Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

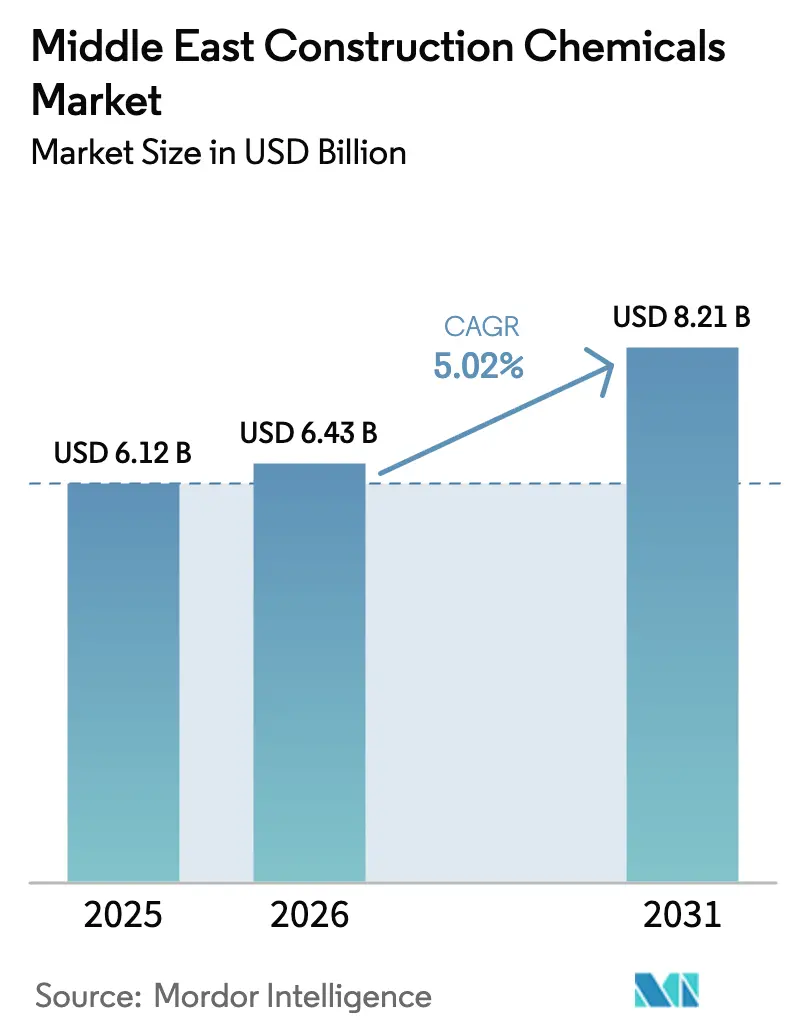

| Base Year Market Size (2025) | USD 6.12 Billion |

| Market Size (2026) | USD 6.43 Billion |

| Market Size (2031) | USD 8.21 Billion |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East Construction Chemicals Market Analysis by Mordor Intelligence

The Middle East Construction Chemicals Market size is expected to increase from USD 6.12 billion in 2025 to USD 6.43 billion in 2026 and reach USD 8.21 billion by 2031, growing at a CAGR of 5.02% over 2026-2031. A strategic pivot from hydrocarbon-centric infrastructure toward diversified, sustainability-focused development is broadening the demand base for high-performance admixtures, low-VOC (Volatile Organic Compound) coatings, and advanced waterproofing solutions. National Vision programs in Saudi Arabia, the United Arab Emirates (UAE), and Qatar are funneling capital into giga-projects that require faster cure times, extreme-temperature tolerance, and longer design lives. Green-building rating systems such as Estidama and GSAS (Global Sustainability Assessment System) elevate specification standards, while hyperscale data centers and desalination plants add technical niches like antistatic flooring and marine-grade coatings. Competitive intensity is rising as global majors localize manufacturing and acquire regional specialists to secure approved-vendor status on giga-tenders.

Key Report Takeaways

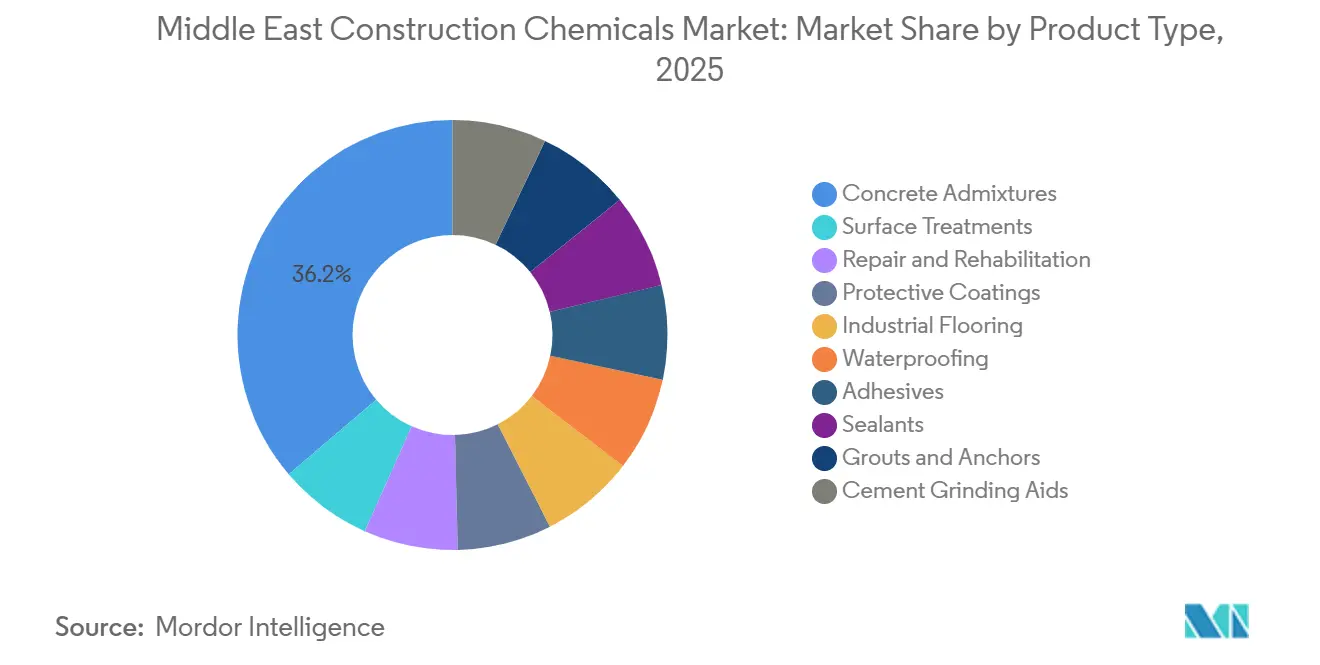

- By product type, concrete admixtures held 36.22% of the Middle East Construction Chemicals market share in 2025, while waterproofing systems recorded the fastest projected growth at a 5.41% CAGR during the forecast period (2026-2031).

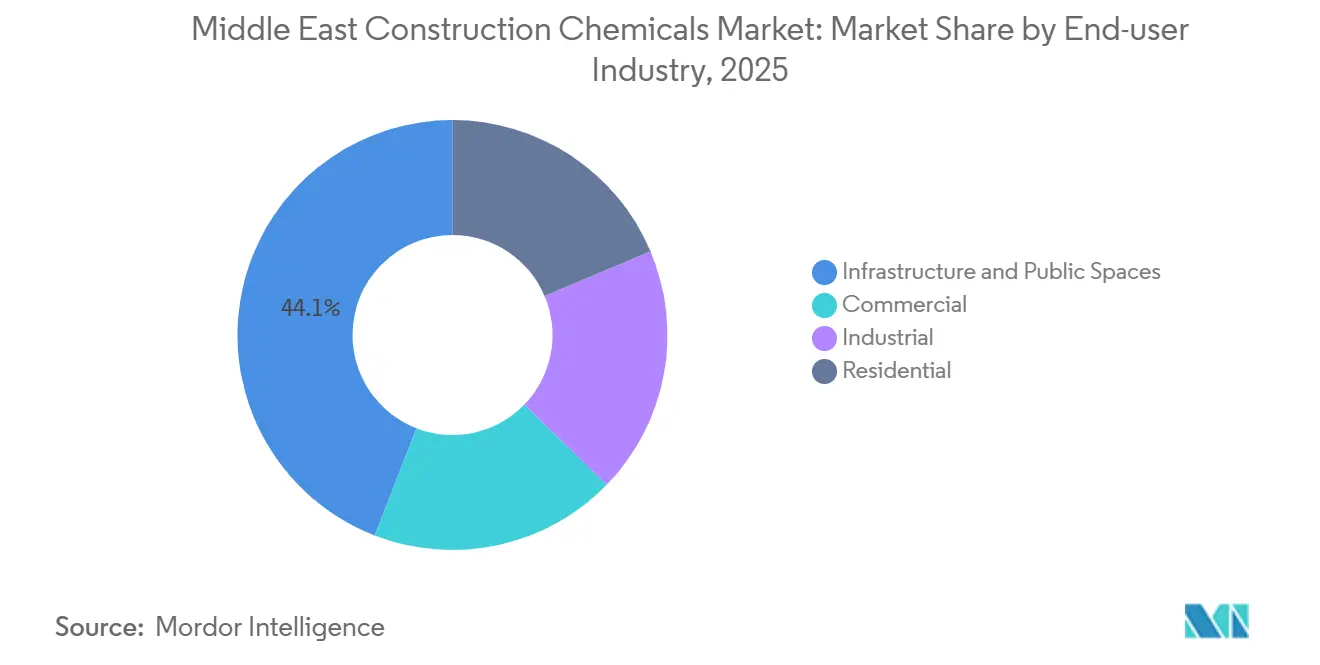

- By end-user industry, infrastructure and public spaces led with 44.12% revenue share in 2025; the residential segment is forecast to expand at a 5.67% CAGR during the forecast period (2026-2031).

- By geography, Saudi Arabia commanded 35.45% of 2025 demand and is advancing at a 5.42% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East Construction Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated infrastructure spending under National Vision programmes | +1.8% | Saudi Arabia, UAE, Qatar (core); spillover to Kuwait, Egypt | Long term (≥ 4 years) |

| Mandated adoption of green-building rating systems (Estidama, GSAS) | +1.2% | UAE (Abu Dhabi), Qatar, expanding to Saudi Arabia | Medium term (2-4 years) |

| Rise of giga-projects requiring specialty, high-performance admixtures | +1.4% | Saudi Arabia (NEOM, Red Sea, Qiddiya), UAE (Expo City) | Long term (≥ 4 years) |

| Rapid expansion of data-center construction needing antistatic flooring | +0.9% | Saudi Arabia, UAE (primary); Qatar (emerging) | Short term (≤ 2 years) |

| Desalination-plant boom driving demand for anti-corrosion coatings | +0.7% | Saudi Arabia, UAE, Kuwait (coastal zones) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Infrastructure Spending Under National Vision Programs

Public funding shifts are steering demand from commodity products to engineered systems with accelerated cure and extreme-temperature performance. Saudi Arabia’s Public Investment Fund earmarked USD 40 billion for transport corridors and industrial cities in its 2026 budget, spurring rapid-set admixture consumption that can reduce pour-to-traffic windows from 28 days to 7 days[1]Public Investment Fund, “Annual Budget 2026,” pif.gov.sa. The UAE’s USD 81.7 billion pipeline emphasizes 100-year-life corrosion-inhibiting admixtures for the Etihad Rail network. Qatar awarded USD 3.2 billion in road contracts in 2025, mandating more than or equal to 30% GGBS (Ground Granulated Blast Furnace Slag) content that necessitates polycarboxylate-ether superplasticizers capable of maintaining workability in high-replacement mixes. Suppliers with in-region technical centers, such as Sika’s 2,400 m² Riyadh lab, are capturing share by providing real-time mix-design support.

Mandated Adoption of Green-Building Rating Systems

Estidama and GSAS certifications have evolved into de facto entry barriers. Abu Dhabi requires a minimum 1 Pearl rating for buildings over 5,000 m², driving adoption of low-embodied-carbon concrete and water-based adhesives with Environmental Product Declarations. Qatar mandates GSAS certification for government projects above QAR 50 million, advancing demand for ISO 14025-compliant products. Multinationals already publish lifecycle data for most SKUs, whereas many regional players are still commissioning third-party verifications, accelerating consolidation. Henkel’s Watertite Xtreme membrane, launched in 2025 with a 35% lower global-warming potential, quickly achieved preferred-vendor status on UAE federal projects.

Rise of Giga-Projects Requiring Specialty Admixtures

Mega developments such as NEOM’s The Line specify 120 MPa concrete with less than 0.1% shrinkage, attainable only through hybrid silica-fume and PCE (Polycarboxylate Ether) blends. The Red Sea Project mandates ISO 12944 C5-M coatings for splash-zone steel, leading Sika to tailor its Sikalastic-560 GCC (Gulf Cooperation Council) formulation for 55°C summer peaks. Qiddiya’s indoor ski facility specifies Jotun Steelmaster 1200WF for 4-hour fire ratings, illustrating how high-profile projects reward vendors that can guarantee batch-to-batch consistency.

Rapid Expansion of Data-Center Construction

Hyperscale operators are injecting demand for antistatic flooring and fire-rated coatings. Microsoft’s USD 1.5 billion Saudi data-center investment chose Sikafloor MultiFlex PS-35 ESD with less than 1×10⁹ ohm resistivity. Amazon Web Services is extending Bahrain and UAE zones, increasing regional capacity to 300 MW by 2030, or roughly 600,000 m² of new server-floor area. Suppliers such as Mapei have reformulated polyurethane resins to preserve ESD properties at 40°C ambient.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening VOC-emission caps on solvent-borne products | -0.6% | UAE (Dubai, Abu Dhabi), Saudi Arabia (Riyadh, Jeddah) | Short term (≤ 2 years) |

| Supply-chain volatility for key raw materials (epoxies, PCEs) | -0.8% | Regional (all markets); upstream dependencies on Asia-Pacific | Medium term (2-4 years) |

| Skilled-labour shortages limiting correct on-site application | -0.5% | Saudi Arabia, UAE, Qatar (acute); Kuwait, Egypt (moderate) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tightening VOC-Emission Caps on Solvent-Borne Products

Dubai Municipality’s Technical Guideline TG-04 sets a 40 g/L limit for interior coatings effective Q1 2027[2]Dubai Municipality, “Technical Guideline TG-04,” dm.gov.ae. Abu Dhabi’s Quality and Conformity Commission added third-party ISO 16000-9 testing in 2025, raising compliance costs that smaller suppliers struggle to absorb. AkzoNobel’s Dulux Trade line, reformulated below 30 g/L, secured 60% of Abu Dhabi government repaint contracts in 2025 despite a 15-20% price premium. Three regional producers have already exited the UAE market rather than fund reformulation.

Supply-Chain Volatility for Key Raw Materials

Force-majeure events at Asian bisphenol-A plants in 2025 raised epoxy-resin prices by 18%, compressing flooring margins. Chinese environmental inspections idled 20% of acrylic-acid capacity, extending PCE lead times from 6 weeks to 14 weeks. BASF responded by expanding its Dilovası dispersions plant by 50,000 tons to buffer Middle East operations. Smaller suppliers must carry higher safety stock, tying up working capital and eroding competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Waterproofing Outpaces Admixtures in Growth Velocity

Concrete admixtures accounted for 36.22% of 2025 revenue, primarily through commoditized plasticizers integrated into ready-mix and precast supply chains. High-range water reducers based on PCEs command USD 800-1,200 per ton premiums due to performance in more than 60 MPa and self-compacting mixes specified on giga-projects. In contrast, waterproofing systems are forecast to grow at a 5.41% CAGR during the forecast period (2026-2031), reflecting developer preference for preventive moisture barriers that lower lifecycle repair costs. Surface treatments and protective coatings comprised 22% of 2025 turnover, propelled by bridge rehabilitation and coastal infrastructure that require ISO 12944 C5-M classifications.

Industrial flooring benefits from data-center and pharmaceutical cleanroom expansion. The Middle East construction chemicals market size for flooring grew as Mapei’s MAPEFLOOR SYSTEM has become the reference specification for 60% of new server halls. Repair and rehabilitation products harness rapid-cure technologies such as BASF’s MasterEmaco, which reaches 25 MPa in six hours and enables overnight road fixes. Adhesives and sealants are rapidly converting to MS-polymer chemistries to comply with VOC caps. Grouts and anchors are gaining visibility in seismic retrofits, while cement grinding aids, currently 2%, grow as producers chase energy efficiency. The Middle East construction chemicals market increasingly rewards suppliers that innovate around regulatory compliance, extreme climates, and labor constraints rather than purely volume metrics.

By End-User Industry: Residential Surge Challenges Infrastructure Dominance

Infrastructure and public spaces captured 44.12% of 2025 consumption on the back of metro extensions, high-speed rail, and civic facilities. Yet residential construction is expanding at a 5.67% CAGR during the forecast period (2026-2031) as Saudi Arabia targets 499,000 additional housing units by 2030 and the UAE plans 390,000 homes under its National Housing Strategy. Each Saudi unit consumes roughly USD 1,800 in chemicals, tilting demand toward tile adhesives, sealants, and crystalline waterproofers.

Commercial buildings' market share was stabilized after the Expo-related supply overhang. Industrial facilities' market share was driven by logistics hubs requiring chemical-resistant flooring. Institutional projects such as hospitals and universities show counter-cyclical resilience; Qatar awarded USD 2.1 billion in hospital contracts in 2025 that specify antimicrobial coatings. The Middle East construction chemicals industry is therefore rebalancing toward a more diversified client mix, prompting historically infrastructure-centric suppliers to introduce retail-packaged lines aimed at small contractors and DIY (Do-It-Yourself) channels.

Geography Analysis

Saudi Arabia retained 35.45% of 2025 revenue and is projected to expand at the region’s fastest 5.42% CAGR during the forecast period (2026-2031). NEOM’s USD 500 billion pipeline, the Red Sea resort islands, and Qiddiya entertainment hub collectively demand more than 2 billion m³ of concrete with admixture spends that can reach USD 15 per cubic meter. Localized capacity builds, such as Mapei’s planned Tabuk plant, trim lead times by 30%, a decisive advantage for projects in remote northern zones. The Public Investment Fund’s USD 40 billion 2026 budget prioritizes transport and industrial corridors that specify ISO-certified batching and technical on-site support.

In the United Arab Emirates, future growth pivots to data-center and logistics assets; the country targets 300 MW of server capacity by 2030, which drives steady demand for antistatic flooring and fire-rated coatings. Estidama Pearl and Dubai Green Building regulations add 22-28% incremental chemical value to certified projects. Jotun’s AED 450 million Abu Dhabi plant, inaugurated in 2026, dedicates 60% of its 40,000-ton capacity to low-VOC architectural and marine coatings.

In Qatar, post-World Cup maintenance contracts are strong, and GSAS mandates continue to drive PCE superplasticizer demand. Kuwait and Egypt show divergent profiles: Kuwait’s desalination expansion favors marine-grade coatings, whereas Egypt’s New Administrative Capital sustains tile adhesive and admixture sales. The rest of the Middle East, Oman, Bahrain, and Jordan, rely heavily on regional distributors, though Sika’s 2025 acquisition of Gulf Additive Factory illustrates a push to integrate secondary markets.

Competitive Landscape

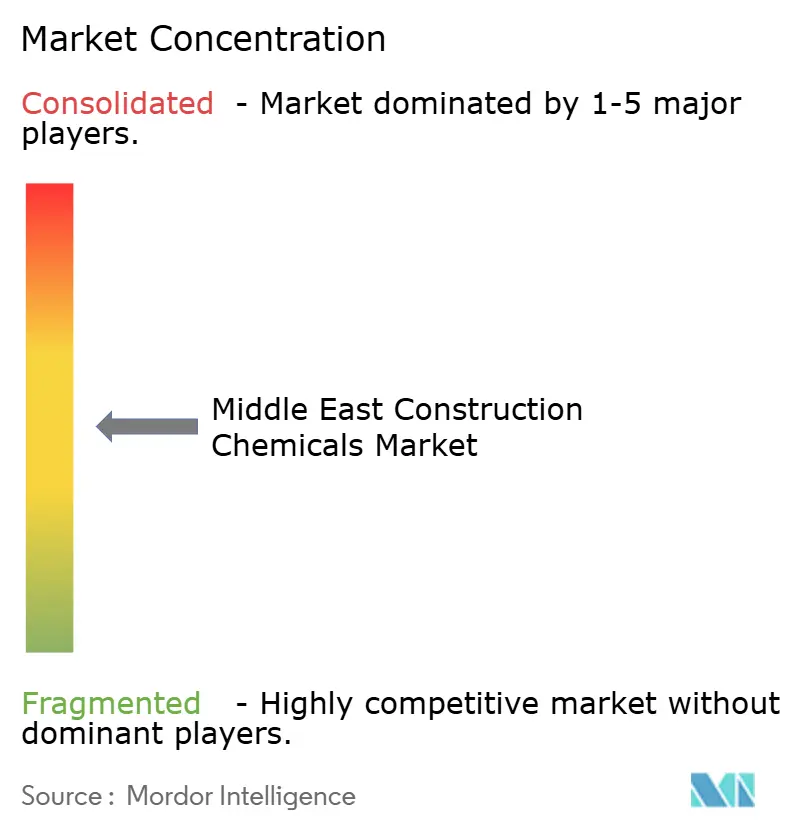

The Middle East Construction Chemicals market is moderately fragmented. Competitive differentiation is shifting from pure chemistry to bundled service models. Field training centers, QR code-linked dosing calculators, and IoT-enabled admixture dispensers are now pivotal as 77% of contractors acknowledge applicator skill gaps. Suppliers holding ISO 14025 EPDs (Environmental Product Declaration) and GCC saline-immersion approvals win disproportionate shares of government tenders, creating regulatory moats that hinder new entrants. Consequently, another consolidation wave is likely as mid-tier players without either scale or service specialization seek exit options before 2028.

Middle East Construction Chemicals Industry Leaders

Sika AG

Dow

Mapei S.p.A.

Saint-Gobain

Saudi Readymix

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Master Builders Solutions announced the agreement to acquire Arkaz Al Sharq Building Materials (Arkaz), a Saudi Arabian construction chemicals company specialising in concrete admixtures, waterproofing, and building products.

- June 2025: Sika AG bolstered its presence in Qatar by acquiring Gulf Additive Factory LLC, a local manufacturer of diverse construction chemical products. This strategic move solidified Sika AG's foothold in the Qatari market and also paved the way for potential expansion opportunities.

Middle East Construction Chemicals Market Report Scope

Construction chemicals are substances that are used to enhance the qualities of construction materials such as asphalt, concrete, mortar, grout, and mortar. These substances can be used to strengthen and extend the life of building materials, lessen shrinkage and cracking, enhance water resistance, and offer corrosion protection. Admixtures, sealants, waterproofing agents, curing compounds, and protective coatings are examples of typical construction chemicals.

The construction chemicals market is segmented by product type, end-user industry, and geography. By product type, the market is segmented into concrete admixtures, surface treatments, repair and rehabilitation, protective coatings, industrial flooring, waterproofing, adhesives, sealants, grouts and anchors, and cement grinding aids. By end-user industry, the market is segmented into commercial, industrial, infrastructure and public space, and residential. The report covers the market size and forecast for five countries in the Middle East region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

By Product Type

| Concrete Admixtures |

| Surface Treatments |

| Repair and Rehabilitation |

| Protective Coatings |

| Industrial Flooring |

| Waterproofing |

| Adhesives |

| Sealants |

| Grouts and Anchors |

| Cement Grinding Aids |

By End-user Industry

| Infrastructure and Public Spaces |

| Commercial |

| Industrial |

| Residential |

By Country

| Saudi Arabia |

| United Arab Emirates |

| Qatar |

| Kuwait |

| Egypt |

| Rest of Middle-East |

| By Product Type | Concrete Admixtures |

| Surface Treatments | |

| Repair and Rehabilitation | |

| Protective Coatings | |

| Industrial Flooring | |

| Waterproofing | |

| Adhesives | |

| Sealants | |

| Grouts and Anchors | |

| Cement Grinding Aids | |

| By End-user Industry | Infrastructure and Public Spaces |

| Commercial | |

| Industrial | |

| Residential | |

| By Country | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Egypt | |

| Rest of Middle-East |

Key Questions Answered in the Report

What is the current value of the Middle East construction chemicals market?

The market is valued at USD 6.43 billion in 2026 and is projected to reach USD 8.21 billion by 2031.

Which product category is growing fastest?

Waterproofing systems are the fastest, expanding at a 5.41% CAGR during the forecast period (2026-2031).

Why is Saudi Arabia the largest regional market?

Vision 2030 giga-projects such as NEOM and Qiddiya drive high concrete and specialty chemical demand, giving Saudi Arabia 35.45% revenue share in 2025.

How do green-building mandates influence product demand?

Estidama and GSAS requirements add 22-28% more specialty admixture value to certified projects, favoring low-VOC and low-carbon formulations.

What are the main challenges for suppliers?

Tightening VOC limits, raw-material price volatility, and skilled-labor shortages all pressure margins and execution quality.

Page last updated on: