China Swine Feed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 26.70 Billion |

| Market Size (2026) | USD 28.10 Billion |

| Market Size (2031) | USD 36.90 Billion |

| Growth Rate (2026 - 2031) | 5.40% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Swine Feed Market Analysis by Mordor Intelligence

The China swine feed market size is projected to grow from USD 26.7 billion in 2025 to USD 28.1 billion in 2026, and further to USD 36.9 billion by 2031, with a CAGR of 5.4% from 2026 to 2031. Industrial complexes driving herd rebuilding are increasingly adopting precision rations tailored to specific nutritional needs, which is significantly boosting per-head feed consumption. A government mandate to reduce soybean meal usage is fostering the adoption of alternative feed components, such as enzymes and amino acids, thereby reducing the country's dependence on soybean imports. The volatility in corn prices is exerting pressure on profit margins, leading integrators to implement advanced digital hedging tools and expand investments in grain storage infrastructure to mitigate risks. Furthermore, foreign research centers are rapidly developing and localizing antibiotic-free starter formulations to align with regional requirements and consumer preferences.

Key Report Takeaways

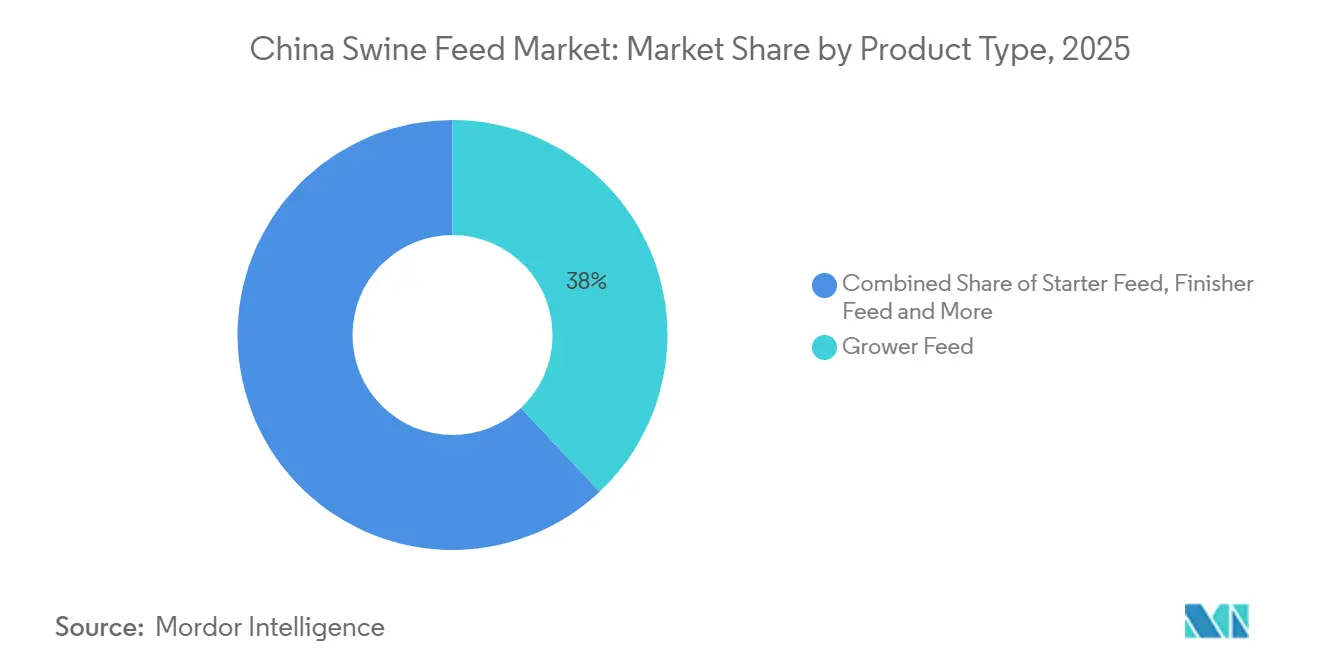

- By product type, grower feed is projected to account for the largest market share of 38% in the China swine feed market in 2025, while the starter feed market size is projected to grow at the fastest CAGR of 5.9% from 2026 to 2031.

- By form, pellets are anticipated to hold the largest market share of 56% in the China swine feed market in 2025, whereas the crumbles market is forecast to register the fastest CAGR of 6.5% from 2026 to 2031.

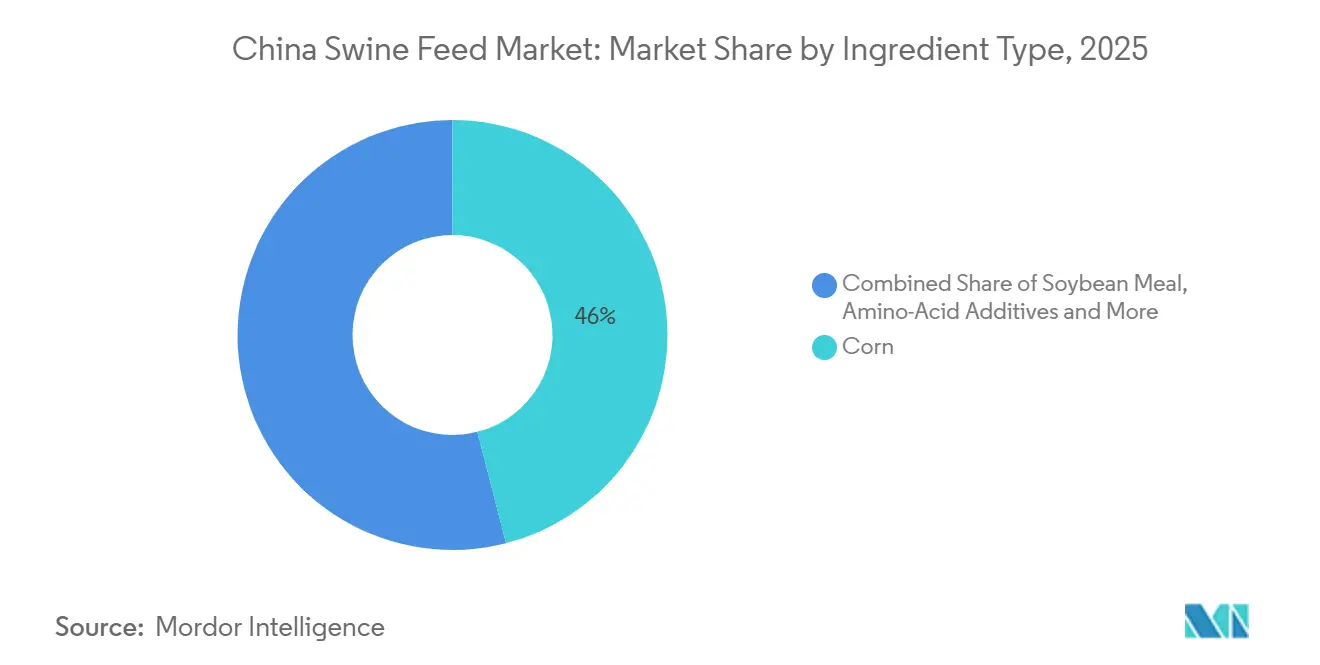

- By ingredient, corn is estimated to retain the largest market share of 46% in the China swine feed market in 2025, while the enzymes (e.g., phytase) market size is projected to grow at the fastest CAGR of 8.1% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China Swine Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid consolidation of large-scale pig farms | +1.2% | Henan, Hebei, Shandong, and Guangdong provinces | Medium term (2-4 years) |

| African Swine Fever (ASF)-triggered surge in biosecure commercial feed | +0.9% | Heilongjiang, Jilin, Liaoning, Henan, and Hebei | Short term (≤ 2 years) |

| Swill-feeding ban spurs commercial feed uptake | +0.6% | Nationwide pilot programs in major feed-producing provinces | Long term (≥ 4 years) |

| Roll-out of precision-feeding IoT platforms | +0.8% | Early adoption in Henan, Shandong, and Sichuan | Medium term (2-4 years) |

| Adoption of recombinant thermostable phytase | +0.5% | Commercial mills serving integrated producers nationwide | Medium term (2-4 years) |

| Retailers carbon-neutral pork procurement targets | +0.3% | Tier-1 cities such as Beijing, Shanghai, Guangzhou, and Shenzhen | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Consolidation of Large-Scale Pig Farms

The rapid consolidation of large-scale pig farms is shifting procurement power toward vertically integrated companies that negotiate directly with grain suppliers and require stage-specific feed rations. Muyuan Foods reported a fully allocated breeding cost of CNY 12 per kilogram (USD 1.65 per kilogram) in March 2025 [1]Source: XinmuNet, “Muyuan Expansion in Henan,” xinmunet.com . The scale of operations enables integrators to operate on-site feed mills, implement stringent biosecurity measures, and reinvest cost savings into nutrition research, further widening the gap between large integrators and smallholders.

African Swine Fever (ASF)-Triggered Surge in Biosecure Commercial Feed

In response to the African Swine Fever (ASF) outbreak, swine producers are tightening biosecurity measures and pivoting towards safer feed sourcing. The Food and Agriculture Organization reported a jump in ASF cases in Vietnam, rising from over 1,600 in 2024 to about 2,495 in 2025, leading to the culling of roughly 1.27 million pigs [2]Source: Food and Agriculture Organization (FAO), “ASF Situation Update – Asia & Pacific,” fao.org. This uptick underscores heightened contamination risks in conventional systems. Given that ASF can be transmitted via feed and farm inputs, producers are turning to heat-treated, certified commercial feed sourced from biosecure mills. This shift is propelling the demand for traceable, HACCP-compliant compound feed products.

Swill-Feeding Ban Spurs Commercial Feed Uptake

China's strict enforcement of swill-feeding bans has significantly altered pig farming practices, increasing reliance on commercial feed. The prohibition of untreated food waste feeding has enhanced biosecurity standards and reduced the risk of disease transmission. This change has led to steady demand for formulated feed products, particularly among large-scale and integrated farms. Additionally, higher feeding costs have driven industry consolidation, benefiting organized producers with efficient procurement systems. This shift contributes to long-term stability in feed demand and promotes the formalization of China's swine production industry.

Roll-Out of Precision-Feeding IoT Platforms

Precision-feeding Internet of Things (IoT) platforms leverage real-time data on animal weight, feed intake, and environmental conditions to optimize daily rations and enhance feed efficiency. Companies like Cargill are incorporating digital farm management solutions, such as Agriness, to facilitate data-driven livestock management. These systems improve monitoring of animal health and resource use, enabling producers to enhance productivity and minimize waste. Research shows that precision feeding technologies can decrease feed waste and improve nutrient efficiency through real-time ration adjustments, contributing to cost-effective swine production [3]Source: ResearchGate, Precision Feeding in Pig Production: A Review, researchgate.net .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Domestic corn-price volatility | −0.4% | Heilongjiang, Jilin, Liaoning, Hebei, and Shandong provinces | Short term (≤ 2 years) |

| Slow herd-rebuilding pace post ASF | −0.6% | Southern provinces such as Guangdong, Guangxi, and Fujian | Medium term (2-4 years) |

| Stricter antibiotic-use regulations | −0.3% | Commercial farms and certified mills nationwide | Medium term (2-4 years) |

| Rising share of insect and fermented proteins in rations | −0.2% | Early adoption in research farms and premium integrators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Domestic Corn-Price Volatility

In February 2026, domestic corn was traded at 2.320 RMB per kilogram (USD 0.32 per kilogram), marking a significant decline from 3.000 RMB per kilogram in late 2022 [4]Source: CEIC Data, “China Corn Spot Price,” CEIC Data, ceicdata.com . This sharp price drop highlights the volatility in the corn market, which poses challenges for producers and traders alike. Such fluctuations create uncertainty in forward contracting, making it difficult for producers to secure stable pricing and plan their operations effectively. Additionally, this price instability may prompt producers to reduce their inventory levels as a precautionary measure, potentially leading to a decline in feed demand and further impacting market dynamics.

Slow Herd-Rebuilding Pace post ASF

The recovery of China's swine herd following the African Swine Fever outbreak continues at a gradual pace, as producers adopt cautious expansion strategies due to volatile pork prices and market uncertainties. Many farmers are emphasizing risk management over rapid restocking, resulting in slower growth in sow inventories. This measured approach is curbing short-term demand for compound feed and influencing overall feed consumption trends. Additionally, the situation is altering supply chain dynamics, with producers prioritizing efficiency and cost control while navigating uncertain market conditions and fluctuating profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Starter Feed Gains Momentum

Grower feed accounted for the largest 38% of the China swine feed market share in 2025, driven by the high feed consumption during the 30 to 70 kilogram growth phase, which requires the largest ration volume per animal. The starter feed market size is projected to register the fastest CAGR of 5.9% from 2026 to 2031. This growth reflects the industry's increasing focus on early-life gut-health programs designed to reduce mortality rates and shorten finishing periods, addressing key challenges in swine production. Finisher Feed remains focused on cost efficiency to optimize production expenses, while Breeder Feed volumes are closely tied to sow inventory trends.

Producers are focusing on nutritional precision during the weaning phase to minimize stress, improve gut health, and enhance growth performance. This has resulted in increased use of functional ingredients, including easily digestible proteins, organic acids, and feed additives that promote immunity and nutrient absorption. Regulatory restrictions on the use of antibiotics and zinc oxide are further driving the development of advanced, compliant starter feed solutions. Additionally, the expansion of large-scale farms and contract rearing systems is boosting the demand for high-quality starter feed, supported by integrated production models aimed at improving feed efficiency and reducing mortality rates.

By Form: Crumbles Outpace Pellets

Pellet is projected to account for the largest market share of 56% for the China swine feed market size in 2025, primarily due to their biosecurity benefits, such as heat kill, which reduces pathogen risks, and their ease of storage, which simplifies handling and transportation. These features make pellets a preferred choice among large-scale producers. Crumbles are anticipated to be the fastest-growing segment, with a forecasted CAGR of 6.5% from 2026 to 2031, as breaking pellets into 1.5-to 2.5 millimeter particles improves feed intake in newly weaned piglets by making the feed easier to consume and digest. Meanwhile, mash is declining in popularity outside of backyard production as integrators focus on streamlining logistics, reducing labor requirements, and adopting more efficient feeding practices.

In China's swine feed market, crumbles are gaining an edge over pellets, thanks to their durability and easier handling. A 2026 study in Scientific Reports highlighted the fragility of pellet feed as breakage rates jumped from 3.22% at 500 rpm to a staggering 21.43% at 1500 rpm, underscoring their vulnerability to mechanical stress. This pronounced breakage tendency bolsters the case for the controlled-crumble method, which boosts porosity yet preserves structural integrity, ensuring consistent feed quality.

By Ingredient: Enzymes Unlock Feed Value

Corn accounted for the largest market share, 46%, of the China swine feed market size in 2025. However, rising maize prices have increased margin pressures, prompting formulators to adopt multi-grain blends to optimize costs and maintain feed efficiency. Enzymes (e.g., Phytase) represent the fastest-growing ingredient class with a CAGR of 8.1% from 2026-2031, driven by the soybean meal reduction mandate, which necessitates tighter protein budget management.

Peer-reviewed studies suggest that incorporating phytase units per kilogram of complete feed can release a significant portion of bound phosphorus, allowing feed mills to reduce monocalcium phosphate usage. This reduction can decrease ration costs while maintaining nutritional adequacy. Additionally, synthetic amino acids, such as lysine and methionine, are used to address specific nutrient deficiencies. Alternative ingredients such as wheat, rice bran, and fermented protein are gaining traction as cost-effective and sustainable feed options, particularly during periods of high corn futures prices.

Geography Analysis

In 2024, Henan, Hebei, and Shandong, forming a pivotal corridor in the Central Plains, showcased their dominance in swine production. A peer-reviewed study leveraging data from the National Bureau of Statistics highlighted Henan's leading position, with a pig inventory of 40.31 million head and a breeding sow inventory of 3.73 million head, both topping national charts [6]Source: Scientific Reports, “Spatiotemporal evolution and regional differences of livestock production in Henan Province,” nature.com . This dense livestock concentration not only fuels a robust demand for compound feed but also benefits from Henan's strategic proximity to major grain-producing regions. Established logistics networks further enhance the cost-effective manufacturing and distribution of feed throughout northern China.

Southern provinces, including Guangdong and Guangxi, are experiencing strong demand for starter feed. This growth is driven by climatic conditions that heighten disease risks and weaning stress in piglets. The hot, humid environment increases pathogen exposure, prompting producers to adopt nutritionally enhanced starter feed to boost early-stage immunity and survival rates. Large integrated producers in these provinces are enhancing biosecurity measures and feed quality standards, accelerating the transition to commercial feed solutions. Additionally, the expansion of intensive farming systems, which rely on consistent, high-performance starter feed, is further supporting productivity and animal health in the region.

The Southwest region, encompassing Sichuan and Yunnan, is emerging as a critical growth area due to rising investments in large-scale swine production and feed infrastructure. The growth of integrated farming operations is driving higher adoption of starter feed, particularly in modern nurseries aimed at improving piglet performance. This region benefits from supportive provincial policies and the availability of land, fostering the establishment of new farms and feed facilities. Furthermore, the adoption of digital tools and improved storage systems is enhancing feed management across dispersed farms, improving operational efficiency and sustaining the growth in starter feed demand.

Competitive Landscape

China's feed market is moderately concentrated in 2025, with the top five companies New Hope Liuhe Co., Ltd., Muyuan Foods Co., Ltd., Chia Tai Investment Co., Ltd. (Charoen Pokphand Group), Wens Foodstuff Group Co., Ltd., and Guangdong Haid Group Co., Ltd., leading in production volume and provincial coverage. Vertically integrated packer-feeders, such as Muyuan Foods, are aggressively acquiring assets to secure grain sourcing and enhance biosecurity measures. This strategy is reducing the addressable demand for third-party mills, as these companies aim to control supply chains and mitigate risks associated with external dependencies, reshaping the competitive landscape.

Twins Group has emerged as the world's largest pig-feed producer by acquiring Zhengbang's distressed assets, including grain elevators and coastal terminals that significantly reduce inbound corn costs. Competitors are now racing to replicate this upstream control to gain similar advantages. For example, Guangdong Haid Group Co., Ltd. has launched joint ventures in Jilin to secure frost-grade maize supplies. Additionally, captive mills are aligning production with hog supply flows, tightening price discipline, and reducing spot-market feed price volatility, which previously benefited independent feed producers, further consolidating the market.

The adoption of digital nutrition platforms and data-driven feeding strategies is increasing competition in the market. Key players are utilizing advanced analytics, real-time monitoring, and precision feeding models to enhance feed formulations and improve operational efficiency. These capabilities are essential for maintaining competitiveness, as producers seek higher performance and cost-effective feed solutions. Companies investing in technology-driven innovations and scalable solutions are better equipped to meet the rising demand in the evolving starter feed market.

China Swine Feed Industry Leaders

New Hope Liuhe Co., Ltd.

Muyuan Foods Co., Ltd.

Chia Tai Investment Co., Ltd. (Charoen Pokphand Group)

Wens Foodstuff Group Co., Ltd.

Guangdong Haid Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Muyuan Foods Co., Ltd. and CP Group have signed a strategic cooperation agreement covering feed, pig farming, slaughtering, food processing, talent development, and capital investment. The partnership unites China's largest pig producer and one of Asia's largest agribusiness conglomerates to collaborate on technology sharing and supply chain optimization.

- May 2025: Cargill opened its first Asia Global Innovation Center for pig nutrition in Yongji, Shanxi. The 34,000-square-meter facility, a joint venture with Changrong Agriculture, conducts over 140 swine trials annually and focuses on feed efficiency, reproductive performance, sustainability, and reducing antibiotics and zinc usage.

- April 2024: Evonik Industries AG enhanced its amino acid production and supply capabilities in China to support animal feed applications, particularly swine nutrition. This expansion aligns with the development of low-protein, high-efficiency feed formulations.

China Swine Feed Market Report Scope

Swine feed is a blend of grains, protein sources, vitamins, and minerals designed to meet the nutritional needs of pigs at various growth stages. It promotes growth, improves feed efficiency, strengthens immunity, and enhances productivity in pork production systems. The China swine feed market report is segmented by product type (starter feed, grower feed, finisher feed, breeder feed), by form (pellet, mash, crumbles), and by ingredient type (corn, soybean meal, amino-acid additives, vitamins and minerals, enzymes, other cereals and fats). The market forecasts are provided in terms of value (USD).

| Starter Feed |

| Grower Feed |

| Finisher Feed |

| Breeder Feed |

| Pellet |

| Mash |

| Crumbles |

| Corn |

| Soybean Meal |

| Amino-Acid Additives |

| Vitamins and Minerals |

| Enzymes (e.g., Phytase) |

| Other Cereals and Fats |

| By Product Type | Starter Feed |

| Grower Feed | |

| Finisher Feed | |

| Breeder Feed | |

| By Form | Pellet |

| Mash | |

| Crumbles | |

| By Ingredient Type | Corn |

| Soybean Meal | |

| Amino-Acid Additives | |

| Vitamins and Minerals | |

| Enzymes (e.g., Phytase) | |

| Other Cereals and Fats |

Key Questions Answered in the Report

What is the current size and projected value of China’s swine feed demand?

It is USD 26.7 billion in 2025 and is forecast to reach USD 36.9 billion by 2031, reflecting a fastest 5.4 % CAGR from 2026-2031.

Which feed product category is growing fastest through 2031?

Starter Feed shows the fastest 5.9 % CAGR from 2026-2031 because integrators focus on early-life gut health and reduced weaning mortality.

Why are enzymes attracting heightened interest from feed formulators?

Thermostable phytase unlocks up to 85% of bound phosphorus, allowing mills to trim inorganic phosphate and save roughly USD 3–5 per metric ton of complete feed.

Which regions present the strongest near-term expansion opportunities?

Henan, Hebei, and Shandong benefit from proximity to grain belts, while Guangdong and Guangxi post rapid gains due to stringent biosecurity rules that favor commercial heat-treated feed.

Page last updated on: