Clinical Data Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.63 Billion |

| Market Size (2031) | USD 6.75 Billion |

| Growth Rate (2026 - 2031) | 13.20% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Clinical Data Management Market Analysis by Mordor Intelligence

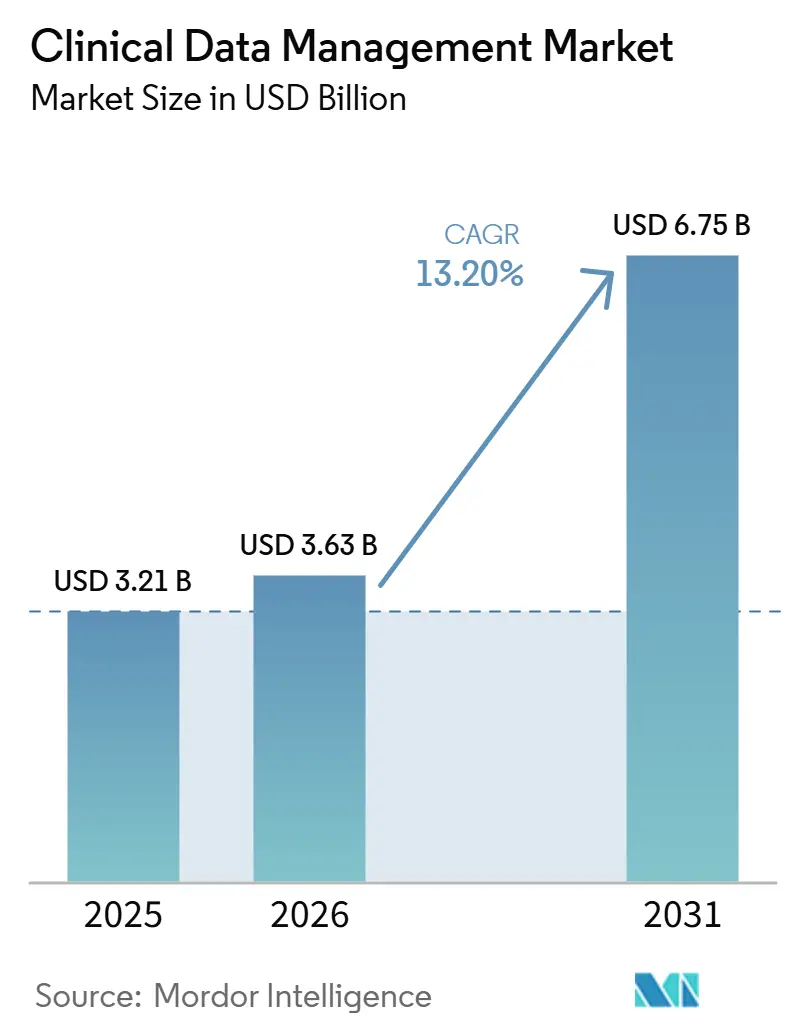

The Clinical Data Management Market size is projected to expand from USD 3.21 billion in 2025 and USD 3.63 billion in 2026 to USD 6.75 billion by 2031, registering a CAGR of 13.20% between 2026 to 2031.

Trial designs have become more complex as sponsors manage longer protocols, broader endpoints, and data from wearables, ePRO tools, imaging systems, and EHR-linked records, rather than relying only on case report forms. Sponsors and CROs now view the clinical data management market as a core operating layer, as faster database lock, cleaner submission packages, and stronger inspection readiness depend on effective data management. Stricter audit trail review under ICH E6(R3), along with broader acceptance of AI-assisted query handling, has shifted many software upgrades from optional investments to required spending. Platform breadth, validated AI features, and seamless integration across EDC, coding, analytics, and reporting workflows now define competitive positioning in the clinical data management market.

Key Report Takeaways

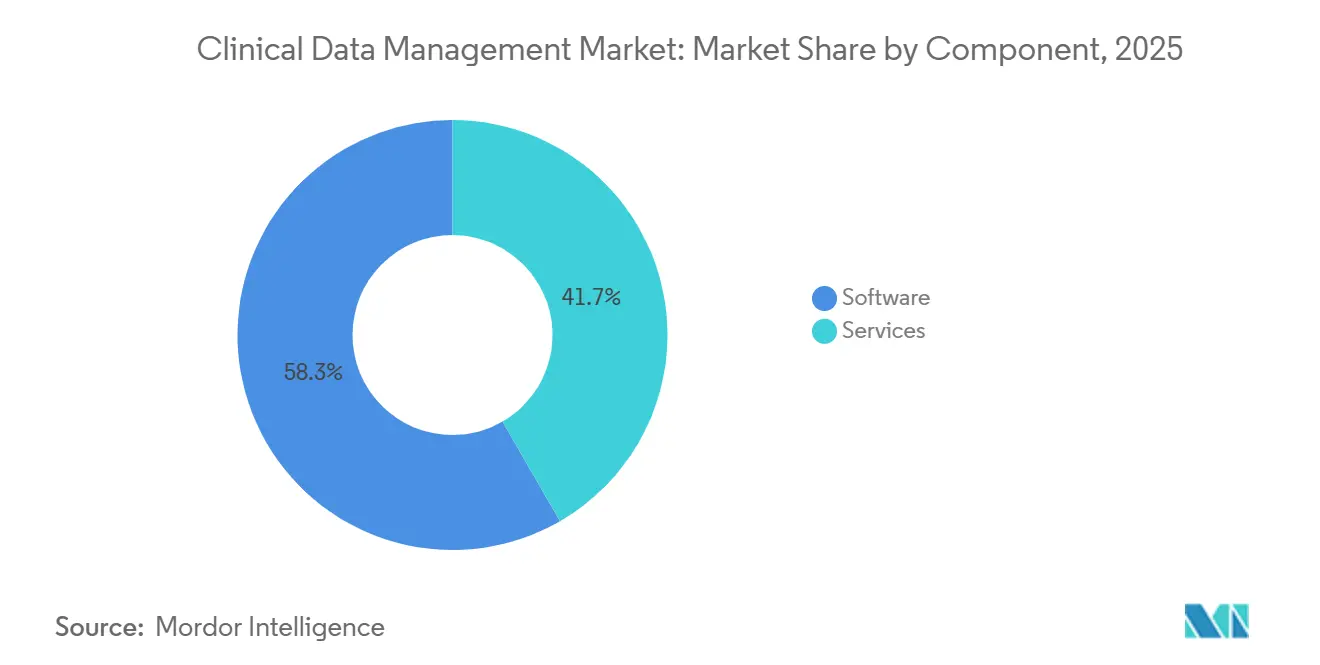

- By component, software led with 58.34% revenue share in 2025, while services are projected at a CAGR of 14.53% through 2031.

- By deployment mode, cloud-based deployment held 55.45% of the clinical data management market in 2026 and is expected to grow at a CAGR of 13.67% through 2031.

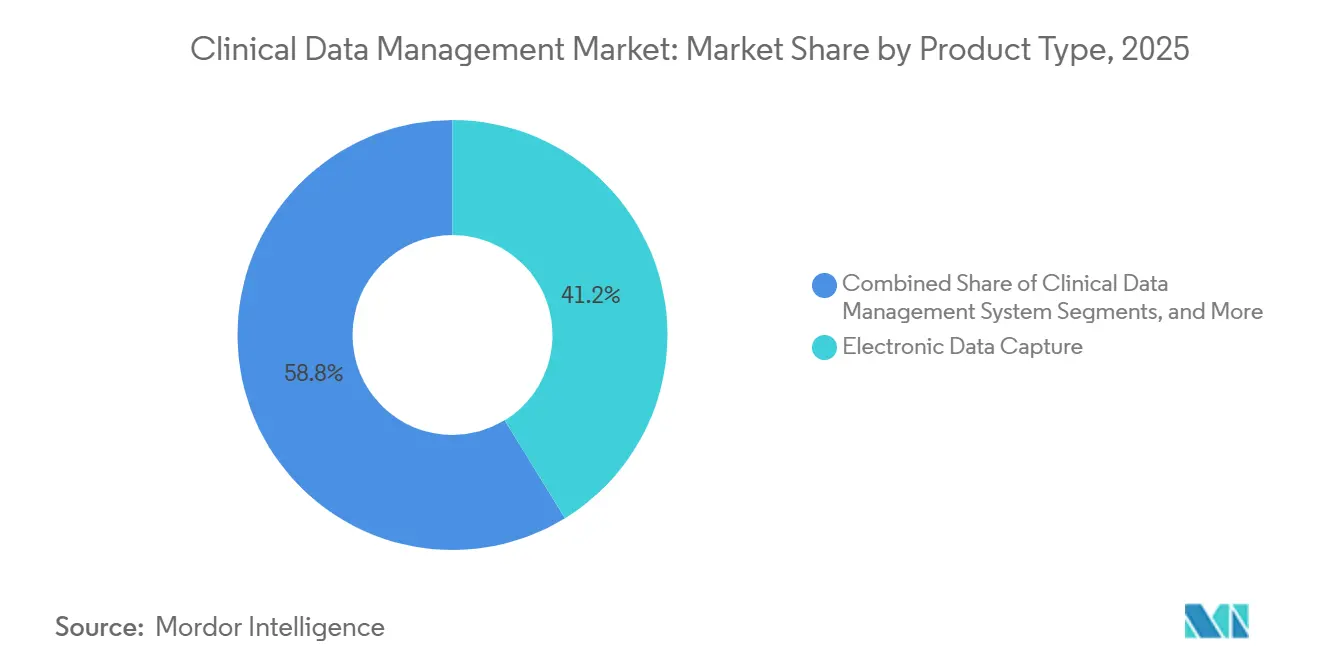

- By product type, electronic data capture accounted for 41.24% share in 2025, while clinical data management system platforms are forecast to expand at a 15.35% CAGR through 2031.

- By application, data collection and capture held 38.67% share in 2025, while submission and regulatory reporting is expected to grow at a 14.67% CAGR through 2031.

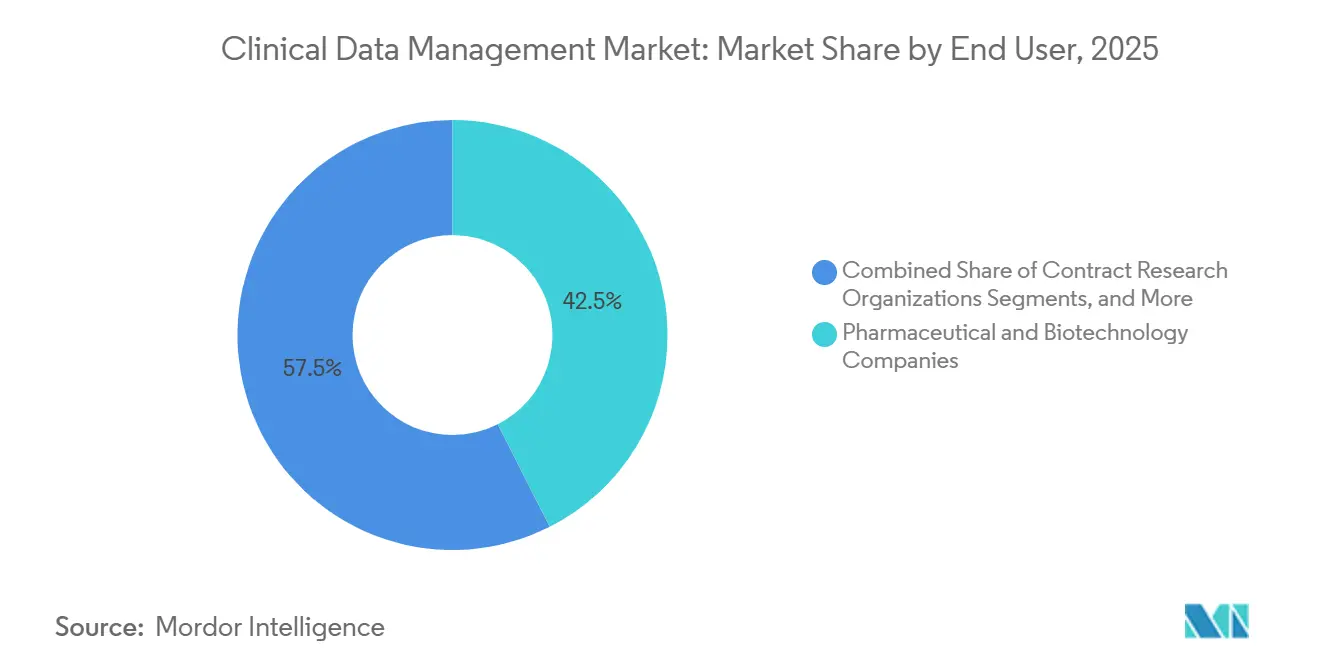

- By end user, pharmaceutical and biotechnology companies captured 42.54% share in 2025, while contract research organizations are projected to grow at the fastest CAGR of 15.55% through 2031.

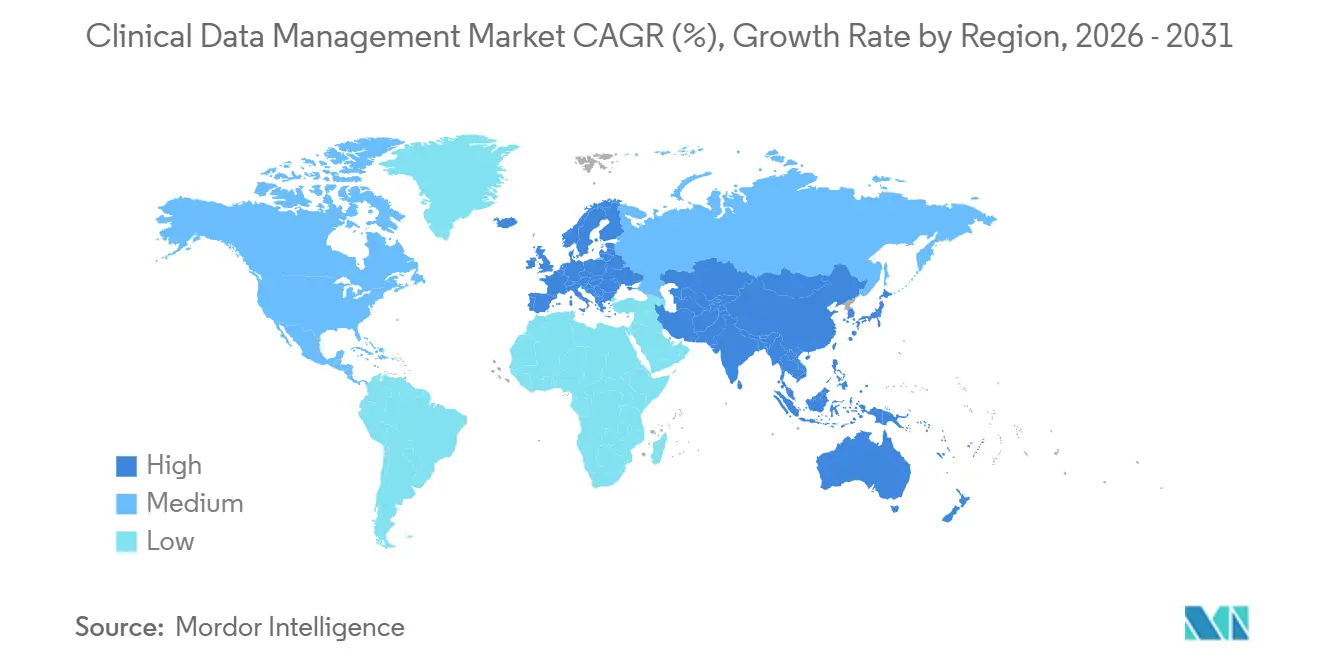

- By geography, North America led with 39.56% share in 2025, while Asia-Pacific is expected to expand at a 14.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Clinical Data Management Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising protocol complexity and multimodal data volume | +2.3% | Global, with highest intensity in North America and Europe | Medium term (2-4 years) |

| Regulatory pressure for audit-ready electronic records | +1.8% | Global, with strongest relevance in North America, Europe, and Japan | Short term (≤ 2 years) |

| Expansion of decentralized and hybrid trials | +2.0% | Global, with fastest uptake in North America and Asia-Pacific | Medium term (2-4 years) |

| AI-enabled data cleaning, coding, and reconciliation | +2.5% | Global, led by North America and Europe | Long term (≥ 4 years) |

| EHR-EDC interoperability and site workflow simplification | +1.5% | North America and Europe, with spillover into Asia-Pacific | Medium term (2-4 years) |

| Rising outsourcing of clinical operations to CROs | +2.0% | Global, with India and China serving as key delivery hubs | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Protocol Complexity and Multimodal Data Volume

Modern oncology and rare disease studies increasingly combine imaging, wearable signals, eCOA inputs, and external laboratory feeds with conventional case report forms, pushing manual workflows beyond practical limits. The Tufts Center for the Study of Drug Development reported a 36% increase in average protocol complexity scores over the decade ending in 2024, with Phase II oncology and cell and gene therapy studies driving much of the rise.[1]Tufts Center for the Study of Drug Development, “Protocol Complexity Trends in Clinical Research,” Tufts University, csdd.tufts.edu In the clinical data management market, each protocol amendment can trigger new edit-check programming, database revisions, and validation work, increasing the cost of every scientific change. Vendors are responding with metadata-driven study setup tools, and Veeva highlighted automated EDC configuration completed in seven API calls from structured protocol metadata in its 2026 trend report.

Regulatory Pressure for Audit-Ready Electronic Records

The FDA’s finalized October 2024 guidance clarified that cloud-based clinical systems carry the same 21 CFR Part 11 obligations as on-premise systems, addressing a long-standing purchasing concern among some conservative users. ICH E6(R3), expected to become operational in 2025, will raise expectations by making planned and risk-based audit trail review a direct Good Clinical Practice requirement during active trial conduct.[2]U.S. Food and Drug Administration, “Electronic Systems, Electronic Records, and Electronic Signatures in Clinical Investigations, Questions and Answers,” FDA, fda.gov Large Phase III trials can generate substantial volumes of audit trail entries, making continuous manual review difficult to sustain at scale. This pressure is shifting the clinical data management market toward systems that support automated anomaly detection, cleaner documentation, and ongoing monitoring rather than end-stage review.

AI-Enabled Data Cleaning, Coding, and Reconciliation

AI functionality within EDC and CDMS environments is shortening query cycles and reducing a part of the human workload that has historically consumed a large share of trial operations. Veeva’s 2026 trend report described industry use cases in which AI-supported workflows reduced query resolution windows from 15 to 30 days to 2 to 5 days, while centralized monitoring tools continued scanning live trial data for outliers and unusual patterns. Novo Nordisk also deployed AI for automated data validation and system testing in 2025, indicating that large sponsors are moving beyond pilots and embedding AI into regulated processes. However, the clinical data management market still faces a regulatory boundary because any AI-driven action that creates or resolves a query becomes an electronic record subject to validation and change-control expectations.

Expansion of Decentralized and Hybrid Trials

Decentralized and hybrid studies distribute data collection across homes, mobile devices, telehealth encounters, and local care settings, creating more integration work within the clinical data management market. A 2025 research letter in npj Digital Medicine found that the gap between sponsor expectations and real-world decentralized trial data quality was tied more to system interoperability than to patient participation issues. Sponsors are also redesigning studies around critical data points, improving the value of clean and timely data even when total collection volume does not rise at the same pace.[3]npj Digital Medicine, “Understanding the Gap Between Expectations and Reality in Decentralized Clinical Trials,” Nature Portfolio, nature.com DIA’s March 2025 discussion of decentralized trial challenges identified integration between site eSource tools and sponsor EDC environments as a leading technical problem, while Medidata and CRIO responded in March 2026 by linking CRIO eSource to the Medidata Platform across more than 2,500 research sites in nearly 30 countries.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High validation and change-control burden for regulated systems | -1.2% | Global, with strongest effect in North America, Europe, and Japan | Short term (≤ 2 years) to Medium term (2-4 years) |

| Fragmented data architecture across trial platforms | -0.8% | Global, with greatest severity in multi-CRO and multi-country trials | Medium term (2-4 years) to Long term (≥ 4 years) |

| Shortage of skilled clinical data management talent | -1.2% | Global, with strongest effect in North America, Europe, and Japan | Short term (≤ 2 years) to Medium term (2-4 years) |

| Integration risk across legacy and cloud systems | -0.8% | Global, with greatest severity in multi-CRO and multi-country trials | Medium term (2-4 years) to Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Validation and Change-Control Burden for Regulated Systems

Validated clinical systems require Installation Qualification (IQ), Operational Qualification (OQ), and Performance Qualification (PQ) documentation, controlled access structures, and durable audit trails, which can extend implementation timelines compared to standard enterprise software. The FDA continues to emphasize disciplined validation and change control for regulated electronic systems, regardless of deployment model. In the clinical data management market, routine upgrades and protocol amendments can create additional requirements across validation, training, database logic, edit checks, and documentation, making vendor-led validation support increasingly important, especially for smaller biotech users.

Fragmented Data Architecture Across Trial Platforms

Most contemporary trials collect data from multiple systems, including Electronic Data Capture (EDC), Clinical Trial Management System (CTMS), Interactive Response Technology (IRT), electronic Clinical Outcome Assessment (eCOA), eConsent, safety tools, laboratory systems, imaging repositories, and external Electronic Health Record (EHR) feeds. The clinical data management market requires significant cross-platform reconciliation because these systems often use different data structures, Application Programming Interfaces (APIs), and audit trail formats. Veeva’s 2026 Clinical Data Trend Report identifies the removal of EHR-to-EDC transcription as a high industry priority, while site eSource adoption remains limited by sponsor-driven technology choices that may not align with site preferences. Multi-CRO studies add further complexity, as each Clinical Research Organization (CRO) partner may use its own platform stack and governance model, slowing database lock timelines and increasing project management demands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Maintains Dominance as Services Accelerate

Software is expected to hold 58.34% of the clinical data management market share in 2025, reflecting strong sponsor preference for subscription-based platforms that reduce on-premise revalidation cycles. The software layer now extends beyond basic data capture by integrating coding, risk-based quality tools, analytics, and submission support in one environment. This broader scope helps large vendors retain installed accounts, as buyers see less value in maintaining multiple disconnected point solutions. The segment also benefits from the need for continuous updates as regulations, protocol designs, and artificial intelligence use cases evolve.

Services are expanding faster, with a 14.53% compound annual growth rate projected through 2031, as sponsors seek external support for execution, oversight, and ongoing optimization. Contract Research Organizations are running studies for sponsors while also packaging data strategy, artificial intelligence monitoring, and workflow design into longer-term service relationships. Alcon’s reported 45% same-day data entry rate across monitored sites in 2025 shows how usage behavior within digital systems is becoming part of service quality measurement. This trend strengthens the link between platform capability and managed-service value while keeping software in the lead.

By Deployment Mode: Cloud-Based Extends Lead Across Trial Types

Cloud-based deployment is expected to hold 55.45% of the clinical data management market in 2026, while also registering the fastest projected compound annual growth rate of 13.67% through 2031. This position reflects clear advantages in update delivery, remote access, study scaling, and multi-site coordination rather than a short-term replacement cycle. The FDA’s 2025 guidance supports adoption by clarifying that cloud systems and on-premise systems must meet the same compliance standard under 21 CFR Part 11. This clarification reduces procurement hesitation among buyers that delayed migration due to perceived regulatory uncertainty.

Cloud deployment also supports the broader shift toward decentralized studies, artificial intelligence-assisted review, and multi-party collaboration. These use cases depend on faster data exchange and easier access across sponsors, Contract Research Organization teams, and site users, which isolated legacy environments make harder to manage. The clinical data management market also benefits from cloud’s ability to standardize release timing and reduce the operational burden of local infrastructure upkeep. However, on-premise systems remain relevant in some large organizations with strict residency rules or deeply customized internal architectures.

By Product Type: EDC Anchors the Market While CDMS Platforms Surge

Electronic Data Capture is expected to hold a 41.24% share in 2025, making it the largest product category in the clinical data management market. Electronic Data Capture still functions as the core transaction layer for interventional trials because every subject visit, form entry, and edit check depends on it. Long-standing regulatory familiarity and broad site experience strengthen its position, as users understand how it fits into inspection-ready workflows. Vendors continue to enhance Electronic Data Capture with artificial intelligence-enabled query handling, cleaner site interfaces, and faster protocol deviation alerts at the point of entry.

Clinical Data Management System platforms are projected to grow at a 15.35% compound annual growth rate through 2031, making them the fastest-moving product type in the clinical data management market. Sponsors are seeking consolidated environments that bring coding, data cleaning, reporting, and submission preparation closer together instead of relying on multiple loosely linked tools. The Medidata and CRIO partnership announced in March 2026 illustrates this expansion by connecting site-level eSource directly into the Medidata Platform across more than 2,500 research sites. In effect, Clinical Data Management System platforms are expanding into the central interoperability layer for trial data flows.

By Application: Data Collection Leads While Regulatory Reporting Accelerates

Data Collection and Capture is expected to command 38.67% of the clinical data management market size in 2025, keeping it in the leading application position. Every trial begins with the capture of clean, timely, and attributable data at the source. New tools, such as artificial intelligence-assisted entry support, device-linked data feeds, and eSource connections, are improving throughput while strengthening this application. As trials become more distributed, this application remains the first point at which data quality can be protected or lost.

Submission and Regulatory Reporting is the fastest-growing application, with a 14.67% compound annual growth rate projected through 2031, as the burden of compliant submission packages continues to rise. Sponsors need structured Study Data Tabulation Model and Analysis Data Model datasets, clear metadata, and inspection-ready outputs that can move quickly once a database is locked. PhaseV’s March 2026 launch of AI Conductor captures this direction by automating Electronic Data Capture integration, Study Data Tabulation Model mapping, Analysis Data Model dataset generation, statistical code production, and publication-ready outputs for FDA submission. Demand is strongest among organizations seeking to reduce the time between lock and submission without expanding manual teams.

By End User: Pharma Anchors Demand as CROs Drive the Fastest Growth

Pharmaceutical and biotechnology companies are expected to hold a 42.54% share in 2025, making them the largest end-user group in the clinical data management market. Their lead comes from the scale of their trial pipelines and their role as the main buyers of enterprise Electronic Data Capture and platform licenses. Large sponsors usually set the digital standards that flow through site networks, service providers, and study partners. Their platform choices shape software demand and the service models surrounding those systems.

Contract Research Organizations are projected to expand at a 15.55% compound annual growth rate through 2031, making them the fastest-growing end-user segment. Contract Research Organizations benefit as direct users and buyers of platforms and as service providers building managed data offerings on sponsor-selected technology. The August 2025 IQVIA and Veeva partnership reflects this model by positioning IQVIA as a Veeva CRO Clinical Data Partner after the companies resolved prior disputes. This arrangement shows how the clinical data management market is linking platform ownership and outsourced execution more closely.

Geography Analysis

North America is expected to hold 39.56% of the clinical data management market share in 2025, maintaining its leading regional position. The region benefits from a strong base of large biopharma sponsors, established contract research organization (CRO) capacity, and a supportive Food and Drug Administration (FDA) environment for cloud-native systems. FDA Bioresearch Monitoring activity in 2025 and 2026 is expected to keep electronic record deficiencies in focus, supporting continued upgrade cycles across sponsor and CRO accounts. The United States remains the primary demand center, while Canada and Mexico are gaining relevance as trial locations that feed data into U.S.-managed platforms.

Europe remains the second-largest region in the clinical data management market, with Germany, the United Kingdom, and France accounting for a major share of demand. The region benefits from a large trial base, mature regulatory expectations, and sustained demand for systems that support multi-country compliance. The European Medicines Agency’s Clinical Trial Regulation 536/2014, enforced through the Clinical Trials Information System (CTIS) environment since 2024, has increased demand for platforms with stronger standardization and multi-jurisdiction capabilities. This requirement supports vendors that offer reliable audit trails and efficient submission coordination across countries.

Asia-Pacific is the fastest-growing geography in the clinical data management market, with a projected CAGR of 14.56% through 2031. China is seeing stronger demand as electronic clinical data submission standards modernize and trial registrations expand, while Japan continues to rely on Pharmaceuticals and Medical Devices Agency (PMDA)-aligned electronic submission requirements. India is strengthening its position as a cost-competitive delivery hub for outsourced clinical data management services, supported by a skilled analyst base and modernized trial approval frameworks. The Middle East and Africa and South America remain smaller in absolute value, but they are gaining relevance as multinational sponsors seek broader patient access and faster site startup.

Competitive Landscape

The clinical data management market remains moderately concentrated at the enterprise tier, where Veeva Systems, IQVIA, Medidata Solutions, Oracle Life Sciences, and ICON compete for large, multi-study mandates. These vendors have expanded beyond electronic data capture (EDC) to offer integrated environments that combine quality oversight, analytics, and submission support within a validated structure. Sponsors increasingly prefer fewer core vendors and stronger accountability across the full trial workflow. As a result, platform scope and compliance depth have become key barriers to entry, helping vendors with broad capabilities capture high-value accounts.

A clear example of strategic repositioning is expected in August 2025, when IQVIA and Veeva are set to announce long-term clinical and commercial partnerships and resolve all prior disputes. This move would indicate a shift in the clinical data management market from direct platform competition toward ecosystem-based partnerships that strengthen customer retention. Veeva’s May 2026 announcement of Falcon is expected to expand automation across document processing, health authority correspondence, and safety case triage. Large vendors are likely to strengthen their market position by embedding artificial intelligence (AI) into compliance-sensitive workflows that smaller firms may find difficult to validate at scale.

The mid-market and specialist tiers remain more fragmented. Vendors such as Castor EDC, OpenClinica, Medrio, YPrime, and Parexel’s integrated data services compete on speed, flexibility, therapeutic fit, and pricing, rather than platform breadth alone. Newer entrants are addressing workflow gaps that larger players have not fully solved. Medable’s June 2026 Digital Data Flow Agent is expected to focus on protocol-to-JavaScript Object Notation (JSON) automation, while Clymb Clinical’s May 2026 Data Mapper is expected to support AI-driven Study Data Tabulation Model (SDTM) and Analysis Data Model (ADaM) mapping.

Clinical Data Management Industry Leaders

IQVIA

Medidata Solutions, Inc.

Parexel International Corporation

Veeva Systems Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Oxurion NV commercially launched the eTMF module for its Exagis eClinical platform, adding AI-assisted study design, data standardization, adaptive randomization optimization, and operational analytics.

- June 2026: Medable Inc. launched its Digital Data Flow (DDF) Agent to convert clinical trial protocols into CDISC USDM 4.0-compliant structured JSON and automate downstream system configuration.

- May 2026: Veeva Systems announced Veeva Falcon, an agentic platform for clinical, regulatory, and safety workflows, with early adopter availability targeted for November 2026.

- May 2026: Clymb Clinical launched Data Mapper, an AI-driven SDTM and ADaM mapping platform that automated CDISC-aligned mapping specifications and ADaM derivation frameworks.

- March 2026: Medidata (Dassault Systèmes) and CRIO formed a strategic partnership to connect CRIO eSource with the Medidata Platform across more than 2,500 research sites in about 30 countries.

- October 2025: Medidata expanded its collaboration with Sanofi to deploy AI-enabled clinical trial data management across Sanofi's trial portfolio and replace standalone legacy tools.

Global Clinical Data Management Market Report Scope

As per the scope of the report, Clinical data management (CDM) is the process of collecting, cleaning, and managing patient data during clinical trials to ensure it is accurate, reliable, and compliant with regulatory standards. It is the critical backbone of medical research that transforms raw trial data into the high-quality evidence needed to approve new drugs and therapies.

The clinical data management market is segmented by component, deployment mode, product type, application, end user, and geography. By component, the market includes software and services. By deployment mode, the market is segmented into cloud-based, on-premise, and hybrid. By product type, the market is categorized into electronic data capture, clinical data management system platforms, clinical trial management integration suites, clinical data analytics and reporting tools, and clinical data standards and validation tools. By application, the market is segmented into data collection and capture, data cleaning and query management, coding and dictionary management, safety and adverse event reconciliation, and submission and regulatory reporting. By end user, the market includes pharmaceutical and biotechnology companies, contract research organizations, medical device companies, academic and research institutions, and hospitals and healthcare providers. By geography, the market is analyzed across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Software |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Electronic Data Capture |

| Clinical Data Management System Platforms |

| Clinical Trial Management Integration Suites |

| Clinical Data Analytics and Reporting Tools |

| Clinical Data Standards and Validation Tools |

| Data Collection and Capture |

| Data Cleaning and Query Management |

| Coding and Dictionary Management |

| Safety and Adverse Event Reconciliation |

| Submission and Regulatory Reporting |

| Pharmaceutical and Biotechnology Companies |

| Contract Research Organizations |

| Medical Device Companies |

| Academic and Research Institutions |

| Hospitals and Healthcare Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Product Type | Electronic Data Capture | |

| Clinical Data Management System Platforms | ||

| Clinical Trial Management Integration Suites | ||

| Clinical Data Analytics and Reporting Tools | ||

| Clinical Data Standards and Validation Tools | ||

| By Application | Data Collection and Capture | |

| Data Cleaning and Query Management | ||

| Coding and Dictionary Management | ||

| Safety and Adverse Event Reconciliation | ||

| Submission and Regulatory Reporting | ||

| By End User | Pharmaceutical and Biotechnology Companies | |

| Contract Research Organizations | ||

| Medical Device Companies | ||

| Academic and Research Institutions | ||

| Hospitals and Healthcare Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the clinical data management market?

The clinical data management market stands at USD 3.63 billion in 2026 and is forecast to reach USD 6.75 billion by 2031 at a 13.20% CAGR.

Which segment leads by component in clinical data management?

Software led the market with 58.34% share in 2025 because sponsors continue to favor integrated SaaS platforms over fragmented legacy tools.

Which product type is growing fastest in this space?

Clinical Data Management System Platforms are projected to grow at a 15.35% CAGR through 2031 as buyers move toward broader platform consolidation.

Why is cloud deployment gaining momentum in clinical trials?

Cloud-based deployment held 55.45% share in 2026 and is growing at 13.67% CAGR because it supports faster updates, easier collaboration, and scalable study execution.

Which end users are driving the strongest future demand?

Pharmaceutical and Biotechnology Companies remain the largest buyers, while CROs are the fastest-growing end users at a 15.55% CAGR through 2031.

Which region offers the best growth outlook?

Asia-Pacific is the fastest-growing region with a projected 14.56% CAGR through 2031, supported by expanding trial pipelines and rising outsourced data management activity.

Page last updated on: