CNC Machines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 79.14 Billion |

| Market Size (2031) | USD 105.70 Billion |

| Growth Rate (2026 - 2031) | 5.96% CAGR |

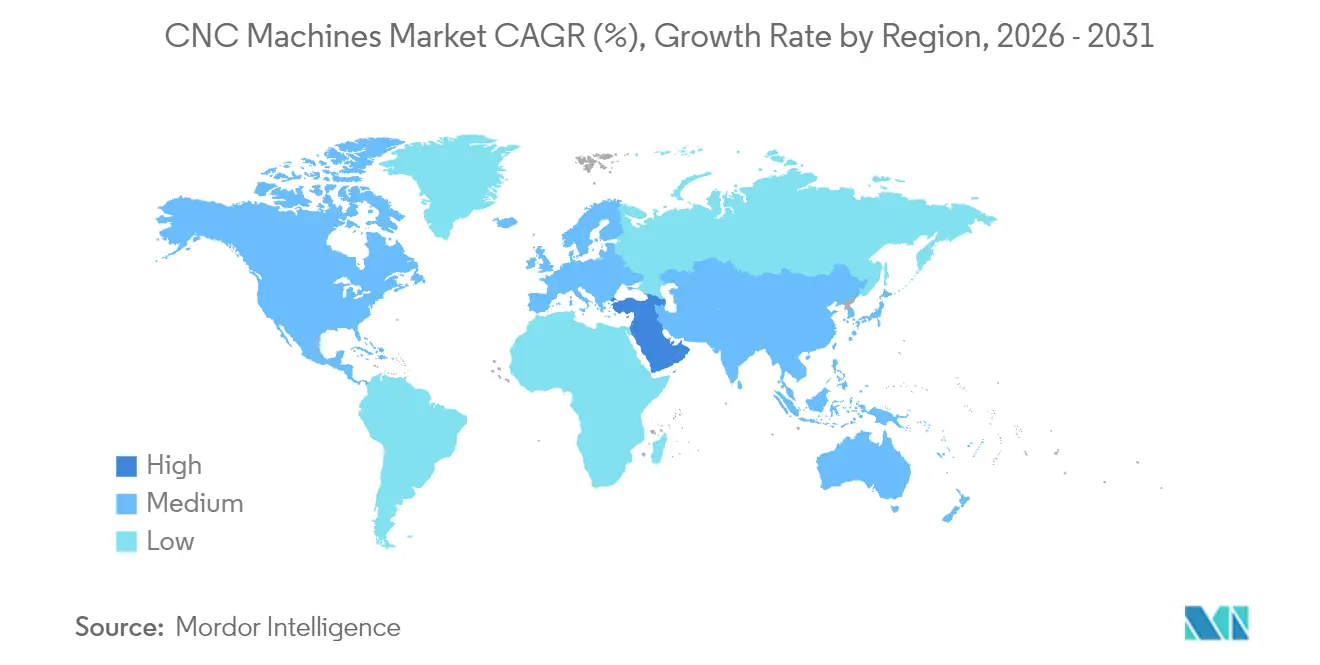

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CNC Machines Market Analysis by Mordor Intelligence

The CNC machine market size is projected to be USD 74.82 billion in 2025, USD 79.14 billion in 2026, and reach USD 105.7 billion by 2031, growing at a CAGR of 5.96% from 2026 to 2031. Strong government incentives for on-shore semiconductor capacity, electrified-mobility supply chains, and aerospace re-equipment programs are steering procurement budgets toward multi-axis, sensor-rich platforms that lift throughput while guarding micron-level tolerances. Digitally fluent job shops are pairing edge analytics with cloud dashboards to predict spindle failure and trim unplanned stops, a shift that converts runtime data into a competitive moat. Hybrid additive-subtractive centers are shortening the distance between near-net and finish machining, improving material yield by roughly one-third for titanium parts. Vendors are also field-testing AI-guided toolpaths that recalibrate feed and speed every 50 milliseconds, cutting cycle time on complex impellers by double digits. Meanwhile, energy-efficient spindle drives and frequency-controlled coolant pumps are becoming table stakes as the European Union counts carbon avoided as seriously as hours saved.

Key Report Takeaways

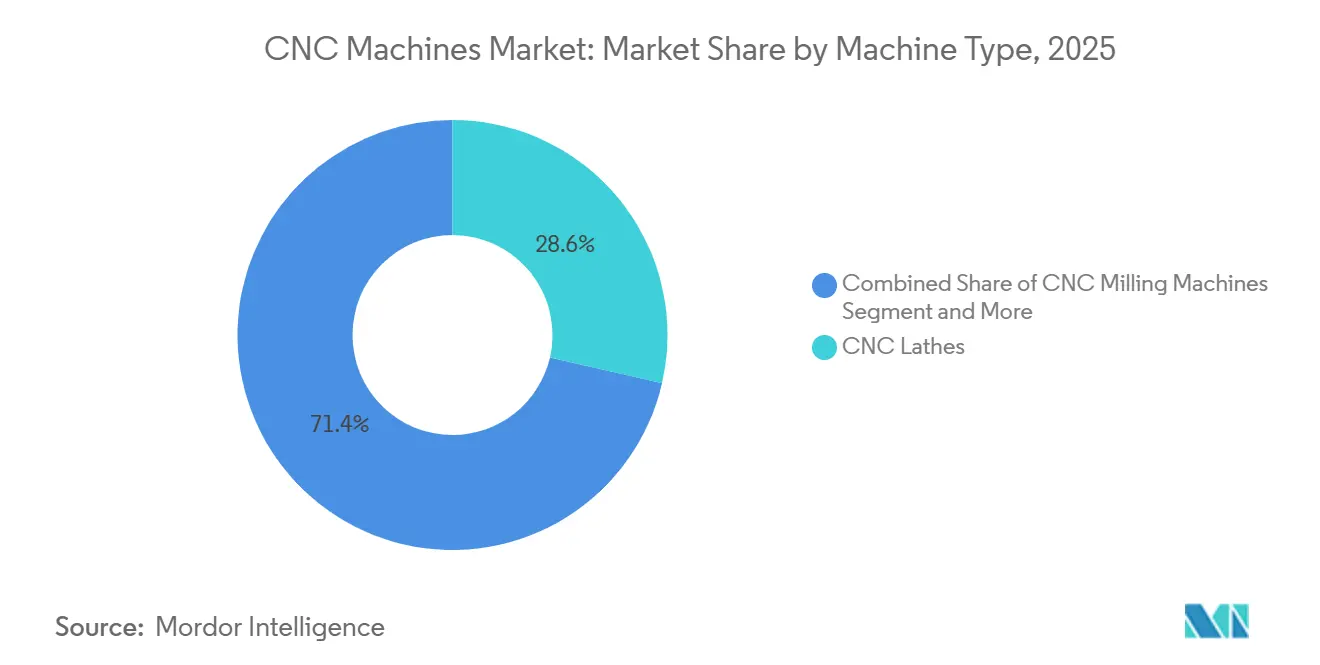

- By machine type, CNC lathes held 28.60% of 2025 revenue, whereas laser cutting units are forecast to expand at a 7.45% CAGR through 2031, making laser the fastest-growing category.

- By axis configuration, 3-axis platforms led with 40.74% of 2025 revenue; 5-axis machines are poised to rise at an 8.25% CAGR through 2031, the quickest pace in this dimension.

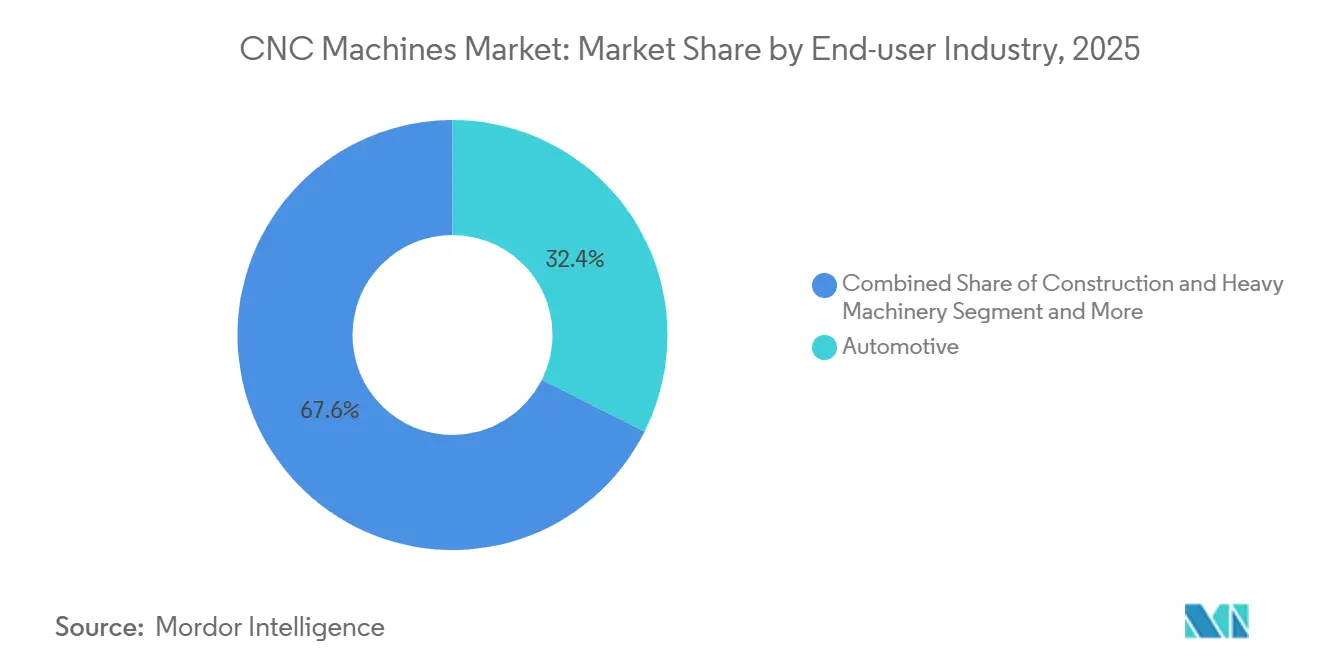

- By end-user, automotive commanded 32.40% of 2025 sales, while medical devices are projected to advance at a 7.15% CAGR to 2031, outpacing every other sector.

- By geography, the Asia-Pacific commanded 45.30% of the 2025 revenue, and the Middle East region is projected to expand at a 6.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global CNC Machines Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industry 4.0-aligned automation upgrades | +1.5% | Global, led by Germany, Japan, South Korea, United States | Long term (≥4 years) |

| Escalating precision demand from EV & aerospace sectors | +1.3% | Global, concentrated in China, United States, Germany, France | Short term (≤2 years) |

| Government subsidies / tax credits for smart-factory modernization | +1.2% | Global, concentrated in North America, EU, China, India | Medium term (2–4 years) |

| Generative-AI CAM enabling real-time adaptive toolpaths | +0.9% | North America, Western Europe, advanced APAC markets | Medium term (2–4 years) |

| Proliferation of hybrid additive-subtractive CNC systems | +0.8% | North America & Europe, spillover to APAC aerospace hubs | Medium term (2–4 years) |

| Carbon-neutral manufacturing mandates spurring energy-efficient CNC retrofits | +0.7% | Europe (EU Green Deal), spillover to APAC and North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Industry 4.0-Aligned Automation Upgrades

Digital twins are moving from PowerPoint to the plant floor. Siemens and DMG MORI embed kinematic models inside SINUMERIK ONE, so a collision check runs before the tool even moves. FANUC’s cloud dashboard predicts spindle failure 72 hours ahead with an 18–22% cut in downtime at automotive beta sites. Standards help: NIST’s 2024 schema specifies uniform tags for vibration, temperature, and axis position, which MTConnect 2.3 now carries to edge gateways. Because data interoperability removes vendor lock-in, machine buyers can layer analytics on top of mixed-brand fleets, a scenario that expands the CNC machine market addressable for retrofit kits.

Escalating Precision Demand From EV and Aerospace Sectors

Battery cases and turbine vanes share a zero-defect mindset that legacy 3-axis mills cannot guarantee. Magna requires battery housings to stay millimeter-flat over two-meter spans; Starrag achieves 0.0001-inch repeatability on nickel superalloy blades with direct-drive rotary axes. Advanced inserts extend tool life by up to 50% at 80 m/min, pulling cost per part below legacy benchmarks. Aerospace and EV primes, therefore, demand 5-axis or grind-hardened centers with on-board thermal compensation. This relentless push for accuracy keeps the CNC machine market tilted toward high-spec platforms with premium service contracts.

Government Subsidies and Tax Credits for Smart-Factory Modernization

Public money is easing balance-sheet strain for mid-tier fabricators that would otherwise postpone upgrades. The U.S. State Manufacturing Leadership Program alone issued more than USD 50 million in 2025 for sensor-instrumented CNC cells, helping recipients shorten payback to under four years.[1]U.S. Department of Energy, “State Manufacturing Leadership Program Awards,” energy.gov In Germany, accelerated depreciation slices the book life of energy-efficient machines to three years, lifting internal-rate-of-return hurdles by roughly 200 basis points. India’s USD 2.3 billion electronics PLI scheme is already underwriting tool purchases for Micron’s and Tata-PSMC’s Gujarat fabs. These carrots collectively thicken the global funnel for replacement and first-time buyers. As the CNC machine market internalizes a lower cost of capital, order backlogs are expected to stretch well into 2027.

Generative-AI CAM Enabling Real-Time Adaptive Toolpaths

Toolpath math is moving from rule-based to probabilistic. Mastercam 2026 tweaks feed every 50 milliseconds, trimming cycle time 10–15% on complex molds. CloudNC trains on 500,000 cuts to pick strategies that squeeze non-cutting moves by a quarter. Autodesk loops topology optimization back into CAD so machinists program two hours instead of eight. ESPRIT EDGE cancels chatter by bumping the spindle speed ±200 rpm when sensors detect 200 Hz vibration. Early adopters gain a margin, widening the technology gap inside the CNC machine market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure & lifecycle costs amplified by 2026 interest-rate environment | -0.9% | Global, acute in North America and Europe | Short term (≤2 years) |

| Persistent skilled CNC programmer/operator shortage despite micro-credential programs | -0.7% | Global, most severe in North America, Germany, Japan | Medium term (2–4 years) |

| Volatile rare-earth magnet prices inflating high-speed spindle bill-of-materials | -0.5% | Global, supply concentrated in China | Short term (≤2 years) |

| Stricter cross-border data/export controls on cloud-connected CNCs limiting global deployments | -0.4% | Global, affecting U.S., EU, China trade corridors | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure and Lifecycle Costs

Equipment leases touched a record USD 11.6 billion in January 2026, yet approval rates slid to 76.8%, hinting that lenders are pricing in default risk. A USD 500,000 5-axis mill now needs 5.5–6 years to break even under 4–5% policy rates, versus four years under the 2024 regime.[2]Federal Reserve Board, “Summary of Economic Projections March 2026,” federalreserve.gov Annual maintenance and tooling can chew through USD 120,000, about a fifth of sticker price. Eurozone buyers feel the pinch as the European Central Bank sits at 3.5%. These economics stall non-critical replacements, tempering short-term growth in the CNC machine market.

Persistent Skilled CNC Programmer and Operator Shortage

Micro-credential boot camps graduate far fewer machinists than openings. The U.S. ACENet program turned out only 420 trainees against 15,000 vacancies in 2025. In Michigan, 40% of certificate holders shift to robotics within two years, chasing better pay and lighter work. Germany’s apprenticeship pipeline offsets merely two-thirds of retirements. Japan’s ≥55-year-old operator share is 38%, and language limits curb Southeast Asian inflows. Labor scarcity therefore caps spindle utilization and slows the CNC machine market in talent-tight regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Lathes Remain Foundational as Laser Cutting Surges

CNC lathes captured 28.60% of 2025 revenue, cementing their role in drive shafts, valve stems, and other rotational parts. Yet laser cutting systems are on track to post a 7.45% CAGR to 2031, the highest among all machine types, as burr-free, low-heat cuts become mandatory for battery-pack enclosures and aluminum aerospace skins. BLM GROUP’s LT-FREE slashed the total cycle from 84 minutes to 31.5 minutes on large-lot tube frames, trimming per-piece cost by 60%. The CNC machine market thus sees lasers moving from sheet-metal job shops into mainstream EV and aviation lines.

Milling, grinding, EDM, and specialty cells keep niche roles. Ultrasonic-assisted units such as DMG MORI’s DMU 20 linear cut sapphire watch cases with 50% less force, opening ceramic and medical markets that grinders once monopolized. Plasma remains cost-effective for >25 mm structural steel, while waterjet and ultrasonic tackle composites and brittle oxides. Although lasers dominate the growth narrative, the breadth of requirements ensures that no single technology will eclipse the variety baked into the CNC machine market.

By Axis Type: 5-Axis Systems Capture Complex Geometries

Three-axis centers owned 40.74% of 2025 revenue, favored by job shops machining prismatic parts at scale. The fastest advance, however, belongs to 5-axis units, forecast to expand at an 8.25% CAGR through 2031 as turbine blades, orthopedic stems, and aerospace brackets demand continuous machining that eliminates re-clamping. DMG MORI’s DMU 60 eVo doubled payload while holding 4 µm circular accuracy, letting suppliers compress impeller lead time from 18 days to six.

Four-axis horizontals still dominate engine blocks and transmission cases, whereas six-axis robots handle very large composites but represent less than 5% of the CNC machine market size for axis-based segmentation. CAM collision-check now simulates holder clearance in real time, shrinking programming errors by almost a third. While 3-axis will remain the volume leader, the migration of high-value work into 5-axis tilts unit mix and average selling price upward within the CNC machine market.

By End-User Industry: Medical Devices Outpace Automotive Growth

Automotive held 32.40% of 2025 sales, supported by engine blocks, gears, and battery trays that reward high-volume, capital-intensive lines. Medical devices, though smaller today, will climb at a 7.15% CAGR to 2031, the quickest among end users, driven by aging populations and tighter ISO 13485 traceability rules. Micron Products sustains ±0.0005-inch on titanium hip stems thanks to coolant-temperature control and sub-micron feedback loops.

Aerospace and defense continue to demand nickel superalloys cut at >80 m/min while meeting ±0.008 mm, an environment suited to torque-motor 5-axis horizontals. Electronics fabs require micro-machining below 100 µm for wafer-handling robots, steering investment toward ultrasonic and laser micromachining cells. Construction, heavy machinery, and general job shops round out demand with lower-tolerance work. The mix shift toward implants and surgical tools means higher margin potential but also stricter regulatory audits, factors reshaping the CNC machine market share distribution across industries.

Geography Analysis

Asia-Pacific ruled with 45.30% of 2025 revenue as China supplied roughly 40% of global machine-tool output and India’s production-linked incentives funneled USD 15 billion into semiconductor fabs that rely on high-precision cutting. ASEAN nations lured near-shoring auto and electronics projects, with Thailand approving 87 CNC-heavy investments worth USD 4.2 billion in 2025.[3]Thailand Board of Investment, “2025 Approved Projects,” boi.go.th Japan and South Korea channeled R&D into predictive-maintenance dashboards, and Australia’s AUKUS submarine deal demanded titanium hull machining. These currents ensure the CNC machine market size in Asia-Pacific continues to widen its absolute lead despite cooling Chinese construction.

North America held a mid-20% slice, reinforced by the CHIPS and Science Act’s USD 52.7 billion fund. Intel, TSMC, and Samsung collectively exceed USD 100 billion in fab builds, each project embedding hundreds of CNC cells for wafer-handling robotics. Haas Automation will open a USD 400 million Nevada complex by late 2026, adding 1.4 million ft² of domestic capacity. Mexico’s 18% year-on-year jump in CNC imports underscores a near-shoring boom. Canada’s aerospace corridor continues to secure 5-axis horizontals for engine core work.

Europe maintained high-teen share amid energy price headwinds. Carbon-neutral rules accelerate retrofit demand; single-pump coolant systems that save 30% electricity qualify for three-year write-offs. The Middle East is the fastest riser at 6.75% CAGR through 2031 as Saudi Vision 2035 seeks 25% manufacturing GDP share and the UAE targets USD 81.7 billion industrial output,. Siemens’ digital twin roll-out across Saudi industrial cities turns efficiency into league tables, spurring new orders. South America, led by Brazil, feeds regional auto and ag-equipment lines, while Africa’s modest but rising CNC demand ties to Chinese-financed rail and mining builds.

Competitive Landscape

Competition is moderate to high: the top seven brands, such as FANUC, DMG MORI, Haas Automation, Okuma, Mitsubishi Electric, Siemens, and Yamazaki Mazak, own a mid-40% slice, leaving room for regional champions and software-first entrants. DN Solutions moved to acquire HELLER in August 2025, folding 4-axis and 5-axis expertise into a turnkey portfolio built for European cell automation. The strategy hints that size and scope now trump pure spindle count as buyers favor bundled hardware-software stacks.

Incumbents double down on digital layers. FANUC’s Smart Digital Twin Manager and Siemens’ SINUMERIK ONE embed condition monitoring at the controller, enabling 18–22% uptime gains in pilot runs. Meanwhile, CloudNC offers cloud-native toolpaths that can ride any ISO controller, staking a claim that software, not iron, will define future edge. Additive-hybrids remain a white space with fewer than a dozen commercialized platforms, giving newcomers room to carve a share in the CNC machine market.

Export controls complicate playbooks. Haas paid USD 2.5 million in 2024 over Entity-List lapses, prompting OEMs to run parallel SKUs for U.S., EU, and China markets. Magnet price spikes forced redesign toward reluctance motors at sub-25 krpm, threatening high-speed niches. Vendors that integrate AI-toolpaths, pallet automation, and energy dashboards into one invoice are likely to outpace metal-only rivals as the CNC machine market rewards ecosystem depth over standalone speed.

CNC Machines Industry Leaders

FANUC Corporation

DMG Mori Co. Ltd

Haas Automation Inc.

Okuma Corporation

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: PMGC Holdings bought SVM Machining for USD 2.25 million to flesh out a multi-site aerospace and medical platform.

- January 2026: DMG MORI rolled out the Automation Control Station, unifying pallet, robot, and tool loaders under one 19-inch panel to cut setup time 15–20%.

- January 2026: DMG MORI unveiled Robo2Go Generation 3 with 70 kg payload and three-pallet option, extending unattended runtime for batch lots.

- January 2026: DMG MORI shipped the CTX 450 4A twin-spindle lathe delivering full 6-sided machining inside a 10.8 m² footprint.

Global CNC Machines Market Report Scope

| CNC Lathes |

| CNC Milling Machines |

| CNC Laser Cutting Machines |

| CNC Plasma Cutters |

| CNC EDM (Die-sink & Wire) |

| CNC Grinding Machines |

| CNC Drilling/Tapping Centers |

| Other Specialty CNC Machines |

| 3-Axis Machines |

| 4-Axis Machines |

| 5-Axis Machines |

| 6-Axis & Above |

| Automotive |

| Aerospace & Defense |

| Electronics & Semiconductor |

| Medical Devices |

| Construction & Heavy Machinery |

| Power & Energy |

| Shipbuilding |

| General Manufacturing & Job Shops |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Peru | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Turkey | |

| Egypt | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Machine Type | CNC Lathes | |

| CNC Milling Machines | ||

| CNC Laser Cutting Machines | ||

| CNC Plasma Cutters | ||

| CNC EDM (Die-sink & Wire) | ||

| CNC Grinding Machines | ||

| CNC Drilling/Tapping Centers | ||

| Other Specialty CNC Machines | ||

| By Axis Type | 3-Axis Machines | |

| 4-Axis Machines | ||

| 5-Axis Machines | ||

| 6-Axis & Above | ||

| By End-user Industry | Automotive | |

| Aerospace & Defense | ||

| Electronics & Semiconductor | ||

| Medical Devices | ||

| Construction & Heavy Machinery | ||

| Power & Energy | ||

| Shipbuilding | ||

| General Manufacturing & Job Shops | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the global CNC machine market be by 2031?

By 2031, the forecast projects a reach of USD 105.7 billion, growing at a CAGR of 5.96% from 2026 to 2031.

Which machine type is growing fastest?

CNC laser cutting systems are projected to advance at a 7.45% CAGR through 2031 as EV battery cases and aerospace skins demand burr-free cuts.

Why are 5-axis machining centers gaining share?

They eliminate re-clamping, improve surface accuracy, and handle complex turbine and medical geometries, driving their 8.25% CAGR to 2031.

What is the main restraint on new CNC investments in 2026?

Elevated interest rates push payback periods beyond five years, dampening short-term equipment purchases despite record leasing volume.

Which region shows the fastest growth?

The Middle East, led by Saudi Arabia and the UAE, is set to grow at a 6.75% CAGR through 2031 on the back of industrial diversification programs.

How are AI toolpaths changing shop economics?

Generative-AI CAM trims cycle times by up to 15%, lifting spindle utilization and allowing digitally adept shops to command premium margins.

Page last updated on: