Clinical Analytics Platforms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

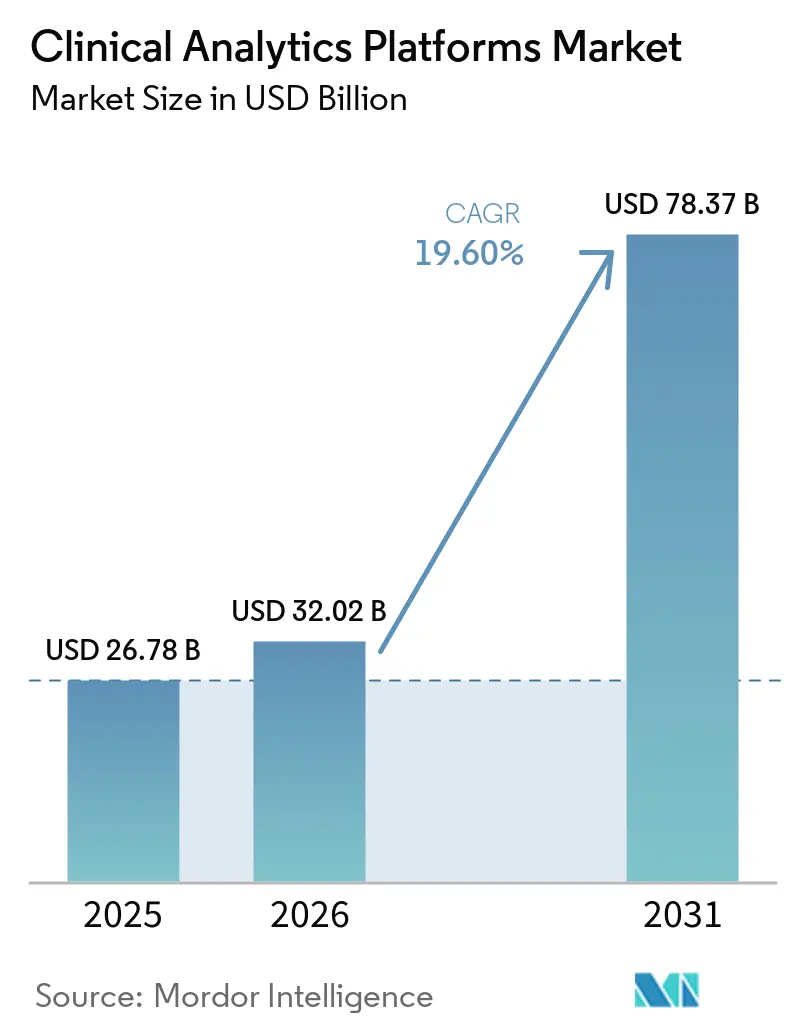

| Market Size (2026) | USD 32.02 Billion |

| Market Size (2031) | USD 78.37 Billion |

| Growth Rate (2026 - 2031) | 19.60% CAGR |

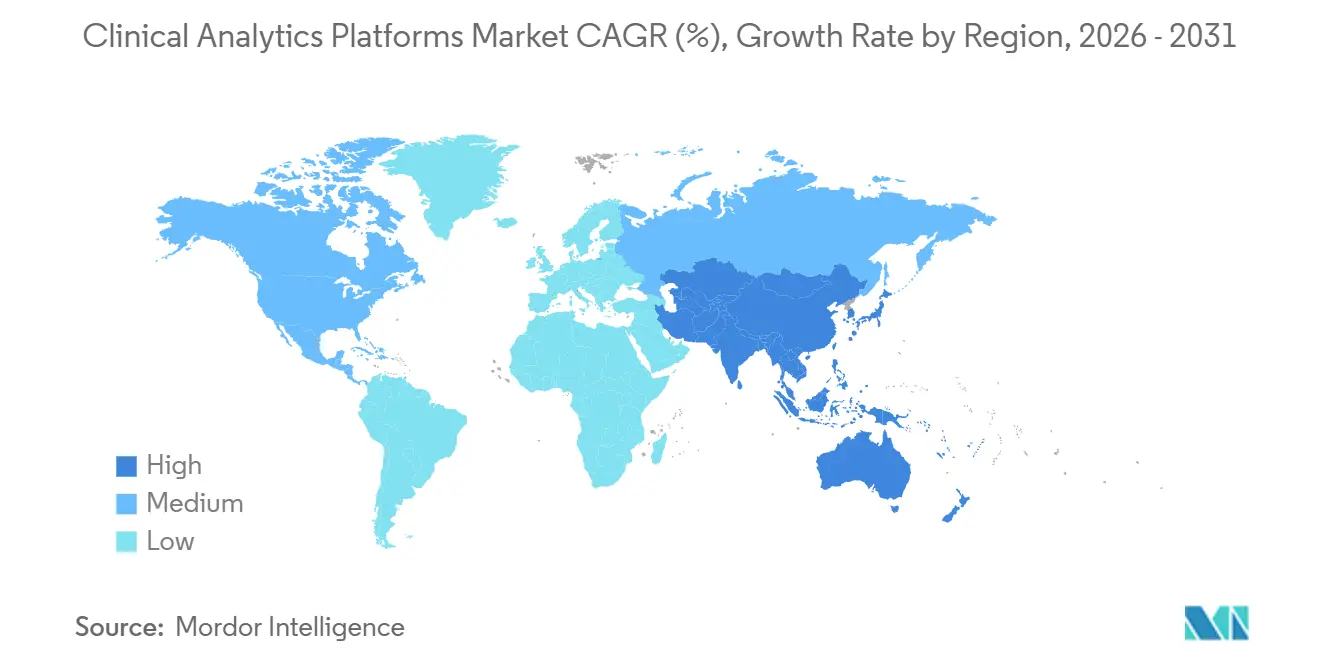

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

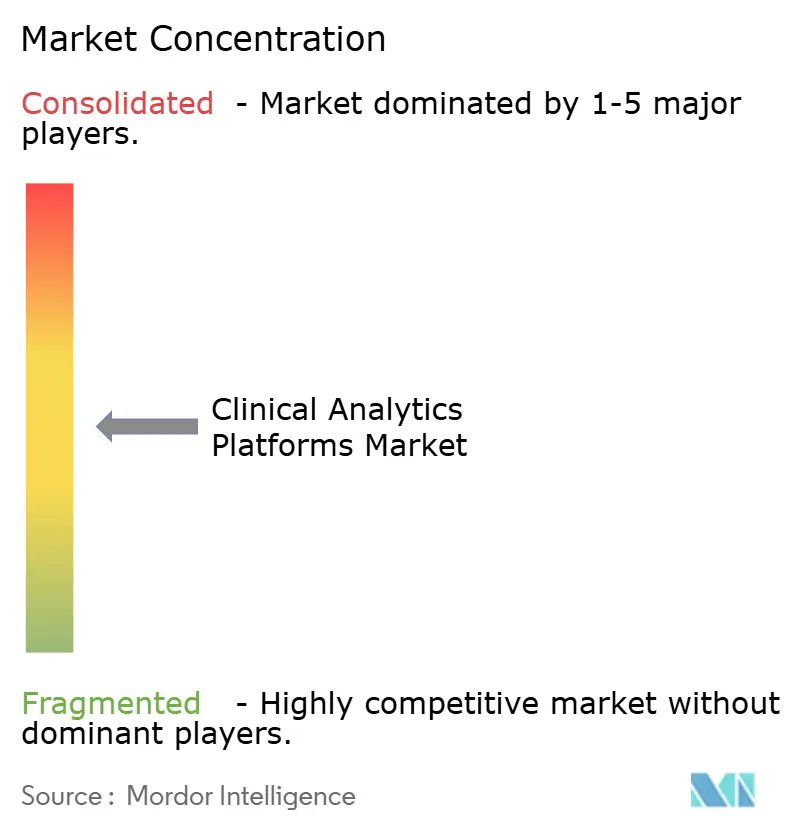

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Analytics Platforms Market Analysis by Mordor Intelligence

The Clinical Analytics Platforms Market size is expected to grow from USD 26.78 billion in 2025 to USD 32.02 billion in 2026 and is forecast to reach USD 78.37 billion by 2031 at 19.60% CAGR over 2026-2031.

Growth in the clinical analytics platforms market is driven by the shift toward value-based reimbursement, increased adoption of FHIR-based interoperability rules, and the rising use of agentic AI across EHR, claims, imaging, and genomics data. These advancements are transforming clinical data from a compliance tool into a critical operational layer that impacts care quality, utilization, and reimbursement performance. The market is witnessing higher demand for unified platforms that integrate ingestion, governance, analytics, and AI execution, replacing isolated tools designed for single workflows.

Key Report Takeaways

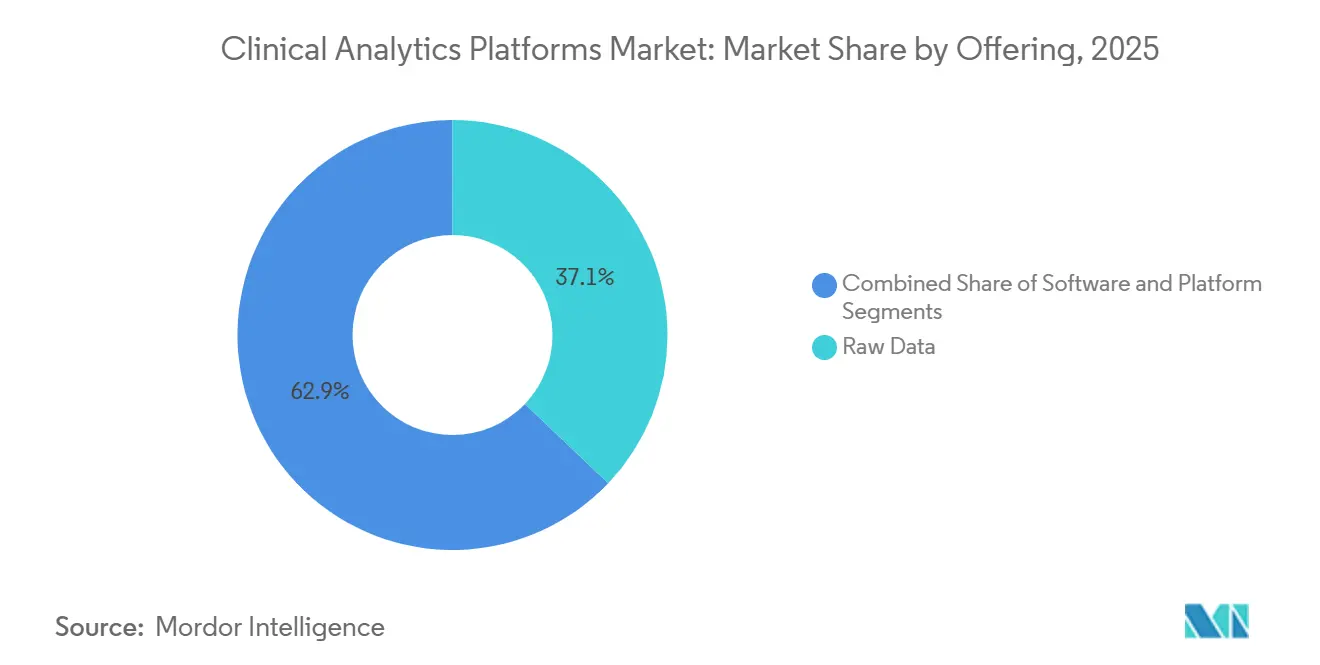

- By offering raw data led with 37.10% share in 2025, while the platform is projected to expand at a 22.70% CAGR through 2031.

- By deployment model, on-premises held 60.95% of the clinical analytics platforms market size in 2025, while cloud-based deployment recorded the highest projected CAGR at 22.55% through 2031.

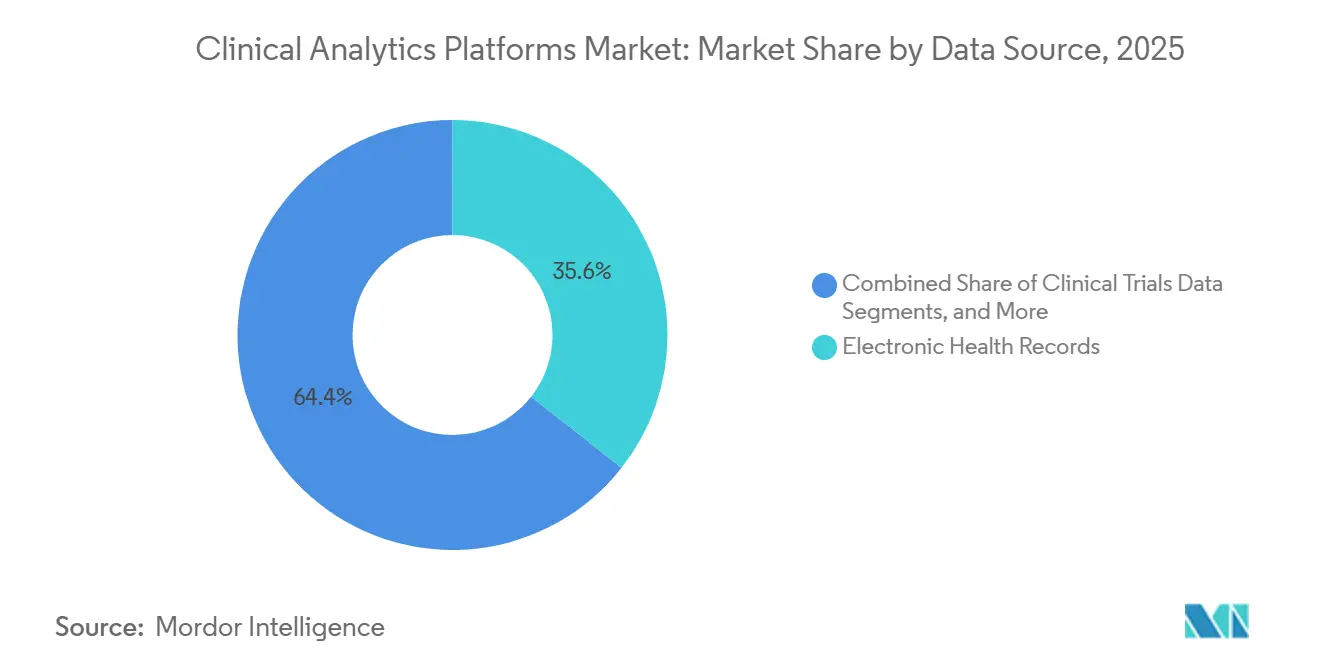

- By data source, electronic health records accounted for 35.60% share in 2025, while clinical trials data is expected to grow at a 20.57% CAGR through 2031.

- By use case, healthcare represented 65.70% share in 2025, while life sciences is projected to grow at a 20.98% CAGR through 2031.

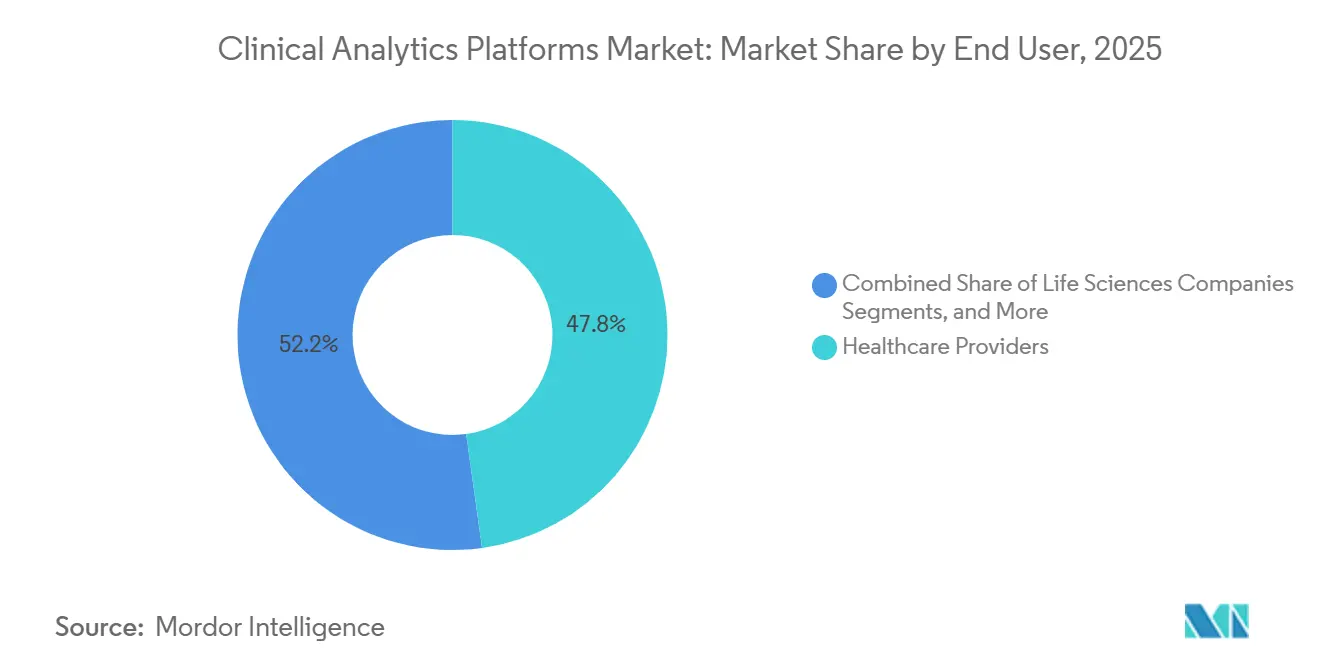

- By end user, healthcare providers held 47.80% share in 2025, while life sciences companies are projected to expand at a 21.65% CAGR through 2031.

- By geography, North America captured 41.12% of the clinical analytics platforms market share in 2025, while Asia-Pacific is projected to grow at a 20.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clinical Analytics Platforms Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Value-based care and outcome-linked reimbursement | +3.2% | Global, concentrated in North America | Medium term (2-4 years) |

| Explosion of multi-modal clinical data across care settings | +3.8% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Cloud and AI/ML modernization of healthcare data infrastructure | +4.5% | Global | Short term (≤ 2 years) |

| Regulatory openness to real-world evidence and precision medicine | +2.5% | North America and EU | Medium term (2-4 years) |

| Bulk FHIR and population-level API maturation | +2.0% | North America, with spillover to EU and APAC | Medium term (2-4 years) |

| CMS interoperability and prior-authorization API mandates | +2.8% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Value-Based Care and Outcome-Linked Reimbursement

CMS introduced the ACCESS Model on July 5, 2026, a 10-year voluntary initiative linking reimbursements to measurable outcomes in chronic disease management rather than service volume. By 2030, CMS aims to place all Traditional Medicare beneficiaries in accountable care relationships, driving demand for analytics to monitor performance, stratify risk, and enable early intervention.[1]Centers for Medicare & Medicaid Services, “CMS Interoperability and Prior Authorization Final Rule CMS-0057-F,” Centers for Medicare & Medicaid Services, cms.gov Source: Nippon Telegraph and Telephone Corporation, “NTT Precision Medicine Platform,” NTT Group, group.ntt This shift rewards organizations that proactively manage risks during care, positioning clinical analytics platforms as integral to reimbursement processes. Vendors combining population health analytics with actionable workflows are better positioned than those focusing solely on retrospective reporting.

Cloud and AI/ML Modernization of Healthcare Data Infrastructure

Healthcare systems are consolidating fragmented analytics into cloud-native platforms that support operational analytics, clinical AI, and research from a unified data layer. UNC Health’s adoption of Microsoft Fabric highlights efforts to streamline data-to-insight processes. Cloud modernization reduces engineering bottlenecks, accelerating model development and workflow deployment. IQVIA’s launch of IQVIA.ai in March 2026, supported by over 100 AI patents and 150 intelligent agents, underscores the rapid integration of AI into clinical workflows.[2]IQVIA, “IQVIA Unveils IQVIA.ai, a Unified Agentic AI Platform Powered by NVIDIA,” Business Wire, businesswire.com Vendors offering scalable infrastructure with curated, clinically relevant data are likely to gain a competitive edge.

CMS Interoperability and Prior-Authorization API Mandates

CMS finalized the Interoperability and Prior Authorization Final Rule on January 17, 2024, requiring payers to implement FHIR-based APIs by January 1, 2027.[3]Centers for Medicare & Medicaid Services, “ACCESS Model Request for Applications,” CMS Innovation Center, cms.gov This rule, while aimed at administrative simplification, also drives the creation of FHIR-native data pipelines supporting analytics like care gap detection and risk scoring. Compliance investments expand the data landscape for analytics, benefiting vendors adept at integrating claims, authorizations, and clinical records into comprehensive patient narratives. Organizations treating this mandate as an analytics upgrade rather than a compliance task are positioned for faster growth.

Regulatory Openness to Real-World Evidence and Precision Medicine

The FDA announced on December 15, 2025, that it would accept real-world evidence in drug and device applications without requiring identifiable patient data. De-identified databases, such as cancer registries and EHR repositories, are now recognized as valid sources. This change strengthens the link between clinical analytics platforms and regulatory workflows, expanding their role beyond commercial analytics. Since 2016, only 35 drugs, biologics, or vaccines included real-world evidence in applications, highlighting significant growth potential. Vendors with governed, traceable, and research-ready datasets are well-positioned for high-value contracts with life sciences companies.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Data privacy, security, and governance burden | -2.3% | Global | Long term (≥ 4 years) |

| Data quality, standardization, and legacy interoperability | -2.8% | Global | Medium term (2-4 years) |

| Post-deployment model drift and fragmented accountability | -1.5% | North America and EU | Medium term (2-4 years) |

| Workflow backlash from alert fatigue, low trust, and hidden costs | -1.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data Privacy, Security, and Governance Burden

Clinical AI workflows manage sensitive health data across ingestion, inference, storage, and monitoring, often exceeding the capabilities of traditional compliance models. This challenge grows when platforms operate across providers, payers, and life sciences, each with unique controls and approval processes. The clinical analytics platforms market is under pressure to adopt privacy-focused architectures like federated analytics, localized processing, and strict auditability. Japan’s NTT Precision Medicine Platform, built on OMOP CDM with a federated design, demonstrates how analytical value can be achieved without moving patient data, which is critical in privacy-sensitive regions.

Data Quality, Standardization, and Legacy Interoperability

The effectiveness of clinical analytics depends on high-quality source data, but many environments remain fragmented with varied coding systems, free-text notes, incomplete records, and disconnected care settings. Data often requires extensive harmonization for longitudinal analysis, predictive modeling, or regulatory evidence generation, increasing costs and time. Japan’s NTT platform and Germany’s HIVEPRO initiative highlight the importance of structured models and standardized data layers in addressing these challenges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platforms Emerge as the Enterprise Integration Layer

In 2025, Raw Data held a 37.10% share of the clinical analytics platforms market, highlighting significant investments in data acquisition, de-identification, harmonization, and creating research-ready assets. Software remains critical, offering modular tools for clinical decision support, population health, and revenue cycle analytics. Platforms are the fastest-growing segment, with a 22.70% CAGR during 2026-2031, driven by the shift toward unified environments integrating ingestion, governance, analytics, and AI inferencing.

Vendor strategies reflect this shift. IQVIA reported USD 16.3 billion in revenue in 2025, leveraging proprietary healthcare data and advancing AI-enabled platforms and workflow tools. Flatiron Health’s 2026 launch of Telescope, a multi-agent adaptive analytics platform, demonstrates how vendors monetize data through AI-native interfaces, simplifying infrastructure navigation.

By Deployment Model: On-Premises Dominates Today, Cloud Architecture Captures Future Investment

On-premises deployment accounted for 60.95% of revenue in 2025, driven by institutional data sovereignty, prior infrastructure investments, and strict PHI handling preferences. Many integrated delivery networks rely on private environments for sensitive workloads tied to legacy processes. However, cloud-based deployment is the fastest-growing segment, with a 22.55% CAGR during 2026-2031, as investments shift to scalable AI-ready infrastructure.

Innovaccer’s 2026 partnership with Snowflake highlights rising cloud adoption, linking the Gravity platform with Snowflake’s AI Data Cloud to support enterprise-scale AI workflows. Hybrid deployment remains vital for organizations balancing local control over legacy systems with cloud-based analytics and AI expansion, especially in Europe and parts of Asia-Pacific, where data residency and sovereign AI infrastructure priorities influence decisions.

By Data Source: EHR Anchors the Market, Clinical Trials Data Accelerates

Electronic Health Records held a 35.60% market share in 2025, serving as the primary structured source of longitudinal clinical data. Claims data remains essential for insights into utilization and cost patterns. Clinical Trials Data is the fastest-growing source, with a 20.57% CAGR during 2026-2031, driven by demand for research efficiency and regulatory policy changes. EHR data anchors the market, but the fastest growth is in evidence generation and trial strategy.

Life sciences companies increasingly seek longitudinal evidence for regulatory reviews, commercial planning, and precision medicine workflows. Inputs from imaging, diagnostics, and pathology are growing as models improve in handling unstructured data. SOPHiA GENETICS processed 108,000 genomic analyses on its DDM Platform in Q1 2026, a 22% year-over-year increase, showcasing the rapid scaling of AI-driven genomic analytics.

By Use Case: Healthcare Leads, Life Sciences Redefines Value Creation

Healthcare accounted for 65.70% of demand in 2025, driven by use cases like clinical decision support, population health, and operational analytics. Life Sciences is the fastest-growing use case, with a 20.98% CAGR during 2026-2031, as pharmaceutical and medtech companies increase spending on real-world evidence, trial feasibility, and patient cohort identification. The largest use case is tied to care delivery, while the fastest growth is linked to evidence generation and pipeline productivity.

Tempus AI’s 2026 collaboration with Gilead exemplifies this shift, providing enterprise-wide access to its Lens platform and multimodal oncology datasets for real-world evidence and AI-driven insights. These partnerships reflect the industry’s move toward recurring access, continuous learning, and integrated workflows.

By End User: Healthcare Providers Hold Share, Life Sciences Companies Accelerate

Healthcare Providers represented 47.80% of demand in 2025, encompassing hospitals, integrated delivery networks, and specialty care organizations using analytics for readmission reduction, care gap closure, and quality reporting. Healthcare Payers remain the second-largest end-user group, leveraging analytics for claims review, prior authorization, and risk adjustment. Life Sciences Companies are the fastest-growing end users, with a 21.65% CAGR during 2026-2031, as pharmaceutical and medtech firms expand platform-based evidence and trial analytics.

Tempus AI’s collaboration with NYU Langone Health on a prospective observational study highlights the shift toward long-term data infrastructure partnerships. SOPHiA GENETICS’ collaborations with MD Anderson Cancer Center and Mount Sinai Health System in 2026 further extend its reach across research and genomic testing environments, solidifying its network of over 990 organizations. These developments show life sciences and research institutions increasingly institutionalizing analytics platforms as core infrastructure.

Geography Analysis

In 2025, North America accounted for 41.12% of the clinical analytics platforms market, making it the largest and most mature region for enterprise clinical analytics adoption. The U.S. drives growth in the region due to value-based care, extensive EHR penetration, and payer-provider data exchange requirements. Additionally, CMS-0057-F encouraged the adoption of FHIR-based APIs to enhance data flow across claims, prior authorizations, and provider records. Canada contributes through provincial health data initiatives, while Mexico, though in earlier stages, is advancing within large urban hospital systems.

Asia-Pacific is the fastest-growing region in the clinical analytics platforms market, with a projected CAGR of 20.20% through 2031. Growth is driven by healthcare digitalization, expanding clinical trial activities, and government focus on structured health data environments. In January 2026, Fujitsu Japan and JMDC linked anonymized DPC hospital data with insurer records, covering 20 million records, enhancing patient journey analysis for pharmaceutical and public sector applications. China is scaling rapidly, with platforms like MSTATA supporting over 1,200 SCI publications since 2024, reflecting widespread adoption across hospital networks.

Europe remains technically advanced but is shaped by privacy, sovereignty, and regulatory infrastructure. Germany’s NUKLEUS platform expanded in July 2025 to support adaptive clinical platform studies and leverage statutory health insurance and cancer registry data across university hospitals. The Middle East and Africa are advancing through sovereign AI healthcare investments, highlighted by the Oracle, Cleveland Clinic, and G42 partnership announced in May 2025. South America, despite progress in digitalization in Brazil and Argentina, remains the smallest regional market.

Competitive Landscape

In the clinical analytics platforms market, established players like IQVIA, Optum, Merative, and InterSystems compete with AI-driven challengers such as Tempus AI, Innovaccer, SOPHiA GENETICS, Komodo Health, and Flatiron Health. Incumbents capitalize on extensive datasets, enterprise workflow access, and long-standing customer relationships, while challengers focus on speed, diverse modalities, and natural-language interfaces to gain traction.

The platform's adoption by 19 of the top 20 pharmaceutical companies highlights how incumbents are leveraging existing relationships to establish AI leadership. In 2026, vendors shifted strategies toward ecosystem depth and product integration over standalone offerings. Flatiron Health launched Telescope, a multi-agent adaptive analytics platform for life sciences, strengthening its position in oncology data, real-world evidence, and AI-driven trial planning. Tempus AI expanded partnerships with Merck, Gilead, NYU Langone Health, and Blood Cancer United, showcasing the bundling of multimodal data and AI tools into extended collaborations. Buyers increasingly prioritize integration speed and reduced operational friction, making ecosystem alignment a competitive advantage in the clinical analytics platforms market.

Clinical Analytics Platforms Industry Leaders

Optum, Inc.

Oracle Corporation

SAS Institute Inc.

IQVIA Holdings Inc.

eClinicalWorks, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Flatiron Health introduced Flatiron Telescope at the ASCO Annual Meeting in Chicago. The platform enables real-time oncology study feasibility assessments and patient cohort insights, supported by over 25 research acceptances, including digital twin modeling for NSCLC treatment prediction and LLM-based analysis of clinical trial adoption.

- April 2026: SOPHiA GENETICS partnered with Mount Sinai Health System to implement the SOPHiA DDM Platform for cancer research and genomic testing. This collaboration expands the platform's global network to over 990 institutions.

- March 2026: IQVIA launched IQVIA.ai, an AI platform developed with NVIDIA, integrating advanced tools with proprietary data. The platform is already utilized by 19 of the top 20 pharmaceutical companies.

- March 2026: Charité and Schwarz Digits established Schwarz Charité Health Data GmbH, with Schwarz Digits holding a 75% stake. The venture focuses on developing the HIVEPRO health data harmonization platform on STACKIT's sovereign cloud, ensuring data residency in Germany.

Global Clinical Analytics Platforms Market Report Scope

As per the scope of the report, clinical analytics platforms are enterprise software solutions designed to collect, aggregate, and analyze medical and operational data. They translate raw clinical information (e.g., EHRs, lab results, claims) into actionable insights, helping healthcare providers and pharmaceutical companies improve patient care, reduce costs, and streamline clinical workflows.

The clinical analytics platforms market is segmented by offering, deployment model, data source, use case, end-user, and geography. By offering, the market includes raw data, software, and platform. By deployment model, the market is segmented into cloud-based, on-premises, and hybrid. By data source, the market is categorized into electronic health records, claims data, clinical trials data, registries & real-world evidence, imaging & diagnostics, lab & pathology, and others. By use case, the market is segmented into healthcare and life sciences. By end-user, the market is segmented into healthcare providers, healthcare payers, life sciences companies, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Raw Data |

| Software |

| Platform |

| Cloud-based |

| On-premises |

| Hybrid |

| Electronic Health Records |

| Claims Data |

| Clinical Trials Data |

| Registries & Real-World Evidence |

| Imaging & Diagnostics |

| Lab & Pathology |

| Others |

| Healthcare |

| Life Sciences |

| Healthcare Providers |

| Healthcare Payers |

| Life Sciences Companies |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Raw Data | |

| Software | ||

| Platform | ||

| By Deployment Model | Cloud-based | |

| On-premises | ||

| Hybrid | ||

| By Data Source | Electronic Health Records | |

| Claims Data | ||

| Clinical Trials Data | ||

| Registries & Real-World Evidence | ||

| Imaging & Diagnostics | ||

| Lab & Pathology | ||

| Others | ||

| By Use Case | Healthcare | |

| Life Sciences | ||

| By End User | Healthcare Providers | |

| Healthcare Payers | ||

| Life Sciences Companies | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the size of the clinical analytics platforms space in 2026 and where is it expected to reach by 2031?

It is valued at USD 32.02 billion in 2026 and is projected to reach USD 78.37 billion by 2031, expanding at a 19.60% CAGR.

Which region leads global demand for clinical analytics platforms?

North America leads with 41.12% share in 2025, supported by mature EHR adoption, value-based care programs, and FHIR-based interoperability mandates.

Which region is growing the fastest through 2031?

Asia-Pacific is the fastest-growing region, with a projected CAGR of 20.20% through 2031 as digital health infrastructure and clinical trial activity expand.

Which offering category is growing the fastest?

Platform is the fastest-growing offering, with a 22.70% CAGR through 2031, as buyers shift toward integrated environments that combine data, governance, and AI.

Why are life sciences companies becoming more important buyers?

Life sciences is the fastest-growing use case at 20.98% CAGR and life sciences companies are the fastest-growing end users at 21.65% CAGR because they are using these platforms for real-world evidence, trial design, and cohort selection.

What is the biggest deployment shift in this space?

On-premises still held 60.95% share in 2025, but cloud-based deployment is growing fastest at 22.55% CAGR as organizations invest in scalable AI-ready infrastructure.

Page last updated on: