Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

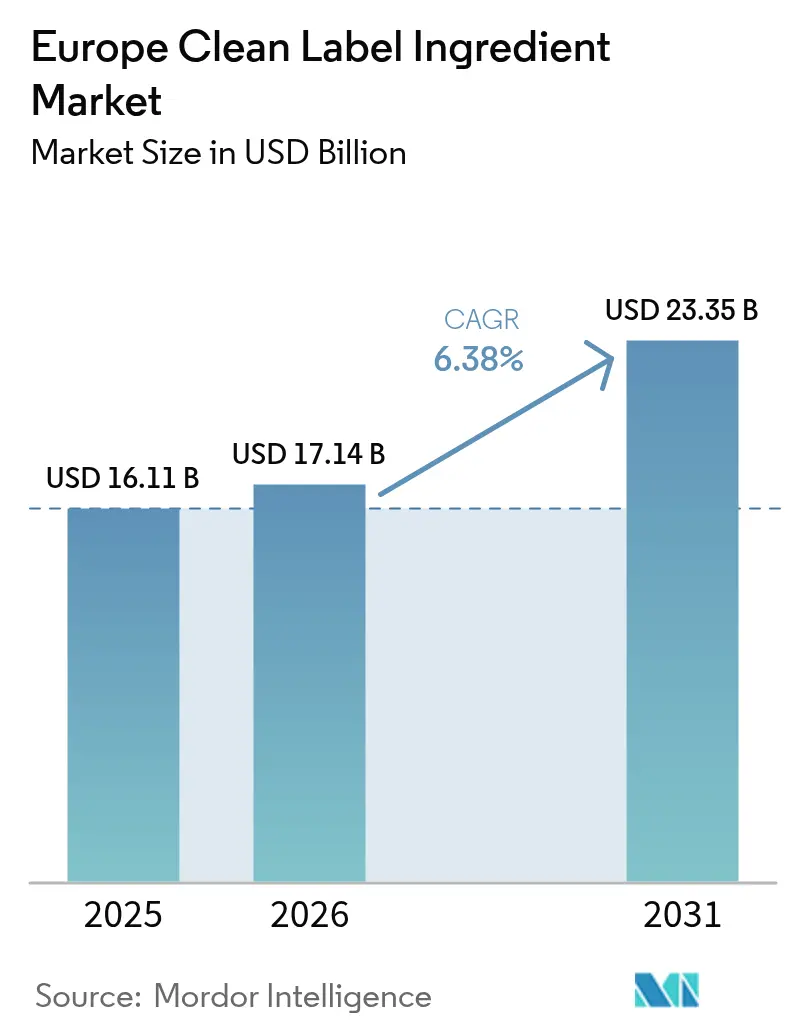

| Base Year Market Size (2025) | USD 16.11 Billion |

| Market Size (2026) | USD 17.14 Billion |

| Market Size (2031) | USD 23.35 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

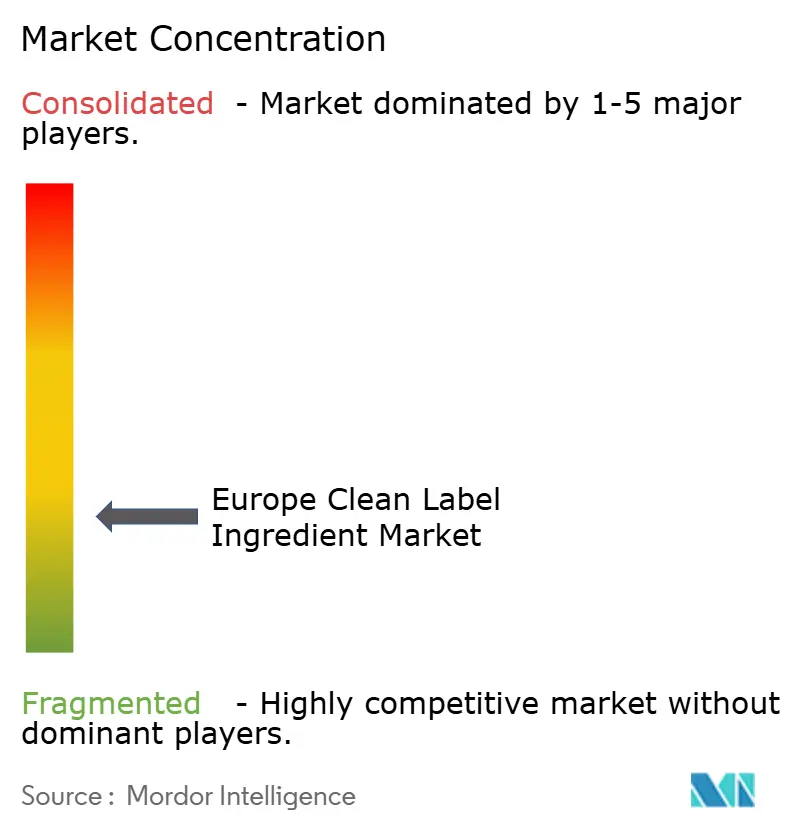

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Clean Label Ingredient Market Analysis by Mordor Intelligence

The Europe clean label ingredient market size was valued at USD 16.11 billion in 2025 and estimated to grow from USD 17.14 billion in 2026 to reach USD 23.35 billion by 2031, at a CAGR of 6.38% during the forecast period (2026-2031). This upward trajectory highlights the increasing consumer preference for natural and transparent labeling, driven by heightened awareness of health and wellness trends. Consumers are actively seeking products with clean labels that exclude artificial additives, preservatives, and synthetic ingredients, aligning with their desire for healthier and more sustainable food options. Additionally, the European Union's stringent regulatory framework plays a pivotal role in shaping the market. Regulations such as (EU) 2018/848, which governs organic production and labeling, and the European Food Safety Authority's (EFSA) ongoing re-evaluations of food additives, are pushing manufacturers to reformulate products with clean label ingredients. These regulatory measures aim to ensure food safety, enhance transparency, and meet the growing demand for natural alternatives. As a result, companies operating in this market are increasingly investing in research and development to innovate and expand their portfolio of clean label ingredients, further fueling market growth.

Key Report Takeaways

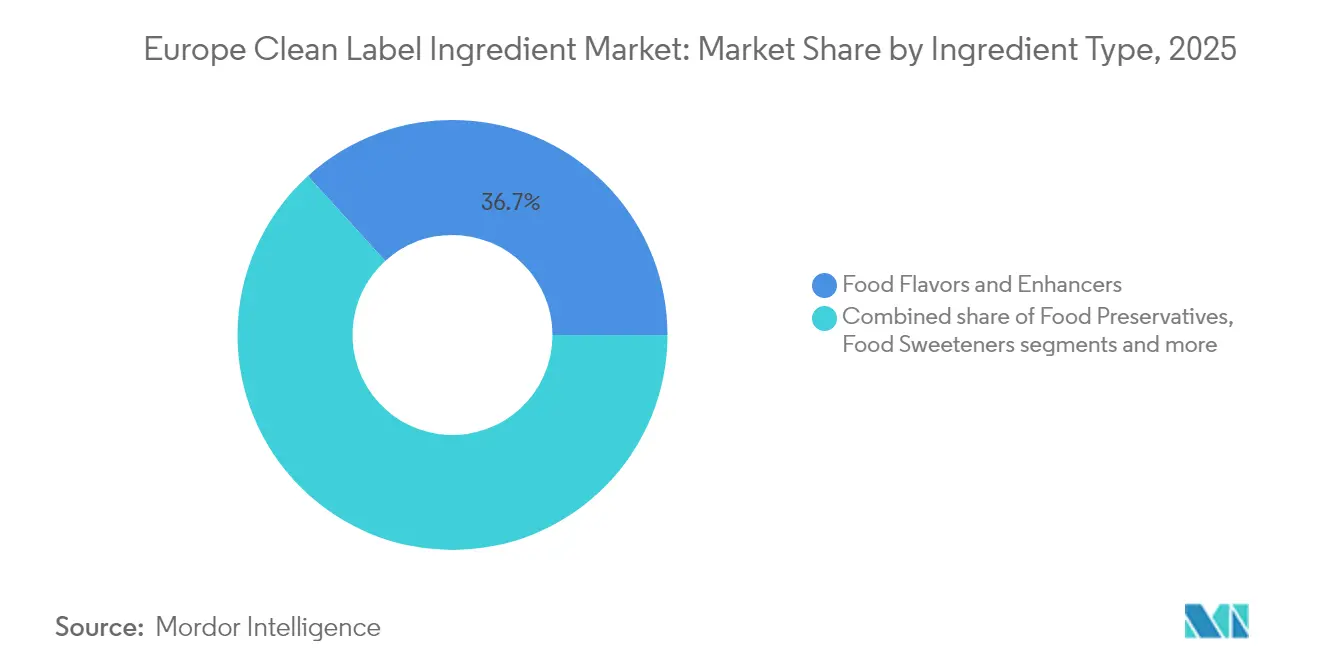

- By ingredient type, food flavors and enhancers led with 36.74% of Europe clean label ingredient market share in 2025; food colorants are projected to grow fastest at 6.95% CAGR to 2031.

- By form, dry ingredients commanded 59.63% share of the Europe clean label ingredient market size in 2025, while liquid forms are poised for an 7.74% CAGR through 2031.

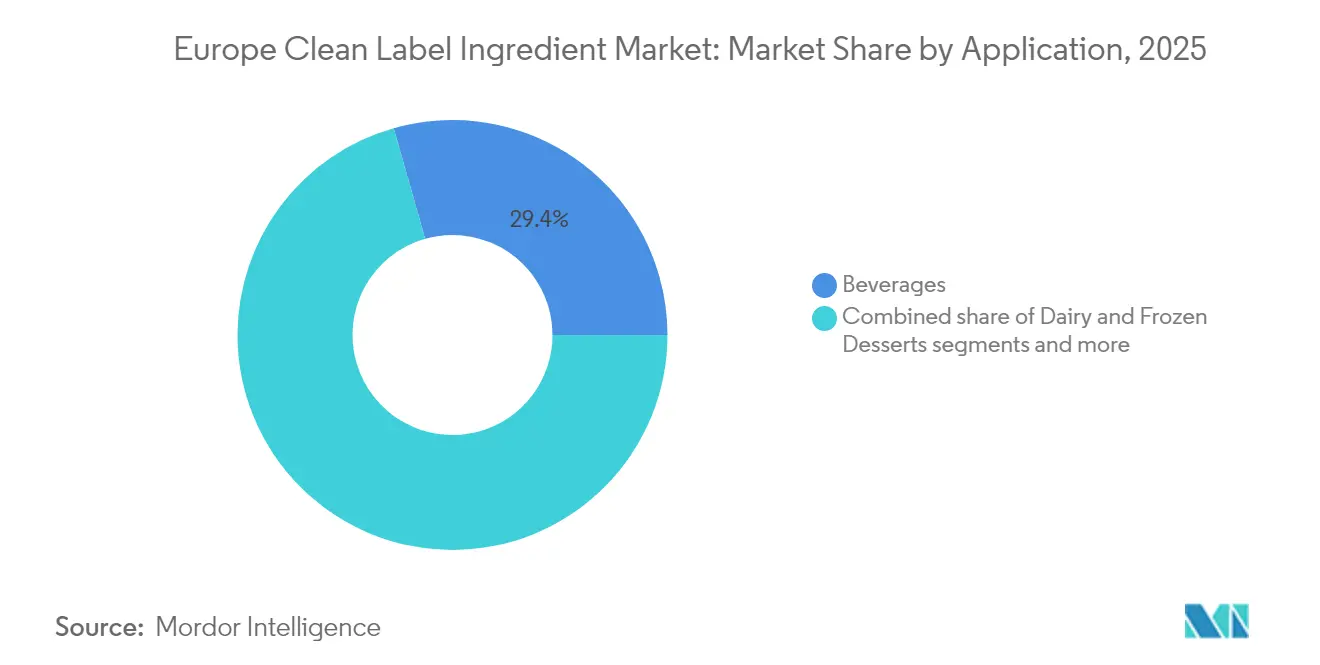

- By application, beverages accounted for 29.41% of the market size in 2025; meat and meat products are expanding at 7.58% CAGR between 2026-2031.

- By geography, Germany captured 22.05% of the market share in 2025 and is advancing at an 7.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Clean Label Ingredient Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for natural and plant-based ingredients | +1.8% | Pan-European with stronger impact in Germany, France, UK | Medium term (2-4 years) |

| Expanding impact of food allergies and intolerances on consumer behavior | +1.2% | EU-wide, particularly Nordic countries | Short term (≤ 2 years) |

| Rising consumer preference for sustainable and ethical products | +1.5% | Western Europe, emerging in Eastern Europe | Long term (≥ 4 years) |

| Increasing penetration of functional and fortified food | +0.9% | Germany, Netherlands, France | Medium term (2-4 years) |

| Soaring label-conscious population across developed regions | +1.1% | EU-wide, concentrated in urban areas | Short term (≤ 2 years) |

| Premiumization and transparency in packaged food | +0.7% | Germany, France, UK, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing demand for natural and plant-based ingredients

Consumers in the region are increasingly prioritizing transparency in food products, driving the demand for natural and plant-based ingredients. A report from the European Food Information Council highlights that a majority of European consumers favor clean-label products, underscoring their preference for recognizable, natural components. Moreover, the European Commission's Farm to Fork Strategy, which underscores the importance of sustainable food systems, bolsters the push for plant-based ingredients in food production. Data from ITC Trade Map reveals that in 2024, Central and Eastern Europe imported natural coloring matter worth USD 86.6 million, a significant rise from USD 61.8 million in 2020, further reflecting the growing demand for natural ingredients [1]Source: International Trade Centre, "Import value of Natural Coloring Matter (HS code 32030010)", www.trademap.org. The European Vegetarian Union (EVU) notes a consistent uptick in the consumption of plant-based alternatives, including oat milk and plant-based meats, throughout Europe. These consumer trends, buoyed by government initiatives championing sustainable agriculture and plant-based diets, are poised to propel the market forward.

Expanding impact of food allergies and intolerances on consumer behavior

The increasing prevalence of food allergies and intolerances is significantly influencing consumer behavior, driving demand for clean-label ingredients in the European market. The European Food Safety Authority (EFSA) has highlighted that approximately 2% of adults and 6% of children in Europe are affected by food allergies, emphasizing the need for transparency in food labeling [2]Source: European Food Safety Authority, "Scientific Opinion on the evaluation of allergenic foods and food ingredients for labelling purposes", www.efsa.europa.eu. Governments and regulatory bodies are actively addressing this issue. For instance, the European Union's Food Information to Consumers (FIC) Regulation mandates clear labeling of allergens on pre-packaged food products. This regulation has encouraged manufacturers to adopt clean label practices, ensuring that consumers can make informed choices. Associations such as the European Federation of Allergy and Airways Diseases Patients' Associations (EFA) are also advocating for stricter labeling norms and increased awareness about food allergies. These efforts have led to a surge in demand for allergen-free and minimally processed ingredients, which align with the clean label trend. For example, companies are increasingly using natural substitutes like rice flour and chickpea flour instead of wheat flour to cater to gluten-intolerant consumers. Similarly, plant-based milk alternatives, such as almond and oat milk, are gaining popularity among individuals with lactose intolerance. These shifts in consumer preferences are driving innovation and growth in the European clean label ingredient market.

Rising consumer preference for sustainable and ethical products

Consumers in the region are increasingly gravitating towards sustainable and ethical products, driven by heightened awareness of health, environmental concerns, and ethical sourcing. This shift has propelled the growth of the clean label ingredients market in Europe. Research from CBI, the Ministry of Foreign Affairs, highlights this trend, projecting that clean-label products will rise from constituting 52% of portfolios in 2021 to over 70% in 2025 and 2026 [3]Source: CBI Ministry of Foreign Affairs, "Which trends offer opportunities," www.cbi.eu. This growth is fueled by consumers becoming more discerning about product ingredients, leading to a surge in demand for clean-label ingredients that are natural, minimally processed, and devoid of artificial additives. In response, manufacturers are prioritizing transparency in both ingredient sourcing and production processes. Concurrently, European regulatory bodies are tightening labeling requirements, further bolstering the clean label movement. As companies increasingly align their offerings with consumer preferences for sustainability and ethics, this trend is poised to significantly influence the market in the coming years.

Increasing penetration of functional and fortified food

The increasing penetration of functional and fortified foods is a key driver of the European clean-label ingredients market. Consumers are increasingly seeking healthier food options, which has led to a growing demand for products enriched with vitamins, minerals, and other functional ingredients. According to the European Food Safety Authority (EFSA), the regulatory framework in Europe supports the development and marketing of fortified foods, provided they meet safety and labeling standards. The Clean Label Alliance has further highlighted that the shift toward functional and fortified foods aligns with the growing consumer demand for natural and minimally processed ingredients. This trend is expected to continue driving the adoption of clean label ingredients across the region, as manufacturers increasingly focus on reformulating their products to cater to these evolving preferences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal fluctuations in ingredient supply | -0.9% | EU-wide, particularly Germany, France, Italy | Medium term (2-4 years) |

| Regulatory challenges in natural product certification | -0.8% | EU-wide, particularly affecting smaller producers | Short term (≤ 2 years) |

| Shorter shelf life of clean label products | -1.1% | Acute in Southern Europe | Medium term (2-4 years) |

| Complex supply chain logistics | -0.9% | EU-wide, severe in Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Seasonal fluctuations in ingredient supply

Seasonal fluctuations in ingredient supply act as a significant restraint in the European clean-label ingredients market. These fluctuations often lead to inconsistencies in the availability of raw materials, directly impacting production schedules and supply chain efficiency. For instance, certain natural ingredients, such as fruits, vegetables, and grains, are subject to seasonal harvest cycles, which can result in limited availability during off-seasons. This variability not only increases procurement costs but also creates challenges in maintaining consistent product quality and meeting consumer demand. Furthermore, adverse weather conditions, such as droughts or floods, can exacerbate these supply issues, further disrupting the market. As a result, manufacturers in the clean label ingredients market must adopt strategic sourcing and inventory management practices to mitigate the impact of these seasonal variations.

Regulatory challenges in natural product certification

Regulatory challenges associated with natural product certification act as a significant restraint on the market. In Europe, the certification process for natural products is often complicated by stringent and varying regulatory requirements across countries. These regulations are intended to ensure product authenticity, safety, and compliance with clean label standards but lack harmonization across the region. This inconsistency forces manufacturers to navigate diverse regulatory frameworks, increasing both the time and costs involved in obtaining certifications. According to the European Commission, food products in the EU must meet specific labeling and certification requirements, further complicating the process for manufacturers. These requirements often demand detailed documentation, rigorous testing, and adherence to strict guidelines, which can be resource-intensive for companies. Additionally, the need to adapt to frequent regulatory updates adds another layer of complexity, requiring continuous investment in compliance efforts. Together, these factors hinder the growth of the clean label ingredients market in Europe by creating barriers for new entrants and complicating operations for existing players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Flavors Dominate, Colors Accelerate

Food flavors and enhancers claimed a 36.74% share of the market in 2025, underscoring their pivotal role in masking off-notes during reformulation, all without turning to synthetic compounds. This segment's growth is bolstered by advancements in fermentation-derived esters and botanical extracts, both of which can endure thermal processing. These innovations cater to the increasing demand for natural and sustainable solutions in food production.

Meanwhile, food colorants, though a smaller player in the market, are racing ahead with a 6.95% CAGR. This surge is fueled by regulatory bans on titanium dioxide and a consumer shift away from azo dyes, reflecting a broader trend toward cleaner and safer food products. Notably, 'coloring foods', legally recognized as ingredients rather than mere additives, empower manufacturers to preserve vibrant hues while upholding a cleaner ingredient list. This distinction allows companies to align with consumer expectations for transparency and natural ingredients, further driving the adoption of clean-label solutions across the region.

By Form: Liquid Innovations Challenge Dry Dominance

Dry formats commands a substantial 59.63% share in 2025. This dominance is attributed to their stable handling, ease of storage, and seamless compatibility with production lines. Products such as dehydrated herb blends, powdered antioxidants, and freeze-dried fruit powders integrate effortlessly into existing mixers, reducing the need for additional capital expenditure. These attributes make dry formats a preferred choice for manufacturers aiming to optimize operational efficiency. Furthermore, dry formats are particularly advantageous for long-term storage and transportation, as they are less prone to spoilage and require minimal preservation measures, making them cost-effective and sustainable.

On the other hand, liquid extracts are emerging as a high-growth segment, projected to register a robust CAGR of 7.74% during the forecast period. This growth is driven by technological advancements, including micro-encapsulation, osmotic concentration, and aseptic packaging, which have effectively resolved previous stability issues. These innovations have enhanced the shelf life and functionality of liquid extracts, making them increasingly attractive for various applications within the clean label ingredients market. Additionally, liquid extracts are gaining traction due to their ease of incorporation into beverages, sauces, and other liquid-based formulations, offering manufacturers greater versatility in product development.

By Application: Beverages Lead, Meat Products Surge

In 2025, beverages accounted for 29.41% of Europe's clean label ingredients market, with notable advancements in juices, teas, and flavored waters prominently showcasing ingredient lists on their front packaging. The growing consumer demand for transparency and healthier options has driven manufacturers to innovate and reformulate their products using clean label ingredients. This trend is particularly evident in the beverages segment, where natural flavors, sweeteners, and colorants are replacing artificial additives to meet consumer expectations.

Concurrently, the meat and meat products segment is experiencing a 7.58% CAGR, driven by processors' pursuit of natural nitrite alternatives and antioxidant systems that ensure shelf life while prioritizing safety. The shift toward clean label solutions in this segment is fueled by increasing awareness of the potential health risks associated with synthetic preservatives. Manufacturers are focusing on incorporating plant-based extracts and other natural solutions to maintain product quality and safety while aligning with clean label standards. This trend reflects the broader movement across the market toward transparency, sustainability, and health-conscious consumption.

Geography Analysis

In 2025, Germany leads the European clean label ingredients market with a 22.05% share, establishing itself as the dominant player in the region. The country also records the highest growth rate at 7.98% CAGR through 2031, reflecting its strong position in both market size and expansion speed. Germany's robust food and beverage industry, combined with increasing consumer demand for clean label products, drives this growth trajectory. The country's focus on innovation and adherence to stringent regulatory standards further strengthens its market leadership.

The United Kingdom and France also hold significant shares in the European clean label ingredients market. The UK benefits from a growing preference for natural and minimally processed ingredients, supported by strict regulatory frameworks that encourage transparency in food labeling. Additionally, the rising health consciousness among consumers in the UK has fueled the demand for clean label products. France, known for its rich culinary heritage, is witnessing a surge in the adoption of clean label ingredients as consumers increasingly prioritize transparency, sustainability, and health-conscious choices in their food products.

Italy, another key country in the region, is experiencing steady growth due to its strong focus on organic and natural food production. The country's emphasis on traditional, high-quality food products aligns well with the clean label trend, making it a significant contributor to the market. Together, Germany, the UK, France, and Italy play a pivotal role in shaping the European clean label ingredients market, driving its growth and development through innovation, consumer awareness, and adherence to evolving regulatory standards.

Competitive Landscape

The European clean label ingredients market demonstrates significant fragmentation. This competitive landscape provides opportunities for both established multinational corporations and specialized ingredient suppliers to expand their market presence. Companies are actively leveraging innovation and strategic positioning to differentiate themselves in this dynamic environment. The market's fragmentation is driven by the diverse range of clean label ingredients, which include natural preservatives, plant-based proteins, and other functional ingredients. This diversity allows smaller players with specialized expertise to compete effectively against larger corporations, creating a level playing field in certain segments.

The increasing consumer demand for transparency, sustainability, and clean-label certifications has further intensified competition in the market. Companies are focusing on developing innovative solutions that align with these consumer preferences, such as clean-label formulations with minimal processing and recognizable ingredients. Additionally, the rise of plant-based and organic food trends has spurred the development of new product offerings, encouraging players to invest in research and development. This has led to a surge in partnerships, acquisitions, and collaborations as companies aim to strengthen their portfolios and enhance their market positioning.

Furthermore, the regulatory environment in Europe plays a crucial role in shaping the competitive dynamics of the clean label ingredients market. Stricter regulations regarding food labeling and ingredient transparency have compelled companies to adopt cleaner formulations and ensure compliance. This has created opportunities for ingredient suppliers to offer innovative solutions that meet regulatory standards while addressing consumer expectations. As a result, the market is witnessing a shift toward sustainable sourcing, clean-label certifications, and the development of functional ingredients that cater to health-conscious consumers. These factors collectively contribute to the evolving competitive landscape of the Europe Clean Label Ingredients Market.

Europe Clean Label Ingredient Industry Leaders

-

Archer Daniels Midland Company

-

Kerry Group PLC

-

Cargill, Incorporated

-

Tate & Lyle PLC

-

International Flavors & Fragrances

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Galactic has launched Galimax Flavor O-50, a natural solution designed to infuse genuine oregano flavor into both meat and plant-based proteins, all while ensuring their freshness is maintained. The introduction of Galimax Flavor O-50 is a response to two significant macro-market trends, highlighting a growing demand for innovations rooted in natural fermentation.

- February 2025: Ulrick & Short, renowned for its expertise in clean label ingredients, has forged a partnership with global distributor Nordmann. This alliance aims to bolster the distribution of Ulrick & Short's clean label ingredients in Austria, France, Germany, and Switzerland.

- July 2024: Ingredion has unveiled two new clean-label citrus fiber ingredients, FIBERTEX® CF 500 and FIBERTEX® CF 100, in the EMEA region. These minimally processed ingredients offer properties like viscosity, gelling, emulsion, and texture stability. Sourced from upcycled citrus peels, they bolster on-pack claims such as “derived from natural sources”, “fruit-based”, and “source of dietary fiber”.

- September 2023: Symrise introduced chickpea and aquafaba ingredients for plant-based products, catering to growing vegan demand with focus on clear labeling and allergen-free attributes. These ingredients support clean label positioning in plant-based applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we view the Europe clean label ingredient market as the cumulative value of food-grade preservatives, sweeteners, colorants, hydrocolloids, and flavor enhancers that comply with EU "recognizable-ingredient" guidelines and are supplied to commercial food and beverage manufacturers. Each ingredient is tracked at the supplier invoice level before first industrial use, which keeps our lens on true B2B demand.

Scope exclusion: Inputs sold exclusively to personal care, nutraceutical, or household-cleaning applications are outside this study.

Segmentation Overview

-

By Ingredient Type

- Food Preservatives

- Food Sweeteners

- Food Colorants

- Food Hydrocolloids

- Food Flavors and Enhancers

- Other Ingredients Types

-

By Form

- Dry

- Liquid

-

By Application

- Bakery and Confectionery

- Dairy and Frozen Desserts

- Beverages

- Meat and Meat Products

- Sauces, and Condiments

- Other Applications

-

By Geography

- United Kingdom

- Germany

- Spain

- France

- Italy

- Netherlands

- Sweden

- Poland

- Belgium

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

We interviewed R&D chefs at beverage brands, sourcing leads at three multinational ingredient suppliers, and category managers from German, French, Polish, and Spanish bakery firms. Their inputs clarified typical dosage rates, emerging clean sweetener premiums, and likely adoption curves, which were crucial for stress-testing desk assumptions.

Desk Research

Our analysts started with publicly available regulators and trade bodies such as Eurostat production indices, EFSA re-evaluation lists for E-numbers, the European Food & Drink Federation's annual output survey, UN COMTRADE import codes for HS 1302/2106, and patent trends from Questel. Company filings, investor decks, and reputable food technology journals supplied additional insight into formulation shifts. D&B Hoovers helped us align segment revenues of listed ingredient vendors to European geographies.

Legislative texts (EU 2018/848 organic regulation) and commodity dashboards from FAO, plus retail launch counts from open Mintel summaries, rounded the desk work, anchoring baseline consumption and price corridors. These sources are illustrative, not exhaustive, and many others were reviewed for validation.

Market-Sizing & Forecasting

The top-down model begins with Eurostat output of processed food categories, multiplies each by average inclusion rates derived from expert calls, and then adjusts using import-export balances to capture cross-border ingredient flows. Select bottom-up checks, supplier Europe revenue roll-ups and sampled ASP × volume screens, calibrate and fine-tune totals. Key drivers in the equation include: reformulation count of new EU product launches, average wholesale xanthan gum price, country-level organic retail sales, Germany's clean label logo penetration, and sugar-tax expansion across member states. Multivariate regression with scenario analysis projects these variables to 2030, letting us gauge upside from stricter additive bans or downside from raw-material shocks. Data gaps in minor countries are filled by per-capita consumption proxies benchmarked to the nearest production peer before final triangulation.

Data Validation & Update Cycle

Outputs pass comparative checks against independent indices, anomaly flags trigger analyst reviews, and a senior panel signs off. We refresh every twelve months, with interim updates whenever material regulatory or price events occur; a last-mile audit is run just before report release so clients receive the freshest view.

Why Mordor's Europe Clean Label Ingredient Baseline Commands Reliability

Published estimates often differ, and our clients ask why. Variances usually stem from what gets counted, how supplier versus retail values are blended, and the cadence at which figures are refreshed.

Key gap drivers include: some studies exclude hydrocolloids or preservatives, others roll retail sales of finished "clean label" foods into ingredient revenue, and several rely on older base years converted with simple inflation. Mordor's model stays ingredient-only, uses 2024 supplier invoices as its anchor, and is updated annually, yielding a tighter, decision-ready baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.11 Bn (2025) | Mordor Intelligence | |

| USD 13.50 Bn (2024) | Global Consultancy A | Narrower ingredient list; heavy reliance on shelf-scan proxies |

| USD 46.92 Bn (2022) | Trade Journal B | Combines finished-food sales with ingredient revenues; older base year not fully rebased |

These comparisons show that when scope, base year, and revenue tier are harmonized, Mordor's disciplined mix of recent supplier data and forward-looking variables offers the most balanced and transparent baseline for strategic planning.

Key Questions Answered in the Report

What is the current size of the Europe clean label ingredients market?

The market stands at USD 17.14 billion in 2026 and is forecast to reach USD 23.35 billion by 2031.

Which ingredient segment holds the largest share?

Food flavors and enhancers lead with 36.74% market share in 2025, reflecting their critical role in maintaining taste during reformulation.

Which application area is growing the fastest?

Meat and meat products are expanding at a 7.58% CAGR as processors seek natural preservation systems that meet strict safety requirements.

Why is Germany pivotal to market growth?

Germany contributes 22.05% of regional revenue and posts an 7.98% CAGR owing to its large processing sector and consumer insistence on non-GMO, locally sourced inputs.

Page last updated on: