Market Overview

| Study Period | 2021 - 2031 |

|---|---|

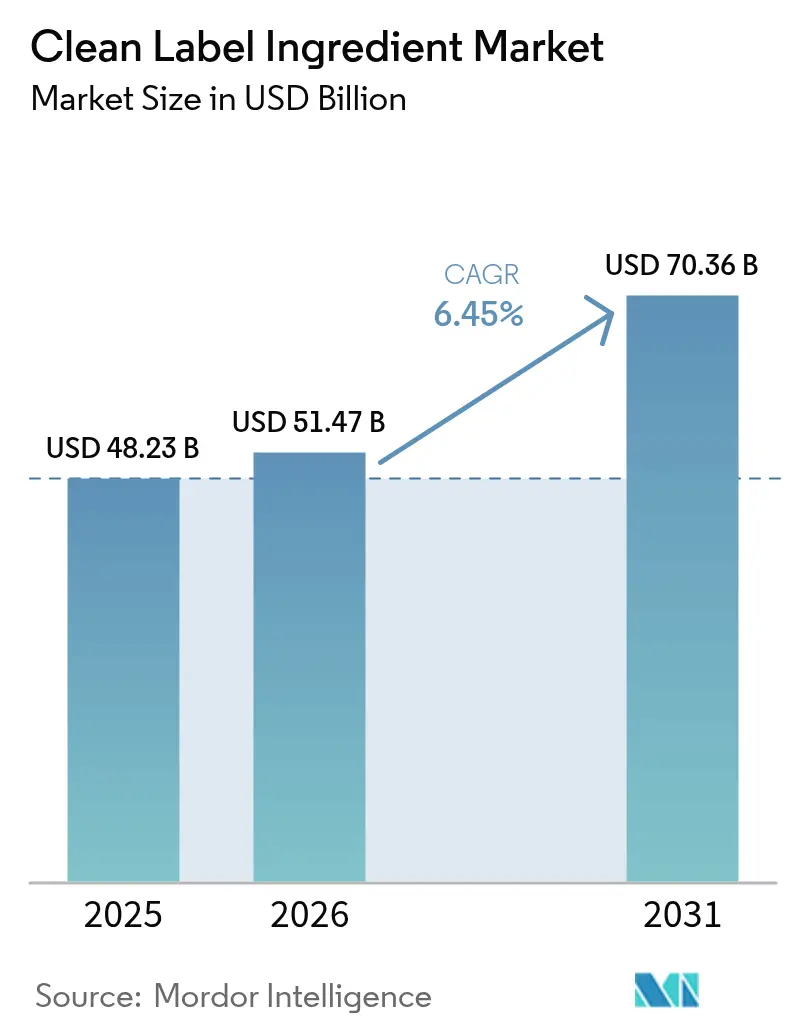

| Market Size (2026) | USD 51.47 Billion |

| Market Size (2031) | USD 70.36 Billion |

| Growth Rate (2026 - 2031) | 6.45% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Clean Label Ingredient Market Analysis by Mordor Intelligence

The clean label ingredients market size was valued at USD 48.23 billion in 2025 and estimated to grow from USD 51.47 billion in 2026 to reach USD 70.36 billion by 2031, at a CAGR of 6.45% during the forecast period (2026-2031). The global clean label ingredients market is driven by increasing consumer demand for transparent, minimally processed, and naturally sourced products in the food and beverage industry. Heightened awareness of health and wellness, along with concerns about artificial additives, preservatives, colors, and genetically modified ingredients, has led manufacturers to reformulate products with simple and recognizable components. Regulatory requirements and stricter labeling standards in developed markets are further encouraging brands to provide clearer ingredient declarations and eliminate synthetic inputs. Moreover, the rising demand for plant-based, organic, and non-allergenic formulations is fostering innovation in natural emulsifiers, stabilizers, sweeteners, and colorants. The growth of premium and functional food segments, combined with the role of social media and digital platforms in educating consumers about ingredient sourcing and processing, is further supporting market expansion globally.

Key Report Takeaways

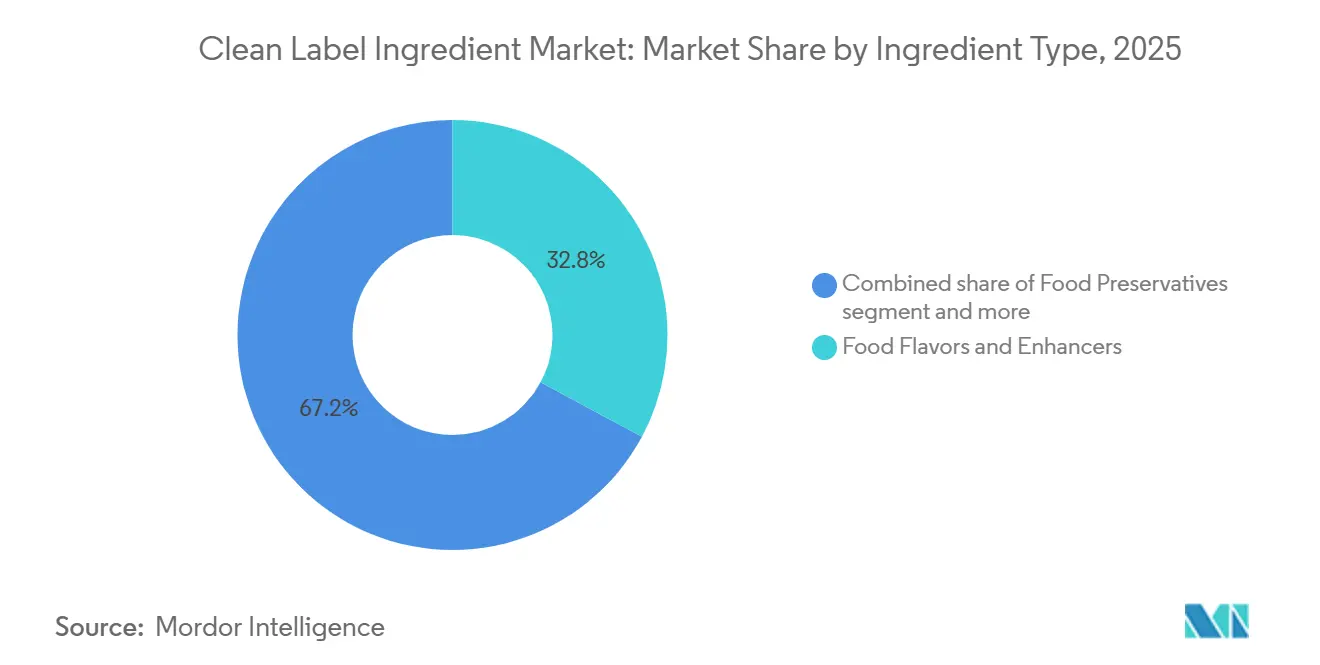

- By ingredient type, food flavors and enhancers led with 32.84% of the clean-label ingredients market share in 2025, while food colorants are forecast to expand at a 7.94% CAGR through 2031.

- By form, dry ingredients accounted for 55.71% share of the clean-label ingredients market size in 2025, whereas liquid formats are projected to grow at an 8.04% CAGR over 2026-2031.

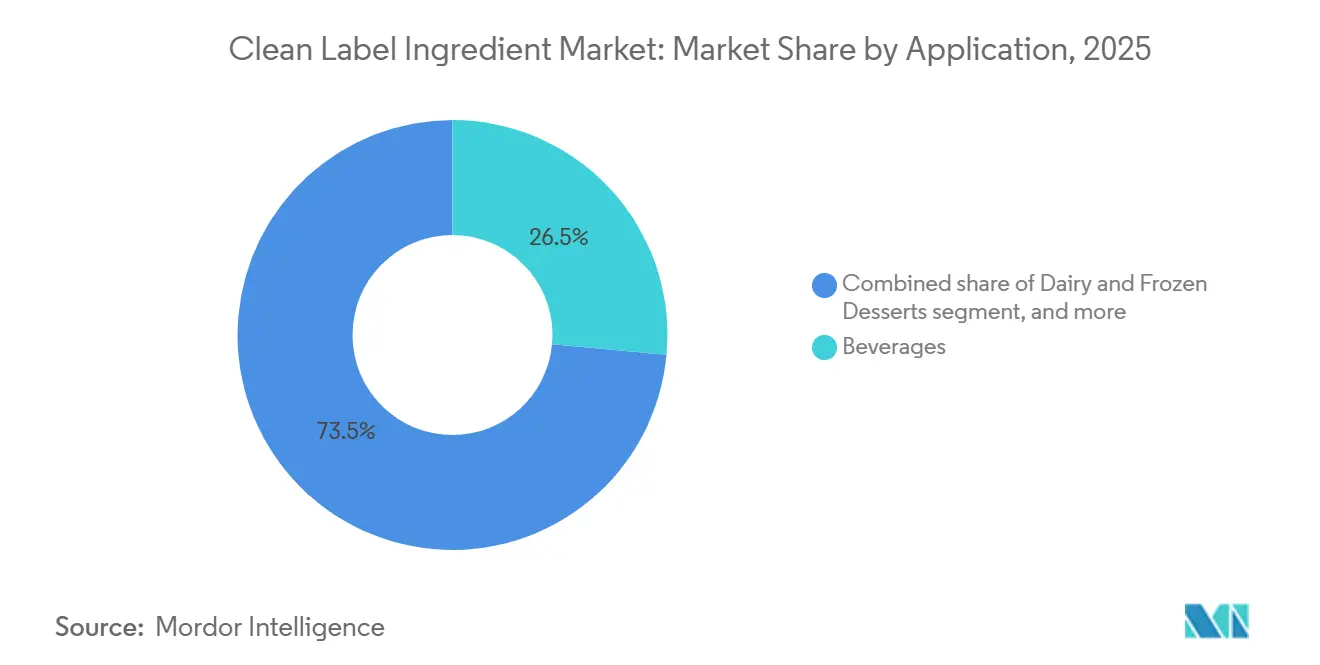

- By application, beverages held 26.47% revenue share in 2025, yet meat and meat products are advancing at a 7.53% CAGR to 2031.

- By geography, North America commanded 34.64% of the 2025 value; however, Europe is set to register the fastest 7.35% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Clean Label Ingredient Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health consciousness and concerns over artificial additives | +1.2% | Global | Medium term (2-4 years) |

| Increasing demand for plant-based, organic, and natural formulations | +1.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Growing consumer preference for "free-from" and transparent labeling | +0.9% | North America and Europe | Short term (≤ 2 years) |

| Expansion of vegan and vegetarian product portfolios | +0.8% | Global, led by Europe and North America | Medium term (2-4 years) |

| Global health emergencies reinforcing demand for healthier diets | +0.6% | Global | Short term (≤ 2 years) |

| Increased R&D investment in clean-label ingredient innovation | +1.0% | Global, concentrated in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising health consciousness and concerns over artificial additives

Consumers are scrutinizing ingredient panels with unprecedented rigor, treating artificial additives as red flags rather than benign processing aids. The FDA's Red No. 3 ban in January 2025 validated years of consumer advocacy, forcing confectionery and bakery manufacturers to reformulate thousands of SKUs within compressed timelines[1]Source: U.S. Food and Drug Administration, "FDA to Revoke Authorization for the Use of Red No. 3 in Food and Ingested Drugs," fda.gov. This regulatory action followed California's 2024 prohibition of the same dye, creating a de facto national standard as brands opted for unified formulations rather than state-specific variants. The shift extends beyond colorants; preservatives such as BHA, BHT, and sodium benzoate face growing retailer restrictions, with major United States grocery chains publishing exclusion lists that mirror consumer petitions. Ingredion's 2025 consumer study documented that 45% of shoppers prioritize ingredient transparency over price, a behavioral pivot that narrows the cost disadvantage of natural alternatives and accelerates adoption across mid-tier brands[2]Source: Ingredion, "Less mystery, more meaning: Clean labels win consumer preference," ingredion.com. This trend is compressing product lifecycles, as brands that delay clean-label transitions risk shelf-space losses to competitors who preemptively reformulate.

Increasing demand for plant-based, organic, and natural formulations

Plant-derived ingredients are transitioning from niche to mainstream as food manufacturers respond to dual pressures: consumer demand for recognizable components and sustainability mandates from retail partners. The European Union's Farm to Fork strategy, launched in 2020 and gaining enforcement momentum through 2025, set a target of 25% organic farmland by 2030, indirectly boosting demand for organic-certified food ingredients as processors align supply chains with retailer sustainability scorecards[3]Source: European Environment Agency, "Agricultural area under organic farming in Europe," eea.europa.eu. Organic food sales in Europe reached record levels in 2025, with Germany, France, and the Netherlands leading per-capita consumption, creating pull-through demand for organic starches, natural emulsifiers, and plant-based texturizers. In North America, the USDA Organic seal remains a premium differentiator, yet its influence is spreading into conventional product lines as brands adopt "organic-inspired" formulations using non-GMO, minimally processed ingredients that approximate organic positioning without full certification costs

Growing consumer preference for “free-from” and transparent labeling

Consumer preference for "free-from" and transparent labeling is a key driver of the global clean label ingredients market. Shoppers are increasingly examining product labels and avoiding artificial additives, synthetic preservatives, GMOs, allergens, and chemically derived ingredients. Modern consumers prioritize clarity regarding ingredient sourcing, processing methods, and functional roles, prompting manufacturers to simplify formulations and use familiar, easily recognizable components. The growing influence of health-conscious millennials and Gen Z consumers, coupled with increased access to nutritional information via digital platforms, has amplified the demand for authenticity and brand accountability. In response, food and beverage companies are reformulating products to eliminate controversial ingredients and emphasize claims such as "no artificial colors," "no added preservatives," and "non-GMO." This trend is driving the adoption of natural emulsifiers, sweeteners, colors, and texturizers in global markets.

Expansion of vegan and vegetarian product portfolios

Vegan and vegetarian product lines are expanding beyond traditional plant-based meat and dairy analogs into condiments, snacks, and ready meals, each requiring clean-label ingredient solutions that deliver texture, flavor, and shelf stability without animal-derived inputs. Hydrocolloids such as pectin, guar gum, and xanthan gum are replacing gelatin and casein in applications ranging from gummy confections to yogurt alternatives, yet formulators face challenges replicating the mouthfeel and heat stability of animal proteins. Yeast extracts and fermented ingredients are gaining traction as umami enhancers in vegan sauces and seasonings, providing savory depth without monosodium glutamate or hydrolyzed vegetable protein, both of which carry negative consumer perceptions despite regulatory approval. The European market is particularly dynamic, with Germany and the United Kingdom leading vegan product launches. This proliferation is driving demand for multifunctional ingredients that simplify formulations, as brands seek to minimize label length while achieving performance parity with conventional products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated cost of clean-label raw materials | -0.7% | Global, acute in price-sensitive emerging markets | Medium term (2-4 years) |

| Low consumer awareness in developing regions | -0.4% | Asia-Pacific (excluding Japan, South Korea), Middle East and Africa, parts of South America | Long term (≥ 4 years) |

| Regulatory complexity and approval challenges | -0.3% | Global, particularly cross-border manufacturers | Medium term (2-4 years) |

| Competition from lower-priced conventional ingredients | -0.5% | Global, concentrated in cost-driven segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Elevated cost of clean-label raw materials

Natural ingredient sourcing incurs structural cost premiums due to agricultural variability, lower extraction yields, and limited supplier bases compared to synthetic alternatives produced via established chemical synthesis routes. Ingredion's 2025 research quantified consumer willingness to pay 20% to 30% premiums for clean-label products, yet this tolerance varies sharply by category and income segment, creating adoption barriers in value-tier products where price elasticity remains high. Natural colorants exemplify this challenge; beetroot red and spirulina extract, both FDA-approved in 2025, cost 3 to 5 times more than synthetic Red No. 40 on a per-unit basis, and their lower tinctorial strength requires higher dosing to achieve equivalent hue intensity. Hydrocolloids face similar economics; organic-certified guar gum and pectin command premiums of 40% to 60% over conventional grades, driven by limited organic acreage and certification costs that cascade through supply chains. These cost differentials compress margins for food manufacturers, particularly in competitive categories like beverages and snacks, where retail pricing power is constrained, forcing brands to absorb costs or reformulate with lower-cost natural alternatives that may compromise sensory attributes.

Low consumer awareness in developing regions

Clean-label adoption exhibits stark geographic disparities, with awareness and willingness-to-pay concentrated in North America, Western Europe, and affluent Asia-Pacific markets, while price sensitivity and unfamiliarity with ingredient terminology limit uptake in emerging economies. In India, despite the Food Safety and Standards Authority of India (FSSAI) implementing stricter additive regulations, ingredient transparency ranks below price, brand familiarity, and convenience in purchase decisions for mass-market food products. Similar patterns emerge in Southeast Asia, Latin America, and Sub-Saharan Africa, where rising middle classes prioritize caloric density and affordability over label claims, and retail infrastructure skews toward traditional trade channels with limited space for premium-positioned clean-label SKUs. This awareness gap constrains market expansion, as ingredient suppliers and food manufacturers face longer education cycles and higher marketing costs to shift consumer preferences, delaying return on reformulation investments in these regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Flavors Lead, Colorants Accelerate

Food flavors and enhancers held 32.84% of market share in 2025, reflecting their ubiquity across applications from beverages to sauces, where they mask off-notes from functional ingredients and deliver signature taste profiles without synthetic additives. Yeast extracts and fermented ingredients are displacing monosodium glutamate and hydrolyzed vegetable protein in savory applications, providing umami depth while satisfying clean-label criteria. Additionally, food Sweeteners are navigating a complex landscape where stevia, monk fruit, and allulose compete for share against legacy options like cane sugar and high-fructose corn syrup, with regulatory approvals varying by region and consumer acceptance still building for some natural alternatives.

Food colorants are projected to grow at 7.94% CAGR through 2031, the fastest rate among ingredient types, driven by regulatory phase-outs of synthetic dyes and consumer rejection of artificial hues. The FDA's approval of beetroot red and spirulina extract as natural colorants, paired with the Red No. 3 ban, is accelerating reformulation in confectionery, dairy, and beverage categories where visual appeal is a primary purchase driver. Food Preservatives are experiencing steady demand as manufacturers replace synthetic sorbates and benzoates with rosemary extract, vinegar-based solutions, and fermentation-derived antimicrobials like nisin, though cost premiums and shorter shelf-life windows remain formulation hurdles.

By Form: Dry Dominates, Liquid Gains in Beverages

Dry ingredients accounted for 55.71% of market share in 2025, favored for their extended shelf life, lower transportation costs, and ease of storage in manufacturing facilities with limited cold-chain infrastructure. Powdered natural colorants, spray-dried flavors, and granulated sweeteners dominate bakery, confectionery, and snack applications where moisture content must be tightly controlled to prevent microbial growth and maintain crispness. Dry formats retain advantages in export-oriented markets and ambient-stable product categories, where transportation economics and shelf-life duration outweigh the processing convenience of liquids.

Liquid forms are expanding at 8.04% CAGR through 2031, the faster growth trajectory, as beverage and dairy manufacturers prioritize uniform dispersion and rapid incorporation in high-speed production lines where dry ingredients risk clumping or incomplete hydration. Liquid natural colors, such as beetroot juice concentrate and turmeric oleoresin, deliver superior color stability in acidic beverage systems compared to powdered equivalents, reducing formulation complexity and quality variability. Liquid preservatives, including vinegar-based solutions and fermented vegetable extracts, are gaining adoption in refrigerated dairy and ready-to-eat meal categories where they integrate seamlessly into aqueous matrices without requiring pre-dissolution steps. The shift toward liquid formats is also driven by clean-label positioning; consumers perceive liquid ingredients as less processed than spray-dried or encapsulated forms, even when functional performance is equivalent.

By Application: Beverages Anchor, Meat Reformulates Rapidly

Beverages captured 26.47% of application share in 2025, driven by clean-label reformulations in carbonated soft drinks, functional beverages, and plant-based milk alternatives, where consumers scrutinize ingredient lists and reject products containing artificial colors, flavors, or preservatives. The category's dominance reflects high SKU counts, frequent new product introductions, and retail shelf visibility that amplifies clean-label claims as competitive differentiators. Natural sweeteners like stevia and monk fruit are displacing aspartame and sucralose in zero-calorie beverages, though formulators continue refining blends to eliminate lingering bitter or metallic notes that depress repeat purchase rates.

Meat and meat products are advancing at 7.53% CAGR through 2031, the fastest growth among applications, as processors replace synthetic nitrites, phosphates, and flavor enhancers with fermentation-derived preservatives, plant extracts, and clean-label binders that maintain color, texture, and shelf life in fresh and processed meats. Bakery and confectionery applications are undergoing parallel transformations, with natural colors replacing synthetic dyes in icings, fillings, and coatings, and enzyme-modified starches substituting for chemically modified alternatives in texture systems. Sauces and condiments are adopting vinegar-based preservatives and natural thickeners to replace synthetic antimicrobials and modified starches, though achieving shelf-stable performance in ambient-distributed products requires higher dosing and careful pH management.

Geography Analysis

North America held 34.64% of the market share in 2025, driven by mature clean-label adoption influenced by consumer activism, retailer exclusion lists, and regulatory measures. Consumer activism has led to increased demand for transparency in product labeling, pushing manufacturers to adopt clean-label practices. Retailer exclusion lists, which outline unacceptable ingredients, have further pressured companies to reformulate products to meet these standards. Regulatory measures, including stricter guidelines on ingredient disclosures, have also played a significant role in shaping the market. The region's leading position is supported by the concentrated power of major grocery chains, which establish industry norms through published ingredient standards, and by a strong supply base of ingredient innovators capable of quickly scaling natural alternatives.

Europe is projected to grow at a CAGR of 7.35% through 2031, marking the fastest regional growth rate. This growth is driven by several factors, including the European Food Safety Authority's additive re-evaluation program, which aims to ensure the safety of food additives used within the region. Additionally, the EU's Farm to Fork sustainability strategy is promoting sustainable food production and consumption practices, further influencing market dynamics. High per-capita organic food consumption in countries such as Germany, France, and the Netherlands is also contributing significantly to this growth, as consumers increasingly prefer organic and clean-label products. The region's stringent regulatory environment is fostering clean-label transitions, with manufacturers proactively reformulating products to comply with potential future restrictions. This proactive approach helps companies avoid disruptions caused by bans or regulatory changes after products have entered the market.

Asia-Pacific exhibits bifurcated dynamics, with Japan, South Korea, and Australia mirroring Western clean-label trends, while China, India, and Southeast Asia balance rapid urbanization and rising health awareness against price sensitivity and lower familiarity with ingredient terminology. China's revised food safety standards, tightened additive limits and introduced traceability requirements that are elevating demand for natural ingredients among domestic and multinational brands targeting premium segments. South America is experiencing gradual adoption, with Brazil's organic food market expanding and Argentina leveraging its agricultural base to supply natural ingredients domestically and for export, though economic volatility and currency fluctuations constrain investment in reformulation. Middle East and Africa are emerging markets for clean-label ingredients, with halal certification intersecting with natural ingredient demand in Muslim-majority countries, and rising health awareness in the Gulf Cooperation Council nations driving premium product launches that feature simplified ingredient panels.

Regulatory Landscape

Clean label functions as a market claim rather than a single, globally harmonized legal definition, so compliance is governed by existing additive and labeling frameworks that are tightening around colorants, purity specifications, and disclosure. In the United States, FDA actions such as the January 2025 revocation of Red No. 3 use in food accelerated reformulation toward natural colors. The FDA Human Foods Program 2026 priority deliverables also highlight food dyes and GRAS transparency, reinforcing the need for well-documented safety substantiation and traceability.

In Europe, the European Food Safety Authority (EFSA) continues its additive re-evaluation program covering legacy additives, keeping regulatory scrutiny active for ingredients used across beverages, bakery, and meat applications. The European Union updated additive rules and purity expectations through amendments under Regulation (EC) No 1333/2008 and related implementing measures. The 2026 changes tighten requirements for certain additives in foods intended for vulnerable groups (for example, infants and foods for special medical purposes), which has pushed suppliers toward higher-purity, tightly specified grades and more complete technical documentation for customer audits.

Value Chain Analysis

The clean-label ingredients value chain starts with agricultural and bio-based feedstocks (fruits, vegetables, spices, grains, seaweeds) and moves through primary processing (milling, extraction, fermentation, enzymatic conversion), formulation and standardization (blends, carriers, dispersion systems), and downstream distribution to food and beverage manufacturers and co-manufacturers. Clean label is operationalized through existing food safety, additive, and labeling rules rather than a single legal category, so documentation, identity preservation (such as non-GMO and organic), and analytical verification (purity, contaminants, allergens) are embedded activities that add cost and lead time across procurement, QA, and customer technical service.

Key bottlenecks include seasonal variability and geographic concentration of natural raw materials, limited scalability for some extraction and fermentation platforms, and the added complexity of certification and traceability for global brands seeking consistent claims across regions. To manage volatility and shorten reformulation cycles, suppliers and brands are using more direct sourcing, regionalized production footprints, and collaborative application development, particularly in performance-sensitive systems such as natural color replacement in acidic beverages and clean-label binders and preservatives for meat and savory products.

Competitive Landscape

The clean-label ingredients market is fragmented, characterized by dispersed competition. No single player holds a dominant share, with regional specialists, fermentation startups, and botanical extract suppliers competing alongside multinational ingredient conglomerates. This structure creates white-space opportunities for agile entrants who can deliver cost-effective natural alternatives with superior functionality, particularly in categories like natural preservatives and plant-based texturizers, where incumbents face performance trade-offs.

Strategic patterns reveal a bifurcation: large players such as Cargill, ADM, and Ingredion are leveraging scale to invest in fermentation platforms and enzyme technologies that reduce production costs, while mid-tier specialists like Kalsec and Sensient focus on niche applications, natural spice extracts, botanical colorants, where technical expertise and customer co-development justify premium pricing.

Technology deployment is reshaping competitive positioning, with companies investing in AI-driven formulation platforms that predict ingredient interactions and optimize sensory outcomes, reducing reformulation cycles from months to weeks. Emerging disruptors include precision fermentation startups producing animal-free dairy proteins and heme analogs, ingredients that satisfy clean-label criteria while addressing sustainability concerns, though commercialization timelines and regulatory approvals remain multi-year hurdles. The competitive landscape is further complicated by vertical integration moves, with food manufacturers acquiring ingredient suppliers to secure supply and capture margin.

Clean Label Ingredient Industry Leaders

-

Archer-Daniels-Midland Company

-

Cargill, Incorporated

-

Ingredion Incorporated

-

DSM-Firmenich

-

International Flavor and Fragrances Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major opportunity is in scaling natural colors, flavors, and functional systems that can deliver consistent performance under reformulation pressure from regulators, retailers, and consumer scrutiny. Capacity investments and partnerships in 2026 show where suppliers are placing bets: Sensient announced a USD 250 million investment to expand natural color production, including added space at its St. Louis site. ADM also invested USD 26 million at its Erlanger, Kentucky flavor facility to strengthen capabilities for naturally derived flavor and color solutions.

Fermentation and protein-enabled clean-label solutions are also creating whitespace beyond traditional additive substitution, supporting plant-based and allergen-positioned formulations while simplifying ingredient statements. Examples include FERM FOOD acquiring a manufacturing site in Skovlund, Denmark with stated scale-up to 20,000 tonnes per year of fermented plant-based ingredients, and Cargill partnering with Voyage Foods to commercialize NextCoa cocoa-free confectionery alternatives in North America. These steps support product developers looking for clean-label texture, flavor modulation, and stability with fewer declarable additives, while also reducing exposure to constrained or controversial ingredients in sensitive categories.

Recent Industry Developments

- July 2026: Archer-Daniels-Midland Company (ADM) partnered with The EVERY Company to enable US-based commercial-scale production of OvoPro egg white protein at ADM's Clinton, Iowa facility using precision fermentation. The partnership expands scalable access to animal-free functional proteins for applications that need foaming and binding performance, while aligning with cleaner ingredient declarations. It also signals deeper collaboration between large ingredient manufacturers and food-tech developers to industrialize new clean-label protein platforms.

- May 2026: Cargill partnered with Voyage Foods to bring NextCoa, a cocoa-free confectionery alternative, to North America. The initiative targets product developers looking for ingredient options positioned around simplified labeling and allergen considerations in confectionery. It broadens the competitive set of clean-label flavor and color-building blocks used to reformulate indulgent categories without traditional commodity inputs.

- January 2026: ADM announced a USD 26 million expansion of its Erlanger, Kentucky innovation campus, adding capacity, automation, and digitalization to support naturally derived flavor and color solutions used in reformulation programs. The investment strengthens throughput and repeatability for clean-label ingredient systems that require tight process control and faster development cycles. It reinforces the role of large-scale capability upgrades as suppliers respond to accelerated removal of artificial additives across multiple food and beverage applications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the clean label ingredients market covers food and beverage ingredients positioned as simple, familiar, and minimally processed, and that help manufacturers replace or reduce artificial-sounding additives in finished products.

Scope exclusions: We exclude finished packaged foods and beverages, and we do not count private label rebranding unless the underlying ingredient sold to manufacturers is within scope.

Segmentation Overview

-

By Ingredient Type

- Food Preservatives

- Food Sweeteners

- Food Colorants

- Food Hydrocolloids and Texturizers

- Food Flavors and Enhancers

- Other Ingredients Types

-

By Form

- Dry

- Liquid

-

By Application

- Bakery and Confectionery

- Dairy and Frozen Desserts

- Beverages

- Meat and Meat Products

- Sauces and Condiments

- Other Applications

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Thailand

- Singapore

- Rest of Asia-Pacific

-

Middle East and Africa

- Saudi Arabia

- South Africa

- United Arab Emirates

- Nigeria

- Morocco

- Egypt

- Turkey

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, align ingredient definitions across countries, and build the first cut of demand signals by application. We referenced public materials such as USDA and FDA labeling guidance, EFSA and European Commission references for food additive and ingredient guidance, and Codex Alimentarius texts for terminology alignment.

To shape the demand pool, we also reviewed sources such as UN Comtrade trade statistics for key ingredient categories, FAOSTAT for agricultural raw material supply indicators, and patent databases to spot formulation activity in natural colors, flavors, and texturants. On top of that, we used company filings, investor presentations, and reputable press to confirm capacity moves and portfolio shifts. These checks were supported by paid subscriptions focused on company financials and intelligence plus news and financials for event validation. These sources are illustrative, and additional public references were used during data collection and follow-up checks.

Primary Interviews and Surveys

Primary work focused on validating what is truly being sold as a clean label ingredient versus what is presented mainly as a labeling claim, since that distinction can move the market total quickly. We spoke with ingredient suppliers, food and beverage manufacturers, distributors, and industry experts across major regions to confirm application mix, typical inclusion rates, pricing direction, and the pace of reformulation in products that are sold as everyday consumer items.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 18% | APAC: 49% |

| Mid tier: 40% | Functional/Unit leaders: 33% | EMEA: 30% |

| Smaller Players: 22% | Managers: 49% | Americas: 21% |

Market-Sizing & Forecasting

Market sizing was built using a top-down and bottom-up cross-check approach, where application-level demand pools were reconstructed first and then validated with supplier-side signals. On the top-down side, we started from packaged food and beverage production volumes and reformulation intensity, then applied clean label penetration and ingredient inclusion rates to estimate value by ingredient functionality.

To keep the model grounded, key inputs included the share of clean label launches by category, average usage rates for natural colors and flavors, substitution patterns for sweeteners and preservatives, form mix between dry and liquid ingredients, and regional pricing direction captured as realistic ASP bands. Selective bottom-up checks were then used to corroborate totals, such as sampled supplier revenue checks, channel discussions on higher-volume ingredient groups, and volume times ASP where usable public signals existed. Where company disclosures were not detailed enough, gaps were handled by using peer benchmarks within the same ingredient type and adjusting only after interview confirmation.

For forecasting, scenario analysis was used because adoption timing depends on reformulation execution, regulatory interpretation, and cost-in-use tradeoffs that shift by region. Assumptions on penetration change, price progression, and application growth were stress-tested with expert feedback, and the final path was chosen only when drivers stayed consistent across multiple interviews.

Data Validation & Update Cycle

Outputs were checked through multiple passes, starting with internal consistency tests across ingredient types, forms, and applications, then followed by regional roll-ups to confirm totals matched the intended scope. Where the model showed sharp jumps, we reviewed the input drivers, re-checked conversion factors, and revisited the relevant interview notes before approving the numbers.

We also compared the totals against independent signals such as trade movement direction for key ingredient categories, reported capacity expansions, and category-level reformulation momentum. The report is refreshed annually, and interim updates are added when material events change supply, demand, or pricing assumptions. Before publication, a final analyst review is completed so clients receive the most current view available.

Mordor Intelligence's Clean Label Ingredients Market Size Compared With Other Published Estimates

It is normal to see different market values for clean label ingredients because the term is used loosely and the product boundary is not identical across studies. Differences also come from what gets counted as an ingredient sale versus a finished food product claim, and from how pricing and currency timing are applied.

By tracking application-level inclusion rates and regional ASP bands, Mordor Intelligence keeps the total tied to ingredient revenues used in food and beverage formulations, which reduces inflation from counting broader natural food categories and non-comparable end uses.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 51.47 B (2026) | |

| Global Consultancy A | USD 47.91 B (2026) | Uses a different base-year setup and narrower ingredient coverage in practice, and the pricing assumptions appear to be applied more conservatively across applications, which pulls down the 2026 value. |

| Industry Research Group B | USD 124.75 B (2023) | Takes a much wider definition that can pull in broad natural and organic ingredient baskets and adjacent end uses, and it also uses an earlier base year, so the value is not directly comparable to a clean label ingredient revenue scope. |

The spread in published numbers mainly comes from definition boundaries and year alignment, not from arithmetic errors. When the scope is limited to ingredient sales linked to specific food and beverage applications, and inputs like penetration, inclusion rates, and price bands are applied consistently, the resulting market size becomes easier to replicate and to track over time.

Key Questions Answered in the Report

What is driving the clean label ingredients market growth?

Demand for healthier diets, stricter additive regulations and brand reformulation initiatives underpin the sector’s 6.45% CAGR forecast.

Which ingredient segment is growing the fastest?

Food colorants lead growth with a projected 7.94% CAGR, propelled by regulatory moves to eliminate synthetic dyes.

Which region currently dominates global revenue?

North America holds the largest regional share at 34.64% owing to a well-informed consumer base and active FDA oversight.

Why do beverages hold the largest application share?

Quick innovation cycles allow beverage makers to showcase natural flavors, colors and functional claims that resonate with health-minded shoppers.

Page last updated on: