Active Data Warehousing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

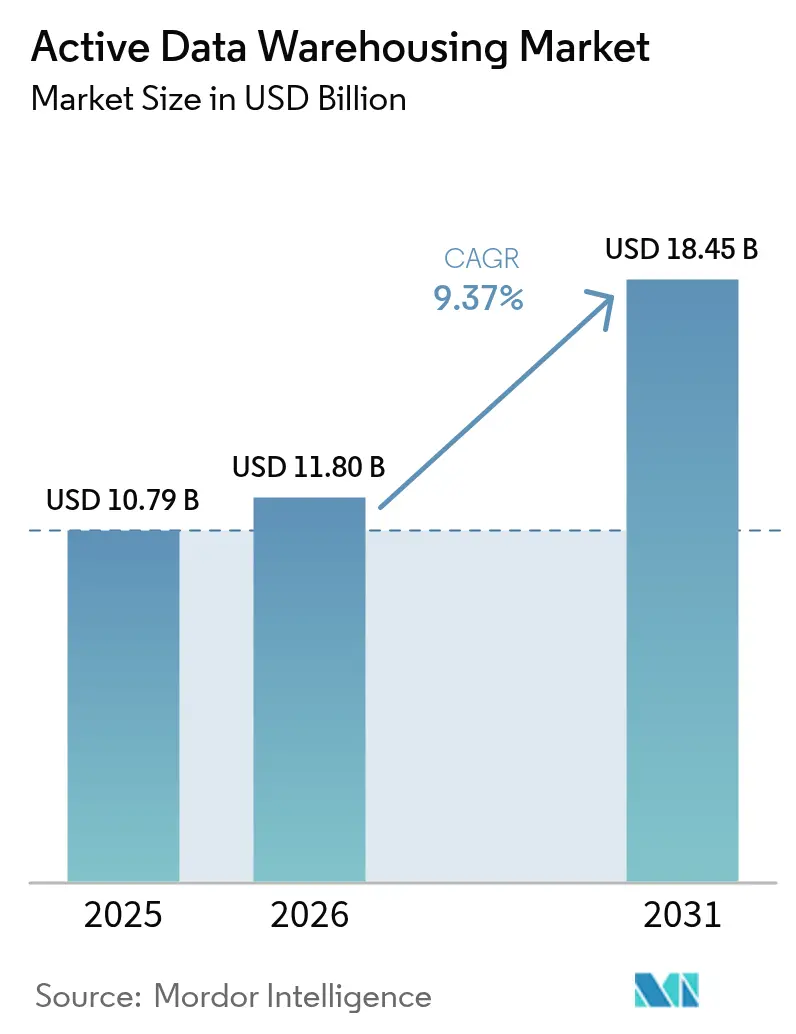

| Market Size (2026) | USD 11.8 Billion |

| Market Size (2031) | USD 18.45 Billion |

| Growth Rate (2026 - 2031) | 9.37% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Active Data Warehousing Market Analysis by Mordor Intelligence

The active data warehousing market size was valued at USD 10.79 billion in 2025 and estimated to grow from USD 11.8 billion in 2026 to reach USD 18.45 billion by 2031, at a CAGR of 9.37% during the forecast period (2026-2031). Demand is shifting from batch-oriented infrastructure toward continuous data ingestion and sub-second query performance as enterprises modernize digital services. Cloud platforms dominate because hyperscaler pricing eliminates capital expenditure and compresses deployment cycles, while hybrid architectures rise in jurisdictions that enforce data residency rules. Platform differentiation now hinges on governance, AI-assisted tuning, and open table formats that lower switching costs. Competitive intensity is set to rise as transactional-analytical convergence, generative AI in query engines, and multi-cloud portability narrow performance gaps across price tiers.

Key Report Takeaways

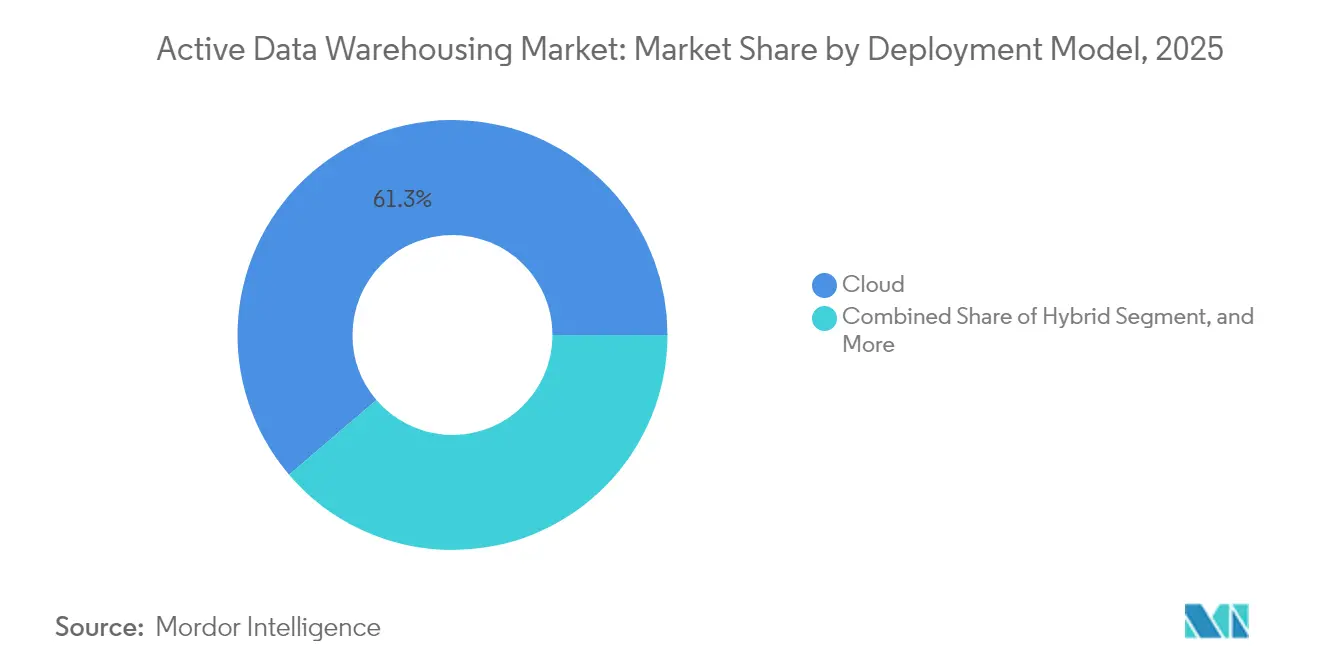

- By deployment model, hybrid environments are expected to expand at a 10.12% CAGR through 2031, while cloud deployments are projected to retain 61.25% of the active data warehousing market share in 2025.

- By component, software contributed 68.95% of the active data warehousing market share in 2025, while services posted the fastest growth rate of 10.05% due to increasing implementation complexity.

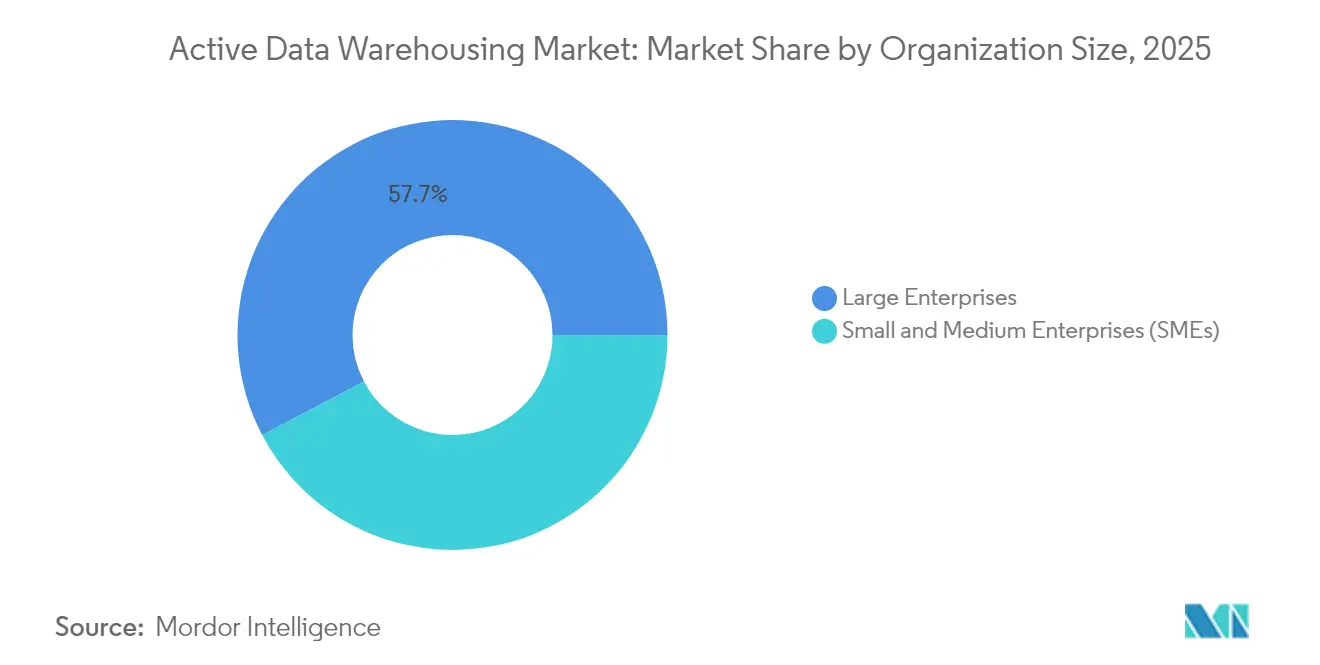

- By organization size, large enterprises accounted for 57.70% of the active data warehousing market share in 2025, whereas SMEs grew at a 9.98% CAGR as consumption pricing aligned costs with revenue cycles.

- By industry vertical, Banking, Financial Services and Insurance (BFSI) contributed 26.20% of the active data warehousing market share in 2025, and healthcare and life sciences posted the highest 10.72% CAGR as interoperability mandates demanded millisecond-latency analytics.

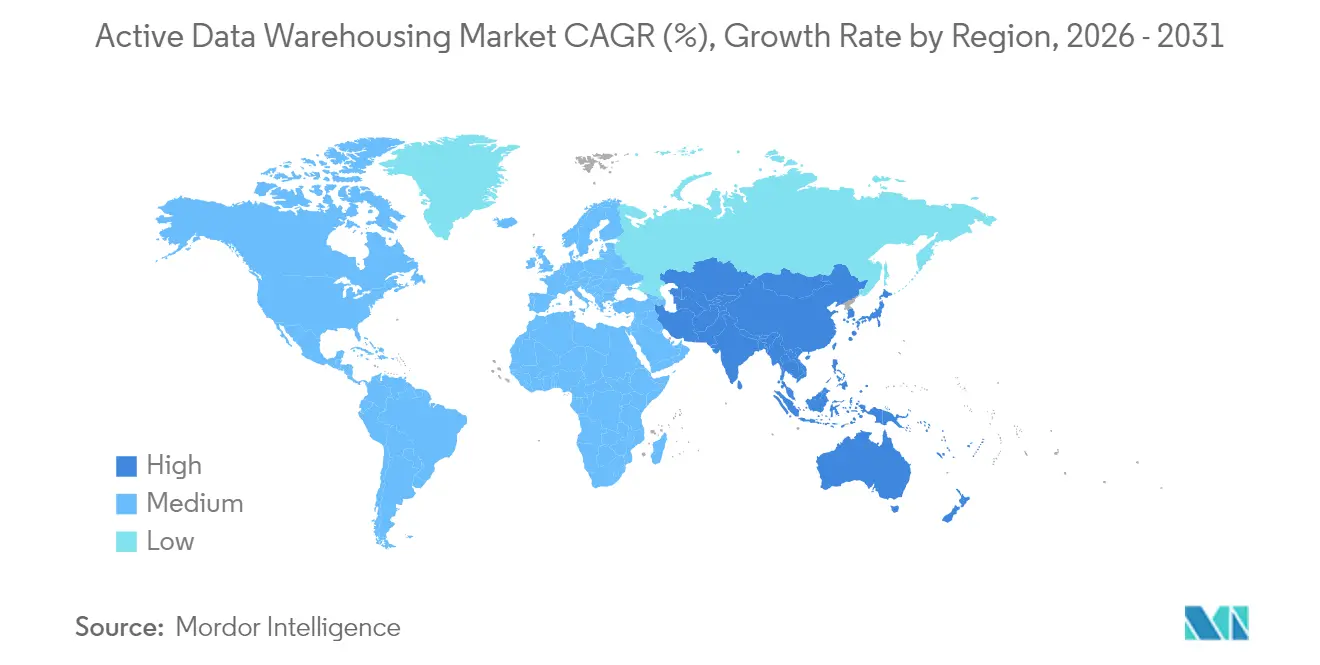

- By geography, North America held 35.10% of the active data warehousing market share in 2025, while Asia Pacific delivered the strongest 10.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Active Data Warehousing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated adoption of real-time analytics by customer-facing applications | +2.3% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Proliferation of cloud-native data warehousing platforms | +1.8% | Global, led by North America, Asia Pacific emerging | Medium term (2-4 years) |

| Rising demand for unified data governance across hybrid environments | +1.5% | Europe and North America core, Asia Pacific growing | Medium term (2-4 years) |

| Integration of AI-driven query optimization for sub-second insights | +1.2% | Global, early adoption in technology hubs | Short term (≤ 2 years) |

| Surge in IoT and edge data generating voluminous streams | +0.9% | Asia Pacific and North America manufacturing corridors | Long term (≥ 4 years) |

| Pay-as-you-go pricing models enhancing accessibility for SMEs | +0.7% | Global, impactful in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Real-Time Analytics By Customer-Facing Applications

Fraud-detection engines now evaluate card transactions within 50-100 milliseconds, a latency window batch warehouses cannot meet. Retailers using real-time inventory visibility cut stock-outs by 23% during the 2024 holiday season. Event-driven platforms route clickstream events to the warehouse as users interact, demanding concurrent high-velocity ingestion and complex query workloads. Hyperscaler services that decouple compute from storage, such as Amazon Redshift Serverless, scale elastically during peak traffic without over-provisioning idle capacity.[1]Amazon Web Services, “Amazon Redshift Serverless,” aws.amazon.com As a result, enterprises now classify sub-second analytics as a competitive baseline rather than an aspirational feature.

Proliferation of Cloud-Native Data Warehousing Platforms

Cloud-native offerings disaggregate compute, storage, and metadata, enabling granular scalability and near-instant provisioning. Snowflake posted 38% year-over-year product revenue growth to USD 2.8 billion in fiscal 2024 as customers migrated from appliance-based systems.[2]Snowflake Inc., “Fiscal 2024 Results,” snowflake.com Support for Apache Iceberg across AWS, Microsoft Fabric, and Google BigQuery removed lock-in concerns and accelerated multi-cloud strategies. Databricks’ USD 1 billion acquisition of Tabular underscored the strategic importance of open table formats that commoditize storage while differentiating compute. Vendors now compete on intelligent workload management and integrated governance rather than raw storage capacity.

Rising Demand for Unified Data Governance Across Hybrid Environments

The European Union’s Data Act, effective 2024, obliges industrial firms to make IoT data available to third parties under strict conditions, requiring governance that spans clouds and on-premises clusters. AWS Lake Formation extended cross-region policy enforcement in 2024, letting administrators apply a single access rule across multiple accounts. Microsoft Purview added scanning for on-premises SQL Server instances, creating a consolidated catalog that travels with the data.[3]Microsoft Corp., “Azure Synapse Analytics,” microsoft.com China’s Personal Information Protection Law forces multinationals to warehouse citizen records locally, fragmenting global datasets and elevating policy-driven data routing needs. Vendors that bundle federated governance into their core services gain strategic advantage.

Integration of AI-Driven Query Optimization For Sub-Second Insights

Google’s Duet AI generates optimized SQL from natural-language prompts and recommends partition strategies, accelerating analytics for non-technical users. AWS injected generative AI into Redshift workload management, allocating compute based on predicted query complexity rather than static queues. Snowflake Cortex AI lets analysts run machine-learning models inside the warehouse, eliminating data-movement latency. Early adopters report 40% faster time-to-insight versus manual tuning approaches. The technology’s value rises as routine reporting workloads dominate enterprise dashboards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High costs of data migration from legacy systems | -1.4% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Skilled talent shortage in real-time data engineering | -1.2% | Global, severe in emerging markets | Medium term (2-4 years) |

| Complexity of ensuring continuous data quality at scale | -0.9% | Global, heightened in regulated industries | Medium term (2-4 years) |

| Stringent data sovereignty regulations limiting cross-border warehousing | -0.8% | Europe, Asia Pacific, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Costs of Data Migration From Legacy Systems

Schema conversion, data validation, and application refactoring can consume 15-25% of modernization budgets, prolonging payback timelines. Teradata workloads require costly rewrites because proprietary SQL extensions lack direct cloud equivalents. Although AWS Schema Conversion Tool and Snowflake Migration Accelerator automate syntax translation, embedded business logic still demands manual remediation. Financial institutions often run legacy and cloud warehouses in parallel for years, doubling operational costs while transition proceeds.

Skilled Talent Shortage in Real-Time Data Engineering

Enterprises struggle to recruit engineers proficient in stream processing frameworks such as Apache Kafka, Spark Structured Streaming, or Flink, extending project timelines. Hyperscalers are expanding training programs, AWS re:Start and Google Cloud Career Certificates to close skills gaps yet supply lags demand. Services partners report 6–9-month onboarding queues for senior real-time architects, pushing organizations to adopt serverless abstractions that mask complexity. Emerging markets feel the shortage most acutely, where local upskilling cannot match the pace of digital-transformation initiatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Gains Momentum Amid Sovereignty Pressures

Hybrid deployments captured a growing share as data gravity and residency mandates shaped architecture decisions. The active data warehousing market size for hybrid environments is forecast to expand at 10.12% CAGR through 2031. Organizations in China, India, and the European Union retain sensitive datasets on-premises while bursting analytical workloads to the cloud, balancing control with flexibility. Vendors offer cloud-managed clusters inside customer data centers, blurring lines between on-premises and hosted services. In parallel, pure-public cloud instances continue to scale transaction-heavy digital businesses, illustrating coexistence rather than displacement.

Cloud-connected appliances such as Oracle Exadata Cloud@Customer and AWS Outposts position on-premises deployment as a stepping stone, allowing low-latency access to operational systems while delegating management to the provider. Workload placement decisions increasingly consider egress fees: shipping petabytes of historical logs to cloud warehouses can outweigh compute savings, anchoring data in local facilities. As a result, hybrid flexibility becomes a long-term architectural default rather than an interim stage.

By Component: Services Surge As Complexity Outpaces Platform Maturity

The software layer still delivered 68.95% of 2025 revenue, yet professional and managed services now post the fastest growth, reflecting skills shortages and architectural complexity. The active data warehousing market share commanded by implementation, migration, and optimization services is poised to rise through 2031 as enterprises confront streaming ingestion, federated governance, and AI-driven tuning. Global system integrators scale headcount to meet demand, while specialized boutiques carve niches in regulated industries.

Services engagement models evolve toward outcome-based contracts tied to query-performance service level objectives and governance compliance KPIs. Platforms embed telemetry that feeds partner dashboards, enabling proactive optimization and automated cost control. Over time, knowledge codifies into accelerators and blueprints, marginally reducing engagement duration but not demand new features such as hybrid OLTP-OLAP workloads introduce fresh implementation challenges.

By Organization Size: SMEs Embrace Consumption Economics

Large enterprises remain the dominant buyers thanks to petabyte-scale data assets, yet SMEs represent the fastest growth cohort. Cloud credit-based billing converts fixed infrastructure costs into variable operational expenses, letting fledgling companies experiment with analytics before revenue scales. Serverless execution and auto-suspend features eliminate idle-cluster burn, aligning spend with workload bursts.

Adoption patterns differ SMEs favor SaaS connectors, visual query builders, and packaged governance over bespoke pipelines. Vendors respond with simplified SKUs, pre-bundled marketplace integrations, and template-driven dashboards. The active data warehousing market size attributed to SMEs is projected to widen as digital-native start-ups embed analytics into core products from inception rather than retrofitting warehouses later.

By Industry Vertical: Healthcare Accelerates Amid Interoperability Mandates

BFSI retained the largest 26.20% revenue share in 2025, powered by real-time risk scoring, liquidity monitoring, and regulatory reporting. Concurrently, healthcare delivers the top 10.72% CAGR as electronic health record interoperability and patient-access rules compel health systems to expose data through standardized APIs. Warehouses must process HL7 or FHIR event streams in milliseconds without compromising privacy, driving demand for encryption-in-use and fine-grained auditing.

Retailers expand same-hour delivery programs that rely on accurate stock and location data, reinforcing the case for sub-second inventory updates. Telecommunications carriers ingest billions of call detail records daily, pairing warehouse analytics with predictive algorithms that preempt network failures. In manufacturing, edge-to-cloud pipelines feed predictive maintenance models, shaving unscheduled downtime. These vertical nuances shape feature roadmaps, prompting vendors to release industry packs with pre-built schemas, compliance templates, and reference dashboards.

Geography Analysis

North America anchored 35.10% of 2025 spending, benefiting from dense hyperscaler footprints, a rich talent pool, and historically permissive cross-border data flows. State-level privacy statutes enacted in 2024, however, fragment policy and necessitate fine-grained residency controls similar to GDPR. Financial institutions migrate workloads in stages, citing 30-35% cost savings and faster model iteration once in cloud warehouses. The region also hosts the bulk of real-time engineering talent, sustaining innovation velocity.

Asia Pacific posts the strongest 10.45% CAGR through 2031. Digital transformation in China, India, and Indonesia creates petabyte-scale data lakes that outgrow legacy appliances. Localization mandates split architectures: citizen data remains in domestic regions while less sensitive workloads leverage global clouds. Hyperscalers deploy additional zones in Mumbai, Jakarta, and Seoul to address residency clauses, and manufacturers in Japan and South Korea adopt edge-processing frameworks to analyze IoT telemetry locally before central aggregation.

Europe operates under the extraterritorial GDPR and the 2024 Data Act, imposing third-party data-sharing requirements on industrial IoT assets. Compliance complexity favors vendors with deep legal and governance tooling. Germany’s industrial champions consolidate disparate warehouses into unified platforms to unlock AI training data while trimming infrastructure overhead. The United Kingdom maintains regulatory alignment via renewed adequacy agreements, yet enterprises hedge by dual-hosting datasets on both sides of the Channel.

The Middle East and Africa witness steady adoption led by national cloud strategies in the United Arab Emirates and Saudi Arabia that make cloud-first architecture mandatory for public agencies. South America’s growth centers on Brazil, where LGPD echoes GDPR principles and accelerates governance upgrades in both public and private sectors.

Regulatory Landscape

Active data warehousing deployments are increasingly shaped by data protection, sovereignty, and interoperability rules that determine where data can be stored and how it can be shared across entities and clouds. In Europe, GDPR obligations are complemented by the EU Data Act, which took effect in 2024 and adds operational requirements around access to and sharing of data generated by connected products and related services. As a result, enterprises are putting fine-grained access controls, auditing, and governed data-exchange workflows in place across hybrid environments.

Regulatory and standards activity in 2024-2026 also points to jurisdiction-specific governance architectures. China issued national standards such as GB/T 44109-2024 (big data governance implementation) and GB/T 45800.1-2025 (national integrated government big data system), which encourage structured governance practices that influence public-sector and regulated-industry warehousing programs. Several governments also advanced digital architecture and data governance frameworks in 2026, including Vietnam issuing digital, data architecture, and data governance management frameworks (July 2026), which reinforces the need for policy-driven data routing, residency-aware deployment patterns, and security-by-design controls within active data warehousing stacks.

Value Chain Analysis

The value chain starts with data generation and capture, including enterprise applications, IoT and edge devices, clickstream, and operational systems. It then moves through ingestion and integration layers (CDC and streaming platforms such as Kafka, Spark Structured Streaming, and Flink, along with managed connectors) into storage and table formats (cloud object storage and open formats such as Apache Iceberg and Delta Lake). Active data warehousing platforms follow with real-time query engines, workload management, and governance and cataloging, including AWS Lake Formation and Microsoft Purview. Consumption layers then include BI, operational analytics, and embedded or agentic applications. Professional services and system integrators remain central for migration, data modeling, and performance engineering, reflecting the continuing skills shortage in real-time data engineering.

Downstream value realization is increasingly tied to vertical operating systems and packaged solutions that combine governed data products with near-real-time analytics. Partnerships show how platform vendors plug into business workflows, including Kinaxis partnering with Databricks (April 2025) to integrate Databricks capabilities into its Maestro orchestration fabric, and logistics operators such as Penske Logistics applying Snowflake-based analytics for real-time visibility (July 2025). Hardware availability also constrains timing across the chain: data center buildouts and upgrades that support cloud and hybrid deployments face bottlenecks, including networking equipment lead times reaching up to 52 weeks and printed circuit boards 20-30 weeks (cited in 2026). These constraints can shape regional capacity timing and hybrid placement decisions for latency-sensitive workloads.

Competitive Landscape

Market concentration is moderate. The five largest vendors, Snowflake, AWS, Microsoft, Google, and Databricks controlled roughly 65% of 2024 cloud revenues, but open formats and multi-cloud strategies keep rivalry high. Hyperscalers leverage bundled pricing across compute, storage, and network services to undercut stand-alone offerings by 20-30% on total cost of ownership. Snowflake defends premium margins with multi-cluster workload isolation that ensures performance even at peak concurrency. Databricks pivots toward Apache Iceberg to commoditize storage, shifting differentiation to AI-optimized compute.

Transactional-analytical convergence intensifies competition. Snowflake Unistore supports operational updates alongside analytics, challenging established mixed-workload databases. Smaller players such as Firebolt deliver index-based engines for ad-hoc queries, and Yellowbrick excels in on-premises high-performance clusters for regulated industries. Generative AI embedded in Redshift and BigQuery narrows performance gaps, forcing suppliers to compete on governance, ecosystem breadth, and compliance attestations like ISO 27001 and SOC 2. Vendors without global legal teams face hurdles as regulatory complexity escalates.

Active Data Warehousing Industry Leaders

Teradata Corporation

Snowflake Inc.

Amazon Web Services Inc.

Microsoft Corporation

Google LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Consolidation around open table formats and cross-cloud interoperability is a core opportunity, as it reduces lock-in while preserving governance, which aligns with hybrid and multi-cloud architectures constrained by residency and transfer rules. In April 2026, Google Cloud introduced BigQuery Cross-Cloud Lakehouse in preview using an Iceberg REST Catalog approach, along with bi-directional federation that can read from Databricks Unity Catalog, Snowflake Polaris, and AWS Glue Data Catalog. These moves create room for vendors and service partners to operationalize consistent policy enforcement, lineage, and cost controls across engines and clouds.

A second opportunity is real-time analytics for agentic and operational workloads that need millisecond-level responsiveness without complex, multi-stage ETL. In June 2026, Databricks announced Lakehouse//RT as a real-time compute engine intended to deliver millisecond query latency on Delta Lake and Apache Iceberg tables, and it expanded ingestion coverage through Lakeflow Connect with over 100 managed connectors. This direction increases demand for active data warehousing architectures that unify streaming ingestion, governance, and low-latency query, particularly where continuous data quality and fine-grained auditing are purchasing criteria, including BFSI fraud detection, telecommunications CDR analytics, and healthcare interoperability-driven event processing.

Recent Industry Developments

- July 2026: Amazon Web Services expanded Amazon Redshift RG instances, powered by AWS Graviton, to the trailing track. The update targets better price-performance for high-concurrency analytics and integrated data lake querying, supporting active warehousing workloads that blend streaming ingestion with fast interactive SQL.

- June 2026: Snowflake expanded its partnership with Anthropic to accelerate enterprise AI adoption through governed AI capabilities on Snowflake data. The collaboration reinforces the push to run AI applications closer to governed warehouse data, increasing emphasis on policy controls, secure data access, and in-warehouse AI workflows.

- October 2025: Google Cloud launched BigQuery Distributed Storage, separating metadata from columnar data blocks to provide 99.999% availability and cross-region replication. The architecture supports latency-sensitive active analytics use cases by improving resilience and enabling replication patterns that align with multi-region operations and governance needs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers software and related services that enable always-on data ingestion, continuous processing, and near real-time analytics in an active data warehouse environment, delivered through on-premises, cloud, or hybrid deployment.

Scope exclusions: We exclude general-purpose storage hardware and standard batch-only data warehouse projects that do not support continuous or near real-time workloads.

Segmentation Overview

- By Deployment Model

- On-Premises

- Cloud

- Hybrid

- By Component

- Software

- Services

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Industry Vertical

- Banking, Financial Services and Insurance (BFSI)

- Retail and Ecommerce

- Telecommunications and IT

- Healthcare and Life Sciences

- Manufacturing

- Government and Public Sector

- Other Industry Vertical

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, understand adoption patterns, and collect anchor indicators that can be checked country by country. We referred to public sources such as the US Bureau of Labor Statistics (for IT spend and wage context), OECD digital economy statistics, World Bank macro indicators, ITU connectivity datasets, and standards and guidance from bodies such as ISO and NIST for terminology and security context.

On top of this, we reviewed company annual reports, earnings call transcripts, product documentation, investor presentations, and reputable press to map how active data warehousing is positioned and packaged across software and services. Select subscription databases for company financials, news, patents, and public contracts were used to cross-check revenue disclosures, investment signals, and major deal activity. The sources mentioned here are illustrative only, and additional public references were used throughout the study to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work was used to confirm what buyers actually pay for, how deployments are split across cloud, on-premises, and hybrid, and which functions are counted as active data warehousing versus adjacent analytics tooling. We spoke with a mix of solution leaders, delivery heads, and user-side data and analytics managers across APAC, EMEA, and the Americas so assumptions on adoption, pricing motion, and refresh cycles could be checked with real purchasing language.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 15% | APAC: 41% |

| Mid tier: 52% | Functional/Unit leaders: 28% | EMEA: 34% |

| Smaller Players: 18% | Managers: 57% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where IT and data platform spending pools by region are reconstructed, and then filtered using adoption and usage signals specific to active data warehousing. Because these platforms are bought and expanded over time, we also sanity-check totals with selective bottom-up work such as sampled vendor revenue splits, channel feedback, and ASP per workload estimates multiplied by active deployments, which are then adjusted for coverage gaps.

Inputs used in the model included cloud versus on-premises mix, workload intensity (streaming ingestion and query concurrency), subscription and service attach rates, enterprise modernization pace, and regulated industry uptake where latency and audit needs are stronger. Forecasts were developed using scenario analysis, with short-listed drivers (cloud migration pace, data volume growth, and service labor availability) being stress-tested and then aligned with what practitioners describe for budgets and refresh cycles. Where a bottom-up slice could not be reliably built for a country or vertical, the gap was handled through proxy ratios from similar markets and then re-checked through interviews before finalizing.

Data Validation & Update Cycle

Results were validated through triangulation across multiple signals, including implied spend per organization, vendor revenue direction, and regional digital investment trends, so extreme outputs could be flagged early. Outliers were reviewed by a second analyst, and assumptions were re-contacted with experts when pricing or adoption inputs moved outside a reasonable band.

The dataset is refreshed annually, and interim updates are triggered when material events occur, such as major pricing changes, platform consolidations, or large shifts in cloud adoption policy. Before delivery, a final analyst pass is completed to re-check currency conversion timing, growth rates, and any newly released public disclosures that can influence the current-year estimate.

Mordor Intelligence's Global Active Data Warehousing Market Market Estimate Compared With Other Published Estimates

Different publications can land on different market sizes because they do not always count the same products, the same service layers, or the same deployment types, even when the market name looks identical. Timing differences also matter since some estimates anchor on older base years and then apply a single growth rate without re-checking key demand signals.

Key gaps for this market usually come from whether the sizing includes adjacent data management and analytics tooling, how cloud subscription value is recognized versus implementation services, and whether hybrid deployments are treated as a separate pool or partially double-counted. By tracking deployment-level mix and refresh timing across regions, Mordor Intelligence keeps the estimate tied to active workloads (continuous ingestion and near real-time queries) rather than folding in broader batch warehousing or general analytics spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.8 B (2026) | |

| Industry Research House A | USD 10.16 B (2024) | Uses an earlier base year and a broader end-use framing, which can mix active warehousing with general analytics and integration spend, and then project forward with fewer deployment-mix checks. |

| Market Tracker B | USD 6.20 B (2024) | Appears to apply a narrower counted scope and may under-capture services and hybrid deployments, which reduces the recognized revenue pool compared with a software-plus-services view. |

The spread across the three numbers is mostly explained by boundary choices and year anchoring, not by disagreement that the market is growing. Our approach makes each included dollar traceable to an active warehousing use case, with clear treatment of software versus services and consistent handling of cloud, on-premises, and hybrid deployments.

Key Questions Answered in the Report

How large is the active data warehousing market in 2026?

The active data warehousing market size is USD 11.8 billion in 2026.

What CAGR is expected through 2031?

The market is projected to expand at a 9.37% CAGR between 2026 and 2031.

Which deployment model is growing fastest?

Hybrid architectures post the strongest 10.12% CAGR as firms balance cloud scale with residency mandates.

Why is healthcare the fastest-growing vertical?

Interoperability mandates and real-time clinical decision support drive an 10.72% CAGR in healthcare and life sciences.

What restraints slow modernization?

High legacy-migration costs and a shortage of real-time data engineers create bottlenecks.

Which region shows the most robust growth?

Asia Pacific leads with a 10.45% CAGR thanks to data-localization laws and expanding digital economies.

Page last updated on: