Kennel Management Software Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.97 Billion |

| Market Size (2031) | USD 3.86 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

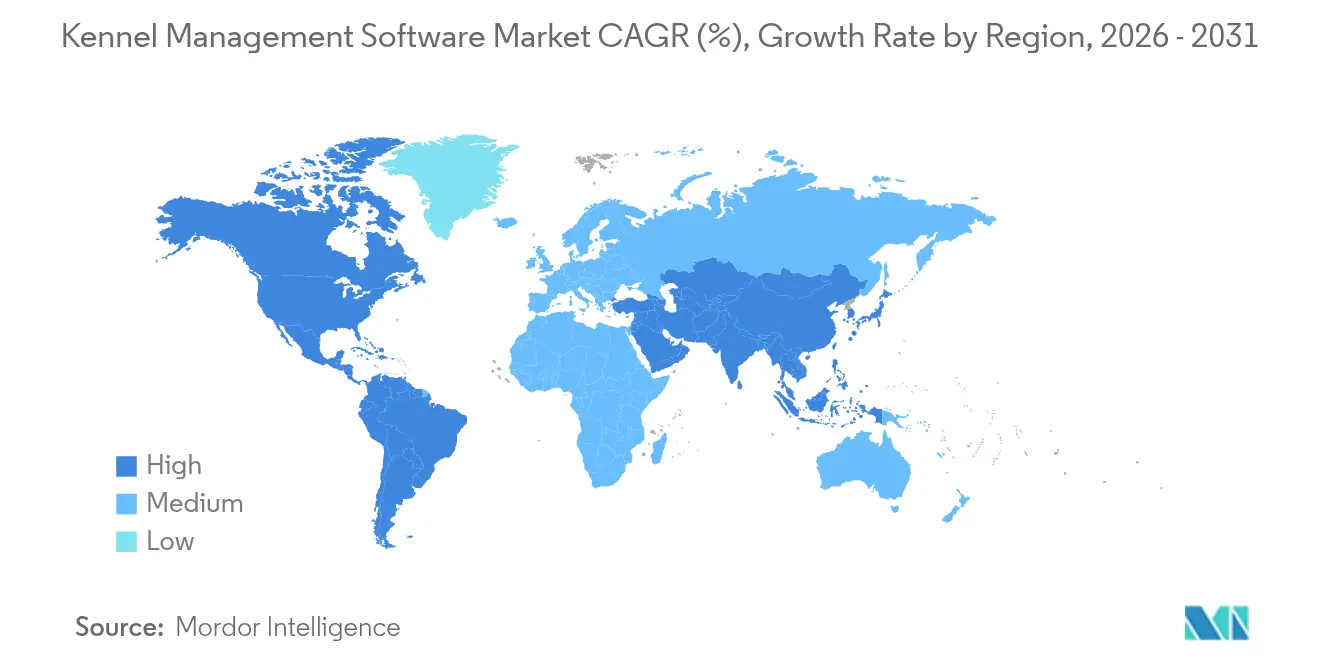

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

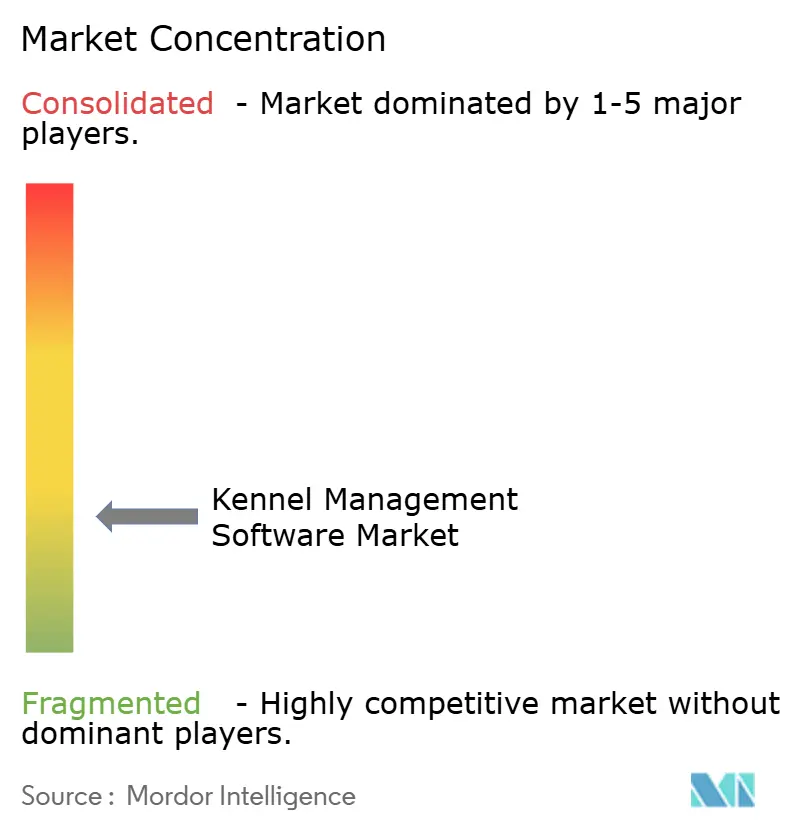

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Kennel Management Software Market Analysis by Mordor Intelligence

Kennel management software market size in 2026 is estimated at USD 2.97 billion, growing from 2025 value of USD 2.82 billion with 2031 projections showing USD 3.86 billion, growing at 5.36% CAGR over 2026-2031. Sustained digitization of pet‐care operations, strengthened by cloud-first architectures and artificial-intelligence modules, keeps the growth trajectory intact. Regulatory mandates that force deeper animal-welfare record keeping continue to accelerate purchase cycles, particularly among micro-kennels looking to professionalize services. Vendors that embed payment gateways and insurance APIs in their platforms capture measurable wallet share as facilities seek all-in-one systems. Headwinds still persist from data-security anxieties and the high switching costs of spreadsheets, but subscription pricing that aligns cost with usage is lowering resistance across all enterprise sizes.

Key Report Takeaways

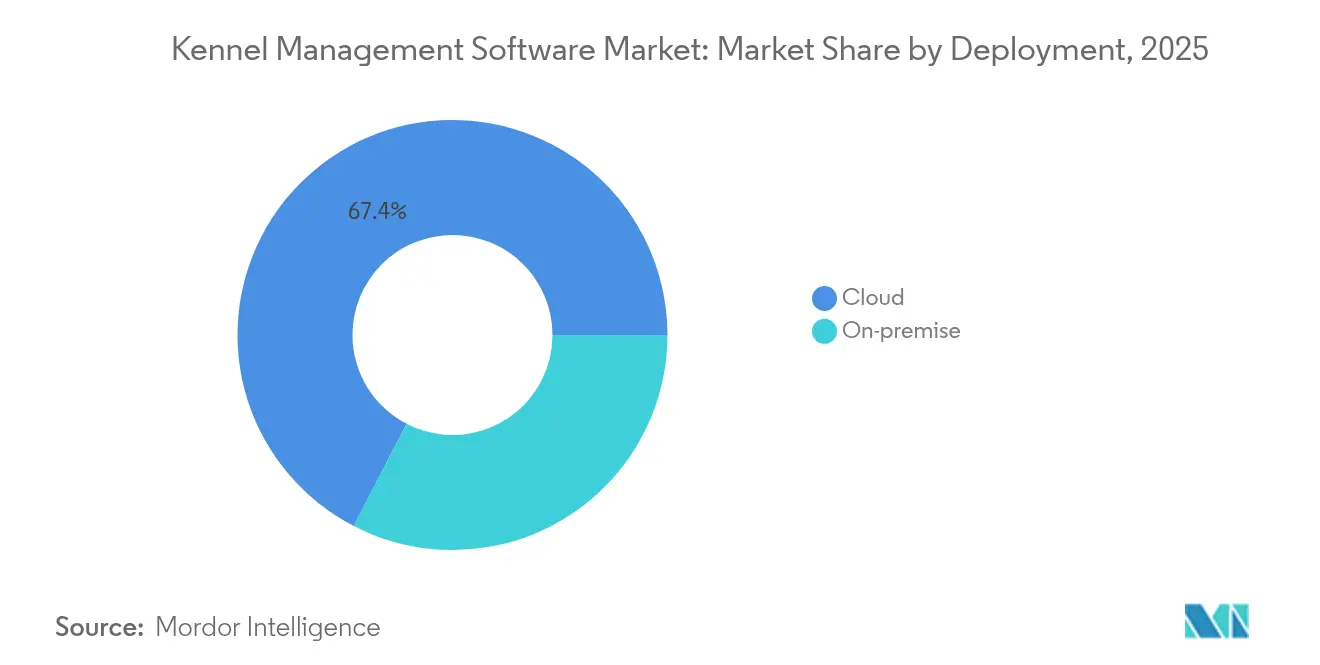

- By deployment, cloud platforms commanded 67.40% of the kennel management software market share in 2025 and are expanding at a 6.31% CAGR to 2031.

- By end-user, boarding and daycare facilities held 45.30% revenue share in 2025, while veterinary boarding is forecast to grow at 7.10% CAGR through 2031.

- By enterprise size, small facilities with 10-49 runs led with a 40.40% share in 2025; micro-kennels (<10 runs) recorded the highest 6.71% growth outlook.

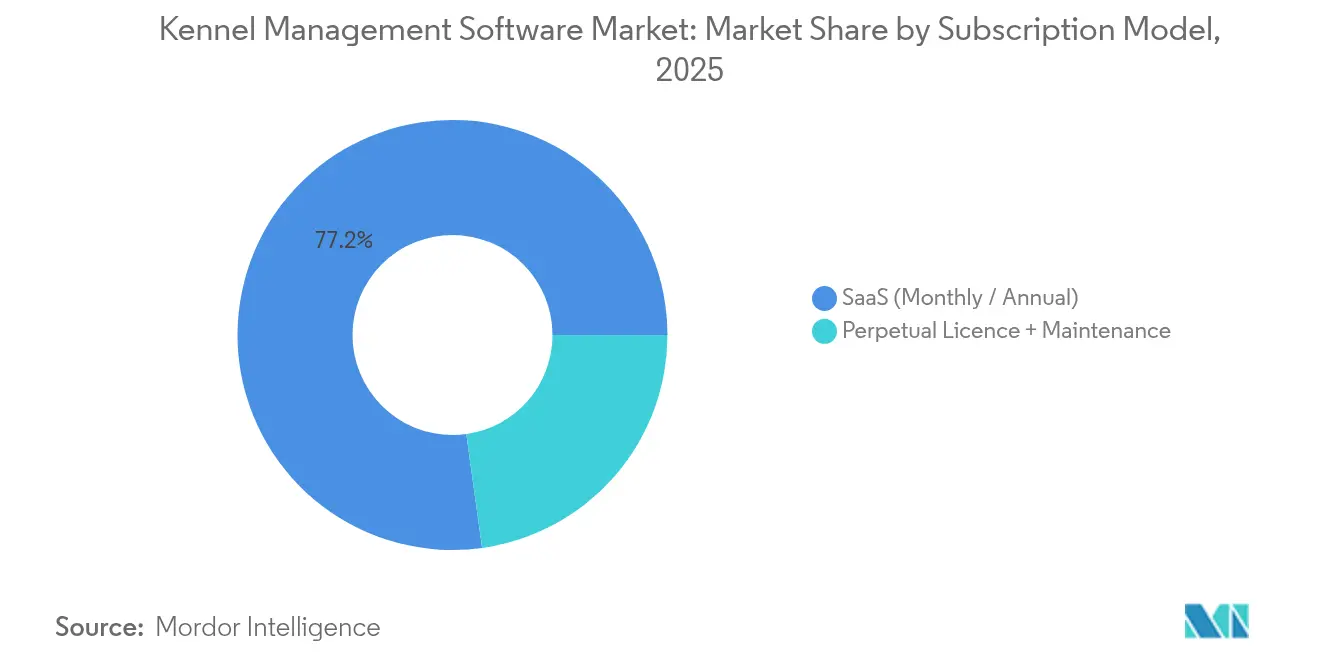

- By subscription model, SaaS agreements captured 77.20% of the kennel management software market size in 2025 and are advancing 6.82% to 2031.

- By geography, North America held a 39.40% share in 2025; Asia-Pacific exhibits the fastest 7.20% CAGR.

- IDEXX, Togetherwork, and Zoetis collectively controlled 18% market share in 2025, reflecting a fragmented competitive field.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Kennel Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising pet ownership & spending | +1.2% | Global; strongest in APAC & North America | Medium term (2–4 years) |

| SaaS uptake across facilities | +0.9% | North America & Europe lead | Short term (≤ 2 years) |

| Integrated payment & CRM demand | +0.7% | North America; growing in Europe & APAC | Medium term (2–4 years) |

| AI-based capacity analytics | +0.6% | North America & Europe | Long term (≥ 4 years) |

| Embedded pet-insurance APIs | +0.4% | North America mainly | Long term (≥ 4 years) |

| Hybrid workplace bolstering daycare | +0.5% | Urban North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Pet Ownership & Spending

Urban pet humanization pushes facilities to digitize every touchpoint so that owners receive hotel-grade experiences. Asia–Pacific pet-care spending is on track to reach USD 34.8 billion in 2029, sustaining demand for platforms that document premium services. In Japan, lifetime dog-ownership costs climbed to JPY 2.446 million (USD 16,000) in 2023, affirming willingness to pay for value-added care tracking.[1]Ohmae Graduate School, “Domestic Pet Market,” ohmae.ac.jp Younger digital-native owners select kennels that offer mobile bookings and live pet updates, which in turn expands the kennel management software market.

Rapid Shift to SaaS-Based Deployment

Subscription models remove the capital hurdle that once blocked software investment for small operators. The European companion-animal segment, moving from USD 3.96 billion in 2022 to USD 5.37 billion by 2027, provides fertile ground for cloud rollouts.[2]EuroDev, “Exploring the Veterinary Industry in Europe,” eurodev.comContinuous upgrades, bundled compliance, and device-agnostic access have normalized SaaS as the default procurement path, intensifying competitive differentiation on user experience rather than price.

Demand for Integrated Payment & CRM Suites

Operators now expect bundled billing, loyalty, and marketing functions inside one pane of glass. PetExec’s Stripe integration, which automates recurring invoices and SMS reminders, exemplifies the push to become a full operating stack rather than a booking calendar. Cross-selling grooming, retail, and daycare services through unified CRM screens tightens retention and lifts average revenue per customer.

Need for Real-Time Capacity & Run-Utilisation Analytics (AI-Driven)

Facilities use AI to shift from static reservations to predictive occupancy optimization. The industry’s acceptance of clinical AI, underscored by Zoetis’ Vetscan Imagyst adoption, legitimizes algorithmic decision support in boarding environments. Dynamic pricing tied to demand curves delivers margin protection during peak periods and boosts run utilization on low-traffic days.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low digital literacy among micro-kennels | -0.8% | Global; higher in rural & emerging markets | Medium term (2–4 years) |

| Data-security & PII compliance burdens | -0.6% | Europe & North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Digital Literacy Among Micro-Kennel Operators

Many micro-facilities run on family labor and informal scheduling, limiting appetite for enterprise software. Sixty-six percent of pet owners in Japan delay veterinary visits due to perceived cost, while 41% cite time constraints, hinting at operators’ sensitivity to workflow complexity. Training clinics on basic system navigation remain costly, restraining penetration even as the segment shows 6.80% CAGR potential.

Data-Security & PII-Compliance Concerns

GDPR in Europe and diverse state privacy statutes in the United States impose stringent record-handling rules. The American Veterinary Medical Association highlights veterinary practices’ duty to guard client data, raising vendor development costs for encryption, consent capture, and audit trails.[3]American Veterinary Medical Association, “VSG-AVMA Principles of Veterinary Data Ownership & Stewardship,” avma.org Smaller kennels hesitate to migrate to shared-cloud environments until vendors prove robust protection and indemnity frameworks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Dominance Reshapes Market Access

Cloud platforms accounted for 67.40% of the kennel management software market in 2025 and are forecast to expand at a 6.31% CAGR. The shift reflects lower upfront spending, seamless integrations, and automatic regulatory updates. Multi-location chains benefit from centralized dashboards that standardize SOPs across sites. Meanwhile, on-premise solutions linger within large hospitals, demanding local data custody but face shrinking refresh budgets. Vendors that demonstrate ISO-27001 and SOC-2 compliance accelerate conversions among late adopters. As a result, cloud continues to expand wallet share and strengthens the overall kennel management software market position.

On-premise systems still serve niche scenarios such as rural areas with inconsistent bandwidth. However, the total cost of ownership rises as aging hardware requires replacement. Security patches become cumbersome without managed services, creating vulnerabilities that regulators scrutinize. Over time, life-cycle economics favor migration, reinforcing the long-term dominance of cloud in the kennel management software market.

By End-User Type: Veterinary Boarding Drives Premium Growth

Boarding and daycare facilities generated 45.30% revenue in 2025, validating their role as the core demand engine. These operators value rapid check-in workflows and mobile updates that reassure owners. Veterinary boarding, although only 11.70% share in 2025, is projected to rise at 7.10% CAGR as medical oversight merges with hospitality. Integrated electronic health records, medication alerts, and post-operative monitoring capabilities influence purchase decisions, positioning software as clinical infrastructure, not merely scheduling support.

Grooming salons and pet retail chains are leveraging CRM modules to upsell spa packages and merchandise. Home-based sitters demand mobile-first tools with quick-tap invoicing. Their growth reveals that even solo operators recognize software’s branding and compliance benefits. The kennel management software market continues to diversify in response to these varying workflows.

By Enterprise Size: Micro Facilities Embrace Digital Transformation

Small enterprises with 10-49 runs led at 40.40% in 2025, reflecting a sweet spot where operational complexity requires automation. Micro facilities (<10 runs) are the fastest climbers, growing 6.71% annually as low-code onboarding and freemium tiers remove the barrier to entry. Medium enterprises (50-199 runs) prioritize API flexibility to link accounting and HR stacks, while chains exceeding 200 runs negotiate enterprise contracts that bundle training and 24/7 support.

For micro-operators, the principal hurdle is digital literacy, yet user-interface simplification and tutorial videos mitigate friction. Payment reconciliation and auto-reminders deliver immediate cash-flow benefits, justifying subscription fees. This grassroots adoption fortifies the long-term breadth of the kennel management software market.

By Subscription Model: SaaS Transformation Accelerates

SaaS contracts captured 77.20% share in 2025 and deliver 6.82% CAGR through 2031. Predictable monthly fees align expenditures with revenue and keep functionality current without manual upgrades. Upsell paths-additional users, integration packs, analytics dashboards-extend customer lifetime value. Perpetual licenses shrink as CFOs switch from capex to opex flexibility.

BarkBox’s 95% subscription retention in pet products illustrates consumer comfort with recurring payments, indirectly educating kennel owners to adopt similar models. Maintenance-charged perpetual deals will persist only in highly customized multi-site environments where internal IT resources already exist.

By Sales Channel: Direct Engagement Builds Customer Relationships

Direct vendor sales dominate with a share of 66.60% in 2025 because they provide full control over demos, onboarding, and support, which is critical when workflows affect animal welfare. Marketplace listings and reseller networks serve long-tail customers seeking local advocates or price shopping are growing at a 6.41% CAGR through 2031. VARs in Asia-Pacific often bundle translation and localized payment gateways, lowering adoption friction. Digital content-webinars, ROI calculators, and case studies-augments lead generation, creating an inbound flywheel. Overall, blended channels ensure the kennel management software market captures demand across experience levels and economic contexts.

Marketplace platforms promoted by veterinary associations foster trust through peer endorsements. Their ranking algorithms, based on verified reviews, pressure vendors to continually elevate customer success metrics. Consequently, direct and indirect channels coexist, each matching distinct buyer personas and budget profiles.

Geography Analysis

North America retained a 39.40% share in 2025, sustained by high pet ownership and well-funded veterinary ecosystems. The United States hosts dense boarding chains that require HIPAA-like record rigor, propelling premium feature uptake. Canada’s pet-food export surge hints at wider sector maturity, indirectly increasing demand for facility software. Regional state privacy regulations keep data-security modules top of mind for buyers, enhancing vendor stickiness. Cross-border mergers produce consolidated chains that standardize on a single platform to leverage economies of scale, further deepening the kennel management software market.

Europe follows as the second-largest region, benefiting from established veterinary care frameworks and robust broadband penetration. Companion-animal health spending is climbing toward USD 5.37 billion by 2027, underpinning steady software conversion. GDPR compels detailed consent tracking, spurring demand for audit trails and encrypted backups. Germany, France, and the United Kingdom spearhead adoption, while Nordic countries emphasize sustainability reporting on the same platforms. Cross-functional modules that couple inventory with prescription labeling deliver compliance efficiencies, making software indispensable rather than discretionary.

Asia-Pacific is the growth engine with 7.20% CAGR through 2031. Japan’s pet population exceeded 15.9 million in 2024, sustaining facility investments in digital infrastructure. China’s Tier-1 cities introduce licensing that mandates electronic welfare logs, accelerating SaaS penetration. South Korea and Singapore, known for the quick adoption of fintech, show enthusiasm for payment-embedded kennel platforms. Localized interfaces and integration with regional e-wallets become decisive factors as Western vendors localize offerings. With disposable incomes rising and urban dwellers prioritizing pet wellness, Asia-Pacific has the potential to overtake North America in the kennel management software market revenue by the early 2030s.

Regulatory Landscape

Kennel management software vendors operate at the intersection of animal-welfare recordkeeping and personal-data protection, which pushes product requirements beyond scheduling into auditable documentation and secure retention. In England, the Animal Welfare (Licensing of Activities Involving Animals) (England) Regulations 2018, supported by GOV.UK statutory guidance for local authorities, require licensed dog-boarding operators to keep registers that can include vaccination and treatment information and be available for inspection. This drives demand for standardized intake, alerts, and searchable logs.

In the United States, federal recordkeeping duties under the Animal Welfare Act framework (7 U.S.C. Section 2140) and USDA regulations (including 9 CFR provisions used for inspection and oversight) reinforce the need for traceable identification and history for dogs and cats handled by covered entities. Additional state and local rules can add building, fire, and public health compliance layers (for example, Connecticut Department of Agriculture standards for commercial kennels). On the data side, facilities using software-based booking and CRM functions must align with privacy regimes such as UK GDPR and the Data Protection Act 2018, GDPR in the EU, and state privacy statutes such as the California Consumer Privacy Act. Buyers therefore expect consent capture, role-based access, encryption, and vendor data-processing agreements in cloud deployments.

Value Chain Analysis

Value creation starts with product and workflow design by kennel management software vendors, then extends through cloud hosting, integration tooling, payments, and go-to-market delivery. Vendors typically build SaaS applications on hyperscale infrastructure (for example, AWS and Azure), monetize via subscriptions and add-ons, and expand ARPU through embedded payments and communications. Downstream, direct sales and onboarding partners implement configuration, data migration from spreadsheets or legacy tools, and staff training, followed by ongoing support and feature updates.

Interoperability with veterinary and practice information management systems is a key value-chain differentiator. Vendors often use REST APIs and webhooks, supported by integration layers or middleware (for example, DataHub Vet), to bridge proprietary schemas and normalize data exchange for vaccination verification, client identity, and visit history. Consolidation and platform bundling also shape the chain: Togetherwork acquired PetExec in December 2024 to deepen payments and software reach across pet-care workflows, and IDEXX acquired ezyVet in June 2025, reinforcing vertical integration between diagnostics, practice management, and adjacent operational scheduling. Bottlenecks tend to concentrate around fragmented PIMS data models, PCI-aligned payment routing, and region-specific privacy and data-residency requirements, which increase implementation complexity for multi-location operators.

Competitive Landscape

The market remains moderately fragmented; the top five suppliers control about 28% revenue, leaving ample space for niche innovators. IDEXX’s June 2025 purchase of ezyVet illustrates a vertical-integration play that fuses diagnostics with practice management to create a defensible ecosystem. Togetherwork’s December 2024 acquisition of PetExec broadens payment reach, signaling consolidation around embedded finance. Zoetis, while focused on therapeutics, invests in AI tools that dovetail into scheduling platforms, demonstrating convergence between healthcare and operations.

Technology differentiation centers on open APIs, mobile UX, and AI-driven insight layers. Vendors that accelerate feature cadence through continuous-deployment pipelines lock in client loyalty. Strategic alliances with payment networks and insurers create new revenue lines while erecting switching barriers. Conversely, data-ownership concerns keep negotiation leverage with customers, particularly in Europe. To win micro-kennels, entrants position stripped-down, modular offerings with transparent pricing, while incumbents upsell enterprise analytics to chains. Overall, strategic M&A, API ecosystems, and embedded finance define the competitive chessboard for the kennel management software market.

Kennel Management Software Industry Leaders

-

PetExec Inc.

-

DaySmart Software (incl. Gingr)

-

Shepherd Software

-

Software Revolutions Ltd (Revelation Pets)

-

Pawfinity

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major whitespace is compliance-led automation that reduces manual effort while producing inspection-ready records across jurisdictions. Features that translate animal-welfare licensing needs into configurable digital workflows (vaccination and treatment capture, automated reminders, audit trails, incident logs, and configurable retention policies) address operational friction tied to GDPR and the patchwork of US state rules, especially for small and micro facilities that struggle with documentation discipline.

Integration-led operating stacks also represent a tangible opportunity, combining booking, payments, CRM, and veterinary data synchronization within one workflow. Evidence of ecosystem investment includes Pets at Home adopting Salesforce Financial Services Cloud (June 2026) to connect insurance and service operations across its retail and veterinary footprint, reinforcing the market shift toward connected customer and service journeys. The December 2024 Togetherwork acquisition of PetExec and the June 2025 IDEXX acquisition of ezyVet similarly highlight active buyer appetite for unified platforms and open-API ecosystems. This creates room for vendors that package prebuilt connectors (PIMS, payments, messaging) and offer tiered modules that let facilities adopt incrementally without replacing their entire toolchain at once.

Recent Industry Developments

- June 2026: Pets at Home expanded its connected pet-care ecosystem by using Salesforce Financial Services Cloud to integrate insurance services, claims management, and service operations with its retail and veterinary systems. The update reinforces demand for kennel and boarding software that can share client identity, consents, and service history across multiple lines of business, raising the bar for API maturity and data governance.

- October 2025: DaySmart Software introduced Practical AI capabilities aimed at improving small business efficiency within its platform portfolio. Adding embedded AI features supports the market shift toward automation in scheduling, communications, and back-office tasks, and increases competitive pressure for other vendors to ship similar productivity layers inside SaaS subscriptions.

- December 2024: Togetherwork acquired PetExec to expand its footprint in pet-care software and payments solutions. The deal strengthened Togetherwork’s ability to bundle kennel operations with an embedded payments stack, intensifying consolidation dynamics and raising switching costs for facilities that standardize on a single vendor for booking, billing, and client management.

Research Methodology Framework and Report Scope

Market Definition and Coverage

The kennel management software market is the revenue earned from software used by pet care facilities to run daily operations, such as booking, pet and client records, invoicing, payments, and staff scheduling, across cloud and on-premise delivery.

Scope exclusions: We exclude general veterinary practice management tools that only store clinical records and do not support boarding or daycare workflows.

Segmentation Overview

-

By Deployment

- Cloud

- On-premise

-

By End-User Type

- Boarding and Daycare Facilities

- Grooming Salons

- Pet Retail and Multi-Service Chains

- Veterinary / Medical Boarding

- Home-based Sitters

-

By Enterprise Size

- Micro (<10 runs)

- Small (10-49 runs)

- Medium (50-199 runs)

- Large (200+ runs / multi-site)

-

By Subscription Model

- SaaS (Monthly / Annual)

- Perpetual Licence + Maintenance

-

By Sales Channel

- Direct (Vendor-Hosted)

- Value-Added Reseller / Marketplace

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Nordics

- Benelux

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN 5

- Australia and NZ

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- Turkey

- South Africa

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

To set the market frame, we rely on public sources that show where demand is building and how pet care businesses are changing. Helpful inputs include official business statistics such as the US Census Bureau, labor and wage series such as the US Bureau of Labor Statistics, and international macro series such as the World Bank and OECD for spend and small business activity.

We also review industry and regulatory references that indicate service volumes and operating norms, including USDA-APHIS guidance and data where boarding rules apply. We add association publications and reputable press that track pet care services and digital adoption. For supplier-side context, we use company filings and investor presentations where available, and we supplement with a paid subscription focused on company financials and news to check revenue mixes and expansion signals. This desk research list is illustrative, and many other public sources were reviewed to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Next, we validate what we learned with interviews and short surveys with software providers, channel partners, and end users such as kennel operators, daycare managers, and multi-site pet care groups. Because buying patterns vary by region and by facility size, we cover APAC, EMEA, and the Americas, and we ask about subscription pricing, typical module bundles, churn behavior, and decision timelines so we can tighten assumptions that are not visible in public data.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | APAC: 42% |

| Mid tier: 45% | Functional/Unit leaders: 40% | EMEA: 36% |

| Smaller Players: 19% | Managers: 47% | Americas: 22% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build that links the count of addressable pet care facilities to software adoption and typical annual spending. We use signals such as the number of pet boarding and daycare locations, multi-site rollout activity, cloud subscription penetration, average users per site, and observed price points for core modules like reservations, billing, and client communications. These inputs translate into an annual value estimate.

Those totals are then checked with selective bottom-up approximations. We sanity-check the result using sampled supplier revenues, publicly visible plan pricing, and channel feedback on average contract value and renewal rates. When direct facility counts are patchy in a country, we use proxy indicators such as small business density and pet services activity, and we stress-test assumptions using primary feedback.

For forecasting, we run scenario analysis so adoption and price uplift can move differently under steady, faster, and slower digitization cases. The forward curve is anchored to expected facility growth, mobile-first workflow adoption, and the pace of product upgrades that tend to shift customers into higher priced tiers over time.

Data Validation & Update Cycle

Validation is done through repeated checks across the model, the inputs, and the final outputs. We compare implied spending per facility against interview ranges, review year-over-year jumps for pricing or adoption that look unusual, and then recheck the assumptions that drive the variance before final sign-off.

A second analyst review is completed for the math, the logic, and the consistency of definitions across regions. The report is refreshed annually, and interim updates are made when material events occur, such as major pricing changes, policy shifts affecting boarding operations, or sharp demand changes. Before delivery, a final pass is done so clients receive the most recently updated view.

Mordor Intelligence's Kennel Management Software Market Size Versus Other Published Estimates

Published numbers for this market can look far apart because each publisher draws the scope line differently and also makes different assumptions on subscription pricing and who is counted as a true kennel software user.

The main gap comes from whether vendor services, broad veterinary clinic software, and non-kennel pet tools are bundled into the same total. Mordor Intelligence counts commercially licensed platforms used for boarding and daycare operations, and excludes systems that only manage clinical records without those workflows.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.97 B (2026) | |

| Industry Research Publisher A | USD 3.10 B (2024) | Uses an earlier base year and a broader definition that explicitly includes services and adjacent end users like veterinary clinics and shelters, which can lift the total beyond boarding and daycare focused spend. |

| Market Intelligence Publisher B | USD 445.86 M (2025) | Appears to stay closer to a narrower software-only revenue pool and may undercount multi-site facility deployments or broader module bundles, which can compress the spend per facility in the modeled total. |

Looking at the three figures together, the spread is mainly explained by scope and by the assumed average annual spend per facility. When the market is kept tied to boarding and daycare operations and cross-checked against adoption and pricing signals, the output becomes easier to reconcile and repeat year to year.

Key Questions Answered in the Report

What is the current size of the kennel management software market?

The kennel management software market stands at USD 2.97 billion in 2026 and is projected to reach USD 3.86 billion by 2031.

Which deployment model holds the largest share?

Cloud deployment leads with 67.40% share in 2025 and is expanding at a 6.31% CAGR through 2031.

Which region is growing fastest?

Asia-Pacific records the highest 7.20% CAGR, propelled by rising pet ownership and digitization across boarding facilities.

Who are the key consolidators shaping the market?

IDEXX, Togetherwork, and Zoetis are prominent consolidators, using acquisitions and AI investments to build integrated ecosystems.

What restrains software adoption among micro-kennels?

Low digital literacy and data-privacy compliance concerns slow uptake, especially in rural and emerging markets.

How do SaaS models benefit kennel operators?

Subscription pricing converts capex into opex, delivers continuous feature updates, and bundles compliance support, improving ROI for facilities of all sizes.

Page last updated on: