China Yacht Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

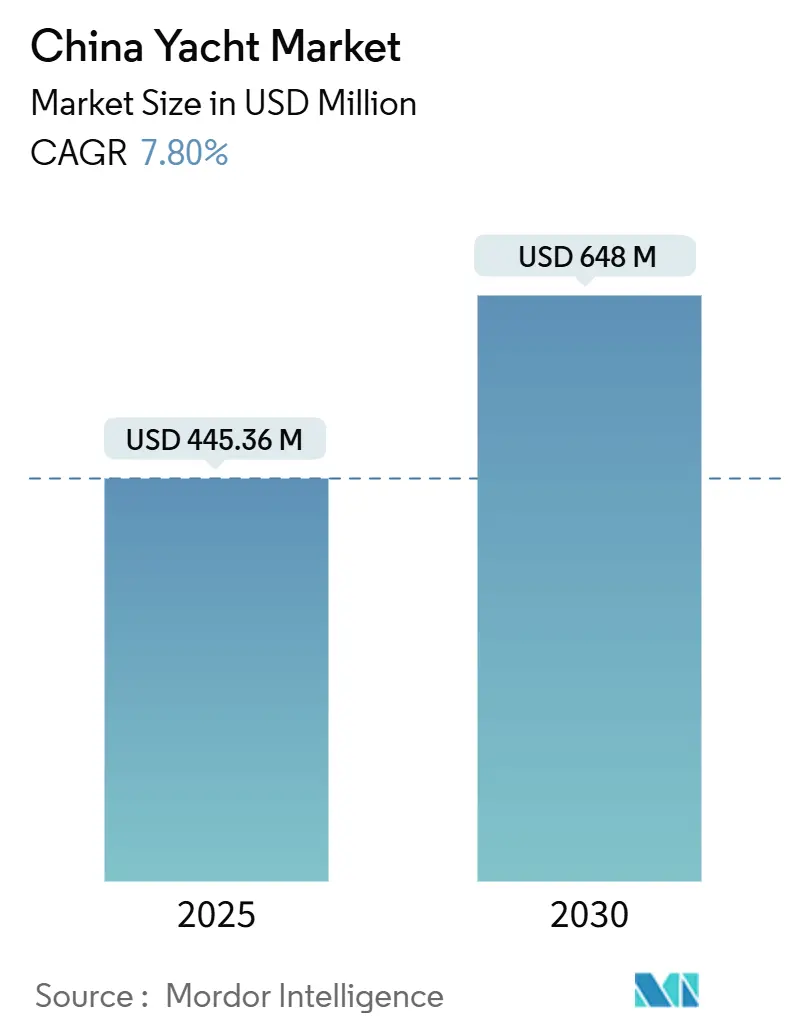

| Market Size (2025) | USD 445.36 Million |

| Market Size (2030) | USD 648 Million |

| Growth Rate (2025 - 2030) | 7.80% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Yacht Market Analysis by Mordor Intelligence

The Chinese yacht market is valued at USD 445.36 million in 2025 and is forecast to reach USD 648 million by 2030, reflecting a 7.8% CAGR across the period and underscoring the country’s steady transition from an import-reliant destination to an integrated consumption-and-production hub. Three intertwined trends power demand growth: expanding high-net-worth wealth pools, policy liberalization led by the Hainan Free Trade Port, and the rapid upgrading of domestic boat-building capabilities. Wealth holders are pivoting from property and collectibles toward experiential leisure assets, pushing upgraders toward larger, longer-range vessels. On the supply side, shipyards in the Pearl River Delta are deploying automotive-style automation and composite fabrication to shorten build cycles and match European finish quality. Commercial charter operations, amplified by Hainan’s tourism targets, offer owners income streams that offset running costs, while electrification partnerships between Chinese battery leaders and Western yacht brands open a new technology race in propulsion. Regulatory bottlenecks outside Hainan—chiefly luxury taxes and scarce berths in Tier-1 marinas—still temper nationwide penetration, but investors view them as addressable frictions rather than structural caps.

Key Report Takeaways

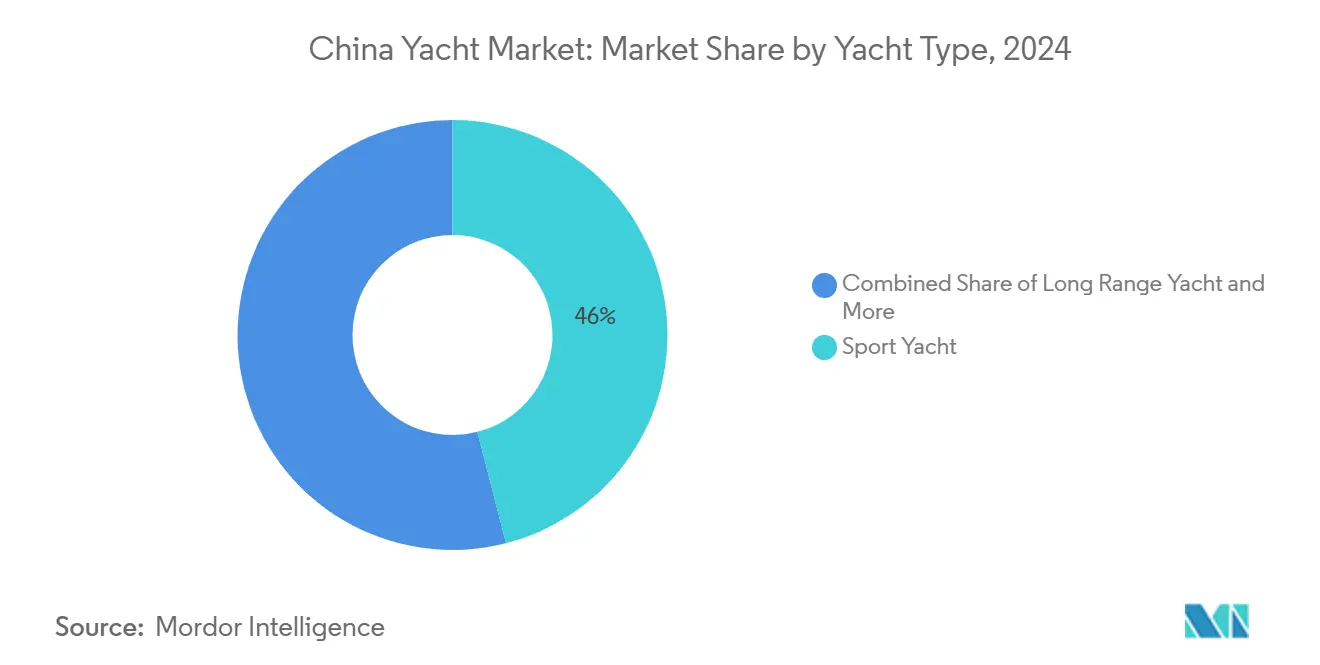

- By yacht type, sport yachts led the China yacht market with 46.01% of share in 2024, whereas long-range yachts are projected to expand at an 11.53% CAGR through 2030.

- By length, the 20 to 40 meter segment accounted for 41.52% of China's yacht market size in 2024, while vessels above 40 meters are advancing at a 12.34% CAGR to 2030.

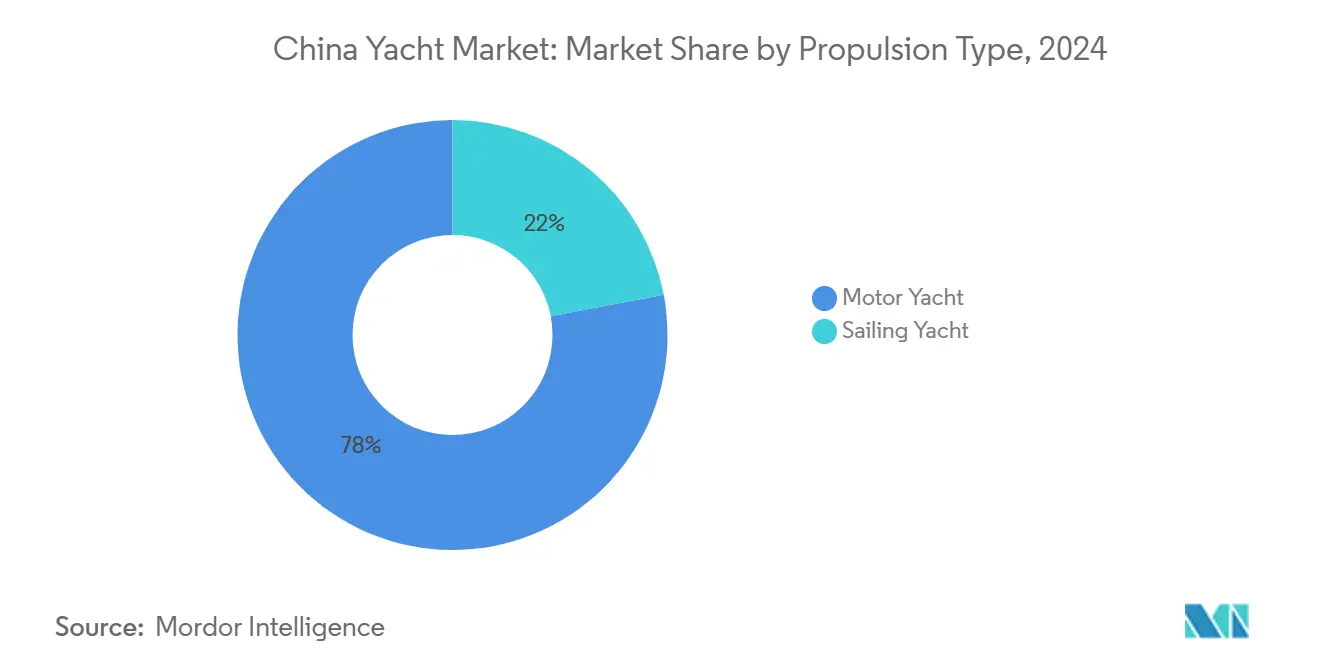

- By propulsion, motor yachts commanded 78.03% share of the China yacht market size in 2024, and electric or hybrid models are growing at an 18.41% CAGR through 2030.

- By application, private ownership held 82.04% of the Chinese yacht market share in 2024, and commercial charter usage is increasing at a 15.21% CAGR over 2025-2030.

China Yacht Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Population of High-Net-Worth Individuals (HNWIs) | +2.1% | National, Concentrated in Tier-1 Cities | Long Term (≥ 4 Years) |

| Hainan Free Trade Port Tariff and Tax Exemptions | +1.8% | Hainan Province, Spillover to Guangdong | Medium Term (2-4 Years) |

| Expansion of Domestic Marina Infrastructure | +1.5% | Coastal Regions, Sanya, Shanghai, Qingdao | Medium Term (2-4 Years) |

| Upgrading Quality and Capacity of Chinese Yacht Builders | +1.2% | National, Concentrated in Pearl River Delta | Long Term (≥ 4 Years) |

| Adoption of Electric/Hybrid Propulsion Under New Emission Norms | +0.9% | National, Early Adoption in Hainan | Short Term (≤ 2 Years) |

| Digital Marinas and Fractional-Ownership Platforms | +0.3% | Tier-1 Cities, Expanding to Tier-2 | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Rising Population of High-Net-Worth Individuals (HNWIs)

China's HNWI expansion creates a demographic foundation that extends beyond traditional wealth metrics into experiential luxury consumption patterns. The concentration of real estate businessmen among yacht owners in established markets like Qingdao, where approximately 60% of the 300+ yacht owners have been local property developers, demonstrates how sector-specific wealth accumulation drives marine luxury adoption[1]Wang Chow, "Owning a boat in China - an unusually candid view," Sail World, sail-world.com. . This wealth concentration effect amplifies during economic transitions, as asset diversification strategies increasingly include luxury collectibles and experiential assets. The target buyer profile typically requires assets exceeding RMB 10 million, with annual berth fees ranging from RMB 130,000 to RMB 170,000 for standard positions, creating natural market segmentation that aligns with China's wealth distribution patterns. Status competition dynamics drive upgrade cycles, with owners progressively acquiring larger vessels to maintain social positioning within business networks. The seasonal migration pattern, where northern yacht owners relocate to Sanya during the winter months, indicates sophisticated usage patterns that support charter market development and marina utilization optimization.

Hainan Free Trade Port Tariff and Tax Exemptions

Hainan's designation as China's largest island-wide free trade port has generated policy momentum that transcends simple duty elimination. The province achieved 63.3% annual average growth in paid-in foreign investments over five years, with capital flows through free trade accounts exceeding USD 35 billion in 2022[2]"Hainan, exploring the Hawaii of China," ARMENPRESS, armenpress.am.. The zero-tariff framework, combined with simplified tax systems and 15% preferential corporate income tax for encouraged industries, creates structural cost advantages that extend to yacht importation, servicing, and charter operations. The expanded duty-free quota to RMB 100,000 annually, alongside broadened product categories and new pickup models, has driven duty-free sales to RMB 43.76 billion in 2023, indicating consumer responsiveness to tax-advantaged luxury consumption. The planned "island-wide special customs operations" and potential RMB free-convertibility status would eliminate currency friction for international yacht transactions and charter bookings. This policy architecture positions Hainan as Asia's yacht services hub, competing directly with Singapore and Hong Kong for high-net-worth marine tourism flows.

Expansion of Domestic Marina Infrastructure

China's marina development strategy reflects broader coastal urbanization priorities that integrate luxury marine facilities with tourism and real estate development. The Sanya International Yachting Centre, with more than 200 berths, serves as a model for integrated marina-resort complexes that combine yacht services with luxury hospitality and retail. Qingdao's Olympic Marina infrastructure, housing over 300 yachts with sophisticated security protocols, demonstrates the scalability of premium marina operations in Tier-1 coastal markets. The Qingdao Wanda Oriental Film Capital Yacht Harbour, completed in 2018 with 230 yacht berths and RMB tens of billions of investment, showcases private sector commitment to large-scale marina development integrated with entertainment and tourism assets[3]Isabelle Lomholt, "Qingdao Yacht Club and Marina, China," e-architect, e-architect.com.. Marina engineering companies like Guangzhou Stark Yacht Marina Engineering are developing modular floating dock systems and breakwater technologies that enable rapid capacity expansion across multiple coastal locations. The integration of marina development with broader port modernization initiatives, including deep-water channel projects and IT system upgrades, creates synergies that reduce infrastructure costs and improve operational efficiency.

Upgrading Quality and Capacity of Chinese Yacht Builders

Chinese yacht manufacturing capabilities have evolved from contract manufacturing toward design integration and brand development, supported by the broader shipbuilding sector's technological advancement. China's shipbuilding industry achieved historic profit margins of 9.71% in the first half of 2025, with operating revenues reaching RMB 398.76 billion and exports accounting for 89.5-93.2% of completions by tonnage. Selene Yachts' Zhuhai facility exemplifies this evolution, with a 150,000 square foot production complex equipped with four 100-ton cranes and described as Asia's largest single yacht production facility, capable of accommodating 36 molds simultaneously. The facility's integration of woodworking, stainless steel fabrication, and composite construction under one roof demonstrates vertical integration capabilities that rival European yacht builders. Weichai Holding Group's strategic reorganization of Ferretti Group provides Chinese industrial conglomerates with direct access to luxury yacht design and manufacturing expertise, creating knowledge transfer opportunities that accelerate domestic capability development. The government's monitoring of shipbuilding capacity to prevent oversupply indicates policy awareness of the need to balance production expansion with market demand, suggesting coordinated industry development rather than unconstrained capacity addition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Luxury Taxes and High Import Duties Outside Hainan | -1.4% | National Excluding Hainan Province | Medium Term (2-4 Years) |

| Scarcity of Marina Berths in Tier-1 Coastal Cities | -0.8% | Shanghai, Shenzhen, Qingdao, Dalian | Long Term (≥ 4 Years) |

| Complex Licensing and High Operating Costs | -0.6% | National, Acute in High-Compliance Regions | Medium Term (2-4 Years) |

| Anti-Corruption Scrutiny on Conspicuous Consumption | -0.5% | National, Especially Tier-1 Business Hubs | Short Term (≤ 2 Years) |

| Source: Mordor Intelligence | |||

Luxury Taxes and High Import Duties Outside Hainan

The tax differential between Hainan and mainland China creates market distortions that concentrate yacht ownership and charter activity within the free trade port while constraining broader national market development. Import duties on luxury goods outside Hainan can exceed 30% when combined with value-added taxes and consumption taxes, creating price premiums that limit market accessibility for mid-tier luxury consumers. This regulatory fragmentation forces yacht distributors to maintain dual inventory and pricing strategies, with mainland operations focusing on ultra-high-net-worth buyers who are less price-sensitive to tax premiums. The concentration effect reduces market liquidity and limits the development of secondary markets for pre-owned yachts, as owners face significant tax implications when relocating vessels between jurisdictions. Anti-corruption campaigns have heightened scrutiny on conspicuous luxury consumption, creating additional compliance costs and reputational risks for corporate yacht ownership and entertainment activities.

Scarcity of Marina Berths in Tier-1 Coastal Cities

Marina berth availability in major coastal cities represents a structural bottleneck that constrains market growth despite rising demand from high-net-worth individuals. Shanghai's limited marina infrastructure relative to its HNWI population creates waiting lists and premium pricing that exclude mid-tier luxury consumers from yacht ownership consideration. The concentration of yacht ownership among real estate businessmen in cities like Qingdao reflects both wealth patterns and berth availability constraints that limit market diversification across professional demographics. Coastal land use regulations and environmental protection requirements complicate new marina development approvals, particularly in established urban areas where waterfront real estate commands premium valuations for residential and commercial development. The seasonal migration pattern from northern cities to Hainan during winter months indicates that berth scarcity drives utilization inefficiencies, with northern facilities underutilized during peak winter tourism periods while southern marinas face capacity constraints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Yacht Type: Long Range Vessels Drive Premium Shift

Sport Yachts maintained 46.01% market share in 2024, reflecting China's preference for day-cruising and coastal entertainment applications that align with business networking and corporate hospitality usage patterns. However, Long Range Yachts represent the fastest-growing segment at 11.53% CAGR through 2030, indicating market maturation toward extended cruising capabilities and international voyage planning. This shift reflects rising confidence among Chinese yacht owners in undertaking longer-distance cruising, supported by improved marina infrastructure along Southeast Asian routes and simplified customs procedures for international yacht travel. The "Others" category, encompassing specialized vessels like explorer yachts and custom builds, benefits from increasing demand for unique designs that differentiate owners within competitive social circles.

The transition toward long-range capabilities aligns with BYD's partnership with Sanlorenzo to develop yacht-dedicated battery systems, targeting mass production of electric yachts in the 30-100 foot range by 2026. Sport yacht dominance reflects the current market's focus on coastal waters and day-use patterns, but the accelerating growth of long-range vessels suggests evolving usage preferences toward destination cruising and extended voyages. The regulatory environment increasingly supports this transition, with China developing 13 cruise homeports from Dalian to Sanya to accommodate both domestic and international vessels, creating infrastructure that benefits long-range yacht operations.

By Length: Superyacht Segment Accelerates Despite Size Constraints

The 20 to 40 meter segment commands 41.52% market share in 2024, representing the sweet spot for Chinese coastal cruising and marina infrastructure compatibility. Vessels above 40 meters surge at a 12.34% CAGR through 2030, driven by ultra-high-net-worth buyers seeking differentiation and status positioning within competitive luxury markets. The Up to 20-meter category serves entry-level luxury buyers and charter operations, benefiting from lower operating costs and broader marina accessibility. This segmentation reflects China's wealth distribution patterns, where the largest market exists in the mid-size luxury category, but the highest growth occurs in ultra-luxury segments driven by wealth concentration effects.

Marina infrastructure development increasingly accommodates larger vessels, with facilities like the Qingdao Wanda Oriental Film Capital Yacht Harbour featuring 230 berths designed for vessels up to superyacht dimensions. The Above 40-meter growth trajectory indicates that Chinese buyers are transitioning from coastal cruising toward international voyage capabilities, supported by improved customs procedures and expanded marina networks throughout Southeast Asia. Berth availability constraints in Tier-1 cities disproportionately affect larger vessels, creating market dynamics where superyacht owners increasingly utilize Hainan's expanded marina infrastructure as their primary base, with seasonal relocations to northern cities during summer months.

By Propulsion Type: Electrification Reshapes Traditional Preferences

Motor Yachts dominate with 78.03% market share in 2024, reflecting established preferences for power and speed that align with Chinese business culture and entertainment usage patterns. Electric/Hybrid Motor Yachts represent the fastest growth at 18.41% CAGR through 2030, driven by environmental regulations, technological advancement, and strategic partnerships between Chinese battery manufacturers and international yacht builders. Sailing Yachts maintain a smaller market presence, limited by cultural preferences for powered vessels and the learning curve associated with sailing proficiency. The electrification trend reflects broader Chinese leadership in battery technology and electric vehicle adoption, creating natural synergies between automotive and marine propulsion development.

BYD's collaboration with Sanlorenzo to establish a Shenzhen-based R&D center for yacht-dedicated batteries demonstrates how Chinese technology companies leverage automotive electrification expertise for marine applications. The partnership targets 20% global electric-yacht battery market share within three years, indicating aggressive expansion plans that could reshape propulsion preferences across international markets. Chinese electric propulsion companies like ePropulsion are developing marine-specific battery and motor systems that address the unique requirements of yacht applications, including saltwater resistance, energy density, and charging infrastructure compatibility. Regulatory compliance frameworks increasingly favor low-emission propulsion systems, particularly in environmentally sensitive areas like Hainan's marine protected zones.

By Application: Charter Market Gains Commercial Momentum

Private ownership maintains 82.04% market share in 2024, reflecting the personal luxury positioning of yacht ownership within Chinese business culture and social status systems. Commercial Charter operations expand at 15.21% CAGR through 2030, supported by Hainan's tourism development strategy and simplified regulations for international cruise operations effective June 2024. The charter market benefits from rising domestic tourism demand, with Hainan targeting 110 million tourists by 2026, creating a substantial customer base for luxury marine experiences. Fractional ownership platforms and digital marina services are hybrid models combining private access with commercial utilization optimization.

The commercial charter acceleration reflects changing consumption patterns among younger affluent demographics who prefer experiential luxury over ownership-based status displays. Charter operations provide yacht owners with revenue generation opportunities that offset ownership costs, which is particularly important given high operating expenses like RMB 80,000 fuel costs for 24-meter powerboat fills and annual berth fees exceeding RMB 130,000. Integrating charter services with broader tourism infrastructure, including luxury hotels and destination experiences, creates package opportunities that enhance revenue per customer and extend average charter durations. Regulatory changes supporting cruise tourism recovery, with 21 international cruise ships beginning operations at Chinese ports since early 2024, demonstrate the government's commitment to marine tourism development that benefits yacht charter operations.

Geography Analysis

Hainan Province anchors the national ecosystem through its free-trade policy stack and warm-water seasonality that supports year-round cruising. The island hosts China’s first zero-tariff maritime leisure regime, making it the logical registry for owners seeking cost efficiency. Sanya’s 200-plus-berth marina integrates customs, refit, and hotel facilities, cementing its role as home port for both domestic and visiting yachts.

The Pearl River Delta is the manufacturing heartland of the Chinese yacht market, with Zhuhai’s Selene facility and surrounding electronics supply chain accelerating drivetrain and infotainment innovation. Proximity to Hong Kong provides financial services, while Shenzhen’s port regulations accept test runs for electric propulsion under sandbox exemptions, fostering R&D.

Northern hubs—Qingdao, Shanghai, and Dalian—serve dense HNWI populations and legacy yacht clubs. Qingdao’s Olympic Marina hosts more than 300 boats, 60% locally owned, and benefits from deep-draft berths suitable for 40-meter superyachts. Shanghai’s tax and berth premiums limit entry-level demand but reinforce exclusivity that sustains high brokerage margins. Seasonal relocation patterns route yachts southward during winter, smoothing nationwide charter inventory cycles and demonstrating geographic interdependence within the Chinese yacht market.

Competitive Landscape

European brands still symbolize prestige, but Chinese builders are closing fit-and-finish gaps rapidly. Sanlorenzo clinched the 2024 Best Foreign Brand award in China, yet the firm’s acquisition of regional dealer Simpson Marine signals reliance on localized sales networks. Simultaneously, BYD’s battery partnership with Sanlorenzo presents a technology fuse that may recalibrate competitive moats in favor of China-centered innovation.

Domestic yards leverage shorter build times and customizable layouts to lure buyers keen on rapid delivery. Weichai’s reboot of Ferretti Group equips Chinese conglomerates with design patents and supply contracts that compress learning curves. Meanwhile, emerging firms position around electrification niches, aligning with national decarbonization goals and turning propulsion technology into a new brand-equity axis.

Institutional capital is also entering upstream nodes: Blackstone’s USD 5.65 billion takeover of Safe Harbor Marinas represents confidence in ancillary infrastructure monetization. Chinese investors observe and may replicate the model domestically, upgrading marina networks into yield-bearing assets while vertically integrating refit yards, retail, and hospitality. This layered competition ensures no single OEM commands a decisive hold on the China yacht market, maintaining open lanes for disruptors.

China Yacht Industry Leaders

-

Ferretti Group

-

Azimut-Benetti Group

-

Sunseeker International

-

Sanlorenzo S.p.A.

-

Heysea Yachts

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BYD announced a strategic partnership with Italian luxury yacht builder Sanlorenzo to establish a joint R&D center in Shenzhen focused on developing yacht-dedicated battery systems, targeting mass production of electric yachts in the 30-100 foot range by 2026 and capturing 20% of the global electric-yacht battery market within three years.

- October 2024: Sunseeker International was acquired from China's Dalian Wanda Group by Orienta Capital Partners and Lionheart Capital after 11 years of Chinese ownership, with new owners planning substantial investment in model development and global expansion while maintaining British production facilities.

China Yacht Market Report Scope

| Sport Yacht |

| Long Range Yacht |

| Others |

| Up to 20 m |

| 20 to 40 m |

| Above 40 m |

| Motor Yacht |

| Sailing Yacht |

| Commercial |

| Private |

| By Yacht Type | Sport Yacht |

| Long Range Yacht | |

| Others | |

| By Length | Up to 20 m |

| 20 to 40 m | |

| Above 40 m | |

| By Propulsion Type | Motor Yacht |

| Sailing Yacht | |

| By Application | Commercial |

| Private |

Key Questions Answered in the Report

What CAGR is forecast for yachts in China?

Market value is set to grow at a 7.8% CAGR between 2025 and 2030, driven by policy incentives and wealth expansion.

Which yacht segment is growing fastest in China?

Long-range yachts lead growth at an 11.53% CAGR as owners pursue longer voyages and higher prestige.

How important is electric propulsion in Chinese yachting?

Electric or hybrid models post an 18.41% CAGR, reflecting emission norms and partnerships between battery makers and global yacht brands.

Why is Hainan critical to China’s yacht ecosystem?

Hainan’s zero-tariff Free Trade Port cuts import costs, offers simplified customs, and hosts marinas that operate year-round.

What restrains broader yacht adoption on the mainland?

High luxury taxes outside Hainan and a shortage of certified berths in Tier-1 cities limit accessibility for new entrants.

Page last updated on: