Closed System Transfer Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.62 Billion |

| Market Size (2031) | USD 2.97 Billion |

| Growth Rate (2026 - 2031) | 12.98% CAGR |

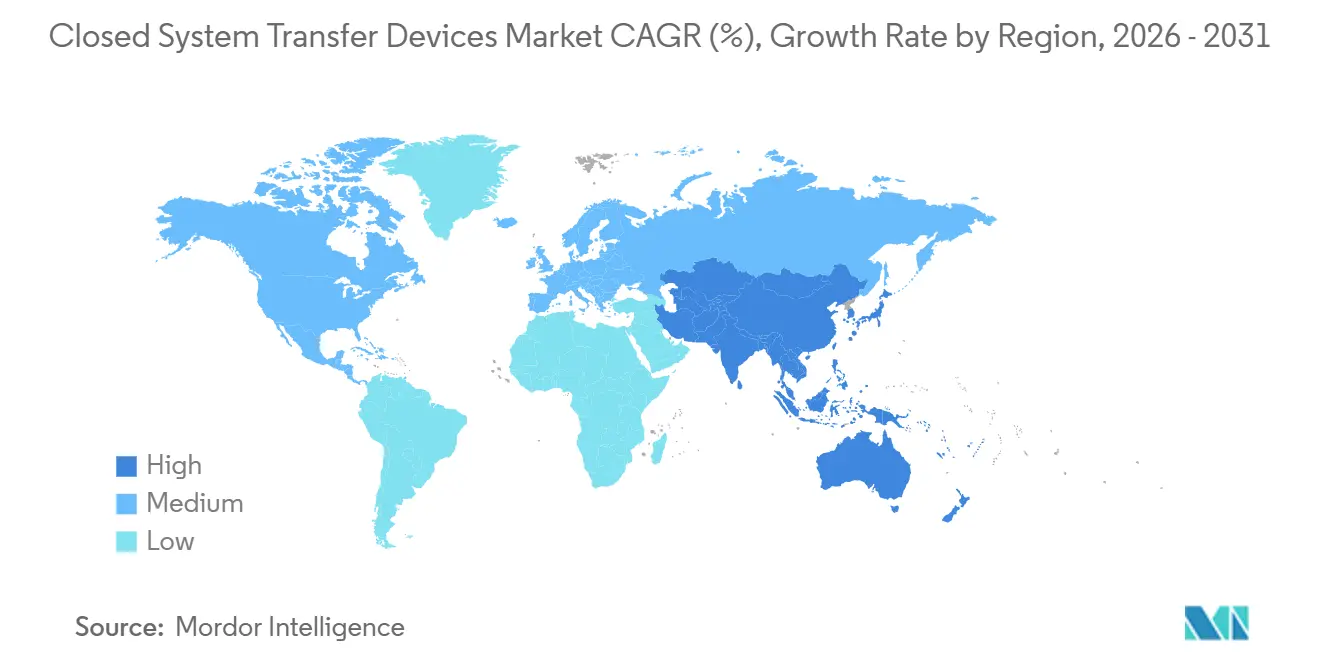

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

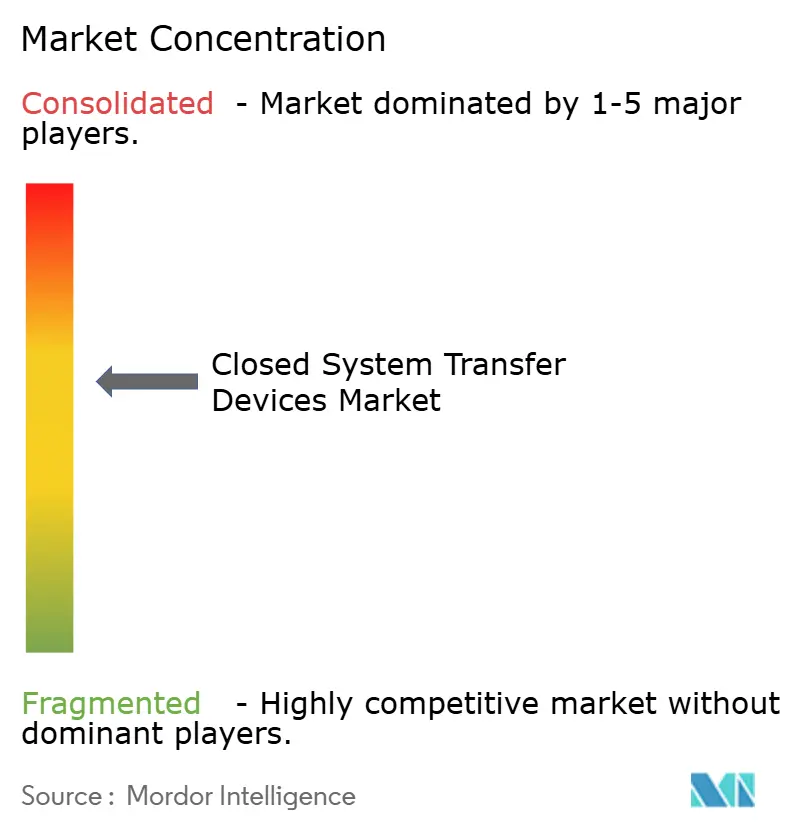

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Closed System Transfer Devices Market Analysis by Mordor Intelligence

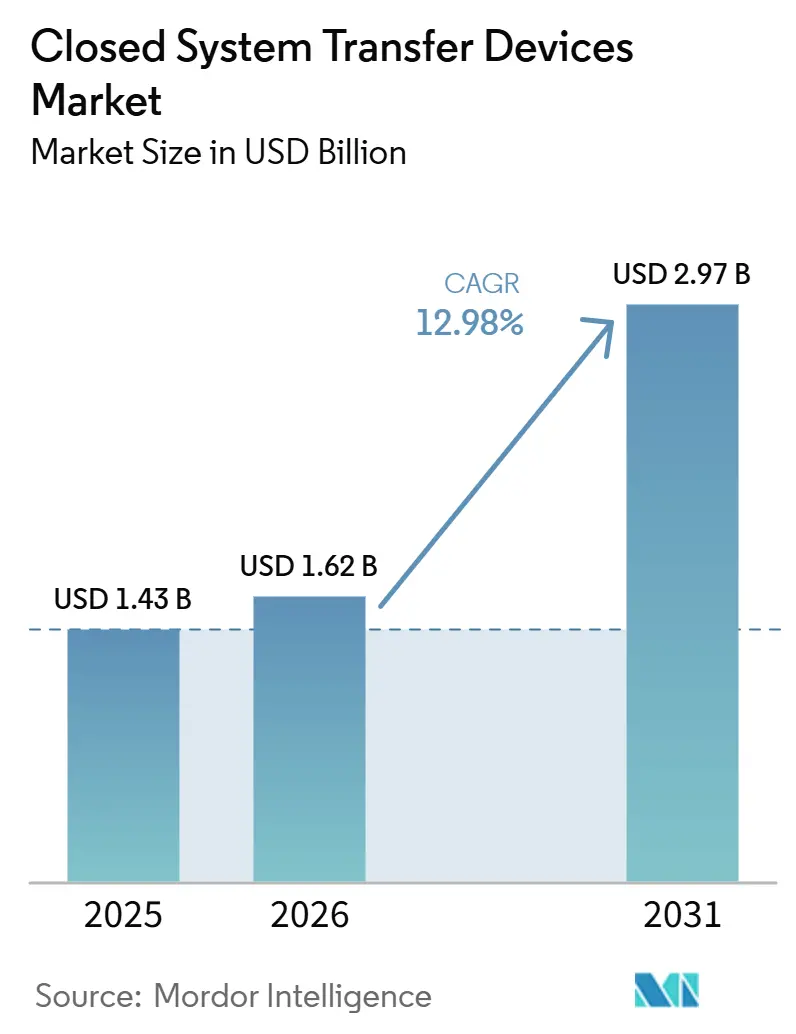

The Closed System Transfer Devices Market size is projected to expand from USD 1.43 billion in 2025 and USD 1.62 billion in 2026 to USD 2.97 billion by 2031, registering a CAGR of 12.98% between 2026 to 2031.

Growth is propelled by stricter occupational-safety rules that now make closed handling mandatory in many hospitals, a steady rise in global chemotherapy volumes, and the widening use of potent biologics that demand airtight containment. Providers that bundle training and environmental-monitoring services with their hardware are capturing multi-year contracts, suggesting that buyers increasingly view CSTDs as part of a broader safety ecosystem rather than stand-alone items. Established players defend share through proprietary connection mechanisms, yet new entrants target underserved regions with lower-cost kits, broadening geographic reach without diluting safety standards. Integrated robotic compounding suites incorporating CSTDs are also gaining traction, as pharmacy leaders seek technology that simultaneously improves accuracy and reduces staff exposure.

Key Report Takeaways

- By geography, North America led with 42.84% closed system transfer devices market share in 2025, while Asia-Pacific is forecast to expand at a 14.86 % CAGR to 2031.

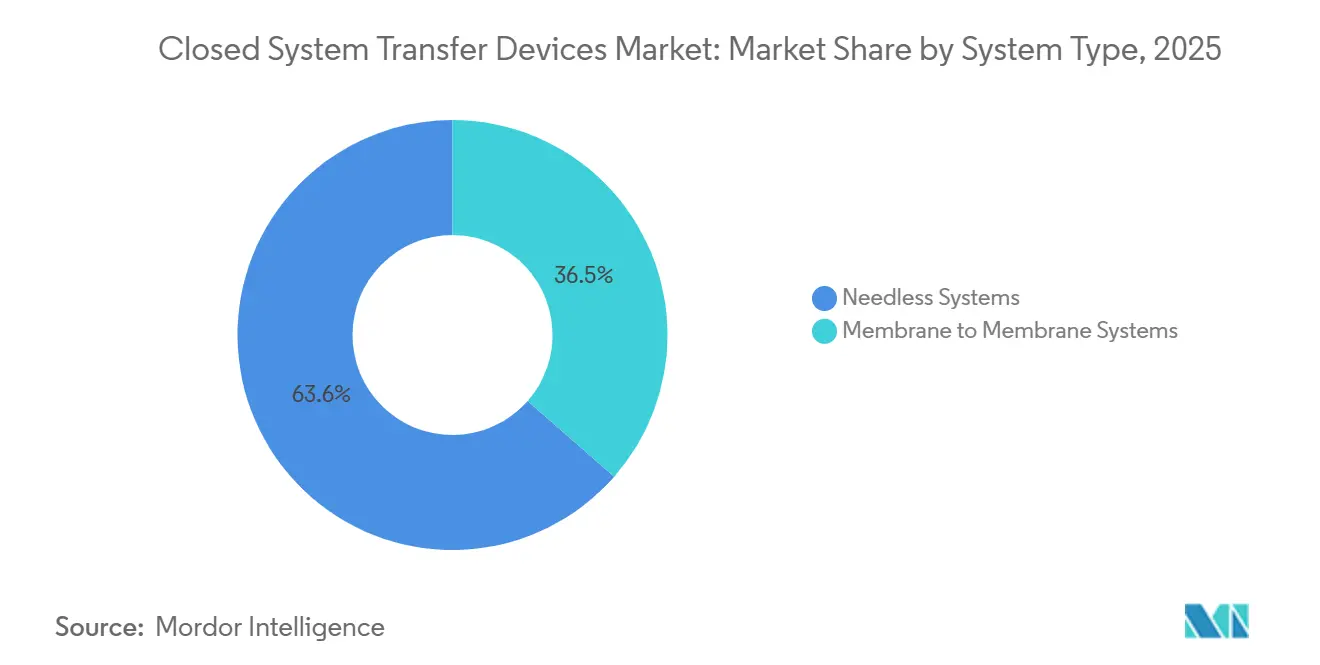

- By system type, needle-less systems accounted for 63.55% of the closed system transfer devices market size in 2025; membrane-to-membrane systems are advancing at a 13.98% CAGR through 2031.

- By closing mechanism, Luer-Lock devices held 37.62% share in 2025, whereas Push to Turn Systems are projected to grow at a 15.58% CAGR to 2031.

- By component, vial access devices captured 46.12% market share in 2025; syringe safety devices are set to grow at a 14.02% CAGR through 2031.

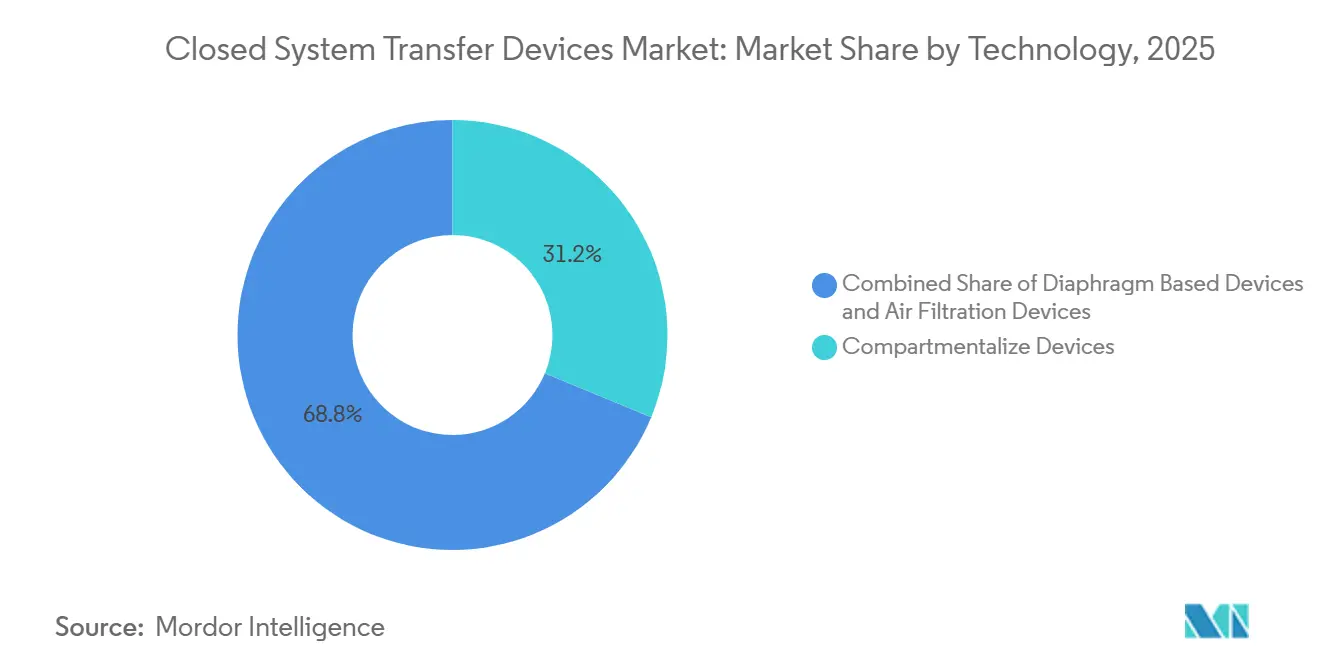

- By technology, diaphragm-based designs commanded 56.35% share in 2025, and compartmentalized devices are forecast to rise at a 14.32% CAGR to 2031.

- By end user, hospitals represented 73.44% of demand in 2025, while oncology centers are expected to post an 14.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Closed System Transfer Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Chemotherapy Volume from Rising Cancer Incidence | +3.2% | Global, with concentration in North America and Europe | Medium term (~ 3-4 years) |

| Stricter Occupational Safety Regulations Elevating Hazardous-Drug Handling Standards | +2.8% | North America & Europe, with emerging impact in Asia-Pacific | Short term (≤ 2 years) |

| Integration of CSTDs into Automated Compounding & Robotics Platforms | +1.9% | North America, Europe, developed Asia | Medium term (~ 3-4 years) |

| Expansion of Hazardous Biologics & Immunosuppressants Requiring Closed Handling | +1.5% | Global | Long term (≥ 5 years) |

| Growing Adoption of Comprehensive Safety-Culture Programs in Healthcare Systems | +1.2% | North America, Europe, Australia | Medium term (~ 3-4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Chemotherapy Volume from Rising Cancer Incidence

Cancer incidence continues to climb, with 2.04 million new cases projected in the United States alone for 2025. Larger case volumes translate into more infusion sessions, creating a cascade of demand for CSTDs at every preparation bench and bedside. Hospitals now treat higher proportions of older patients, a demographic often prescribed multi-agent regimens that elevate occupational exposure risk per dose. Facilities therefore allocate capital budgets toward devices that promise both vapor and droplet containment, a linkage that now appears in many grant proposals for new oncology wings. One noteworthy shift is that procurement committees increasingly measure proposed device impact not only by exposure data but by projected reductions in staff sick days, aligning safety investments with workforce-planning metrics.

Stricter Occupational Safety Regulations Elevating Hazardous-Drug Handling Standards

USP <800> became compendially applicable in November 2023 and has been adopted by more than 30 states, pivoting hazardous-drug guidance from recommendation to mandate[1]USP, “Hazardous Drugs—Handling in Healthcare Settings,” United States Pharmacopeia, usp.org. Similar enforcement traction is visible in provincial Canadian rules and in updated Occupational Safety and Health Administration (OSHA) references to hazardous-drug handling. Because regulators can now audit compliance down to product model numbers, purchasing decisions routinely involve the legal or risk-management office, widening the stakeholder pool. That additional scrutiny prompts suppliers to publish third-party containment data in readily digestible dashboards, evidencing a marketing trend that mirrors the regulation’s emphasis on measurable performance. An emergent inference is that regulatory pressure indirectly boosts demand for ancillary products such as environmental monitoring swabs, as institutions seek proof of ongoing compliance rather than one-time validation.

Integration of CSTDs into Automated Compounding & Robotics Platforms

Robotic compounding systems increasingly embed proprietary CSTD connectors, shrinking the number of manual steps in syringe and bag preparation. Performance studies on ICU Medical’s Diana platform report negligible microbiological contamination and tight filling accuracy for volumes above 5 mL. Pharmacy architects now allocate floor space for single-operator robotic alcoves, a layout that changes HVAC load calculations because the machine, not the operator, drives airflow needs. The automation trend also shifts skill profiles: technicians rotate toward equipment supervision, while entry-level staff handle upstream logistics such as vial unboxing. By blending mechanical precision with closed-transfer containment, integrated systems establish a new benchmark for both sterility and safety in high-throughput oncology pharmacies.

Expansion of Hazardous Biologics & Immunosuppressants Requiring Closed Handling

A growing number of monoclonal antibodies and cell-signaling inhibitors meet hazardous-drug criteria under the National Institute for Occupational Safety and Health (NIOSH) 2024 list. These molecules can adsorb to plastic surfaces, compelling buyers to scrutinize material compatibility before authorizing high-value formulary items. Hospitals increasingly develop in-house compatibility matrices that cross-reference each biologic with specific CSTD models, a practice that also guides annual staff-competency checks. Vendors respond by issuing protein-binding data in clinical dossiers, enabling pharmacists to select the least sorptive pathway for fragile biologics. A practical outcome is that procurement cycles now include laboratory-bench pilots with biologic surrogates, extending evaluation timelines but yielding more precise matchmaking between drug and device.

Restraints Impact Analysis*

| Restraint Impact Analysis | “(~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Lifecycle Cost of CSTD Implementation vs. Standard IV Components | -2.1% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| Lack of Universal Performance Standards Causing Procurement Uncertainty | -1.4% | Global | Medium term (~ 3-4 years) |

| Compatibility Challenges with Legacy IV & Infusion Infrastructure | -0.7% | Global, with concentration in facilities with older infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Lifecycle Cost of CSTD Implementation vs Standard IV Components

Full deployment of CSTDs entails acquisition, staff training, workflow redesign, and disposal, creating cost hurdles for smaller clinics. Unlike standard IV components, CSTDs must often be discarded as hazardous waste, which carries higher disposal fees by weight. Hospitals therefore perform cost-avoidance modeling that assigns dollar values to potential worker-exposure incidents, a tactic gaining traction among financial officers. Some systems negotiate volume-based rebates with suppliers, but rural facilities with lower drug throughput lack such leverage, reinforcing an urban-rural adoption divide. An emerging workaround is group purchasing organizations that aggregate demand from distributed clinics, enabling lower per-device pricing and easing entry barriers in resource-constrained settings.

Lack of Universal Performance Standards Causing Procurement Uncertainty

While NIOSH has released a draft testing protocol, final adoption remains pending[2]National Institute for Occupational Safety and Health, “Closed System Drug-Transfer Device (CSTD) Research,” Centers for Disease Control and Prevention, cdc.gov. The absence of uniform pass-fail criteria means hospitals rely on disparate test methods, complicating apples-to-apples comparison. Purchasing teams often default to vendor-supplied data, yet risk managers remain wary of marketing bias, prompting some institutions to conduct internal surrogate-vapor studies in biosafety cabinets. This bespoke testing lengthens procurement cycles and can delay capital outlay by an entire fiscal year. A side effect is that suppliers offering transparent, peer-reviewed data enjoy quicker purchasing decisions, proving that credible science doubles as a commercial accelerator in a standards vacuum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Needle-less Systems Lead While Membrane Technology Accelerates

Needle-less systems hold 63.55% Closed System Transfer Devices market share in 2025, and that dominance roots in their dual benefit of sharps elimination and vapor containment. Hospitals value the simplified credentialing these devices provide because staff already trained on needle-free connectors transition seamlessly to hazardous-drug workflows. A fresh observation is that many institutions now pair needle-less CSTDs with antimicrobial IV ports, seeking a one-stop solution for safety and infection control.

The membrane-to-membrane segment is forecast to grow at a 13.98% CAGR between 2026 and 2031, steadily enlarging its share of the Closed System Transfer Devices market size. Dual-membrane architectures provide redundant seals, a feature especially appealing for high-potency chemotherapy and emerging antibody–drug conjugates. Pharmacy managers increasingly cite vapor-containment data when justifying the higher unit price, showing value analysis committees have adopted containment efficacy as a core metric. This segment’s rise indirectly encourages cross-disciplinary collaboration because engineering departments must verify that HVAC pressure relationships support the new workflow.

By Closing Mechanism: Luer-Lock Dominance Challenged by Push to Turn Systems Innovation

Luer-Lock devices maintain 37.62% Closed System Transfer Devices market share for 2025, leveraging ISO 80369-7 standardization to plug into existing infusion ecosystems. Many institutions prefer Luer-Lock because it removes retraining costs and simplifies equipment compatibility audits. Yet the ease of twisting connections occasionally produces partial engagement errors in high-volume pharmacies, prompting safety teams to explore alternatives.

Push to Turn Systems are projected to register a 15.58% CAGR through 2031, making them the fastest-expanding subcategory within the Closed System Transfer Devices industry. Furthermore, audible and tactile feedback during locking in Click-to-Lock systems provides real-time confirmation, reducing incidence of mis-threaded connections during peak workload periods. A complementary trend is the rise of color-coded Click-to-Lock variants that visually align mating parts, an ergonomic twist that supports situational awareness in dimly lit chemotherapy units. Procurement data reveal that these intuitive connectors cut setup time per dose, allowing pharmacists to reallocate saved minutes toward verification tasks.

By Component: Vial Access Devices Maintain Leadership Position

Vial access devices account for 46.12% of the Closed System Transfer Devices market size in 2025, as every chemotherapy preparation starts at the vial interface. Their high-volume usage means marginal improvements—such as reduced priming volume—translate into measurable drug-cost savings when multiplied across thousands of doses. Hospitals newly onboarding biologics rely on vial adapters with reinforced septa that withstand multiple punctures, thereby accommodating multi-dose protocols without compromising barrier integrity.

Syringe safety devices are projected to expand at a 14.02% CAGR between 2026 and 2031, fueled by innovations that combine plunger-lock features with closed-transfer tips. A key inference is that syringe devices now double as training aids: clear plungers allow educators to demonstrate correct fluid path closure during in-service sessions. Bag access devices remain a dependable staple, yet modular accessory kits that integrate flow restrictors and air-clearing chambers are gaining mindshare as pharmacists seek fine-grained control over infusion variables.

By Technology: Diaphragm-based Devices Maintain Market Leadership

Diaphragm-based units comprise 56.35% market share within the Closed System Transfer Devices industry in 2025, leveraging stretchable elastomers that reseal after connection cycles. Their mechanical simplicity results in fewer moving parts, reducing maintenance demands in busy oncology departments. Fresh procurement data show that diaphragm-based systems often pass pressure-leak tests after more connection cycles than originally claimed, extending product longevity.

Compartmentalized devices forecast a 14.32% CAGR from 2026 to 2031, rising on the promise of discrete fluid channels that prevent aerosol escape even during pressure equalization. Air-filtration devices retain a solid niche among facilities that handle high-volatility compounds because built-in filters balance syringe pressure without manual venting. Innovations now focus on micro-textured sealing surfaces that remain supple across wide temperature bands, ensuring consistent performance in both refrigerated and ambient settings.

By End-User: Hospitals Dominate While Oncology Centers Surge

Hospitals account for 73.44% of Closed System Transfer Devices market size in 2025, reflecting centralized chemotherapy preparation and advanced regulatory oversight. Pharmacy directors find that integrated CSTD programs reduce environmental contamination counts, which in turn supports magnet accreditation audits. Teaching hospitals, in particular, leverage CSTD deployment data in research grant applications that examine occupational health outcomes.

Oncology centers are projected to grow at an 14.05% CAGR through 2031, the fastest rate among end users in the Closed System Transfer Devices market. Furthermore, the Oncology Nursing Society has published home-infusion guidelines that emphasize maintaining a closed path from vial to patient. Device makers are responding with compact, all-in-one kits that pair pre-capped syringes with tamper-evident packaging, simplifying chain of custody outside institutional walls. This shift distributes risk mitigation responsibilities to family caregivers, prompting education modules that distill safe-handling steps into smartphone-friendly formats.

Geography Analysis

North America’s 42.84% share of the Closed System Transfer Devices market in 2025 is anchored by robust enforcement of USP <800> and updated NIOSH hazardous-drug lists. U.S. hospital groups often tie CSTD investments to broader antimicrobial stewardship programs, linking chemical isolation with infection-control metrics. Canada follows a similar trajectory but exhibits provincial variation that encourages vendors to customize rollout timelines province by province. Mexico’s private oncology clinics, stimulated by cross-border patient flows, increasingly mirror U.S. safety protocols to attract international clientele. US-based group purchasing organizations extend favorable contract pricing across the continent, harmonizing access and accelerating penetration.

Europe ranks second by revenue, with its Closed System Transfer Devices industry shaped by the European Union’s Carcinogens and Mutagens Directive, which classifies hazardous drugs as occupational carcinogens. Countries such as Germany and France mandate surface contamination monitoring, so hospitals often integrate CSTD deployment into multi-year capital projects that include new clean-room construction. Eastern European clinics tap into EU structural funds to finance CSTD adoption, thereby narrowing a historical safety gap with Western counterparts. Brexit has introduced separate regulatory paths for the United Kingdom, yet most NHS trusts converge on ISO standards, sustaining cross-channel product interchangeability. A discernible pattern is that European tenders increasingly specify device reusability counts, reflecting environmental priorities under the EU Green Deal.

Asia-Pacific is the fastest-growing geography, projected to compound at 14.86% annually through 2031 as cancer incidence rises and hospital infrastructure expands. China’s new provincial cancer centers include CSTD budgets in their master plans, signaling that the technology is perceived as a baseline requirement rather than a premium add-on. Japan’s mature health system prioritizes low-dead-space designs to minimize wastage of high-cost biologics, illustrating how reimbursement pressure shapes technical preference. India’s metro hospitals pilot low-cost CSTD variants while rural centers experiment with rental models that bundle device supply with disposal services, revealing adaptive business strategies to match heterogeneous purchasing power. Across Asia-Pacific, device makers often partner with local distributors that handle language-specific labeling and training, shortening the adoption curve.

Competitive Landscape

The top three vendors—Becton, Dickinson & Co. (BD), ICU Medical, and Equashield—control a significant share of the market, an outcome of entrenched intellectual-property portfolios and global distribution footprints. BD’s 2024 acquisition of a critical-care division for USD 4.2 billion broadens its infusion-therapy suite, signaling a strategic push toward vertically integrated medication-safety bundles clinicalservicesjournal.com. ICU Medical leverages its closed-system pumps to lock customers into an ecosystem that spans preparation to administration, allowing cross-selling of CSTD components. Equashield differentiates via its dual-membrane designs, securing rapid traction in facilities managing high-potency chemotherapy.

Second-tier competitors concentrate on niche innovations such as biologic-optimized pathways or single-use kits for home infusion. These challengers rarely compete head-to-head on broad portfolios; instead they target unmet micro-segments, forcing incumbents either to innovate swiftly or acquire. Patent filings reveal a shift toward ergonomic features, indicating that user experience now ranks alongside containment efficacy as a market differentiator. An observable trend is that investors favor suppliers able to document not only safety metrics but total-cost-of-ownership savings, reflecting the market’s maturation from compliance-driven to value-driven purchasing.

White-space opportunities persist in low-resource regions where price sensitivity remains high. Start-ups experimenting with recycled-plastic diaphragms aim to cut unit costs without sacrificing barrier performance, a move that could disrupt volume play in emerging markets if validated. Meanwhile, established companies fortify their positions with training portals and virtual-reality modules that reduce onboarding time, effectively converting education into a competitive moat. As performance standards evolve, the ability to supply peer-reviewed validation data at regulator-level granularity will likely separate long-term winners from opportunistic entrants.

Closed System Transfer Devices Industry Leaders

-

Becton, Dickinson and Company

-

ICU Medical, Inc.

-

Baxter International Inc.

-

B. Braun Melsungen AG

-

Equashield LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: BD displayed new delivery formats for biologics and patient self-care at Pharmapack 2025, underscoring its strategy to integrate closed-transfer safety features into broader drug-delivery solutions.

- December 2024: NIOSH updated its List of Hazardous Drugs, expanding agents that require closed handling and prompting hospitals to reassess device-compatibility matrices.

- October 2024: BD and Ypsomed announced a collaboration to advance self-injection systems for high-viscosity biologics, pairing prefillable syringes with an autoinjector platform that maintains compatibility with BD’s existing closed-transfer portfolio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the closed-system transfer device (CSTD) market as worldwide sales of sterile, single-use devices that create sealed pathways to block hazardous-drug vapors, aerosols, or droplets during compounding, transport, and administration. According to Mordor Intelligence analysts, the scope covers needleless and membrane-to-membrane systems, vial access parts, syringe safety units, bag or line adapters, and related connectors supplied to hospitals, oncology clinics, and specialty infusion centers.

Scope exclusion: stand-alone infusion pumps, generic IV lines, and aftermarket cleaning kits are not counted.

Segmentation Overview

-

By System Type

- Needle-less Systems

- Membrane-to-Membrane Systems

-

By Closing Mechanism

- Color-to-Color Alignment Systems

- Luer-Lock Systems

- Push-to-Turn Systems

- Click-to-Lock Systems

-

By Component

- Syringe Safety Devices

- Vial Access Devices

- Bag Access Devices

- Other Accessories

-

By Technology

- Compartmentalized Devices

- Diaphragm-based Devices

- Air-Filtration Devices

-

By End-User

- Hospitals

- Oncology Centers

- Others

-

Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Structured conversations with oncology pharmacists, compounding technicians, biomedical engineers, and hospital buyers across North America, Europe, and key Asia-Pacific markets validate secondary findings, reveal hidden cost drivers, and tune penetration ratios that shape our revenue pool.

Desk Research

We begin by mining tier-one public sources such as NIOSH hazard alerts, USP <800> compliance bulletins, WHO cancer incidence files, UN Comtrade shipment codes, and EMA recall notices to size demand, track regulatory momentum, and spot usage surges. Company 10-Ks, hospital procurement tenders, and peer-reviewed pharmacy journals flesh out price ranges and adoption curves across regions.

To benchmark revenues, Mordor's team interrogates D&B Hoovers for company financials and screens global news on Dow Jones Factiva. Patent abstracts from Questel and shipment tallies from Volza further refine volume assumptions. The list above is illustrative; many additional authoritative feeds are consulted before figures are locked.

Market-Sizing & Forecasting

We launch a top-down build that starts with country-level chemotherapy procedure counts, multiplies them by average doses, and then applies validated CSTD penetration rates to create the addressable unit base. Supplier shipment samples and channel checks offer a bottom-up sense-check on volumes and average selling prices, with gaps bridged through ratio analysis. Key variables tracked include new cancer incidence, hospital bed additions, USP <800> enforcement timelines, pharmacy automation uptake, average selling price drift, and device replacement cycles. Forecasts rely on multivariate regression, with scenario analysis layered on to capture sudden regulatory or reimbursement shocks.

Data Validation & Update Cycle

Outputs pass automated variance screens, peer review, and senior sign-off. Mordor analysts refresh every twelve months and trigger interim updates after material events such as major recalls or guideline changes, ensuring clients receive the latest view.

Why Our Closed System Transfer Devices Baseline Commands Reliability

Published estimates often diverge because firms apply different device mixes, adoption curves, and price-erosion paths. By anchoring scope strictly to sealed-pathway devices and refreshing data annually, Mordor limits drift and maintains transparency.

Key gap drivers include varied inclusion of accessories, differing USP <800> compliance timelines, and contrasting ASP assumptions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.43 B | Mordor Intelligence | - |

| USD 1.49 B | Global Consultancy A | Omits membrane-to-membrane adapters; applies uniform 7 % ASP erosion |

| USD 1.98 B | Industry Analytics B | Counts aftermarket cleaning kits and assumes rapid Asia-Pacific uptake |

In sum, Mordor Intelligence delivers a balanced, clearly traceable baseline that decision-makers can reproduce and trust.

Key Questions Answered in the Report

How big is the Closed System Transfer Devices (CSTD) Market?

The CSTD Market size is expected to reach USD 1.62 billion in 2026 and grow at a CAGR of 12.98% to reach USD 2.97 billion by 2031.

Why are CSTDs important in oncology settings?

Chemotherapy agents can be mutagenic, teratogenic, or carcinogenic; CSTDs provide a physical barrier that lowers occupational exposure for pharmacists, nurses, and support staff during drug preparation and administration.

Are CSTDs mandated by U.S. regulations?

USP <800> requires healthcare facilities that handle hazardous drugs to implement CSTDs for administration when possible, and many state boards of pharmacy include enforcement provisions.

How do membrane-based CSTDs differ from needle-less systems?

Membrane-based devices rely on dual flexible barriers that reseal upon disconnection, while needle-less systems focus on eliminating sharps; both aim for full containment but differ in connection mechanics and preferred clinical scenarios.

Can CSTDs be used in home-care environments?

Yes; home-infusion guidelines recommend portable CSTD kits that maintain a closed pathway from pharmacy to patient, protecting caregivers and ensuring consistent safety outside hospital settings.

What factors influence CSTD total cost of ownership?

Costs include device acquisition, staff training, workflow adaptation, and hazardous-waste disposal; assessing all components provides a clearer picture of return on safety investment for healthcare facilities.

Page last updated on: