Southeast Asia Cross-border E-commerce Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 45.39 Billion |

| Market Size (2026) | USD 50.37 Billion |

| Market Size (2031) | USD 84.74 Billion |

| Growth Rate (2026 - 2031) | 10.97% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Southeast Asia Cross-border E-commerce Market Analysis by Mordor Intelligence

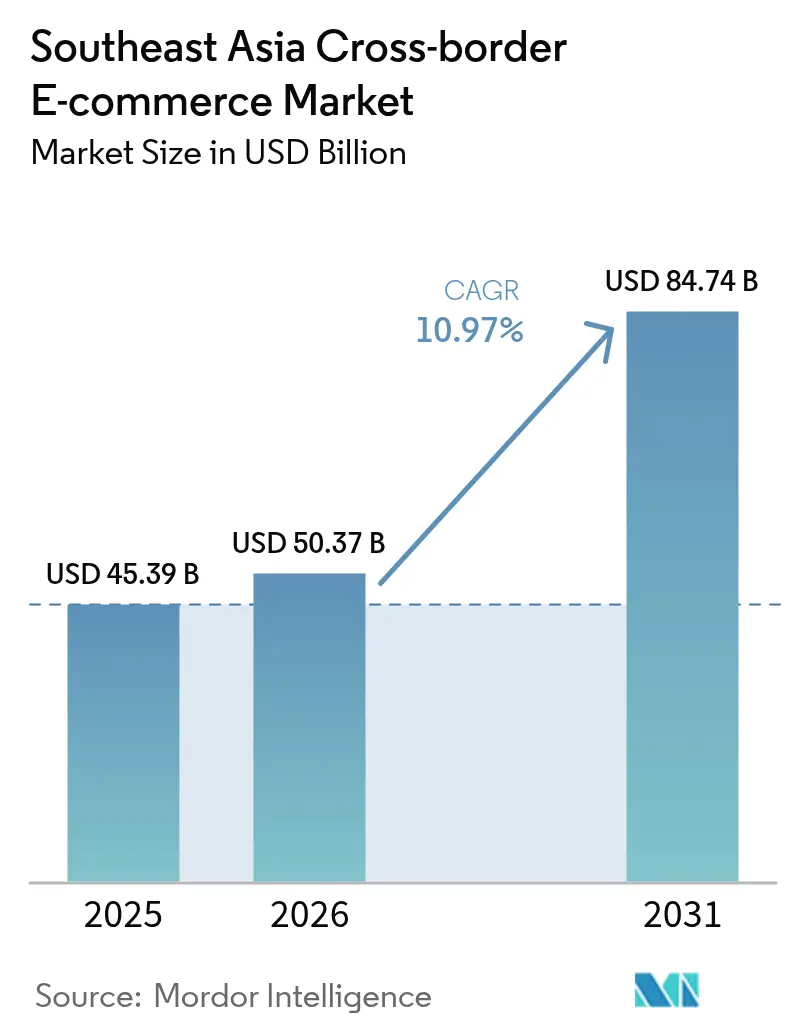

The Southeast Asia Cross-border E-commerce Market size was valued at USD 45.39 billion in 2025 and estimated to grow from USD 50.37 billion in 2026 to reach USD 84.74 billion by 2031, at a CAGR of 10.97% during the forecast period (2026-2031).

Rising disposable incomes, a growing base of 402 million digital consumers, and a rapid pivot toward mobile-first shopping continue to underpin demand. Tariff concessions under the Regional Comprehensive Economic Partnership (RCEP) are lowering average landed costs for Chinese and Korean goods, intensifying competition in electronics and beauty lines. Domestic e-wallet super-apps now power 70% of checkout value, streamlining payments across borders and stimulating higher ticket sizes. Bonded-warehouse logistics, supported by ASEAN customs transit protocols, are cutting intra-regional delivery times to under three days, reinforcing buyer confidence and repeat purchase rates.

Key Report Takeaways

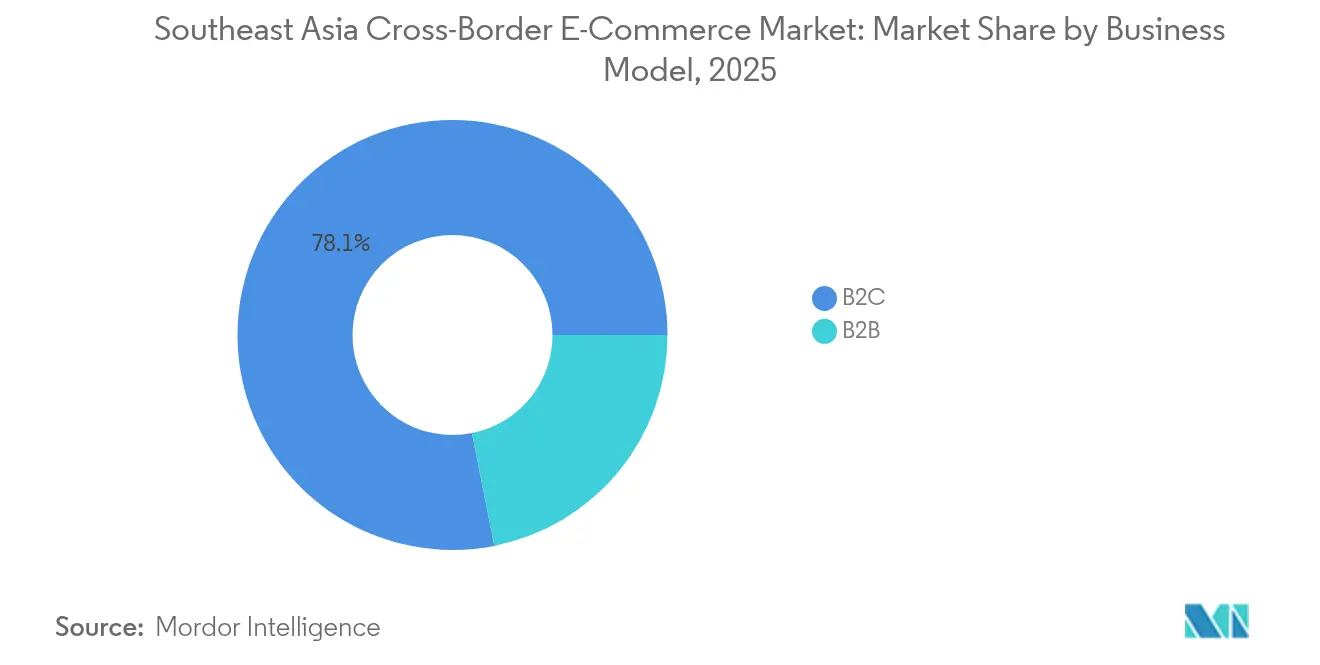

- By business model, the B2C segment captured 78.12% of the Southeast Asia cross-border e-commerce market share in 2025. The Southeast Asia cross-border e-commerce market for B2B is projected to expand at a 8.99% CAGR between 2026-2031.

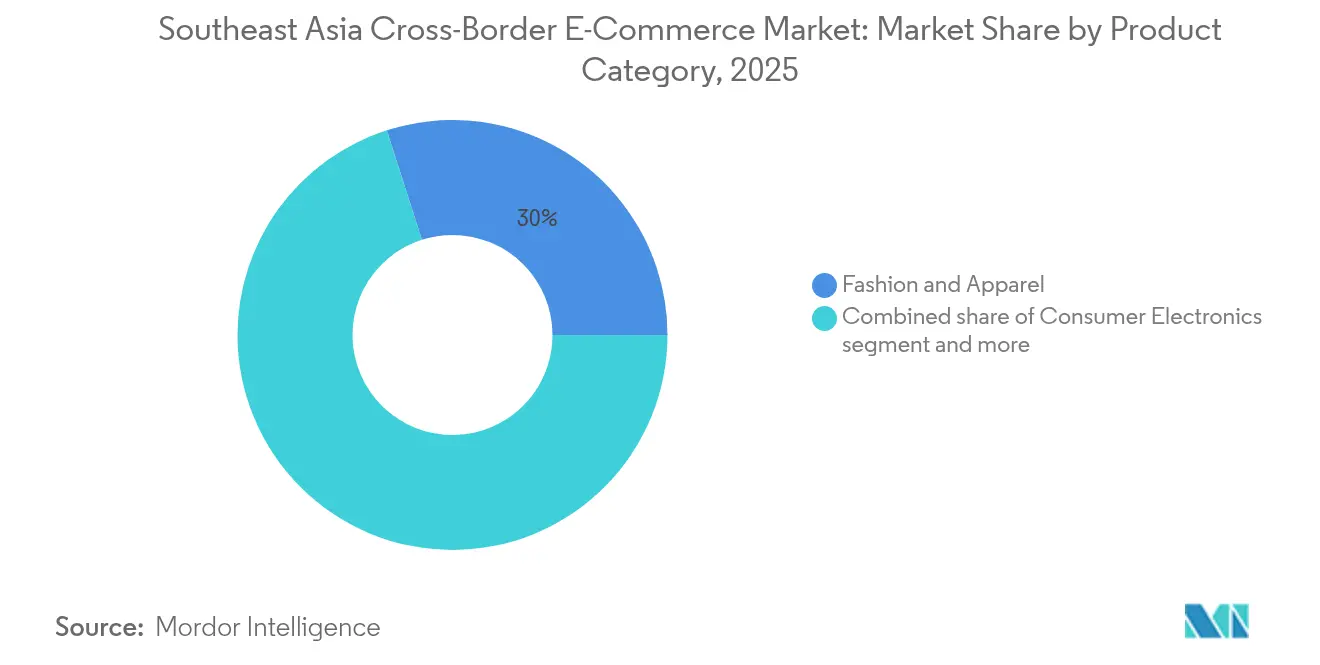

- By product category, fashion and apparel led with 29.95% of Southeast Asia cross-border e-commerce market revenue share in 2025. The Southeast Asia cross-border e-commerce market for beauty and personal care is forecast to grow at a 10.72% CAGR between 2026-2031.

- By sales channel, online marketplaces held 72.64% of the Southeast Asia cross-border e-commerce market share in 2025. The Southeast Asia cross-border e-commerce market for social commerce is advancing at a 19.74% CAGR between 2026-2031.

- By geography, Indonesia contributed 34.12% of the Southeast Asia cross-border e-commerce market's 2025 revenue. The Southeast Asia cross-border e-commerce market for Vietnam is set to grow at an 11.08% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Cross-border E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic e-wallet super-apps (GrabPay, GCash, MoMo) accelerating cross-border checkout | +2.2% | Strongest in Philippines, Vietnam, Singapore | Medium term (2-4 years) |

| RCEP tariff cuts (4-8%) on Chinese & Korean goods | +2.8% | Most pronounced in Indonesia, Thailand, Vietnam | Medium term (2-4 years) |

| Video-commerce & live streaming converting social-media GMV | +1.7% | Indonesia, Thailand, Vietnam, Philippines | Short term (≤2 years) |

| B2B2C bonded-warehouse model cutting delivery to <3 days | +2.0% | Malaysia, Singapore, Thailand; benefits across ASEAN | Medium term (2-4 years) |

| Buy-now-pay-later expansion among Gen-Z shoppers | +1.3% | Indonesia, Singapore, Philippines | Short term (≤2 years) |

| ASEAN Customs Transit System enabling duty-suspended trucking | +1.1% | Cambodia, Laos, Myanmar, Vietnam | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Domestic E-wallet Super-apps Driving Cross-border Payments

The proliferation of GrabPay, GCash, and MoMo is redefining checkout preferences across the Southeast Asia cross-border e-commerce market. Regional mobile-wallet users are projected to reach 2.6 billion by 2025, with transaction values climbing to USD 636 billion. Platform interoperability and QR-code standardization are lowering foreign-exchange friction, encouraging first-time cross-border purchases among the unbanked[1]Asian Development Bank, “Asian Economic Integration Report 2024,” Asian Development Bank, adb.org. In the Philippines, GCash has converted more than half of its active users into international shoppers, while Vietnam’s MoMo continues to embed buy-now-pay-later micro-credit for higher-value imports. Elevated wallet penetration is closing the trust gap that once hindered regional sellers.

RCEP Tariff Reductions Reshaping Regional Trade Flows

Since 2024, average tariffs on Chinese and Korean origin goods have fallen by 4-8%, lifting trade volumes for electronics and beauty lines in the Southeast Asia cross-border e-commerce market. Merchants are funneling inventory through specialized hubs in Malaysia and Thailand, leveraging duty suspension zones to pre-position stock. Electronics brands report double-digit improvements in price competitiveness, and beauty labels are launching region-wide campaigns timed to tariff milestones. Customs harmonization remains uneven, yet collaborative frameworks under RCEP are gradually aligning documentation procedures to accelerate throughput.

Video-commerce Revolutionizing Consumer Engagement

Live-stream shopping now converts 15% of social-media gross merchandise value into cross-border orders. Influencer-led storytelling, scarcity cues, and real-time discounts are driving impulse purchases in beauty, fashion, and home décor verticals. Platforms integrate one-click checkout, shrinking the path-to-purchase to under 25 seconds. In Indonesia, leading live-stream hosts average session view-times exceeding 20 minutes, sharply boosting add-to-cart rates. Advertisers are redirecting budgets from static feeds to interactive formats, expecting video-based sales to outpace traditional banner campaigns by 2027.

B2B2C Bonded-warehouse Model Transforming Regional Logistics

Lazada’s Malaysia Fulfilment Hub exemplifies a bonded-warehouse network that slashes delivery latency to under three days for intra-ASEAN orders. AI-driven inventory forecasting trims stockouts by 35% and raises on-time-delivery metrics to 97%. The model reduces cross-border shipping costs by 23-30% relative to direct-ship flows, unlocking incremental margins for sellers and lower prices for buyers[2]Singapore Economic Development Board, “Logistics Industry Review 2024,” Singapore Economic Development Board, edb.gov.sg. Customs pre-clearance protocols allow goods to clear within six hours versus up to three days previously. Beauty and consumer electronics benefit most since shelf-life and seasonality risks decline with proximate stockholding.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented de-minimis thresholds (USD 75–150) clouding landed costs | -1.7% | Indonesia, Malaysia, Thailand | Medium term (2-4 years) |

| High reverse-logistics costs; >22% fashion return rates | -1.3% | Indonesia, Philippines | Short term (≤2 years) |

| Patchy FX controls delaying seller payouts by up to 5 days | -0.8% | Indonesia, Vietnam; spillover to Thailand, Malaysia | Short term (≤2 years) |

| Social-commerce fraud eroding trust in Tier-2/3 cities | -0.5% | Indonesia, Vietnam, Philippines; emerging in Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented De Minimis Rules Creating Landed-Cost Opacity

In Southeast Asia's cross-border e-commerce market, varying thresholds muddle price transparency. Merchants grapple with multiple tax engines, leading to inflated operating costs and checkout confusion for shoppers. Indonesia's import VAT on low-value parcels dampens impulse purchases. While negotiations on the ASEAN Digital Economy Framework seek to standardize small-parcel rules, a consensus before 2026 seems improbable. Meanwhile, sellers are turning to landed-cost calculators and tailored promotions to navigate these regulatory challenges.

High Reverse-Logistics Costs Hampering Profitability

Return rates surpass 22% in cross-border fashion flows, straining margins for platforms and sellers alike. Multiple handling, island geographies, and fragmented courier networks push reverse-shipping charges to nearly double forward-rate equivalents. Investments in smart lockers, size-recommendation algorithms, and consolidated drop points are emerging countermeasures. Early adopters in Singapore have cut average processing times by 30%, but scale deployment across archipelagic markets remains capital-intensive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2C Dominance Masks B2B Growth Potential

The B2C segment continued leadership in the Southeast Asia cross-border e-commerce market. Familiar marketplace storefronts, localized language support, and integrated parcel-tracking sustain traffic growth, particularly among first-time buyers in Indonesia and Thailand. Cross-border order frequency has risen as younger demographics seek niche international labels unavailable offline.

Commercial procurement is gathering momentum. The B2B segment, though smaller, is on track for a 8.99% CAGR to 2031 as manufacturers in Vietnam and Thailand digitize sourcing. Simplified customs corridors under the ASEAN Customs Transit System now cut documentation by up to 50%, accelerating just-in-time inventory moves. Platform providers are layering trade-finance tools and verified supplier badges to raise trust levels. Collective purchasing among micro-enterprises further signals that the Southeast Asia cross-border e-commerce market is evolving beyond purely consumer transactions.

By Product Category: Beauty Segment Outpacing Fashion’s Volume Lead

Fashion and apparel retained a 29.95% slice of 2025 revenue, upheld by affordable fast-fashion labels and influencer-curated collections. Repeat purchase cycles stay short at 45 days as new drops entice shoppers across mobile apps. Yet fashion’s extensive size-related returns create profitability pressures, nudging platforms to refine fit-prediction engines.

Beauty and personal care, supported by tutorial-based video-commerce, is advancing at a 10.72% CAGR. Brands leverage micro-influencers for region-specific skin-tone demonstrations, driving trial and cross-selling. Electronics also profit from tariff concessions, while home appliances move slowly due to bulky shipping. Across segments, AI-powered product recommendation stacks are tailoring storefronts, heightening engagement, and lifting the Southeast Asia cross-border e-commerce market size for discretionary categories.

By Sales Channel: Social Commerce Disrupting Marketplace Dominance

Online marketplaces remain the default gateway, commanding 72.64% of 2025 transactions. Their scale enables preferential courier rates and country-wide cash-on-delivery options that newer channels struggle to match. Loyalty programs and flash-sale mechanics keep user retention high, although growth is moderating as saturation sets in.

Social commerce exhibits a 19.74% CAGR trajectory, spearheaded by embedded checkout functions on short-video platforms. Seller count on integrated video-commerce ecosystems grew fivefold between 2022 and 2024, fueled by low entry barriers and viral content loops. Direct-to-consumer webstores gain traction in Singapore and Malaysia, where payment security and high digital literacy support independent checkout. These parallel formats illustrate how the Southeast Asia cross-border e-commerce market continues to diversify, with shoppers comfortable shifting between discovery-rich social feeds and logistics-efficient marketplaces.

Geography Analysis

Indonesia anchors the Southeast Asia cross-border e-commerce market with a 34.12% revenue share. A population exceeding 280 million, expansive social-media usage, and supportive instant-payment rails sustain purchasing power. Government initiatives aimed at real-time gross settlement and digital identity verification are easing onboarding, though import levies still weigh on price competitiveness for certain categories.

Vietnam represents the fastest-growing landscape, clocking an 11.08% CAGR through 2031. Mobile’s majority share of online checkouts underscores consumer comfort with handheld shopping. The country’s manufacturing base and dense free-trade-agreement network give sellers logistical proximity to source stock and ship cost-effectively, thereby enhancing the Southeast Asia cross-border e-commerce market size for small and medium exporters.

Thailand is set to account for a significant portion of the projected revenue in 2025. Affiliate-commerce programs, where a notable 83% of buyers heed influencer recommendations, are fueling this demand surge. Meanwhile, relaxed duty-free thresholds on low-value items have emboldened Chinese sellers, elevating the competitive landscape for local brands. While Singapore, Malaysia, and the Philippines each command mid-single-digit revenue shares, their roles in the ecosystem are pivotal. Singapore stands out as the nucleus for payments and logistics; Malaysia is home to essential bonded hubs; and the Philippines, with its youthful digital demographic, champions mobile-first strategies. Together, these dynamics underscore the robustness of Southeast Asia's cross-border e-commerce landscape.

Competitive Landscape

The Southeast Asia cross-border e-commerce market displays moderate concentration. Shopee, Lazada, Tokopedia, and TikTok Shop jointly command the majority of aggregate GMV, creating economies of scale in advertising, payments, and last-mile delivery. Shopee’s hyper-localized campaigns and extensive courier alliances preserve leadership in Indonesia, Malaysia, and the Philippines.

TikTok’s USD 1.5 billion acquisition of a controlling stake in Tokopedia in late 2024 introduced a social-commerce engine into a mature marketplace framework. Monthly active users across the merged entity now eclipse 225 million, augmenting video-enabled discovery with proven logistics workflows. Lazada, backed by Alibaba, continues to expand bonded-warehouse capacity in Malaysia and Thailand, aiming to compress delivery windows to match domestic standards across ASEAN.

Niche disruptors such as WEBUY pioneer community-buying models that swap individual parcel shipping for consolidated bulk drops, trimming logistics expenses in suburban clusters. Payment service providers embed buy-now-pay-later options to amplify basket sizes, while AI engines personalize storefronts down to neighborhood-level demand profiles. Competition is thus shifting from pure scale toward integrated commerce ecosystems that blend content, credit, and fulfillment—an evolution that will shape investment flows into the Southeast Asia cross-border e-commerce market during the next five years.

Southeast Asia Cross-border E-commerce Industry Leaders

-

Shopee (Sea Ltd)

-

Lazada Group (Alibaba)

-

Tokopedia (GoTo)

-

Bukalapak

-

Qoo10 Pte Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Vingroup and Shopee signed an MoU to deploy VinFast electric vehicles for last-mile delivery and install smart lockers in urban retail complexes.

- May 2025: DHL acquired IDS Fulfillment to deepen U.S. e-commerce capabilities, creating spill-over opportunities for Southeast Asian sellers entering North America.

- March 2025: DHL closed the CRYOPDP purchase, bolstering temperature-controlled logistics for cross-border healthcare shipments.

- February 2025: Accelerated Global Solutions acquired a 15% stake in KGW Logistics, unlocking faster trans-Pacific lanes for Southeast Asian exporters.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Southeast Asia cross-border e-commerce market as the value of physical goods ordered online in which the merchant and final consumer are registered in different countries, settlement occurs digitally, and the parcel crosses at least one customs border before last-mile delivery. Both B2C marketplace orders and SME-run web-stores shipping into ASEAN are included; limited B2B flows handled through the same parcel channels are also captured as they share identical fulfilment economics.

Scope exclusion: digital-only products, domestic e-commerce, and bulk freight forwarding fall outside this analysis.

Segmentation Overview

-

By Business Model

- B2C

- B2B

-

By Product Category

- Fashion and Apparel

- Consumer Electronics

- Home Appliances

- Furniture

- Beauty and Personal Care

- Toys, Food and Others

- Others

-

By Sales Channel

- Online Marketplaces

- Direct-to-Consumer (Webstores)

- Social Commerce (Live, Chat)

-

By Country

- Indonesia

- Thailand

- Vietnam

- Philippines

- Malaysia

- Singapore

- Rest of Southeast Asia

Detailed Research Methodology and Data Validation

Primary Research

Interviews were held with third-party logistics leads, payment aggregators, and high-volume merchants in Indonesia, Thailand, Vietnam, and Singapore. Short form surveys with cross-border shoppers and sellers clarified average basket values, return ratios, and the share of purchases routed through bonded warehouses. Insights from these conversations helped us fine-tune duty-threshold effects and reconcile secondary signals.

Desk Research

We began by mapping trade and consumer demand using open datasets such as the UN Comtrade mirror exports, ASEANstats customs releases, Singapore IMDA e-payments dashboards, and Indonesia's Directorate-General of Customs import filings. Analyst teams enriched these with shopper behavior surveys from agencies like Google, Bain, and Temasek, card-scheme charge-volume reports, and marketplace disclosures lodged in SEC 20-F filings. Subscription resources, including D&B Hoovers for merchant revenues and Dow Jones Factiva for deal flow, were tapped to benchmark seller scale and investment run-rates. The sources cited illustrate the breadth consulted; many others guided gap checks and iterative validation.

Market-Sizing & Forecasting

The top-down model starts with recorded import parcel counts and declared values reported by customs, which are then adjusted for under-declaration using interview-based discount factors. Results are corroborated with a selective bottom-up roll-up of major marketplace GMV and sampled average selling price multiplied by parcel volumes obtained from shipping consolidators. Key variables feeding the model include smartphone penetration, digital-wallet share of online payments, de-minimis duty limits, average customs clearance time, and the live-commerce GMV mix. A multivariate regression links these drivers to historical cross-border value and produces the base forecast that is stress-tested under moderate and high-tariff scenarios. Assumed data gaps, chiefly in informal re-shipper volumes, are bridged through proxy indicators such as small-packet air cargo weight.

Data Validation & Update Cycle

Outputs pass a two-stage peer review, variance thresholds trigger re-checks against new marketplace disclosures, and anomalous swings prompt a callback to key experts. Models are refreshed annually; material events, such as policy shifts or major platform M&A, initiate an interim update before client delivery.

Why Mordor's Southeast Asia Cross-Border E-Commerce Baseline Commands Reliability

Published estimates often diverge because firms choose dissimilar product scopes, treat marketplace fees differently, or refresh data on uneven cadences.

Key gap drivers include our inclusion of low-value B2B parcels, adjustment for under-declared customs values, and yearly refresh, whereas others may rely on shopper-intent surveys or broader retail GMV.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 45.39 billion (2025) | Mordor Intelligence | |

| USD 13.5 billion (2023) | Regional Consultancy A | Counts only B2C marketplace parcels; excludes web-store exports |

| USD 17 billion (2025) | Global Consultancy A | Omits SME B2B flows and applies static FX rates |

| USD 50 billion (2025) | Industry Journal B | Blends domestic GMV with cross-border and relies on respondent self-reporting |

The comparison shows that figures shrink when narrower scopes are applied and balloon when domestic sales creep in. By anchoring the baseline to traceable customs evidence and then tempering it with marketplace and interview checks, Mordor Intelligence delivers a balanced, decision-ready starting point for strategy teams seeking dependable numbers.

Key Questions Answered in the Report

What is the current size of the Southeast Asia cross-border e-commerce market in 2026?

It is valued at USD 50.37 billion in 2026.

How fast is the Southeast Asia cross-border e-commerce market expected to grow?

The market is forecast to register a 10.97% CAGR, reaching USD 84.74 billion by 2031.

Which business model leads the market today?

B2C transactions dominate with a 78.12% share of 2025 revenue.

Which sales channel is growing the fastest?

Social commerce, powered by live-stream and video-commerce formats, is advancing at a 19.74% CAGR through 2031.

Why is Vietnam considered the fastest-growing country market?

Strong manufacturing capacity, supportive trade agreements, and high mobile-commerce adoption propel Vietnam to an 11.08% CAGR.

What logistical innovation is cutting delivery times within ASEAN?

Bonded-warehouse hubs combined with the ASEAN Customs Transit System now trim delivery to under three days for intra-regional orders.

Page last updated on: