Cloud Migration Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

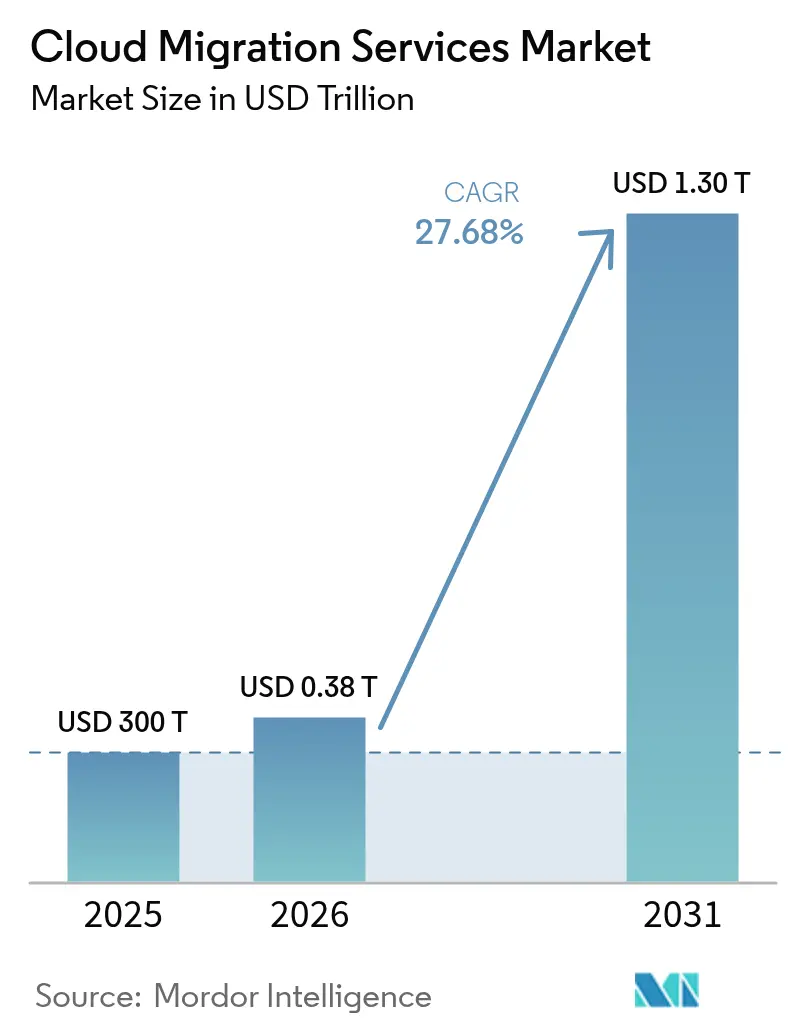

| Market Size (2026) | USD 0.38 Trillion |

| Market Size (2031) | USD 1.3 Trillion |

| Growth Rate (2026 - 2031) | 27.68% CAGR |

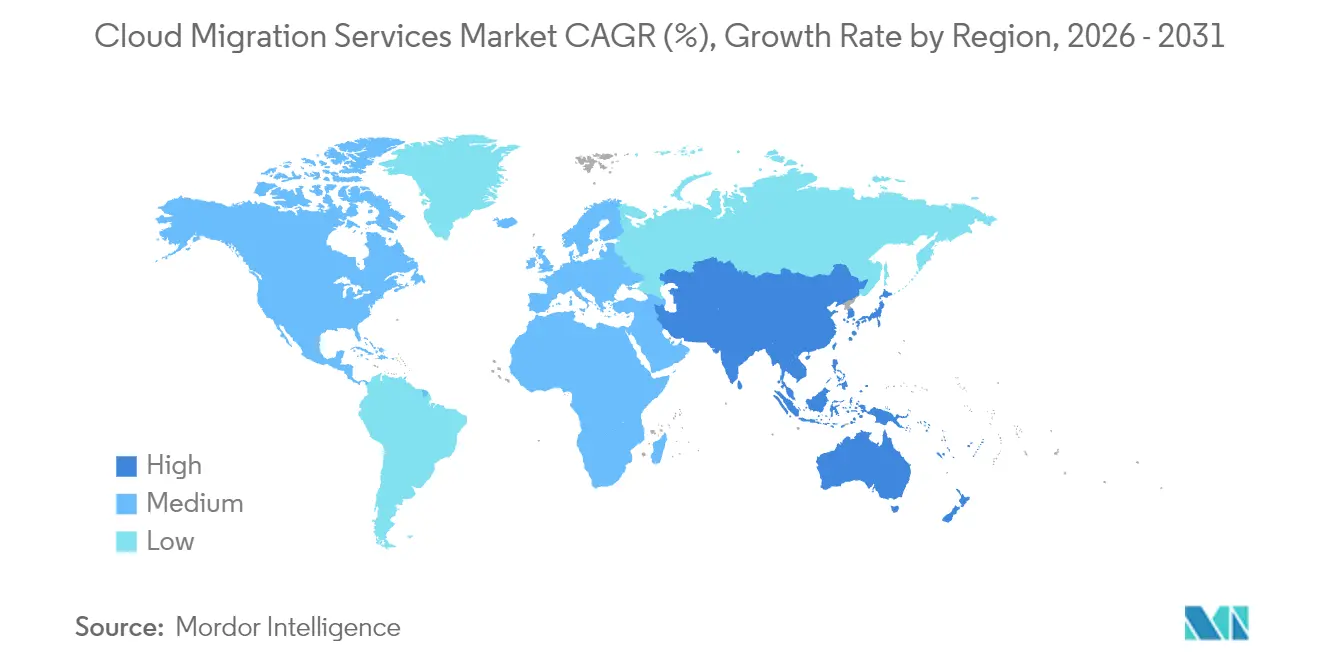

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

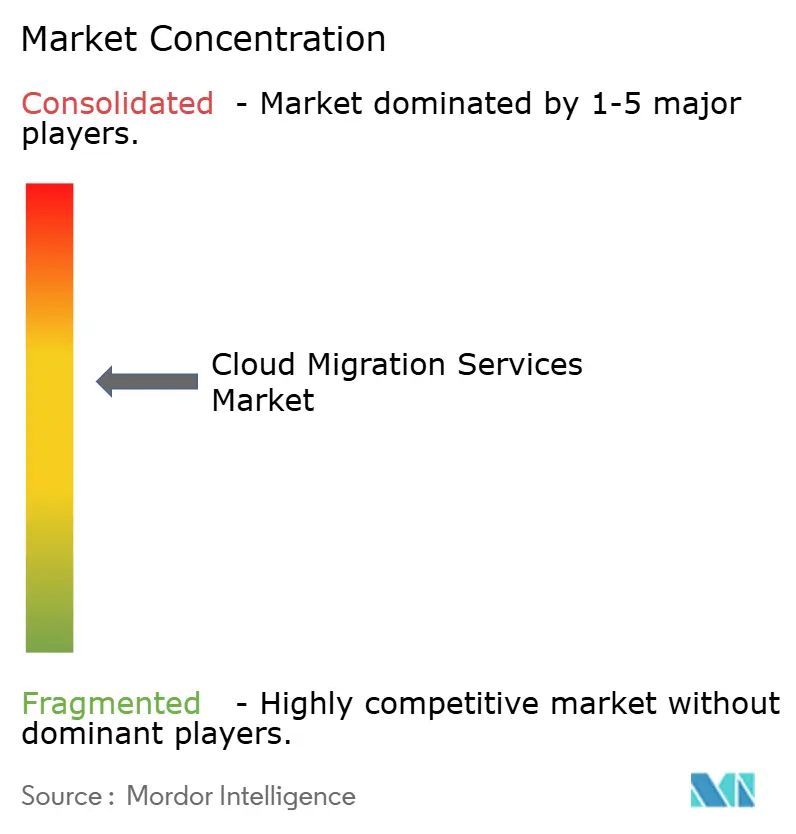

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Migration Services Market Analysis by Mordor Intelligence

The cloud migration services market size was valued at USD 300 billion in 2025 and estimated to grow from USD 383.04 billion in 2026 to reach USD 1299.48 billion by 2031, at a CAGR of 27.68% during the forecast period (2026-2031). This rapid upside reflects how enterprises are shifting from capital-intensive on-premises assets toward scalable cloud environments that permit faster innovation cycles and superior cost control. Momentum is fueled by generative-AI workload acceleration, expanding hybrid strategies, and mounting Scope-3 carbon-reporting obligations that favor cloud-native architectures. Public cloud keeps its leadership position, yet hybrid patterns are gaining ground as firms work to balance performance with compliance and cost-optimization goals. Large enterprises remain the biggest spenders, but small and medium enterprises (SMEs) are closing the gap as automated migration toolchains lower technical barriers. Across industries, Banking, Financial Services and Insurance (BFSI) and Healthcare are pacing adoption, while hyperscale providers and niche specialists continue to broaden service portfolios amid vendor-lock-in and egress-fee concerns.

Key Report Takeaways

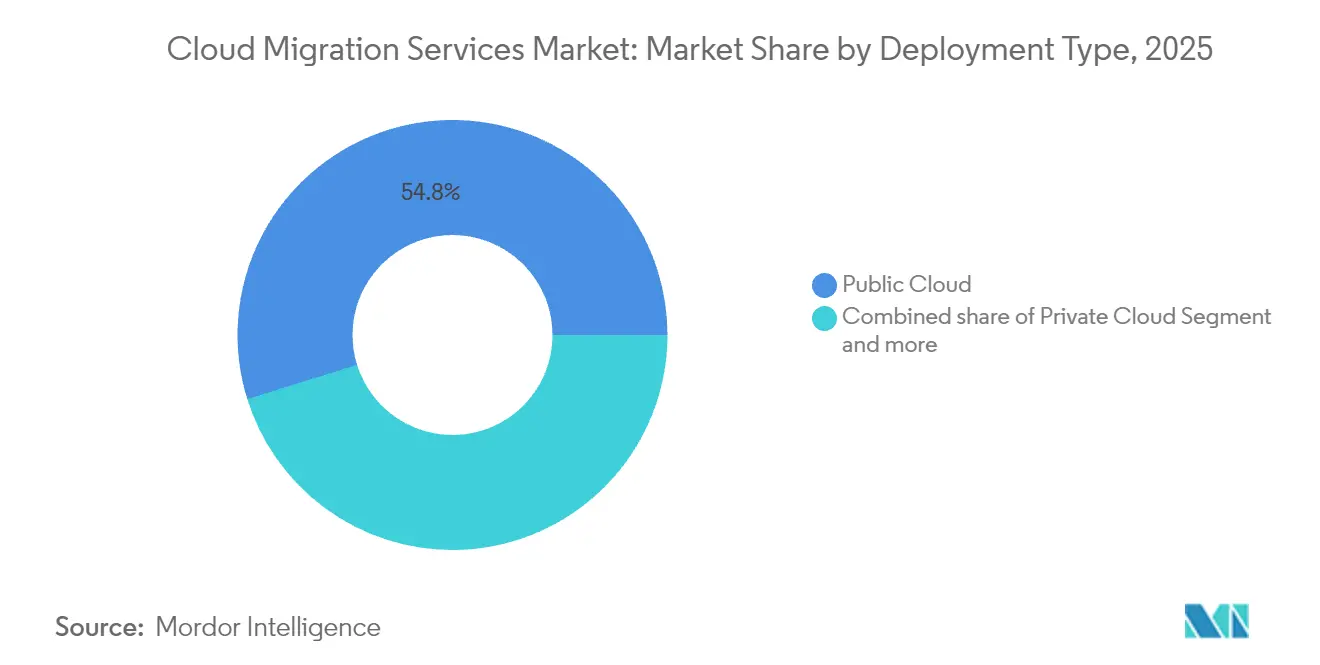

- By deployment type, public cloud retained 54.82% of cloud migration services market share in 2025, while hybrid cloud is projected to expand at an 18.35% CAGR to 2031.

- By enterprise size, large enterprises held 61.20% share of the cloud migration services market size in 2025; SMEs are advancing at an 17.65% CAGR through 2031.

- By service type, Software-as-a-Service led with 46.10% revenue share in 2025; Platform-as-a-Service is the fastest-growing at a 21.35% CAGR through 2031.

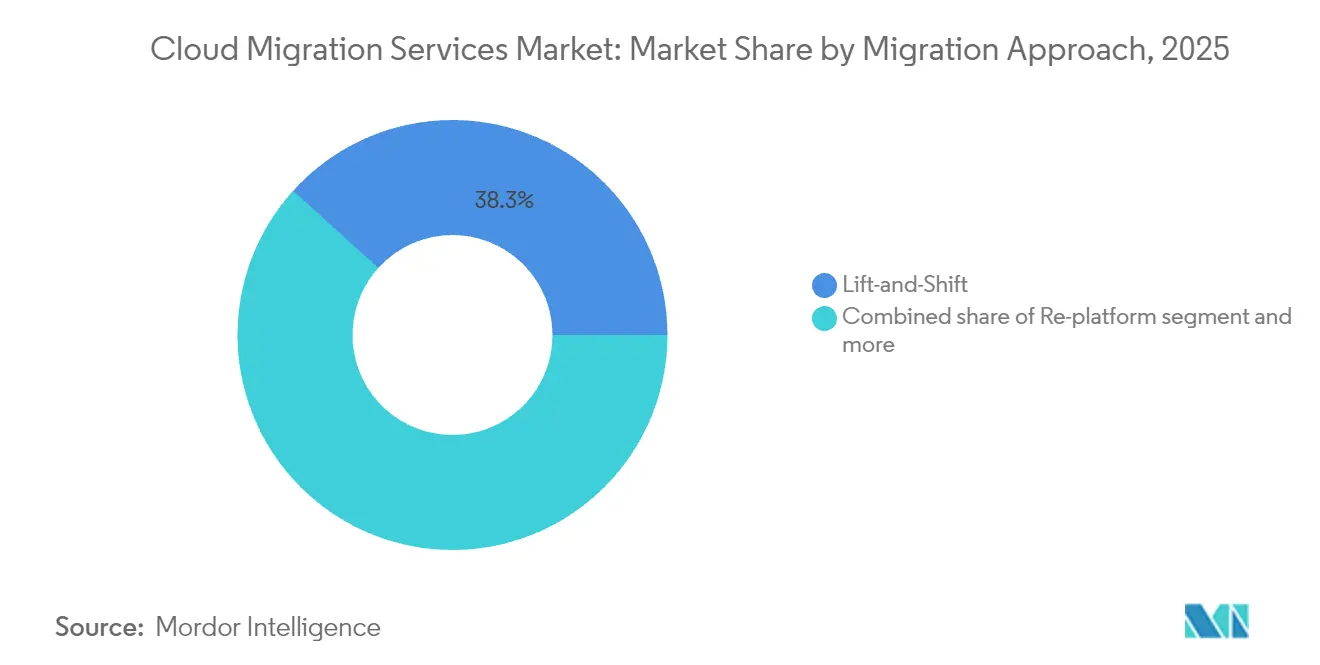

- By migration approach, lift-and-shift accounted for 38.30% of current activity in 2025, whereas refactor/re-architect strategies are climbing at a 22.35% CAGR to 2031.

- By end-user vertical, BFSI commanded 24.30% of cloud migration services market share in 2025; Healthcare and Life Sciences are forecast to grow at a 18.55% CAGR through 2031.

- By geography, North America captured 37.10% share in 2025; Asia-Pacific is set to register an 18.15% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Migration Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-efficiency and scalability advantages | +6.2% | Global | Medium term (2-4 years) |

| Rising remote-work and BYOD penetration | +4.8% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Government digital-transformation funding | +3.1% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Proliferation of hybrid / multi-cloud models | +2.9% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Generative-AI-driven refactoring | +1.7% | North America and Europe early adoption, Asia-Pacific following | Short term (≤ 2 years) |

| Scope-3 carbon-aware migrations | +1.2% | Europe leading, North America and Asia-Pacific adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-efficiency and Scalability Advantages of Cloud Adoption

Enterprises continue to realize 20-30% operational-expenditure savings after moving workloads to the cloud, primarily by eliminating capital-intensive hardware refresh cycles and right-sizing resources on demand. Infomart’s business-to-business platform migration to Oracle Cloud Infrastructure cut data-center costs by 38% while boosting performance flexibility. Elastic resource provisioning now allows organizations to handle unexpected demand spikes without the six-to-twelve-month procurement delays common in physical data-center environments. Budget freed from infrastructure upkeep is increasingly redirected toward innovation initiatives that sharpen competitive differentiation. These cumulative benefits give cost-rationalization strategies the highest positive impact on the forecast CAGR.

Rising Remote-work and BYOD Penetration

Hybrid work models have solidified, prompting organizations to migrate collaboration suites, identity services and security controls to the cloud to guarantee consistent user experiences across locations and devices. A recent survey shows 89% of IT leaders intend to raise cloud spending in 2025 to support distributed teams. BYOD complicates perimeter security, steering enterprises toward zero-trust architectures that are easier to enforce in cloud-native form. Consequently, migrations increasingly encompass secure access service edge, endpoint management and real-time analytics layers that maintain workforce productivity from any location. This trend exerts a strong, near-term pull on project pipelines, particularly in North America and Europe.

Government Digital-transformation Funding

Public-sector investment continues to underpin large-scale migrations. The United States allocated USD 8.3 billion in the 2024 federal IT budget specifically for cloud modernization. Similar initiatives in Alaska, Utah and Virginia offer reference architectures other jurisdictions emulate. European authorities are simultaneously financing sovereign-cloud programs to preserve data residency while capturing cloud efficiency gains. Budgets extend beyond compute contracts to encompass workforce reskilling, cyber-resilience and compliance frameworks, ensuring a consistent funding stream through the medium term.

Proliferation of Hybrid / Multi-cloud Strategies

Eighty-four percent of organizations now rely on hybrid or multi-cloud environments to optimize AI workload placement. This model lets firms keep latency-sensitive or regulated data close to users while exploiting hyperscale elasticity for analytics. Vendor diversification protects against lock-in and supports negotiation leverage, but multiplies management complexity. Demand therefore rises for service providers that can validate interoperability, automate policy enforcement and deliver observability across divergent platforms. As these expertise shortages persist, the driver’s impact extends into the long term.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security and regulatory-compliance risks | -3.4% | Global, heightened in Europe and regulated industries | Medium term (2-4 years) |

| Legacy-application complexity and interoperability | -2.1% | Global, concentrated in manufacturing and finance | Long term (≥ 4 years) |

| Escalating cloud egress fees | -1.8% | Global, affecting multi-cloud strategies | Short term (≤ 2 years) |

| Vendor lock-in amid sovereign-cloud mandates | -1.5% | Europe leading, expanding to Asia-Pacific and select North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-security and Regulatory-compliance Risks

European firms struggle to reconcile General Data Protection Regulation (GDPR) stipulations with public-cloud service models, while global financial institutions juggle overlapping jurisdictional rules that rarely address cloud data flows explicitly. [1]Computing News Desk, “GDPR Challenges Slow Public-Cloud Adoption,” computing.co.uk The shared-responsibility model often blurs accountability for encryption, logging and incident response. In some cases, sovereign-cloud requirements force organizations to pay premiums for localized capacity or retain on-premises infrastructure, extending migration timelines. These factors temper growth across nearly every industry, especially healthcare, banking and government.

Legacy-application Complexity and Interoperability

Decades-old mainframe and monolithic applications require significant re-engineering before they can run economically in cloud environments. Japan Airlines migrated its mileage-program systems from an IBM mainframe to AWS in eight months using automated COBOL-to-Java tools, following a deep modernization effort. [2]TIS, “Japan Airlines Completes Mainframe Migration to AWS,” tis.co.jp Maintaining integrations between legacy and newly migrated workloads adds parallel-run complexity, sometimes leading to cost overruns. Skill shortages in both legacy platforms and cloud-native design further widen project risk, extending the restraint's drag well into the long term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Hybrid Configurations Drive Innovation

Hybrid deployments are the fastest riser, advancing at an 18.35% CAGR as enterprises balance low-latency on-premises demands with public-cloud scale. Public cloud still holds 54.82% cloud migration services market share due to the mature security posture of hyperscale providers. Edge-cloud integrations now push compute closer to the user while maintaining elastic backend analytics connectivity, signaling that future architectures will combine multiple execution venues within a single workflow. Migration specialists able to orchestrate workload placement across these nodes remain in high demand.

Enterprises no longer view deployment as a binary choice. Financial institutions position trading engines on private clusters for sub-millisecond latency while offloading regulatory reporting to cost-efficient public buckets. Healthcare groups process imaging data on-site, then route anonymized sets to AI pipelines in the cloud. These nuanced blueprints underline why hybrid options will keep expanding their footprint within the cloud migration services market.

By Enterprise Size: SMEs Accelerate Adoption

Large enterprises accounted for 61.20% of cloud migration services market size in 2025, reflecting multi-year transformation budgets and global rollouts. Yet SMEs exhibit an 17.65% CAGR, propelled by packaged migration toolchains that cut setup time and lower expertise thresholds. Cloud providers now segment offerings—white-glove consulting for Fortune 500 clients versus prescriptive templates for smaller firms—thereby widening addressable demand without eroding margins.

SMEs gravitate toward SaaS replacements and managed services to avoid staffing expensive in-house operations teams. Conversely, large entities pursue phased re-architecting across dozens of business units, often underpinned by center-of-excellence teams that codify governance and security blueprints. This bifurcation requires service vendors to maintain differentiated go-to-market motions tailored to each cohort’s budget cycles and compliance obligations.

By Service Type: PaaS Emerges as Growth Engine

Software-as-a-Service led 2025 revenue with a 46.10% slice, mirroring entrenched productivity and CRM platforms. Platform-as-a-Service, however, is projected to climb at a 21.35% CAGR through 2031 as developers pivot to containerization and microservices architectures. Infrastructure-as-a-Service remains foundational for lift-and-shift workloads that demand OS-level control.

The PaaS surge underscores a shift from infrastructure procurement to application lifecycle acceleration. Serverless functions, managed Kubernetes and automated CI/CD pipelines now form the baseline for modern app delivery. Migration engagements increasingly include code-refactoring to exploit these abstractions, shortening feature release cycles and curbing operating cost.

By Migration Approach: Refactoring Gains Strategic Priority

Lift-and-shift still represented 38.30% of project volume in 2025, favored by organizations needing quick data-center exits. Yet refactor and re-architect initiatives are expanding at a 22.35% CAGR as enterprises chase long-term efficiency. Re-platforming remains a compromise path when teams modify databases or middleware but leave core code intact. Replacement via SaaS continues to grow for commodity workflows such as HR or expense management.

Generative-AI-backed modernization platforms now parse millions of code lines to surface remediation tasks, drastically reducing manual effort during refactor journeys. NEC’s use of “cotomi” AI with SAP S/4HANA Cloud evidenced the acceleration potential of these toolchains. Over the forecast horizon, automated refactoring is expected to tilt budgets away from lift-and-shift toward cloud-native optimization.

By End-user Vertical: Healthcare Accelerates Digital Transformation

BFSI retained 24.30% of cloud migration services market size in 2025, reflecting tight regulatory deadlines and intense digital-channel competition. Healthcare and Life Sciences are the fastest movers, heading toward a 18.55% CAGR thanks to electronic health-record mandates and the expansion of telemedicine. Retail relies on cloud elasticity for peak-season traffic handling, while public sector agencies invest in secure citizen-service portals.

Manufacturers integrate IoT feeds with predictive asset maintenance models, demanding scalable analytics backends. Energy utilities connect distributed renewable assets to cloud control planes for real-time grid balancing. Each vertical faces unique compliance and integration tasks, prompting service providers to build industry-specific accelerators that flatten migration learning curves.

Geography Analysis

North America captured 37.10% of 2025 spend, anchored by early adopters that now focus on AI optimization and multi-cloud cost governance. The United States leads through federal cloud programs such as the USD 8.3 billion modernization budget, while Canada and Mexico leverage improved network backbones to accelerate adoption. Across the region, organizations are integrating predictive workload placement engines to refine consumption models and curb egress charges, reinforcing North America’s position at the core of the cloud migration services market.

Asia-Pacific is projected to post an 18.15% CAGR to 2031, propelled by state-level digital-transformation funds and hyperscaler investments. Microsoft earmarked USD 2.9 billion for data-center expansion in Japan, demonstrating confidence in Japan’s cloud trajectory. India is on course for a USD 25.5 billion cloud sector by 2028, reflecting widespread modernization across BFSI, retail and government. China’s domestic providers, supported by data-localization rules, continue to grow market share via tailored sovereign offerings. The region’s diverse regulatory landscape shapes a patchwork of hybrid and multi-cloud designs that migration firms must navigate.

Europe pairs steady growth with stringent data-sovereignty controls. Germany and the United Kingdom remain the largest adopters, yet France and Spain are championing sovereign-cloud frameworks that bolster domestic vendors. GDPR enforcement compels meticulous residency mapping and encryption governance across every project. Consequently, hybrid strategies dominate, allowing sensitive workloads to stay on national soil while analytics and AI tasks harness scalable regional nodes. This dynamic will keep Europe’s migration profile firmly tied to compliance-first architectures throughout the forecast period.

Competitive Landscape

The market’s structural complexion is moderately fragmented. Amazon Web Services, Microsoft Azure and Google Cloud Platform constitute the backbone for most enterprise migrations, yet industry-specific integrators and boutique consultancies thrive by solving legacy and regulatory pain points. Oracle secured a cloud deal that could exceed USD 30 billion in annual revenue from fiscal 2028, signaling the scale of enterprise commitments. IBM’s USD 6.4 billion HashiCorp acquisition aims to enhance hybrid-cloud automation, while smaller players such as HYCU extend data-mobility platforms to blunt vendor-lock-in concerns.

Strategic themes coalesce around AI-powered refactoring, multi-cloud policy orchestration and edge-cloud convergence. Providers differentiate through automated code conversion, zero-trust security overlays and predictive cost-optimization engines. Specialized firms have carved defensible niches in mainframe modernization and healthcare compliance, areas where domain knowledge trumps raw scale. Price competition intensifies on generic lift-and-shift work, yet consultative engagements involving regulated workloads or heavy refactor commands premium margins.

M&A momentum is expected to persist as hyperscalers and global systems integrators acquire niche tooling to plug capability gaps and shorten time-to-value for large deals. At the same time, open-source frameworks for provisioning and policy management are lowering barriers for new entrants, ensuring the cloud migration services market remains competitive while gradually consolidating at the top tiers.

Cloud Migration Services Industry Leaders

Accenture plc

Amazon Web Services Inc.

Cisco Systems Inc.

Cognizant Technology Solutions Corporation

DXC Technology Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: TIS supported Meidensha in migrating its disaster-recovery site to Oracle Cloud Infrastructure, cutting costs by 50% while sustaining stability via Oracle Exadata Database Service

- July 2025: Zscaler enabled ADK Holdings to shift to a cloud-based IT stack, trimming help-desk response time by 50% for 3,000 staff across 20 offices

- July 2025: Oracle announced a future cloud agreement forecast to deliver more than USD 30 billion annually, with MultiCloud database revenue rising over 100%

- June 2025: Infomart migrated its B2B platform to Oracle Cloud Infrastructure, achieving a 38% data-center-cost reduction through OCI GoldenGate replication.

Global Cloud Migration Services Market Report Scope

Cloud migration services involves the movement of applications, data, and other business elements to a cloud computing environment. There are various types of cloud services migrations an enterprise can perform. One standard model is transferring data and applications from a local, on-premises data center to the public cloud. However, a cloud migration could also entail moving data and applications from one cloud platform or provider to another -- a model known as cloud-to-cloud migration. The study has focused on the trend analysis of the adoption of public, hybrid, and private clouds for cloud migration and the type of service provided by the vendors in the market for the application in a wide range of end-user verticals globally. The market estimations indicate the revenues accrued from cloud migration services (the move from on-premises or legacy infrastructure to the cloud) utilised by the enterprises across regions.

The Cloud Migration Services Market is segmented by type of deployment (public, private, and hybrid), by enterprise size (SMEs and large enterprises), by type of service (PaaS, IaaS, and SaaS), by end-user vertical (BFSI, healthcare, retail, government, IT and telecommunication, manufacturing and other end-user vertical), and by geography (North America, Europe, Asia Pacific, Latin America, Middle East & Africa). The report offers market forecasts and size in value (USD) for all the above segments.

| Public Cloud |

| Private Cloud |

| Hybrid Cloud |

| Multi-Cloud |

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| Infrastructure-as-a-Service (IaaS) |

| Platform-as-a-Service (PaaS) |

| Software-as-a-Service (SaaS) |

| Lift-and-Shift (Re-hosting) |

| Re-platform |

| Refactor / Re-architect |

| Replace (SaaS Substitution) |

| Banking, Financial Services and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Government and Public Sector |

| IT and Telecommunication |

| Manufacturing |

| Energy and Utilities |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Africa | South Africa | |

| Nigeria | ||

| By Deployment Type | Public Cloud | ||

| Private Cloud | |||

| Hybrid Cloud | |||

| Multi-Cloud | |||

| By Enterprise Size | Small and Medium Enterprises (SMEs) | ||

| Large Enterprises | |||

| By Service Type | Infrastructure-as-a-Service (IaaS) | ||

| Platform-as-a-Service (PaaS) | |||

| Software-as-a-Service (SaaS) | |||

| By Migration Approach | Lift-and-Shift (Re-hosting) | ||

| Re-platform | |||

| Refactor / Re-architect | |||

| Replace (SaaS Substitution) | |||

| By End-user Vertical | Banking, Financial Services and Insurance (BFSI) | ||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Government and Public Sector | |||

| IT and Telecommunication | |||

| Manufacturing | |||

| Energy and Utilities | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Africa | South Africa | ||

| Nigeria | |||

Key Questions Answered in the Report

What is the current value of the cloud migration services market?

The cloud migration services market size is USD 0.38 trillion in 2026 and is projected to climb to USD 1.30 trillion by 2031.

Which deployment model is growing fastest?

Hybrid cloud leads growth with an 18.35% CAGR through 2031 as enterprises align workload placement with latency, compliance and cost goals.

Why are SMEs increasingly adopting cloud migration services ?

Automated toolchains and tiered service models lower technical barriers and costs, enabling SMEs to capture enterprise-grade capabilities while fueling an 17.65% CAGR.

How do regulatory concerns restrain adoption?

Data-sovereignty mandates such as GDPR complicate compliance, forcing organizations to design hybrid or sovereign solutions that slow migration timelines.

What impact will generative AI have on future migrations?

AI-enabled code-analysis and refactoring tools are reducing modernization effort, accelerating the shift from lift-and-shift to cloud-native architectures expected to dominate by 2031.

Which region is expected to grow the quickest?

Asia-Pacific is forecast to register an 18.15% CAGR through 2031, driven by government investments and expanding hyperscale capacity.

Page last updated on: