Cocoa Fiber Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

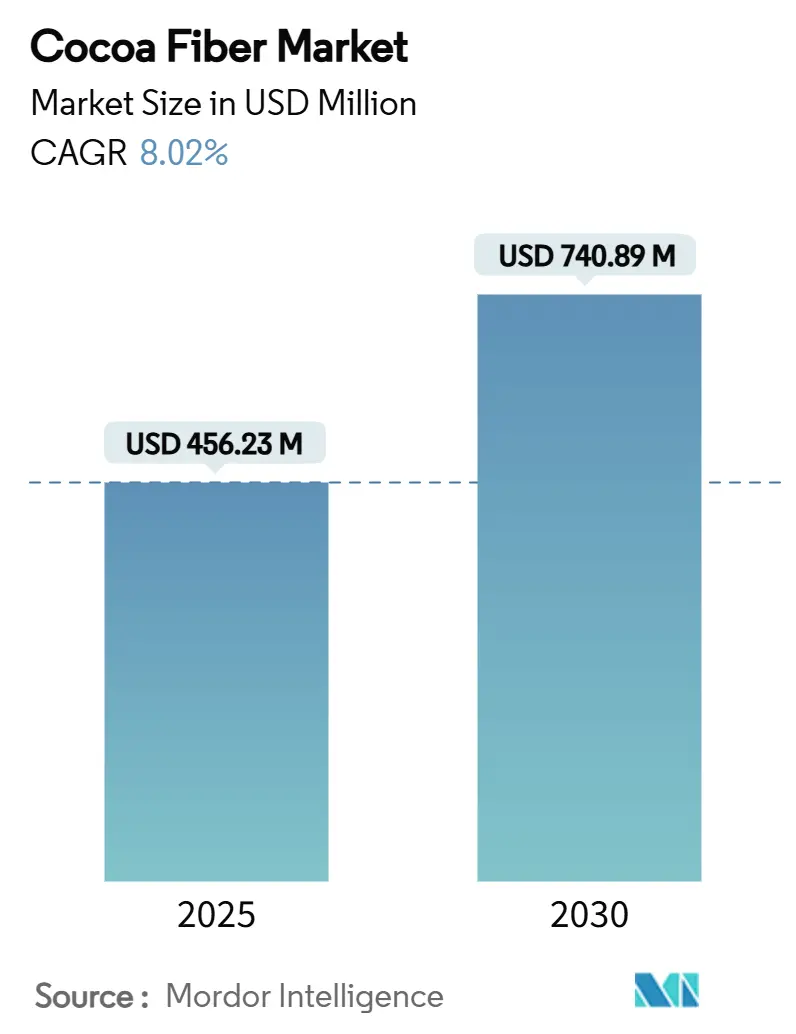

| Market Size (2025) | USD 456.23 Million |

| Market Size (2030) | USD 740.89 Million |

| Growth Rate (2025 - 2030) | 8.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cocoa Fiber Market Analysis by Mordor Intelligence

The cocoa fiber market size stood at USD 456.23 million in 2025 and is forecast to reach USD 740.89 million in 2030, posting an 8.02% CAGR during 2025-2030. This solid growth pace reflects the widening use of upcycled ingredients across food, personal care, and nutraceutical lines, together with strong regulatory support for dietary-fiber claims. Brand owners are turning to cocoa shell fiber to offset cocoa-price inflation, improve product nutrition, and strengthen sustainability credentials, which raises adoption across mainstream bakery and confectionery portfolios. Expanded consumer interest in clean-label foods, coupled with technology that standardizes particle size and removes contaminants, further propels the cocoa fiber market, while the ingredient’s natural chocolate flavor supports premium positioning in high-growth segments such as functional snacks and cosmetics. Heightened competition from coffee silverskin and fruit-based fibers puts pricing pressure, yet cocoa fiber’s unique sensory attributes and prebiotic profile maintain its appeal.

Key Report Takeaways

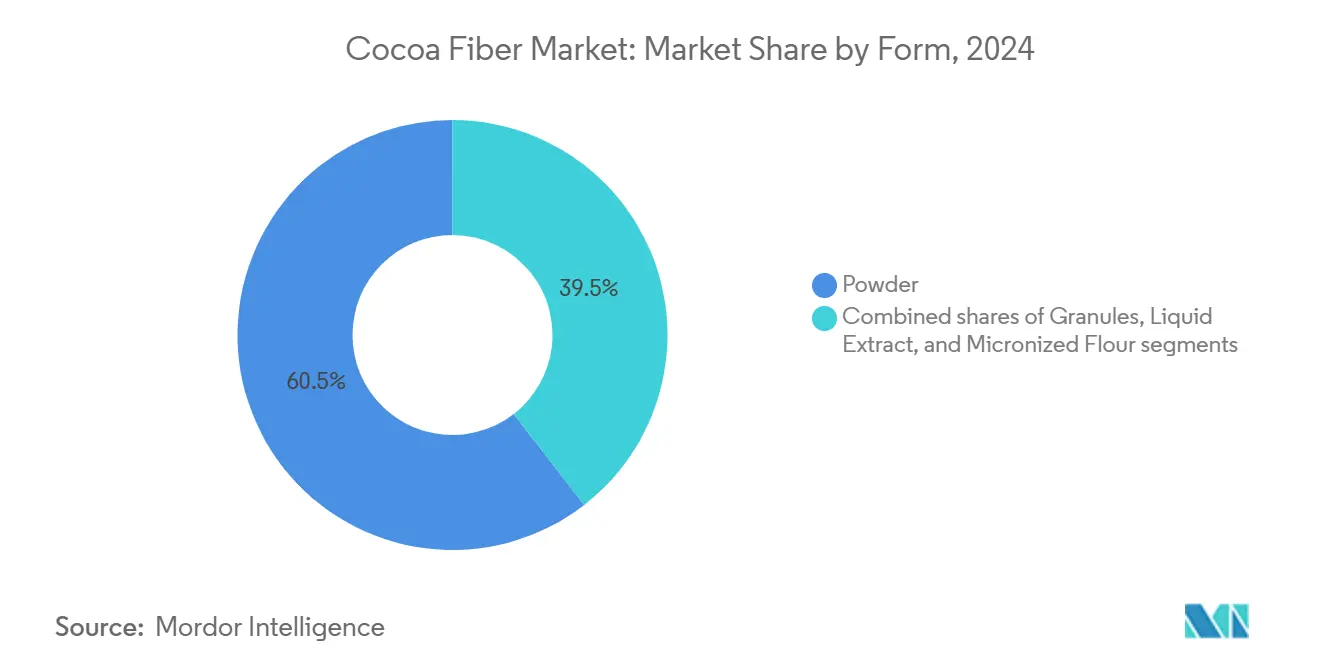

- By product form, powder held 60.50% of the 2024 cocoa fiber market share and is projected to advance at a 9.50% CAGR to 2030.

- By fiber type, soluble dietary fiber captured 56.78% of the 2024 share; mixed fiber blends are forecast to climb at a 9.02% CAGR through 2030.

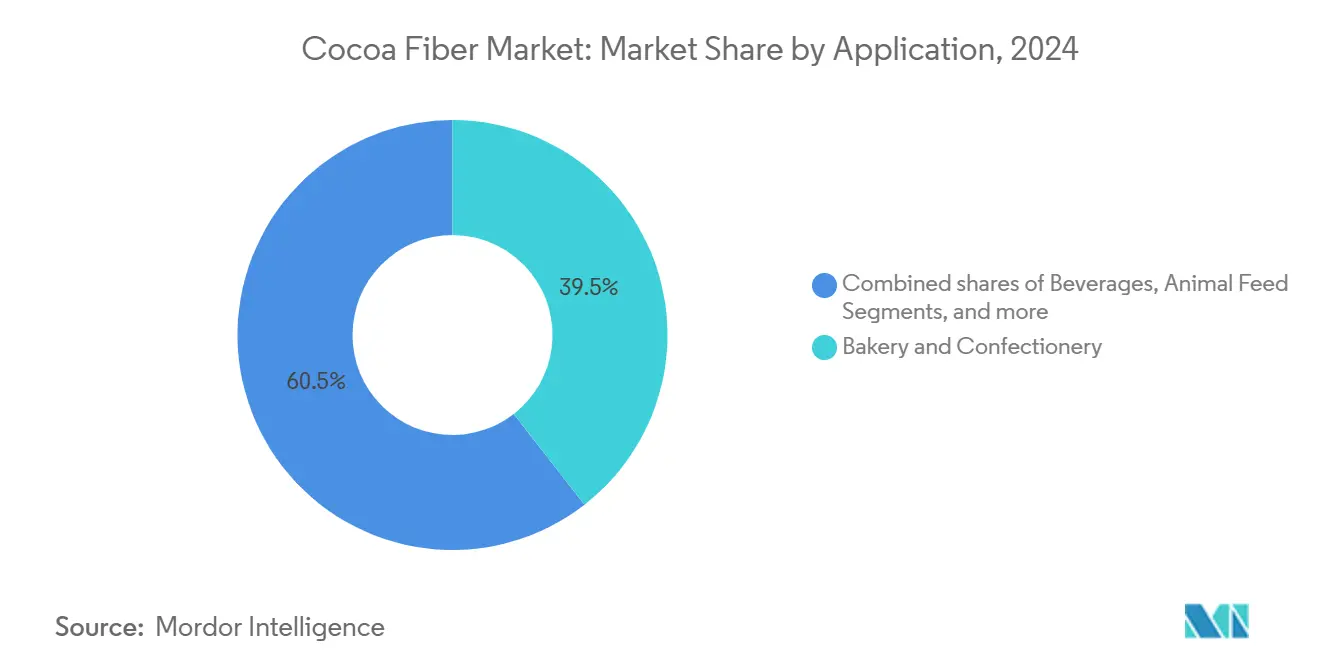

- By application, bakery and confectionery accounted for 39.49% of the shares in 2024, whereas personal care and cosmetics are set to rise at a 9.84% CAGR.

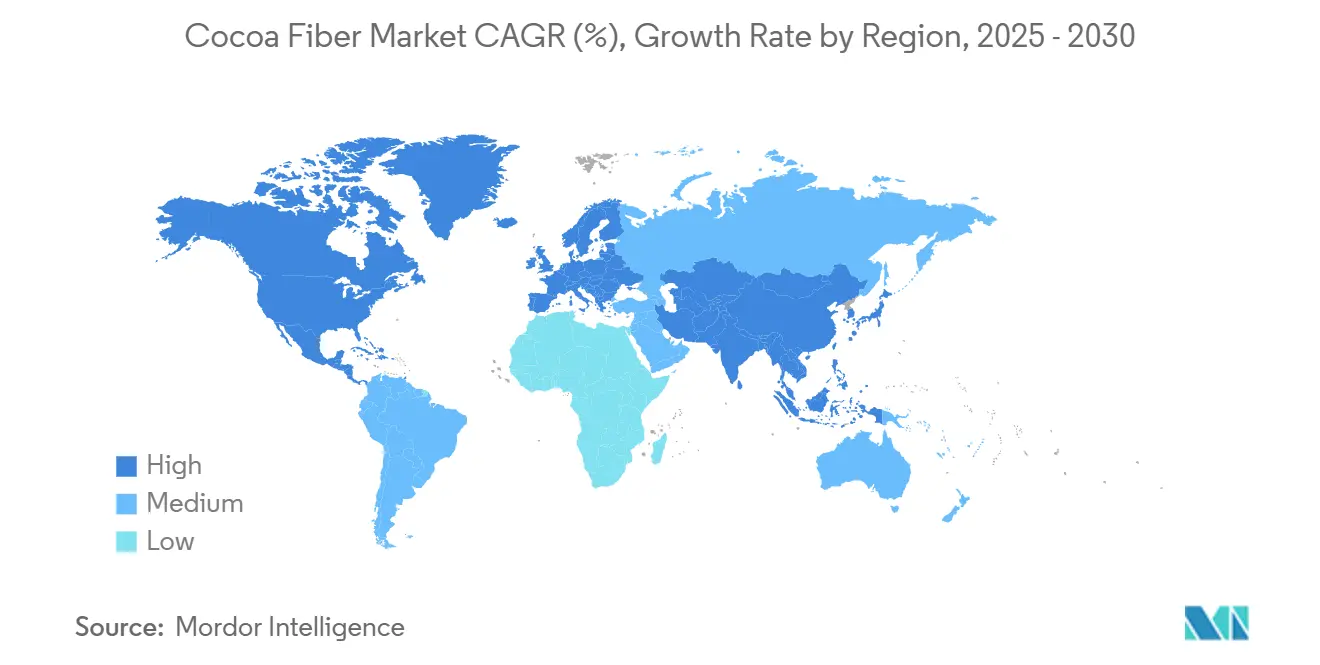

- By geography, Europe led with a 32.12% share in 2024, yet Asia-Pacific is positioned to add the highest incremental value at a 10.02% CAGR to 2030.

Global Cocoa Fiber Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for fiber-enriched bakery and confectionery products | +1.8% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Regulatory backing for dietary-fiber health claims | +1.5% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Escalating upcycling and zero-waste commitments by food and beverage majors | +1.2% | Global, led by multinational corporations | Medium term (2-4 years) |

| Cocoa-price inflation spurring use of cocoa-shell fiber as cost-saving extender | +0.9% | Global, particularly Latin America and West Africa | Short term (≤ 2 years) |

| Clean-label "upcycled ingredient" positioning boosts premium pricing | +0.7% | North America and Europe, premium market segments | Medium term (2-4 years) |

| Prebiotic credentials enabling metabolic-health product launches | +0.6% | Asia-Pacific core, spill-over to North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Fiber-Enriched Bakery and Confectionery Products

Increasing consumer awareness of the health benefits of dietary fiber is influencing the formulation of bakery and confectionery products. Manufacturers are focusing on natural alternatives to synthetic fiber additives to meet evolving consumer preferences. Cocoa shell fiber, derived from the outer shell of cocoa beans, offers both functional fiber content and a natural chocolate flavor. This eliminates the need for additional flavoring agents and aligns with clean-label requirements, which emphasize transparency and the use of minimally processed, natural ingredients. Research indicates that incorporating 6% cocoa shell fiber into wheat bread can increase specific volume by 5% without compromising taste acceptance, enabling the production of fiber-enriched products that retain consumer appeal. The United States Food and Drug Administration (FDA) has recognized the role of dietary fiber in reducing the risk of coronary heart disease, as outlined in regulation 21 CFR 101.77 [1]Source: Code of Federal Regulations, "21 CFR 101.77,” ecfr.gov. This acknowledgment supports health claims on such products, promoting broader adoption in bakery applications. Additionally, as manufacturers aim to reduce sugar content while maintaining flavor, cocoa shell fiber provides a practical solution that addresses both nutritional and flavor requirements.

Regulatory Backing for Dietary-Fiber Health Claims

Government agencies globally recognize the health benefits of dietary fiber and have established regulatory frameworks to support the use of cocoa shell fiber. The United States Food and Drug Administration (FDA)'s 2024 qualified health claim for cocoa flavanols in high-flavanol cocoa powder provides a scientific basis for incorporating cocoa-derived ingredients into health-related applications [2]Source: Food and Drug Administration, "FDA Announces Qualified Health Claim for Cocoa Flavanols in High Flavanol Cocoa Powder and Reduced Risk of Cardiovascular Disease", fda.gov. Similarly, the European Food Safety Authority (EFSA)'s evaluation of cellulose food additives under the E 460-469 classifications confirms the safety of cocoa shell fiber at current usage levels, with recommended daily exposure limits of 660-900 milligrams per kilogram (mg/kg) of body weight. In Canada, the Canadian Food Inspection Agency (CFIA)'s guidelines on prebiotic claims mandate scientific evidence to substantiate health benefits while allowing the classification of non-digestible carbohydrates as fiber. These regulatory measures promote market growth by establishing clear protocols for health claims and effective consumer communication.

Escalating Upcycling and Zero-Waste Commitments by Food and Beverage Majors

Leading food and beverage companies are increasingly adopting circular economy principles to achieve sustainability goals and address evolving consumer expectations, thereby driving the demand for upcycled ingredients such as cocoa shell fiber. Nestlé and Cargill's Cocoa Income Accelerator Program, which aims to enhance the livelihoods of 160,000 farming families by 2030, also targets a 50% reduction in greenhouse gas (GHG) emissions as part of its broader sustainability objectives. Similarly, Olam Food Ingredients (ofi) plans to implement sustainable agricultural practices across more than 1 million hectares by 2030, incorporating the utilization of cocoa byproducts into their comprehensive sustainability strategy. According to the World Resources Institute (WRI), approximately 75% of cacao pods are discarded, presenting significant opportunities to reduce waste by converting these byproducts into functional ingredients such as dietary fiber. Research conducted by ETH Zurich demonstrates that using all components of the cocoa fruit, including the shells, not only increases fiber content but also reduces saturated fat levels in chocolate production. These advancements are driving the growing market demand for cocoa shell fiber as companies work to achieve sustainability targets and enhance supply chain efficiency.

Cocoa-Price Inflation Spurring Use of Cocoa-Shell Fiber as Cost-Saving Extender

The sharp rise in cocoa prices, increasing by 131% in the fiscal year 2023/24 as reported by Barry Callebaut, a leading manufacturer of high-quality chocolate and cocoa products, has prompted manufacturers to explore cost-effective alternatives and extenders to manage production costs. Cocoa shell fiber, derived from the outer shell of cocoa beans, serves as both a functional ingredient and a partial cocoa substitute. It offers chocolate flavor characteristics while reducing the reliance on cocoa solids, thereby helping manufacturers mitigate the impact of rising raw material costs. Research conducted at Abertay University has developed "koji flour," a fermented flour made using Aspergillus oryzae (a type of fungus), which can lower cocoa usage by up to 30% while maintaining flavor profiles and reducing carbon emissions by 98%. Advanced processing techniques have further enabled cocoa shell fiber to act as a natural colorant and flavor enhancer, making it particularly advantageous during periods of elevated cocoa costs in chocolate and confectionery production. These economic pressures have accelerated the adoption of cocoa alternatives as manufacturers aim to reduce costs while upholding product quality and ensuring consumer satisfaction.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited food-grade supply chain and quality variability | -1.4% | Global, particularly developing cocoa regions | Medium term (2-4 years) |

| Heavy-metal (cadmium) compliance challenges | -1.1% | Europe and North America, strict regulatory markets | Long term (≥ 4 years) |

| Bitter taste/dark colour limiting inclusion rates in light-coloured foods | -0.8% | Global, affecting premium food segments | Short term (≤ 2 years) |

| Rising competition from alternative upcycled fibers (coffee, fruit) | -0.6% | North America and Europe, competitive markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Food-Grade Supply Chain and Quality Variability

The cocoa fiber market faces supply chain constraints due to inadequate food-grade processing infrastructure and varying quality standards across cocoa-producing regions. Cocoa shell processing requires specialized equipment and quality control systems to ensure food safety and consistent nutritional profiles, which creates barriers to market expansion. Cocoa shells contain harmful components, including mycotoxins, heavy metals, and polycyclic aromatic hydrocarbons, requiring advanced decontamination technologies such as high voltage electrical discharge (HVED) to meet food-grade standards. The absence of standardized processing protocols across cocoa origins leads to variations in fiber content, particle size distribution, and bioactive compound concentrations, affecting formulation consistency for food manufacturers. A study of Ghana's cocoa processing indicates that only 50% of available processing capacity is utilized due to supply constraints and operational challenges, demonstrating infrastructure limitations in byproduct processing, according to the Netherlands Enterprise Agency[3]Source: Netherlands Enterprise Agency, "Cocoa Processing Study Final report", rvo.nl. These supply chain inefficiencies increase costs and restrict scalability, particularly for smaller manufacturers seeking consistent cocoa shell fiber supplies.

Rising Competition from Alternative Upcycled Fibers (Coffee, Fruit)

The market for upcycled ingredients faces increased competition from alternative fiber sources, primarily coffee silverskin and fruit byproducts. Coffee silverskin, which constitutes 4.2% of coffee bean weight, contains 60% total dietary fiber, including 14% soluble fiber, and exhibits significant antioxidant activity from Maillard reaction products. Studies show that coffee silverskin promotes beneficial bifidobacteria growth, demonstrating its prebiotic properties and competing directly with cocoa shell fiber in functional food applications. Fruit byproducts from apple, citrus, and berry processing present neutral flavor profiles and contain various bioactive compounds. These characteristics attract manufacturers seeking fiber ingredients without flavor limitations. The coffee industry's global supply chain and processing infrastructure enable efficient scaling of alternative fiber production, while fruit byproducts utilize existing seasonal availability and regional processing networks. This competitive environment affects cocoa shell fiber pricing and market positioning. To maintain market share against these emerging alternatives, cocoa shell fiber producers must emphasize their product's distinct functional properties, regulatory approvals, and specific application benefits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form: Powder Dominance Drives Processing Innovation

Powder form holds 60.50% market share in 2024, supported by established processing infrastructure and compatibility across food, nutraceutical, and personal care formulations. The powder segment's prominence stems from manufacturers' preference for standardized particle size distribution and consistent flowability characteristics required for automated production systems. The segment maintains the highest growth rate at 9.50% CAGR through 2030, supported by advancements in micronization technology and surface modification techniques that improve functional properties.

Granules fulfill specialized applications that require controlled release or texture modification, specifically in breakfast cereals and snack products, where distinct fiber particles deliver sensory benefits. Liquid extracts are used in beverage and dairy formulations, utilizing water-soluble bioactive compounds while avoiding particle suspension issues. Micronized flour, an emerging category, focuses on integration into fine-textured applications, with research showing particle sizes under 30 μm achieve optimal dispersion. Processing methods, including planetary ball milling and cavitational extraction, enable specific particle size profiles that enhance functional performance across applications.

By Fiber Type: Mixed Blends Emerge as Growth Leaders

Soluble dietary fiber accounts for 56.78% of the market share in 2024, due to its proven health benefits, including cholesterol reduction and glycemic control. This segment's growth stems from robust research validation and established regulatory pathways for health claims under FDA and EFSA guidelines. Insoluble dietary fiber maintains its position in bulk-forming applications and provides cost-effective fiber fortification in bakery and confectionery products.

Mixed fiber blends are growing at 9.02% CAGR, as manufacturers seek customized fiber profiles that combine functional benefits with sensory acceptance. These formulations combine cocoa shell's insoluble fiber matrix with soluble components, such as inulin or oligosaccharides, to enhance prebiotic activity and digestive tolerance. Studies show that mixed fiber formulations achieve higher glucose adsorption capacity and α-amylase inhibitory activity compared to single-fiber alternatives. The increasing focus on personalized nutrition drives the demand for specialized fiber blends that target specific health outcomes while maintaining product quality.

By Application: Personal Care Accelerates Beyond Food

Bakery and confectionery applications hold a dominant 39.49% market share in 2024, utilizing cocoa shell fiber's natural chocolate flavor and functional properties in baked goods. Research validates successful incorporation rates of up to 8% in bread products and 30% in cookie formulations without affecting sensory qualities. The beverage segment shows growth potential, particularly in functional drinks that target health-conscious consumers seeking natural fiber sources with flavor benefits.

The personal care and cosmetics segment exhibits the highest growth rate at 9.84% CAGR, driven by cocoa shell fiber's antioxidant properties in beauty formulations. The industry's increasing focus on natural and upcycled ingredients creates demand for cocoa shell fiber in anti-aging and skin health products, supported by research showing high phenolic compound content and sun protection properties. Nutraceuticals and dietary supplements utilize the fiber's prebiotic properties and metabolic health benefits, while animal feed applications incorporate it for nutritional enhancement, considering theobromine content limits. In dairy and frozen desserts, cocoa shell fiber serves as a texture modifier and natural chocolate flavor enhancer, supporting clean-label formulations.

Geography Analysis

Europe holds 32.12% market share in 2024, supported by comprehensive EFSA regulations and widespread consumer acceptance of functional ingredients. The region's strong position stems from advanced food processing capabilities and established applications across bakery, confectionery, and personal care segments. European manufacturers leverage their proximity to major cocoa processing facilities and maintain strong supply relationships with West African cocoa producers. The EU's Novel Food Regulation 2015/2283 facilitates cocoa-derived ingredients' market entry, with cocoa extracts already authorized in the Union list. However, EU Regulation 488/2014's strict cadmium limits present compliance challenges for cocoa shell fiber applications.

Asia-Pacific demonstrates the highest growth rate with a 10.02% CAGR through 2030, driven by food processing industry expansion and increasing consumer health awareness. Growth factors include rising middle-class populations seeking functional foods and government food security initiatives promoting alternative nutrition sources. India and Indonesia show substantial demand for cocoa powder and derivatives, creating opportunities as processing capacity grows. The region's competitive manufacturing costs and developing regulatory frameworks support functional ingredient adoption, while increasing dietary fiber awareness drives market growth across food categories.

North America holds a stable market position, supported by clear regulatory pathways established by the United States Food and Drug Administration and steady demand for clean-label ingredients. The region leverages advanced food technology capabilities and well-established cocoa supply chains from Latin America. The United States Food and Drug Administration's recognition of dietary fiber health benefits under Title 21 of the Code of Federal Regulations (21 CFR 101.77) contributes to market growth, while the "Closer to Zero" initiative aimed at reducing heavy metals in food impacts the applications of cocoa shell fiber. South America and the Middle East and Africa exhibit significant growth potential driven by advancements in local cocoa processing and increasing food fortification requirements. This is exemplified by Nigeria's cocoa processing expansion through Johnvents Group's investment of USD 40.5 million in a new facility.

Competitive Landscape

The cocoa fiber market shows moderate concentration, with established cocoa processors maintaining advantages through existing infrastructure, while specialized ingredient companies develop innovative extraction technologies and applications. Players like Custom Fiber and Healy Group utilize integrated supply chains from cocoa bean procurement to processing, enabling efficient byproduct utilization and quality control.

The market's concentration stems from the high costs of food-grade processing infrastructure and regulatory compliance, including cadmium testing and mitigation requirements. Competition centers on technological differentiation and specific applications rather than price-based strategies. Companies actively pursue patents for processing methods, including cavitational extraction, microencapsulation, and fiber modification techniques. The personal care segment presents growth opportunities, where cocoa shell fiber's antioxidant properties and sustainability aspects create premium market segments with higher margins than traditional food applications.

New market entrants focus on specialized extraction methods and direct farmer relationships, while established companies maintain their position through scale advantages and regulatory compliance expertise. The market reflects increasing emphasis on sustainability and circular economy principles, with companies positioning cocoa shell fiber within comprehensive waste reduction and value creation strategies.

Cocoa Fiber Industry Leaders

-

Greenfield Natural Ingredients

-

Custom Fiber

-

Healy Group

-

The Ingredients Expert

-

Touton S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Johnvents Group partnered with British International Investment (BII) to invest USD 40.5 million in Nigeria's cocoa sector, expanding the Premium Cocoa Products facility capacity from 13,000 to 30,000 metric tonnes per year. The investment supports Johnvents' goal of achieving 100% traceable cocoa by 2027 and creates significant opportunities for cocoa shell fiber production as processing capacity doubles in West Africa's emerging cocoa processing hub.

- December 2024: OFI (Olam Food Ingredients), in collaboration with LOTTE, Fuji Oil Co., and MC Agri Alliance, launched its first cocoa biochar pilot project in Dankwa County, Central Province of Ghana. The project involved converting discarded cocoa pod husks into biochar using biochar cone machines, aiming to lock carbon in the soil to reduce the carbon footprint and improve soil health on cocoa farms.

Global Cocoa Fiber Market Report Scope

| Powder |

| Granules |

| Liquid Extract |

| Micronized Flour |

| Insoluble Dietary Fiber |

| Soluble Dietary Fiber |

| Mixed Fiber Blends |

| Bakery and Confectionery |

| Beverages |

| Dairy and Frozen Desserts |

| Nutraceuticals and Dietary Supplements |

| Animal Feed |

| Personal Care and Cosmetics |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Netherlands | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Product Form | Powder | |

| Granules | ||

| Liquid Extract | ||

| Micronized Flour | ||

| By Fiber Type | Insoluble Dietary Fiber | |

| Soluble Dietary Fiber | ||

| Mixed Fiber Blends | ||

| By Application | Bakery and Confectionery | |

| Beverages | ||

| Dairy and Frozen Desserts | ||

| Nutraceuticals and Dietary Supplements | ||

| Animal Feed | ||

| Personal Care and Cosmetics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Netherlands | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast revenue for cocoa fiber by 2030?

The cocoa shell market is projected to reach USD 740.89 million in 2030, reflecting an 8.02% CAGR during 2025-2030.

Which product form dominates global demand?

Powder form leads with 60.50% share in 2024 due to processing versatility and is seen growing at a 9.50% CAGR.

Which region is expanding the fastest?

Asia Pacific is forecast to record a 10.02% CAGR through 2030.

Which application segment is growing quickest?

Personal care and cosmetics leads growth at 9.84% CAGR as brands tap antioxidant and exfoliating properties.

Page last updated on: