Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 0.82 Billion |

| Market Size (2031) | USD 1.05 Billion |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Construction Chemicals Market Analysis by Mordor Intelligence

The Africa Construction Chemicals Market size is estimated at USD 0.82 billion in 2026, and is expected to reach USD 1.05 billion by 2031, at a CAGR of 5.07% during the forecast period (2026-2031). Demand is rising because rapid urbanization collides with historic infrastructure gaps, pushing builders to specify performance additives that extend structural life and lower ownership costs. Public authorities favor speed and durability, steering procurement toward pre-blended mortars, low-VOC sealants, and supplementary cementitious materials that comply with emerging carbon rules. Multinational suppliers exploit these shifts by opening regional labs, while domestic firms concentrate on affordable distribution in commodity admixtures. The Africa construction chemicals market also benefits from megaprojects such as Egypt’s New Administrative Capital and Nigeria’s Dangote Refinery, which create large, time-bound spikes in product offtake and set higher performance benchmarks that gradually spill into residential and commercial work.

Key Report Takeaways

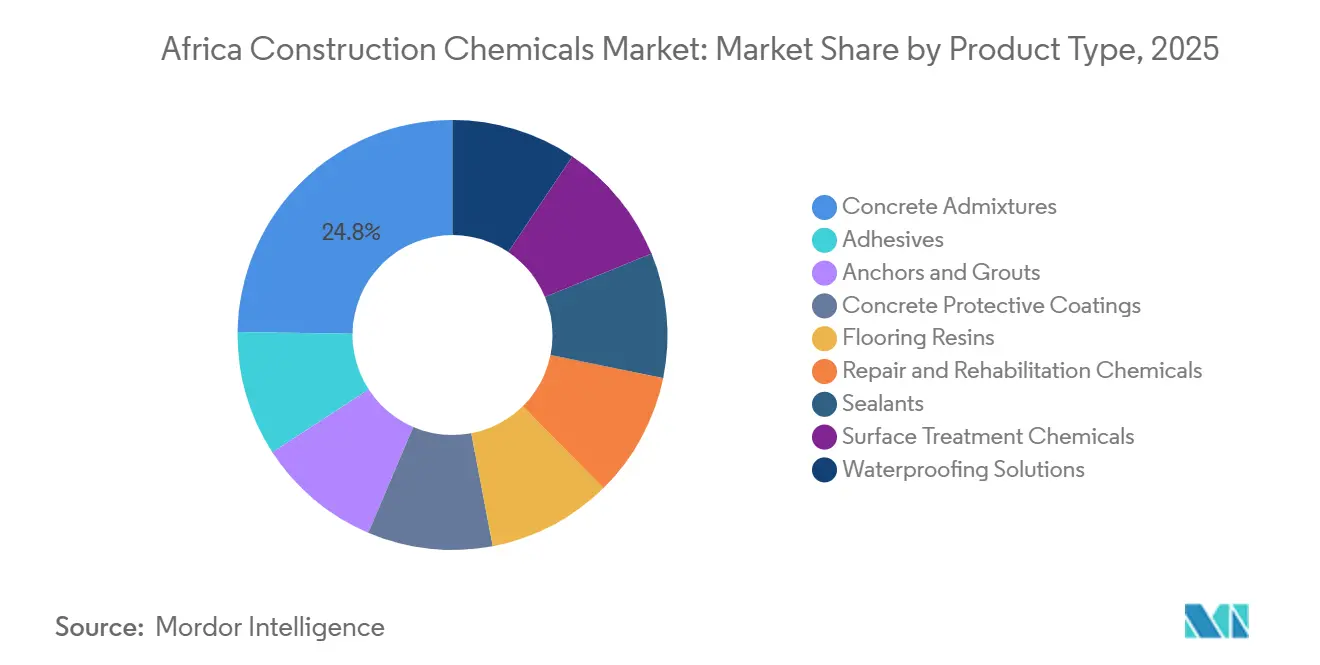

- Concrete admixtures accounted for 24.78% of Africa construction chemicals market share in 2025, while waterproofing solutions are advancing at a 5.72% CAGR through 2031.

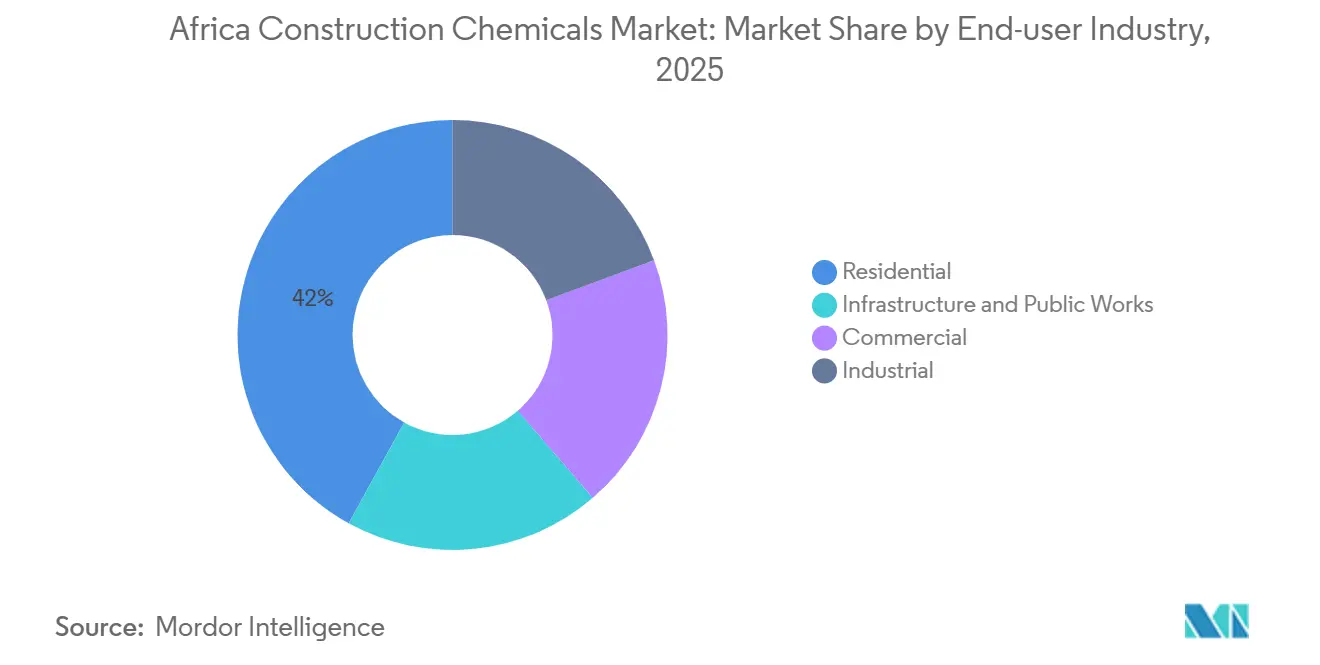

- Residential construction held 41.98% of the Africa construction chemicals market size in 2025, but infrastructure and public works are expanding at a 6.40% CAGR to 2031.

- Rest of Africa aggregated 51.48% of 2025 demand, whereas Egypt is projected to post the fastest 6.34% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Africa Construction Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure megaproject pipeline expansion | +1.2% | Egypt, Nigeria, Morocco; spillover to Kenya, Tanzania | Medium term (2-4 years) |

| Affordable-housing policy roll-outs and urban densification | +0.9% | South Africa, Egypt, Nigeria; emerging in Ghana, Côte d'Ivoire | Short term (≤ 2 years) |

| Demand for high-strength, energy-efficient structures | +0.7% | Global, with early adoption in South Africa, Egypt | Long term (≥ 4 years) |

| Green-cement tax incentives and embodied-carbon regulation | +0.6% | South Africa, Morocco; pilot programs in Egypt | Long term (≥ 4 years) |

| Valorisation of mining tailings into supplementary cementitious materials | +0.4% | South Africa, Zambia, DRC; limited to mining-intensive regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Infrastructure Megaproject Pipeline Expansion

Egypt committed USD 18 billion to infrastructure in 2025, with its New Administrative Capital alone requiring 45 million m³ of concrete through 2030. Similar momentum is visible in Nigeria, where the Dangote Refinery consumed specialty mortars and coatings to protect concrete from hydrocarbons and set new procurement standards for industrial facilities. Morocco’s high-speed rail extension to Marrakech, financed by the African Development Bank, demands low-shrinkage admixtures to curb slab cracking, raising technical entry barriers. Kenya’s Lamu Port–South Sudan–Ethiopia Corridor requires ISO 9001-certified chemical vendors, signaling a growing preference for lifecycle value rather than lowest cost. Contractors tend to stockpile membranes and grouts ahead of rainy seasons, shortening lead times and rewarding distributors with in-country warehousing. Collectively, these megaprojects enlarge the Africa construction chemicals market by channeling premium specifications from marquee infrastructure into mainstream residential and commercial projects.

Affordable-Housing Policy Roll-Outs and Urban Densification

South Africa’s Breaking New Ground program delivered 120,000 subsidized units in 2025, each using polymer-modified mortars that satisfy 50-year durability targets mandated by the National Home Builders Registration Council[1]“Breaking New Ground Adds 120,000 Homes,” Engineering News, engineeringnews.co.za. Egypt’s Social Housing Initiative seeks 1 million units by 2030 and specifies pre-blended tile adhesives to avoid on-site mixing errors, consolidating volume among accredited suppliers. Nigeria’s National Housing Fund, despite funding gaps, stimulates private developers in Lagos and Abuja to adopt self-leveling floors that accelerate handover schedules. Accra and Nairobi now pursue vertical densification that consumes more anchoring systems and façade sealants per project than single-level sprawl. Predictable multi-year demand allows chemical producers to site blending plants nearer to growth corridors, cutting freight costs and hedging currency swings. The Africa construction chemicals market, therefore, gains a reliable residential volume base that underpins broader capacity investments.

Demand for High-Strength, Energy-Efficient Structures

High-rise builders in Johannesburg, Cairo, and Lagos now specify concrete above 60 MPa compressive strength to optimize floor-area ratios and reduce column footprints. BASF’s MasterGlenium superplasticizers enabled water-cement ratios below 0.35 and captured 18% of South Africa’s high-performance admixture sub-segment in 2025[2]BASF Investor Presentation FY 2025, basf.com. Morocco’s updated energy code prioritizes thermal mass; this encourages phase-change material-enhanced concrete trials using Sika’s CoolCrete in Casablanca. African Union Agenda 2063 stresses climate adaptation, prompting procurement of reflective surface coatings that lower heat-island effects. Coastal projects increasingly include corrosion-inhibiting admixtures to curb chloride ingress, thereby adding specialty demand to what once was a volume-driven sector. These preferences enlarge the value pool within the Africa construction chemicals market and steer R&D toward multifunctional products.

Green-Cement Tax Incentives and Embodied-Carbon Regulation

South Africa’s amended Carbon Tax Act levies ZAR 190 (USD 10) per ton of CO₂ that exceeds a benchmark, heightening interest in slag and fly-ash blends. Morocco grants a 20% corporate tax rebate when manufacturers use industrial by-products in cementitious blends, channeling EUR 45 million of private capital into low-carbon upgrades since 2024. Egypt introduced voluntary embodied-carbon labeling in 2025; while adoption is nascent, global developers are already demanding compliance, pressuring local suppliers to quantify footprints. Divergent VOC ceilings across markets raise complexity: a waterproofing system cleared in South Africa often needs reformulation before Egyptian approval, lifting R&D costs and narrowing the playing field. Global formulators with distributed labs can amortize these expenses, whereas smaller firms risk market exit, nudging the Africa construction chemicals market toward greater concentration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening VOC and hazardous-chemicals limits | -0.5% | South Africa, Egypt; emerging in Nigeria, Kenya | Medium term (2-4 years) |

| Import-dependent raw-material price volatility | -0.6% | All markets except South Africa (partial local production) | Short term (≤ 2 years) |

| Counterfeit/sub-spec products eroding contractor confidence | -0.3% | Nigeria, Kenya, Tanzania; limited in South Africa, Morocco | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tightening VOC and Hazardous-Chemicals Limits

South Africa now caps VOCs in sealants and coatings at 50 g/L under the National Environmental Management Act, forcing a pivot to water-borne chemistries. Multinationals amortize testing and certification globally, but regionals face unworkable unit costs, prompting product discontinuation. Egypt’s Industrial Emissions Directive bans select phthalates in flooring resins, temporarily cutting supply in the commercial segment. Nigeria drafts similar rules, yet enforcement gaps allow low-compliance imports to coexist with premium lines, eroding contractor confidence. As regulations converge toward EU standards, firms without reformulation capacity risk exclusion from donor-funded infrastructure that mandates third-party certification. This compliance squeeze subtracts growth points from the Africa construction chemicals market.

Import-Dependent Raw-Material Price Volatility

Polymer feedstocks, representing up to 60% of formulation costs, remain largely imported, subjecting local blenders to currency swings and freight shocks. The South African rand fell 12% versus the euro in 2025, compressing margins for contracts priced in rand but supplied with euro-denominated resins. Nigeria’s FX restrictions postponed resin shipments for 90 days, leading to project stalls or quality compromises. Red Sea shipping diversions lifted Rotterdam-to-Lagos freight by 35%, adding USD 200 per ton to landed costs. Dangote’s Lagos polymer plant, due in 2028, may relieve regional scarcity, yet near-term exposure persists. Such volatility induces risk premiums in pricing, checks investment appetite, and brakes the Africa construction chemicals market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Waterproofing Outpaces Legacy Admixtures

Concrete admixtures captured 24.78% of Africa construction chemicals market share in 2025 because they remain standard inputs for ready-mix producers across the continent. Yet waterproofing solutions are expanding at a 5.72% CAGR through 2031, reflecting a pivot toward climate resilience in flood-prone cities such as Lagos and Cape Town. Large infrastructure projects, including the Cairo Metro tunnels, now specify integrated membrane systems like SikaProof, which embed moisture barriers during casting and elevate chemical intensity per cubic meter of concrete. Growing preference for crystalline admixtures that self-seal micro-cracks also pushes substitution away from surface coatings toward internal waterproofing.

Repair and rehabilitation products gain momentum as bridges and water plants built during the 1970s-1990s reach renewal cycles. South Africa’s ZAR 20 billion bridge maintenance backlog accelerates uptake of polymer-modified mortars that extend asset life by 15 years. Data-center construction by hyperscalers fuels demand for electrostatic-dissipative flooring resins, a niche that neither global nor regional players dominate, creating whitespace within the Africa construction chemicals market. Meanwhile, VOC limits challenge solvent-borne protective coatings; contractors remain hesitant to transition fully to water-borne alternatives without equivalent durability data, slowing the replacement cycle.

By End-User Industry: Residential Dominance Masks Infrastructure Surge

Residential projects commanded 41.98% of the 2025 volume because sub-Saharan governments subsidize housing to manage urban migration. Polymer-rich mortars, tile adhesives, and sealants help achieve rapid completion targets, anchoring steady demand within the Africa construction chemicals market. Yet infrastructure and public works are expanding at a 6.40% CAGR, driven by multilateral lenders that condition loans on green-building compliance. Egypt mandated 20% clinker replacement for public works in 2025, doubling slag-blended admixture sales in one budget cycle. Commercial high-rises in Sandton and Westlands trial self-healing concrete, positioning office developers as early adopters of premium systems.

Industrial facilities, from mining sites in the Copperbelt to refineries in Port Harcourt, require chemical resistance and abrasion tolerance, supporting specialty coating sales at higher margins. As urbanization matures and housing programs taper, infrastructure’s policy tailwind keeps it on track to overtake residential in value contribution by 2031. Consequently, suppliers recalibrate portfolios to align with transport corridors, power plants, and water projects rather than purely residential developers.

Geography Analysis

Rest of Africa, encompassing more than 40 smaller markets, absorbed 51.48% of 2025 demand, yet distribution remains fragmented, raising logistical costs and complicating certification. Egypt races ahead at a 6.34% CAGR because centralized procurement and a USD 58 billion pipeline provide predictable volume. Sika and BASF opened blending plants in the Suez Economic Zone, trimming delivery times and quarantining margins from currency shocks. South Africa achieves mid-single-digit growth, underpinned by strict South African Bureau of Standards protocols that elevate product quality and create export staging grounds into Botswana and Namibia.

Nigeria shows dual characteristics: premium demand in Lagos and Abuja contrasts with low-spec purchases in secondary cities. Currency swings and counterfeit infiltration temper growth, yet upcoming petrochemical self-sufficiency could shift cost structures favorably by 2028. Morocco rides EU partnership programs, making it an early adopter of low-VOC sealants and recycled-content admixtures. Kenya, Tanzania, and Ghana benefit from Chinese-funded infrastructure that imports international specifications, forcing local vendors to raise quality or exit, gradually consolidating the regional arm of the Africa construction chemicals market.

Competitive Landscape

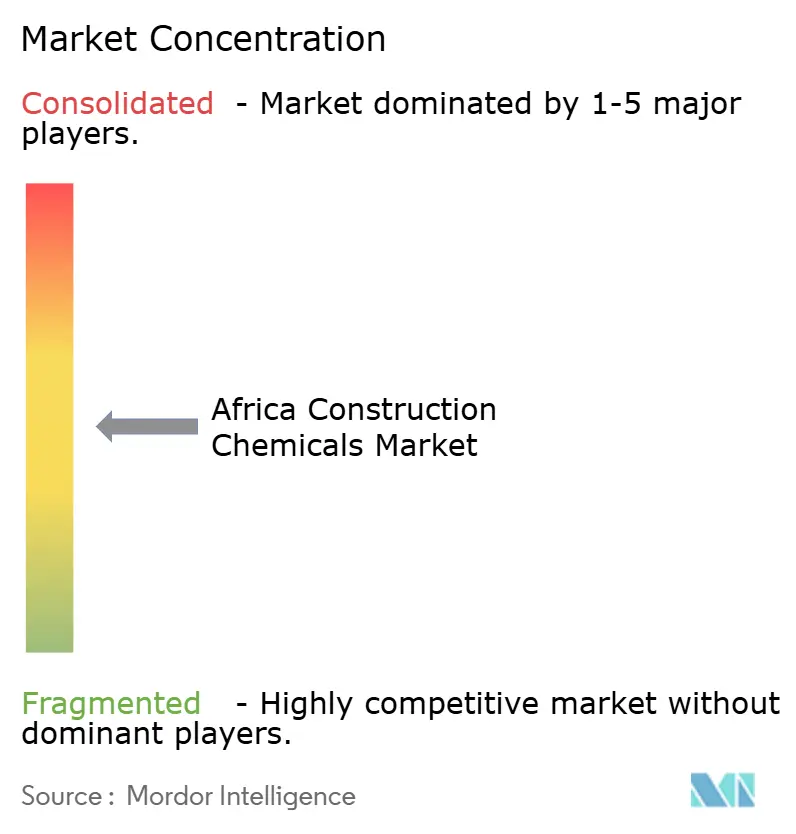

The Africa Construction Chemicals market is moderately consolidated. Sika’s mobile in-situ testing units embed engineers at job sites in Egypt and South Africa, creating switching costs where performance failures carry liquidated damages. Regional champions like Dangote Industries, AfriSam, and PPC Ltd leverage price competitiveness and raw-material proximity in commodity admixtures, though they lack deep R&D for advanced chemistries. Whitespace remains in specialized flooring for data centers, seismic retrofitting grouts, and ultra-high-performance concrete. Disruptors such as Dangote’s forthcoming polymer plant aim to backward-integrate feedstocks, potentially lowering cost bases for internal chemical lines and reshaping competitive intensity across West Africa.

Africa Construction Chemicals Industry Leaders

Saint-Gobain

BASF

Sika AG

Mapei S.p.A.

Dangote Industries Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: MC-Bauchemie forged a strategic joint venture with SwissChem Construction Chemicals. This collaboration aims to bolster MC-Bauchemie's foothold and operational prowess in Egypt and its neighboring regions. SwissChem boasts a reputation for its diverse offerings, including concrete admixtures, waterproofing solutions, grouts, anchoring products, and advanced flooring systems.

- June 2025: Sika, a Swiss group specializing in construction chemicals, inaugurated a production facility close to Agadir, Morocco. This plant will produce mortar and admixtures tailored for both local and regional markets. Positioned strategically, the new site aims to cater to Morocco's southern region and its neighbor, Mauritania.

Africa Construction Chemicals Market Report Scope

Construction chemicals are substances that are used to improve the properties of building materials such as asphalt, concrete, mortar, grout, and mortar. These materials can be used to reinforce and prolong the life of building materials, reduce shrinkage and cracking, improve water resistance, and provide corrosion protection. Examples of common construction chemical types include mixes, sealants, waterproofing agents, curing compounds, and protective coatings.

The African construction chemicals market is segmented into product type, end-user industry, and geography. By product type, the market is segmented into concrete admixtures, surface treatments, repair and rehabilitation, protective coatings, industrial flooring, waterproofing, adhesives, sealants, grouts and anchors, and cement grinding aids. By end-user industry, the market is segmented into commercial, industrial, infrastructure and public space, and residential. The report covers the market size and forecast in four countries in the African region. For each segment, the market sizing and forecasts have been done on the basis of value (USD million).

By Product Type

| Adhesives |

| Anchors and Grouts |

| Concrete Admixtures |

| Concrete Protective Coatings |

| Flooring Resins |

| Repair and Rehabilitation Chemicals |

| Sealants |

| Surface Treatment Chemicals |

| Waterproofing Solutions |

By End-user Industry

| Infrastructure and Public Works |

| Commercial |

| Industrial |

| Residential |

By Geography

| South Africa |

| Egypt |

| Nigeria |

| Morocco |

| Rest of Africa |

| By Product Type | Adhesives |

| Anchors and Grouts | |

| Concrete Admixtures | |

| Concrete Protective Coatings | |

| Flooring Resins | |

| Repair and Rehabilitation Chemicals | |

| Sealants | |

| Surface Treatment Chemicals | |

| Waterproofing Solutions | |

| By End-user Industry | Infrastructure and Public Works |

| Commercial | |

| Industrial | |

| Residential | |

| By Geography | South Africa |

| Egypt | |

| Nigeria | |

| Morocco | |

| Rest of Africa |

Key Questions Answered in the Report

How large is the Africa construction chemicals market in 2026?

The market stands at USD 0.82 billion in 2026 and is forecast to reach USD 1.05 billion by 2031.

Which product segment is growing fastest?

Which product segment is growing fastest?

What end-user will drive future demand?

Infrastructure and public works are set to expand at a 6.40% CAGR, outpacing residential as lenders link funding to low-carbon criteria.

Why is Egypt the growth hotspot?

Egypt benefits from a USD 58 billion project pipeline, localization incentives for chemicals, and 6.34% forecast CAGR between 2026 and 2031.

How are regulations shaping supply?

Stricter VOC and carbon rules force reformulation, favoring multinationals with R&D resources and prompting consolidation across the region.

Page last updated on: