Intraoral Cameras Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

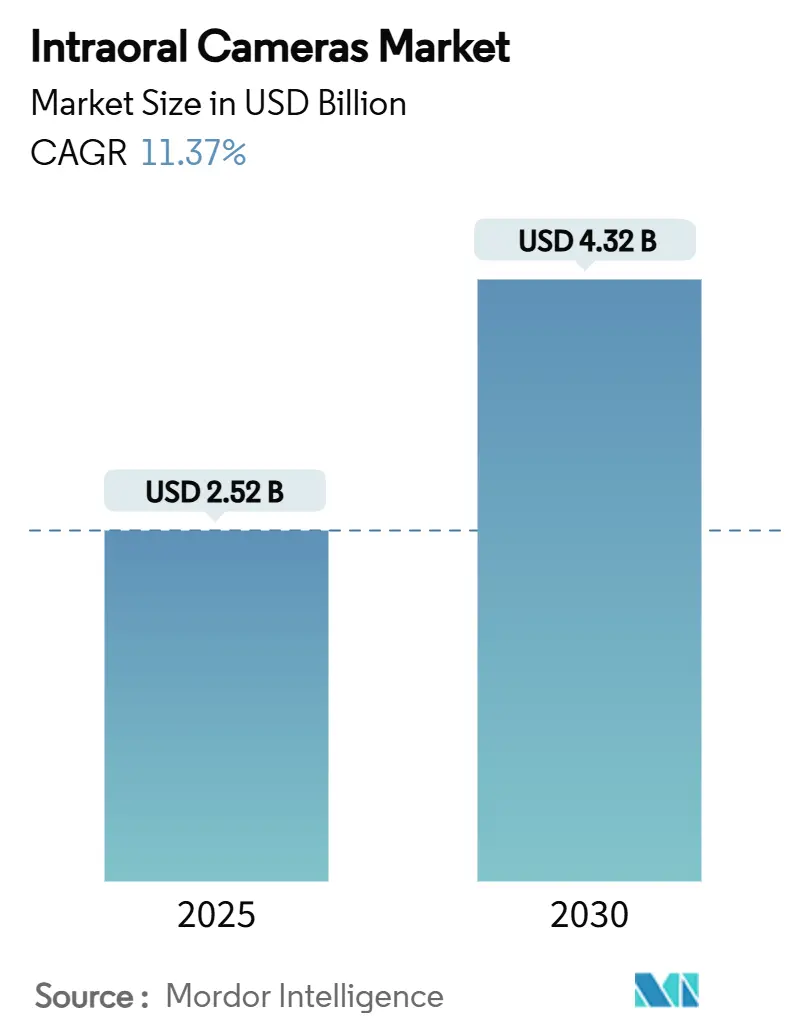

| Market Size (2025) | USD 2.52 Billion |

| Market Size (2030) | USD 4.32 Billion |

| Growth Rate (2025 - 2030) | 11.37% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intraoral Cameras Market Analysis by Mordor Intelligence

The intraoral cameras market is valued at USD 2.52 billion in 2025 and is forecast to reach USD 4.32 billion by 2030, expanding at an 11.37% CAGR. The market size increase reflects rapid teledentistry adoption, rising AI requirements, and stricter infection-control rules that together shift imaging from film to cloud-native workflows. Wireless scanners lower chair-time and let specialists review images instantly, improving throughput and revenue. Practices also favor cameras that integrate with AI decision-support modules, which improves diagnostic consistency and boosts reimbursement acceptance. Competitive activity centers on open application-programming-interface ecosystems that let offices link scanners, practice-management software, and cloud storage without vendor lock-in, reducing lifetime operating cost.

Key Report Takeaways

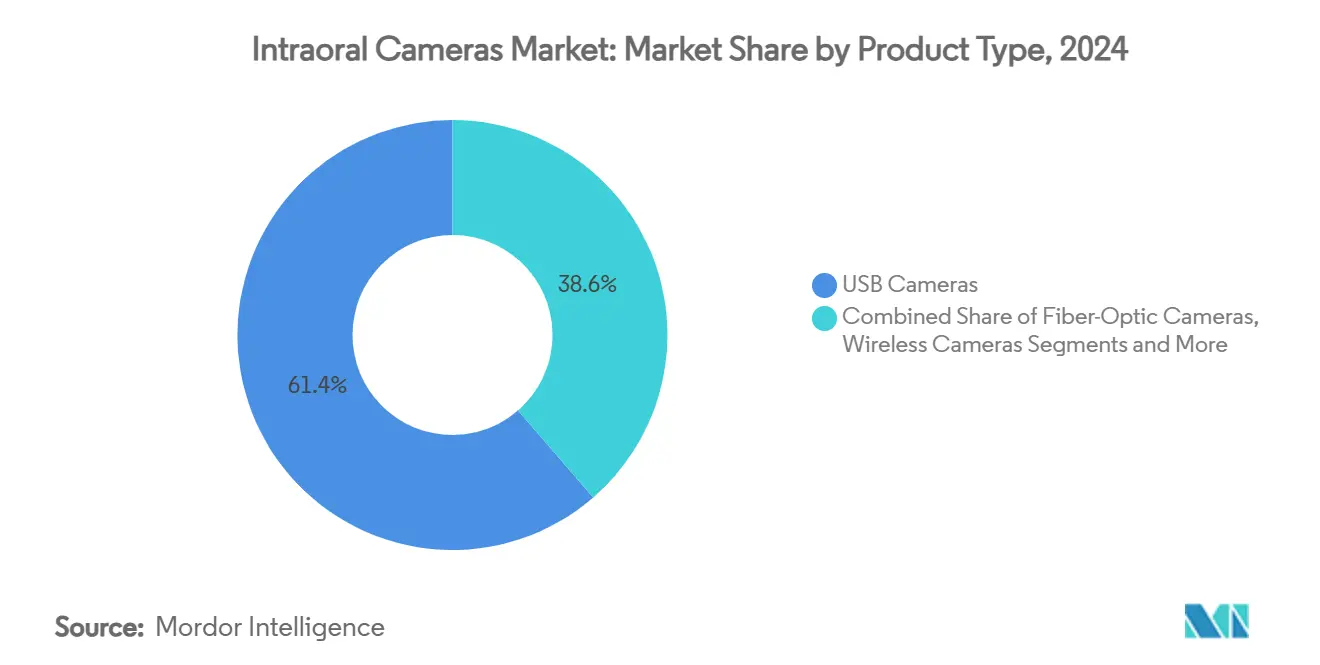

- By product type, USB cameras led with 61.36% revenue share in 2024, while wireless systems are projected to post a 14.56% CAGR to 2030.

- By sensor technology, CCD devices held 53.47% of intraoral cameras market share in 2024; CMOS sensors are forecast to advance at a 15.22% CAGR through 2030.

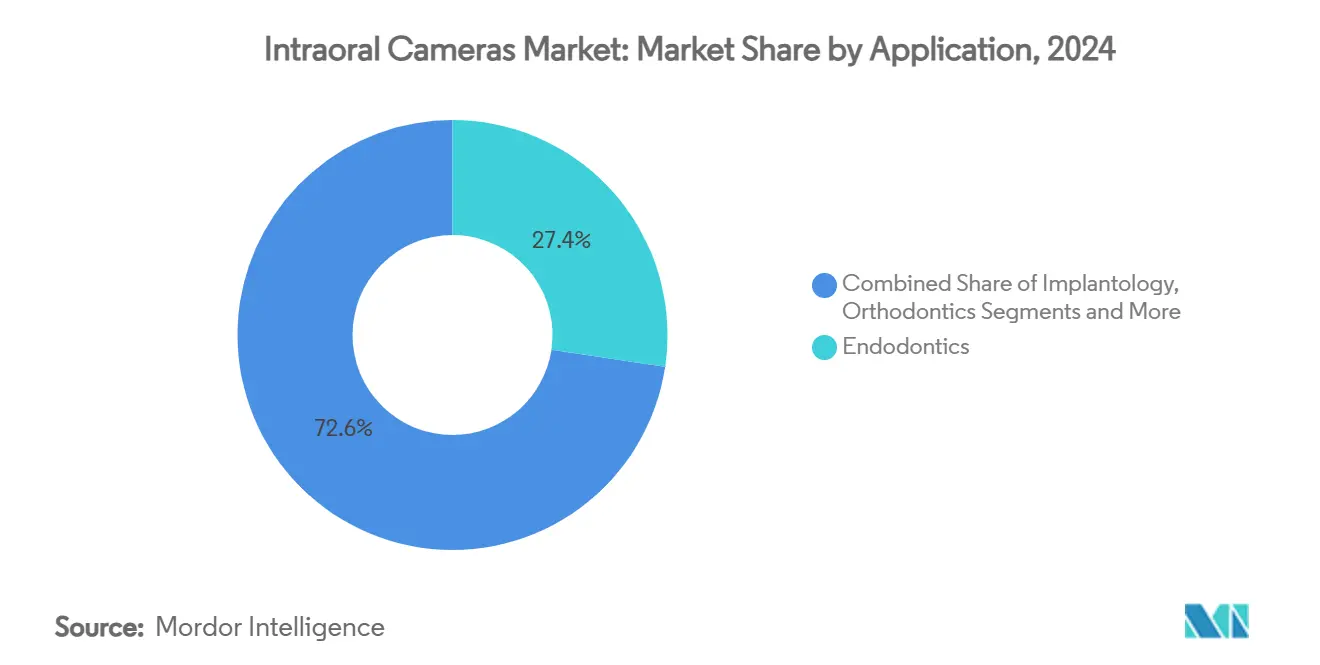

- By application, endodontics captured 27.36% of intraoral cameras market size in 2024, whereas orthodontics is poised for 14.76% CAGR growth to 2030.

- By end user, dental clinics accounted for 68.47% of intraoral cameras market size in 2024 and are set to expand at a 13.84% CAGR through 2030.

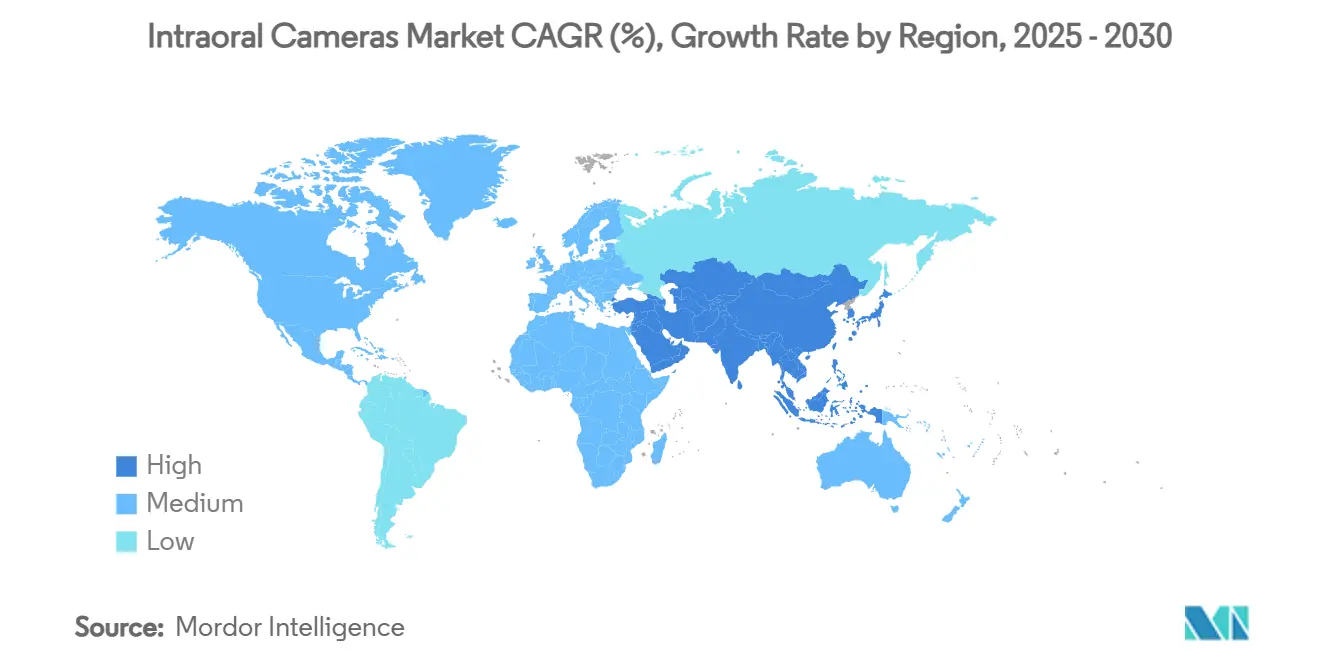

- By geography, North America commanded 36.72% of 2024 revenue; Asia-Pacific is projected to lead growth with a 13.47% CAGR to 2030.

Global Intraoral Cameras Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of dental caries and periodontal disease | +2.1% | Asia-Pacific and Latin America highest impact | Long term (≥ 4 years) |

| Rapid adoption of chair-side digital workflows | +1.8% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Accelerated uptake of teledentistry requiring high-quality imaging | +2.3% | Global with regulatory backing in US, Canada, Australia | Short term (≤ 2 years) |

| AI-driven diagnostic software demanding consistent imaging | +1.9% | North America and Europe, early uptake in Japan and South Korea | Medium term (2-4 years) |

| Social-media-fuelled demand for cosmetic dentistry visuals | +1.4% | Global with strongest pull in urban centers | Short term (≤ 2 years) |

| Infection-control standards favouring disposable-sheath devices | +1.2% | Strictest enforcement in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Dental Caries and Periodontal Disease

The growing burden of caries and periodontal disease keeps diagnostic demand high because early visual evidence improves patient acceptance of preventive therapy. Intraoral cameras reveal enamel demineralization and gingival changes that traditional radiographs may miss. Devices using fluorescence such as KaVo’s DIAGNOcam Vision Full HD add radiation-free detection that enhances patient safety. Insurers increasingly accept photo documentation to justify claims, which reinforces equipment purchases.

Rapid Adoption of Chair-Side Digital Workflows

Dental offices now integrate scanning, planning, and communication on one interface, cutting manual data transfer and wait times. Dentsply Sirona’s Primescan 2 streams images to any web-connected device, removing hardware locks and lowering ownership cost. Faster turnaround elevates patient satisfaction and keeps clinics competitive, fueling the intraoral cameras market.

Accelerated Uptake of Teledentistry Requiring High-Quality Imaging

Post-pandemic regulations permit remote diagnosis, provided image clarity equals chair-side assessment. Studies show teledentistry reaches 80–88% sensitivity when imagery meets quality standards.[1]Nalia Gurgel-Juarez et al., “Accuracy and Effectiveness of Teledentistry: A Systematic Review of Systematic Reviews,” Evidence-Based Dentistry, nature.com United States guidance formalizes format and security rules, giving practices confidence to invest. Demand therefore rises for wireless cameras that transmit consistent, high-resolution files.

AI-Driven Diagnostic Software Demanding Consistent Imaging

Machine-learning models perform best with standardized image resolution and lighting. The American Dental Association urges practices to choose equipment that aligns with AI pipelines.[2]American Dental Association, “Digital Dentistry and Technology,” ada.org Partnerships such as VideaHealth and Henry Schein One embed AI in hygiene programs, normalizing algorithm-ready imaging for new graduates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial equipment and upgrade costs | -1.7% | Greatest pressure in emerging markets | Medium term (2-4 years) |

| Reimbursement gaps for imaging procedures | -1.3% | North America and Europe variable by payer | Long term (≥ 4 years) |

| Data-security and privacy concerns with cloud connectivity | -0.9% | Strictest rules in EU and California | Short term (≤ 2 years) |

| Semiconductor supply volatility | -1.1% | Manufacturing concentrated in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Equipment and Upgrade Costs

Premium wireless cameras bundled with AI analytics cost far more than basic USB models. Budget-sensitive offices delay upgrades, especially where patient volume is low. Dentsply Sirona highlighted margin pressure from pricing sensitivity in its 2024 results. Vendors face the challenge of balancing advanced features with accessible pricing to protect wide adoption in the intraoral cameras market.

Reimbursement Gaps for Imaging Procedures

Coverage varies by insurer and region. Some payers limit diagnostic codes, leaving practices to absorb costs. Japan’s device market shows reimbursement scrutiny that slows premium technology uptake. Practices hesitate to commit capital without predictable returns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wireless Innovation Challenges USB Dominance

USB cameras held 61.36% of the intraoral cameras market in 2024 because they provide dependable imaging at an entry-level cost. The segment remains essential for routine documentation, especially in start-up clinics. However, wireless systems are on track for a 14.56% CAGR to 2030 as practices prioritize mobility and seamless integration with teledentistry portals. The intraoral cameras market size attributed to wireless devices is expected to grow the fastest between 2025 and 2030, mirroring demand for cordless operation during outreach programs and chair-side consultations.

Wireless adoption reflects rising expectations for hardware-agnostic workflows that share scans instantly across cloud dashboards. Dentsply Sirona’s Primescan 2 exemplifies this shift by streaming to any browser, removing old computer constraints. Fiber-optic and analog models retain niche roles, yet their contribution continues to shrink as digital transformation accelerates in the intraoral cameras market.

By Sensor Technology: CMOS Advancement Challenges CCD Leadership

CCD sensors retained 53.47% of intraoral cameras market share in 2024 because of proven color accuracy, important for shade matching. Nonetheless, CMOS sensors are projected to expand at 15.22% CAGR through 2030, powered by lower energy use and faster on-chip processing that suits AI overlays. The intraoral cameras market size for CMOS devices will therefore rise steadily as practices expect real-time caries detection on portable displays.

Hybrid solutions that merge CCD clarity with CMOS speed represent an experimental middle ground. Bibliometric mapping confirms research interest in AI integration, which favors CMOS because it supports high frame rates for live annotation.[3]Zhichang Zhang, “Machine learning in dentistry and oral surgery,” head-face-med.biomedcentral.com The portfolio shift signals that image-sensor innovation will remain a decisive factor in supplier competitiveness.

By Application: Orthodontics Growth Outpaces Endodontics Leadership

Endodontics accounted for 27.36% of the intraoral cameras market in 2024 thanks to its dependence on precise imaging for canal exploration. High-definition cameras guide apical cleaning and aid post-treatment monitoring, keeping demand stable. Meanwhile, orthodontics is forecast to grow at 14.76% CAGR through 2030 as clear aligner cases surge and AI-driven cephalometric apps gain traction.

Intraoral cameras feed face-driven planning engines that cut appointment time and improve alignment predictability. Implantology, prosthodontics, and periodontics add steady volume, while cosmetic dentistry leverages cameras for marketing content, together expanding the intraoral cameras market.

By End User: Dental Clinics Drive Market Growth

Dental clinics generated 68.47% of revenue in 2024 and will continue to post a 13.84% CAGR because independent practitioners make rapid buying decisions to stay competitive. The intraoral cameras market size in clinics benefits from shorter equipment approval cycles and direct links between image quality and case acceptance. Hospitals adopt cameras mainly for oral surgery wards and trauma screening, yielding moderate growth.

Dental schools and research institutes purchase high-spec models for training and protocol validation, keeping them a high-value niche. Mobile and teledentistry operators, though still small, illustrate future upside as governments back rural outreach. Evidence from institutional teledentistry programs shows reliable camera performance in remote pathology review. Their expansion will further diversify the intraoral cameras market.

Geography Analysis

North America led the intraoral cameras market with 36.72% share in 2024, supported by insurance codes that reimburse preventive imaging and by early teledentistry law harmonization. United States agencies publish clear cloud-security checklists, encouraging practices to connect scanners directly to remote specialists. Canada mirrors these trends, while Mexico accelerates public clinic modernization, collectively sustaining steady regional equipment turnover.

Asia-Pacific is projected to be the fastest-growing territory, delivering a 13.47% CAGR through 2030. China clarified device registration rules in 2024, shortening approval pathways for digital scanners. Japan remains an innovation hub despite reimbursement pressure, incentivizing suppliers to bundle cost-saving AI features. India, Indonesia, and Vietnam dedicate public funds to oral-health programs, creating first-time buyers and widening the intraoral cameras market base.

Europe exhibits moderate yet steady growth as dentists balance new-tech enthusiasm with stringent GDPR compliance. Germany and France welcome AI modules once data-protection impact assessments are met. United Kingdom focuses on National Health Service cost containment, pushing public practices toward value-oriented USB models. The Middle East, Africa, and South America show rising adoption in urban private clinics where premium cosmetic services justify higher camera investment, adding incremental volume to the intraoral cameras market.

Competitive Landscape

The intraoral cameras market shows moderate fragmentation. Legacy manufacturers such as Dentsply Sirona and Envista Holdings harness global distribution, while niche firms target differentiation through specialized optics and AI overlays. Competitive intensity rises as hardware, software, and cloud services converge into single purchase decisions. Vendors that integrate scanners with practice-management dashboards and secure backup gain stickiness.

Strategic moves illustrate this shift. Dentsply Sirona rolled out the DS Core cloud framework that syncs Primescan 2 images with treatment apps, giving clinicians device-agnostic access. OMNIVISION launched the ultra-small OCH2B30 module aimed at compact handheld scanners, broadening white-label options for emerging brands. Align Technology upgraded its iTero Lumina line to add AI-ready restorative functions, exemplifying convergence between orthodontic and restorative workflows.

Start-ups focus on subscription licensing that lowers initial cost and bundles artificial-intelligence analytics. Cloud-native platforms enable remote firmware updates, extended warranties, and pay-per-scan models that appeal to cost-conscious practices. These shifts forecast continued rivalry on ecosystem openness rather than raw hardware specifications in the intraoral cameras market.

Intraoral Cameras Industry Leaders

Carestream Dental

Envista Holdings

Dentsply Sirona

Planmeca Oy

Acteon Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Align Technology introduced restorative modules for the iTero Lumina intraoral scanner line, adding interproximal caries detection and multidisciplinary workflow support.

- June 2024: OMNIVISION released the OCH2B30 CameraCubeChip module, delivering 3D imaging for portable intraoral scanners.

- January 2024: KaVo unveiled the ProXam iCam intraoral camera featuring macro mode and foot control for enhanced documentation.

Global Intraoral Cameras Market Report Scope

| USB Cameras |

| Fiber-Optic Cameras |

| Wireless Cameras |

| Analog / Traditional Cameras |

| CCD Sensors |

| CMOS Sensors |

| Hybrid (CCD + CMOS) Sensors |

| Endodontics |

| Implantology |

| Orthodontics |

| Prosthodontics |

| Periodontics |

| Others |

| Dental Clinics |

| Hospitals |

| Dental Academic & Research Institutes |

| Others (Mobile/Teledentistry Providers) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | USB Cameras | |

| Fiber-Optic Cameras | ||

| Wireless Cameras | ||

| Analog / Traditional Cameras | ||

| By Sensor Technology | CCD Sensors | |

| CMOS Sensors | ||

| Hybrid (CCD + CMOS) Sensors | ||

| By Application | Endodontics | |

| Implantology | ||

| Orthodontics | ||

| Prosthodontics | ||

| Periodontics | ||

| Others | ||

| By End User | Dental Clinics | |

| Hospitals | ||

| Dental Academic & Research Institutes | ||

| Others (Mobile/Teledentistry Providers) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current value of the intraoral cameras market?

The intraoral cameras market is valued at USD 2.52 billion in 2025.

2. How fast is the intraoral cameras market expected to grow?

The market is projected to expand at an 11.37% CAGR, reaching USD 4.32 billion by 2030.

3. Which product type holds the largest share of the intraoral cameras market?

USB cameras lead with 61.36% revenue share in 2024.

4. Why are wireless intraoral cameras growing quickly?

Wireless models support teledentistry workflows and real-time cloud collaboration, leading to a 14.56% forecast CAGR.

5. Which region offers the fastest market growth opportunity?

Asia-Pacific is projected to deliver a 13.47% CAGR thanks to regulatory reforms and healthcare digitalization.

6. How are AI applications influencing camera specifications?

AI modules require standardized high-resolution images, which is driving adoption of CMOS sensors and cloud-connected scanners.

Page last updated on: