Coal Tar Pitch Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.76 Billion |

| Market Size (2031) | USD 5.92 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

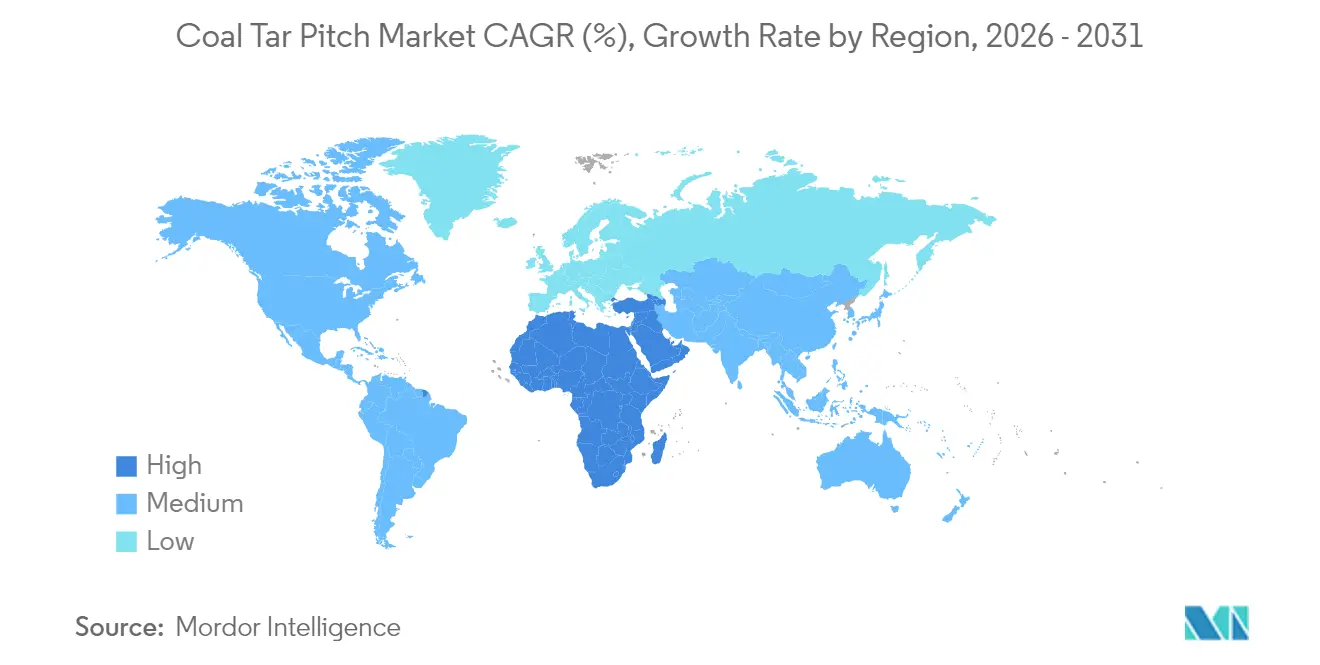

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

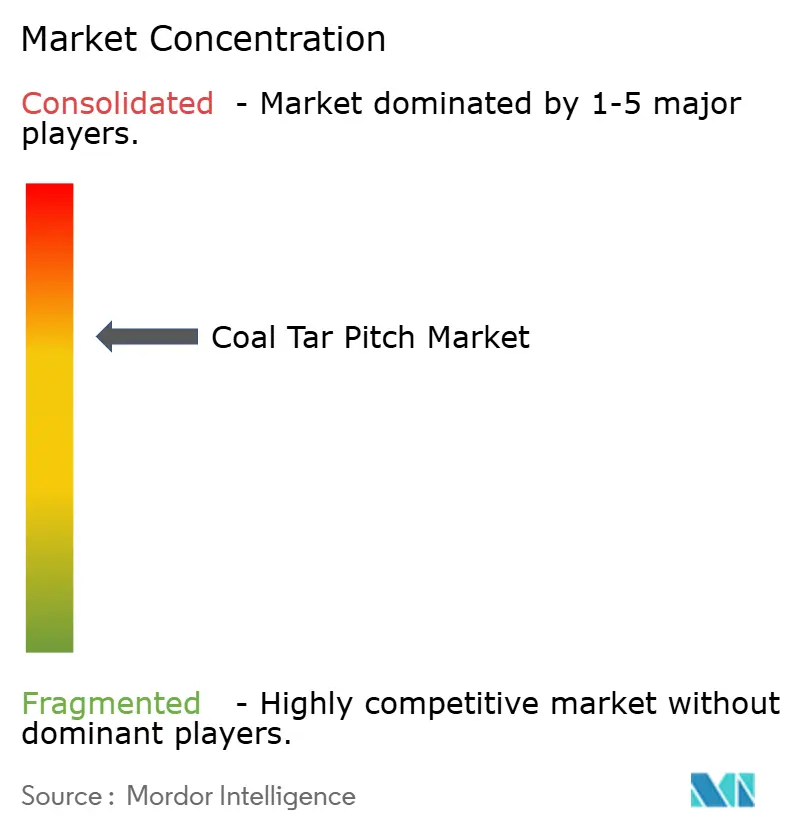

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coal Tar Pitch Market Analysis by Mordor Intelligence

Coal Tar Pitch market size in 2026 is estimated at USD 4.76 billion, growing from 2025 value of USD 4.56 billion with 2031 projections showing USD 5.92 billion, growing at 4.45% CAGR over 2026-2031. Robust aluminum-smelting activity across the Asia-Pacific region anchors demand, while engineered low-PAH grades open up incremental revenue streams in Europe and North America. Price volatility in crude oil, recurring supply tightness due to shrinking coke-oven fleets, and widening regulatory restrictions shape the competitive landscape. Producers that can simultaneously guarantee consistent quality, reduce toxic constituents, and optimize logistics capture outsized value as end-users pivot toward circular and decarbonized production routes. Heightened strategic interest in automotive carbon-fiber applications and graphite-electrode binders further cushions the coal tar pitch market against cyclical softness in legacy roofing and pavement-sealer uses.

Key Report Takeaways

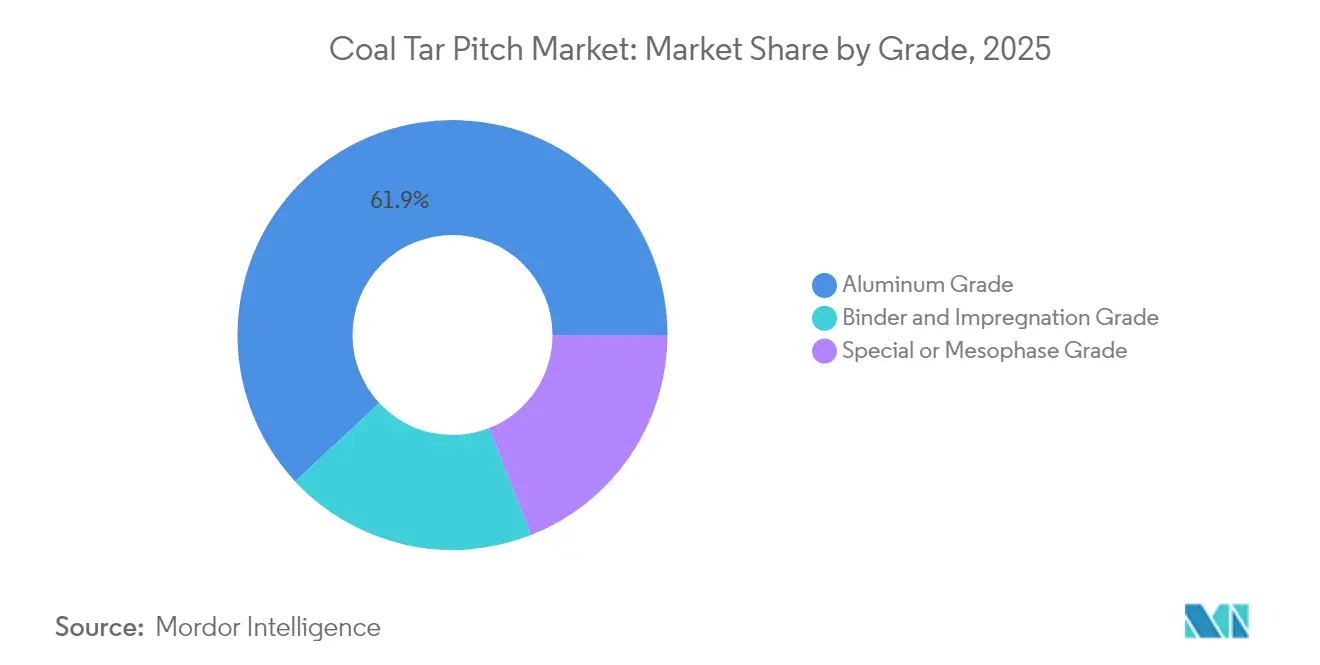

- By grade, Aluminium Grade held 61.92% of the Coal Tar Pitch market share in 2025. The Special/Mesophase Grade is expected to expand at a 5.83% CAGR by 2031, the fastest pace among all grades.

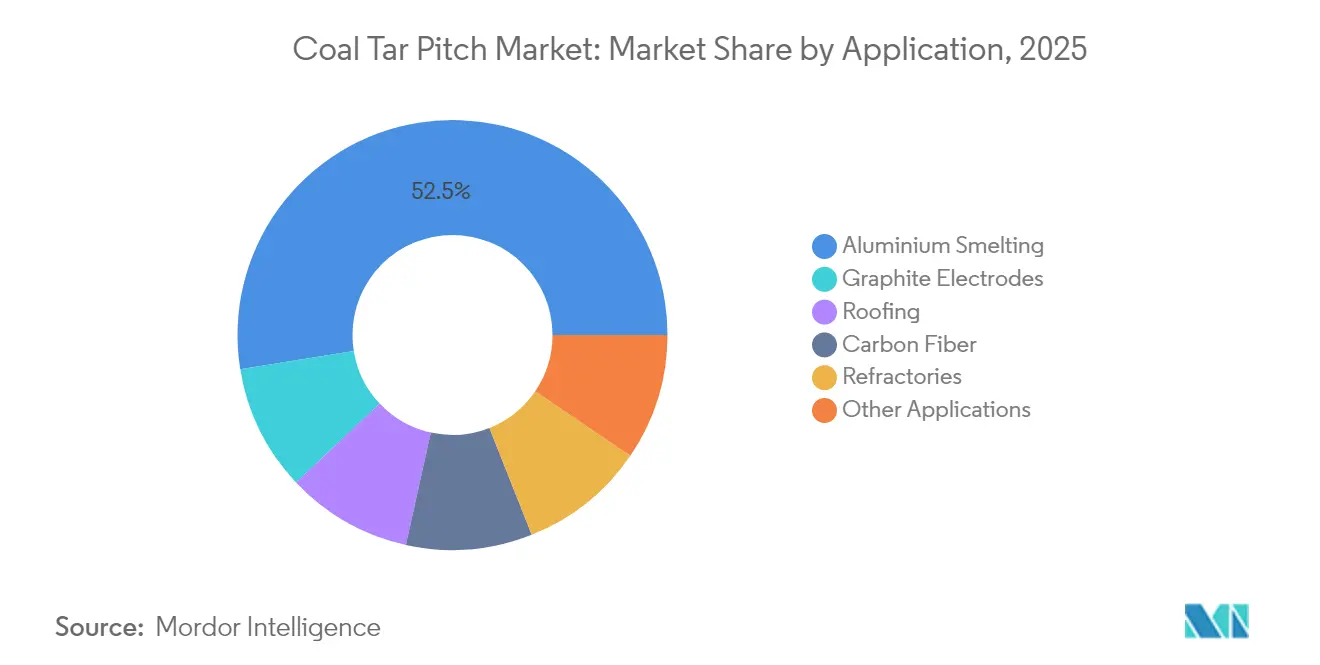

- By application, aluminum smelting contributed 52.54% of the Coal Tar Pitch market size in 2025. Carbon fiber applications are forecast to advance at a 6.11% CAGR between 2026 and 2031, the quickest among all end uses.

- By geography, the Asia-Pacific region accounted for 63.61% of the market share in 2025, while the market share of the Middle East and Africa is poised to grow at the fastest rate, with a share of 5.55% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Coal Tar Pitch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Aluminium-smelter Expansions in China and India | +1.8% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Increasing Adoption of Graphite-electrode EAF Steelmaking | +1.2% | Global, with concentration in APAC and North America | Long term (≥ 4 years) |

| Robust Refractory Brick Output in Asia-Pacific | +0.9% | Asia-Pacific, secondary impact in Europe | Short term (≤ 2 years) |

| Low-PAH engineered Pitch Gaining EU-REACH Approvals | +0.7% | Europe and North America, expanding globally | Medium term (2-4 years) |

| Automotive Push for Pitch-based Carbon-fiber Light-weighting | +0.6% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Aluminium-smelter Expansions in China and India

Chinese and Indian greenfield smelters were responsible for 53.12% of the 2024 global aluminum-sector coal tar pitch offtake, underscoring a supply chain that now revolves around the Asia-Pacific’s industrial corridors. Capacity creep in China persists despite headwinds from energy policy, while India’s state-backed production ramps are reorienting regional trade flows. Himadri Speciality Chemicals leveraged its 70% domestic market share to increase H1 FY25 volumes by 32% to 278,232 MT, confirming the momentum of scale-up[1]Himadri Speciality Chemical, “Q2 FY25 Results,” himadrispeciality.com.

Increasing Adoption of Graphite-electrode EAF Steelmaking

Steelmakers are actively substituting blast furnaces with electric arc furnaces (EAF) to comply with decarbonization mandates. GrafTech’s 13% 2024 sales-volume growth to 103.2 k MT illustrates the resurgence of electrode demand, although non-LTA prices slid 19%. Each electrode requires a high-purity binder to withstand 3,500°C arcs, positioning premium coal tar pitch grades as indispensable inputs. Long project lead times for EAF retrofits signal multi-year runways, fortifying baseline consumption within the coal tar pitch market across both developed and emerging economies.

Robust Refractory Brick Output in Asia-Pacific

Rapid industrialization has elevated Asia-Pacific’s refractory brick shipments, which directly lifts demand for specialized pitch binders that confer thermal shock resistance above 1,600 °C. Rain Industries’ CARBORES platform captures this niche by delivering a similar carbon yield with 90% less toxic content compared to legacy binders[2]Rain Carbon, “CARBORES® Product Sheet,” raincarbon.com. Substitution risk is low because alternative resins exhibit inferior high-temperature cohesion, ensuring refractory manufacturers maintain coal tar pitch sourcing even as environmental scrutiny intensifies.

Low-PAH Engineered Pitch Gaining EU-REACH Approvals

The European Commission’s Regulation (EU) 2025/660 caps 18 PAHs at 50 mg/kg effective April 2026, pressuring legacy grades out of automotive and sporting goods segments. Producers responded by commercializing engineered, ultra-low-PAH (Polycyclic Aromatic Hydrocarbons) formulations at 15–25% price premiums, trading cost for regulatory certainty and market access. Early movers now negotiate multi-year contracts with European graphite-electrode and refractories mills, illustrating how compliance-oriented innovation secures share within the coal tar pitch market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shrinking Coke-oven Fleet in North America and EU Cuts Tar Supply | -1.10% | North America and Europe, secondary impact globally | Medium term (2-4 years) |

| Tightening PAH Exposure and Wastewater Norms Worldwide | -0.80% | Global, most stringent in Europe and North America | Short term (≤ 2 years) |

| Crude-oil Price Swings Undermine Coal-tar Cost Advantage | -0.50% | Global, with higher impact in price-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shrinking Coke-oven Fleet in North America and EU Cuts Tar Supply

Steel decarbonization has shut down multiple coke batteries, reducing tar availability for pitch distillation. Koppers trimmed operations to three facilities and signaled formula-priced contracts to hedge feedstock risk. Supply scarcity elevates spot prices even when end-market demand weakens, compressing margins for downstream electrode and refractory producers within the coal tar pitch market.

Tightening PAH Exposure and Wastewater Norms Worldwide

Canada’s 2025 toxic-substances listing and the New York State ban on high-PAH pavement sealers illustrate an accelerating global clampdown. Compliance retrofits add laboratory and wastewater treatment overheads that smaller distillers struggle to absorb. While this trend curtails legacy roofing volumes, it simultaneously channels investment toward ultralow-PAH alternatives, reconfiguring value pools across the coal tar pitch industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Grade: Aluminum Grade Retains Scale Advantage While Mesophase Unlocks Premium Uses

Aluminium Grade dominated the Coal Tar Pitch market with a 61.92% share of the market size in 2025, driven by smelter expansions that increased carbon-anode demand in China and India. Its entrenched position affords economies of scale, enabling producers to amortize regulatory-compliance capex across large volumes. The grade’s high softening point and consistent QI (quinoline-insoluble) levels make it the default binder for prebake anodes, a specification unlikely to change until inert-anode technology matures post-2031.

The Special/Mesophase Grade segment, although accounting for 19.04% of the 2025 volume, is scaling fastest at a 5.83% CAGR, thanks to its role in automotive and aerospace carbon-fiber composites. Process innovations that lower cost to USD 10/kg under large-batch regimes widen the addressable base for mid-performance parts. Producers leveraging continuous pitch-polymerization reactors can pivot quickly between conventional and mesophase outputs, cushioning revenue in the coal tar pitch market against cyclical smelter downturns.

By Application: Aluminum Smelting Leads, Carbon Fiber Traction Accelerates

Aluminum smelting accounted for 52.54% of the Coal Tar Pitch market share in 2025, translating to a stable long-term offtake anchored to global primary metal output. Contract structures typically span 12–18 months with price formulas referencing coal and aluminum indices, offering predictable cash flow for integrated refiners.

Carbon-fiber applications are projected to capture a 6.11% CAGR through 2031 as electric-vehicle platforms prioritize lightweight battery packs. Early adopters in Japan and Germany are already specifying mesophase-based fabrics for structural panels, making this the key growth engine of the coal tar pitch market throughout the decade. Graphite-electrode binders follow at mid-single-digit growth linked to EAF (Electric Arc Furnace) steel trajectories, while roofing volumes contract under consumer-product PAH bans.

Geography Analysis

The Asia-Pacific region commanded 63.61% of 2025 consumption, reflecting an integrated coke-oven and smelting ecosystem that reduces logistics costs and mitigates tariff exposure. China’s Xinjiang and Inner Mongolia clusters anchor low-cost aluminum output, while India’s eastern corridor smelters accelerate domestic self-sufficiency. These two nations, combined, consumed 70% of global pitch in 2025, a share expected to remain stable through 2031 as new furnaces come online in Odisha and Yunnan provinces.

North America’s demand share is under pressure from smelter rationalization and stricter environmental codes, yet the region’s dense EAF steel build-out sustains electrode-binder volumes. Europe’s slice is bifurcated: legacy volumes erode under PAH curbs, yet engineered low-PAH grades fetch premium pricing in Germany, France, and Scandinavia. The Middle East & Africa emerge as the fastest-growing region, with a 5.55% CAGR, driven by state-backed investments in the UAE (United Arab Emirates) and Saudi Arabia's aluminum clusters. Latin America maintains a small but stable base tied to Brazilian refractory and electrode demand, whereas policy uncertainty delays large-scale smelting upgrades. Across all regions, supply-chain diversification strategies now weigh proximity to compliant coke-oven tar against regulatory risk, prompting multi-sourcing models that reshape trade lanes within the Coal Tar Pitch market.

Competitive Landscape

The Coal Tar Pitch market is moderately consolidated. Strategic levers now revolve around feedstock security, environmental accreditation, and downstream integration into carbon-fiber or anode finishing. Mitsubishi Chemical and Sumitomo Rubber’s 2025 tire-recycling venture demonstrates scope for circular-economy synergies that furnish alternative tar streams. Smaller regional distillers are increasingly adopting toll-processing alliances with steelmakers to secure tar flows, underscoring a shift toward collaborative risk-sharing across the coal tar pitch market.

Coal Tar Pitch Industry Leaders

Rain Carbon Inc.

Himadri Chemicals Speciality Ltd.

Koppers Inc.

Deza, a.s.

JFE Chemical Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: India-based Rain Industries announced the commencement of the first phase of a new coal tar pitch (CTP) facility in the Andhra Pradesh Special Economic Zone, India, scheduled for the second half of 2025. The company anticipates higher CTP demand and improved efficiency by locating distillation capacity near coal tar production.

- July 2023: Epsilon Carbon, an Indian producer of coal tar pitch derivatives, partnered with South32, a global mining and metals company. Epsilon Carbon will supply liquid coal tar pitch to South32's sites in South Africa and Mozambique.

Global Coal Tar Pitch Market Report Scope

Coal tar pitch is a byproduct of the distillation of coal tars obtained from the high-temperature pyrolysis of coal. Coal tar pitch is a hard and brittle substance mainly containing aromatic, resinous compounds and other hydrocarbons and their derivatives. The market is segmented into grade, application, and geography. By grade, the market is segmented into aluminum grade, binder and impregnating grade, and special grade. By application, the market is segmented into aluminum smelting, graphite electrodes, roofing, carbon fiber, refractories, and other applications. The report also covers the market size and forecasts for the coal tar pitch market in 15 countries across major regions. The market sizing and forecasts for each segment have been done based on revenue (USD million).

| Aluminium Grade |

| Binder and Impregnation Grade |

| Special / Mesophase Grade |

| Aluminium Smelting |

| Graphite Electrodes |

| Roofing |

| Carbon Fiber |

| Refractories |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Grade | Aluminium Grade | |

| Binder and Impregnation Grade | ||

| Special / Mesophase Grade | ||

| By Application | Aluminium Smelting | |

| Graphite Electrodes | ||

| Roofing | ||

| Carbon Fiber | ||

| Refractories | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Italy | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the Coal Tar Pitch Market size in 2026?

The Coal Tar Pitch Market size is USD 4.76 billion in 2026.

How fast will demand for Special/Mesophase Grade grow?

Special/Mesophase Grade is projected to register a 5.83% CAGR through 2031 as automotive carbon-fiber adoption rises.

Which application currently dominates usage?

Aluminum smelting leads, accounting for 52.54% of global consumption in 2025.

Why are low-PAH grades gaining traction?

EU REACH limits on PAHs drive end-users to source engineered grades like CARBORES with 90% fewer toxic compounds.

Which region offers the highest growth potential?

Middle East & Africa is forecast to expand at 5.55% CAGR through 2031 on the back of new aluminum clusters.

Page last updated on: