Point Of Care Coagulation Testing Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

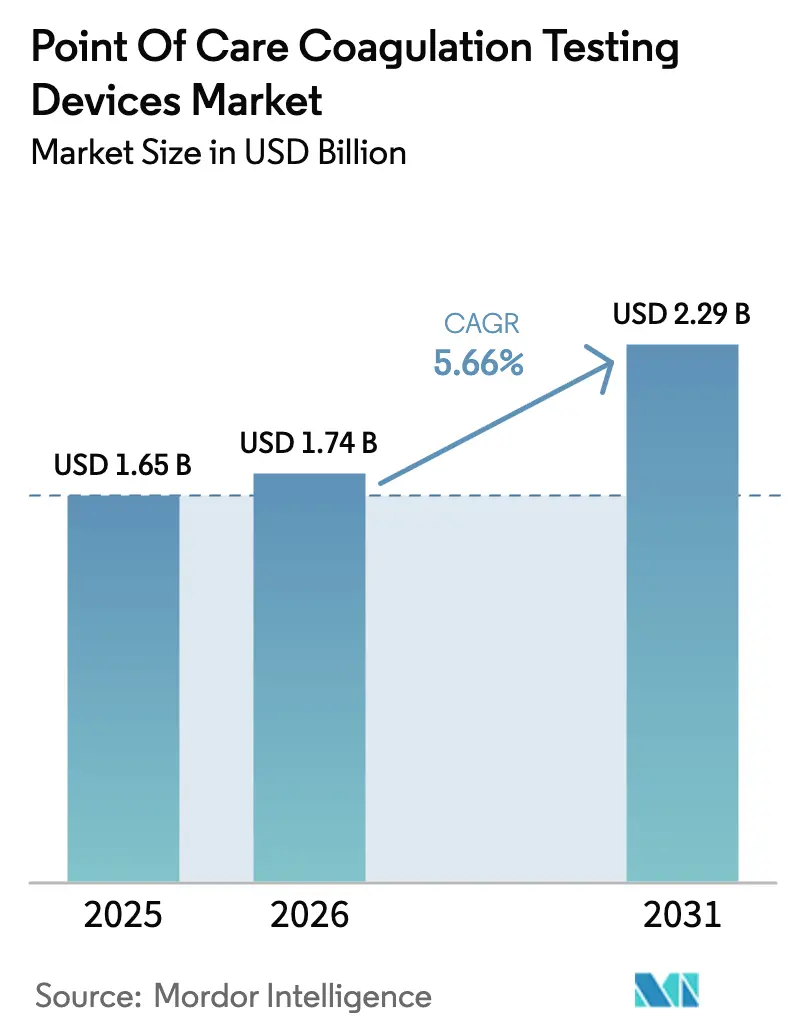

| Market Size (2026) | USD 1.74 Billion |

| Market Size (2031) | USD 2.29 Billion |

| Growth Rate (2026 - 2031) | 5.66% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

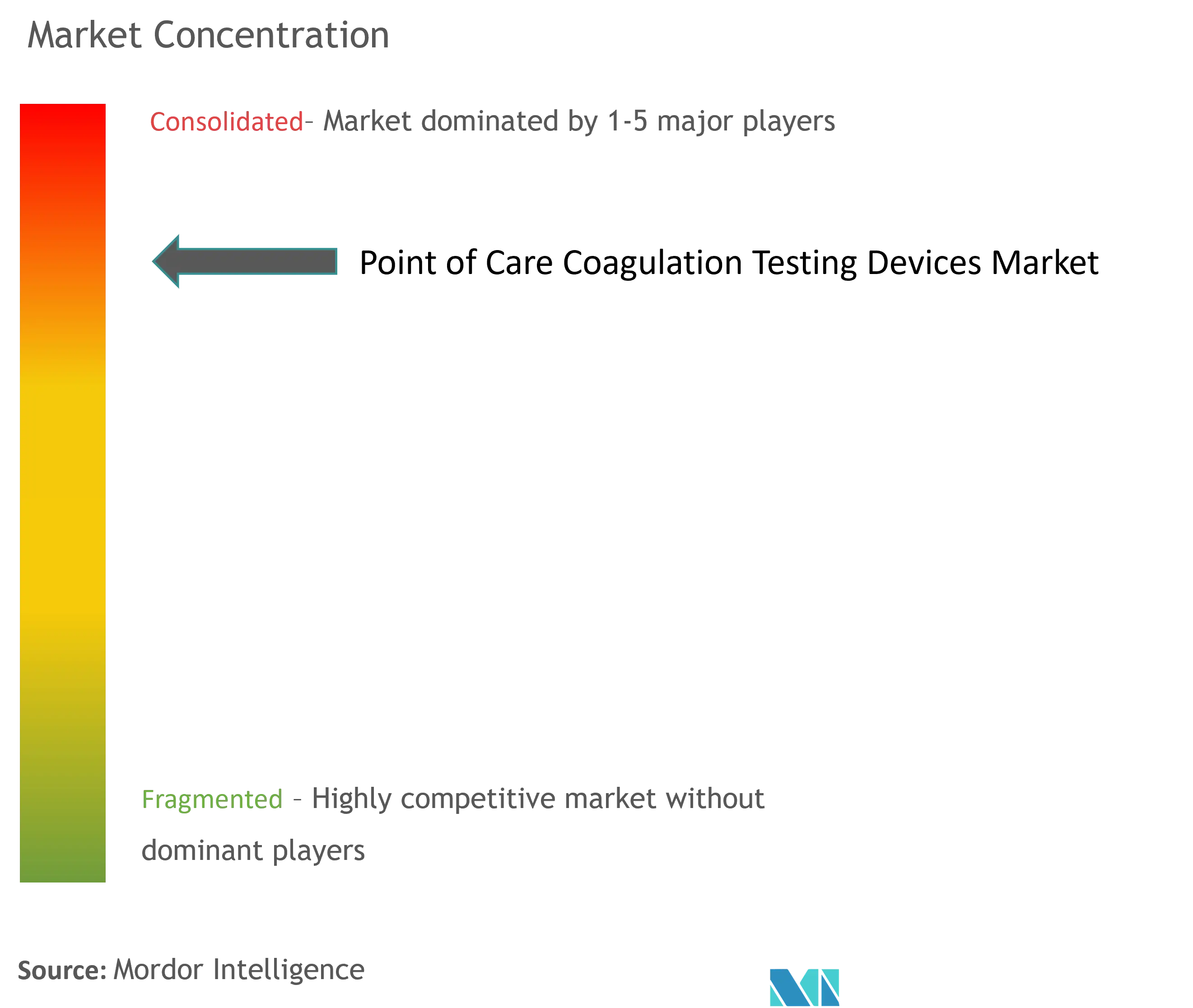

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Point Of Care Coagulation Testing Devices Market Analysis by Mordor Intelligence

The Point Of Care Coagulation Testing Devices Market size is expected to grow from USD 1.65 billion in 2025 to USD 1.74 billion in 2026 and is forecast to reach USD 2.29 billion by 2031 at 5.66% CAGR over 2026-2031.

Precision Diagnostics at the Bedside: Revolutionizing Coagulation Management

Uptake accelerates as hospitals, emergency rooms, and home-care settings demand near-instant coagulation insights for trauma, cardiovascular events, and oral-anticoagulant management. Growth is anchored by rapid adoption of electrochemical detection, which supports compact form factors, low sample volumes, and high analytical precision. Rising numbers of patients on direct oral anticoagulants, broader use of viscoelastic testing in critical care, and the shift toward patient self-monitoring further strengthen demand. The market also benefits from innovations that link devices to electronic health records, enabling clinicians to integrate bedside data into therapy decisions in real time.

Key Report Takeaways

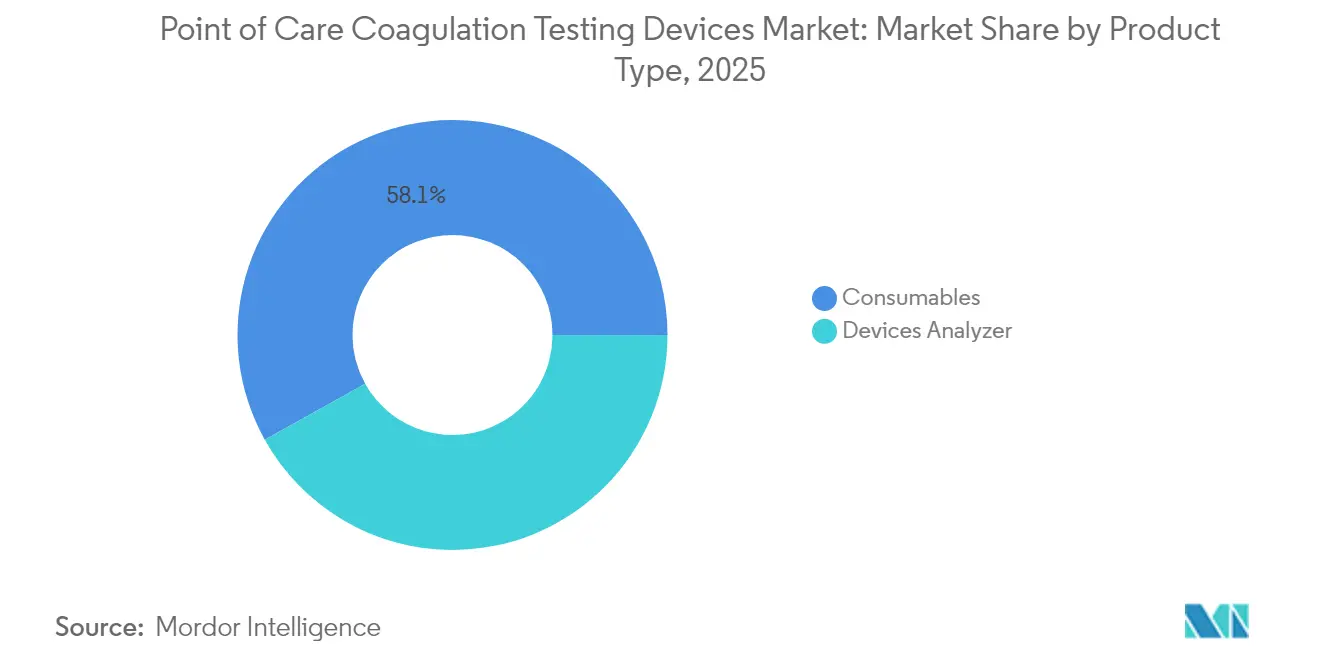

- By product type, consumables held 58.10% of point of care coagulation testing device market share in 2025, while analyzers trail but gain ground through miniaturization.

- By test type, Prothrombin Time/INR contributed 57.02% revenue share in 2025; viscoelastic assays record the fastest CAGR at 8.52% through 2031.

- By technology, electrochemical detection accounted for 61.05% share in 2025 and is expected to expand at 6.12% CAGR to 2031.

- By sample type, whole blood commanded 76.88% of point of care coagulation testing device market size in 2025; capillary blood sampling grows at 7.28% CAGR to 2031.

- By end-user, hospitals and clinics controlled 51.78% revenue share in 2025, while home-care settings rise fastest at 7.66% CAGR to 2031.

- By geography, North America led with 41.92% share in 2025; Asia-Pacific is set to grow at 7.31% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Point Of Care Coagulation Testing Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Rapid uptake of DOAC patient self-monitoring | ~ +0.8 % | North America & EU; early adoption in Japan | Medium term |

| Expansion of ER-based viscoelastic testing protocols | ~ +0.6 % | Global tier-1 trauma centers; fastest scaling in APAC | Short term |

| Increasing patient population with bleeding disorders | ~ +0.4 % | Global, pronounced in China & India | Long term |

| Benefits offered over conventional laboratory coagulation testing | ~ +0.3 % | Global | Long term |

| Chinese CDC mandate for ACT testing in cardiovascular cath-labs | ~ +0.7 % | China (spill-over to wider APAC) | Short term |

| Gulf-region stroke centers’ preference for cartridge-based aPTT | ~ +0.3 % | GCC (Saudi Arabia, UAE, Qatar) | Medium term |

| Source: Mordor Intelligence | |||

Rapid uptake of DOAC patient self-monitoring

Surging prescriptions of direct oral anticoagulants have created a cohort that requires frequent, convenient monitoring. Recent studies confirm the readiness of many patients to manage therapy with handheld coagulometers that give results in less than 60 seconds [1]Source: Shu-Hua Bakhru, “Validation of a Whole Blood Coagulometer Sensitive to the Direct Oral Anticoagulants,” Scientific Reports, nature.com. Clinicians now apply standardized readiness tools such as the PERSONAE scale to select candidates for home use. Device makers respond with cartridges calibrated for apixaban and rivaroxaban levels, driving widespread placement in primary care and pharmacy settings. As Factor XI inhibitor trials progress, developers foresee even broader demand for specialty panels that quantify novel agent activity. Integration with smartphone apps sends encrypted readings to clinicians, ensuring therapy adjustment without clinic visits.

Expansion of ER-based viscoelastic testing protocols

Emergency departments increasingly rely on viscoelastic assays that report clot initiation, firmness, and lysis within 15 minutes. Systems such as TEG 6S and ROTEM sigma have proved decisive in trauma pathways that target balanced transfusion ratios. The World Health Organization’s patient blood-management guidance urges adoption, and many centers now embed viscoelastic algorithms in massive transfusion protocols. Portable instruments cut the delay found in central-lab pathways, supporting real-time decisions for platelet or fibrinogen supplementation. Post-COVID experience, which highlighted hypercoagulable states, further normalizes bedside viscoelastic workflow in mixed medical ICUs.

Increasing patient population with bleeding disorders

Global prevalence of hemophilia, von Willebrand disease, and other inherited bleeding disorders grows as diagnostic reach improves. Updated pediatric venous-thromboembolism guidelines recommend direct oral anticoagulants with point of care confirmation of drug effect [2]Source: Paul Monagle, “ASH/ISTH 2024 Updated Guidelines for Treatment of Venous Thromboembolism in Pediatric Patients,” Blood Advances, ashpublications.org. Aging societies add to demand; about 8% of adults over 65 take chronic anticoagulation. These trends place sustained pressure on facilities to maintain immediate coagulation insight that minimizes adverse events. Device manufacturers expand reagent panels to accommodate high-throughput screening in outreach clinics.

Benefits offered over conventional testing

Point of care systems slash turnaround from hours to minutes, reducing unnecessary transfusion by up to 40% in major surgeries. Rapid answers shorten emergency room stays, cut repeat phlebotomy, and improve patient satisfaction. Contemporary electrochemical sensors match laboratory accuracy for INR, fibrinogen, and D-dimer while using micro-samples. Coupled with electronic health record interfaces, results post automatically, streamlining audit trails and billing. These efficiency gains resonate across high-income and emerging markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR | Geographic Relevance | Peak Impact |

|---|---|---|---|

| Reimbursement gaps for laboratory tests | ~ −0.7% | France, Spain, Brazil; U.S. private payers | Short term |

| Shortage of skilled technicians for advanced platforms | ~ −0.5% | Emerging markets (LATAM, Africa, parts of SEA) | Medium term |

| Limited shelf-life of heparin-sensitive cartridges in tropics | ~ −0.3 % | ASEAN, Sub-Saharan Africa | Short term |

| Stringent MDR documentation burden on EU SME device makers | ~ −0.4 % | EU-27 (spill-over to U.K.) | Medium term |

| Source: Mordor Intelligence | |||

Reimbursement gaps for laboratory tests

Protecting Access to Medicare Act revisions scheduled for 2025 will trim reimbursement for hundreds of assays, including coagulation panels, by as much as 15% each year. Smaller hospitals and independent labs anticipate tighter margins and may postpone equipment upgrades until clarity emerges. Private insurers that mirror the federal fee schedule could extend the effect. Although legislation such as the Saving Access to Laboratory Services Act aims to ease reductions, delayed funding keeps the outlook uncertain for providers assessing payback on capita

Shortage of skilled technicians for advanced platforms

Sophisticated viscoelastic and ultrasound-resonance systems require operators who understand hemostasis biology, quality control, and middleware connectivity. Workforce surveys highlight shortages of personnel able to interpret graphs and troubleshoot software, particularly in lower-income regions. Vendors now deliver remote mentoring and automated interpretation algorithms, yet the skills gap remains a barrier until broad training initiatives gain traction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Consumables sustain revenue momentum

The point of care coagulation testing device market size for consumables reached USD 958.8 million in 2025, translating into 58.10% of global revenue. Each cartridge or strip is single use, locking in repeat sales that insulate suppliers from procurement cycles. Dry-reagent advances extend shelf life beyond 18 months, easing logistics in warm climates. Analyzer miniaturization moves devices into ambulatory surgery centers and emergency transport. The launch of DOAC-specific cartridges boosts recurring sales further because cardiology clinics add weekly testing requirements.

Peripheral innovation continues as quick-response QR codes on consumable packs automate lot tracking, error reduction, and recall management. Analyzers account for the remaining revenue and are shifting toward fully wireless modules that share data with hospital information systems, a feature that tightens infection-control protocols by keeping equipment inside isolation rooms.

By Test Type: Prothrombin Time remains foundational

Prothrombin Time/INR testing delivered USD 940.8 million, equivalent to 57.02% of 2025 revenue. Despite expanding DOAC use, warfarin therapy prevails in mechanical valve patients and resource-limited settings, anchoring demand. Activated Clotting Time serves cardiac surgery and catheter labs where heparin dosing requires minute-by-minute feedback. Viscoelastic tests are the growth engine, registering an 8.52% CAGR that outpaces all other categories, as surgeons and intensivists adopt comprehensive clot-strength assessment.

D-dimer panels gained new importance after COVID-19 because elevated fibrin-degradation fragments correlate with thrombotic complications. Guideline thresholds for sensitivity above 95% and negative predictive value above 97% ensure clinical confidence, prompting manufacturers to enhance optical detection modules in select analyzers.

By Technology: Electrochemical detection dominates precision

Electrochemical sensors controlled 61.05% of 2025 revenue and are expected to reach 63.7% by 2031, supported by robust signal-to-noise ratios and low power draw. Optical detection retains a foothold in labs favoring direct clot visualization, yet its footprint shrinks as point of care units encroach. Mechanical and ultrasound resonance platforms record the highest incremental growth, thanks to FDA-cleared systems that relay viscoelastic profiles in under 15 minutes.

Research into resonant acoustic rheometry reveals new use cases for plasma testing that may bring high-speed fibrinolysis profiling to trauma corridors. Artificial-intelligence overlays are emerging, with algorithms trained on thousands of tracings to flag sepsis-associated coagulopathy days before clinical evidence appears.

By Sample Type: Whole blood leads while capillary sampling rises

Whole blood assays represented 76.88% of 2025 test volumes because they require no centrifugation and minimize pre-analytical error. Point of care coagulation testing device market size for whole blood protocols is forecast to climb steadily, underpinned by emergency medicine and operating room usage. Capillary sampling posts a 7.28% CAGR as fingerstick collection enables self-testing. Validation studies confirm over 95% correlation to venous draws for INR and fibrinogen, paving the way for pediatric and oncology applications where venipuncture avoidance improves compliance.

Plasma remains the laboratory gold standard, yet microfluidic separation chips may let future point-of-care devices deliver plasma-quality analytics from a single droplet, reducing hematocrit interference and widening critical-care acceptance

By End-user: Hospitals lead; home-care accelerates

Hospitals and clinics captured 51.78% of global shipments in 2025, relying on devices for trauma bays, operating theaters, and intensive care. Diagnostic laboratories augment central analyzers with bedside meters for stat results. Blood banks deploy units for donor screening to protect inventory integrity.

Home-care exhibits the fastest growth at 7.66% CAGR as payers recognize lower admission rates when patients self-monitor. Subscription-based programs deliver monthly cartridge kits plus app-driven reminders. Clinicians access dashboards that present weekly trends, letting them titrate doses remotely. This decentralized approach supports value-based care models and aligns with telehealth expansion.

Geography Analysis

North America accounted for 41.92% of 2025 revenue, driven by high procedure volumes, favorable reimbursement, and more than 50,000 handheld meters in active use. Adoption benefits from integrated trauma networks that place viscoelastic devices in helicopters and ambulances. The 2025 reimbursement cuts mandated by PAMA temper growth but have not halted capital cycles as providers link testing to transfusion cost savings that outweigh fee reductions.

Europe remains a strong contributor with a mature trauma system and stringent evidence-based purchasing. An aging demographic—over 20% of citizens are above 65 in several member states—boosts chronic anticoagulant monitoring. Regulators closely examine mergers; the Competition and Markets Authority cleared Roche’s LumiraDx acquisition after confirming continued market choice. Cross-border procurement alliances create purchasing power that favors multi-analyte platforms with open connectivity standards.

Asia-Pacific posts the highest regional CAGR at 7.31% through 2031, propelled by China, Japan, and India. Government initiatives such as India’s Production Linked Incentive scheme encourage domestic device production, lowering unit costs and accelerating rural adoption. Rising middle-class insurance coverage, combined with elevated cardiovascular risk profiles, adds structural demand. The region also pilots smartphone-linked capillary assays in community clinics, addressing access gaps in remote areas without central labs.

Latin America and the Middle East & Africa remain smaller markets yet exhibit CAGRs above 8%. Private hospital chains in Brazil and Saudi Arabia embrace viscoelastic testing to differentiate premium surgical packages. Public systems gradually allocate funds for handheld INR meters in anticoagulation clinics to reduce congestion and improve patient flow.

Competitive Landscape

The point of care coagulation testing device market is moderately concentrated. Abbott, Siemens Healthineers, Werfen, and Haemonetics together hold roughly 45% of global revenue, benefitting from broad portfolios, global distribution reach, and sustained R&D investment. Roche expanded its footprint with the 2024 purchase of LumiraDx assets, adding rapid-test manufacturing capacity that spans coagulation, infectious disease, and cardiac markers.

Differentiation increasingly centers on turnaround speed, connectivity, and breadth of test panels. HemoSonics uses ultrasound resonance to deliver a full hemostasis profile in less than 15 minutes, gaining traction in high-acuity surgery. Dexcom’s expiring analyte-sensor patent opens the door for next-generation amperometric cartridges that may carry lower costs and longer shelf lives.

Strategic alliances proliferate as suppliers bundle hardware, consumables, and informatics. Merit Medical’s 2025 acquisition of Biolife Delaware complements its vascular-closure offerings and deepens relationships with interventional radiologists. Meanwhile, AI startups partner with device leaders to embed predictive analytics that flag thrombosis risk days before onset, driving a shift from reactive to preventive care.

Hybrid sales models are emerging: subscription packages guarantee consumable supply, ongoing software updates, and remote device diagnostics in exchange for multi-year contracts, an approach that stabilizes revenue and reduces capital-budget hurdles for smaller facilities.

Point Of Care Coagulation Testing Devices Industry Leaders

F. Hoffmann-La Roche Ltd

Siemens Healthineers AG

Abbott

Werfen

HemoSonics, LLC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: HemoSonics named Best Medical Device Company at the Triangle Business Journal Life Sciences Awards, reflecting market acceptance of its rapid ultrasound-based analyzer.

- May 2025: Merit Medical acquired Biolife Delaware for USD 120 million, adding topical hemostatic agents to its portfolio.

- April 2025: HemoSonics secured the Medical Device Network Excellence Award for marketing success of the Quantra system.

- February 2025: Novo Nordisk reported expanded hemophilia portfolio with Alhemo approval, increasing long-term monitoring needs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the point-of-care coagulation testing devices market as handheld or benchtop analyzers and their dedicated consumables that deliver rapid clotting parameters (PT/INR, ACT, aPTT, viscoelastic profiles, D-dimer) at or near the patient site. We include units used inside emergency rooms, operating theaters, dialysis suites, ambulances, and home-care plans where the user performs or interprets the test outside a central laboratory.

Scope exclusion: large-volume laboratory coagulation analyzers and generic POC diagnostics such as blood gas or glucose meters are excluded from the revenue pool.

Segmentation Overview

- By Product Type

- Devices/Analyzers

- Handheld Systems

- Benchtop Systems

- Consumables

- Devices/Analyzers

- By Test Type

- Prothrombin Time / INR

- Activated Clotting Time (ACT)

- Activated Partial Thromboplastin Time (aPTT)

- Viscoelastic Tests (TEG, ROTEM, Quantra)

- D-dimer & Fibrin Degradation Tests

- By Technology

- Electrochemical Detection

- Optical Detection

- Mechanical/Viscoelastic Sensing

- Ultrasound-based Resonance

- By Sample Type

- Whole Blood

- Capillary Blood

- Plasma

- By End-user

- Hospitals and Clinics

- Diagnostic Laboratories

- Blood Banks & Transfusion Centers

- Others

Detailed Research Methodology and Data Validation

Primary Research

We spoke with hematologists, trauma surgeons, point-of-care coordinators, procurement officers, and product managers across North America, Europe, and Asia-Pacific. Their insights helped us validate installed base estimates, strip consumption ratios, and emerging demand in home-care anticoagulation programs, thereby filling gaps flagged during desk work.

Desk Research

We extracted baseline volumes, device approvals, and patient pools from open datasets such as FDA 510(k) summaries, EMA device registries, the WHO Global Bleeding Disorders Database, United States CMS outpatient claims, and Eurostat surgical procedure files. Trade association releases from bodies like the International Society on Thrombosis and Haemostasis, peer-reviewed journals, and company 10-K filings furnished usage patterns and average selling prices. Paid repositories that Mordor analysts access, including D&B Hoovers for company splits and Questel for patent intensity, supplied additional context. The sources listed illustrate our approach; many other publications were consulted for cross-checks and clarification.

Market-Sizing & Forecasting

A top-down reconstruction begins with global elective and emergency surgery volumes, warfarin and DOAC patient cohorts, and average tests per patient; these demand pools are then priced using region-specific ASPs. Selective bottom-up roll-ups of leading supplier revenues and channel checks act as guardrails that adjust totals within an acceptable variance band. Core model drivers include aging population growth, trauma incidence, adoption rate of viscoelastic platforms, penetration of home self-testing, reagent-to-device attachment ratios, and average analyzer life cycles. Multivariate regression on age-adjusted surgery counts, DOAC prevalence, and healthcare spending forecasts yields the 2025-2030 trajectory. Where supplier revenue splits were incomplete, we imputed values using shipment records and regional price benchmarks disclosed during interviews.

Data Validation & Update Cycle

Outputs pass automated variance screening, senior analyst review, and reconciliation against fresh regulatory filings before sign-off. Reports refresh every twelve months, with interim updates triggered by material events such as major product launches or guideline changes; a final validation round occurs immediately prior to client delivery.

Why Mordor's Point of Care Coagulation Testing Devices Baseline Remains the Most Reliable

Published figures often diverge because firms choose dissimilar device scopes, apply different ASP assumptions, and refresh models on uneven calendars.

Key gap drivers include inclusion of central lab systems, exclusion of consumables, currency treatment, and reliance on unvalidated spend surveys rather than patient-level demand signals. By grounding estimates in procedure counts and verified installed bases, Mordor Intelligence offers a balanced, transparent baseline that decision-makers can reproduce.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 1.65 B (2025) | Mordor Intelligence | - |

| 2.80 B (2024) | Global Consultancy A | Bundles central lab analyzers and service contracts into POC scope |

| 2.33 B (2025) | Regional Consultancy B | Uses constant 2021 exchange rates and limited home care validation |

| 1.84 B (2024) | Trade Journal C | Counts hardware only, omits consumables and software upgrades |

Together, the comparison shows how varying scope and assumptions inflate or deflate totals, while our disciplined variable selection keeps Mordor's numbers firmly anchored and easy to trace.

Key Questions Answered in the Report

What factors are propelling the point of care coagulation testing device market?

Demand is driven by the need for real-time hemostasis data in surgery and emergency care, the rise in DOAC therapy, and the shift toward home-based monitoring that minimizes clinic visits.

Which test type dominates current revenues?

Prothrombin Time/INR testing accounts for 57.02% of 2025 revenue because warfarin remains prevalent and requires frequent INR checks.

Who are the key players in Point Of Care Coagulation Testing Devices Market?

Single-use cartridges and strips deliver 58.10% of 2025 sales, providing predictable, recurring income that cushions manufacturers from capital-equipment cycles.

Which region shows the fastest growth?

Asia-Pacific records a 7.31% CAGR between 2026 and 2031, benefiting from expanding healthcare infrastructure, larger chronic-disease populations, and supportive government initiatives.

What technological trend is gaining adoption in trauma care?

Viscoelastic testing delivers a full clotting profile in under 15 minutes, enabling precise transfusion management and reducing blood-product waste.

What challenges could hamper future growth?

Lower laboratory reimbursement in North America and Europe and a global shortage of technicians skilled in advanced viscoelastic platforms may slow new installations in some facilities.

Page last updated on: