Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

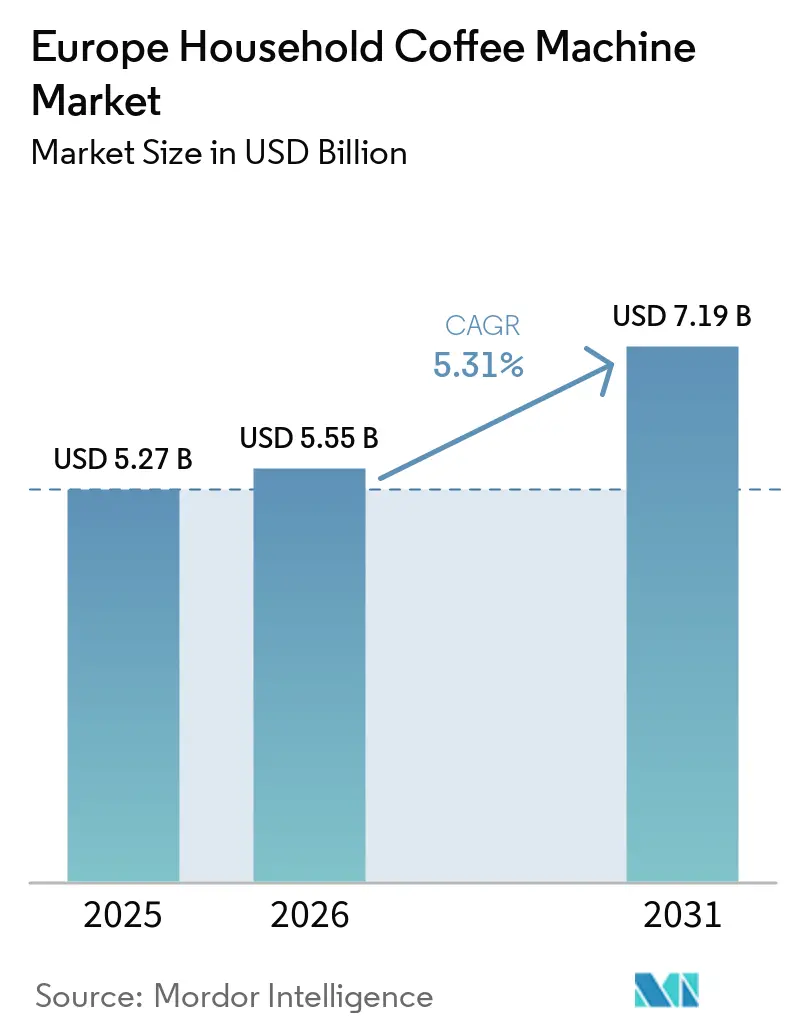

| Base Year Market Size (2025) | USD 5.27 Billion |

| Market Size (2026) | USD 5.55 Billion |

| Market Size (2031) | USD 7.19 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Household Coffee Machine Market Analysis by Mordor Intelligence

The Europe household coffee machine market size is expected to grow from USD 5.27 billion in 2025 to USD 5.55 billion in 2026 and is forecast to reach USD 7.19 billion by 2031 at a 5.31% CAGR from 2026 to 2031. Demand reflects more at-home café-style consumption as hybrid work patterns hold steady and as consumers shift toward higher-value devices that deliver automation and consistent quality. Regulatory changes under the European Union Packaging and Packaging Waste Regulation, effective August 2026, are accelerating sustainable design choices for machines and capsules, which are changing material selection, labeling, and reverse logistics[1]European Commission, “Packaging and Packaging Waste Regulation,” Official Journal of the European Union, eur-lex.europa.eu . The market is expected to witness continued growth, supported by rising demand for convenience and premium coffee experiences. Generation Z is emerging as a significant demographic, showcasing strong preferences for quality, craftsmanship, and personalization in coffee consumption. This group is increasingly investing in at-home brewing equipment, particularly automatic machines capable of grinding whole beans and offering multiple brewing options.

Key Report Takeaways

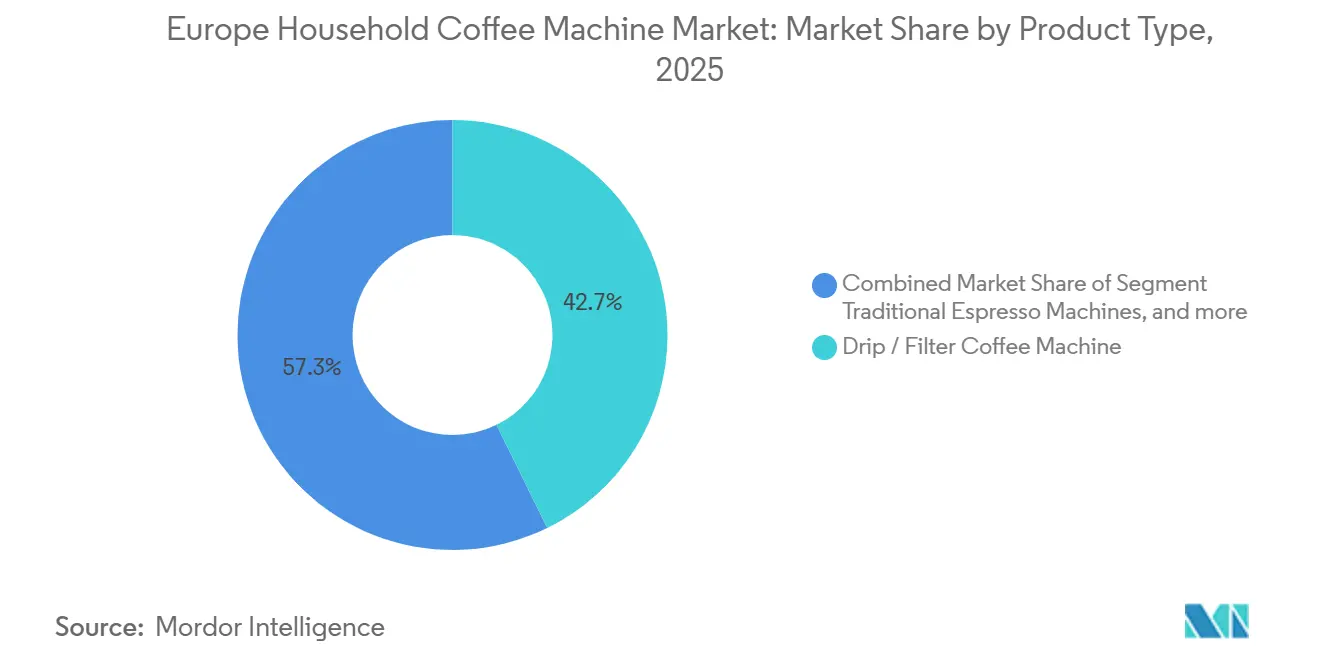

- By product type, drip or filter machines led with 42.74% revenue share in 2025 in the Europe household coffee machine market. Bean-to-cup systems are forecast to grow at a 7.34% CAGR through 2031.

- By automation level, manual and semi-automatic machines held 48.35% of the Europe household coffee machine market share in 2025. Super-automatic systems are projected to expand at a 7.12% CAGR through 2031.

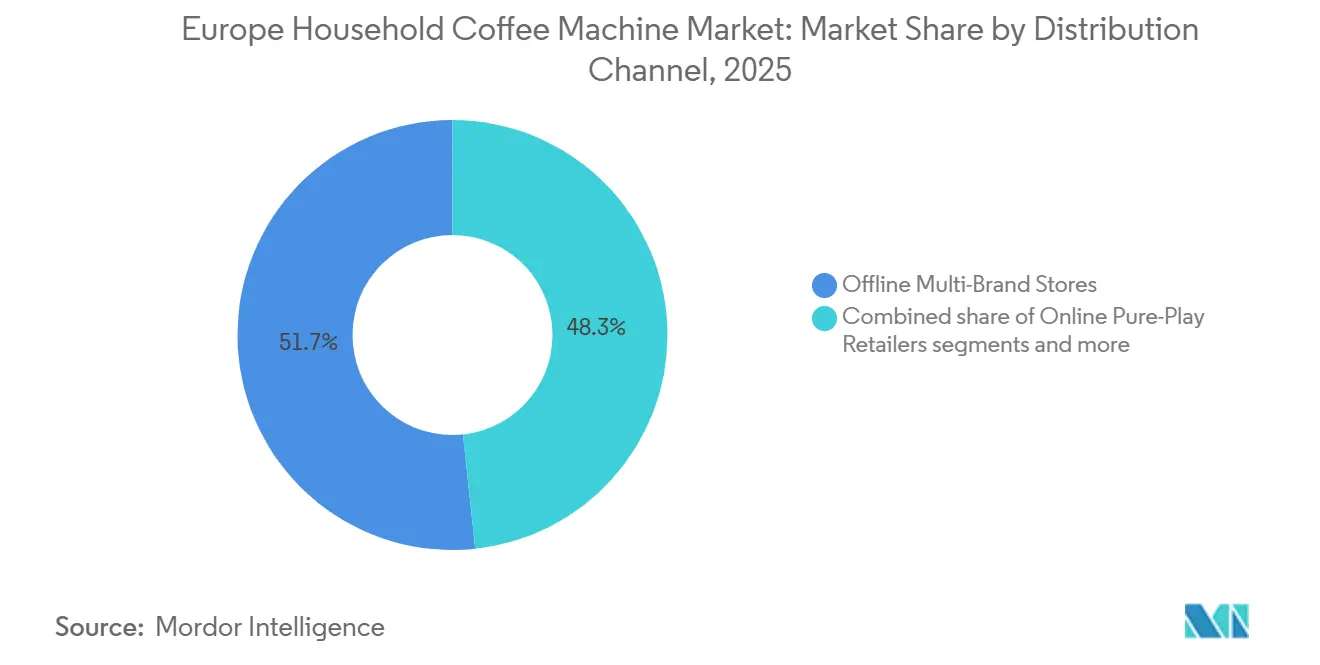

- By distribution channel, offline multi-brand stores held 51.68% share in 2025. Online pure-play retailers are set to grow at a 6.88% CAGR through 2031.

- By geography, Germany led with 22.01% of the Europe household coffee machine market share in 2025. Spain is projected to record the fastest growth with a 6.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Household Coffee Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premiumization and café-style consumption at home | +1.8% | Global, with early gains in Germany, France, and BENELUX | Short term (≤ 2 years) |

| Convenience adoption of capsule ecosystems (hardware + recurring pods) | +1.3% | North America and the European Union core markets | Medium term (2-4 years) |

| Rapid uptake of bean-to-cup fully automatic machines | +2.1% | APAC core, spill-over to Western Europe | Medium term (2-4 years) |

| PPWR-driven redesign toward recyclable or compostable capsules | +0.9% | European Union-27 markets | Long term (≥ 4 years) |

| Subscription-linked machine placement and auto-replenishment | +0.6% | National, with early gains in the United Kingdom, the Netherlands, Nordics | Medium term (2-4 years) |

| Hybrid work sustaining elevated at-home coffee occasions | +1.2% | Global, with strong traction in major European Union economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premiumization and Café-Style Consumption at Home

Households are allocating more of their coffee budgets to machines that deliver café-quality beverages, which is shifting spending from entry-level drip devices to bean-to-cup and enthusiast-grade manual espresso systems. Manufacturers report that premium lines in Europe maintained momentum through 2025 even as pricing pressure rose, suggesting that consumers value extraction quality and design when trading up[2]De'Longhi Group, “H1 2025 Results and Segment Commentary,” De'Longhi Group, delonghigroup.com . Capsule innovation now connects premium positioning with environmental credentials, as brands bring certified compostable and recycled-content formats to market and expand assortments to preserve choice. Premium launches also embed visible sustainability features such as high recycled plastic content and plastic-free packaging, which align with rising consumer expectations and anticipated compliance needs. Local manufacturing and design collaborations help support price realization and brand equity, enabling differentiated narratives that protect margin. The regulatory direction is clear, with content, labeling, and end-of-life rules tightening toward 2030, which reinforces investment in safer materials and verified claims.

Convenience Adoption of Capsule Ecosystems (Hardware + Recurring Pods)

Capsule systems in Europe’s coffee pods and capsules segment link the machine purchase to a recurring stream of pods, which strengthens loyalty and provides predictable replenishment economics. New European Union rules require compostability for certain coffee formats in 2028 and recyclability targets by 2030, which is accelerating the redesigning of materials and supporting logistics for take-back or curbside collection. Brand initiatives include moving to recycled aluminum, scaling paper-based compostable capsules, and expanding access to return channels, although consumer participation in recycling programs still lags potential in many markets. In markets such as France, broader acceptance of aluminum capsules in mainstream household recycling has improved clarity on disposal routes for many consumers. Subscription-linked machine placement is gaining ground, with subsidized hardware tied to minimum monthly capsule commitments that raise lifetime value. PPWR implementation also sets precedents in hospitality and foodservice packaging that influence expectations and compliance strategies for household formats.

Rapid Uptake of Bean-to-Cup Fully Automatic Machines

Fully automatic bean-to-cup systems offer one-touch espresso and milk beverages, which attract busy households that want café outcomes with minimal intervention. Despite aggressive pricing by competitors in 2025, leading brands underscored the strategic importance of fully automatic lines and continued to prioritize product development and channel coverage. Feature sets are advancing to include quieter brewing, app-connected personalization, and simplified maintenance, which improves satisfaction and supports premium price bands. Smart-home interoperability is starting to matter, as devices connect to home platforms for scheduling, voice control, and remote diagnostics that reduce the perceived total cost of ownership. Food-contact regulations in the European Union maintain clear migration limits for plastics used in brew units and reservoirs, which keeps design teams focused on compliant materials and verified suppliers. Concerns over certain chemical substances continue to drive substitution toward safer alternatives in gaskets, seals, and coatings, adding to engineering workloads as companies align with European policy direction.

Hybrid Work Sustaining Elevated At-Home Coffee Occasions

Flexible work has changed when and where Europeans brew coffee, increasing the frequency and value of at-home occasions and stabilizing demand for higher-quality equipment. Surveys indicate that quality coffee can improve perceived well-being and productivity, which reinforces investment in better machines and beans as part of daily routines. Employers are upgrading office coffee programs to meet the expectations of workers who benchmark the office against their home setup, which raises the bar on equipment even beyond the household. Social content has popularized the “home café” aesthetic, which favors compact designs, simple controls, and colorways that integrate into living spaces rather than traditional appliance styling. Connected features that enable recipes, remote control, and proactive maintenance make ownership more enjoyable and predictable for consumers who split time between home and office. The persistence of flexible work arrangements across large European employers suggests sustained support for premium home brewing over the medium term.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Market saturation and extended replacement cycles in mature Western European households | -1.2% | Germany, United Kingdom, BENELUX, Nordics—core markets with 75%+ penetration | Medium term (2-4 years) |

| Energy efficiency and eco-design regulation compliance costs (ErP Lot 25 revisions, energy labeling) | -0.6% | EU27 markets; stricter enforcement in Germany, France, Nordics | Short term (≤ 2 years) |

| Consumer price sensitivity and trade-down pressure amid persistent inflation and economic uncertainty | -0.8% | Spain, Italy, Rest of Europe; emerging impact in UK post-cost-of-living crisis | Short term (≤ 2 years) |

| Inadequate authorized service and spare-parts infrastructure for complex bean-to-cup machines in smaller markets | -0.5% | Rest of Europe, Spain, Italy—limited service networks outside capital cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Market Saturation and Extended Replacement Cycles in Mature Western European Households

In Germany, the United Kingdom, and Nordic markets, over half of households now own coffee machines. This widespread adoption has shifted consumer behavior from buying new machines to replacing old ones. Germany alone accounts for 22% of regional revenue, but consumption contracted sharply to 41 million units in 2024, an 18% year-over-year decline from a 2021 peak of 57 million units, signaling that the easy growth phase has ended. It indicates that the market's rapid growth phase may have ended[3]Indexbox, “Domestic Coffee Machine Europe Market Overview 2024,” Indexbox, indexbox.io . With the market nearing saturation, manufacturers are focusing on enhancing product features rather than expanding sales volumes. However, this shift has resulted in tighter profit margins as technical upgrades quickly become standard. The European Union's right-to-repair directive presents challenges and opportunities for manufacturers. It creates new revenue streams from after-sales services but also requires affordable spare parts and repair access for a specified duration. It extends the lifespan of coffee machines and increases the time between replacements. In affluent regions such as Benelux and Nordic countries, households are delaying upgrades to premium products as long as their current bean-to-cup systems remain functional. The strategy of planned obsolescence, which previously supported appliance turnover, is now facing significant obstacles.

Energy Efficiency and Eco-design Regulation Compliance Costs (Erp Lot 25 Revisions, Energy Labeling)

In May 2025, European Union Regulation 2023/826 enforced standby power limits of 0.5 watts initially and will tighten to 0.3 watts for off mode by 2027. It represents a significant reduction from the previous 1-watt threshold. Such stringent measures pose challenges for connected devices, especially fully automatic machines that depend on constant power for IoT features and instant-heat boilers. Notably, coffee makers, accounting for 5% of the nearly 3 billion devices under this revised standby framework, are feeling the pinch. Brands are now racing against time, redesigning heating blocks, embedding advanced power-management circuits, and undergoing stringent third-party tests to ensure market entry. However, the burden is not evenly distributed. Smaller producers grapple with the weight of certification cycles and mandatory documentation updates. These fixed costs can significantly dent competitiveness, especially when stacked against industry giants like De'Longhi and Philips. These larger manufacturers have the advantage of distributing compliance costs across vast global portfolios. Adding to the challenges, the Ecodesign for Sustainable Products Regulation (European Union) 2024/1781 has introduced further complexities. This regulation mandates the use of recyclable materials and requires digital product passports to monitor resource flows. Such requirements amplify expenses on top of existing energy mandates, pushing the market toward consolidation. Players with in-house sustainability engineering teams stand to gain the most.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bean-to-Cup Surges as Automation Democratizes

Drip or filter machines held the largest share of 2025 at 42.74%, while bean-to-cup systems are projected to grow the fastest at 7.34% through 2031, reflecting a strong appetite for one-touch espresso and milk recipes at home. This balance underscores how the European household coffee machine market continues to pivot from legacy volume segments toward higher-value offerings that deliver consistent quality and convenience. Capsule or pod formats remain important because of their simplicity and broad flavor portfolios, although packaging rules are raising the bar on compostability and recyclability at scale. At the premium end, manual espresso serves enthusiasts who value control and craft, with selective product launches and design collaborations keeping the segment visible without needing mass volume. Premium capsules that combine sensory quality with certified sustainability are reinforcing the upgrade dynamic among consumers who want both performance and environmental credibility.

Connectivity is becoming a key differentiator, with app-guided personalization and maintenance prompts helping consumers keep machines calibrated and clean. Brands are also spotlighting quiet operation, efficient milk systems, and simplified cleaning pathways to reduce effort and support everyday use in compact European kitchens. Compliance with European Union food-contact rules drives careful polymer selection for brew groups and reservoirs, which favors suppliers that can demonstrate traceability and testing. These product traits reinforce premiumization while sustaining the installed base of drip or filter devices for budget-minded buyers, creating a ladder of options that broadens the Europe household coffee machine market.

By Automation Level: Super-Automatic Systems Gain Share Amid Labor Savings

Manual and semi-automatic machines held a 48.35% share in 2025, while fully automatic super-automatic systems are projected to rise at a 7.12% CAGR through 2031. The Europe household coffee machine industry has leaned into this divide by offering streamlined semi-automatic designs that preserve hands-on control while removing complexity from grinding and temperature management. For fully automatic lines, one-touch drink libraries, reliable milk texturing, and rapid heat-up are now table stakes for competitive positioning in mainstream price tiers. Smart-home integration is likely to spread further as brands embed home platform connectivity to schedule brews and surface maintenance notifications. These improvements help close the gap between café beverages and home outcomes, supporting the premiumization path that underpins value growth.

Engineering priorities reflect European policy signals on safety and sustainability, with more attention to durable designs, parts availability, and transparent documentation. Food-contact rules require disciplined supplier quality management, which steadies material choices for reservoirs, tubing, and seals. Subscription bundles also complement higher automation levels by offering predictable replenishment and ownership support through official channels. As features cascade from flagship to entry price points, cost-effective designs that protect reliability will be essential to sustain adoption and brand trust across the Europe household coffee machine market.

By Distribution Channel: Online Pure-Play Retailers Outpace Brick-and-Mortar

Offline multi-brand stores held the largest 2025 share at 51.68%, supported by display, demo, and instant availability. The European household coffee machine market is still moving online because of a broader assortment, user reviews, and delivery convenience that resonate with time-pressed buyers. Brand-owned direct-to-consumer sites are also scaling, enabling manufacturers to capture first-party data and manage the full lifecycle of the consumer relationship from machine to consumables. Specialty kitchenware retailers retain relevance at the premium end, where trained staff and curated assortments help explain features and justify price points. This mix allows consumers to research, trial, and purchase across channels while reinforcing the upgrade path.

Online pure-play retailers are projected to be the fastest-growing format through 2031, which is reshaping how brands plan promotions, content, and bundled offers. Unified commerce platforms that align inventories, prices, and promotions across digital and physical touchpoints are becoming critical enabling infrastructure for large appliance portfolios. European Union packaging and labeling rules are adding digital disclosure requirements, which favor scaled players that can manage EPR registration and traceability across markets. This environment supports healthy competition across formats and gives consumers more control over discovery and ownership across the European household coffee machine market.

Geography Analysis

Germany led with a 22.01% share in 2025, supported by high penetration of premium appliances and a strong culture of at-home coffee experiences. A large base of specialty roasters sustains consumer interest in higher-quality beans that pair well with manual and automatic machines. Leading manufacturers highlighted steady demand in Germany for both capsule models and manual bean-to-cup machines during 2025, even as pricing competition intensified. Broader European appliance portfolios have faced margin compression linked to competitive dynamics and cost inflation, which underscores the need for product differentiation and disciplined execution. Hard-water conditions in several German regions continue to make descaling and water treatment part of the ownership picture, supporting accessory purchases and maintenance solutions. These traits anchor Germany’s role as a large, sophisticated market within the Europe household coffee machine market.

France shows distinct channel and brand dynamics, reflecting deep familiarity with both aluminum and compostable capsule systems, as recycling coverage for aluminum has expanded within household streams. Premium designs that combine precision engineering and heritage themes support value capture, while local manufacturing contributes to trusted positioning. The United Kingdom’s vibrant branded coffee scene continues to influence home replication trends, with consumers adopting devices that can deliver specialty drinks on demand. Subscription-linked machine placement is more visible in France and the United Kingdom, improving loyalty metrics as brands convert hardware buyers into repeat buyers of capsules and beans. Together, France and the United Kingdom reinforce premium and convenience narratives that benefit mid to high-end segments across the Europe household coffee machine market.

Spain is forecast to grow at a 6.68% CAGR through 2031, powered by rising disposable incomes, hospitality recovery, and a cultural tilt toward enjoying café experiences at home. Italy’s espresso heritage remains an anchor for manual and semi-automatic segments, even as capsule and fully automatic lines adjust to PPWR-driven material and labeling shifts. BENELUX markets emphasize circularity and collective action on recycling, with brands working together to expand collection and processing for capsules. Nordic markets tend to favor designs with clear sustainability credentials and energy-conscious brewing, a fit with specialty filter equipment advances highlighted by leading Italian manufacturers investing in Nordic partners[4]Simonelli Group, “Investment in 3TEMP and Nordic Strategy,” Simonelli Group, nuovasimonelli.it . Eastern European markets value affordability and reliability, where drip or filter and capsule devices maintain momentum, with manufacturers using localized assortments to manage currency and price sensitivity. Enforcement intensity and timelines may vary at the national level, yet European Union-level rules are harmonizing minimum expectations, which supports consistent product planning throughout the Europe household coffee machine market.

Competitive Landscape

The European household coffee machine market exhibits moderate concentration, with the top five players together estimated at slightly greater than half of the combined share, and leaders balancing premium positioning with defensive pricing in competitive categories. One cornerstone move was the acquisition of a major stake in La Marzocco by a top household leader, which extends coverage across prosumer and ultra-premium tiers while complementing existing commercial coffee assets. Management commentary in 2025 made clear that aggressive competitor pricing weighed on fully automatic volumes, even as mix and scale helped protect results. This dynamic confirms that scale, channel breadth, and portfolio span are central to defending share while upgrading installed bases across the Europe household coffee machine market.

Broader multi-brand groups illustrated the earnings sensitivity of small appliances to foreign exchange, tariffs, and consumer timing, with a reported decline in operating results from activity during 2025 and a plan focused on procurement and industrial efficiencies through 2027. Innovation-led differentiators include noise-reduction, simplified cleaning, and high recycled content, which help brands hold price points despite promotions in key weeks. Smart-home anchors are also emerging, with Matter-enabled connectivity and interoperable platforms positioning coffee machines within broader connected kitchens. These strategies address the consumer need for reliability, convenience, and lower ownership friction, while maintaining alignment with European policy frameworks on materials and labeling.

White-space opportunities include capsule-system retrofits that align with European Union sustainability requirements, mid-priced connected bean-to-cup lines curated with specialty roasters, and extended-warranty offers that monetize service excellence. Reports from major appliance portfolios have also flagged rising competition from Asian entrants and online-native retailers capturing price-sensitive demand, which reinforces the need for digital-first commercial capabilities. Leading premium fully automatic brands continue to push sensors and recipe intelligence, while capsule leaders scale paper-based compostable options with third-party certifications. Professional coffee cloud platforms from large groups provide a technology pathway that can inform consumer offerings, particularly on telemetry and preventive care, strengthening differentiation and attachment across the Europe household coffee machine market.

Europe Household Coffee Machine Industry Leaders

De'Longhi Group

Philips Domestic Appliances (Versuni; incl. Saeco, Gaggia)

Groupe SEB (Krups; Rowenta)

BSH Hausgeräte (Bosch; Siemens)

Nestlé Nespresso

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Keurig Dr. Pepper launched a EUR 31.85 per share all-cash tender offer for JDE Peet's, with plans to spin off combined coffee operations into a new global pure-play coffee company after closing in Q2 2026.

- September 2025: Ardian and Hameur Group entered exclusive discussions to sell Magimix to Lavafields Group, aligning their strategy to focus on professional equipment at Robot-Coupe.

- August 2025: Keurig Dr. Pepper and JDE Peet's announced a definitive agreement for KDP to acquire JDE Peet's in an all-cash transaction, followed by a tax-free spin-off to create two independent United States-listed companies, with closing anticipated in H1 2026.

Europe Household Coffee Machine Market Report Scope

This report aims to find opportunities in the coffee machine market in European households, with a continuous increase in coffee consumption and production worldwide. Since 2012, the price of coffee has observed a continuous fluctuation, with which the use of the coffee machine is correlated to an extent, and they both affect each other. Different varieties of coffee machinery available to consumer stores play a major role in providing consumer machinery in-built with different technologies and usage purposes. Geographical-wise, production and consumption have a major impact on consumer behavior.

The Europe household coffee machine market is segmented by product type, automation level, distribution channel, and geography. By product type, the market is divided into drip/filter coffee machines, capsule/pod coffee machines, traditional espresso machines, bean-to-cup coffee machines, and pour-over and manual specialty machines. By automation level, the market is segmented into manual and semi-automatic machines and fully automatic machines. By distribution channel, the market includes multi-brand electrical and appliance stores, specialty coffee and kitchenware stores, online pure-play retailers, direct-to-consumer webshops, and mass merchandisers and hypermarkets. Geographically, the market analysis covers the United Kingdom, Germany, France, Spain, Italy, BENELUX (Belgium, Netherlands, Luxembourg), NORDICS (Denmark, Finland, Iceland, Norway, Sweden), and the rest of Europe. The report provides market size and forecasts for the Europe household coffee machine market in value (USD) across all the above segments.

By Product Type

| Drip / Filter Coffee Machines |

| Capsule / Pod Coffee Machines |

| Traditional Espresso Machines |

| Bean-to-Cup Coffee Machine |

| Pour-Over and Manual Specialty Machines |

By Automation Level

| Manual and Semi-Automatic Machines |

| Fully Automatic Machines |

By Distribution Channel

| Multi-Brand Electrical and Appliance Stores |

| Specialty Coffee and Kitchenware Stores |

| Online Pure-Play Retailers |

| Direct-to-Consumer Webshops |

| Mass Merchandisers and Hypermarkets |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| BENELUX (Belgium, Netherlands, Luxembourg) |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) |

| Rest of Europe |

| By Product Type | Drip / Filter Coffee Machines |

| Capsule / Pod Coffee Machines | |

| Traditional Espresso Machines | |

| Bean-to-Cup Coffee Machine | |

| Pour-Over and Manual Specialty Machines | |

| By Automation Level | Manual and Semi-Automatic Machines |

| Fully Automatic Machines | |

| By Distribution Channel | Multi-Brand Electrical and Appliance Stores |

| Specialty Coffee and Kitchenware Stores | |

| Online Pure-Play Retailers | |

| Direct-to-Consumer Webshops | |

| Mass Merchandisers and Hypermarkets | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the Europe household coffee machine market growth outlook through 2031?

The Europe household coffee machine market is projected to reach USD 7.19 billion by 2031 at a 5.31% CAGR from 2026 to 2031, supported by premiumization, automation, and sustainability-led redesigns.

Which product categories are leading, and which are growing fastest in Europe?

Drip or filter machines led with 42.74% share in 2025, while bean-to-cup systems are forecast to grow the fastest at 7.34% through 2031, reflecting demand for one-touch café-quality outcomes at home.

How is regulation shaping household coffee machines and capsules in Europe?

The European Union Packaging and Packaging Waste Regulation sets milestones for compostability in 2028 and recyclability by 2030, which is influencing materials, labeling, and reverse logistics for machines and capsules.

Which channels are gaining momentum for coffee machines in Europe?

Online pure-play retailers are set to outpace offline formats through 2031, while multi-brand stores still hold the largest 2025 share and serve as important demo and discovery venues.

Which countries are central to demand, and where is growth strongest?

Germany held the largest 2025 share at 22.01%, reflecting a mature and premium-oriented base, while Spain is projected to grow fastest at a 6.68% CAGR through 2031.

What is driving the shift to fully automatic machines?

Consumers value one-touch convenience, recipe variety, and app-connected personalization, and brands are responding with quieter brewing, simplified cleaning, and smart-home interoperability to strengthen adoption.

Page last updated on: