Maple Syrup Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.93 Billion |

| Market Size (2031) | USD 4.04 Billion |

| Growth Rate (2026 - 2031) | 6.63% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

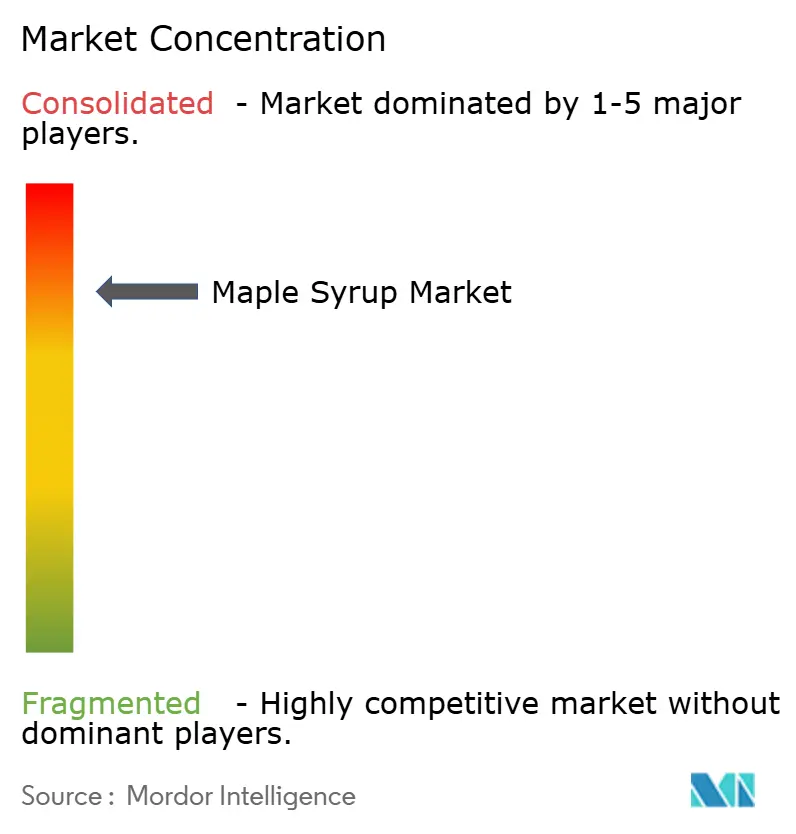

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Maple Syrup Market Analysis by Mordor Intelligence

The maple syrup market size was valued at USD 2.75 billion in 2025 and estimated to grow from USD 2.93 billion in 2026 to reach USD 4.04 billion by 2031, at a CAGR of 6.63% during the forecast period (2026-2031). Rising consumer preference for natural sweeteners, clean-label foods, and transparent sourcing underpins robust demand growth across all regions. Quebec’s strategic reserve fell from 133 million pounds to 6.9 million pounds in 2024, tightening supply and pushing producers to adopt yield-optimization technology according to Statistics Canada[1]Statistics Canada, "Quebec’s strategic reserve", www150.statcan.gc.ca. Furthermore, climate variability, evidenced by shorter sap seasons and lower sugar content, intensifies this supply pressure as per United States Environmental Protection Agency[2]United States Environmental Protection Agency, "climate variability", www.epa.gov . Industrial buyers now integrate maple syrup into processed foods, beverages, and sports nutrition, broadening usage beyond retail staples. At the same time, geographic expansion into Asia-Pacific and diversification into organic formats create fresh revenue streams for stakeholders in the maple syrup market.

Key Report Takeaways

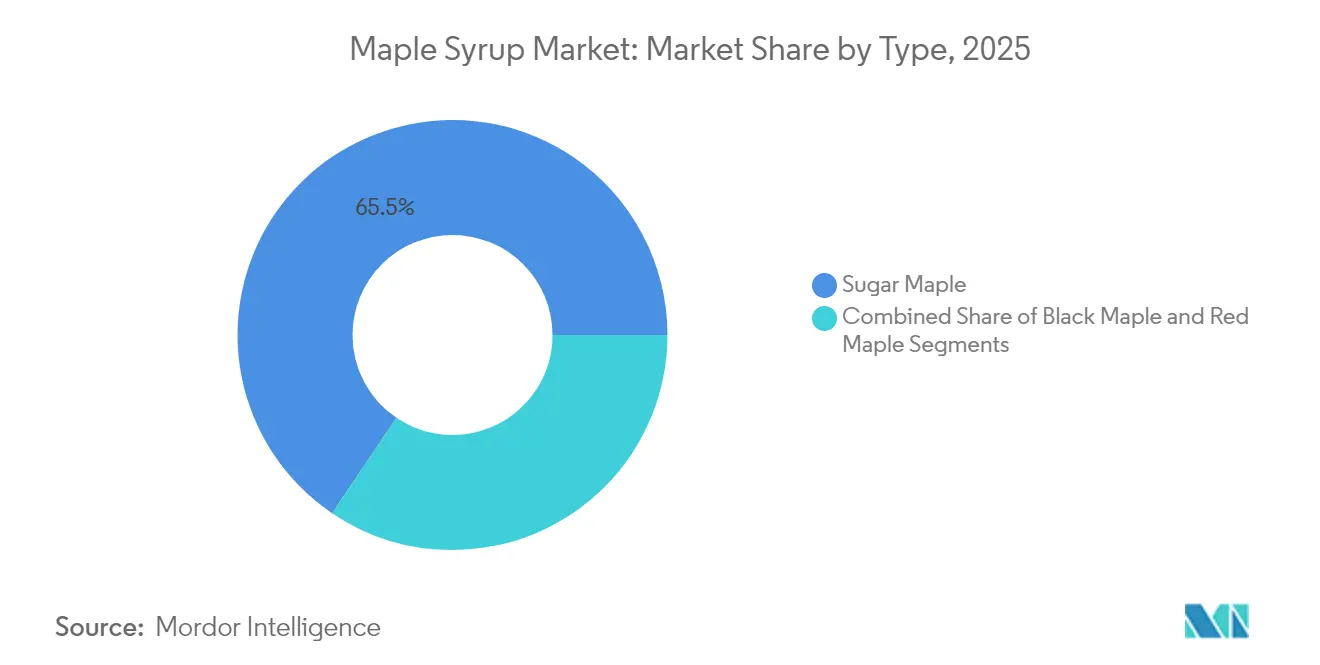

- By type, sugar maple accounted for 65.54% of the maple syrup market size in 2025; black maple will rise at an 8.12% CAGR between 2026 and 2031.

- By category, conventional products led with 69.42% revenue share in 2025, while organic offerings are set to expand at a 8.78% CAGR through 2031.

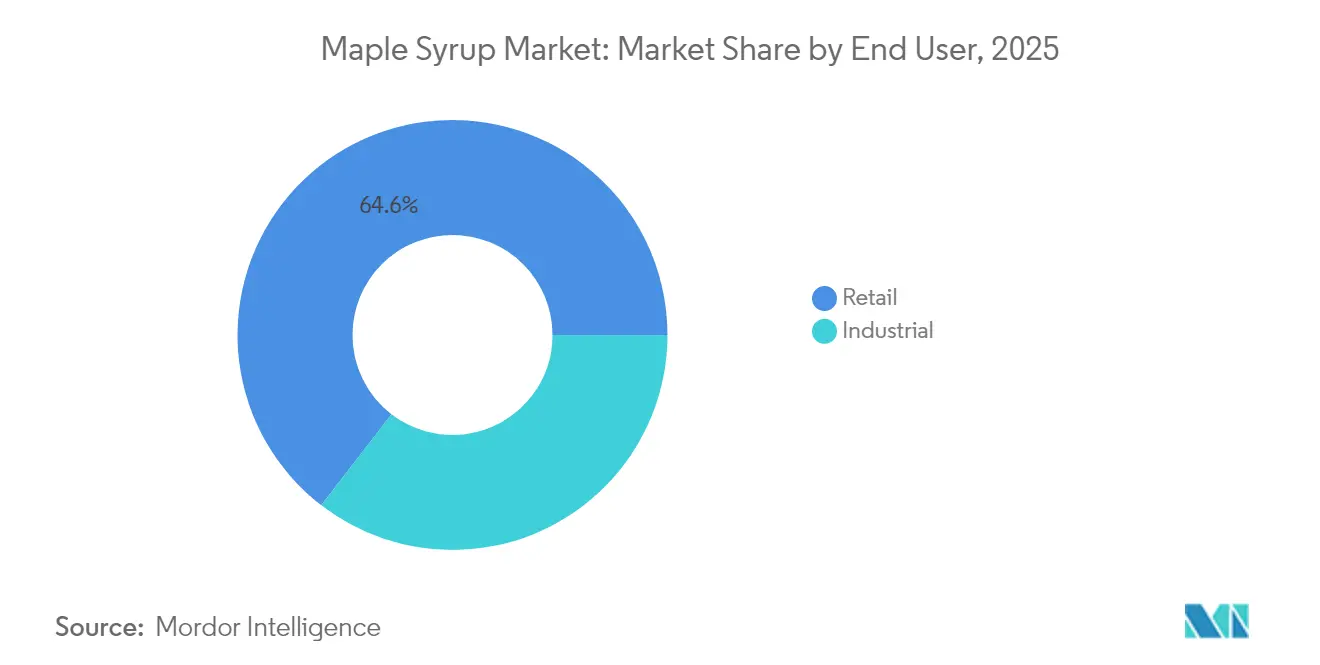

- By end-user, retail retained 64.55% share of the maple syrup market size in 2025; industrial channels are forecast to climb at an 8.29% CAGR to 2031.

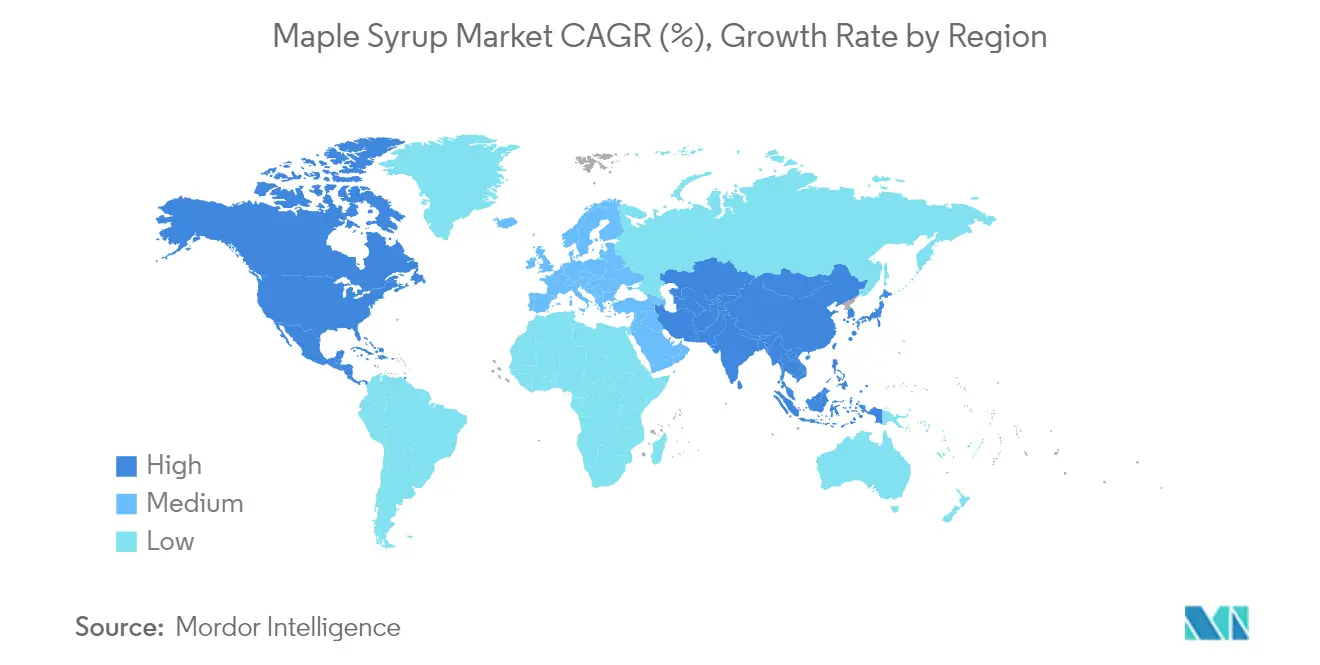

- By geography, North America held 71.48% of maple syrup market share in 2025; Asia-Pacific is projected to grow at a 9.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Maple Syrup Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer demand for natural and low-sugar sweeteners | +1.2% | Global, with premium positioning in North America and Europe | Medium term (2-4 years) |

| Increasing use in processed and ready-to-eat foods | +0.8% | North America core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Expanding role as a flavoring agent in dairy, bakery, and beverages | +1.1% | Global, with European premium applications leading | Medium term (2-4 years) |

| Emerging use in sports nutrition and functional foods | +0.9% | North America and Europe, early adoption in Asia-Pacific | Long term (≥ 4 years) |

| Government support for maple syrup production and exports in canada | +1.0% | North America, with export spillover globally | Short term (≤ 2 years) |

| Rising adoption in plant-based and vegan diets | +0.7% | Global, concentrated in urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Demand for Natural and Low-Sugar Sweeteners

As consumers increasingly turn to natural alternatives, the maple syrup market is witnessing a notable uptick, especially as they distance themselves from refined sugars. According to the U.S. Department of Agriculture[3]U.S. Department of Agriculture, "Organic Retail Sales", ers.usda.gov , organic retail sales hit USD 69.7 billion in 2023, with natural sweeteners carving out a larger share as consumers prioritize clean-label ingredients. A one-minute antioxidant test from McGill University empowers producers to validate nutritional benefits, bolstering health claims. In Europe, importers are ramping up procurement volumes, opting for sustainable syrups over artificial additives. The growing awareness of the environmental impact of food production is also driving demand for maple syrup, as it is perceived as a more eco-friendly option. Additionally, the rise of plant-based diets has further increased the appeal of maple syrup as a versatile and natural sweetener. Innovations in packaging and product formulations are also helping producers cater to evolving consumer preferences. Collectively, these dynamics are expanding the use of maple syrup beyond traditional breakfast applications and enhancing consumers' willingness to pay a premium, thus reshaping the competitive landscape of the maple syrup market.

Increasing Use in Processed and Ready-to-Eat Foods

In a nod to consumer preferences for recognizable ingredients, food manufacturers are increasingly incorporating maple syrup into a diverse range of products, from snacks and sauces to beverages and ready meals. According to CBI (Centre for the Promotion of Imports from developing countries)[4]CBI (Centre for the Promotion of Imports from developing countries), "Europe's Import of Maple Syrup", www.cbi.eu , Europe’s import value for natural syrup is on the rise, with Germany, France, and the United Kingdom actively seeking clean-label inputs. Highlighting the market's potential, B&G Foods has entered into long-term supply agreements for its Maple Grove Farms line, bolstering its shelf-stable product launches. Such industrial demand not only stabilizes off-season interest but also encourages processors to secure contracts, fortifying the overall resilience of the maple syrup market. Additionally, the growing consumer inclination toward natural sweeteners over artificial alternatives has further propelled the demand for maple syrup. The product's rich nutritional profile, including antioxidants and minerals, has also contributed to its popularity among health-conscious consumers. Furthermore, the increasing adoption of maple syrup in plant-based and vegan food products has opened new growth avenues for the market.

Expanding Role as a Flavoring Agent in Dairy, Bakery, and Beverages

From yogurt and cheese to pastry glazes and specialty coffees, maple syrup is elevating flavor profiles. McCormick & Company underscores the importance of natural ingredients in its flavor strategy. European craft bakeries leverage syrup as a hallmark of authenticity, boosting profit margins and reducing seasonality. Beverage producers, spanning craft cocktail bars to functional drink brands, are increasingly incorporating maple syrup, broadening their revenue streams in the process. The growing consumer preference for clean-label and organic products further supports the demand for maple syrup. Additionally, its versatility as a natural sweetener positions it as a healthier alternative to refined sugar. This trend is expected to drive innovation in product formulations across various food and beverage categories.

Emerging Use in Sports Nutrition and Functional Foods

Maple syrup's unique flavor profile is gaining recognition as a premium ingredient in dairy products, baked goods, and specialty beverages, driving value-added applications beyond traditional sweetening functions. The trend toward artisanal and craft food products is creating opportunities for maple syrup as a signature ingredient that conveys authenticity and regional character. McCormick & Company's global flavor leadership position demonstrates how natural ingredients like maple syrup are becoming integral to product differentiation strategies in competitive food categories. The beverage industry is experimenting with maple syrup in craft cocktails, specialty coffees, and functional drinks, expanding consumption occasions beyond breakfast. This diversification reduces seasonal demand volatility and creates higher-margin applications that justify premium pricing structures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Climate change impacts on maple tree health and sap production | -0.9% | North America core production regions | Long term (≥ 4 years) |

| Geographical constraints of sugar maple tree availability | -0.6% | Global, limiting production expansion | Long term (≥ 4 years) |

| Competition from alternative sweeteners | -0.8% | Global, particularly in price-sensitive segments | Medium term (2-4 years) |

| High initial investment costs for production equipment | -0.4% | North America, affecting new entrant barriers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from Alternative Sweeteners

The maple syrup market faces intensifying competition from diverse natural and artificial sweetener options, particularly in price-sensitive applications where cost considerations outweigh premium positioning. Alternative natural sweeteners like agave, honey, and stevia are gaining market share in health-conscious consumer segments, while artificial sweeteners maintain cost advantages in industrial applications. The competitive pressure is most acute in processed food applications where functionality and cost-effectiveness determine ingredient selection over flavor considerations. Consumer education about maple syrup's unique nutritional profile and sustainability credentials becomes critical for maintaining market position against aggressive marketing of alternative sweeteners. Price volatility in maple syrup, driven by climate-related production variability, creates opportunities for competitors to gain market share during periods of maple syrup scarcity or high pricing.

Climate Change Impacts on Maple Tree Health and Sap Production

Climate variability is fundamentally altering maple syrup production patterns, with warming temperatures shortening sap collection seasons and reducing sugar content in harvested sap. The U.S. Environmental Protection Agency reports that Vermont's maple syrup production is experiencing shortened seasons due to warmer winter temperatures, with the ideal geographic range for production expected to shift northward by nearly 250 miles by 2100. University of Vermont research indicates that 89% of producers have encountered negative impacts from climate change, including unpredictable sap runs and declining production yields. Through technological advancements in sap collection and forest management, producers are diversifying species, incorporating climate-resilient red maple varieties. The industry's sustainability hinges on these adaptive strategies and possible shifts in production centers, casting uncertainty on established operations and infrastructure investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Sugar Maple Dominance Faces Climate Pressure

Sugar maple accounted for 65.54% of maple syrup market share in 2025, underpinned by high sucrose content and entrenched processing infrastructure. Yet climate stress fuels black maple’s 8.12% CAGR, as producers diversify stands to reduce weather risk. Red maple and even boxelder trials in Utah indicate that non-traditional species can extend production zones, signalling a gradual rebalancing of supply sources. Sugar maple’s dominance is therefore expected to erode slightly, although its superior flavor keeps it central to premium positioning in the maple syrup market. Boxelder sap studies from Utah State University show yields up to 26.4 liters per tap, supporting expansion into arid western states.

Production economics revolve around tap density and sugar concentration. Sugar maple’s higher sugar percentage still delivers favorable cost curves despite rising fuel and labor. However, black maple’s hardiness and tolerance for warmer nights lower climate risk exposure, which may attract new investment. Producers weigh these trade-offs when planning long-term sugarbush composition, reinforcing a dynamic supply structure in the maple syrup market.

By Category: Organic Acceleration Outpaces Conventional Growth

Conventional syrup held 69.42% of revenue in 2025, due to scale advantages and retail familiarity. The organic segment, however, is expanding at 8.78% CAGR, spurred by the USDA USD 300 million Organic Transition Initiative that subsidizes certification and practice conversion. Organic quality premiums help offset higher audit and segregation expenses. European buyers, led by Germany, favor certified imports, creating export incentives for Canadian producers. Organic maple syrup exceeds conventional product price by up to 30% in many supermarkets, supporting producer margins.

While conventional volumes still anchor shelf presence, input cost inflation and reserve depletion pressure pricing. These factors narrow the price gap and raise consumer openness to organic alternatives. Robust audit trails and new rapid antioxidant testing from McGill University increase transparency, which strengthens consumer trust and accelerates organic penetration. The maple syrup market thus shows a gradual tilt toward certified products without displacing mainstream offerings.

By End User: Industrial Applications Drive Growth Beyond Retail

In 2025, retail channels accounted for 64.55% of the maple syrup market, driven by its integral role in household cooking and breakfast traditions. Meanwhile, industrial channels, growing at a robust 8.29% CAGR, have expanded to encompass bakeries, beverage brands, sports nutrition, and even cosmetics. B&G Foods has secured multi-year contracts, ensuring input stability for its shelf-stable sauces and snacks. Foodservice operators are increasingly incorporating maple syrup into seasonal menus and craft beverages, effectively broadening its usage throughout the year.

Following prototypes from Cornell University, sports nutrition brands are now formulating gels and drinks with maple syrup, emphasizing clean-label energy. Concurrently, innovators in personal care are delving into maple's phenolic compounds, harnessing them for skincare products, thus carving out a niche yet promising category. The growing demand for natural and organic ingredients further supports the adoption of maple syrup across industries. Additionally, advancements in processing technologies are enhancing the quality and shelf life of maple syrup, making it more appealing to manufacturers. This diversification of applications is expected to drive sustained growth in the market over the forecast period. This broadening of channels not only diminishes the seasonality of maple syrup but also deepens its integration into global supply chains, significantly expanding the maple syrup market.

Geography Analysis

North America accounts for 71.48% of current demand in 2025, benefiting from dense forest resources and ingrained culinary traditions. Canada produced 19.9 million gallons in 2024, a 91.3% jump over the weather-impacted 2023 season according to Statistics Canada. The United States generated 4.18 million gallons, though Vermont’s total fell 15% year on year due to erratic freeze-thaw cycles. Reserve depletion in Quebec tightens spot supply, which amplifies price swings across the maple syrup market.

Europe remains a premium destination, importing USD 100.55 million in 2023, with Germany, the Netherlands, and the United Kingdom as top buyers according to the World Bank. Food and beverage makers substitute refined sugars with maple to capture sustainability-minded shoppers. Regulatory alignment around organic and sustainable sourcing favors certified products, fostering stable growth even at higher price points.

Asia-Pacific is the fastest riser, recording a 9.07% CAGR through 2031 on the back of urban middle-class expansion and growing appetite for Western flavors. Japan leads imports courtesy of preferential tariffs and high purchasing power according to USDA (U.S. Department of Agriculture). Australian and South Korean retailers spotlight maple syrup in specialty aisles, while food processors incorporate it into sauces and ice creams. Limited local production keeps the region reliant on imports, extending long-term upside for global suppliers in the maple syrup market.

Note: Segment shares of all Individual segments will be available upon report purchase

Regulatory Landscape

Maple syrup quality, grading, and labeling are governed by food regulators and grade standards that shape both domestic compliance and export requirements. In Canada, the Canadian Food Inspection Agency (CFIA) oversees maple product labeling and grade rules under the Safe Food for Canadians Act framework, and the Canadian Grade Compendium (Volume 7) details the grade designations used in trade. In the United States, USDA Agricultural Marketing Service (AMS) standards define grades for maple syrup. These standards are voluntary, but they become enforceable when products carry official U.S. grade marks.

At the state level, additional rules influence producer practices and inspections. Vermont's Agency of Agriculture, Food and Markets maintains maple product requirements, including Grade A composition specifications, and it began periodic compliance inspections in July 2025 for maple operations covered by state rules. Separately, trade measures affecting imported equipment (rather than finished syrup) have been cited as a cost variable for producers, which can increase sensitivity to capital purchases such as storage and processing hardware when exemptions do not apply.

Value Chain Analysis

The value chain starts with forest management and tapping (tubing, spouts, and collection systems), followed by sap collection, concentration (commonly reverse osmosis), evaporation, filtration, and quality testing before bulk storage. Quebec remains the central aggregation and commercialization hub, where bulk syrup from many producers is pooled and marketed through collective structures. The Producteurs et productrices acéricoles du Québec (QMSP) coordinates sales mechanisms, grade compliance, and strategic supply tools, including the Quebec reserve, which helps buffer poor seasons.

Downstream, processors and packers handle blending, grading verification, bottling, and labeling for retail and industrial customers, then distribute through grocery, specialty retail, foodservice, and ingredient channels to international buyers. In 2026, QMSP reported 229.5 million pounds of production and noted that processors purchased 202 million pounds, with 181.3 million pounds exported, highlighting the importance of export logistics and documentation across many destination markets. Key friction points include packaging automation requirements, inspection and traceability demands, and the operational impact of enforcement actions. In April 2026, QMSP pursued legal action regarding alleged adulteration and non-compliance with collective marketing rules, reinforcing the role of oversight in protecting grade integrity and downstream brand trust.

Competitive Landscape

The maple syrup market is consolidated. Some of the major players include B&G Foods, Inc., The J.M. Smucker Company, Vermont's Pleasant Valley Maples, Crown Maple LLC, and Bascom Maple Farms, Inc., among others. The Federation of Quebec Maple Syrup Producers oversees approximately 72% of the global supply and regulates export quotas, affording it significant scale leverage. Large processors such as B&G Foods utilize vertical integration and multi-channel distribution to command shelf space and industrial contracts. Technology is rising as a differentiator; McGill University’s AI-enabled quality test allows producers to guarantee antioxidant levels, which supports premium pricing.

Smaller farms pursue organic certification, farm-gate sales, and specialty infusions to stand out. Direct-to-consumer platforms enable higher margins and stronger brand storytelling. Partnerships between equipment makers and producers accelerate the adoption of high-vacuum tubing and sensor networks that raise yields per tap. Investment also flows toward research on alternative tree species, aiming to hedge climate risk and open new geographies for the maple syrup market.

Strategic actions underscore this dual track. B&G Foods expanded industrial capacity to serve snacking clients, while several Vermont cooperatives pooled resources for export logistics. At the same time, niche brands launched maple-based sports gels and skincare lines. These moves illustrate an evolving ecosystem where scale efficiency and niche innovation coexist.

Maple Syrup Industry Leaders

-

B&G Foods Inc.

-

The J.M. Smucker Company

-

Vermont Pleasant Valley Maples

-

Crown Maple LLC

-

Bascom Maple Farms, Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Productivity and energy-efficiency upgrades are a clear opportunity area as producers respond to tighter supply conditions and higher operating costs without expanding land footprint. A 2026 peer-reviewed study reported that vacuum extraction materially lifts sap yield versus gravity systems, supporting broader adoption of high-vacuum collection alongside reverse osmosis and optimized evaporation in professional operations. Equipment makers are also advancing electrification pathways for sugarhouses, illustrated by CDL Inc.'s launch of the Master-E electric evaporator system in April 2025, which aligns with producer interest in reducing fuel dependence and improving controllability during variable seasons.

Controlled capacity expansion in core supply regions and broader geographic participation also create whitespace for processors and brand owners. Quebec continues to manage growth through tap issuance programs, including the announcement of 7 million new taps in June 2025, while 2026 production and export volumes reported by QMSP underscore how reliant the market is on scalable, compliant bulk supply for both retail and industrial demand. On the demand side, opportunities concentrate in industrial ingredient use (processed foods, beverages, and sports nutrition) and in certified product differentiation, where CFIA and USDA-aligned grading and labeling frameworks support smoother cross-border trade for standardized grades and for organic lines sold into premium import markets.

Recent Industry Developments

- March 2026: B&G Foods completed the divestiture of its Green Giant U.S. frozen product line effective March 2, 2026. The transaction sharpened portfolio focus around shelf-stable brands, supporting continued prioritization of Maple Grove Farms within the company's branded food platform.

- February 2025: B&G Foods entered into a new credit agreement and related financing arrangements, as disclosed in an SEC filing. The refinancing strengthened liquidity and covenant structure that underpins working-capital needs and procurement programs across its shelf-stable portfolio, including maple syrup-related brands.

- November 2024: McGill University researchers introduced an AI and Raman spectroscopy method that measures antioxidant content in maple syrup in under one minute. Faster, lower-cost quality verification supports premium positioning and tighter batch-to-batch control for producers and packers supplying both retail and industrial customers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of maple syrup sold commercially, including pure and blended offerings, across retail and foodservice uses, measured in value terms at the point of sale from producers and brand owners.

Scope exclusions: We exclude non-maple syrups, maple-flavored sweeteners without maple content, and maple-derived products that are not syrup (such as maple sugar and maple candies).

Segmentation Overview

-

By Type

- Sugar Maple

- Black Maple

- Red Maple

-

By Category

- Conventional Maple Syrup

- Organic Maple Syrup

-

By End User

- Retail

-

Industrial

- Food Processing Companies

- Foodservice

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to map the supply base and set practical boundaries for what qualifies as maple syrup in trade and production statistics. We relied on public, non-paywalled sources such as agriculture departments and statistical agencies in key producing regions, customs and trade databases released by governments, food labeling and organic standards from regulators, and association or board publications tied to maple producers.

To translate these inputs into a usable market model, pricing and volume signals were cross-checked against company filings, investor presentations, and reputable press coverage on crop seasons, plus export-import commentary from public trade releases. Where needed, we also used paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export records to confirm directional trends and resolve unclear points. These desk sources are not exhaustive, and many other references were used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating how the market behaves in practice, with a specific focus on grade mix, pack sizes, and the split between retail demand and ingredient usage. We spoke with stakeholders across producers, packers, distributors, and food manufacturers, then we checked inputs with buyers and channel specialists so assumptions on pricing, seasonality, and availability could be corrected before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 19% | APAC: 46% |

| Mid tier: 45% | Functional/Unit leaders: 30% | EMEA: 31% |

| Smaller Players: 19% | Managers: 51% | Americas: 23% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where production, trade flows, and consumption patterns were reconstructed by region, then converted into value using observed price bands for bulk and packaged syrup. To keep the totals grounded, we corroborated the results with selective bottom-up approximations, such as sampled supplier and brand roll-ups, channel checks, and a volume times average selling price build using typical pack formats.

Key model inputs included annual maple sap and syrup output trends in main producing areas, export and import movements that explain redistribution, average price spreads between bulk and retail packs, the shift toward organic and premium grades, and food manufacturing usage intensity for bakery, dairy, and beverage flavoring. For forecasts, scenario analysis was applied around crop yield variability and pricing, with demand expectations shaped by primary feedback on natural sweetener adoption and private-label expansion. Where company-level revenue was not separable for maple syrup alone, gaps were handled through product-mix estimates and cross-checks against shipment and category proxies.

Data Validation & Update Cycle

Results were validated through multiple checks, where model outputs were compared against independent signals such as trade intensity, production season outcomes, and observed price direction across key channels. Outliers were reviewed, assumptions were challenged in internal analyst reviews, and follow-up calls were triggered when a metric moved materially or did not reconcile with interview feedback.

Reports are refreshed on an annual cycle, with interim updates when major events occur, including unusual harvest swings, policy changes affecting labeling, or meaningful pricing shocks. Before delivery, we run a final pass to confirm the latest public releases and news signals are reflected in the final view.

Mordor Intelligence's Maple Syrup Market Estimate Compared With Other Published Estimates

Published maple syrup market sizes often do not align because the scope is set differently, the value point in the chain is not consistent, and the base year pricing used for conversion can vary. Differences can also appear when one estimate leans heavily on a single region or a single channel, which can unintentionally undercount food manufacturing demand or overcount reseller margins.

The biggest gap driver is whether reseller and retail markups are added on top of producer and brand owner revenues, where Mordor Intelligence keeps the value anchored to maple syrup sales without stacking downstream resales, then checks totals against production and trade signals to avoid double counting.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.93 B (2026) | |

| Industry Publisher A | USD 1.64 B (2025) | Uses an earlier base year and appears to apply a narrower value build, with limited clarity on whether industrial demand and bulk pricing are treated separately from retail-packed syrup. |

| Global Publisher B | USD 1.70 B (2025) | States a factory-gate framing and shorter horizon, which can keep totals lower if packaged retail uplift and cross-border redistribution effects are not fully reconciled. |

The spread in the table mainly comes from value-chain treatment and base-year alignment, not from disagreement that the category is growing. By tying volumes to production and trade movements and then applying transparent price and mix assumptions, the model stays repeatable and easier to reconcile when new season data is released.

Key Questions Answered in the Report

What is the current size of the maple syrup market?

The maple syrup market size stands at USD 2.93 billion in 2026 and is forecast to reach USD 4.04 billion by 2031.

Which region dominates maple syrup consumption?

North America leads with 71.48% of 2025 revenue, supported by concentrated production in Quebec and Vermont.

What factors drive the rapid growth of organic maple syrup?

Organic certification attracts premium-seeking consumers and benefits from the USDA Organic Transition Initiative, leading to a 8.78% CAGR through 2031.

How is climate change affecting maple syrup production?

Warmer winters shorten sap runs and reduce sugar content, prompting producers to adopt technology and diversify tree species.

Why are industrial applications important for future growth?

Food processors, beverage makers, and sports nutrition brands are integrating maple syrup as a clean-label ingredient, propelling an 8.29% CAGR in industrial demand.

Page last updated on: