Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 59.57 Billion |

| Market Size (2031) | USD 74.67 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Industrial Chocolate Market Analysis by Mordor Intelligence

The industrial chocolate market was valued at USD 57.88 billion in 2025 and is estimated to grow from USD 59.57 billion in 2026 to reach USD 74.67 billion by 2031, registering a compound annual growth rate (CAGR) of 4.62% during 2026-2031. The global industrial chocolate market is experiencing growth driven by increasing demand from large-scale food manufacturers that use chocolate as a primary ingredient in bakery, confectionery, dairy products, and ready-to-eat desserts. Urbanization and rising disposable incomes have led to higher consumption of packaged sweets and indulgent snacks. According to the World Bank Group, the urban population as a percentage of the total population was 58% in 2024[1]Source: The World Bank Group, "Urban population (% of total population)," data.worldbank.org. Product innovations, including premium, single-origin, organic, and reduced-sugar formulations, are further encouraging adoption by various brands. Moreover, the expansion of cafés, quick-service restaurants, and artisanal dessert chains has increased bulk chocolate procurement. According to the International Franchise Association, in 2024, 199,931 quick-service restaurant franchise establishments in the United States[2]Source: International Franchise Association, "Franchising Economic Outlook -2025," franchise.org. Seasonal gifting traditions and the growth of e-commerce distribution channels are also contributing to the rising demand for industrial chocolate production and supply.

Key Report Takeaways

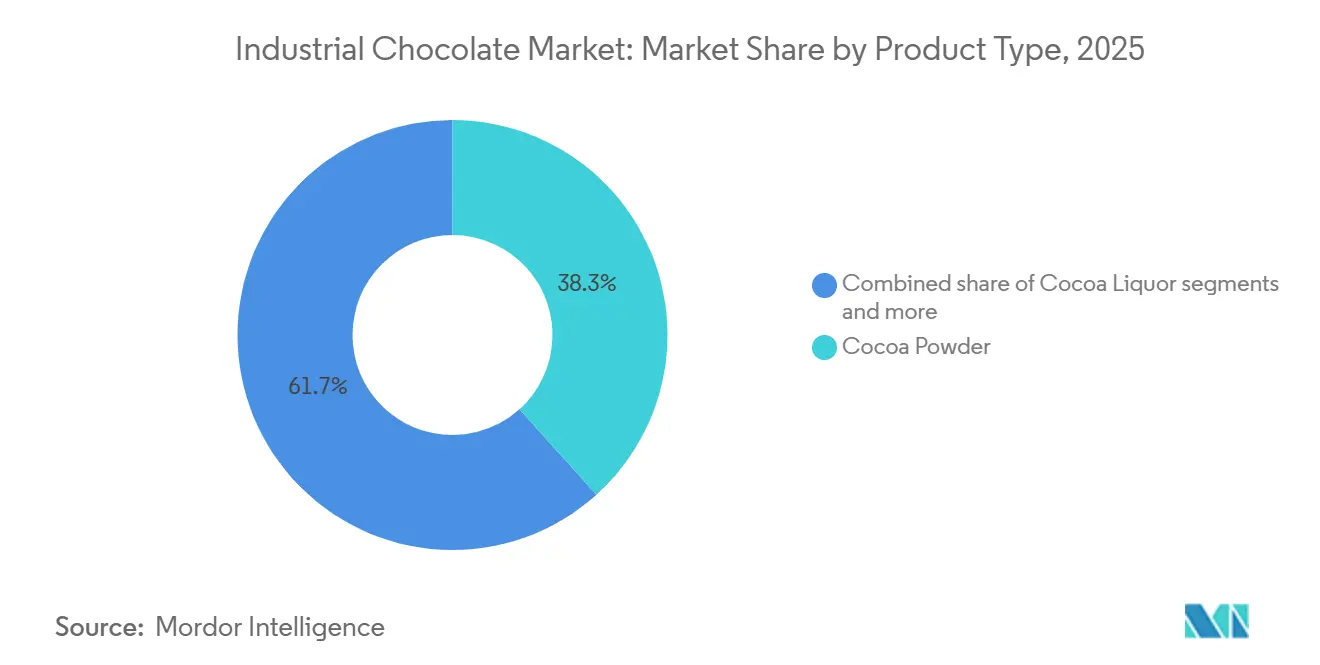

- By product type, cocoa powder led with 38.33% of the industrial chocolate market share in 2025, while compound chocolate is projected to rise at a 6.35% CAGR during 2026-2031.

- By cocoa content, medium-cocoa variants held 46.13% share in 2025; high-cocoa products are forecast to expand at a 6.24% CAGR through 2031.

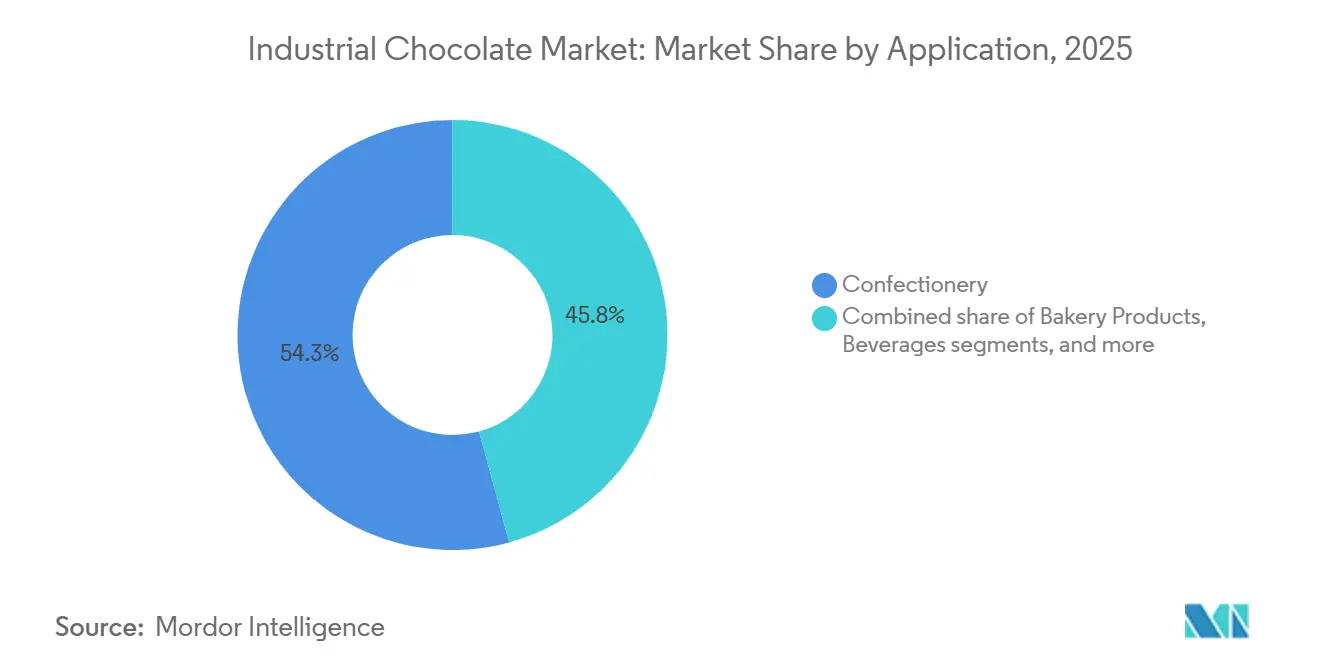

- By application, confectionery captured 54.25% of 2025 revenue, and frozen desserts and ice creams are on track for a 6.91% CAGR to 2031.

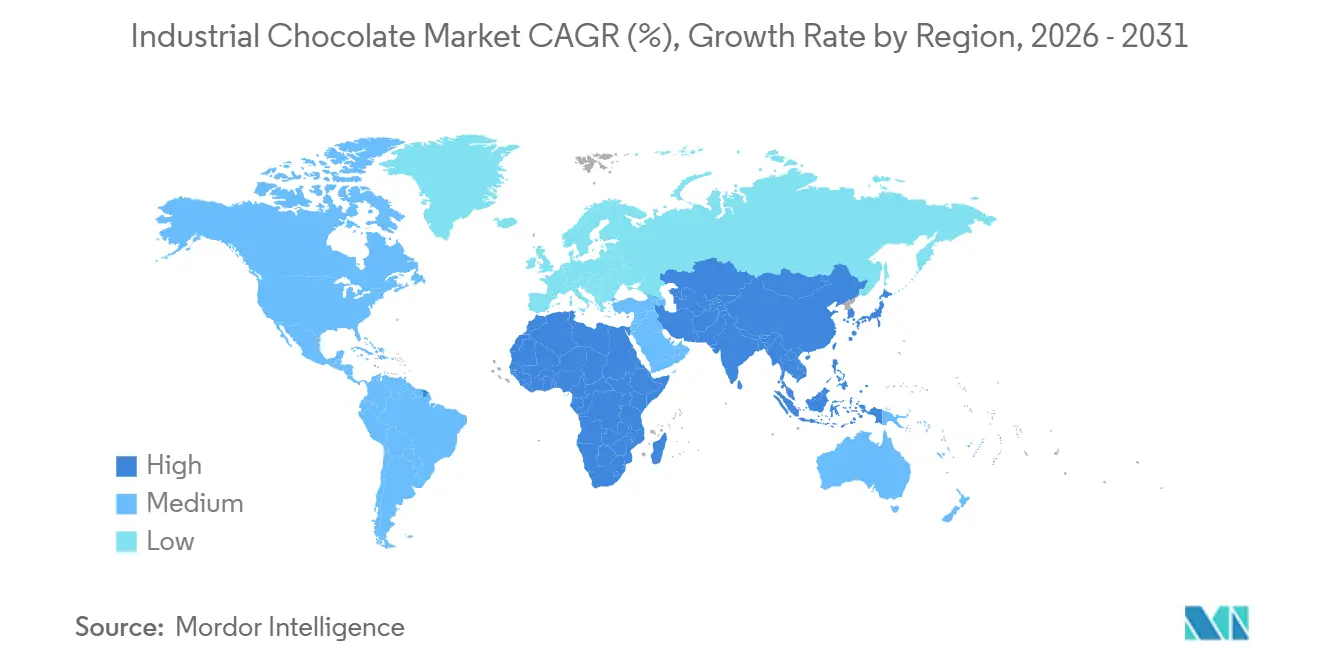

- By geography, Europe accounted for 34.05% of the 2025 value, whereas Asia-Pacific is expected to grow at a 6.58% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Industrial Chocolate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding bakery, confectionery, dairy, dessert, and ice-cream sectors increasing demand for multi-use chocolate ingredients | +1.2% | Global, with pronounced growth in Asia-Pacific and Middle East | Medium term (2-4 years) |

| Growing preference for premium, artisanal, single-origin, and bean-to-bar chocolates | +0.9% | North America, Europe, urban Asia-Pacific hubs | Long term (≥ 4 years) |

| Rising demand for dark, low-sugar, sugar-free, and functional chocolates due to health benefits | +0.8% | North America, Europe, Australia | Medium term (2-4 years) |

| Advancements in processing technologies improving quality, efficiency, and specialized formulations | +0.6% | Global, led by Europe and North America | Short term (≤ 2 years) |

| Increasing adoption of organic ingredients, natural sweeteners, and clean-label formulations | +0.7% | North America, Europe, Australia | Medium term (2-4 years) |

| Stringent food safety, labeling, and sustainability regulations driving certified production practices | +0.5% | Europe (EFSA), North America (FDA), spreading to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding bakery, confectionery, dairy, dessert, and ice-cream sectors increasing demand for multi-use chocolate ingredients

The expansion of the bakery, confectionery, dairy, dessert, and ice cream industries is driving increased demand for versatile chocolate ingredients in bulk production. Food manufacturers are utilizing industrial chocolate in various forms, including chips, compounds, coatings, fillings, and cocoa powders, to produce a diverse range of products such as cakes, cookies, pastries, flavored milk, frozen desserts, and premium sweets. With growing consumer interest in indulgent and innovative flavors, producers are consistently introducing chocolate-based variations, necessitating a reliable and scalable supply of ingredients. This broad applicability positions industrial chocolate as a critical raw material for large-scale food processing, contributing to the global growth of the market.

Growing preference for premium, artisanal, single-origin, and bean-to-bar chocolates

The growing consumer preference for premium, artisanal, single-origin, and bean-to-bar chocolates is a significant driver of the global industrial chocolate market. Consumers increasingly value chocolate for its quality, authenticity, and sensory appeal rather than solely for its affordability. This trend has prompted brands to incorporate higher-grade cocoa, unique flavor profiles, and traceable sourcing into their products. To address these evolving preferences, confectionery and bakery manufacturers source specialized couverture, high-cocoa-content masses, and origin-specific ingredients from industrial suppliers that ensure consistent taste and standardized processing at scale. Even mass-market companies are enhancing their product lines with premium offerings, limited editions, and cleaner labels, thereby increasing the demand for high-quality bulk chocolate inputs and contributing to overall market growth.

Rising demand for dark, low-sugar, sugar-free, and functional chocolates due to health benefits

The growing demand for dark, low-sugar, sugar-free, and functional chocolates is driving significant growth in the global industrial chocolate market. Health-conscious consumers are increasingly seeking indulgent foods that align with wellness objectives, such as reduced sugar intake, higher antioxidant levels, and improved metabolic health. This trend is prompting food manufacturers to reformulate products with higher cocoa content, alternative sweeteners, and functional ingredients like fiber, protein, or probiotics, thereby increasing the demand for specialized bulk chocolate formulations. Industry data highlights this shift, according to Barry Callebaut's "Top Chocolate Trends 2024," 77% of consumers prefer milk chocolate with more cocoa and less sugar, 41% aim to reduce sugar consumption, and 15% are avoiding sugar entirely[3]Source: Barry Callebaut, "Top Chocolate Trends 2024," barry-callebaut.com. Consequently, industrial suppliers are broadening their portfolios to include high-cocoa, no-added-sugar, and functional chocolate bases, supporting large-scale production and driving overall market growth.

Increasing adoption of organic ingredients, natural sweeteners, and clean-label formulations

The increasing use of organic ingredients, natural sweeteners, and clean-label formulations is driving the growth of the global industrial chocolate market. Consumers are showing a preference for products made with identifiable and minimally processed ingredients, leading food brands to replace artificial additives, refined sugars, and synthetic flavors with organic cocoa, plant-based sweeteners like stevia or coconut sugar, and natural emulsifiers. To align with these preferences while ensuring taste, texture, and shelf stability, manufacturers rely on specialized industrial chocolate that adheres to certification standards and delivers consistent processing performance. This emphasis on transparency and ingredient traceability is boosting the large-scale procurement of certified and clean-label chocolate inputs, thereby increasing demand across confectionery, bakery, and dairy applications globally.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cocoa supply volatility | -0.8% | Global, most acute in Europe and North America dependent on West African imports | Short term (≤ 2 years) |

| Rise of plant-based, low-sugar substitutes, and non-chocolate snacks | -0.4% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Trade barriers, export restrictions from cocoa-origin countries | -0.3% | Europe, North America, Asia-Pacific importers | Medium term (2-4 years) |

| Quality consistency challenges | -0.2% | Global, particularly affecting mid-tier processors | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cocoa supply volatility

Cocoa supply volatility significantly restrains the global industrial chocolate market, as chocolate production relies heavily on the stable availability and pricing of cocoa beans. Factors such as weather irregularities, including unpredictable rainfall patterns and temperature fluctuations, can severely impact cocoa yields. Crop diseases like black pod and frosty pod rot further reduce harvest volumes, while aging plantations with declining productivity exacerbate supply challenges. Geopolitical issues in major cocoa-producing regions, such as trade restrictions, political instability, and labor disputes, also contribute to supply disruptions. These factors collectively lead to sharp price fluctuations, raising procurement costs for manufacturers and complicating long-term pricing agreements. Companies are often forced to either absorb reduced margins or pass higher costs to customers, impacting profitability. Additionally, the uncertainty hinders production planning for large-scale food processors that depend on a consistent supply of ingredients, thereby slowing market growth and limiting predictable expansion.

Rise of Plant-Based, Low-Sugar Substitutes, and Non-Chocolate Snacks

The increasing popularity of plant-based alternatives, reduced-sugar substitutes, and non-chocolate snack options is constraining the growth of the global industrial chocolate market by shifting consumer preferences toward perceived healthier or more varied indulgence options. Consumers are increasingly substituting traditional chocolate products with fruit-based snacks, nut bars, protein treats, and cocoa-free confectionery made from ingredients like carob to reduce sugar consumption or avoid allergens and dairy. This trend is prompting food manufacturers to diversify their product formulations, moving away from chocolate-centric recipes, which in turn reduces the bulk demand for cocoa-derived ingredients. As retail shelves accommodate a growing range of functional and alternative snack categories, the resulting competitive pressure limits volume growth for industrial chocolate suppliers, thereby slowing the overall market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Compound Chocolate Gains as Butter Costs Soar

Cocoa powder held 38.33% of the market value in 2025, driven by its versatile applications in bakery, beverages, dairy products, and ready-to-eat desserts. Manufacturers favor cocoa powder for its ability to deliver a strong chocolate flavor with low fat content. Its ease of mixing, extended shelf life, and compatibility with products such as drink premixes, biscuits, cakes, and breakfast cereals make it a cost-effective flavoring option for large-scale production. Additionally, the rising demand for chocolate-flavored health drinks, protein-based products, and reduced-fat formulations enhances its usage, as cocoa powder offers intense flavor while enabling brands to manage calorie content and maintain texture consistency.

Compound chocolate is the fastest-growing product type at 6.35% CAGR through 2031, due to its cost-effectiveness, ease of processing, and reliable performance in large-scale food production. Unlike pure chocolate, compound chocolate utilizes vegetable fats instead of cocoa butter, removing the need for complex tempering processes. This enables faster production of coatings, enrobing, fillings, and decorations in bakery and confectionery applications. Its superior heat resistance and consistent structure make it particularly suitable for warm climates and extended distribution chains. These attributes have led manufacturers to increasingly use compound chocolate in products such as biscuits, wafers, ice cream coatings, and snack bars, driving significant global volume growth.

By Cocoa Content: High-Cocoa Formulations Capture Health Halo

Medium-cocoa commanded 46.13% of the 2025 market share, supported by its balanced taste profile, which combines a distinct chocolate flavor with mild sweetness. This makes it well-suited for mass-market applications such as bakery products, biscuits, molded confectionery, and flavored dairy items. Manufacturers favor this type of chocolate due to its broad consumer appeal, particularly in everyday snacks and affordable treats, while still providing a recognizable chocolate experience. Its versatility in applications such as fillings, chips, and coatings enables producers to maintain consistent flavor across extensive product portfolios, supporting steady bulk purchases from industrial suppliers.

High-cocoa variants are expanding at 6.24% CAGR from 2026-2031 driven by growing consumer interest in intense flavors, premium positioning, and the perceived health benefits associated with higher cocoa content. Food manufacturers are incorporating it into dark chocolate bars, gourmet desserts, premium ice creams, and reduced-sugar formulations to differentiate their products and justify premium pricing. The growth of artisanal and high-quality product lines, coupled with the demand for antioxidant-rich indulgent offerings, is encouraging manufacturers to procure high-cocoa ingredients in significant volumes, thereby contributing to the growth of this segment within the industrial chocolate market.

By Application: Frozen Desserts Outpace Traditional Confectionery

Confectionery applications accounted for 54.25% of the 2025 revenue, encompassing enrobed bars, molded pralines, and seasonal novelties, where chocolate serves as the primary ingredient rather than a complementary flavor. The confectionery segment plays a key role in driving demand within the industrial chocolate market, supported by ongoing innovations in candies, molded chocolates, filled pralines, and seasonal gifting products. Manufacturers depend on substantial quantities of consistent-quality chocolate for applications such as shells, centers, coatings, and inclusions to ensure efficient high-speed production and uniform taste across batches. Factors such as increasing impulse snacking habits, the growth of affordable treats in emerging markets, and frequent limited-edition product launches prompt brands to boost production, resulting in consistent procurement of industrial chocolate ingredients.

Frozen desserts and ice creams represent the fastest-growing application, with a CAGR of 6.91% (2026-2031). The increasing consumption of premium and indulgent frozen desserts is driving the use of industrial chocolate in ice creams and related products. Chocolate is extensively utilized in syrups, coatings, chips, ripples, and cores to enhance texture and flavor complexity, particularly in multi-layered and filled formats. The rising popularity of café-style desserts, novelty frozen snacks, and take-home tubs has encouraged manufacturers to include more chocolate-based inclusions. Additionally, compound coatings with improved melt resistance facilitate large-scale distribution, further fueling demand in this application segment.

Geography Analysis

Europe accounted for 34.05% of the global market value in 2025. The industrial chocolate market in Europe is driven by the region's strong tradition of chocolate consumption and its well-established bakery, confectionery, and premium dessert industries, which require significant volumes of high-quality chocolate ingredients. Consumers demonstrate a strong preference for dark, high-cocoa, organic, and ethically sourced products, prompting manufacturers to procure specialized couverture and certified cocoa on a large scale. Continuous product innovation, such as filled chocolates, seasonal assortments, and gourmet pastries, supports steady industrial demand. Additionally, the growth of café culture and artisanal patisserie chains has increased the use of industrial chocolate in coatings, fillings, and decorations. Furthermore, the expansion of private-label offerings in supermarkets and the popularity of gifting occasions across the region contribute to sustained large-scale production and procurement of industrial chocolate.

Asia-Pacific is a key growth region, projected to achieve a CAGR of 6.58% through 2031, driven by markets such as China, India, and Southeast Asia. The industrial chocolate market in the region is expanding due to rapid urbanization and the increasing westernization of eating habits, which are fostering greater acceptance of chocolate-based snacks, particularly among younger consumers. The growth of organized retail, convenience stores, and online grocery platforms has enhanced product availability, encouraging manufacturers to scale up production using industrial chocolate ingredients. Multinational food brands are investing in local manufacturing facilities to streamline supply chains and adapt flavors to regional preferences, including matcha, red bean, and tropical fruit combinations, thereby boosting bulk ingredient procurement. Furthermore, the rising gifting culture during festivals and the popularity of small portion packs tailored to price-sensitive consumers are contributing to increased manufacturing volumes across the region.

In North America, the industrial chocolate market benefits from strong demand driven by large contract manufacturers and private brands supplying supermarkets, vending channels, and foodservice operators. This demand supports continuous bulk ingredient sourcing. In South America, market growth is supported by the presence of major cocoa-producing countries, which facilitate regional processing, reduce dependence on imports, and encourage local manufacturing of chocolate-based consumer goods. In the Middle East and Africa, market expansion is fueled by the increasing number of hospitality developments, which drive the production of chocolate-containing snacks and desserts designed for on-the-go consumption. Across these regions, manufacturers are investing in automated processing lines and enhanced storage infrastructure, boosting production capacity and streamlining the procurement of industrial chocolate.

Competitive Landscape

The industrial chocolate market is moderately consolidated. Major processors, including Barry Callebaut and Cargill, collectively manage a significant share of global cocoa processing. Leading companies are enhancing control over raw material sourcing through vertical integration and long-term partnerships with farming communities, aiming to improve supply security and ensure compliance with traceability standards. Additionally, they are investing in alternative fat technologies and formulation efficiencies to mitigate cost fluctuations and better serve large-scale bakery and food processing clients.

Mid-sized players, such as Puratos and Kerry Group, compete by offering application-specific solutions, including heat-resistant or performance-enhanced chocolate tailored to specific manufacturing environments. Innovation opportunities are also emerging in the functional chocolate segment, where smaller challenger brands are targeting nutrition-focused consumers with products featuring added bioactive ingredients. In response, large food corporations are increasing research and patent activity to develop nutrient-fortified chocolate that maintains stability during processing.

Smaller premium manufacturers differentiate themselves by sourcing rare cocoa varieties through direct trade, enabling them to achieve higher margins in specialty retail channels. Meanwhile, technology adoption is becoming a critical factor in competition. Market leaders are leveraging advanced quality monitoring tools and digital traceability systems to comply with stringent regulatory and sustainability requirements. In contrast, companies relying on traditional testing and documentation methods face a higher risk of exclusion from regulated supply chains. Certifications related to food safety and sustainable sourcing are now baseline requirements, raising entry barriers for less developed processing regions and intensifying competitive pressures across the industry.

Industrial Chocolate Industry Leaders

-

Fuji Oil Co. Ltd.

-

Cargill

-

Barry Callebaut

-

Puratos

-

Guittard

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Barry Callebaut opened a global innovation hub in Singapore dedicated to advancing chocolate development using artificial intelligence technologies. Located in the Geneo complex within Singapore Science Park, the facility houses two specialized centers of excellence: an AI-driven chocolate and cocoa research unit and a cacao coatings innovation unit. This investment aligns with the company’s strategy to enhance product development capabilities and address challenges posed by recent cocoa price fluctuations and reduced consumer demand.

- August 2025: Barry Callebaut expanded its operations in India by inaugurating its third chocolate production facility in the country. The new greenfield plant, covering approximately 20,000 square meters in the Ghiloth Industrial Area of Neemrana near Delhi, is equipped with advanced production lines capable of manufacturing chocolate and compound products in various formats. It also includes an integrated storage infrastructure. Strategically located to serve clients in North and Central India, the facility aims to enhance distribution efficiency and reduce delivery times in one of the world's fastest-growing chocolate markets.

- March 2024: Cargill expanded its foodservice portfolio by launching chocolate chips, block chocolates, and cocoa powder under the NatureFresh Professional brand, showcased at AAHAR 2024. The company also introduced customized solutions tailored for the Indian bakery and food industry, aligning with its strategy to establish itself as a comprehensive innovation partner for professional manufacturers.

Global Industrial Chocolate Market Report Scope

Industry chocolate is the primary foremost ingredient required for the production of consumable chocolate or desserts which requires the application of varied kinds of chocolate. The global industrial chocolate market (henceforth referred to as the market studied) is segmented by product type, application, and geography. By product type, the market is segmented into Cocoa Powder, Cocoa Liquor, Cocoa Butter, and Compound Chocolate. Based on the application, the market studied is segmented into Bakery Products, Confectionary, Bakery Premixes, Beverages, Frozen Desserts and Ice creams, and Other Applications. Bakery Products are further subdivided into, cakes, biscuits, pastries, and other bakery products. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done based on value (in USD million).

By Product Type

| Cocoa Powder |

| Cocoa Liquor |

| Cocoa Butter |

| Compound Chocolate |

By Cocoa Content

| Low Cocoa |

| Medium Cocoa |

| High Cocoa |

By Application

| Bakery Products |

| Confectionery |

| Bakery Premixes |

| Beverages |

| Frozen Desserts and Ice Creams |

| Other Applications |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| United Arab Emirates | |

| Nigeria | |

| Morocco | |

| Egypt | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Cocoa Powder | |

| Cocoa Liquor | ||

| Cocoa Butter | ||

| Compound Chocolate | ||

| By Cocoa Content | Low Cocoa | |

| Medium Cocoa | ||

| High Cocoa | ||

| By Application | Bakery Products | |

| Confectionery | ||

| Bakery Premixes | ||

| Beverages | ||

| Frozen Desserts and Ice Creams | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| United Arab Emirates | ||

| Nigeria | ||

| Morocco | ||

| Egypt | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will global demand for industrial chocolate be by 2031?

The industrial chocolate market size is projected to reach USD 74.67 billion by 2031, supported by a 4.62% CAGR over 2026-2031.

Which product type is growing fastest?

Compound chocolate is forecast to register the highest growth at a 6.35% CAGR through 2031.

Why is Asia-Pacific attracting most new investment?

China’s rising middle class and India’s capacity expansions underpin a 6.58% regional CAGR, the strongest worldwide.

Who are the market leaders?

Barry Callebaut, Cargill, Puratos, Fuji Oil, and Olam are among the key players in the global industrial chocolate market.

Page last updated on: