Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.48 Billion |

| Market Size (2031) | USD 19.4 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Household Coffee Machine Market Analysis by Mordor Intelligence

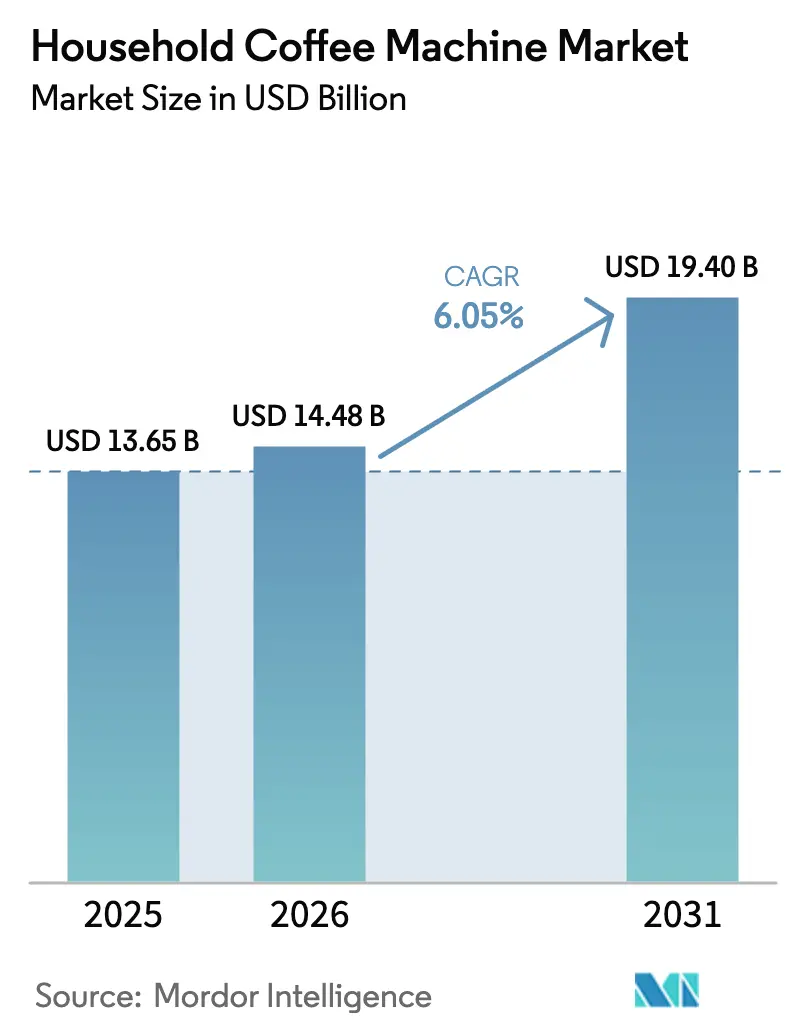

The household coffee machines market size was valued at USD 13.65 billion in 2025 and estimated to grow from USD 14.48 billion in 2026 to reach USD 19.4 billion by 2031, at a CAGR of 6.05% during the forecast period (2026-2031). Rising in-home coffee preparation, premium home-brewing experiences that undercut café prices, and improving smart-appliance technology combine to accelerate the coffee machine market. Consumers in developed economies increasingly substitute retail visits with premium pods, bean-to-cup automation, and connected brewers that mimic barista output. Regulatory moves that reward energy-efficient designs spur innovation and replacement demand, while digital shopping habits broaden access to a wider product range. The fast-evolving competitive field now blends long-standing appliance leaders with agile entrants leveraging e-commerce reach and smart-home ecosystems.

Key Report Takeaways

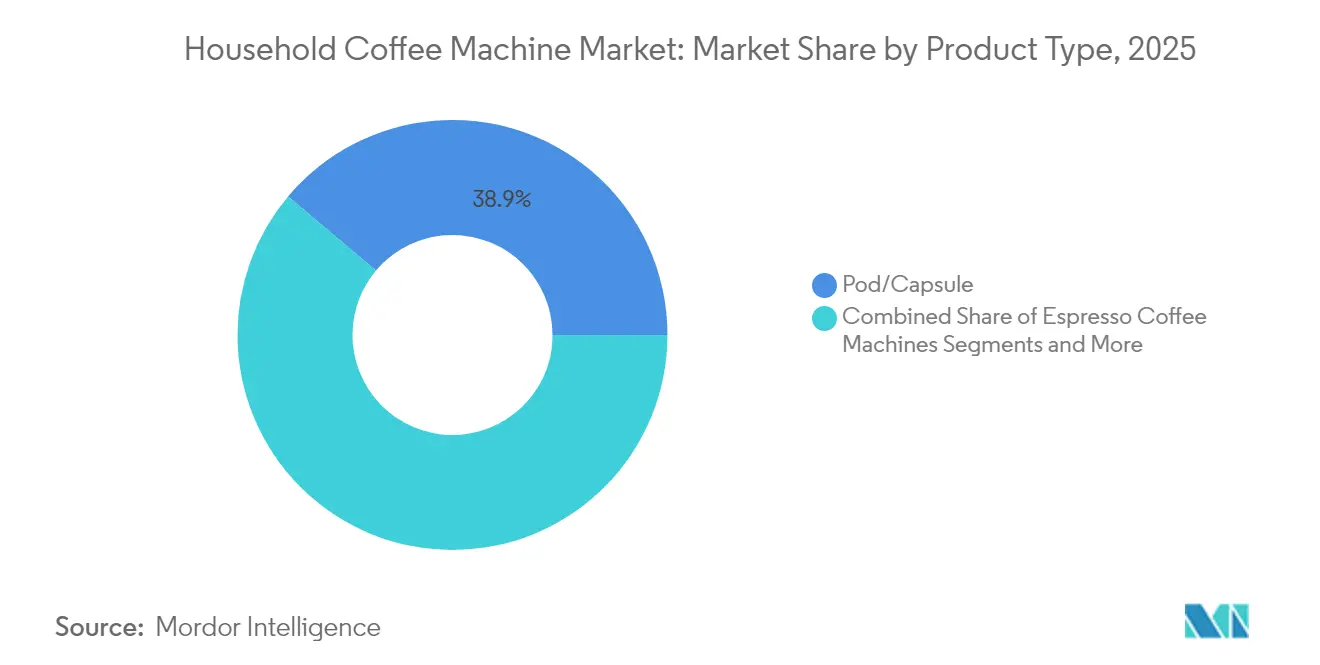

- By product type, pod and capsule machines led with 38.86% of household coffee machines market share in 2025, while bean-to-cup machines are projected to expand at an 8.34% CAGR through 2031.

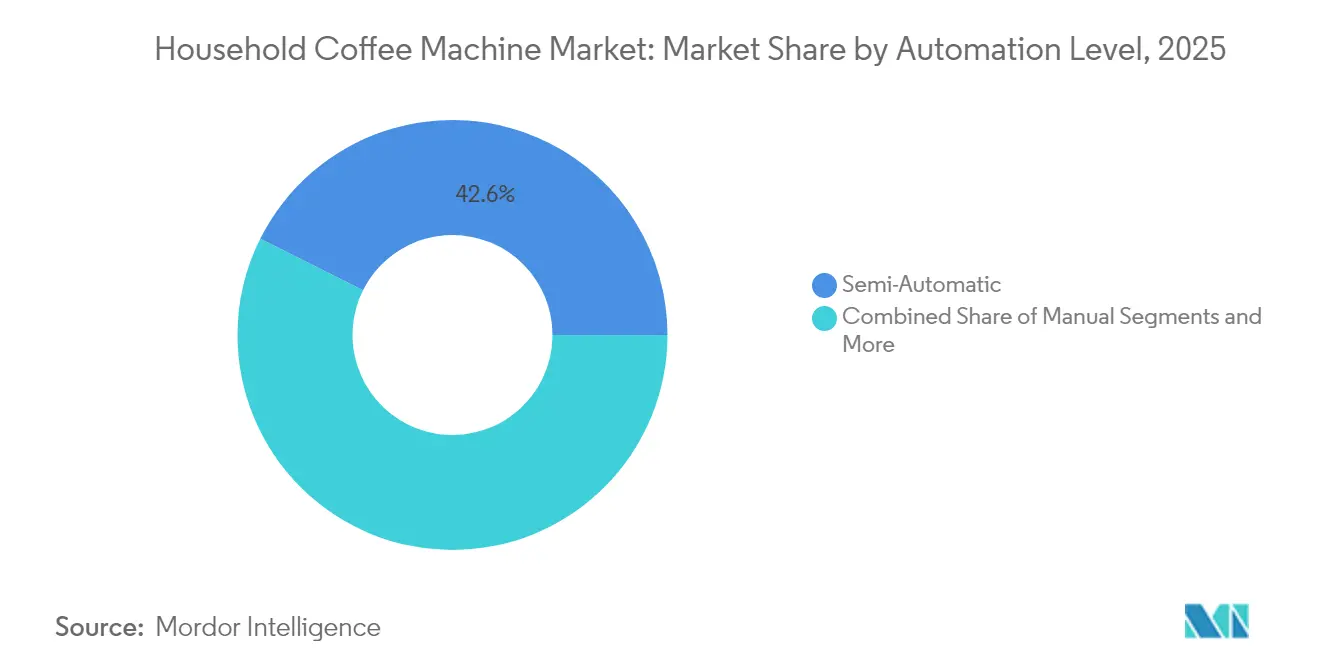

- By automation level, semi-automatic machines accounted for 42.62% of the household coffee machines market size in 2025; fully automatic units recorded the fastest trajectory at 7.75% CAGR.

- By distribution channel, supermarkets and hypermarkets held 46.85% of the household coffee machines revenue share in 2025, whereas online retail is advancing at a 9.22% CAGR to 2031.

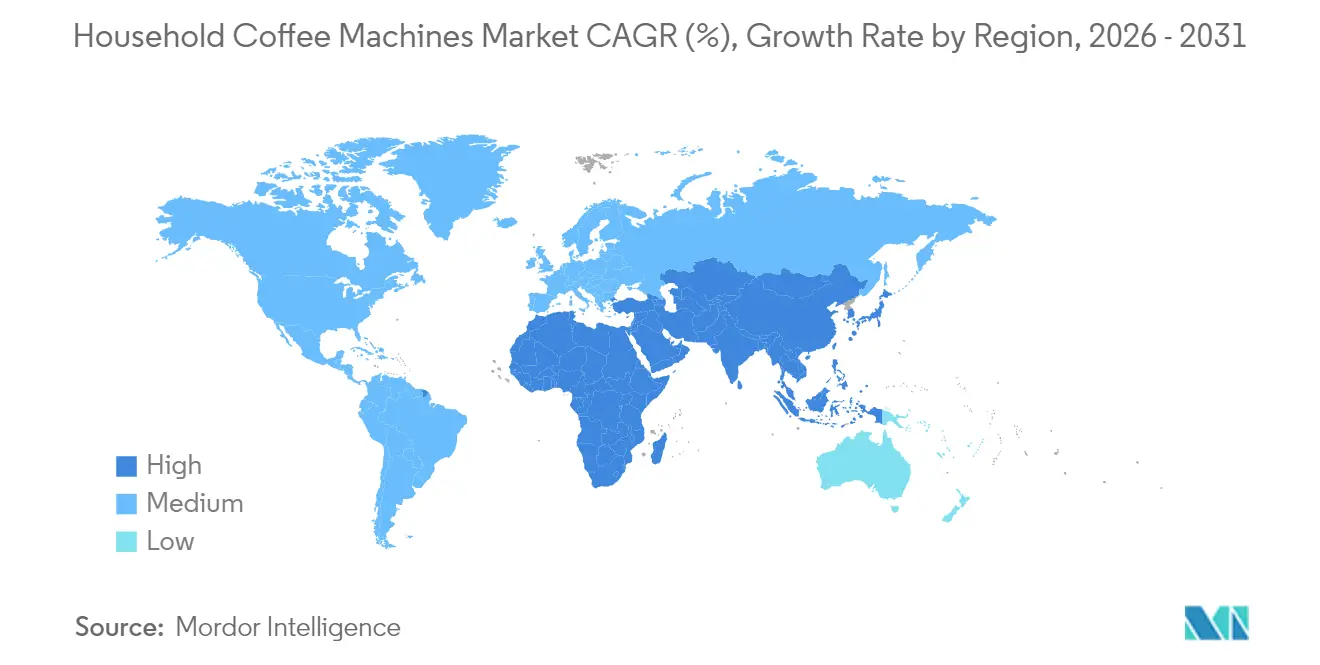

- By geography, North America represented 32.88% of the household coffee machines revenue in 2025, while Asia-Pacific is set to post the highest regional CAGR at 7.41% by 2031.

- Keurig Dr Pepper, De’Longhi Group, Nestlé Nespresso, Breville Group, and Hamilton Beach collectively controlled a sizable portion of the global market in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Household Coffee Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer Shift to At-Home Coffee Rituals in North America & Europe | +1.8% | North America & Europe | Medium term (2-4 years) |

| Convenience-Led Surge in Pod/Capsule Subscriptions | +1.2% | Global, strongest in North America | Short term (≤ 2 years) |

| Growing Espresso Culture in Tier-1 Asian Cities | +1.5% | Asia-Pacific core, spill-over to MEA | Long term (≥ 4 years) |

| IoT-Enabled Smart Machines Elevating Replacement Demand | +0.9% | Global, led by North America & Europe | Medium term (2-4 years) |

| Energy-Efficient Designs Driven by EU Eco-Directives | +0.7% | Europe, with global manufacturing implications | Long term (≥ 4 years) |

| Direct-to-Consumer Bundled Coffee-Machine Plans | +0.4% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Consumer Shift to At-Home Coffee Rituals in North America and Europe

Remote and hybrid work patterns entrenched a daily home-brewing habit across developed markets. Household penetration of single-serve and bean-to-cup appliances rose alongside inflation-driven café avoidance. The National Coffee Association reported that coffee would replace bottled water as the most purchased beverage by US consumers in 2025[1]Source: National Coffee Association, “National Coffee Data Trends 2025,” ncausa.org . Manufacturers responded with compact countertop designs and flavor-forward recipes that replicate café specials, such as pistachio lattes, boosting premium equipment sales. Seasonal flavor experimentation resonates with Gen Z buyers who favor personalization. These lifestyle shifts sustain demand beyond cyclical income changes, embedding long-term volume growth for the coffee machines market.

Convenience-Led Surge in Pod and Capsule Subscriptions

Subscription plans that bundle brewers with recurring capsule deliveries transform one-time hardware purchases into annuity streams for brand owners. Keurig Dr Pepper reported an installed base exceeding 38 million US households, demonstrating the lock-in advantage of closed systems. Nespresso’s direct-to-consumer expansion in Asia couples rapid capsule replenishment with premium positioning that appeals to new urban consumers. EU circular-economy rules accelerate the shift toward aluminum and compostable capsules, and industry leaders fund in-market recycling schemes that mitigate environmental concerns. Convenience, portion control, and mess-free disposal keep pod machines central to daily routines, ensuring sustained volume momentum.

Growing Espresso Culture in Tier-1 Asian Cities

Rising middle-class incomes and aspirational café lifestyles underpin strong espresso adoption in Mainland China, India, and Southeast Asia. China overtook the United States in branded coffee shop outlets in 2024, and Sucafina forecasts Asian coffee consumption to climb above 4.4% annually by 2026. Mobile-app ordering now accounts for 80% of Chinese coffee transactions, setting expectations for connected home devices that integrate with popular payment and loyalty platforms. First-time buyers often enter through affordable capsule systems before trading up to bean-to-cup units as palates mature. The region’s demographic profile and digital openness position Asia-Pacific as the primary growth engine for the coffee machines market.

IoT-Enabled Smart Machines Elevating Replacement Demand

Connected brewers move coffee preparation from manual prints to data-rich experiences. ThermoplanConnect enables live diagnostics, remote recipe updates, and fleet management, reducing downtime for commercial operators. At the household level, voice assistants trigger scheduled brewing, while apps learn consumption patterns to optimize energy use. The US Department of Energy has published upgraded energy conservation standards for coffee brewers that take effect in 2029[2]Source: Federal Register, “Energy Conservation Program: Revised Standards for Commercial Coffee Brewers,” federalregister.gov . Compliance favors new-generation machines with smart power management and efficient heating elements, prompting accelerated replacement cycles. The technology premium widens margins and differentiates brands in a crowded field.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High ASPs Limiting Penetration in Price-Sensitive South America | -0.8% | South America, with spillover to emerging markets | Medium term (2-4 years) |

| Regulatory Scrutiny on Single-Use Capsules in the EU | -0.6% | Europe, with global implications for manufacturers | Long term (≥ 4 years) |

| Semiconductor Shortages Inflating Lead-Times | -0.5% | Global, most acute in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| RTD Coffee Popularity Cannibalising Entry-Level Machines | -0.4% | Global, strongest in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High ASPs Limiting Penetration in Price-Sensitive South America

Currency devaluation and commodity-driven inflation lift the cost of imported appliances in several Latin markets. Retail coffee prices in Brazil spiked in 2024, and additional increases are forecast for 2025, constraining discretionary spending. Entry-level machines hold their ground, yet premium espresso systems struggle for reach. Select manufacturers pivot to modular designs that allow gradual feature upgrades, improving affordability. Simultaneously, premium coffee beans enjoy double-digit growth in metropolitan Brazil, signaling distinct niches within the region. Targeted promotional finance and local assembly agreements could narrow the price gap over the medium term.

Regulatory Scrutiny on Single-Use Capsules in the EU

Europe continues to tighten sustainability mandates. The new Ecodesign Regulation (EU) 2024/1781 enforces minimum energy-efficiency thresholds and recyclable materials for coffee appliances[3]Source: European Parliament, “Regulation (EU) 2024/1781 Establishing Ecodesign Requirements,” europarl.europa.eu . Manufacturers must also prepare digital product passports that track resource usage over a unit’s life. Compliance costs weigh more heavily on smaller producers, prompting consolidation and technology partnerships. Market leaders invest in recycled aluminum flows and biodegradable polymer research to preserve capsule convenience while meeting environmental objectives. Although the rules raise short-term costs, they stimulate innovation that supports long-term competitiveness in the coffee machines market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pod Systems Drive Volume, Bean-to-Cup Captures Value

Pod and capsule machines delivered 38.86% of global revenue in 2025, reflecting the twin appeal of speed and consistency. Many households regard capsule brewers as the simplest path to espresso-quality drinks without barista skills. The subscription sales model for consumables locks in brand switching costs while generating predictable replenishment volume. Nespresso leverages this framework by offering boutique recycling hubs and loyalty rewards that anchor premium positioning. Domestic Chinese challengers such as Joyoung price aggressively, broadening entry-level access and propelling regional growth.

Bean-to-cup machines, by contrast, dominate the upper price tiers and represent the fastest-growing line with an 8.34% CAGR to 2031. This segment attracts enthusiasts seeking freshly ground beans, automatic milk texturing, and personalized profiles. Commercial variants command list prices of USD 10,000–20,000 and offer programmable recipes for cafés and offices. As connectivity improves, cloud-based telemetry aids predictive maintenance, reducing downtime and justifying inclusive service contracts. Drip coffee makers retain relevance among budget-minded users, especially in North American markets where filter taste profiles remain popular. Traditional percolators and pour-over gear occupy cultural niches but contribute little incremental revenue. The diverging paths of convenience-driven pods and experience-driven bean-to-cup units highlight a barbell structure that guides product development and marketing investments across the coffee machines market.

By Automation Level: Semi-Automatic Dominance Faces Full-Auto Challenge

Semi-automatic machines captured 42.62% of 2025 revenue, balancing hands-on extraction control with approachable learning curves. Enthusiast consumers appreciate the craft element yet benefit from built-in pressure stability and temperature accuracy. Manufacturer upgrades now bundle pressure profiles, smart tamping sensors, and PID controllers, extending the lifespan of the semi-automatic class. The category also enjoys robust aftermarket communities offering customizable portafilters and burr upgrades that lengthen ownership cycles.

Fully automatic systems grow the fastest at 7.75% CAGR because their one-touch simplicity resonates with busy households that prioritize repeatable results. Embedded grinders, milk systems, and self-cleaning programs compress preparation time to seconds. The coffee machines market size for fully automatic equipment reached USD 4.88 billion in 2026 and is forecast to top USD 7.07 billion by 2031. IoT integration further elevates the appeal by enabling remote start, consumable reordering, and energy-saving modes. Voice assistants such as Alexa and Google Home now pair with several flagship brewers, bringing coffee routines into broader smart-home ecosystems. Manual lever machines serve a passionate niche of purists but lack the scale to challenge mainstream segments

By Distribution Channel: Digital Transformation Accelerates Retail Evolution

Online retail represents the fastest trajectory, advancing at 9.22% CAGR through 2031. The pandemic-era shift to digital discovery persisted as consumers learned to compare specifications, read peer reviews, and access niche brands beyond local shelves. Lavazza reported a 28% year-on-year rise in global e-commerce revenue in 2024. Leading marketplaces amplify promotional peaks, with coffee machine demand spiking during events such as Prime Day. Brands bundle subscription offers and extended warranties to reinforce direct orders, capturing first-party shopper data that informs product roadmaps.

Despite digital gains, supermarkets and hypermarkets maintained 46.85% channel share in 2025 by offering instant product availability and the convenience of same-basket capsule refills. Omnichannel strategies now merge physical displays with QR-code access to online content, bridging information gaps. Specialty coffee retailers preserve a role as experiential hubs for machine demonstrations, latte art tutorials, and accessory cross-selling. Direct-to-consumer brand stores expand through high-footfall malls where immersive brewing bars educate potential buyers and convert trial into sales.

Geography Analysis

North America contributed 32.88% of global revenue in 2025 and remains the largest regional market. High household penetration and a mature café culture form a solid baseline, yet innovation continues to unlock incremental spending. Keurig Dr Pepper shipped 10.4 million brewers in 2024, reinforcing replacement cycles and pod subscription growth. Smart-home adoption catalyzes demand for Wi-Fi and voice-controlled units, while sustainability concerns channel attention to energy ratings and recyclable materials. Canadian consumers mirror US preferences, with premium single-serve units outperforming entry-level drip models, and Mexico records steady uptake driven by urban middle-class expansion.

Asia-Pacific is the fastest-growing territory, recording a 7.41% CAGR toward 2031. The coffee machines market size for the region stood at USD 3.58 billion in 2026 and is projected to exceed USD 5.12 billion in 2031. China’s branded café boom spills into home adoption as consumers seek to replicate familiar espresso beverages. Domestic appliance makers integrate local payment apps and social-sharing features, tailoring value propositions to tech-savvy millennials. India follows with strong demand in metropolitan pockets, while Vietnam, Indonesia, and the Philippines expand from low installed bases. Local assembly initiatives limit tariffs and customize voltage specifications, enhancing affordability and cultural fit.

Europe delivers stable growth despite strict environmental legislation. The Ecodesign Regulation compels appliance makers to redesign heating blocks, standby consumption, and material recyclability. Early adopters accept marginal price premiums for units carrying EU energy labels, reinforcing a virtuous cycle of sustainability investment. Southern Europe’s espresso tradition underpins demand for semi-automatic machines, whereas Northern markets lean toward fully automatic convenience. South America’s potential remains tempered by macroeconomic volatility. Retailers in Brazil introduce installment plans to mitigate currency depreciation, yet replacement cycles lengthen as consumers delay non-essential upgrades. The Middle East and Africa offer niche prospects, anchored by specialty café proliferation in the Gulf and rising urbanization in East Africa, although fragmented distribution and price sensitivity pose challenges.

Competitive Landscape

The household coffee machine industry increasingly depends on companies' ability to innovate while maintaining operational efficiency. Incumbent players must focus on continuous product development, incorporating advanced features like customization options and smart connectivity while ensuring user-friendly interfaces. Building strong distribution networks, particularly in emerging markets, remains crucial for market expansion. Companies need to develop comprehensive after-sales service networks and maintain strong relationships with retailers and e-commerce platforms to ensure market penetration and customer satisfaction.

For contenders looking to gain market share, differentiation through unique features, design aesthetics, or price positioning is essential. The relatively low risk of substitution from alternative coffee brewing equipment methods provides opportunities for new entrants to establish themselves in specific market segments. Success factors include developing strong brand identities, establishing efficient supply chains, and creating compelling value propositions that address specific consumer needs. Regulatory compliance, particularly regarding product safety and environmental standards, plays a crucial role in market success, with companies needing to adapt their products and processes to meet evolving requirements across different regions.

Household Coffee Machine Industry Leaders

Keurig Dr Pepper Inc.

De’Longhi Group

Nestlé Nespresso SA

Breville Group Ltd.

Hamilton Beach Brands Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2024: Westrock Coffee unveiled a USD 315 million ready-to-drink plant in Arkansas featuring advanced robotics to target RTD demand.

- May 2024: Melitta Group acquired a majority stake in South Africa’s Caturra to accelerate Africa growth.

- March 2024: Louis Dreyfus Company agreed to purchase Brazilian instant-coffee exporter Cacique, enhancing its soluble portfolio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the household coffee machine market as all factory-built appliances designed to brew coffee in a domestic setting, spanning manual drip makers through fully automatic bean-to-cup systems and smart, IoT-enabled units. Values reflect brand-new equipment shipped to retailers or direct-to-consumer channels in USD at ex-factory prices.

Scope exclusion: Commercial espresso stations and office-service vending brewers are outside this appraisal.

Segmentation Overview

- By Product Type

- Drip Coffee Machines

- Espresso Coffee Machines

- Pod/Capsule Coffee Machines

- Bean-to-Cup (Automatic Espresso) Machines

- Percolators & Others

- By Automation Level

- Manual

- Semi-Automatic

- Fully Automatic

- Smart Connected / IoT-Enabled

- By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Stores

- Online Retail

- Direct-to-Consumer (Brand Stores & Subscriptions)

- Other Offline Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

We interviewed appliance distributors, online category managers, and product engineers across North America, Europe, and Asia-Pacific to test adoption curves, average selling prices, and replacement cycles. Surveys with everyday coffee enthusiasts helped us validate pod-machine penetration assumptions and channel shifts that desk research could only partially surface.

Desk Research

Mordor analysts first mapped global demand using open data from bodies such as the International Coffee Organization, UN Comtrade, World Bank Household Expenditure series, and appliance safety registries. They then layered insights from industry associations like the European Coffee Federation and the Small Appliance Manufacturers Association. Company filings and investor decks supplied pricing and margin indicators, while D&B Hoovers and Dow Jones Factiva provided revenue splits that anchor brand-level shipment ratios. The sources cited here illustrate but do not exhaust the secondary material reviewed.

Market-Sizing & Forecasting

A top-down production and trade reconstruction converts small-appliance output, import, and export data into regional demand pools, which are then sense-checked through selective bottom-up roll-ups of leading supplier shipments and sampled ASP × volume checks. Key variables like household coffee consumption per capita, single-serve pod share of brews, e-commerce share of small appliances, specialty coffee shop density, and discretionary income growth feed a multivariate regression that projects value through 2030. Gap areas in bottom-up inputs are bridged with weighted medians from primary interviews.

Data Validation & Update Cycle

Outputs undergo variance screening against independent retail indices; outliers trigger analyst rework and second-level peer review. Reports refresh each year, with interim updates if currency swings, trade policy shifts, or material technology launches alter baseline demand. A pre-publication sweep ensures clients receive the most current view.

Why Mordor's Global Household Coffee Machine Baseline Commands Reliability

Published estimates differ because firms choose distinct product baskets, price bases, and forecast cadences.

Key gap drivers include: some publishers fold office brewers into totals, others lock forecasts to constant 2022 dollars, and a few extrapolate forward sales from pandemic-era peaks without validating replacement cycles.

Mordor's model, by contrast, isolates true household units, refreshes variables annually, and blends cautious replacement assumptions with live ASP tracking.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 13.65 B | Mordor Intelligence | - |

| USD 11.75 B | Global Consultancy A | Excludes smart brewers; uses 2020 ASPs |

| USD 15.00 B | Industry Association B | Combines household and office units; optimistic 10-year replacement |

The comparison shows that, while other figures swing wide, Mordor's disciplined scoping, annual refresh, and dual validation give decision-makers a balanced, transparent baseline they can trace back to explicit variables and repeatable steps.

Key Questions Answered in the Report

What is the projected growth rate for the coffee machines market between 2026 and 2031?

The market is forecast to grow at a 6.05% CAGR, climbing from USD 14.48 billion in 2026 to USD 19.4 billion by 2031.

Which product segment is expanding the fastest?

Bean-to-cup automatic machines lead growth with an 8.34% CAGR through 2031, reflecting rising demand for café-quality drinks at home.

How quickly is online retail gaining ground as a sales channel?

Online retail is advancing at a 9.22% CAGR, outpacing all other channels as consumers favor digital research and direct-to-door delivery.

Which region offers the highest growth potential over the next five years?

Asia-Pacific shows the strongest outlook with a 7.41% CAGR, underpinned by China’s expanding espresso culture and rapid urbanization across India and Southeast Asia.

What regulatory changes are most likely to affect product design?

The EU Ecodesign Regulation, effective July 2024, and US energy-efficiency standards set for 2029 are pushing manufacturers toward more energy-efficient and recyclable machines.

Page last updated on: