Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 125.32 Billion |

| Market Size (2026) | USD 131.44 Billion |

| Market Size (2031) | USD 166.86 Billion |

| Growth Rate (2026 - 2031) | 4.88% CAGR |

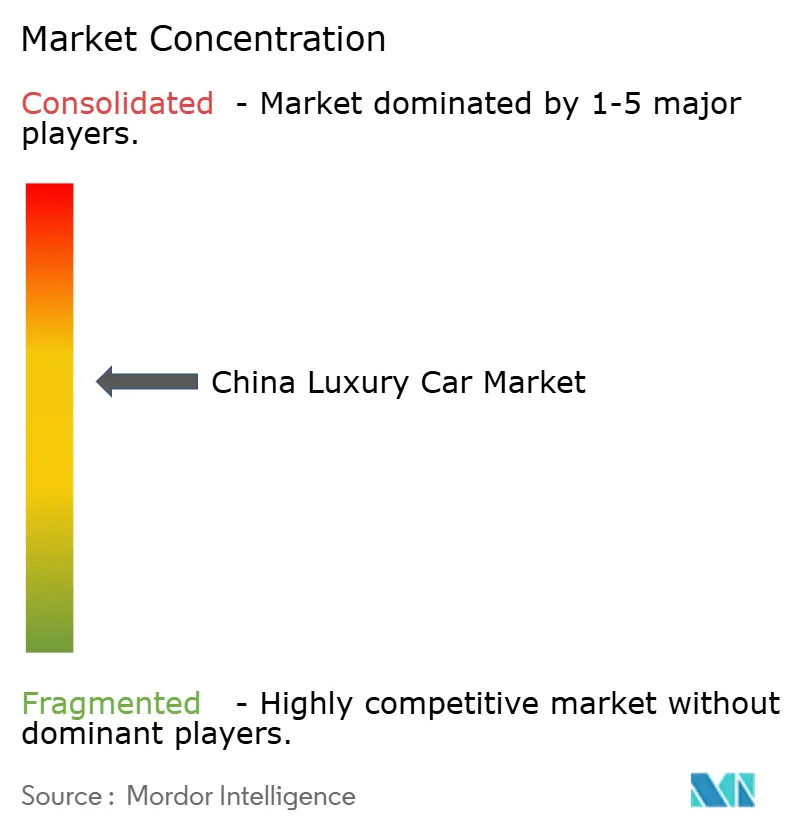

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Luxury Car Market Analysis by Mordor Intelligence

The China luxury car market size is expected to grow from USD 125.32 billion in 2025 to USD 131.44 billion in 2026 and is forecast to reach USD 166.86 billion by 2031 at 4.88% CAGR over 2026-2031. This expansion is underpinned by accelerating electrification, rising disposable income in lower-tier cities, and policy support that favors new-energy vehicles. Demand momentum also stems from consumers who now view premium vehicles as mobile technology platforms, prompting manufacturers to elevate autonomous-driving capabilities and connected-services ecosystems. Competitive intensity has sharpened as domestic electric-luxury brands close traditional technology gaps, while foreign marques localize platforms to safeguard their positions within the China premium car market. Ongoing semiconductor localization and evolving tax regulations will continue to reshape margins, supply-chain strategies, and product-mix decisions across the value chain.

Key Report Takeaways

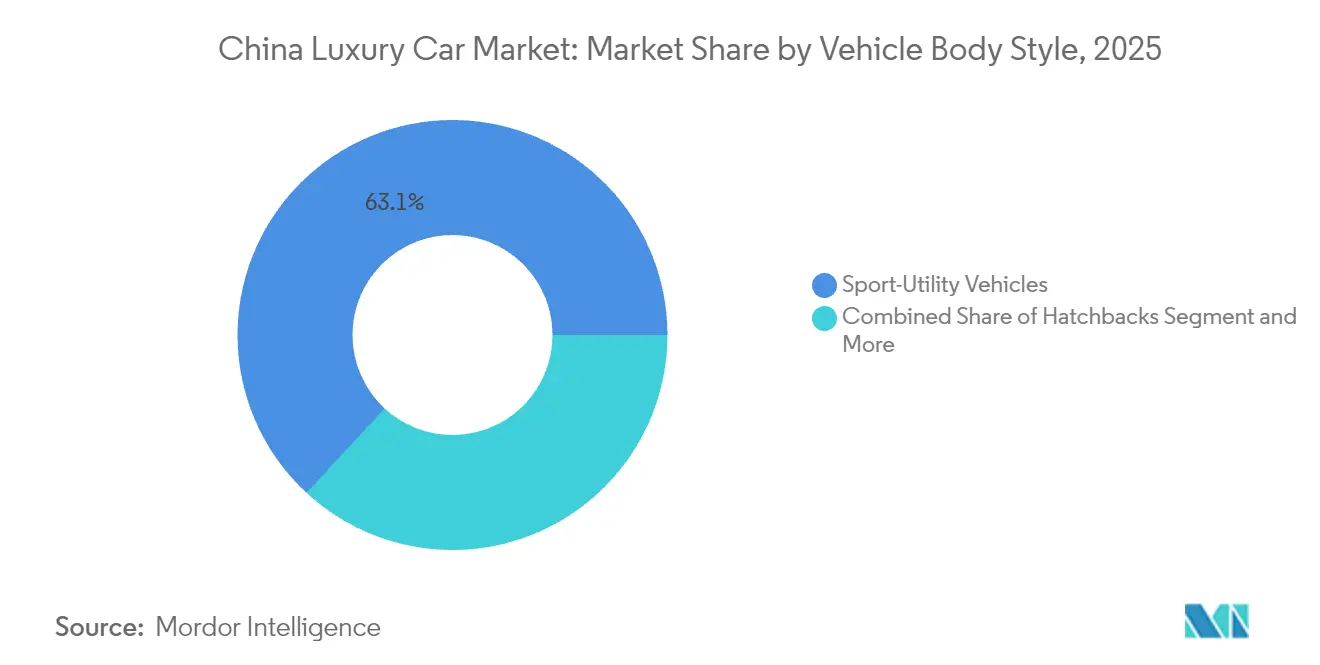

- By vehicle body style, SUVs controlled 63.12% of the Chinese luxury car market share in 2025 and are projected to post a 6.25% CAGR through 2031.

- By powertrain, internal combustion models retained 61.95% of the China luxury car market size in 2025, but battery-electric vehicles will advance at a 9.72% CAGR to 2031.

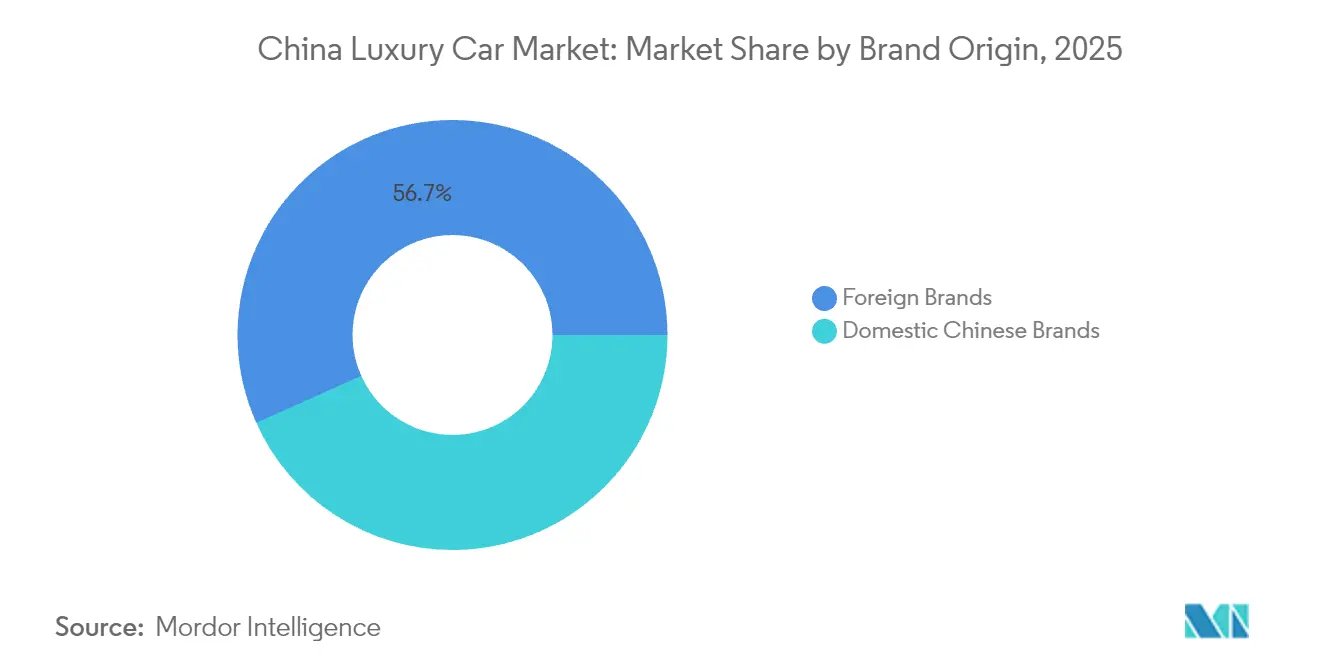

- By brand origin, foreign marques held 56.70% of the China luxury car market in 2025, whereas domestic brands are forecast to expand at an 11.12% CAGR through 2031.

- By sales channel, authorized dealerships accounted for 72.05% of the China luxury car market in 2025, while online direct-to-consumer platforms are growing at a 7.88% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Luxury Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Wealth in Tier-2 And Tier-3 Cities | +1.2% | Chengdu, Wuhan, Xi'an, Hangzhou | Medium term (2-4 years) |

| Growth of Domestic EV-Luxury Brands | +0.9% | Nationwide, export spillover | Medium term (2-4 years) |

| NEV Incentives Targeting Premium Cars | +0.8% | Beijing, Shanghai, Shenzhen | Short term (≤ 2 years) |

| Rising Demand for Brand Status | +0.6% | Tier-1 and tier-2 cities | Long term (≥ 4 years) |

| L3 Autonomy Lifting ASP | +0.4% | Shanghai, Beijing, Guangzhou | Medium term (2-4 years) |

| NFT-Based Digital Ownership Perks | +0.1% | Tech-forward tier-1 hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Wealth in Tier-2 and Tier-3 Cities

Household incomes in secondary urban centers are growing annually, outpacing tier-1 growth and spawning a new cohort of premium buyers who view vehicles as status symbols and technology showcases. Domestic brands such as Li Auto delivered 500,508 units in 2024, illustrating how aspirational families embrace large premium SUVs equipped with ADAS. Trade-in subsidies worth up to RMB 20,000 (~USD 2,800 ) have amplified purchasing power, allowing middle-class households to enter the China premium car market[1]“2024 Premium BEV Market Share Announcement,”, NIO Inc., nio.com.

Expansion of Domestic EV-Luxury Brands

Domestic champions have combined battery-swapping networks, Level 2+ autonomy, and over-the-air upgrades to capture demand. NIO delivered 221,970 vehicles in 2024, and Li Auto reached half a million annual deliveries within five years of launch. Such growth reshapes the China premium car market by shifting the basis of competition from combustion-engine heritage to software ecosystems and service models [2]“December 2024 Delivery Update,”, Li Auto Inc., lixiang.com.

L3 Autonomy Features Driving Higher ASP

As cities begin to approve pilot programs, automakers are increasingly integrating advanced Level 3 driver assistance systems into high-end vehicle trims. This trend not only elevates overall transaction values but also underscores a collective industry shift. GAC's nationwide rollout plans for later this year further emphasize the industry's consensus: higher automation levels are becoming a hallmark of next-generation premium vehicles.

NFT-Based Digital Ownership Perks

Luxury OEMs are embedding NFT galleries and blockchain ownership certificates into their infotainment suites, presenting digital collectibles that underscore exclusivity. These features not only enhance the premium experience but also cater to the growing demand for digital assets among high-net-worth individuals. Initial trials in Shanghai and Shenzhen hint at budding revenue streams linked to in-car digital commerce, showcasing the potential for integrating blockchain technology into the automotive sector.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Luxury-Tax Burden on Mid-Tier Premiums | -0.7% | Beijing, Shanghai, Guangzhou | Short term (≤ 2 years) |

| High-End Semiconductor Shortages | -0.5% | Nationwide | Short term (≤ 2 years) |

| Data-Security Regulation on Connected Cars | -0.3% | Nationwide | Medium term (2-4 years) |

| Premium Ride-Hailing Options | -0.2% | Beijing, Shanghai, Shenzhen, Guangzhou | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Security Regulation on Connected Vehicles

China’s Data Security Law compels automakers to store vehicle-generated data domestically, inflating costs for foreign OEMs that must duplicate global cloud architectures. Limitations on cross-border data flows complicate over-the-air update pipelines, diminishing feature parity with global platforms and restraining differentiation in the China premium car market[3]“Automakers Face Costly Data Localization Hurdles in China,”, Nikkei Asia, asia.nikkei.com.

Premium Ride-Hailing Curbing Ownership Intent

Affluent urban residents increasingly rely on premium ride-hailing fleets, eroding incremental ownership demand in tier-1 cities. While this service substitutes some individual purchases, it simultaneously expands fleet sales opportunities for luxury OEMs pivoting toward mobility-service partnerships.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Body Style: SUVs Anchor Premium Electrification

SUVs captured 63.12% of the Chinese premium car market 2025, underscoring consumer preference for commanding driving positions and family-oriented interiors. The SUV sub-segment will expand at a 6.25% CAGR through 2031 as battery-electric flagships like the NIO ES6 and Li Auto L9 dominate showroom traffic. Sedans maintain gravitas in executive transport, but incremental volume shifts to versatile multi-purpose vehicles designed for multi-generational households. GAC’s forthcoming Level 3 rollout and Li MEGA’s flexible seating highlight how automation and interior versatility set new luxury benchmarks.

The second-order effects include a stronger demand for long-wheelbase chassis and adaptive air-suspension packages that enhance ride comfort on variable road quality in lower-tier cities. Hatchbacks remain niche yet benefit from tight urban parking constraints, particularly in coastal megacities where congestion is severe. SUV leadership also advances battery-swapping adoption because larger underbodies accommodate standardized modules, reinforcing infrastructure network effects unique to the Chinese premium car market.

By Powertrain Type: Electric Momentum Outpaces Combustion

Internal-combustion vehicles still represented 61.95% of the 2025 volume, translating to the most significant current slice of the China premium car market size. Yet battery-electric models will climb at a 9.72% CAGR through 2031, propelled by purchase-tax exemptions, falling battery costs, and growing charger density nationwide. Plug-in hybrids serve as range-anxiety hedges, bridging coastal infrastructure gaps. Fuel-cell pilots remain experimental owing to hydrogen logistics, limiting near-term influence.

Battery-electric leadership amplifies software-centric value propositions—advanced driver-assistance, immersive infotainment, and continuous over-the-air updates—that combustion rivals cannot match. Domestic OEMs leverage vertically integrated power-electronics supply chains to reduce bill-of-materials and comply with chip-localization directives. Consequently, the China premium car market share for electric nameplates in the RMB 300,000-600,000 bracket is projected to exceed 55% by 2031, displacing turbocharged six-cylinder sedans historically favored by status-conscious executives.

By Brand Origin: Domestic Brands Narrow the Gap

Foreign marques retained 56.70% volume in 2025, but domestic brands are growing more than double the overall China premium car market CAGR at 11.12%, thanks to localized engineering and rapid software iteration. NIO and Li Auto exemplify the shift by pairing proprietary autonomous stacks with lifestyle-oriented after-sales programs. Mercedes-Benz’s USD 2 billion investment in China-specific MMA and VAN.EA platforms reflect how global players localize chassis, wheelbase, and power-train specs to defend market share.

Domestic entrants differentiate via user-community engagement, battery-swap subscriptions, and unified digital-service pricing, creating annuity-like revenue. Their ascent also alters supplier dynamics, rewarding local chip designers and tier-1 electronics firms aligned with national tech sovereignty goals. The Chinese premium car market will likely see foreign-domestic joint innovations such as Volkswagen’s XPeng collaboration, which merges legacy manufacturing scale with native EV software competencies.

By Sales Channel: Digital Direct Sales Advance

Authorized dealerships still manage 72.05% of transactional volume, yet direct-to-consumer online channels are expanding at 7.88% CAGR as affluent buyers seek price transparency and frictionless experiences. Tesla’s showroom-plus-app blueprint spurred NIO and Li Auto to roll out 500+ urban “houses” that blend café lounges, VR configurators, and after-sales desks under one roof.

Online platforms compress negotiation cycles and boost accessory-attachment rates through data-driven upselling. Dealers are adapting by shifting from transactional revenue to subscription service plans and certified pre-owned programs that sustain footfall. Over time, omnichannel models that synchronize in-app order placement with at-home delivery will unlock incremental margin for OEMs, reinforcing the strategic pivot toward direct relationships inside the China premium car market.

Geography Analysis

Major urban centers, including Beijing, Shanghai, Guangzhou, and Shenzhen, are witnessing a concentrated demand for premium vehicles. These cities boast well-developed charging infrastructures, favorable licensing policies, and a tech-savvy consumer base, bolstering early adoption. Furthermore, they act as testing grounds for cutting-edge technologies, such as Level 3 autonomy and ultra-fast charging. This environment offers manufacturers a prime opportunity to hone their connected services and business models before venturing into wider markets.

Manufacturers expanding the dealer-owned showroom model in these hubs benefit from lower real-estate costs and rising brand visibility. The China premium car market size contribution from these four first-tier hubs (Beijing, Shanghai, Guangzhou, Shenzhen) is projected to double by 2031 as infrastructure investment closes the gap with coastal regions.

Tier-3 locales represent the new frontier. Government “vehicles-to-the-countryside” campaigns pair rural charging grants with incremental trade-in bonuses, nudging early adopters toward compact luxury SUVs. NIO’s “Power Up Counties” program adds battery-swap stations to smaller prefectures, neutralizing range anxiety and enabling domestic brands to pre-empt foreign rivals that rely on city-center retail. As income convergence spreads, regional diversity in consumer taste will require flexible product portfolios that accommodate both chauffeur-driven sedans and family-oriented MPVs.

Regulatory Landscape

China's luxury car market operates under a tightening mix of NEV, connected-vehicle, taxation, and competition-compliance rules that affect product mix and pricing. On July 20, 2025, the consumption tax scope for ultra-luxury vehicles shifted to a lower threshold of RMB 900,000 per vehicle (excluding VAT), increasing tax exposure for high-trim imports and domestic flagships and shaping configuration and MSRP decisions.

Electrification compliance is also guided by MIIT-led dual-credit management, with NEV credit proportion targets set at 48% for 2026 and 58% for 2027. Eligibility conditions for 2026-2027 vehicle purchase tax exemptions for NEVs reference GB 36980.1-2025-related technical requirements, while smart connected vehicle entry requirements require submissions of technical parameters on driver assistance and OTA capabilities, adding ongoing compliance workload for premium brands that differentiate through software.

Value Chain Analysis

The value chain in China's luxury car market covers upstream batteries, semiconductors, and smart-cockpit and ADAS components, followed by vehicle design and localized engineering. Manufacturing is carried out via wholly owned plants and joint ventures, with distribution split across authorized dealerships, company-owned stores, and online direct-to-consumer channels. The largest operational changes are tied to deeper localization of intelligent components (batteries, smart cockpits, ADAS) and faster China-specific R&D decision-making, as foreign brands work with local partners to shorten software iteration cycles.

Downstream, aftersales and ecosystem services (including OTA updates, subscriptions, charging and battery-swap services, and certified pre-owned programs) are gaining importance for value capture as transaction margins face pressure. Industry programs also support circulation and retail modernization across the chain, including a 2025-2026 stabilization and growth work plan issued jointly by multiple departments and MOFCOM-linked efforts that designated 40 pilot cities for auto circulation reforms by June 2026, which is aimed at supporting retail transformation and secondary-market development.

Competitive Landscape

Competition sits at a moderate concentration level as no single player controls an overwhelming share, yet rivalry is intense. Mercedes-Benz, BMW, and Audi still command the legacy internal-combustion space, but NIO, Li Auto, XPeng, and Huawei-backed AITO carve out leadership in the premium BEV arena. Volkswagen’s 4.99% stake in XPeng and co-developed E-class sedan illustrate how global groups now invest locally to stay relevant.

The strategic playbook splits: Legacy luxury OEMs leverage brand heritage, robust dealer networks, and access to global R&D budgets, whereas domestic disruptors bet on software roadmaps, ecosystem services, and asset-light digital retail. Semiconductor localization mandates favor China-rooted manufacturers already partnered with domestic chipmakers, raising entry barriers for imports that must redesign electronic architectures to comply with data-security rules.

Margins remain under pressure as price-based promotions intensify; however, subscription software services, in-house self-driving chips, and premium maintenance plans offer new profit pools. Success increasingly hinges on mastery of full-stack technology, from silicon to cloud, rather than traditional drivetrain engineering, redefining what scale and capability mean inside the China premium car market.

China Luxury Car Industry Leaders

Lexus (Toyota Motor Corporation)

Daimler AG (Mercedes-Benz)

Volkswagen Group (Audi AG)

BMW AG

Tesla Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy and compliance changes are creating openings for premium OEMs that can adapt product positioning, pricing governance, and NEV qualification quickly. The July 2025 change to apply the ultra-luxury vehicle consumption tax from a RMB 900,000 (excluding VAT) threshold raises sensitivity to trim strategy and option bundling. At the same time, SAMR's pricing-behavior compliance push (draft guidance in December 2025 and a formal compliance guide issued in February 2026) increases the need for disciplined pricing processes, dealer policy coordination, and transparent list pricing. BMW China's January 2026 official retail price adjustments across 31 models reflects this shift, signaling reduced reliance on terminal discounting.

Technology localization remains the most actionable opportunity in the premium segment, especially for China-tailored intelligent connected vehicles and ADAS-led differentiation. Audi and SAIC's April 2026 strategic cooperation to establish the AUDI Innovation and Technology Center in Shanghai provides a concrete route for localized ICV development, while large-scale manufacturing upgrades continue to be funded for NEV platforms, including Stellantis and Dongfeng's May 2026 announcement of a combined investment of over RMB 8 billion to expand DPCA in Wuhan for new Peugeot and Jeep energy vehicles. Together, these actions point to where suppliers, software partners, and localized engineering capabilities can translate into share gains across premium electrification and connected-services stacks.

Recent Industry Developments

- May 2026: Stellantis and Dongfeng announced a combined investment of over RMB 8 billion to expand their DPCA joint venture in Wuhan for production of new Peugeot and Jeep energy vehicles. The plan supports retooling toward NEV programs and adds competitive pressure in higher-trim segments where international groups are seeking localized cost and feature parity.

- February 2025: Toyota Motor Corporation established a new wholly owned company in Shanghai's Jinshan District to develop and produce battery electric vehicles and batteries, with production scheduled to start in 2027 and initial annual capacity of around 100,000 units. The move strengthens local supply-chain control and provides a platform for Lexus and Toyota to accelerate premium BEV localization in China.

- September 2024: Mercedes-Benz announced plans to jointly invest over RMB 14 billion with local partners in China to develop new platforms and China-specific models, including electric long-wheelbase variants. The investment highlights the ongoing localization race among legacy luxury brands as domestic premium EV competitors raise expectations on software, connectivity, and cabin technology.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers luxury passenger cars sold in China, measured as the value generated from new-vehicle sales across the luxury price and feature band, where higher comfort, performance, equipment, and brand positioning are present.

Scope exclusions: Used-car resales, parts and service revenue, insurance, and financing activity are excluded from the market value unless directly bundled into the new-vehicle transaction.

Segmentation Overview

- By Vehicle Body Style

- Hatchbacks

- Sedans

- Sport-Utility Vehicles (SUVs)

- Multi-purpose Vehicles (MPVs)

- By Powertrain Type

- Internal-Combustion (ICE) Vehicles

- Electric Vehicles (BEV, PHEV, HEV, FCEV)

- By Brand Origin

- Domestic Chinese Brands

- Foreign Brands

- By Sales Channel

- Authorized Dealerships

- Company-Owned Stores

- Online Direct-to-Consumer

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to establish the starting points for volumes, pricing context, and policy signals that shape luxury demand in China. We referenced public sources such as releases from the China Association of Automobile Manufacturers, notices from the Ministry of Industry and Information Technology, China Customs trade statistics, National Bureau of Statistics macro series, and selected peer-reviewed automotive and battery papers.

On the company side, filings, investor presentations, official brand pressrooms, and dealership network announcements were reviewed to understand model cycles, powertrain mix shifts, and channel strategy changes. Where required, we also used paid subscriptions focused on company financials and intelligence, patent databases, and vehicle sales and parc datasets to cross-check model lineups and adoption timing. These desk sources are illustrative only, and additional public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was carried out via expert interviews and structured surveys with automakers and importers, dealer groups, fleet and leasing stakeholders, and supporting ecosystem participants such as charging and component specialists. Since this is a China-only market, respondent coverage was spread across key demand hubs and fast-growing lower-tier city clusters, then used to test assumptions on luxury price bands, discounting behavior, and EV share progression.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | |

| Mid tier: 54% | Functional/Unit leaders: 34% | |

| Smaller Players: 14% | Managers: 54% |

Market-Sizing & Forecasting

Sizing started from a top-down rebuild of the China new passenger vehicle demand pool. Public sales series and trade signals were filtered into a luxury-only subset using price band and model positioning checks. Those totals were then corroborated using selective bottom-up approximations, including sampled model sales by body style and powertrain multiplied by observed transaction price ranges, followed by dealer channel checks to adjust for discounting and mix.

Key inputs used in the model included luxury passenger vehicle sales volumes, the share of SUVs versus sedans, the EV and hybrid mix within luxury, average selling price movement by powertrain and trim, the pace of new model launches and refresh cycles, and policy items that shift purchase intent (such as new-energy incentives and registration constraints in large cities). When data gaps appeared for smaller brands or newer nameplates, we applied conservative proxies based on comparable launches and dealer footprint growth, and those assumptions were revisited during expert calls.

For forecasting, scenario analysis was applied around electrification speed, premium consumer sentiment, and pricing normalization, and then the most likely path was selected after it matched feedback from interviews. Output growth rates were also tested against macro indicators and luxury penetration expectations so the final time series remains realistic year over year.

Data Validation & Update Cycle

Validation is handled through triangulation across independent signals, followed by repeated variance checks before results are signed off. We compare model outputs against vehicle sales and mix indicators, import trends where relevant, announced capacity and localization milestones, and channel-level commentary on pricing and inventory. Any outliers are reworked until both the math and the market story align.

A multi-step analyst review is used to check assumptions, unit conversions, and currency treatment, and re-contact is triggered when pricing or powertrain mix differs from expected ranges. Reports are refreshed annually, and interim updates are made when material events occur, such as sudden policy shifts or major product cycle changes. Before delivery, the model is rerun with the latest available inputs so clients receive an updated view rather than an older snapshot.

Mordor Intelligence's China Luxury Car Market Size Compared Against Other Published Estimates

Published market values for China luxury cars can differ substantially because the term luxury is applied differently across sources, and because some estimates mix new-car sales value with broader auto spending. Timing also matters, since the same market can be reported in different base years with different currency conversion dates.

The largest gaps typically come from scope choices, such as including entry-level premium models, counting used-car transactions, or folding in financing and aftersales revenue, which can lift the headline value quickly. Another driver is pricing logic, where some estimates use list prices or assume strong ASP growth, while others use transaction pricing and adjust for discount cycles and the faster EV mix shift. This is the approach used to keep the 2025 value anchored to new-vehicle demand signals in this study by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 125.32 B (2025) | |

| Global Consultancy A | USD 195.00 B (2024) | Uses a broader luxury definition that spans price bands from entry-level to ultra-high-end, and can implicitly blend list-price style ASP assumptions across fuel types. This makes the value less comparable to a new-vehicle transaction-price approach. |

| Industry Commentary B | USD 195.00 B (2024) | Often presented as a headline figure without a clear separation between luxury new-car value and adjacent market activity. The refresh timing can also lag major discounting or mix changes that move luxury ASPs. |

The spread in the table is mainly explained by what gets counted as luxury and how pricing is treated in the base year. When the scope is limited to new luxury vehicle sales value and the assumptions are checked with dealer and mix signals, the resulting number is easier to trace back to repeatable steps and practical market indicators that can be revalidated in future updates.

Key Questions Answered in the Report

How large is the China premium car market in 2026?

The market is valued at USD 131.44 billion in 2026, with a projected USD 166.86 billion by 2031.

What is the expected growth rate for premium battery-electric vehicles?

Battery-electric models are forecast to register a 9.72% CAGR between 2026 and 2031.

Which vehicle body style leads sales?

SUVs dominate with 63.12% share in 2025 and remain the fastest-growing body style.

How are domestic brands performing against foreign marques?

Domestic players are expanding at an 11.12% CAGR, rapidly narrowing the historical gap with foreign brands.

How will semiconductor localization affect manufacturers?

OEMs must redesign electronic architectures to reach 100% domestic chip content by 2026, influencing sourcing strategies and technology roadmaps.

Page last updated on: