United States Cross-Border E-Commerce Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

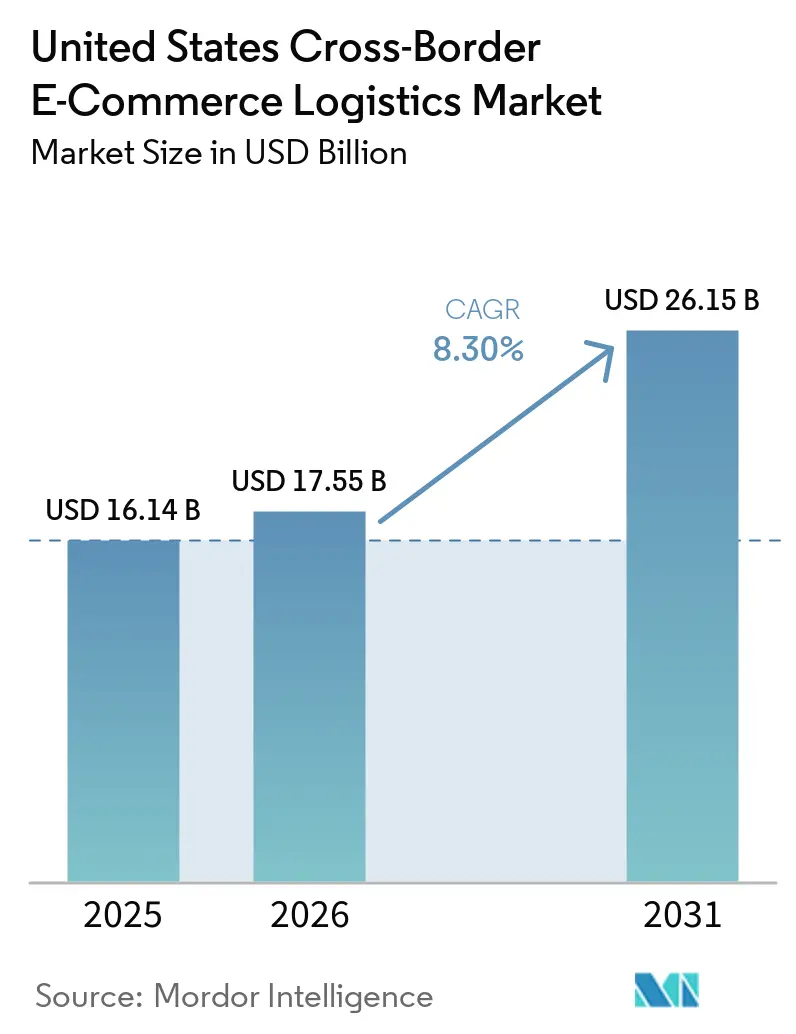

| Base Year Market Size (2025) | USD 16.14 Billion |

| Market Size (2026) | USD 17.55 Billion |

| Market Size (2031) | USD 26.15 Billion |

| Growth Rate (2026 - 2031) | 8.30% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Cross-Border E-Commerce Logistics Market Analysis by Mordor Intelligence

The United States cross-border e-commerce logistics market was valued at USD 16.14 billion in 2025 and is estimated to grow from USD 17.55 billion in 2026 to reach USD 26.15 billion by 2031, at a CAGR of 8.30% during the forecast period from 2026 to 2031.

The United States retail e-commerce sales reached USD 326.7 billion in Q1 2026, up 9.8% year over year, which confirms that transaction volume remains strong enough to keep cross-border routing, customs handling, and international delivery networks under sustained pressure. The United States cross-border e-commerce logistics market is being shaped by two forces at the same time, faster supplier response from nearshored production and broader outbound selling by US brands through large marketplace ecosystems. The suspension of de minimis treatment from August 29, 2025, did not remove demand from the United States cross-border e-commerce logistics market, but it did push parcel flows into more documentation-heavy and duty-paid channels that require greater spending on brokerage, bonded inventory, and returns control. That shift is also changing competition in the United States cross-border e-commerce logistics market, because providers with customs technology, bonded facilities, and marketplace integrations are in a better position than operators that depend mainly on low-cost parcel movement.

Key Report Takeaways

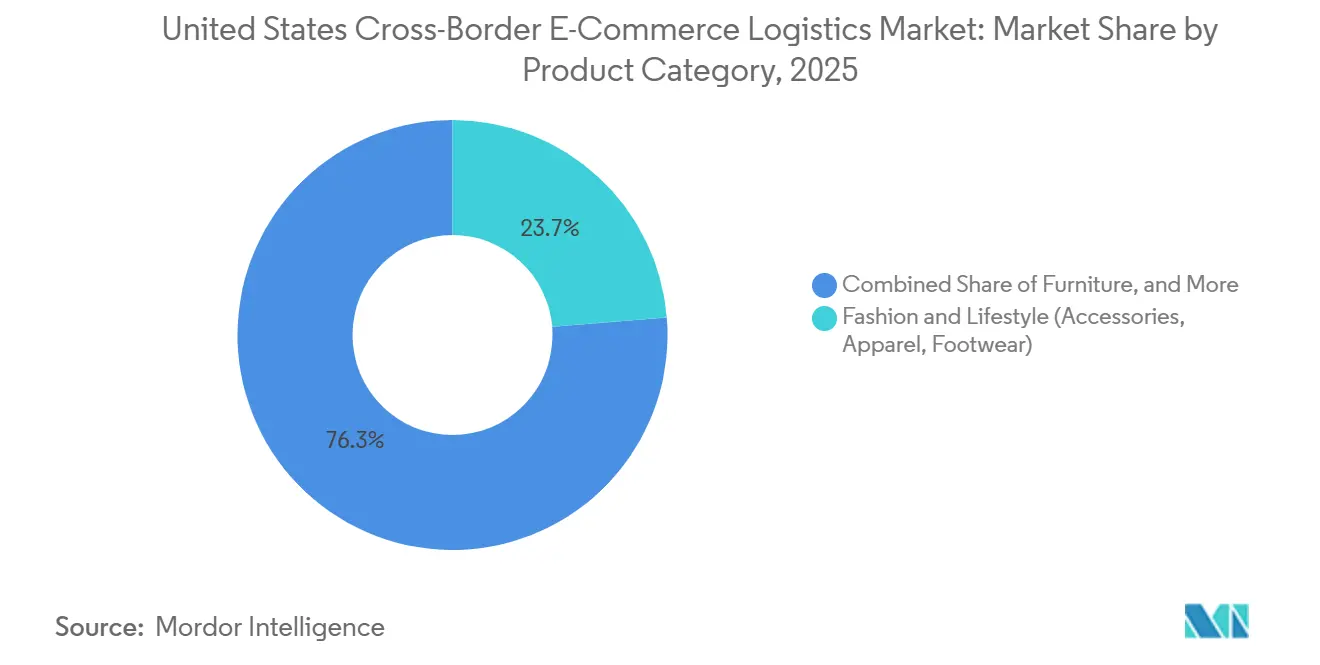

- By product category, fashion and lifestyle held 23.65% of the United States cross-border e-commerce market share in 2025, while personal and household care is projected to expand at a 9.29% CAGR through 2031.

- By logistics function, transportation accounted for 68.39% of the United States cross-border e-commerce market size in 2025, while value-added services and others are forecast to grow at a 13.48% CAGR through 2031.

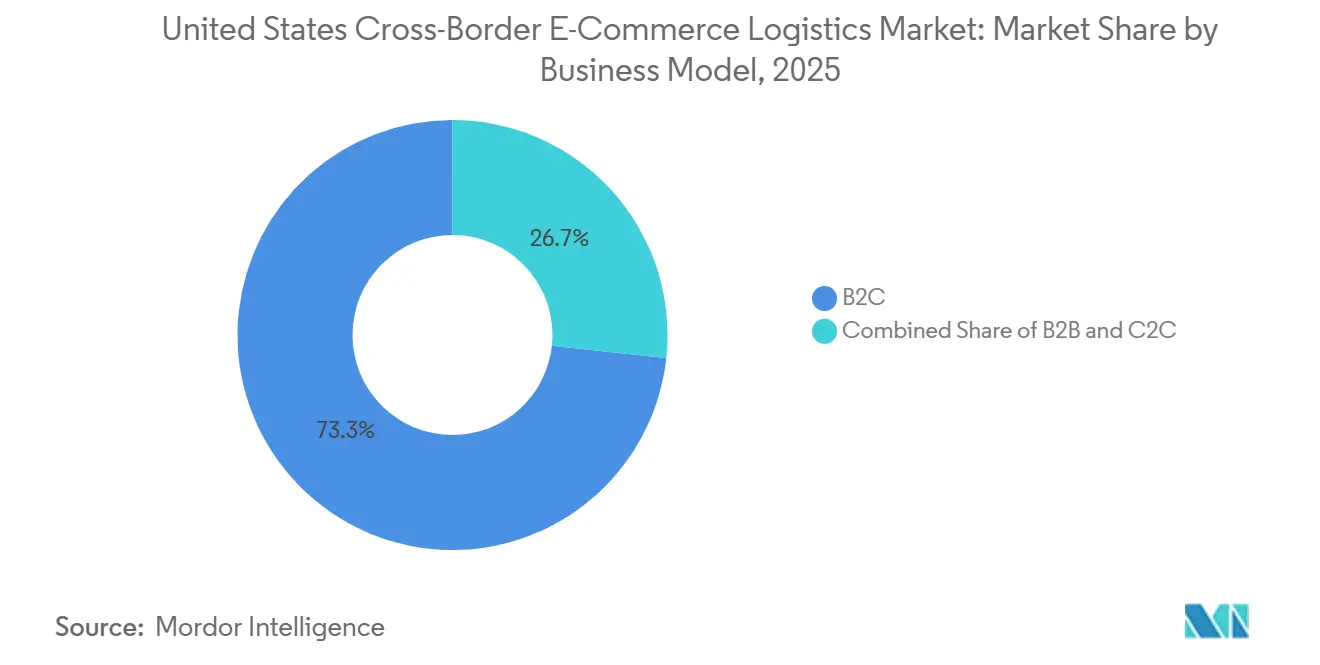

- By business model, B2C held 73.30% of the United States cross-border e-commerce logistics market share in 2025, while C2C recorded the highest projected CAGR at 16.65% through 2031.

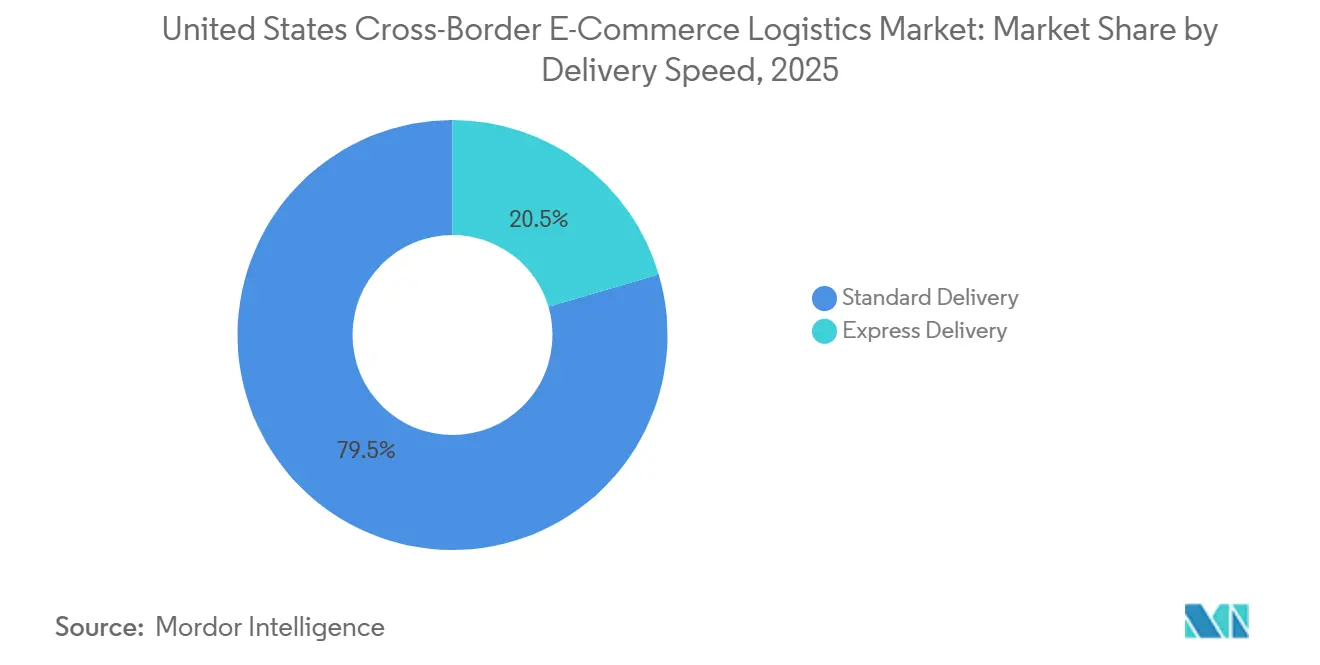

- By delivery speed, standard delivery retained 79.54% of the United States cross-border e-commerce logistics market share in 2025, while express delivery is projected to advance at an 11.33% CAGR through 2031.

- By flow direction, inbound flows represented 68.00% of the United States cross-border e-commerce logistics market size in 2025, while outbound flows are projected to grow at a 9.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Cross-Border E-Commerce Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Marketplace-led International Selling Expansion | +2.1% | Global, core impact on US outbound to APAC, Europe, and Canada | Medium term (2-4 years) |

| AI-enabled Logistics Visibility and Customs Orchestration | +1.3% | Global, highest adoption on US-China and transatlantic lanes | Short term (≤ 2 years) |

| USMCA-enabled North American Corridor Optimization | +1.0% | North America, US-Mexico and US-Canada | Medium term (2-4 years) |

| Delivery-speed Visibility and Checkout Transparency Expectations | +0.8% | Global, concentrated in consumer-facing B2C markets | Short term (≤ 2 years) |

| DDP Checkout and Landed-cost Visibility Adoption | +0.7% | US outbound to Europe and APAC, US inbound from all origins | Short term (≤ 2 years) |

| Shift Toward US-based Bonded and FTZ Inventory Positioning | +0.5% | US national, early gains in Laredo, El Paso, Los Angeles, and Dallas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Marketplace-Led International Selling Expansion

Marketplace platforms are expanding access to overseas demand, giving the United States cross-border e-commerce logistics market a broader outbound base than it had when cross-border selling was limited to large merchants. Amazon opened Amazon Supply Chain Services on May 4, 2026, and made its freight, distribution, fulfillment, and parcel network available to businesses across industries, which marks one of the largest platform-led entries into the logistics stack tied to online commerce. Amazon said the network behind this offer includes more than 100 aircraft, more than 24,000 intermodal containers, and customs clearance capability, which means the platform is now competing more directly with established integrators and freight providers for cross-border flows[1]“Understanding eCommerce Marketplaces,” International Trade Administration, U.S. Department of Commerce, trade.gov. This matters for the United States cross-border e-commerce logistics market because customs, delivery, and fulfillment tools are moving closer to the point of sale, and merchants can add international channels without building a full internal trade compliance team. The result is that the United States cross-border e-commerce logistics market is capturing more export activity from brands that once treated foreign sales as too complex or too expensive to manage. It also reinforces the faster growth outlook for outbound flows, because marketplace-linked selling lowers the operational barrier between digital demand and physical shipment creation.

AI-Enabled Logistics Visibility and Customs Orchestration

AI tools are becoming more central to the United States' cross-border e-commerce logistics market because customs work, routing decisions, and disruption handling now require greater speed and consistency than manual processes can provide. Maersk launched Trade & Tariff Studio on June 25, 2025, and said the system applies AI across more than 6,000 product codes and 20,000 sub-codes with live input from more than 2,700 customs experts, which shows how classification and tariff analysis are moving into structured digital workflows. Maersk also stated that 20% of shipments are delayed by inadequate customs preparation, underscoring why merchants are placing greater value on providers that can reduce document errors before cargo reaches the border. project44 launched Autopilot on May 11, 2026, and said the platform processes more than 700 million logistics events daily across 259,000 carriers in 186 countries, with documented outcomes that included a 4% reduction in freight spend and up to 40% lower disruption-related costs. In the United States cross-border e-commerce logistics market, that kind of event visibility helps smaller merchants gain access to shipment intelligence that was once concentrated among larger enterprises. It also supports the growth of value-added services, because the commercial advantage is shifting from pure transport capacity toward better exception management, duty calculation, and customs readiness.

USMCA-Enabled North American Corridor Optimization

The North American lane remains one of the strongest growth engines for the United States cross-border e-commerce logistics market because it combines large freight density, shorter transit times, and a policy framework that still rewards regional sourcing and distribution. The Bureau of Transportation Statistics reported that the United States freight with Canada and Mexico reached a record USD 144.8 billion in March 2025, and that trucks carried the majority of land-border surface trade, underscoring the importance of road-linked fulfillment for regional e-commerce flows. Texas A&M International University reported that the Laredo gateway processed USD 340 billion in trade in 2024, confirming that a single corridor already carries a very large share of North American cross-border trade. C.H. Robinson said the first formal USMCA review in 2026 creates both opportunity and transition risk, because rules of origin and corridor economics will remain central to routing and sourcing decisions. That matters for the United States cross-border e-commerce logistics market because merchants and logistics providers are using Mexico and Canada not only as final destinations, but also as distribution extensions tied to nearshoring, bonded inventory, and faster replenishment. As that corridor becomes more valuable, providers with strong customs support, road capacity access, and regional warehouse positioning should continue to gain ground[2]“March 2025 Marks Record in Value of U.S. Freight with Canada and Mexico,” U.S. Department of Transportation, bts.gov.

Delivery-Speed Visibility and Checkout Transparency Expectations

Service promises have become stricter in the United States cross-border e-commerce logistics market, and buyers increasingly expect to see delivery windows and full landed costs before they commit to an order. This is one reason the United States cross-border e-commerce logistics market is seeing faster growth in Express services than in Standard services, because premium buyers are paying for predictability as much as for speed. ePost Global said that duty-paid orders reduce the surprise costs that often trigger refused deliveries and return flows, making transparent checkout and DDP execution more valuable for merchants that sell higher-value products across borders. The commercial effect is strongest in categories where average order values are high enough to absorb premium shipping, but the margin loss from refusal or return is even higher. The United States cross-border e-commerce logistics market is, therefore, rewarding providers that can offer a single integrated service covering duties, delivery estimates, and parcel tracking from checkout to final handoff. This also explains why DDP checkout and landed-cost visibility are moving from optional features into core service requirements in both inbound and outbound e-commerce lanes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| De Minimis Rollback and Tariff Stacking | -2.1% | Global, most acute on US inbound from China, ASEAN, and Europe | Short term (≤ 2 years) |

| Regulatory Complexity for Regulated and Battery-linked Categories | -0.8% | Global, concentrated on US inbound from China and APAC via air freight | Medium term (2-4 years) |

| UFLPA-origin Traceability Burden on Low-value Parcels | -0.5% | US inbound from China, with extension risk to ASEAN transshipment routes | Medium term (2-4 years) |

| Duty-paid Returns and Refused-delivery Friction | -0.4% | US inbound and outbound, with high friction in EU, Canada, and MEA markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

De Minimis Rollback and Tariff Stacking

The largest near-term restraint on the United States cross-border e-commerce logistics market is the rollback of de minimis treatment, because it changes the operating model for a very large parcel base. The White House stated that the suspension, effective August 29, 2025, removed duty-free treatment for low-value commercial shipments globally, which ended the main cost pathway that had supported direct parcel flows under the USD 800 threshold. The United States Customs and Border Protection said every e-commerce shipment still has to meet the applicable entry and compliance requirements, and the agency’s guidance now places more weight on accurate classification, declared value, and entry processing than the prior low-friction parcel model did. The White House also noted that more than 1.36 billion de minimis shipments entered the United States in 2024, which shows the scale of the operational reset now being absorbed by merchants, carriers, and brokers. In the United States cross-border e-commerce logistics market, this does not remove demand, but it does raise the documentation, customs labor, and landed-cost burden tied to each parcel. It also strengthens the case for bonded warehousing, FTZ inventory positioning, and logistics networks capable of formal entry, because merchants now need more controlled ways to manage duty exposure and delivery certainty.

Regulatory Complexity for Regulated and Battery-Linked Categories

Battery-linked goods are becoming a larger operational constraint on the United States cross-border e-commerce logistics market, especially on air lanes from Asia, where electronics and connected devices are common. IATA’s 66th edition Dangerous Goods Regulations, effective in 2025, recommended a 30% state of charge limit for lithium-ion batteries in air shipments and expanded the framework for a wider range of battery classifications. The same regulatory tightening extends further in 2026 for batteries above 2.7Wh, meaning handling requirements are becoming stricter just as merchants are seeking faster alternatives to older, low-value parcel channels. In the United States cross-border e-commerce logistics market, this adds processing steps before export, increases handling discipline inside fulfillment centers, and limits the ease with which sellers can shift goods from postal to premium air services. The effect is especially important for consumer electronics, power tools, e-bikes, and connected devices, because the products combine strong e-commerce demand with compliance-sensitive transport conditions. This does not stop cross-border demand in those categories, but it does favor providers with tested battery-handling procedures, multimodal options, and better customs document preparation[3]“Lithium Batteries, Dangerous Goods Regulations 66th Edition,” IATA, iata.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Fashion Leads Volume, Personal Care Builds Momentum

Fashion and Lifestyle accounted for 23.65% of the United States cross-border e-commerce logistics market size in 2025, making it the largest revenue contributor. That lead came from a mix of high-frequency inbound apparel and accessories from Asian production hubs and outbound luxury and lifestyle shipments from US brands to buyers in Asia-Pacific and the Middle East. The segment remains strong because classification workflows, return handling, and parcel routing are already well established compared with more regulated product groups. In the United States cross-border e-commerce logistics market, fashion and lifestyle still benefit from repeat purchase behavior and a broad merchant base that ranges from global labels to smaller marketplace sellers. The maturity of the lane also means providers compete less on basic movement and more on delivery speed, prepaid duty options, and return control.

Personal and household Care is projected to grow at a 9.29% CAGR through 2031, which gives it the strongest momentum among product categories in the United States cross-border e-commerce logistics market. This part of the United States cross-border e-commerce logistics industry is benefiting from demand for specialty wellness items, prestige beauty products, and health-related goods that are not always easy to source through domestic channels alone. The shift suggests that future share gains will come from categories with higher value density and tighter handling needs rather than only from apparel volume. Consumer electronics and household appliances still account for meaningful inbound demand, but the battery rules on air shipments are increasing execution complexity for providers that serve those lanes. Foods and beverages and furniture remain part of the United States cross-border e-commerce logistics market, but their growth is held back by perishability on one side and dimensional weight economics on the other, which makes provider specialization more important than simple parcel scale.

By Logistics Function: Transport Anchors Revenue, Value-Add Commands Margin

Transportation accounted for 68.39% of the United States cross-border e-commerce logistics market share in 2025, reflecting the cost-weighted share of air, ocean, road, and rail movements across international lanes. This lead is especially visible on North American corridors, where road transport remains central to regional trade and rapid replenishment. The United States cross-border e-commerce logistics market still relies on transport capacity as its largest revenue pool, but the margin profile of the business is changing as compliance demands rise. Warehousing, distribution, and inventory management remain the next major functions because merchants need better control over landed cost timing, inventory release, and returns routing after the de minimis rollback. Bonded and FTZ facilities are becoming more relevant in the United States cross-border e-commerce logistics market because they allow duty deferral and more flexible release planning in a trade environment with higher documentation pressure.

Value-added services and others is projected to grow at a 13.48% CAGR through 2031, making it the fastest-expanding function in the United States cross-border e-commerce logistics market. That growth reflects rising demand for DDP management, customs brokerage, returns handling, classification support, and merchant-facing visibility tools rather than only more trucks or more aircraft. SEKO Logistics launched DutyPay in May 2025 to improve customs compliance and clearance execution, which shows how service providers are formalizing duty and entry workflows that used to be handled in a more fragmented way. Maersk and project44 have also expanded the technology layer around tariff and event management, which supports the move toward software-enabled value-added offerings inside the United States cross-border e-commerce logistics market. The result is a market where transportation still anchors revenue, but compliance intelligence and digital control are capturing a larger share of commercial value.

By Business Model: B2C Dominates, Platform Marketplaces Fuel C2C Surge

B2C held 73.30% of the United States cross-border e-commerce logistics market share in 2025, which makes it the dominant business model across both import and export flows. The scale of this segment comes from DTC brands, retail marketplaces, and merchant storefronts that move products to end consumers in parcelized formats across many destination countries. In the United States cross-border e-commerce logistics market, B2C remains the core volume base because consumer-oriented order density is still much larger than peer-to-peer or trade-oriented shipment counts. At the same time, the economics of B2C have shifted, as parcels that once benefited from duty-free treatment now require full duty payment and stricter documentation requirements. That means the leading providers in the United States cross-border e-commerce logistics market are the ones that can combine checkout, duty collection, customs filing, parcel visibility, and returns execution in one operating flow.

C2C is projected to grow at a 16.65% CAGR through 2031, making it the fastest-growing business model in the United States cross-border e-commerce logistics market. Resale platforms, authenticated luxury channels, and social commerce are expanding the pool of sellers who need commercial-grade logistics support, even if they are not conventional retailers. This part of the United States cross-border e-commerce logistics industry grows quickly because peer-to-peer cross-border transactions still need the same core services, accurate classification, prepaid duties, and dependable final-mile delivery. B2B remains smaller in parcel count but important in shipment value, because higher-entry commercial formats become more relevant as merchants move away from the old low-value parcel structure after the de minimis change. This mix leaves the United States cross-border e-commerce logistics market with a stable consumer core, a faster-growing peer-to-peer layer, and a denser commercial entry layer that favors providers with strong brokerage capability[4]“E-Commerce Frequently Asked Questions,” U.S. Customs and Border Protection, cbp.gov.

By Delivery Speed: Standard Anchors Volumes, Express Commands Margins

Standard delivery retained 79.54% of the United States cross-border e-commerce logistics market share in 2025, keeping it the largest speed tier in the market. Its lead reflects merchant cost discipline across dense inbound lanes from Asia Pacific and Mexico, where many buyers still accept longer cross-border transit windows in exchange for lower shipping charges. Standard services also work well in categories with high purchase frequency and order values that are not large enough to cover a premium delivery fee. In the United States cross-border e-commerce logistics market, this keeps Standard relevant even as policy changes and service expectations raise the value of faster options. The segment remains important because most cross-border volume still needs economically viable routing before it needs premium speed.

Express delivery is projected to grow at a 11.33% CAGR through 2031, making it the fastest-growing segment in the United States cross-border e-commerce logistics market. Merchants are upgrading selected shipments to Express not only to meet consumer expectations, but also to reduce refused deliveries and reverse logistics costs for higher-value goods. Nippon Express launched NX Ocean Fast Track on June 5, 2026 to offer transit times between standard ocean and air on Asia to North America routes, which shows how providers are actively redesigning the middle ground between lower-cost and higher-speed transport. That development matters because part of the United States cross-border e-commerce logistics market is now being shaped by products that need better speed certainty without paying for full air freight. The result is a delivery-speed mix where standard still carries most volume, but express and near-express services capture more of the revenue and merchant attention.

By Flow Direction: Import Flows Anchor the Market, Export Corridors Accelerate

Inbound flows accounted for 68.00% of the United States cross-border e-commerce logistics market size in 2025, making imports the largest direction. This reflects the United States' position as a large consumer destination for goods shipped from China, ASEAN, Mexico, Canada, and Europe via parcel and freight channels. The scale of inbound activity is also supported by the regional freight base, with trade between the United States, Canada, and Mexico reaching a record monthly value in March 2025. In the United States cross-border e-commerce logistics market, import-heavy flows still shape network design, bonded storage needs, and customs brokerage demand more than outbound movements do. This is why providers continue to build capacity around inbound documentation, regional transport links, and better release planning at major gateways.

Outbound flows are projected to grow at a 9.29% CAGR through 2031, giving exports a faster growth profile in the United States cross-border e-commerce logistics market. The main reason is that more US brands can now reach foreign buyers through marketplace channels and integrated logistics services without creating large in-house compliance teams. Canada and Mexico remain the most practical export extensions because they combine geographic proximity with established trade processes, while Europe and parts of Asia Pacific continue to attract premium United States brand demand. As outbound tools improve, the United States cross-border e-commerce logistics market is becoming less dependent on import growth alone and more balanced between inbound consumer demand and outbound brand expansion.

Geography Analysis

North America remained the most important operating geography for the US cross-border e-commerce logistics market in 2025 because import flows held 68.00% of revenue, and the US, Canada, and US Mexico corridors carried the heaviest regional ground movement. The Bureau of Transportation Statistics reported a record USD 144.8 billion in freight trade between the United States and Canada and Mexico in March 2025, confirming the scale of the corridor that underpins regional e-commerce replenishment and parcel injection. The same agency reported that trucks moved USD 67.5 billion of freight with Canada that month, underscoring the centrality of road-linked services to cross-border execution. Texas A&M International University reported that Laredo processed USD 340 billion in trade in 2024, reinforcing the corridor’s role as the network's highest-density logistics gateway. In the United States cross-border e-commerce logistics market, this concentration supports greater investment in brokerage, bonded storage, and regional linehaul capacity, as merchants need fast, repeatable movement across land borders.

Asia Pacific remains the dominant origin for inbound parcel and freight activity in the US cross-border e-commerce logistics market, and its role is becoming increasingly complex. FedEx expanded its Taiwan Transshipment Center in March 2026 and said the facility can sort 9,000 packages per hour, which signals a direct infrastructure bet on Asia Pacific linked e-commerce and supply chain growth. The region also faces more handling sensitivity because battery-linked products are common on these lanes, and IATA’s updated dangerous goods rules are tightening air shipment requirements. Europe remains important to the United States cross-border e-commerce logistics market as both an inbound source of premium goods and an outbound destination for the United States brands that need predictable duties and delivery standards. Its relative advantage is service maturity, because merchants and logistics providers on transatlantic lanes are more likely to treat prepaid duties, tracked delivery, and managed returns as standard operating requirements.

The Middle East and Africa and South America represent smaller but potentially faster-expanding outbound spaces for the United States cross-border e-commerce logistics market through 2031. These corridors start from a lower base, but they benefit when US brands use marketplace and managed logistics tools to enter destinations beyond the first wave of English-language markets. The United States cross-border e-commerce logistics market is likely to approach these regions selectively, focusing on cities and lanes where payment acceptance, customs predictability, and premium brand demand are already established. That means future gains in these regions will depend less on raw parcel scale and more on whether providers can offer DDP execution, reliable transit visibility, and controlled returns at a reasonable cost.

Competitive Landscape

The United States cross-border e-commerce logistics market is moderately concentrated at the network layer, with DHL, FedEx, UPS, Kuehne+Nagel, Maersk, DSV, SEKO, Flexport, Global-e, Passport, and Zonos competing across different parts of the merchant-to-customs workflow. The largest global operators still hold an advantage in the US cross-border e-commerce logistics market because they combine international transport assets, brokerage reach, and warehouse infrastructure across several continents. DSV strengthened its position after the Schenker transaction, and the company said it targets DKK 9 billion in annual synergies with full financial impact expected in 2027, which shows the scale at which global forwarding competition is being rebuilt. Amazon raised the competitive pressure further when it opened Amazon Supply Chain Services to businesses outside its own marketplace in May 2026, because that move gives merchants access to freight, fulfillment, and parcel delivery within one large operating environment. In the United States cross-border e-commerce logistics market, this kind of platform entry matters because it combines transaction data, demand visibility, and logistics execution in a way that few incumbents can fully match.

Technology and compliance capability are becoming as important as transport scale in the US cross-border e-commerce logistics market. Maersk’s Trade & Tariff Studio and project44’s Autopilot reflect a wider move toward software-led customs preparation, tariff analysis, and shipment-event control. SEKO’s DutyPay platform shows the same pattern from a brokerage and compliance angle, where merchants need a more formal way to manage duties and entries after the de minimis change. This is why the United States cross-border e-commerce logistics market is no longer defined only by who can move parcels fastest, but also by who can reduce customs friction, prevent checkout surprises, and handle returns with less margin loss. Specialists such as Global-e, Passport, and Zonos continue to matter because they focus on checkout localization, duty calculation, and merchant workflow integration rather than on fleet scale alone.

The clearest opening in the United States cross-border e-commerce logistics market sits in the mid-market merchant group that is too large for manual shipping administration and too small for fully customized enterprise contracts. These merchants need bonded inventory options, formal customs support, and flexible multi-carrier execution without taking on the cost structure of a large multinational shipper. CBP’s e-commerce guidance and the wider post-de minimis operating model are making those capabilities more necessary in 2026, not less. Providers that can combine customs orchestration, inventory positioning near ports, and merchant-facing visibility should be best placed to capture this part of the market as the compliance burden continues to rise.

United States Cross-Border E-Commerce Logistics Industry Leaders

United Parcel Service of America, Inc. (UPS)

FedEx

DHL Group

Amazon, Inc.

Kuehne+Nagel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Nippon Express (NX Group) launched NX Ocean Fast Track on June 5, 2026, a new Asia-to-North America sea freight service on Tokyo, Shanghai, Haiphong to Los Angeles routes. The service delivers transit times between standard ocean and air, targeting e-commerce and high-tech cargo requiring speed without the full air freight cost premium, with container discharge from vessel targeted within 24 hours of US arrival.

- May 2026: Amazon launched Amazon Supply Chain Services, opening its entire logistics infrastructure, freight, distribution, fulfillment, and parcel delivery to businesses of all sizes and industries beyond the Amazon marketplace.

- May 2026: project44 launched Autopilot, a no-code AI agent deployment platform for supply chain teams, built on 18 months of production AI agent deployment. Documented outcomes include a 4% reduction in freight spend, a 70% reduction in manual coordination, and up to a 40% reduction in disruption-related costs.

- May 2026: DHL eCommerce Solutions and Flexport announced a deep technical integration connecting Flexport's freight-forwarding and customs clearance infrastructure directly to DHL's last-mile carrier network across 45 countries, with a unified dashboard for Shopify, BigCommerce, and WooCommerce merchants. The integration entered open beta for US-based merchants with general availability expected in Q3 2026.

United States Cross-Border E-Commerce Logistics Market Report Scope

| Foods and Beverages |

| Personal and Household Care |

| Fashion and Lifestyle (Accessories, Apparel, Footwear) |

| Furniture |

| Consumer Electronics and Household Appliances |

| Other Products |

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing, Distribution and Inventory Management | |

| Value-added Services and Others |

| B2C |

| B2B |

| C2C |

| Express |

| Standard |

| Outbound (Exports) | Canada |

| Mexico | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa | |

| South America | |

| Inbound (Imports) | Canada |

| Mexico | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa | |

| South America |

| By Product Category | Foods and Beverages | |

| Personal and Household Care | ||

| Fashion and Lifestyle (Accessories, Apparel, Footwear) | ||

| Furniture | ||

| Consumer Electronics and Household Appliances | ||

| Other Products | ||

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing, Distribution and Inventory Management | ||

| Value-added Services and Others | ||

| By Business Model | B2C | |

| B2B | ||

| C2C | ||

| By Delivery Speed | Express | |

| Standard | ||

| By Flow Direction | Outbound (Exports) | Canada |

| Mexico | ||

| Europe | ||

| Asia-Pacific | ||

| Middle East and Africa | ||

| South America | ||

| Inbound (Imports) | Canada | |

| Mexico | ||

| Europe | ||

| Asia-Pacific | ||

| Middle East and Africa | ||

| South America | ||

Key Questions Answered in the Report

What is the size of the United States cross-border e-commerce logistics sector in 2026?

The United States cross-border e-commerce logistics market is estimated at USD 17.55 billion in 2026 and is projected to reach USD 26.15 billion by 2031 at an 8.30% CAGR.

Which product category leads revenue in this space?

Fashion and lifestyle led with a 23.65% share in 2025, supported by strong inbound apparel volumes and stable outbound luxury and lifestyle flows.

Which business model is growing the fastest?

C2C is projected to grow at a 16.65% CAGR through 2031, driven by resale, authenticated luxury transactions, and social commerce-linked cross-border shipments.

Why did compliance become more important after 2025?

The August 2025 de minimis suspension increased the need for full duty payment, entry processing, and stronger customs documentation for low-value shipments.

Which logistics function has the fastest growth outlook?

Value-added services and others is forecast to grow at a 13.48% CAGR through 2031 because merchants now need more duty management, customs support, and returns processing.

Why is Express delivery gaining share even though Standard still leads volume?

Express is projected to grow at 11.33% CAGR because buyers want predictable delivery windows, and merchants use duty-paid faster services to reduce refusals and reverse logistics costs.

Page last updated on: