Freelance Platforms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

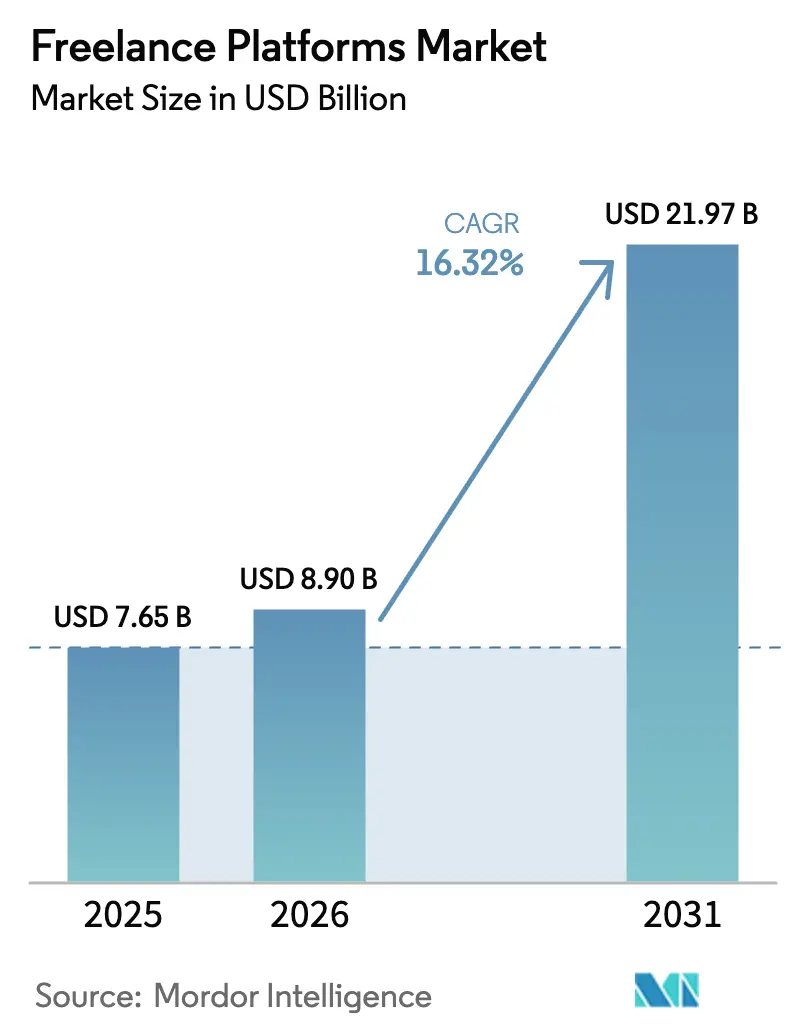

| Market Size (2026) | USD 8.9 Billion |

| Market Size (2031) | USD 21.97 Billion |

| Growth Rate (2026 - 2031) | 16.32% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Freelance Platforms Market Analysis by Mordor Intelligence

Freelance platforms market size in 2026 is estimated at USD 8.9 billion, growing from 2025 value of USD 7.65 billion with 2031 projections showing USD 21.97 billion, growing at 16.32% CAGR over 2026-2031. Shifts toward hybrid work, rising demand for niche digital skills, and growing cost-optimization pressures keep the momentum strong for the freelance platforms market. Enterprise buyers increasingly favor platform-mediated talent engagement because it delivers compliance, variable cost structures, and rapid access to specialized capabilities. AI-powered matching and productivity tools now underpin most competitive differentiation, while emerging cross-border invoicing rules reduce friction in global payments. Geographically, North America retains leadership in penetration rates, yet Asia-Pacific is expanding fastest as enterprises in the region accelerate digital transformation plans.

Key Report Takeaways

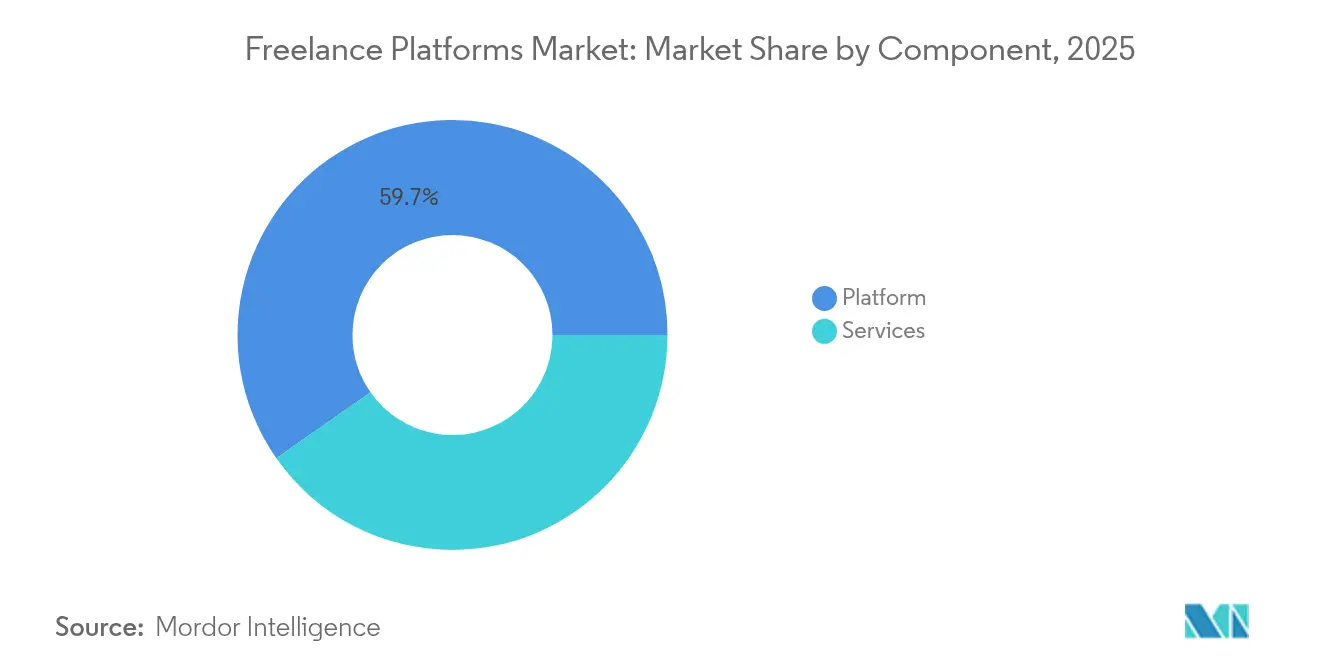

- By component, platform models led with 59.72% of the freelance platforms market share in 2025; services are projected to grow at an 18.05% CAGR through 2031.

- By application, project management held 23.12% revenue share in 2025, while web and graphic design is forecast to advance at a 18.78% CAGR to 2031.

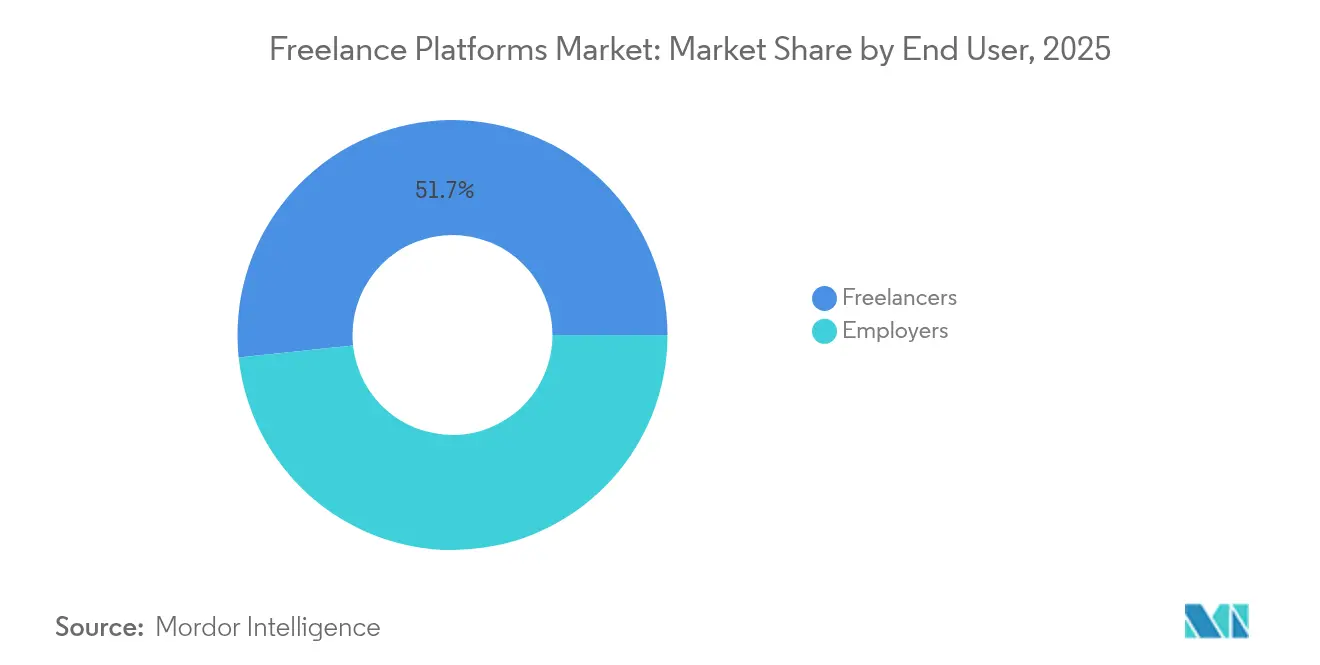

- By end user, freelancers accounted for 51.66% of the freelance platforms market size in 2025; employer adoption is rising at an 17.95% CAGR through 2031.

- By organization size, small and medium enterprises controlled 65.02% share of the freelance platforms market size in 2025, whereas large enterprises represent the fastest expansion at an 18.55% CAGR.

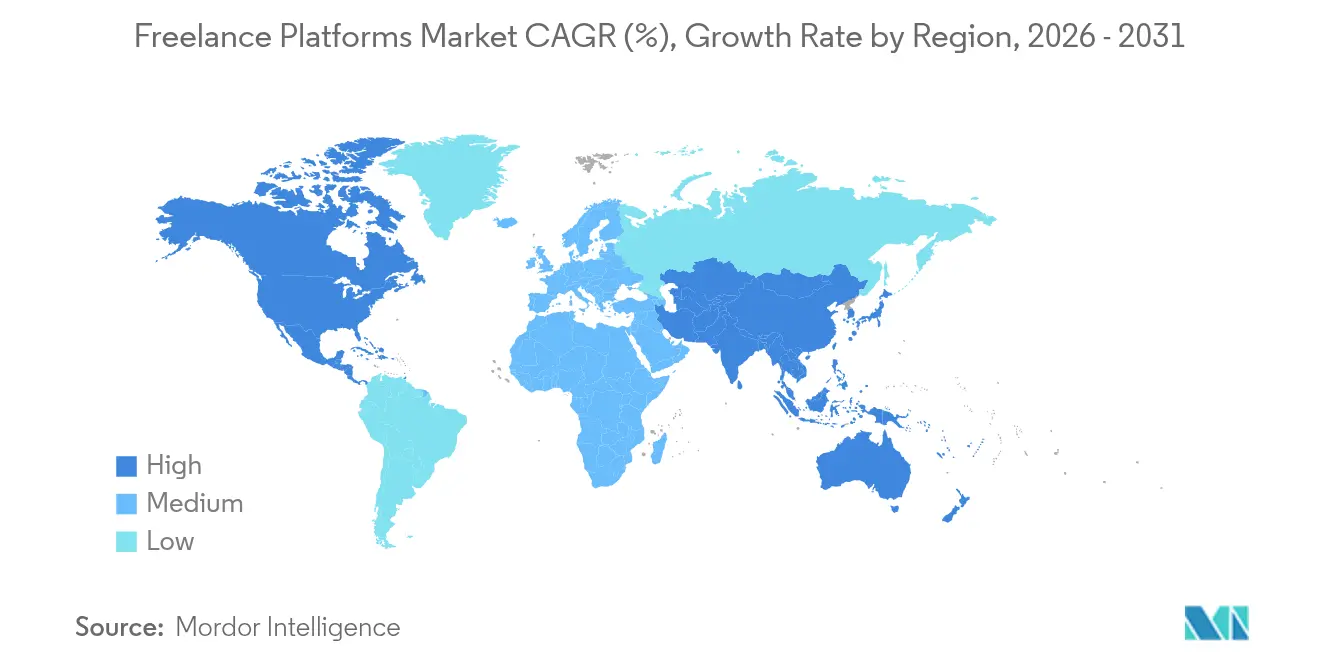

- By geography, North America commanded 32.64% revenue in 2025; Asia-Pacific is charting the highest regional CAGR at 18.22% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Freelance Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid and flexible workforce strategies | +4.2% | North America, Europe, Global spill-over | Medium term (2-4 years) |

| Rising demand for specialized digital skills | +3.8% | Asia-Pacific, North America | Long term (≥ 4 years) |

| Cost-optimization pressure on enterprises | +3.1% | North America, Europe | Short term (≤ 2 years) |

| Cross-border e-invoicing regulations | +2.4% | Europe, Asia-Pacific, North America | Medium term (2-4 years) |

| Generative-AI copilots for freelancers | +2.9% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| AI-powered matching algorithms improving hire speed | +2.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift toward hybrid and flexible workforce models.

Platform adoption accelerated after the U.S. Department of Labor’s 2024 rule clarified contractor classification, giving enterprises a compliant path to blend internal and external talent [1]U.S. Department of Labor, “Employee or Independent Contractor Classification Final Rule,” dol.gov . A global advertising group saved USD 9.6 million in one year by shifting consultant spend to a managed marketplace. Large corporations now bake contingent workforce planning into core strategy, using platforms to secure emerging skills faster than conventional hiring cycles allow. Surveyed firms report an 84% jump in non-employee talent use since the pandemic. The freelance platforms market, therefore, benefits from a structural rather than cyclical re-allocation of labor budgets.

Rising demand for specialized digital skills

Demand for AI, machine learning, and advanced programming skills rose 60% year-over-year, pushing freelance hourly rates up 44% above platform averages. Japanese data shows Go and Ruby specialists commanding monthly pay near JPY 852,000 (USD 5,680) and JPY 839,000 (USD 5,593), respectively. Enterprises prize cross-functional experts who can connect technology build-outs with business value, motivating platforms to refine AI-driven matching to surface niche talent. High pricing power and scarce supply combine to sustain premium fee structures, reinforcing growth prospects for the freelance platforms market.

Cost-optimization pressure on enterprises

Contingent workforce spend now touches 30% of large procurement budgets, prompting sharper focus on variable labor strategies. A leading U.K. service provider cut GBP 500,000 (USD 625,000) in six months by consolidating contractors through a compliance-ready platform. Savings extend to real estate and onboarding costs, while variable pricing improves budget predictability. Platforms that guarantee classification accuracy are rapidly gaining share with enterprise procurement teams seeking both savings and risk mitigation.

Generative-AI copilots boost platform worker productivity.

Fiverr’s “Fiverr Go” lets freelancers train AI models on their portfolios, freeing time for higher-value tasks. Upwork’s Uma assistant recommends proposals and automates mundane steps, supporting the company’s USD 769.3 million revenue in 2024. Productivity gains shorten delivery cycles and entice larger projects, shifting the freelance platforms market narrative from labor arbitrage toward capability enhancement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Trust and payment-security concerns | -2.1% | Global; acute in emerging markets | Short term (≤ 2 years) |

| Regulatory ambiguity on worker classification | -1.8% | North America, Europe | Medium term (2-4 years) |

| Algorithm-bias lawsuits | -1.3% | North America, Europe | Medium term (2-4 years) |

| Escalating digital advertising costs | -1.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Trust and payment-security concerns

Escrow tools and two-factor identity verification now form baseline requirements for platforms expanding into geographies with weak payment rails. SafePay adoption on Guru and similar services shows improvement, yet fraud techniques continue to evolve, forcing ongoing investment in compliance and anti-money-laundering safeguards. Trust issues therefore remain a near-term drag on the freelance platforms market.

Algorithm-bias lawsuits are increasing compliance costs

New York City’s Local Law 144 demands annual bias audits for automated hiring tools, a standard other jurisdictions are adopting. Platform operators must document fairness across multiple demographic attributes, adding legal fees and sophisticated data-science oversight to operating costs. The freelance platforms market absorbs these expenses through higher take-rates or subscription fees, which may deter price-sensitive segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platform dominance steers ecosystem expansion

Platform revenue streams captured 59.72% of the freelance platforms market share in 2025 on the strength of commission-based models that scale with transaction volume. Marketplaces such as Upwork and Freelancer rely on network effects, reinforcing their lead as user rolls deepen. The services component, however, is outpacing at an 18.05% CAGR, propelled by enterprise demand for managed solutions that guarantee compliance and project outcomes.

Managed service providers like CXC Global administer over 12,000 contractors monthly, showcasing an appetite for turnkey workforce orchestration. Hybrid models now blend marketplace agility with curated service layers, creating tiered offerings for large buyers. This evolution signals that the freelance platforms industry is widening its value capture along the full talent-management lifecycle.

By Application: Design momentum challenges project management lead

Project management tools held 23.12% of the freelance platforms market size in 2025, reflecting universal demand for agile execution across functions. Yet web and graphic design is expanding at 18.78% CAGR, fueled by AI-assisted creative workflows that lower entry barriers for SMEs seeking premium visuals.

Software development assignments continue to command premium budgets in emerging tech stacks, while sales and marketing freelancers gain ground as firms migrate to performance-linked contracts. Niche domains such as legal compliance and financial modeling surface within “other applications,” underscoring opportunities for vertical specialization. Platforms that deepen expertise within each application tier stand to capture higher wallet share and retention.

By End User: Employer demand reshapes two-sided marketplace dynamics

Freelancers remain the larger cohort at 51.66% of 2025 users, but employer onboarding is rising at an 17.95% CAGR as corporations operationalize external workforce programs. Compliance-ready portals appeal to regulated industries, ensuring taxes, benefits, and worker status are correctly handled.

On the supply side, freelancers benefit from AI-driven proposal tools that raise win rates and billing efficiency, anchoring them to the ecosystem. Marketplace success, therefore, hinges on balanced investment in employer UX and freelancer enablement, reinforcing liquidity on both sides of the freelance platforms market.

By Organization Size: Enterprise integration shifts platform priorities

Small and medium enterprises still account for 65.02% of the freelance platforms market share in 2025, mirroring the channel’s early adoption roots. Large enterprises now grow fastest at 18.55% CAGR, demanding SOC 2-compliant infrastructure, audit trails, and ERP integration. An aerospace firm saved USD 3 million after embedding a vendor management module within its USD 800 million contractor program.

Enterprise penetration drives higher average deal sizes but raises service expectations around risk mitigation and data security. Platforms investing in single-sign-on, API interoperability, and global payroll are best placed to win these high-value contracts and reinforce the freelance platforms market trajectory.

Geography Analysis

Asia-Pacific posted the highest 18.22% CAGR outlook, underpinned by rapid digitalization and policy frameworks such as ViDA electronic invoicing that simplify cross-border transactions. Companies in Japan routinely pay skilled freelancers more than USD 5,000 monthly, signaling a robust willingness to pay for top talent . Growth in Southeast Asia is likewise accelerating as local firms leapfrog traditional hiring constraints.

North America remains the revenue leader with a 32.64% share, supported by mature infrastructure and an early-adopter enterprise culture. The U.S. regulatory environment, though complex, offers clear federal frameworks that encourage compliant contractor engagement. Canada adds momentum with supportive provincial guidelines around remote work taxation.

Europe sustains steady expansion as GDPR-aligned data safeguards increase trust and as the forthcoming 2030 ViDA mandate ensures seamless intra-EU invoicing. In Latin America, currency volatility poses challenges, yet localized wallets prove effective at promoting freelance adoption. The Middle East and Africa present nascent but promising pockets, especially among tech hubs in the Gulf Cooperation Council, where government innovation agendas boost demand for specialized gig talent.

Competitive Landscape

The freelance platforms market shows moderate concentration anchored by Upwork, Fiverr, and Freelancer, yet vertical contenders and AI-native challengers chip away at category breadth. Upwork alone holds 61.25% of platform revenue, aided by 125 skill categories and enterprise integrations [3]Upwork Inc., “Strategic Partnership with Beeline,” upwork.com. Fiverr differentiates through AI-augmented creative services and freelancer equity incentives that deepen talent loyalty.

Strategic alliances intensify: Upwork partnered with Beeline to integrate marketplace talent into vendor management workflows, expanding reach to Fortune 500 procurement desks. Payoneer moved upstream by acquiring Skuad for USD 61 million, unifying payments with employer-of-record services that satisfy enterprise compliance demands.

Consolidation within Europe is visible as Freeland Group executes a seventh takeover, aiming to create an end-to-end, regionally compliant platform. Yet disruption looms from AI-native entrants like Lanceboard, which offers pre-screened talent pools and automated task assignment, targeting speed-sensitive use cases. Sustained leadership thus requires investment in vertical depth, AI transparency, and comprehensive compliance toolkits.

Freelance Platforms Industry Leaders

Upwork Global Inc.

Fiverr International Ltd.

Skyword, Inc.

Guru.com

Freelancer Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Beeline and Upwork announced strategic partnership integrating Upwork’s talent ecosystem into Beeline’s vendor management platform.

- August 2024: Payoneer completed USD 61 million acquisition of Skuad, strengthening global workforce management capabilities

- June 2024: Workhoppers, an AI-based freelancer marketplace, was acquired by an undisclosed buyer, signaling ongoing consolidation.

- April 2024: Upwork launched a multi-tier Partner Program with OpenAI, GoDaddy, and Dropbox to extend productivity tools.

Global Freelance Platforms Market Report Scope

Freelance platforms refer to the online platforms where businesses and individuals can connect with freelancers or independent professionals to collaborate on various projects or tasks. These platforms serve as intermediaries, facilitating the matching of freelancers' specialized skills and services with the specific needs of clients or businesses seeking to outsource work.

The freelance platforms market is segmented by component (platform and services), application (project management, sales and marketing, IT, web and graphic designing, and other applications), end-user (employers and freelancers), and geography (North America, Europe, Asia Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Platform |

| Services |

| Project Management |

| Sales and Marketing |

| IT and Software |

| Web and Graphic Design |

| Other Applications |

| Employers (Enterprises and SMBs) |

| Freelancers |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Platform | ||

| Services | |||

| By Application | Project Management | ||

| Sales and Marketing | |||

| IT and Software | |||

| Web and Graphic Design | |||

| Other Applications | |||

| By End User | Employers (Enterprises and SMBs) | ||

| Freelancers | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the freelance platforms market?

The global market is worth USD 8.9 billion in 2026.

How fast is the sector projected to grow?

It is expected to post a 16.32% CAGR and reach USD 21.97 billion by 2031.

Which component is expanding most quickly?

The services component is forecast to grow at an 18.05% CAGR as enterprises seek managed solutions.

Why are Asia-Pacific growth rates higher than North America?

Rapid digitalization, favorable invoicing regulations, and premium pricing for specialized skills drive APAC’s 18.22% CAGR outlook.

What technology trend most influences productivity on platforms?

Generative-AI copilots that automate routine tasks and improve matchmaking accuracy are boosting freelancer productivity and client satisfaction.

How are regulations shaping platform strategies?

Rules clarifying worker classification and mandating algorithm-bias audits compel platforms to invest in compliance tools, pushing them toward enterprise-grade services.

Page last updated on: