (≤ 2 years) |

| Rising endorsments from doctors and healthcare professionals | +0.7% | National, with stronger influence in urban areas | Medium term (2-4 years) |

| Supportive government guidelines and recommendations | +0.6% | National | Long term (≥ 4 years) |

| Growwing demand for preventive healthcare | +0.5% | National, with premium segments in West and Northeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High prevalence of vitamin D Deficiency among U.S. adults

Vitamin D deficiency in the United States affects a broad demographic spectrum, creating significant market potential beyond conventional supplement consumption. According to the 2024 National Health and Nutrition Examination Survey NHANES data, over 99% of participants do not meet recommended vitamin D intake levels from food and beverage sources alone [1]Source: Office of Dietary Supplements, “ODS Update: Recent Developments in Dietary Supplement Science,” ods.od.nih.gov. This trend indicates a persistent nutritional gap despite increased awareness and supplementation efforts. Centers for Disease Control and Prevention data from 2024 indicates a notable disparity, with non-Hispanic Black Americans experiencing a 31% deficiency rate compared to 3% among non-Hispanic whites [2]Source: Centers for Disease Control and Prevention, "CDC's Second Nutrition Report," cdc.gov. This demographic variation presents opportunities for targeted product development and distribution strategies. The substantial deficiency rates across population groups suggest potential market expansion through specialized formulations, innovative delivery systems, and demographic-specific marketing approaches.

Aging population seeks vitamin D supplements for osteoporosis

The demand for vitamin D supplements is driven by various health factors, including age-related bone health, hormonal changes, medication effects, and lifestyle considerations. According to the Food and Drug Administration data from 2024, over 10 million Americans have osteoporosis [3]U.S. Food and Drug Administration, "Osteoporosis," fda.gov . The National Cancer Institute data from 2025 indicates that prostate cancer patients receiving androgen deprivation therapy require higher vitamin D supplementation (50,000 IU weekly), as standard doses are insufficient to prevent treatment-induced bone loss [4]National Cancer Institute, "High-dose Vitamin D Supplementation for ADT-Induced Bone Loss in Older Prostate Cancer Patients", prevention.cancer.gov. These factors contribute to the increased consumption of vitamin D supplements among the elderly population. The growing awareness of vitamin D deficiency, combined with increasing healthcare costs and preventive health measures, further drives market growth. Medical professionals are increasingly prescribing vitamin D supplements as part of comprehensive treatment plans, particularly for patients with limited sun exposure, those following specific diets, or individuals with absorption issues.

Expansion of e-commerce and DTC channels

The digital transformation of vitamin D supplement distribution has altered consumer purchasing patterns, expanded market reach, and reduced dependence on traditional retail channels. Online distribution has improved accessibility across demographic groups and geographic regions. Direct-to-consumer sales allow manufacturers to establish customer relationships while increasing profit margins by eliminating retail intermediaries. This distribution model has effectively reached underserved markets and consumer segments. E-commerce platforms provide consumers with access to personalized supplement formulations and offer convenience and product selection beyond traditional retail capabilities.

Rising endorsments from doctors and healthcare professionals

Healthcare professional recommendations remain the primary driver for vitamin D supplementation decisions. The 2024 Endocrine Society guidelines influence market dynamics by refining clinical protocols. These guidelines discourage routine vitamin D testing for healthy adults under 75 while promoting targeted supplementation for specific groups, including children (1-18 years), pregnant individuals, adults over 75, and people with prediabetes. Clinical practice guidelines now acknowledge vitamin D's broader health implications beyond bone health, including cardiovascular benefits and immune function support, which strengthens healthcare professional recommendations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Presence of counterfeit products hinders growth | -0.4% | National, with higher impact in online channels | Short term (≤ 2 years) |

| Potential side effects | -0.3% | National | Medium term (2-4 years) |

| Availability of alternative products | -0.2% | National, with stronger impact in health-conscious regions | Long term (≥ 4 years) |

| Raw material scarcity | -0.2% | National, with supply chain dependencies on China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Presence of counterfeit products hinders growth

The dietary supplement market faces significant challenges due to adulteration issues, as evidenced by FDA enforcement actions in 2024-2025. These actions revealed systematic contamination problems affecting market integrity and consumer trust. Notable recalls during this period included: Force Forever - containing undeclared diclofenac and dexamethasone, Vitafer-L Gold Liquid - containing undeclared tadalafil, and VitalityXtra capsules - contaminated with sildenafil and diclofenac. While these contamination incidents primarily affect male enhancement and pain relief supplements, they have triggered increased regulatory oversight and consumer skepticism across the entire dietary supplement market. The FDA has intensified its enforcement efforts, including issuing warnings about tejocote root supplements substituted with toxic yellow oleander. The quality control challenges extend beyond domestic manufacturing to international supply chains, necessitating enhanced testing protocols and supplier verification procedures. In response, the FDA has revised its guidance on New Dietary Ingredient Notifications, implementing stricter safety documentation requirements for manufacturers and establishing stronger barriers to entry for potential fraudulent operators.

Potential side effects

The 2024 Endocrine Society review found limited evidence connecting specific serum thresholds to broader clinical outcomes, resulting in conservative dosing recommendations for low-risk adult patients. The comprehensive clinical trials, including the VITAL study, demonstrated minimal preventive benefits in otherwise healthy participants, which influenced treatment decisions among healthcare providers. Standard laboratory tests may not accurately assess vitamin sufficiency levels across different ethnic groups, making the development of universal dosage guidelines particularly challenging. These emerging scientific findings, combined with ongoing research in the field, support the implementation of moderate dosing approaches rather than high-dose supplementation protocols, particularly in populations without documented deficiencies or specific medical conditions that require elevated supplementation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: D3 Dominance Drives Innovation

Vitamin D3 accounts for 92.65% market share in 2025 and is growing at a 6.02% CAGR, as it remains the primary form for increasing 25(OH)D levels in the body. The United States vitamin D supplements market revenue for D3 products is projected to maintain this growth pattern through 2031, driven by increasing consumer awareness about vitamin D deficiency and its health implications. Vitamin D2 maintains its position in vegan supplements and food fortification applications, particularly after the Federal Register approved UV-treated mushroom powder as a source, offering plant-based alternatives to traditional vitamin D supplements.

Manufacturers are developing enhanced formulations using calcifediol complexes that offer improved absorption rates, targeting consumers who need higher bioavailability due to medical conditions or absorption issues. While research continues on provitamin D3-enriched tomatoes as a potential alternative source, production capabilities, scalability challenges, and regulatory approval processes will determine implementation timelines. The development of these innovative delivery methods reflects the industry's response to growing consumer demand for more effective vitamin D supplementation options.

By Form: Capsules Lead Market Share While Gummies Show Fastest Growth

Capsules and softgels held a 34.12% market share in 2025, primarily due to their precise dosing capabilities and healthcare professional endorsements. These formats gained widespread adoption because of their easy-to-swallow nature, oxidation protection, and uniform absorption characteristics. Gummy supplements recorded the highest growth at 6.62% CAGR, driven by consumer demand for convenient and palatable options. The appealing taste and child-friendly characteristics of gummies have shaped consumer buying patterns. Pharmavite's Ohio manufacturing facility has increased domestic production capacity, while research continues to advance nutrient stability at room temperature.

Traditional tablets remain popular among price-sensitive consumers due to their lower manufacturing costs and longer shelf life. Powders provide flexible dosing options and mix easily with drinks or food, attracting health-focused consumers. Liquid supplements serve infants and people with swallowing difficulties, offering quick absorption and easy administration. In addition, sales typically increase during winter months when sun exposure decreases and immune health concerns rise, with e-commerce promotions boosting purchases of flavored chewable products.

By Source: Plant-Based Surge Reflects Values Shift

Animal-based vitamin D supplements constitute 70.58% of vitamin D production in 2025, while plant-based/vegan alternatives experience growth at a 7.01% CAGR. Consumer demand for sustainable products drives the adoption of mushroom-derived vitamin D2 and yeast-based vitamin D3 alternatives. The shift toward plant-based options aligns with environmental awareness and ethical considerations. Protein alternatives fortified with vitamin D3 maintain over 90% nutrient stability during processing, enabling manufacturers to expand into diverse product categories. This stability ensures consistent nutritional content across food and beverage applications.

The production of synthetic vitamin D ensures consistent quality across batches while minimizing variations in potency and purity. The synthetic manufacturing process enables better control over production parameters, including temperature, pressure, and reaction conditions, which maintains stable supply throughout the year. This method reduces reliance on seasonal raw materials and weather-dependent harvesting cycles. Manufacturers maintain low contamination levels through rigorous quality control measures, automated production systems, and sterile manufacturing environments in response to consumer safety concerns. Source transparency, including detailed product labels showing manufacturing dates, batch numbers, and quality parameters, along with third-party certifications from recognized testing laboratories, has become a distinguishing factor that strengthens consumer confidence. These certifications often include comprehensive analyses of product purity, potency, and absence of contaminants.

By Health-Focus Positioning: Bone Health Dominates While Immune Support Shows Fastest Growth

Bone and joint health maintains the largest market share at 37.64% in 2025, driven by vitamin D's essential role in calcium absorption and bone mineralization. The immune support segment demonstrates the highest growth potential with a 5.69% CAGR through 2031. Research validating vitamin D's cardiovascular benefits has expanded market opportunities, with cardiovascular institutes recommending individualized vitamin D supplementation based on patient risk factors. The prenatal care segment continues to grow as medical guidelines advocate vitamin D supplementation during pregnancy to improve maternal outcomes and fetal development.

The health-focused segments reflect broader recognition of vitamin D's diverse health benefits beyond bone health, including immune function, cardiovascular health, and metabolic regulation. Ongoing research into vitamin D's potential role in cancer prevention and cognitive function may create new market opportunities, pending conclusive clinical evidence. Market positioning increasingly focuses on preventive healthcare, aligned with consumer preferences for proactive health management.

By Distribution Channel: Specialty Health Stores Lead Distribution as E-commerce Gains Ground

Specialty and health stores command a 40.79% market share in 2025, driven by pharmacist consultations, personalized recommendations, and specialized product selections. Online retail channels demonstrate a 6.55% CAGR, aligning with broader e-commerce market patterns. Subscription services ensure regular purchases through customized delivery schedules, while digital recommendation systems suggest premium products based on consumer preferences and purchase history. The United States vitamin D supplements market's digital distribution channels expand through enhanced delivery capabilities and improved user experience.

Supermarkets and hypermarkets provide high visibility for mainstream consumers through strategic shelf placement and promotional displays, while pharmacies utilize insurance-based loyalty programs and professional consultation services to promote condition-specific supplements. Successful market players maintain consistent brand positioning across physical and digital channels, combining professional expertise with online accessibility and seamless shopping experiences.

Geography Analysis

The South accounted for 34.21% of revenue in 2025, driven by its large population, high obesity rates, and increased osteoporosis prevalence. Despite abundant sunlight exposure, vitamin D deficiency remains common among non-Hispanic Black residents. Regional outreach programs incorporate culturally relevant messaging and offer capsule or chewable formats preferred by older consumers. Pharmacist-led education programs continue to influence purchasing decisions through established patient relationships.

The Western region shows a 7.52% CAGR, driven by increased focus on preventive healthcare and consumer adoption of direct-to-consumer testing kits that combine supplements with personal health tracking. Subscription-based delivery services increase vitamin D purchase frequency, while plant-based options appeal to environmentally conscious consumers. Retailers combine vitamin D products with functional beverages and plant-protein snacks to increase sales.

The Northeast and Midwest regions experience seasonal vitamin D deficiency due to reduced UVB exposure during winter months, leading to increased sales from October through March. Healthcare providers combine vitamin D awareness initiatives with flu vaccination programs as part of comprehensive public health campaigns. Manufacturers align their promotional strategies with these seasonal patterns, maintaining peak demand despite reduced deficiency risk during summer months.

Competitive Landscape

The United States vitamin D supplements market exhibits significant fragmentation, creating opportunities for both established pharmaceutical companies and specialized supplement manufacturers to capture market share through differentiated positioning and innovative product development. This fragmented structure reflects diverse consumer preferences across age groups, health conditions, and delivery mechanisms, from traditional tablets to innovative gummy formulations that appeal to different demographic segments.

Major players in the market include Amway Corporation, Nestlé S.A., andHarbin Pharmaceutical Group, among others. These players are adopting various strategies such as product innovations, partnerships, expansions, mergers, and acquisitions. The competitive dynamics increasingly favor companies that can navigate complex regulatory requirements while delivering clinically validated formulations that align with evolving healthcare provider recommendations and consumer health priorities.

Strategic differentiation occurs through multiple vectors, including bioavailability enhancement, delivery system innovation, and targeted health positioning that addresses specific consumer segments and clinical applications. White-space opportunities exist in personalized supplementation approaches, plant-based formulations for vegan consumers, and specialized applications for high-risk populations such as prostate cancer patients requiring high-dose vitamin D protocols that exceed standard supplementation recommendations.

United States Vitamin D Supplements Industry Leaders

-

Haleon PLC

-

Nestlé S.A.

-

Harbin Pharmaceutical Group

-

The Procter & Gamble Company

-

Amway Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Pharmavite opened a new manufacturing and research and development facility in New Albany, Ohio. The nutrition and wellness company invested USD 250 million in the facility. The 225,000-square-foot facility, which produces Nature Made vitamins and supplements, is the company's first in the region and includes expansion capacity. The facility is currently manufacturing products and can meet the growing demand for vitamin gummies, which have experienced nearly 100% growth in popularity since 2019.

- October 2024: Immunotec launched SunRay, a weekly Vitamin D supplement containing Calcifediol (25-hydroxyvitamin D), available exclusively in the United States through Immunotec. SunRay aims to help consumers maintain optimal Vitamin D levels, which support mood regulation, hormonal balance, immune function, bone health, and energy levels.

- March 2024: Nature Made, a vitamin and supplement brand, introduced Nature Made Zero Sugar‡ vitamin D Gummies. This new product line provides the same benefits as traditional Nature Made Gummies without added sugar, accommodating diverse dietary preferences.

United States Vitamin D Supplements Market Report Scope

Vitamin D is mostly found in fish liver oils, egg yolks, and milk or is created in response to ultraviolet radiation, which is necessary for proper bone and tooth structure. Vitamin D supplements are made from vitamin D. The United States vitamin D supplement market is segmented by type and distribution channel. Based on type, the market is segmented into vitamin D2 and vitamin D3. Based on distribution channels, the market is segmented into supermarkets, hypermarkets, pharmacies, health stores, online stores, and other distribution channels. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Type

| Vitamin D2 |

| Vitamin D3 |

By Form

| Tablets |

| Capsules and Softgels |

| Gummies |

| Powders |

| Liquid |

| Others |

By Source

| Synthetic |

| Animal-Based |

| Plant-Based/Vegan |

By Health-Focus Positioning

| Bone and Joint Health |

| Immune Support |

| Prenatal Care |

| General Wellness |

| Others |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty and Health Stores |

| Online Retailers |

| Other Distribution Channels |

By Geography

| Northeast |

| Midwest |

| South |

| West |

| By Type | Vitamin D2 |

| Vitamin D3 | |

| By Form | Tablets |

| Capsules and Softgels | |

| Gummies | |

| Powders | |

| Liquid | |

| Others | |

| By Source | Synthetic |

| Animal-Based | |

| Plant-Based/Vegan | |

| By Health-Focus Positioning | Bone and Joint Health |

| Immune Support | |

| Prenatal Care | |

| General Wellness | |

| Others | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Specialty and Health Stores | |

| Online Retailers | |

| Other Distribution Channels | |

| By Geography | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is the current value of the US vitamin D supplements market?

The United States vitamin D supplements market stood at USD 1.64 billion in 2026 and is anticipated to reach USD 2.12 billion by 2031.

Which product type dominates sales?

Vitamin D3 accounts for 92.65% of 2025 revenue and maintains leadership due to superior bioavailability.

Why are gummies growing so quickly?

Gummies combine palatable flavors with ease of use, helping compliance and posting a 6.62% CAGR, the fastest among all formats.

Which region is expanding the fastest?

The West leads with a projected 7.52% CAGR, driven by digital health adoption and proactive wellness attitudes.

Page last updated on: