China-to-Europe Cross-Border B2C E-commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

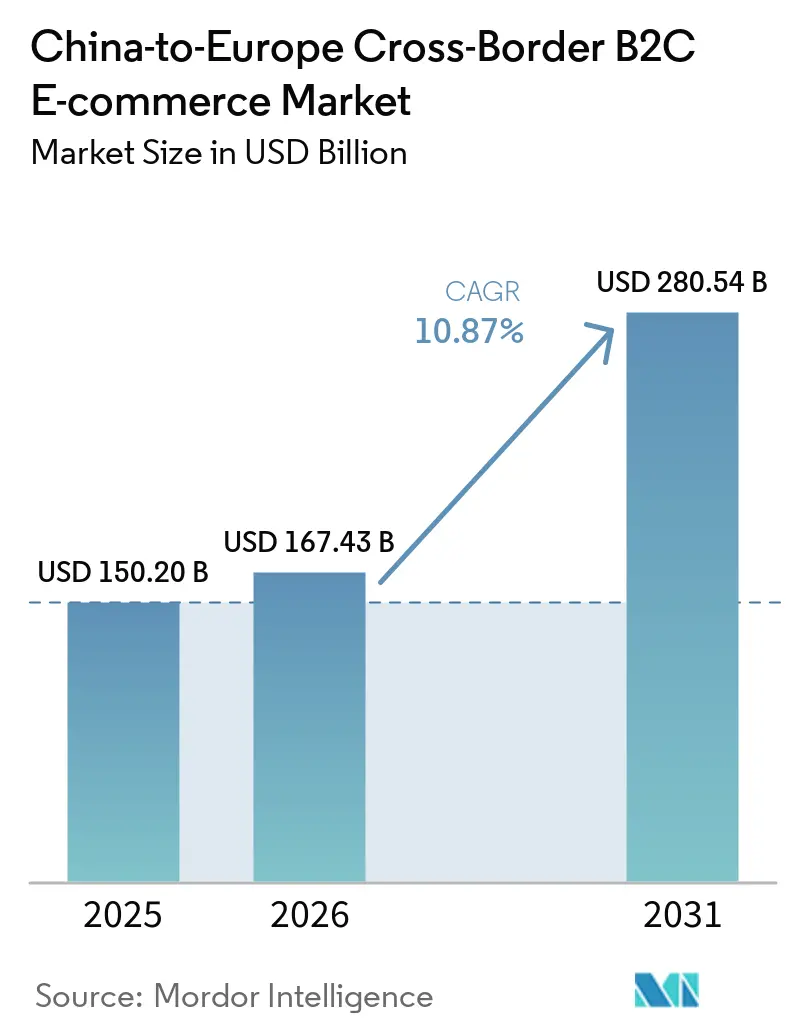

| Base Year Market Size (2025) | USD 150.20 Billion |

| Market Size (2026) | USD 167.43 Billion |

| Market Size (2031) | USD 280.54 Billion |

| Growth Rate (2026 - 2031) | 10.87% CAGR |

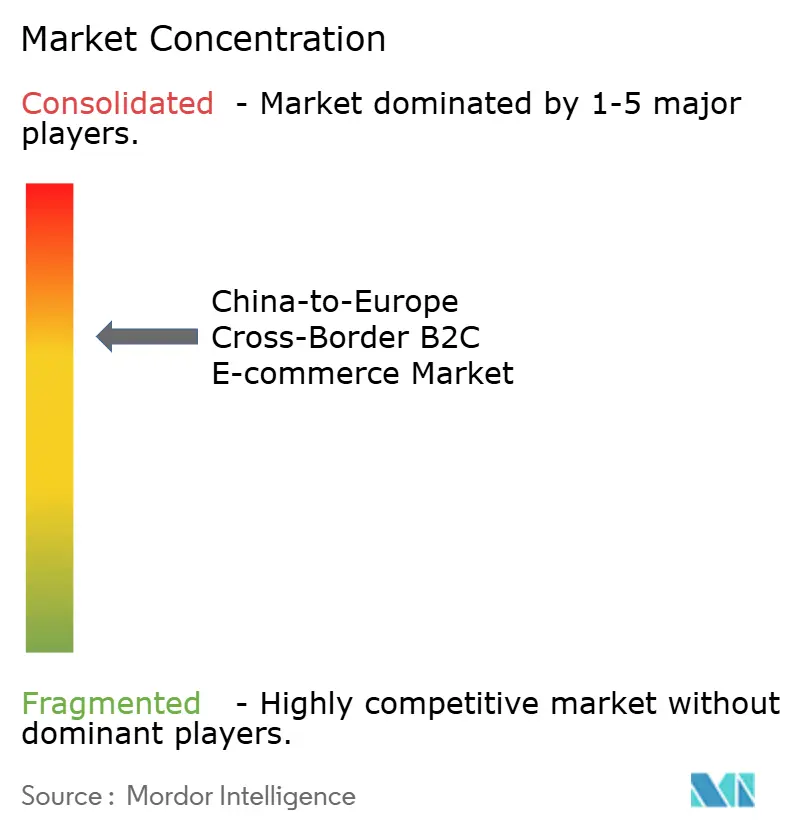

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China-to-Europe Cross-Border B2C E-commerce Market Analysis by Mordor Intelligence

The China-to-Europe cross-border B2C e-commerce market size is projected to be USD 150.20 billion in 2025, USD 167.43 billion in 2026, and USD 280.54 billion by 2031, growing at a CAGR of 10.87% from 2026 to 2031.

The China-to-Europe cross-border B2C e-commerce market is being shaped by a shift from parcel-led imports to warehouse-led fulfillment, which is improving delivery reliability and narrowing the service gap with domestic retailers. Platform competition is also moving beyond discounting, as larger operators are building local logistics, returns handling, and regulatory capacity within Europe. Social commerce is expanding customer acquisition channels, giving Chinese brands a stronger path into younger user cohorts across several European countries. At the same time, the July 2026 EU customs change for low-value parcels is weakening the older cost advantage of direct-from-China shipping and rewarding sellers that can consolidate inventory into European networks. Rising enforcement under the Digital Services Act and the broader product safety and packaging framework is likely to keep volume concentrated among the better-capitalized platforms that can absorb compliance costs across multiple European jurisdictions.

Key Report Takeaways

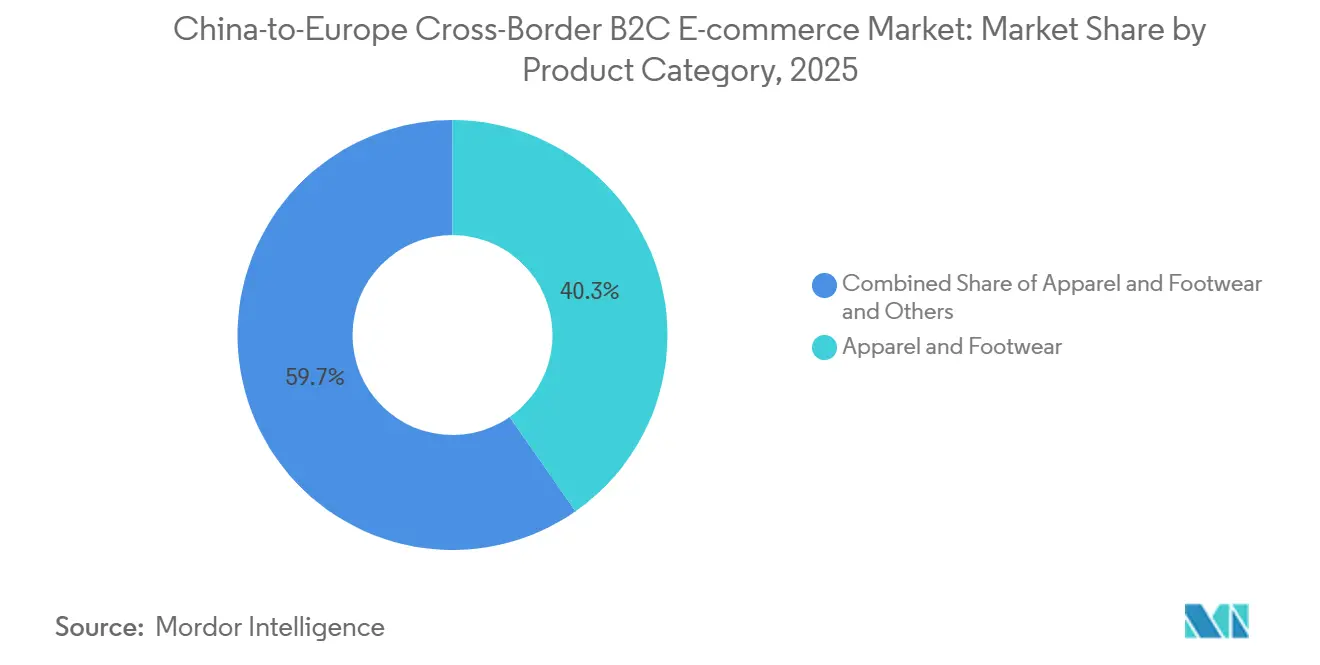

- By product category, apparel and footwear accounted for 40.31% of the China to Europe cross-border B2C e-commerce market size in 2025, and the same segment is forecast to expand at 13.94% through 2031.

- By sales channel, online marketplaces held 70.1% of the China to Europe cross-border B2C e-commerce market share in 2025, while social commerce is projected to record the highest CAGR at 22.91% through 2031.

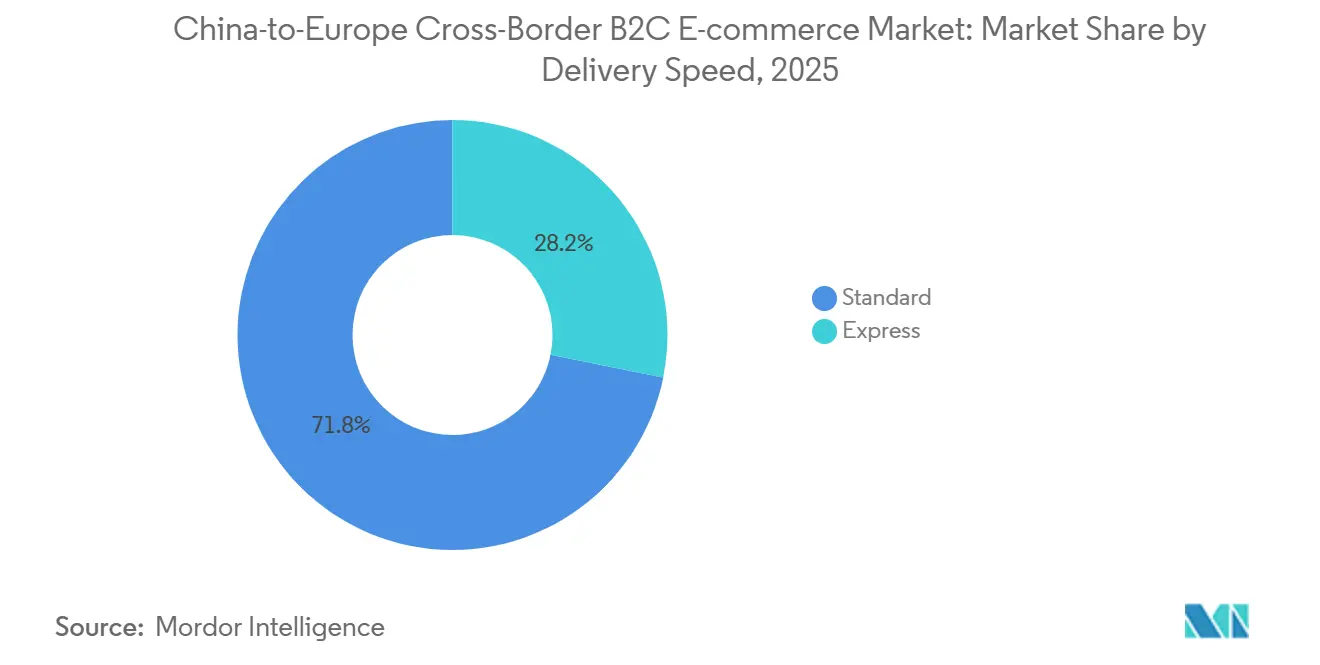

- By delivery speed, standard delivery represented 71.83% of the China to Europe cross-border B2C e-commerce market share in 2025, while express delivery is expected to advance at 16.08% through 2031.

- By destination country, Western Europe held 57.67% of the China to Europe cross-border B2C e-commerce market share in 2025, while Eastern Europe is expected to grow at 15.79% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China-to-Europe Cross-Border B2C E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-Value Pricing and Endless Assortment | +2.5% | Global, strongest in Western Europe and Eastern Europe | Short term (≤ 2 years) |

| Marketplace-Led Cross-Border Discovery | +2.0% | Global, accelerating in Western Europe and Northern Europe | Medium term (2-4 years) |

| EU-Local Warehousing and Faster Delivery | +1.8% | Western Europe core with spillover into Central and Eastern Europe | Short term (≤ 2 years) |

| Faster Growth in Eastern Europe and Nordics | +1.2% | Eastern Europe and Northern Europe | Medium term (2-4 years) |

| AI-Shopping Rewards Delivery-Data Transparency | +0.8% | Western Europe early adopters with spillover from China-origin platform systems | Medium term (2-4 years) |

| Returns-Fee Normalization Supports Cross-Border Conversion | +0.5% | Western Europe first, then Southern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ultra-Value Pricing and Endless Assortment

Price remains a primary draw for shoppers using Chinese platforms across Europe, and that continues to support the China-to-Europe cross-border B2C e-commerce market. The advantage comes from a supply base that can launch large SKU ranges quickly and at low unit cost. Apparel, accessories, home items, and small electronics fit this model well because they combine trend turnover with manageable shipping economics. The model is now under more pressure because the new EU parcel duty reduces the landed price edge on direct shipments. Even so, platforms that can hold inventory within Europe are better placed to maintain the value proposition while weaker sellers lose pricing flexibility.

Marketplace-Led Cross-Border Discovery

Online marketplaces remain the main discovery layer for cross-border shopping, which gives the China-to-Europe cross-border B2C e-commerce market a broad traffic base. Consumers often enter through familiar platform search, recommendations, and promotion slots rather than through independent brand sites. This structure benefits platforms that can combine catalog depth with localized service rules, payments, and returns. It also means branded Chinese sellers can scale faster because marketplaces reduce the cost of finding new customers in each country. The model is likely to stay important even as direct-to-consumer and social channels grow, because marketplaces still aggregate trust, visibility, and repeat demand at a larger scale.

EU-Local Warehousing and Faster Delivery

The warehousing push across Europe is one of the clearest structural supports for the China-to-Europe cross-border B2C e-commerce market. Shein opened its primary European logistics hub in Wrocław, Poland, with 740,000 m² of capacity designed to support its regional fulfillment footprint[1]SHEIN Group, “SHEIN Opens State-of-the-Art European Logistics Hub in Wrocław, Poland,” SHEIN Group Newsroom, sheingroup.com. Local inventory changes cost structure, because sellers can bring stock in bulk and distribute closer to demand instead of treating every order as a separate cross-border parcel. It also improves return handling and delivery consistency, which matters more as European consumers compare Chinese platforms with domestic service levels. The benefit is even stronger under the new customs regime, as warehouse-led models can soften the impact of per-item parcel charges.

Faster Growth in Eastern Europe and Nordics

The geographic mix is becoming more important in the China-to-Europe cross-border B2C e-commerce market, as growth is no longer driven solely by the largest Western European economies. Eastern Europe is expanding faster, driven by rising digital commerce adoption and Poland's growing role as a distribution hub. The Nordics also remain attractive because online shopping habits are mature and cross-border acceptance is comparatively high. These areas create room for Chinese platforms to build share outside the most contested Western markets. The result is a wider demand map for the market, with scale still coming from Western Europe and new momentum coming from Eastern and Northern Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Duty-Free Threshold Removal and Parcel Fees | -3.2% | EU-wide for all non-EU parcel flows | Short term (≤ 2 years) |

| DSA, GPSR, and VAT Compliance Pressure | -1.8% | EU-wide, strongest in larger Western European markets | Medium term (2-4 years) |

| PPWR and EPR Packaging Redesign Burden | -0.8% | EU-wide, with a stronger effect in regulated packaging markets | Medium term (2-4 years) |

| Local Creator-Commerce Execution Costs | -0.5% | Western Europe first, then broader EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Duty-Free Threshold Removal and Parcel Fees

The removal of the EUR 150 (USD 163) customs duty exemption for small parcels is the most direct near-term headwind for the China-to-Europe cross-border B2C e-commerce market. The EU Council approved a flat EUR 3 (USD 3.3) per-item charge for parcels valued at EUR 150 or less (USD 163), effective from July 1, 2026. This directly weakens the economics of low-ticket direct shipping from China into Europe. It also pushes sellers toward consolidation of their assortments because multi-item orders can incur greater duty exposure. The policy favors operators that have already moved toward European warehousing and will be hardest on smaller merchants that still depend on individual parcel flows.

DSA, GPSR, and VAT Compliance Pressure

Compliance pressure is rising quickly, increasing the fixed costs of participation in the China-to-Europe cross-border B2C e-commerce market. The European Commission opened formal proceedings against Shein in February 2026 under the Digital Services Act, raising concerns about recommender system transparency, addictive design features, and illegal product listings. Temu also remained under DSA scrutiny after the Commission had already opened formal proceedings against the platform earlier under the same framework. GPSR obligations add product documentation and accountability requirements, while VAT compliance via IOSS creates additional reporting requirements for cross-border operators. Together, these rules reward scale because large platforms can spread legal, operational, and reporting costs across far higher order volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Apparel and Footwear Anchors Revenue, Niche Categories Accelerate

Apparel and footwear accounted for 40.31% of the China-to-Europe cross-border B2C e-commerce market in 2025 and is also the fastest-growing product segment, with a 13.94% CAGR through 2031. That combination is unusual because the largest segment is also the one expanding the quickest. The category aligns well with cross-border economics because products are light, margins can absorb promotional pricing, and trend cycles are short. It also aligns with the strengths of Chinese manufacturing, where fast design turnover and a broad assortment support repeat purchase behavior.

The segment is benefiting further from the move toward European warehousing because faster regional fulfillment reduces fit-related friction and makes returns more manageable. This is especially important for fashion orders, where size variation and multi-item baskets are common. The broader China-to-Europe cross-border B2C e-commerce industry also offers apparel sellers a path to premiumization once customer acquisition is established, rather than forcing them to compete solely on entry price.

By Sales Channel: Marketplace Dominance Is Eroding at the Margin

Online marketplaces accounted for 70.1% of total sales in 2025, confirming that the China-to-Europe cross-border B2C e-commerce market still relies mainly on platform-led demand aggregation. Marketplace scale remains hard to replace because it combines traffic, payment confidence, and built-in discovery across multiple countries. This also helps Chinese sellers expand into Europe without having to build brand awareness from scratch in every market. Direct-to-consumer webstores remain relevant for brands seeking greater control over pricing, loyalty data, and post-purchase service.

Social commerce is the fastest-growing sales channel, with a 22.91% CAGR through 2031. It is becoming a more serious route to customer acquisition in the China-to-Europe cross-border B2C e-commerce market. TikTok Shop expanded to Austria, Belgium, the Netherlands, and Poland in June 2026, taking its European footprint to 10 countries[2]Source: TikTok, “TikTok Shop Expands Across Europe, Bringing Content-Driven Commerce to Austria, Belgium, Netherlands, and Poland,” TikTok Newsroom, newsroom.tiktok.com. That wider coverage matters because it gives brands and sellers a more unified route into creator-led discovery across Europe. The China-to-Europe cross-border B2C e-commerce industry is therefore becoming more channel-diverse, but marketplaces still retain the larger revenue base for now.

By Delivery Speed: Standard Holds Volume but Express Captures Value Buyers

Standard delivery retained 71.83% of total volume in 2025, which shows that most buyers still accept a waiting period when prices remain attractive. In the China-to-Europe cross-border B2C e-commerce market, this segment is no longer defined only by long direct shipping from China. The service level inside standard delivery has improved because more orders are now processed through European fulfillment nodes. As a result, the label has stayed the same while the real customer experience has become more competitive.

Express delivery is growing at 16.08% through 2031, reflecting the behavior of higher-frequency buyers who value speed once trust has already been established. Express is especially relevant in larger Western European countries where repeat shopping and higher basket values are more common. The broader shift toward European warehouse capacity is supporting that move because it makes next-day or two-day delivery more realistic in selected corridors. Shein’s Wrocław logistics hub is part of that structural change, since local inventory can support faster outbound fulfillment and smoother returns processing across the region.

Geography Analysis

Western Europe accounted for 57.67% of the China-to-Europe cross-border B2C e-commerce market size in 2025, and Germany, France, and the UK remained the revenue core. These markets remain central because they combine larger online spending pools with denser fulfillment and returns infrastructure. The China-to-Europe cross-border B2C e-commerce market is also more tightly regulated here, which raises the entry bar but gives established larger platforms a stronger moat. Amazon stated that EU small businesses reached a record EUR 40 billion (USD 43.5 billion) in sales in 2025, showing that European marketplace activity remained strong alongside the rise of Chinese-origin platforms[3]Source: Amazon EU, “EU Small Businesses Reach Record EUR 40 Billion in Sales on Amazon,” Amazon EU Newsroom, aboutamazon.eu. That suggests competition in Western Europe is not purely zero-sum, as both local and cross-border sellers are expanding within large digital retail ecosystems.

Eastern Europe is the fastest-growing regional destination in the China-to-Europe cross-border B2C e-commerce market, with a 15.79% CAGR through 2031. Poland has become the key bridge because it combines logistics investment with reach into surrounding Central and Eastern European markets. Shein’s Wrocław hub reinforces that role and shows how cross-border flows are being reorganized around regional stockholding rather than only long-haul parcel imports. This shift should continue to support adoption across nearby markets where local e-commerce ecosystems are still developing, and delivery expectations are rising.

Northern Europe remains smaller in value terms, but it offers a higher-quality demand profile for the China-to-Europe cross-border B2C e-commerce market. Consumers in the Nordics and Baltics are comfortable with online purchases and already operate inside the same EU VAT and customs framework that supports warehouse-led cross-border expansion. TikTok Shop’s broader European rollout points to a discovery model that can help brands build trust first and compete on price later in these markets. Over time, Northern Europe is likely to matter more for higher-value baskets and for categories where service reliability matters as much as low price.

Competitive Landscape

The China-to-Europe cross-border B2C e-commerce market shows moderate to high platform-level concentration, even though seller participation remains fragmented. Scale is increasingly defined by three capabilities: logistics depth within Europe, multi-country demand capture, and the ability to manage compliance risk. This is why competition is moving away from simple price matching and toward service reliability, local stock positioning, and regulatory readiness. The platforms that can fund these layers are pulling ahead because smaller operators struggle to match delivery speed and legal preparedness across several countries. That pattern should continue to strengthen as customs, packaging, and product-safety rules become more stringent.

Leading players are clustering around warehouse-first logistics, social-led traffic capture, and stronger seller operating systems. Shein’s opening of its Wrocław logistics hub is a clear example of the first strategy because it gives the company a regional fulfillment base inside Europe. TikTok Shop’s expansion to 10 European countries by June 2026 is an example of the second because it widens the creator-commerce route for sellers and brands entering Europe. LightInTheBox’s 2025 results point to the third strategy, as the company used AI-led operational changes and branded assortment expansion to improve margin quality rather than competing solely on shipping speed.[4]Source: LightInTheBox Holding Co., Ltd., “LightInTheBox Reports Fourth Quarter and Full Year 2025 Financial Results,” PR Newswire, prnewswire.com

Regulatory exposure is becoming a competitive filter in its own right. The European Commission’s formal proceedings against Shein showed that platform design, product governance, and recommendation systems are now part of the operating cost of European expansion. Temu also remained under formal DSA proceedings, reinforcing the point that scale platforms will be judged on systemic compliance, not just consumer reach. As a result, the next phase of the China-to-Europe cross-border B2C e-commerce market is likely to favor a smaller group of well-funded operators. At the same time, niche sellers survive mainly through category specialization, differentiated branding, or by using third-party marketplaces with established local trust.

China-to-Europe Cross-Border B2C E-commerce Industry Leaders

Alibaba Group

Temu

SHEIN

Amazon

JD.com

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: TikTok Shop expanded to Austria, Belgium, the Netherlands, and Poland, bringing its footprint to 10 European countries. The launch included a Sell Across Europe tool that enables multi-country sales through a single registration.

- May 2026: Shein opened a major logistics center in Cannock as part of a EUR 250 million (USD 289 million) five-year European investment strategy, with the facility designed to improve delivery speed and supply chain resilience across UK and European markets.

- April 2026: Shein partnered with THG Fulfil to provide direct order-flow integration from the Shein marketplace into THG Fulfil's fulfillment network, enabling next-day delivery cut-offs, seamless returns processing, and end-to-end logistics for sellers on the Shein UK marketplace. The partnership supports over 2,500 active UK sellers on Shein Marketplace.

- December 2025: Shein opened a 740,000 m² logistics hub near Wrocław, Poland, as its primary European distribution center. The site features robotic picking and automated sorting and was expected to reach full operational capacity by the end of 2025.

China-to-Europe Cross-Border B2C E-commerce Market Report Scope

| Consumer Electronics |

| Apparel and Footwear |

| Furniture, Home Decor, and Household Products |

| Outdoors and Sports |

| Other Product Categories |

| Online Marketplaces |

| Direct-to-Consumer (Webstores) |

| Social Commerce (Live, Chat) |

| Express |

| Standard |

| Western Europe | Germany |

| France | |

| UK | |

| BENELUX | |

| Spain | |

| Italy | |

| Rest of Western Europe | |

| Eastern Europe | Poland |

| Czech Republic | |

| Hungary | |

| Romania | |

| Rest of Eastern Europe | |

| Northern Europe (Nordics and Baltic Countries) |

| By Product Category | Consumer Electronics | |

| Apparel and Footwear | ||

| Furniture, Home Decor, and Household Products | ||

| Outdoors and Sports | ||

| Other Product Categories | ||

| By Sales Channel | Online Marketplaces | |

| Direct-to-Consumer (Webstores) | ||

| Social Commerce (Live, Chat) | ||

| By Delivery Speed | Express | |

| Standard | ||

| By Destination Country | Western Europe | Germany |

| France | ||

| UK | ||

| BENELUX | ||

| Spain | ||

| Italy | ||

| Rest of Western Europe | ||

| Eastern Europe | Poland | |

| Czech Republic | ||

| Hungary | ||

| Romania | ||

| Rest of Eastern Europe | ||

| Northern Europe (Nordics and Baltic Countries) | ||

Key Questions Answered in the Report

What is the projected value of China to Europe's cross-border B2C e-commerce by 2031?

It is projected to reach USD 280.54 billion by 2031, rising from USD 167.43 billion in 2026 at a 10.87% CAGR.

Which product category leads current revenue and growth?

Apparel and footwear lead with a 40.31% share in 2025 and are also the fastest-growing product segments at a 13.94% CAGR through 2031.

Why is Western Europe still the main revenue center?

Western Europe accounted for 57.67% of the total value in 2025 because Germany, France, and the UK combined for stronger spending power, better logistics coverage, and higher repeat purchase rates.

Which region is growing the fastest across Europe?

Eastern Europe is the fastest-growing destination, with a 15.79% CAGR through 2031, supported by rising digital commerce adoption and stronger use of Poland as a logistics hub.

How important are online marketplaces in cross-border sales from China?

Online marketplaces accounted for 70.1% of total sales in 2025, which shows that platform-led discovery and trust remain central to purchasing behavior.

What is the biggest near-term risk for sellers shipping directly from China?

The biggest near-term risk is the EU’s new parcel duty framework for low-value imports, which reduces the historical price advantage of direct parcel shipping and favors warehouse-led models.

Page last updated on: