GCC Cross-Border E-commerce Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

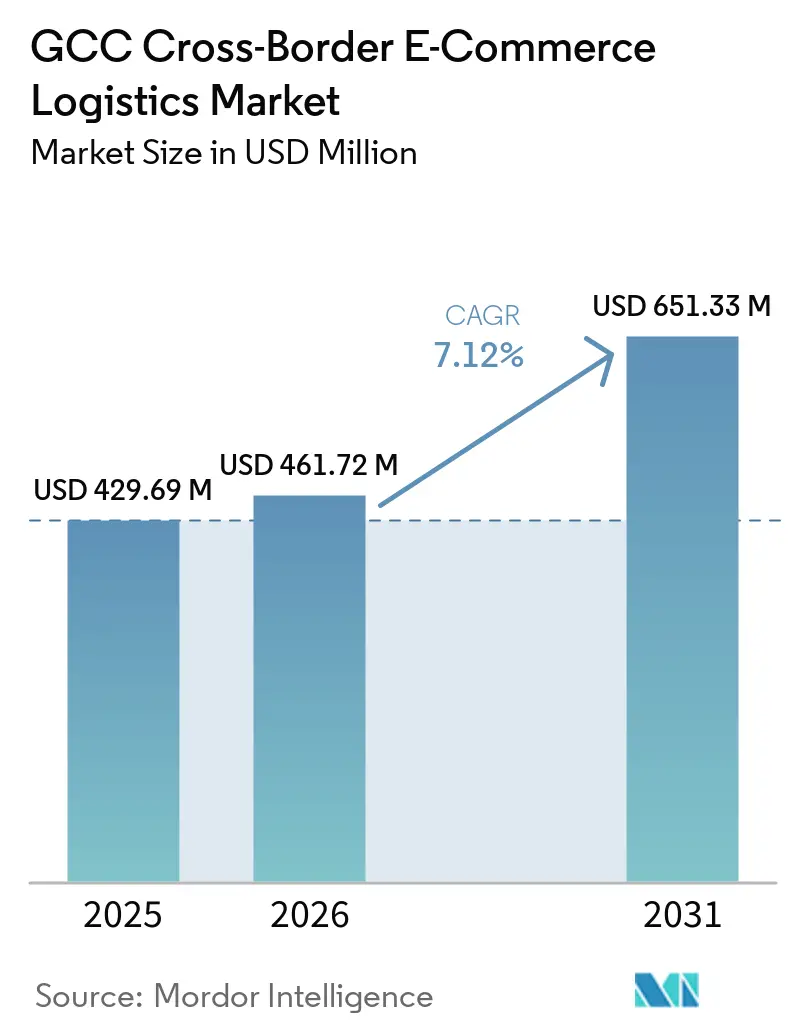

| Base Year Market Size (2025) | USD 429.69 Million |

| Market Size (2026) | USD 461.72 Million |

| Market Size (2031) | USD 651.33 Million |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GCC Cross-Border E-commerce Logistics Market Analysis by Mordor Intelligence

The GCC Cross-Border E-commerce Logistics Market size is expected to increase from USD 429.69 million in 2025 to USD 461.72 million in 2026 and reach USD 651.33 million by 2031, growing at a CAGR of 7.12% over 2026-2031.

The GCC Cross-Border E-commerce Logistics Market is expanding on the back of high digital adoption, strong consumer purchasing power, and the region’s growing role as a gateway between Asian production centers and Gulf demand centers. Inbound parcel flows still shape the revenue base because the region depends heavily on imported fashion, electronics, and personal care goods, while service standards are moving closer to domestic e-commerce benchmarks. The GCC Cross-Border E-commerce Logistics Market is also shifting toward bundled services, as merchants increasingly need customs handling, returns processing, and localized fulfillment under a single contract. Saudi Arabia remains the largest demand center for parcel consumption, while the UAE continues to serve as the main entry and redistribution hub due to its port infrastructure and free-zone ecosystem. Competitive positioning in the GCC Cross-Border E-commerce Logistics Market is now determined by network density, customs capability, and the ability to offer faster delivery without losing cost control.

Key Report Takeaways

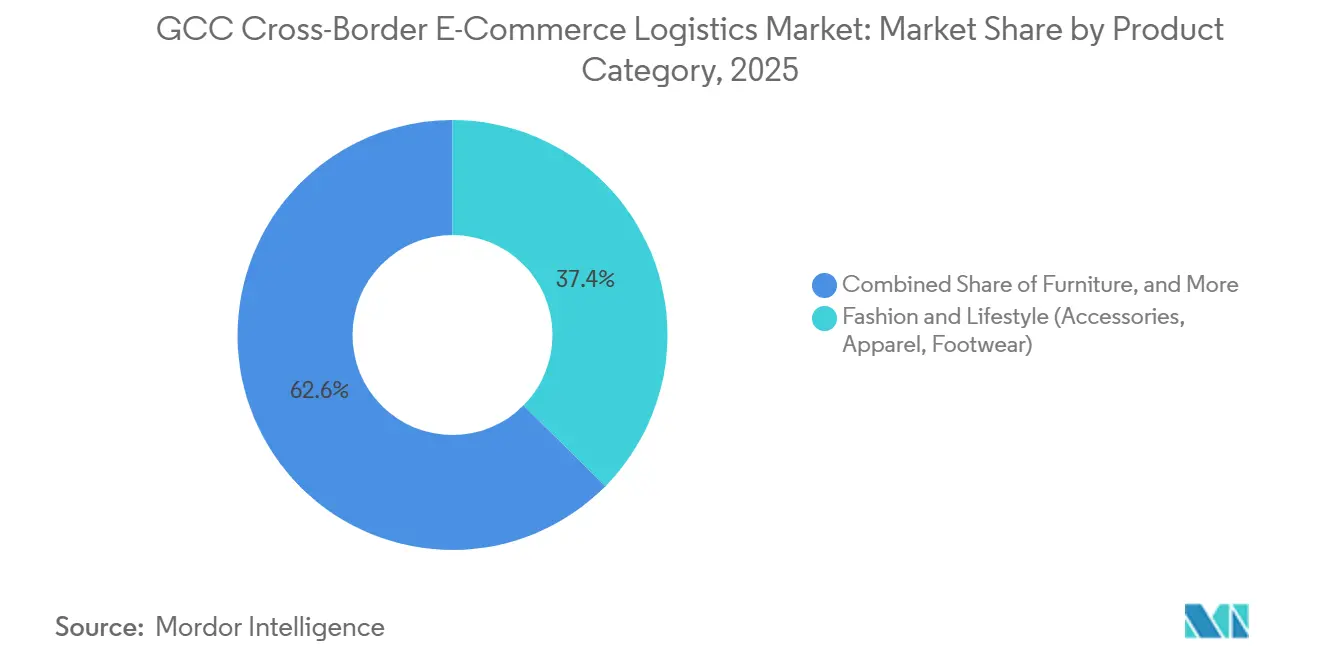

- By product category, fashion and lifestyle accounted for 37.41% of the GCC Cross-Border E-commerce Logistics Market share in 2025, while health and beauty/personal care is forecast to expand at an 8.11% CAGR through 2031.

- By logistics function, transportation accounted for 73.33% of the GCC Cross-Border E-commerce Logistics Market size in 2025, while value-added services and others are projected to grow at a 12.30% CAGR through 2031.

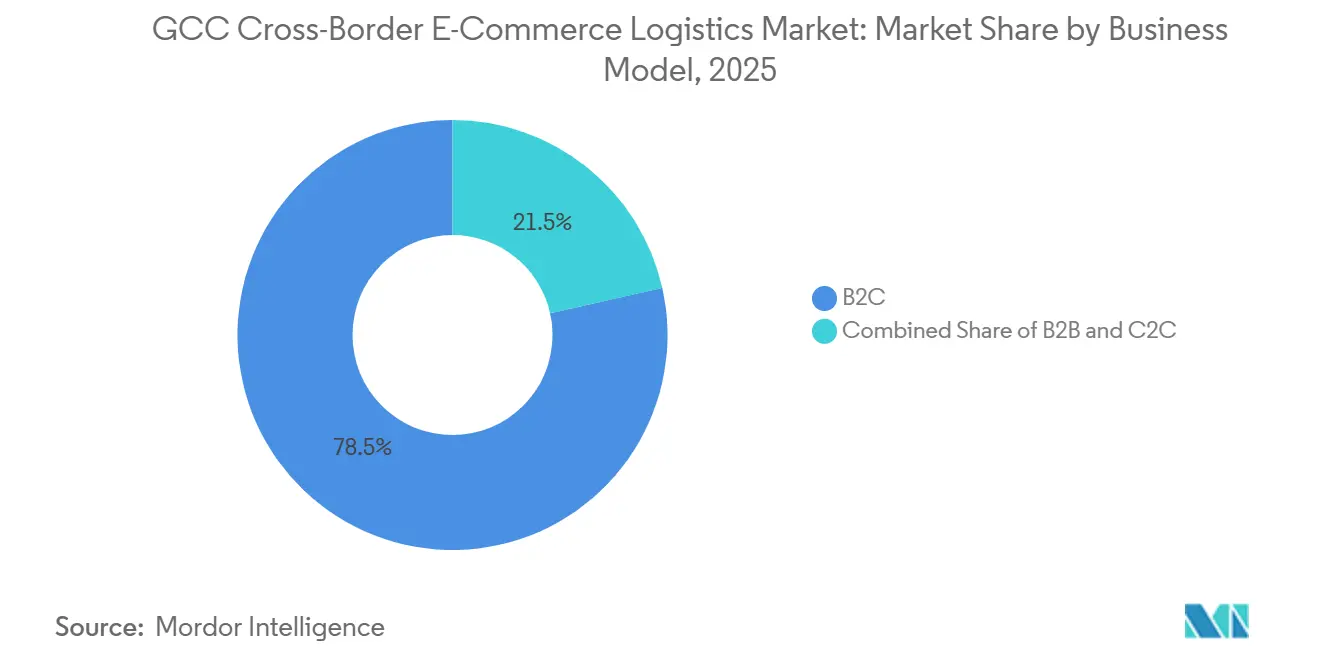

- By business model, B2C accounted for 78.50% of the GCC Cross-Border E-commerce Logistics Market share in 2025, while C2C is projected to grow at a 15.47% CAGR through 2031.

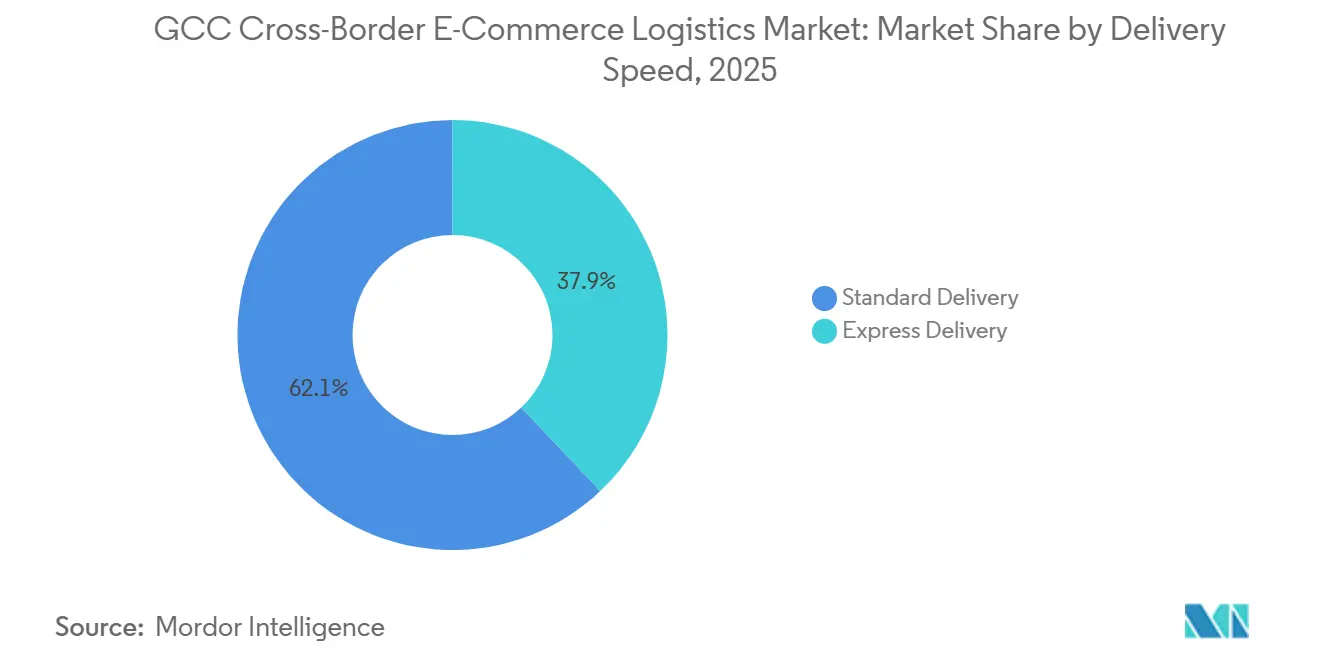

- By delivery speed, standard delivery accounted for 62.07% of the GCC Cross-Border E-commerce Logistics Market share in 2025, while express delivery is expected to grow at a 10.15% CAGR through 2031.

- By flow direction, inbound logistics accounted for 71.00% of the GCC Cross-Border E-commerce Logistics Market share in 2025, while outbound logistics is projected to expand at an 8.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

GCC Cross-Border E-commerce Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for international brands | +1.8% | Saudi Arabia, UAE core, spill-over to Kuwait, Qatar | Medium term (2-4 years) |

| Double-digit GCC e-commerce growth | +2.4% | Global, primary gains in Saudi Arabia and UAE | Short term (≤ 2 years) |

| Free zones and customs digitization | +1.5% | UAE, Saudi Arabia | Medium term (2-4 years) |

| Faster-delivery expectations | +1.2% | UAE, Saudi Arabia core urban clusters | Short term (≤ 2 years) |

| Saudi national address enforcement | +0.9% | Saudi Arabia exclusively | Short term (≤ 2 years) |

| IOR and SOR market-entry models | +1.1% | All 6 GCC states, with entry gains in UAE and Saudi Arabia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for International Brands

Demand for imported brands remains one of the clearest growth supports for the GCC Cross-Border E-commerce Logistics Market. Consumers across the Gulf continue to spend heavily on foreign apparel, cosmetics, accessories, and electronics because domestic manufacturing depth in these categories remains limited. This pattern is pushing logistics contracts beyond basic parcel movement and toward premium handling, controlled packaging, and stronger return-management capabilities[1]“Common Customs Law of the GCC States,” GCC Secretariat, gcc-sg.org.. It is also creating a broader role for operators to coordinate product compliance, especially for regulated goods that undergo import checks before release. As a result, the GCC Cross-Border E-commerce Logistics Market is earning a larger share of revenue from service complexity rather than from volume growth alone.

Double-Digit GCC E-Commerce Growth

Rapid online retail expansion continues to lift parcel volumes and support the GCC Cross-Border E-commerce Logistics Market. Seasonal demand peaks are becoming easier to forecast, which allows carriers and fulfillment operators to position inventory in advance rather than absorb demand shocks at the last minute. The growth in orders is also changing the freight mix because merchants are moving more regulated products, higher-value goods, and mixed-origin shipments that require different customs treatment. This makes customs support, bonded storage, and delivery coordination more important than simple line-haul capacity[2]“TGA: 15 Days Until National Address Requirement for Parcel Shipments,” TGA Official Website, tga.gov.sa. The GCC Cross-Border E-commerce Logistics Market, therefore, benefits not only from rising order counts but also from rising handling intensity per shipment.

Free Zones and Customs Digitization

Free-zone development and customs digitization are improving the operating environment for the GCC Cross-Border E-commerce Logistics Market. Merchants are increasingly using Gulf gateway locations to centralize inventory, reduce paperwork delays, and support multi-country distribution from one entry point. Digital customs workflows also help operators manage documentation, classification, and release steps with less manual intervention than before. This matters most for cross-border sellers that need consistent processing across several destination states with different tax and product rules. Over time, the GCC Cross-Border E-commerce Logistics Market should see lower friction on repeat shipments as digitized clearance systems become more common across the bloc.

Faster-Delivery Expectations

Delivery speed has become a more important purchase factor, reshaping the GCC Cross-Border E-commerce Logistics Market. Consumers who already receive fast domestic deliveries now expect imported goods to arrive in much shorter windows than the region was accustomed to in the past. Express delivery indicates that merchants and buyers are willing to pay for faster cross-border fulfillment as conversion rates improve. FedEx expanded direct, nonstop connectivity from the United States and Europe to Saudi Arabia in September 2025, demonstrating how major operators are reducing transit time on premium lanes. Network design in the GCC Cross-Border E-commerce Logistics Market is therefore moving closer to an express-first model in major urban corridors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Customs and VAT fragmentation | -1.1% | All 6 GCC states, sharpest friction on Saudi Arabia-UAE intra-GCC flows | Long term (≥ 4 years) |

| High shipping and reverse-logistics costs | -0.8% | Global, with acute impact on low-ARPU categories | Medium term (2-4 years) |

| Product registration bottlenecks | -0.5% | Saudi Arabia, UAE | Medium term (2-4 years) |

| DDU and COD refusal loops | -0.4% | Saudi Arabia, Oman, Kuwait | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Customs and VAT Fragmentation

The GCC Cross-Border E-commerce Logistics Market still faces friction from uneven customs treatment and tax administration across the 6 states. Operators that serve several destination markets must manage different documentation rules, tax treatments, and release requirements even when the shipment enters through one regional gateway. This increases compliance costs and raises the value of integrated technology that can automate invoicing and multi-country tax handling. Larger carriers absorb this burden more effectively because they can spread compliance investment across broader parcel volumes. Smaller operators remain more exposed, which keeps the GCC Cross-Border E-commerce Logistics Market less efficient than a fully harmonized customs area would allow.

High Shipping and Reverse-Logistics Costs

High delivery and returns costs remain a clear restraint on the GCC Cross-Border E-commerce Logistics Market. Last-mile delivery accounts for a large share of total fulfillment costs in many cross-border cases due to long travel distances, inconsistent address quality, and climate-related operational constraints. Returns add further pressure, especially in fashion, where cross-border buyers are more likely to reject or send back items after delivery. That burden is harder to recover on low-ticket categories because reverse movement, re-clearance, and duty recovery can cost more than the original parcel economics support. Until return consolidation and smarter routing reach a broader scale, the GCC Cross-Border E-commerce Logistics Market will continue to face margin pressure in value-sensitive categories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Fashion Anchors Value as Health and Beauty Reshapes Growth

Fashion and lifestyle accounted for 37.41% of the GCC Cross-Border E-commerce Logistics Market size in 2025, making it the largest product category by value. This leadership reflects the region’s young consumer base, strong preference for imported labels, and continued demand for apparel, footwear, and accessories sourced from Europe and Asia. In the GCC cross-border e-commerce logistics industry, fashion parcels require more than basic shipping, as packaging quality, returns handling, and rapid replenishment influence merchant performance. The category remains large, but it is also becoming more operationally demanding as international marketplaces and direct-from-origin sellers push higher order frequency into Gulf destinations.

Health and beauty / personal care is projected to grow at a 8.11% CAGR through 2031, making it the fastest-growing product category. Growth in this segment is supported by rising demand for imported skincare, wellness products, and premium personal care lines that are not always available through local retail channels. Compliance requirements are more stringent here because cosmetics and supplements often require additional registration and release management before final delivery. Consumer electronics and household appliances continue to carry some of the highest shipment values, which supports the use of air freight on time-sensitive corridors. Foods and beverages and furniture still account for a smaller share because food imports can face tighter restrictions, while furniture often carries an unfavorable volumetric cost profile for cross-border fulfillment.

By Logistics Function: Transport Commands Share as Value-added Services Lead Growth

Transportation held 73.33% of the GCC Cross-Border E-commerce Logistics Market share in 2025, confirming that line-haul movement still captures the majority of revenue in the current model. Air freight remains the leading transport mode within this segment because fashion, electronics, and premium consumer goods need shorter transit times from Asia and Europe into Gulf markets. Sea freight plays a role for heavier and lower-value goods where delivery time is less critical, while road transport remains essential for onward movement once parcels enter gateway markets. The GCC cross-border e-commerce logistics industry still depends heavily on transport capacity, but monetization is widening beyond pure movement.

Value-added services and others are forecast to grow at a 12.30% CAGR through 2031, which makes it the fastest-growing logistics function. This reflects growing merchant demand for bonded warehousing, returns handling, kitting, customs support, and localized buyer communication under a single logistics contract. Warehousing, distribution, and inventory management are also gaining importance as brands seek to place stock closer to Gulf consumers in order to shorten delivery windows. JD.com’s logistics platform opened a warehouse in the UAE in 2025 and later announced a 70,000 m² smart logistics hub with Abu Dhabi Airports, which signals continuing infrastructure investment around regional fulfillment depth. As these facilities scale, the GCC Cross-Border E-commerce Logistics Market should derive a larger share of revenue from warehousing and service integration rather than from transport alone.

By Business Model: B2C Dominates as C2C Emerges as the Structural Disruptor

B2C accounted for 78.50% of the GCC Cross-Border E-commerce Logistics Market share in 2025 and remains the dominant business model. Consumer-facing platforms still define parcel volume, delivery expectations, and the need for fast and reliable import fulfillment across Saudi Arabia and the UAE. The size of B2C reflects the region’s dependence on imported consumer goods and the strength of online shopping across fashion, electronics, and personal care. It also explains why carriers continue to invest in service consistency, address accuracy, and returns processing as part of their core operating model.

C2C is forecast to grow at a 15.47% CAGR through 2031, making it the fastest-growing business model. This shift is linked to luxury resale, authenticated sneakers, and other peer-to-peer categories where parcel value is high, and service expectations are strict. C2C shipments often require stronger packaging, tighter transit controls, and greater confidence in item condition than standard B2C orders. B2B remains smaller by value than B2C, yet it stays strategically important because commercial importers and marketplace sellers still generate attractive contract revenue under managed compliance models. Together, these patterns show that the GCC Cross-Border E-commerce Logistics Market is broadening from mass consumer parcel delivery into higher-service and higher-trust fulfillment tiers.

By Delivery Speed: Standard Maintains Share While Express Defines Competitive Positioning

Standard delivery accounted for 62.07% of the GCC Cross-Border E-commerce Logistics Market share in 2025, indicating that price-sensitive volume still anchors the market. This segment is strongest in lower-ticket, bulkier categories, where consumers accept longer delivery windows in exchange for lower shipping charges. Standard service is also useful for merchants that optimize around consolidated imports and cost discipline rather than premium speed. Even so, the gap between standard and express expectations is narrowing as domestic e-commerce benchmarks influence cross-border buying behavior.

Express delivery is projected to grow at a 10.15% CAGR through 2031, making it the fastest-growing speed tier. The main driver is not only consumer impatience but also stronger conversion for listings that qualify for faster delivery promises on major online platforms. FedEx supported this shift by establishing direct nonstop connections from the United States and Europe into Saudi Arabia in 2025, reducing transit time on high-value international lanes. Emirates SkyCargo also stated that it would expand its dedicated freighter fleet to 21 aircraft by December 2026 and launch Emirates Courier Express, reinforcing the commercial logic behind premium cross-border delivery services. The GCC Cross-Border E-commerce Logistics Market is therefore increasingly using express capability as a competitive differentiator rather than a niche service.

By Flow Direction: Inbound Dominates as Outbound Gains Strategic Momentum

Inbound logistics held 71.00% of the GCC Cross-Border E-commerce Logistics Market size in 2025, reflecting the region’s continued dependence on imported consumer products. Asia-Pacific remains the main origin base for these flows, especially for apparel, electronics, and personal care goods moving into Saudi Arabia and the UAE. This structure is tied to the Gulf’s consumption-led economy and its limited manufacturing depth in several major e-commerce categories. It also means that gateway performance, customs handling, and import service quality continue to shape the market's economics more than export execution does today.

Outbound logistics is projected to grow at an 8.11% CAGR through 2031, even though it starts from a smaller base. Export-oriented programs in the Gulf are creating more room for cross-border parcel movement from the region into South Asia, Europe, and other destination markets. Asyad Group completed its acquisition of Ligentia in April 2026 and expanded its operational footprint to 76 cities across 24 countries, which strengthens Oman’s position in outbound corridor development. Outbound margins can be attractive because fewer providers have built origin-side infrastructure for export parcel flows than for inbound consumer imports. That makes outbound growth strategically important for the GCC Cross-Border E-commerce Logistics Market even while inbound still dominates the revenue base.

Geography Analysis

Asia-Pacific remains the dominant origin region for inbound flows into the GCC Cross-Border E-commerce Logistics Market. China, South Korea, Japan, Bangladesh, and Vietnam supply a large share of the electronics, fashion, and personal care goods moving into the Gulf. The region’s importance is rising further as Asian logistics providers expand local warehousing and fulfillment depth near Gulf end markets. JD.com opened a warehouse in the UAE and announced a 70,000 sqm smart logistics hub in Abu Dhabi, indicating that Asian-origin operators are moving toward destination inventory models rather than relying solely on long-haul forwarding. Emirates SkyCargo also signed a preferred partnership with Teleport in April 2025 to strengthen trade and e-commerce flows between Southeast Asia and Dubai, reinforcing the commercial depth of the Asia-Pacific to Gulf corridor.

Europe and North America generate some of the highest-value parcels in the GCC Cross-Border E-commerce Logistics Market. European origins remain especially important for the Fashion and Lifestyle segment, while North America is relevant for premium consumer goods and direct-to-consumer brands. Direct connectivity matters more on these lanes because delivery speed strongly affects conversion on higher-ticket products. FedEx’s expanded nonstop service into Saudi Arabia points to the pricing power embedded in direct express connections from the United States and Europe to Gulf destinations.

The Middle East and Africa serve both as a regional distribution zone and as a re-export corridor for the GCC Cross-Border E-commerce Logistics Market. Goods often enter through major Gulf gateways and then move onward within the wider region after customs processing and storage. This gives the UAE and Saudi Arabia an important relay role in addition to their domestic demand role. DP World’s 2026 partnership with Al Dahra to strengthen food security and build GCC agri-logistics highlights the growing relevance of Africa-linked outbound and re-export corridors for regional trade movement. South America remains smaller, but it still represents a developing destination opportunity as the GCC broadens its outbound reach over time[3]“GCC Unified Guide for Customs Procedures at First Points of Entry,” GCC Secretariat, gcc-sg.org.

Competitive Landscape

The GCC Cross-Border E-commerce Logistics Market is moderately fragmented, and no single operator controls every layer of the value chain. Competition spans international forwarding, customs management, warehousing, line-haul transport, last-mile delivery, and returns. Global integrators such as DHL, FedEx, UPS, Kuehne+Nagel, and Maersk compete alongside regional specialists including Aramex, SMSA Express, Naqel Express, and iMile. The larger global players bring capital, air capacity, and network reach, while regional operators often retain an advantage in address handling, local compliance execution, and delivery density. This balance keeps the GCC Cross-Border E-commerce Logistics Market open enough for new investment, but difficult for any one firm to dominate across all service layers.

State-connected and infrastructure-linked operators add another layer of competition. Emirates SkyCargo is expanding its freighter fleet and cross-border courier offering, which strengthens its role in premium and time-sensitive international fulfillment. FedEx has also deepened its Saudi footprint with direct air links aligned with the Kingdom’s logistics ambitions, demonstrating how infrastructure commitments are tied to national corridor development. These moves matter because service quality in the GCC Cross-Border E-commerce Logistics Market increasingly depends on how closely air, customs, and final-mile operations can be integrated.

Chinese-origin operators represent one of the clearest disruptive forces in the GCC Cross-Border E-commerce Logistics Market. JD.com’s expanding warehouse footprint and planned Abu Dhabi smart hub show a willingness to invest in destination-side assets rather than depend only on third-party relay networks. At the same time, competitive advantage is moving beyond physical assets and toward digital integration, because merchants increasingly value customs readiness, address verification, and real-time shipment visibility. Asyad’s acquisition of Ligentia and its Ligentix control-tower capability is one example of how technology is becoming central to corridor management and outbound service development. Over the next few years, the GCC Cross-Border E-commerce Logistics Market is likely to reward operators that combine local compliance strength, warehouse depth, and digitally managed international flows[4]“Shaping New Trade Corridors,” GFMag, gfmag.com.

GCC Cross-Border E-commerce Logistics Industry Leaders

Aramex

DHL Group

FedEx

SF Express

United Parcel Service of America, Inc. (UPS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Dubai CommerCity announced an enhanced integration of its cross-border e-commerce platform in collaboration with Dubai Customs, Dubai Municipality, and NAQEL Express, deploying a blockchain-enabled system that automates processes from order placement and customs clearance to final delivery. The initiative positions Dubai as a globally competitive digital trade hub and enables end-to-end traceability for cross-border shipments passing through the UAE free zones.

- May 2026: DSV inaugurated a new 30,000 sqm build-to-suit logistics warehouse at Jebel Ali Free Zone South Campus, Dubai, developed in partnership with Arcapita's Lintara Properties. The facility enhances DSV's multimodal logistics capabilities at the GCC's largest containerized trade gateway.

- April 2026: Asyad Group completed its second major international acquisition in under 2 years, purchasing UK-based 4PL provider Ligentia and its proprietary Ligentix digital control-tower platform, expanding Asyad's operational presence to 76 cities across 24 countries. The acquisition gives Asyad outbound capabilities on Europe and South Asia corridors critical for Oman's export-diversification agenda.

- February 2026: CJ Logistics launched its Global Distribution Center (GDC) at Riyadh's Special Integrated Logistics Zone, a USD 41.4 million facility with daily handling capacity exceeding 20,000 parcels built under a partnership with the Saudi General Authority of Civil Aviation to serve as a Korea-Middle East e-commerce logistics hub.

GCC Cross-Border E-commerce Logistics Market Report Scope

| Foods and Beverages |

| Personal and Household Care |

| Fashion and Lifestyle (Accessories, Apparel, Footwear) |

| Furniture |

| Consumer Electronics and Household Appliances |

| Other Products |

| Transportation | Road |

| Air | |

| Sea and Inland Waterways | |

| Rail | |

| Warehousing, Distribution and Inventory Management | |

| Value-added Services and Others |

| B2C |

| B2B |

| C2C |

| Express |

| Standard |

| Outbound (Exports) | North America |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa | |

| South America | |

| Inbound (Imports) | North America |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa | |

| South America |

| By Product Category | Foods and Beverages | |

| Personal and Household Care | ||

| Fashion and Lifestyle (Accessories, Apparel, Footwear) | ||

| Furniture | ||

| Consumer Electronics and Household Appliances | ||

| Other Products | ||

| By Logistics Function | Transportation | Road |

| Air | ||

| Sea and Inland Waterways | ||

| Rail | ||

| Warehousing, Distribution and Inventory Management | ||

| Value-added Services and Others | ||

| By Business Model | B2C | |

| B2B | ||

| C2C | ||

| By Delivery Speed | Express | |

| Standard | ||

| By Flow Direction | Outbound (Exports) | North America |

| Europe | ||

| Asia-Pacific | ||

| Middle East and Africa | ||

| South America | ||

| Inbound (Imports) | North America | |

| Europe | ||

| Asia-Pacific | ||

| Middle East and Africa | ||

| South America | ||

Key Questions Answered in the Report

What is the current size of the GCC cross-border e-commerce logistics space?

It stands at USD 461.72 million in 2026 and is forecast to reach USD 651.33 million by 2031 at a 7.12% CAGR.

Which product category generates the most value in Gulf cross-border e-commerce logistics?

Fashion and lifestyle led with a 37.41% share in 2025, supported by strong demand for imported apparel, footwear, and accessories.

Which logistics function is growing the fastest in the GCC?

Value-added services and others are the fastest-growing function with a 12.30% CAGR through 2031, as merchants need returns management, customs support, and bonded warehousing.

Why does inbound logistics dominate across the GCC?

Inbound flows held 71.00% of revenue in 2025 because the region imports a large share of its fashion, electronics, and personal care demand.

What is driving faster delivery demand for imported online orders in Saudi Arabia and the UAE?

Domestic same-day and next-day benchmarks have reset buyer expectations, pushing express delivery to a 10.15% CAGR through 2031.

Which business model is rising fastest in cross-border online fulfillment across the Gulf?

C2C is projected to grow at a 15.47% CAGR through 2031, supported by luxury resale, authenticated goods, and high-value peer-to-peer commerce.

Page last updated on: