Chinese Automotive Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

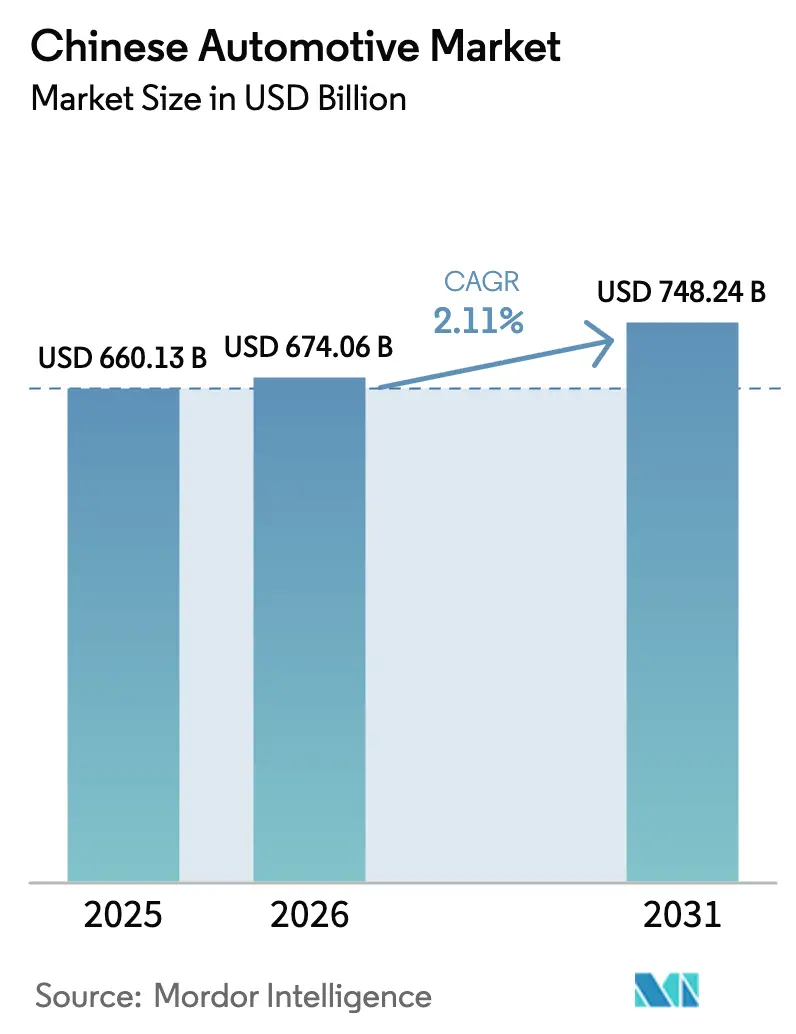

| Base Year Market Size (2025) | USD 660.13 Billion |

| Market Size (2026) | USD 674.06 Billion |

| Market Size (2031) | USD 748.24 Billion |

| Growth Rate (2026 - 2031) | 2.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chinese Automotive Market Analysis by Mordor Intelligence

Chinese Automotive Market size in 2026 is estimated at USD 674.06 billion, growing from 2025 value of USD 660.13 billion with 2031 projections showing USD 748.24 billion, growing at 2.11% CAGR over 2026-2031. This growth outlook shows how the market is shifting from pure volume expansion to value creation built on electrification, software-defined features, and premium positioning. Passenger-car demand continues to supply most unit sales. Yet, New Energy Vehicles (NEVs) already account for 40.9% of total registrations, signaling an inflection point where electric drivetrains outpace internal-combustion growth. Battery-cost reductions, a nationwide build-out of charging points, and a steady pipeline of provincial incentives sustain momentum even as overall sales growth moderates. Competitive intensity rises as domestic players deepen vertical integration, while foreign incumbents redesign strategies to protect share and restore margins amid cost pressure and stricter efficiency rules.

Key Report Takeaways

- By vehicle type, passenger cars captured 47.62% of the Chinese automotive market share in 2025, whereas light commercial vehicles are projected to advance at a 2.14% CAGR during the forecast period (2026-2031).

- By propulsion, internal-combustion models retained a 62.35% share of the Chinese automotive market in 2025, yet electric vehicles are poised to grow fastest at a 15.34% CAGR during the forecast period (2026-2031).

- By application, personal use accounted for 53.62% of the Chinese automotive market share in 2025, while public transport is on track for a 2.23% CAGR during the forecast period (2026-2031).

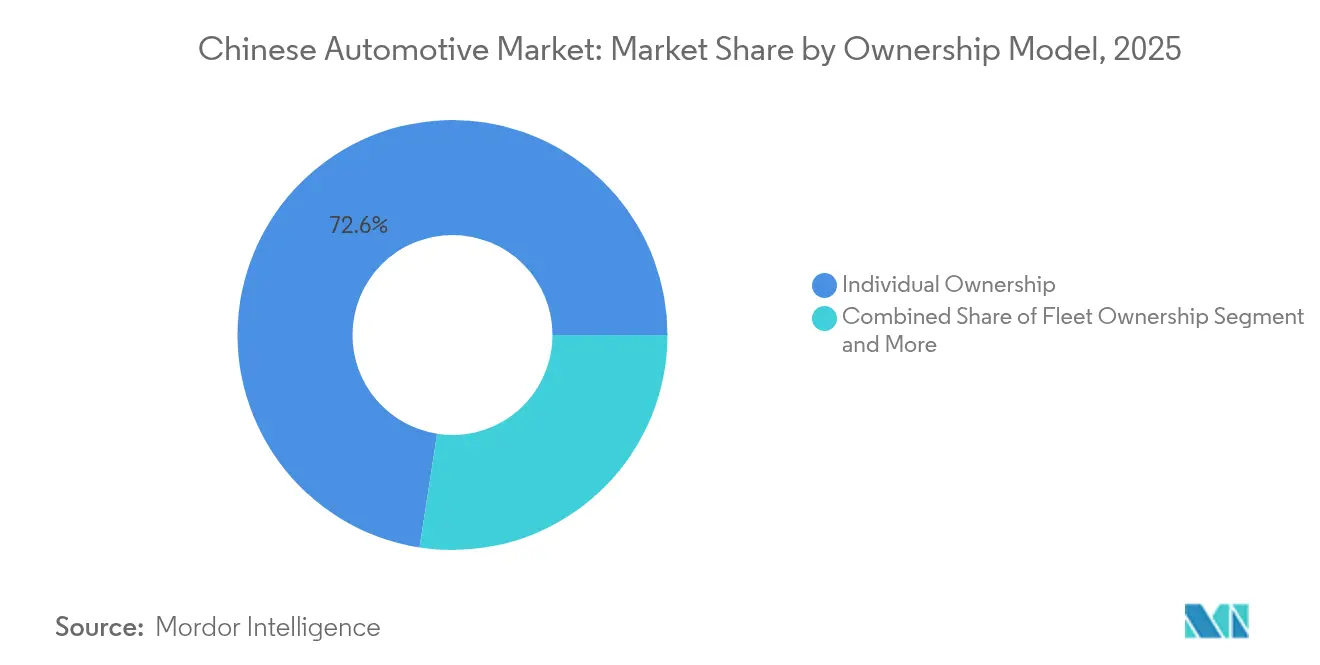

- By ownership model, Individual buyers held a 72.55% of the Chinese automotive market share in 2025; subscription services are set to expand at a 2.18% CAGR during the forecast period (2026-2031).

- OEM dealers delivered 56.02% of the Chinese automotive market share by sales channel in 2025. In contrast, direct-to-consumer models are expected to drive the growth at a 2.22% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Chinese Automotive Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CAAM-Led Rebound | +0.8% | National, concentrated in Tier 1-2 cities | Short term (≤ 2 years) |

| Mandatory 2030 CAFE Phase-2 Standards | +0.4% | National, with stricter enforcement in Beijing, Shanghai | Long term (≥ 4 years) |

| Rapid Cost Decline | +0.3% | National, with manufacturing hubs in Jiangsu, Guangdong | Medium term (2-4 years) |

| National Charging-Infrastructure Build-Out | +0.2% | National, prioritizing Tier 2-3 cities | Medium term (2-4 years) |

| Provincial Subsidies | +0.1% | Regional, focused on Beijing-Tianjin-Hebei, Guangdong | Long term (≥ 4 years) |

| OEM-Run Subscription Models | +0.1% | Urban centers, Tier 1-2 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

CAAM-Led Rebound In Domestic Demand Post-2024

Vehicle sales rebounded slightly in 2024, nearly one-tenth year-over-year lift driven by coordinated financing programs, dealer incentives, and inventory normalization led by the China Association of Automobile Manufacturers. Urban consumers in Tier 1 cities absorbed most incremental volume, but policy support also stimulated replacement demand in core inland hubs. CAAM’s ability to synchronize supply with retail pull demonstrates effective quasi-government market stewardship[1]China Association of Automobile Manufacturers, “Annual Vehicle Sales Report 2024,” caam.org.cn .

Mandatory 2030 CAFE Phase-2 Standards

Phase-2 regulations compel fleetwide consumption cuts by leveraging a dual-credit mechanism where surplus NEV credits offset internal-combustion deficits. While the framework favors electrification, it permits curb-weight manipulation that can dilute real efficiency gains. Smaller automakers lacking robust NEV pipelines carry higher compliance burdens and may become takeover targets as penalties sharpen after 2027[2]Ministry of Industry and Information Technology, “Phase-2 Corporate Average Fuel Consumption Requirements,” miit.gov.cn .

Rapid Cost Decline in LFP Battery Chemistry

Lithium-iron-phosphate packs benefit from localized supply chains, intrinsic safety, and material cost advantages over nickel-rich cathodes. BYD and CATL scale economies push pack prices low enough to enable mass-market EV models below USD 15,000, widening the consumer base and eroding the price premium over internal-combustion variants[3]BYD Company Limited, “2024 Annual Results Announcement,” byd.com .

National Charging-Infrastructure Build-Out Under NEV Plan 2025

China installed 12.82 million charging points by 2024, prioritizing underserved Tier 2 and Tier 3 cities. Utilization variance remains high, but high-power DC sites along highways now shorten long-distance trip times, while 11 kW AC posts dominate residential compounds. Interoperability gaps between private-sector networks persist, prompting fresh payment and connector standards guidelines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Allocation Still Less Than 80% | -0.4% | National, affecting all OEMs and suppliers | Medium term (2-4 years) |

| Soaring Lithium Spot Prices | -0.3% | Global supply chain, domestic battery manufacturing | Short term (≤ 2 years) |

| Plateauing Tier-2/3 City Charging Density | -0.2% | Regional, concentrated in inland and smaller cities | Medium term (2-4 years) |

| Grey-Market Exports Tightening Domestic Used-Car Supply | -0.1% | National, with export concentration in Xinjiang | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Semiconductor Allocation Still Below 2019 Baseline

Automotive chip shortages cap assembly lines despite nominal demand recovery. High-margin trims get priority, pulling advanced driver-assistance functions into premium price brackets. Beijing’s push for quarter locally sourced automotive semiconductors by 2025 adds transition risk as suppliers scale unproven nodes.

Soaring Lithium Spot Prices Since 2024

In early 2025, prices for battery-grade lithium carbonate saw a notable surge, driven by increasing demand from the electric vehicle (EV) industry and supply chain constraints. This uptick in prices has led to increased pack costs, forcing OEMs to postpone essential price reductions vital for hastening the widespread adoption of EVs. Concurrently, miners in China are aggressively seeking overseas acquisitions to bolster their lithium supplies and reduce dependency on domestic sources. Yet, intensified geopolitical scrutiny, including stricter regulations and national security concerns, has extended the timelines for these acquisitions, adding to the market's volatility and uncertainty.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Segments Drive Electrification

Passenger cars remain the anchor at 47.62% of the Chinese automotive market share in 2025. Still, Light commercial vehicles are expected to post a 2.14% CAGR during the forecast period (2026-2031), due to last-mile logistics growth. Parcel-delivery vans and micro-trucks receive targeted municipal incentives and lane privileges that compress payback periods. Two-wheelers transition rapidly to electric because of low battery requirements and city licensing benefits. Off-highway machinery shows slower electrification as remote sites lack grid access, though hydrogen programs in mining trucks offer a break-even path post-2028.

Commercial fleets value high daily utilization and predictable routes, making the total cost of ownership decisive. OEMs deliver purpose-built EV chassis with swappable battery options, shrinking downtime. Freight platforms integrate telematics to orchestrate charge scheduling and route optimization, reinforcing the adoption loop. Local authorities grant green plate exemptions and parking subsidies, tilting procurement toward electric.

By Propulsion Type: ICE Dominance Faces EV Acceleration

Internal-combustion engines held 62.35% of the Chinese automotive market share in 2025, yet their lead narrowed steadily. Electric vehicles are expected to grow at a 15.34% CAGR during the forecast period (2026-2031), helped by shrinking LFP pack costs and CAFE credits. Hybrids provide a bridge solution, addressing range anxiety without complete charging dependence, especially in lower-tier cities. Fuel-cell trucks remain experimental but receive subsidies for port logistics.

Portfolio shifts differ by price band. Luxury buyers adopt EVs for performance and status, while rural consumers retain gasoline sedans until charging density improves. BYD’s global deliveries in 2024 prove that vertical integration accelerates scale and margin capture. Foreign OEMs chase compliance by importing plug-in hybrids and partnering with battery producers to manage pack sourcing risk.

By Application: Public Transport Leads Growth Acceleration

Personal use generated a 53.62% share in the Chinese Automotive Market in 2025, but public transport fleet electrification is expected to post a 2.23% CAGR during the forecast period (2026-2031). Under green-credit mandates, municipalities are procuring battery electric buses, which in turn stimulates domestic chassis suppliers and battery integrators. This initiative not only supports the local supply chain but also aligns with broader sustainability goals by reducing urban emissions. Additionally, commercial deliveries are incentivized for nighttime charging and designated loading zones, further reinforcing the economics of electric vehicles (EVs) by optimizing operational efficiency and reducing peak-hour congestion.

Industrial users are turning to electric forklifts and factory shuttle buses to reduce emissions and noise on-site. These vehicles not only contribute to a quieter and cleaner work environment but also help companies meet regulatory compliance and sustainability targets.

By Ownership Model: Subscription Services Gain Momentum

Traditional individual ownership still dominates the Chinese automotive market, with a 72.55% share in 2025, reflecting status signaling and inter-city travel habits. Subscription products are expected to grow fastest at a 2.18% CAGR during the forecast period (2026-2031), as carmakers bundle connectivity, insurance, and battery upgrades. Fleet managers leverage centralized procurement to secure bulk battery warranties, while shared mobility pilots navigate regulatory limits on vehicle density in central districts.

Urban Gen Z drivers prefer access over possession, eroding historical taboo around non-ownership. Manufacturers apply over-the-air analytics to adjust mileage tiers, unlocking recurring revenue beyond the one-off sale. Residual-value control benefits leasing captives by feeding certified-pre-owned inventory into lower-income tier markets.

By Sales Channel: Digital Transformation Accelerates

OEM dealers comprise a 56.02% share in the Chinese Automotive Market in 2025, leveraging workshop networks for after-sales retention. Direct-to-consumer storefronts on e-commerce platforms are expected to grow at a 2.22% CAGR during the forecast period (2026-2031), led by EV brands emphasizing software updates and seamless ownership apps. Independent dealers thrived in price-sensitive inland provinces where buyers favor multi-brand comparison.

Digital journeys start online, even when transactions finish offline. Virtual showrooms, live-streamed walk-arounds, and augmented-reality configurators capture early-stage attention. Negotiation transparency and faster delivery slots underpin channel loyalty as OEMs balance margin control with regional service coverage.

Geography Analysis

China’s economic rebalancing redirects demand inland. Tier 1 cities remain premium and early-EV markets but confront saturation and plate quotas that cap incremental registrations. Provinces like Sichuan added more than eight lakh charging piles in 2024, yet charger uptime and power ratings trail coastal benchmarks.

Tier 2 and Tier 3 hubs deliver fresh volume but require price parsimonious trims and extended warranty offers to align with disposable income. Consumer finance companies extend longer tenor loans, cushioning upfront EV sticker prices. Local governments align subsidy packages with industrial-park job creation goals, luring assembly plants westward for balanced growth.

Border regions become export gateways; Khorgos handled multiple used-car shipments in 2024, tightening domestic secondhand supply and propping residual values. Western corridors attract battery recycling ventures that capitalize on cross-border feedstock, supporting circular-economy goals.

Competitive Landscape

Domestic brands held over three-fifths of the share in 2024, with market concentration intensifying as scale advantages compound battery cost leadership. BYD’s sales crown it EV leader, while SAIC leverages joint ventures to preserve ICE relevance among legacy buyers. Foreign players respond with alliances; Volkswagen deepened its platform pact with XPENG to cut parts costs and speed Chinese-specific BEV rollouts.

Scale economics reward vertical integration from cathode refining to pack assembly. CATL supplies external customers and its scooter subsidiary, smoothing capacity utilization. Traditional OEMs facing margin erosion explore mergers; Honda and Nissan discussed consolidation after sales drops in November 2024, signaling urgency to regain lost ground.

Technology firms encroach on adjacent sectors. Huawei supplies in-car operating systems and lidar, pairing with Changan to launch the Luxeed S7 sedan. Semiconductor houses expand 28-nm automotive lines to counter chip shortages. Niche players chase hydrogen truck pilots, banking on policy push and rising diesel costs to seed demand.

Chinese Automotive Industry Leaders

SAIC Motor

BYD Co., Ltd.

FAW Group

Dongfeng Motor

Geely Holding

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Dongfeng Motor entered merger talks with Changan Automobile to pool R&D spend and platform assets.

- March 2025: FAW Group and Leapmotor signed a strategic cooperation pact covering battery integration and joint manufacturing.

- February 2024: XPENG and Volkswagen extended their software collaboration, launching a joint sourcing program to trim BEV component costs.

Chinese Automotive Market Report Scope

| Two-Wheeler |

| Three-Wheeler |

| Passenger Cars |

| Commercial Vehicles |

| Off-Highway Vehicles |

| Internal Combustion Engine |

| Hybrid Vehicle |

| Electric Vehicle |

| Personal |

| Commercial |

| Public Transport |

| Industrial Use |

| Individual Ownership |

| Fleet Ownership |

| Subscription-Based |

| Shared Mobility |

| OEM Dealers |

| Independent Dealers |

| Online Platforms |

| Direct-to-Consumer |

| By Vehicle Type | Two-Wheeler |

| Three-Wheeler | |

| Passenger Cars | |

| Commercial Vehicles | |

| Off-Highway Vehicles | |

| By Propulsion Type | Internal Combustion Engine |

| Hybrid Vehicle | |

| Electric Vehicle | |

| By Application | Personal |

| Commercial | |

| Public Transport | |

| Industrial Use | |

| By Ownership Model | Individual Ownership |

| Fleet Ownership | |

| Subscription-Based | |

| Shared Mobility | |

| By Sales Channel | OEM Dealers |

| Independent Dealers | |

| Online Platforms | |

| Direct-to-Consumer |

Key Questions Answered in the Report

What is the current value of the Chinese automotive market?

The market is valued at USD 674.06 billion in 2026.

How fast is the Chinese automotive market expected to grow?

It is projected to expand at a 2.11% CAGR, reaching USD 748.24 billion by 2031.

Which vehicle segment is growing quickest in China?

Light commercial vehicles lead with a 2.14% CAGR through 2031.

What portion of Chinese vehicle sales were NEVs in 2024?

New Energy Vehicles made up 40.9% of total sales.

Who leads the domestic electric-vehicle race?

BYD shipped 4.27 million vehicles worldwide in 2024, outpacing all rivals.

Why are subscription models gaining share?

Bundled insurance, maintenance, and flexible terms attract younger urban drivers, driving a 2.18% CAGR in the segment.

Page last updated on: