Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 12.5 Billion |

| Market Size (2026) | USD 13.11 Billion |

| Market Size (2031) | USD 16.59 Billion |

| Growth Rate (2026 - 2031) | 4.84% CAGR |

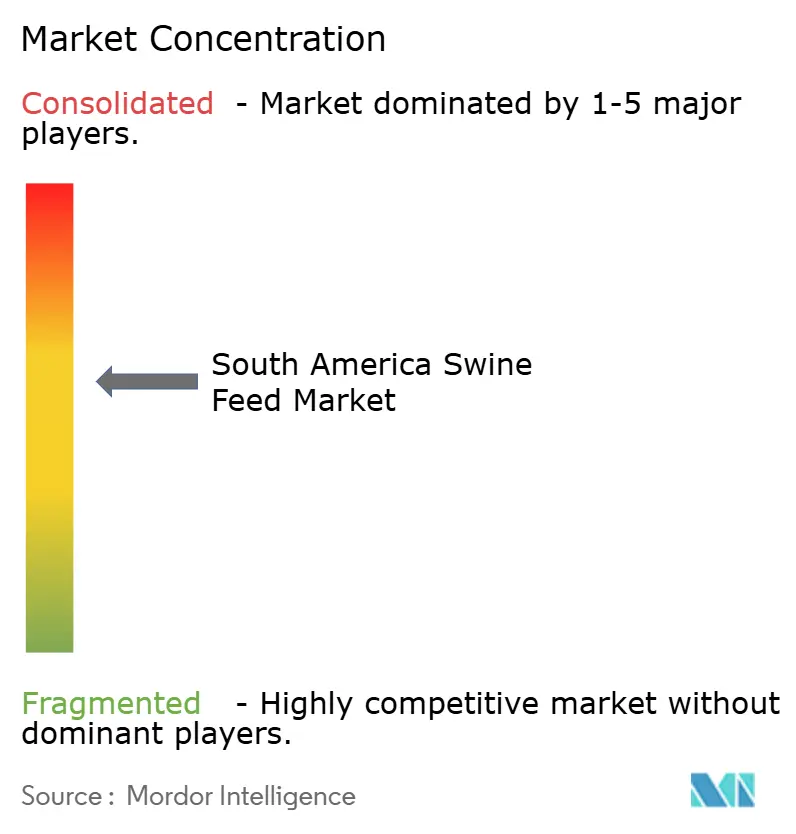

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Swine Feed Market Analysis by Mordor Intelligence

South America swine feed market size in 2026 is estimated at USD 13.11 billion, growing from 2025 value of USD 12.5 billion with 2031 projections showing USD 16.59 billion, growing at 4.84% CAGR over 2026-2031. Recent strength reflects robust pork production growth, fueled by domestic protein demand shifts and sustained export opportunities, especially into Asian destinations recovering from African swine fever disruptions. Brazil’s integrated producers continue scaling output to match foreign contracts, while Argentina’s pork‐centric dietary transition accelerates feed purchases amid persistent beef price inflation. Exchange‐rate swings create formulation cost volatility, yet technology investments in precision nutrition and supply-chain analytics are helping manufacturers defend margins. Currency conversions, tax reform benefits and improved harvest prospects have combined to widen capital budgets for feed-mill upgrades that bolster long-term competitiveness in the South America swine feed market.

Key Report Takeaways

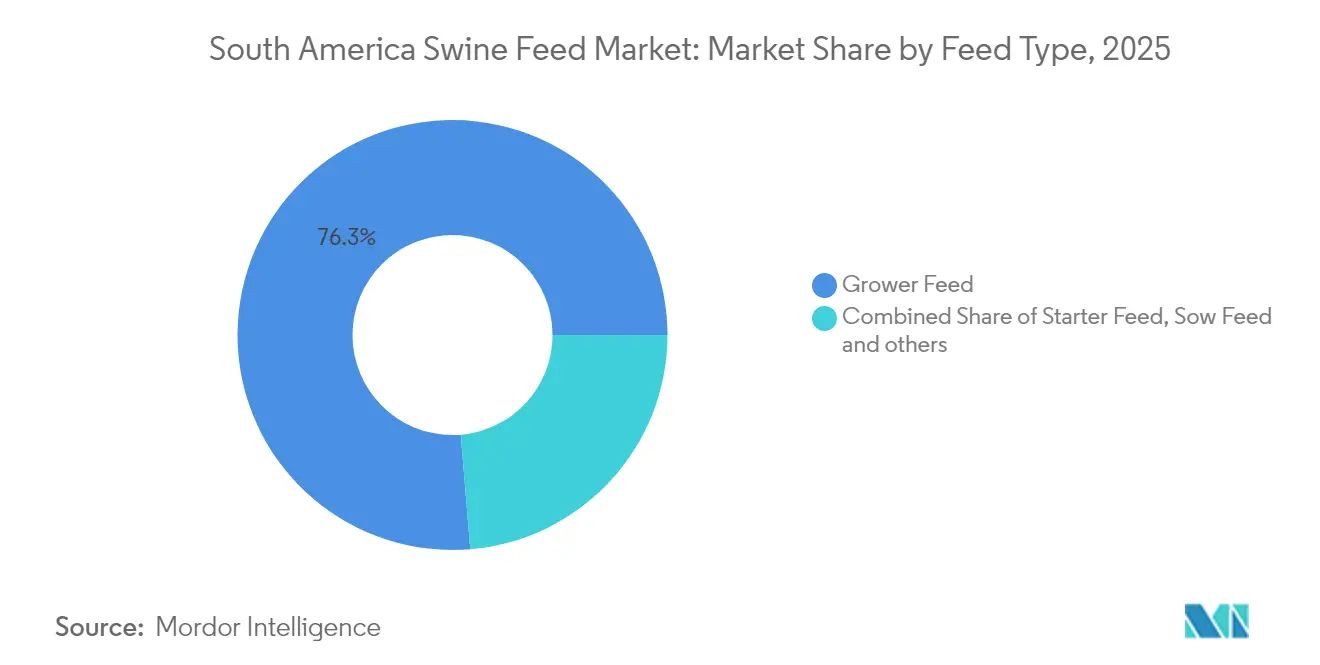

- By feed type, grower feed dominated with a 76.32% market share in 2025, while starter feed grew at a 6.56% CAGR (2026-2031), reflecting increased focus on early-life performance optimization.

- By country, Brazil maintained leadership with 57.55% of the South America swine feed market in 2025, driven by its dominant pork production capacity and export-oriented feed industry. Argentina emerged as the fastest-growing market with a 6.05% CAGR during the forecast period, driven by economic pressures shifting preferences away from beef.

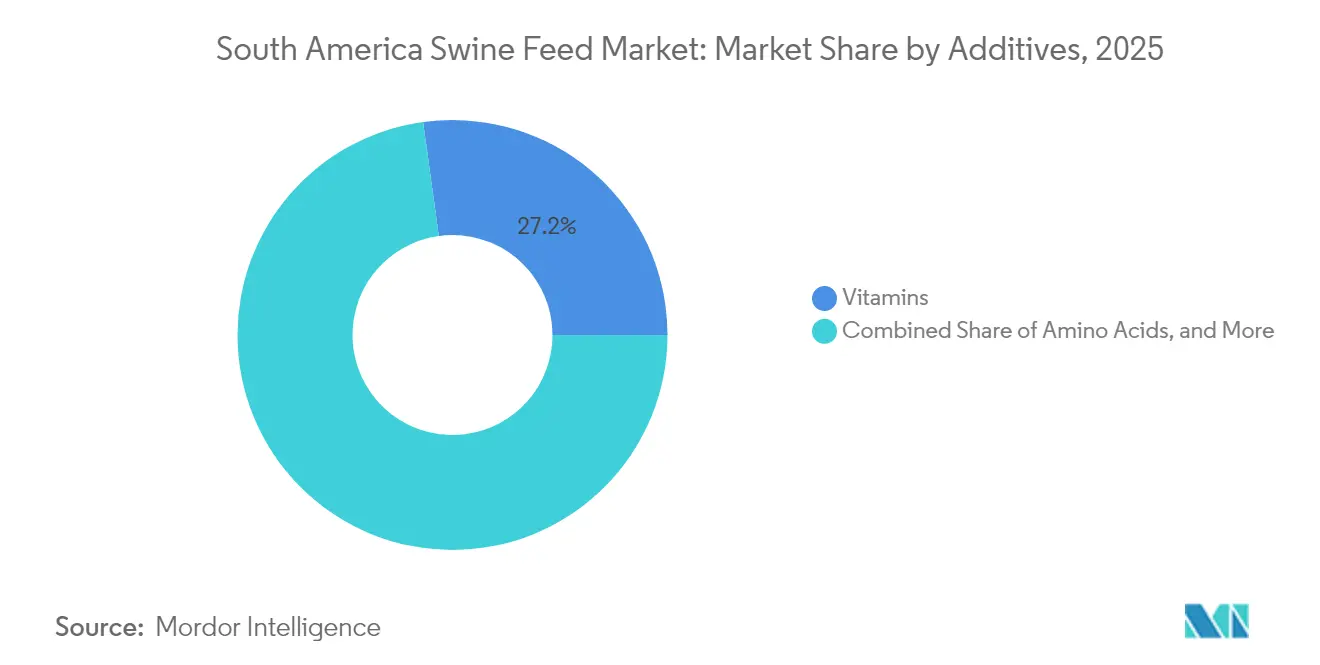

- By additives, vitamins held a 27.62% share of the market in 2025, driven by increasing demand for immune-boosting nutrition. Probiotics and prebiotics are estimated to grow at a 7.18% CAGR during 2026-2031, as manufacturers focus on premium product differentiation and export competitiveness.

- By company, Cargill, ADM, and SHV Holdings together controlled a significant share of the South America swine feed market in 2024, reflecting moderate industry concentration.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Swine Feed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of export-oriented pork production in Brazil | 1.20% | Brazil, with spillover to Argentina and Chile | Medium term (2-4 years) |

| Adoption of antibiotic alternatives (probiotics, organic acids) | 0.80% | Global, with early adoption in Brazil and Chile | Long term (≥ 4 years) |

| Lower corn and soybean input prices after 2024 harvest recovery | 0.60% | South America core, particularly Brazil and Argentina | Short term (≤ 2 years) |

| Government tax-reform incentives for feed manufacturing | 0.40% | Brazil, with potential expansion to other countries | Medium term (2-4 years) |

| Precision-nutrition tech deployment in commercial feed mills | 0.30% | Brazil and Chile leading, Argentina following | Long term (≥ 4 years) |

| Growth of specialty premixes tailored to genotype-specific diets | 0.20% | Regional, concentrated in commercial operations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Export-Oriented Pork Production in Brazil

Brazil shipped 990.7 thousand metric tons of pork during the first nine months of 2024, a 7.7% year-over-year jump that intensified feed demand. Revenue increased significantly, despite currency headwinds, reflecting the demand for specialized nutrient-rich feed formulations. Major integrated companies like JBS and BRF are increasing their hog populations, driving higher demand for grow-finish feed across their vertically integrated feed mills. New slaughter facilities in Santa Catarina and Paraná are increasing regional corn consumption while boosting demand for soybean-based protein concentrates. Trade agreements with Mexico, Chile, and Japan are reducing market risks and securing long-term feed volume commitments. The South American swine feed market is projected to maintain steady growth through 2030, supported by export opportunities.

Adoption of Antibiotic Alternatives (Probiotics, Organic Acids)

Regulators and import customers are phasing out antibiotic growth promoters, prompting swine integrators to reformulate diets with Bacillus-based probiotics, organic acids and targeted enzymes. Peer-reviewed trials show a 30% reduction in post-weaning diarrhea when Bacillus strains replace in-feed antibiotics. Chilean and Brazilian mills have pioneered commercial blends that preserve average daily gain while enhancing carcass uniformity, allowing exporters to qualify for premium label claims in Europe and North America. The shift has motivated ingredient suppliers to expand regional R&D centers capable of tailoring multi-strain products to local corn–soy meal matrices. As regulatory momentum spreads, probiotic inclusion is poised to permeate everyday rations across the South America swine feed market.

Lower Corn and Soybean Input Prices After 2024 Harvest Recovery

The United States Department of Agriculture (USDA) projects Brazil’s corn output at 129 million tonnes for 2024-2025, up 7 million from the prior season, alleviating raw-material tightness [1]USDA Foreign Agricultural Service (FAS). Livestock and Products Annual - Brazil. August 27, 2024. Accessed September 19, 2025. https://apps.fas.usda.gov/newgainapi/api/Report/DownloadReportByFileName?fileName=Livestock%20and%20Products%20Annual_Brasilia_Brazil_BR2024-0023.pdf. Soybean crushing expansions by multinationals have similarly improved meal availability, trimming finished-feed cost curves. Although domestic corn premiums remained elevated in early 2025, forward curves indicate easing into the second half as on-farm inventories normalize. Lower raw-material prices widen gross margins for compounders, freeing up capital for enzyme inclusion, quality-control testing and digital traceability tools. Cost relief also supports competitive export pricing, reinforcing volume gains for the South America swine feed market.

Government Tax-Reform Incentives for Feed Manufacturing

Brazil’s constitutional tax overhaul replaces the layered PIS/COFINS and ICMS structure with a dual VAT, exempting staple meat products and creating straightforward credit recovery for imported micro-ingredients [2]Agência Brasil. “Reforma tributária isenta cesta básica de impostos.” Agência Brasil, accessed September 19, 2025. https://agenciabrasil.ebc.com.br. Feed mills gain from simpler compliance and reduced cascading taxes on vitamin and amino-acid imports, cutting formulation costs. The phased rollout between 2026 and 2033 offers planning certainty, incentivizing multinationals to accelerate capex on mill modernization. Improved fiscal efficiency underpins Brazil’s bid to solidify its hub status within the South America swine feed market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| African swine fever biosecurity costs despite no outbreaks yet | -0.70% | South America, with highest impact in border regions | Medium term (2-4 years) |

| High currency volatility raising additive import costs | -0.50% | Regional, particularly Argentina and Brazil | Short term (≤ 2 years) |

| Climate-linked harvest risks for corn and soy supplies | -0.40% | Argentina and southern Brazil primarily | Medium term (2-4 years) |

| Public pressure to curb deforestation in soy supply chains | -0.20% | Brazil Cerrado region, with global implications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

African Swine Fever Biosecurity Costs Despite No Outbreaks Yet

South America remains ASF-free, yet preventive biosecurity investments have surged as importers tighten sanitary requirements. Brazil’s bilateral agreement with Singapore guarantees trade continuity via compartmentalization but mandates rigorous traceability and feed decontamination protocols [3]Agrofy News, “Brasil blinda exportação de suínos…,” AGROFY.COM.BR Source: MASP, “Importaciones argentinas de carne de cerdo…,” MASP.LMNEUQUEN.COM. Producers now employ organic-acid feed treatments shown to lower ASFV viability in ingredients, raising per-ton feed costs. Capital diverted to bio-exclusion measures restrains spending on productivity drivers, tempering near-term gains in the South America swine feed market.

High Currency Volatility Raising Additive Import Costs

The Argentine peso’s slide and the Brazilian real’s depreciation have inflated landed costs of imported vitamins and amino acids. Argentina’s pork imports increased significantly in Q1-2025 partly because local processors struggled with additive inflation that eroded cost competitiveness. Smaller mills lacking hedging facilities adjust formulations frequently, compounding operational complexity. Currency swings thus squeeze margins and obscure budgeting visibility for stakeholders in the South America swine feed market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Feed Type: Grower Rations Dominate Volume While Starter Diets Accelerate

Grower rations constitute the largest slice, with 76.32% of the total market in 2025, reflecting the extended 25-100 kg phase when pigs consume the highest daily intake. The South America swine feed market size for grower diets benefited from Brazil’s record export shipments in 2024, lifting factory output in Santa Catarina and Paraná. Multisite integrators exploit scale economies by sourcing high-energy corn locally and balancing amino-acid profiles with domestically crushed soybean meal. Formulators are layering enzymes such as phytase to elevate phosphorus availability and control cost per kilogram of gain. Although sow diets claim modest tonnage, they remain strategically important as genetic lines push litter sizes higher. Mills are piloting precision micro-bin systems that modulate vitamin E and selenium inclusion according to gestation stage, safeguarding farrowing performance.

Starter diets are the fastest climber with an estimated CAGR of 6.56% during 2026-2031, mirroring the industry’s pivot toward improved early-life nutrition. Formulas now blend highly digestible plasma proteins, heat-stable probiotics, and short-chain fatty acids to support gut maturation. Larger capital outlays for specialty proteins are justified by tighter feed conversion and lower nursery mortality. Chilean integrators report weaning-to-sale improvements of 5 days following the adoption of enhanced starter packs. As export customers demand tighter antibiotic stewardship, early gut-health programs are expected to unlock further growth within the South America swine feed market.

By Additives: Functional Ingredients Move Center Stage

Vitamins retain a baseline role, holding the largest market share at 27.62% in 2025, as they are essential across all swine production stages for supporting immunity, reproduction, and metabolic functions. The shift toward high-quality diets has increased vitamin inclusion rates in feed formulations, while functional feed additives generate additional market value.

The South America swine feed market share captured by probiotics continues climbing, with an estimated CAGR of 7.18% during 2026-2031, as integrated producers pursue antibiotic-free label differentiation. Bacillus subtilis strains formulated for tropical feed conditions deliver stable spore counts during pelleting, securing performance advantages in high-temperature mills. Organic acidifiers, especially buffered formic–propionic blends, have become standard across large Brazilian complexes for Salmonella risk mitigation. Enzyme solutions targeting non-starch polysaccharide breakdown improve digestive energy yield, lowering feed cost per kilogram of gain amid currency swings.

Amino acids are gaining strategic attention as formulators lean on low-crude-protein diets to cut nitrogen emissions aligned with Environmental, Social and Governance metrics demanded by global buyers. Regional crushers have expanded threonine and tryptophan premix capacity, reducing import dependency. Emerging additive niches include precision-chelated minerals and essential oils backed by in-vivo efficacy data. Collectively, these innovations highlight the premiumization wave coursing through the South America swine feed market.

Geography Analysis

Brazil anchors regional dynamics, commanding 57.55% of value and sustaining trajectory at a 4.63% CAGR through 2031. Concentrated feed hubs in São Paulo, Paraná and Santa Catarina capitalize on proximity to grain belts and container ports, reducing inland transport premiums. AI-enabled logistics platforms now synchronize raw-material intake with production schedules, shrinking safety stocks and improving cash conversion cycles. Tax-reform credits slated for 2026-2033 will further enhance competitiveness by streamlining VAT recovery on imported micro-ingredients.

Argentina represents the fastest-moving geography, expanding at 6.05% CAGR (2026-2031) as pork solidifies its place in household menus. Consumer migration from beef accelerated in 2024 when retail prices for prime cuts surged beyond inflationary thresholds. Local crushers supply abundant soybean meal, allowing mills to deploy lower inclusion rates of imported amino acids. Government approval of Paraguay’s pork import certificate in March 2025 broadens outbound trade horizons, reinforcing producer confidence to build finisher barns that feed directly into the South America swine feed market.

Chile, Peru and Colombia combine cutting-edge technology with smaller herd bases, yielding niche opportunities for high-specification additives and data-driven herd management services. Chile’s Agrosuper sets the regional benchmark for feed-mill dosing precision, while Peru leverages new free-trade agreements to grow export-oriented pork segments. Colombia’s macro stability invites foreign direct investment into modern feed plants. Elsewhere, Uruguay, Paraguay and Bolivia slowly transition toward commercial rations, aided by knowledge transfer programs under the Standards and Trade Development Facility. These diverse trajectories collectively enrich growth prospects for the South America swine feed market.

Competitive Landscape

Moderate concentration characterizes the South America swine feed market, with the top five suppliers holding the majority of sales. Cargill, Inc. leads the market after layering AI-powered inventory tools onto its Brazilian mills in early 2025. ADM follows, leveraging proprietary premix blends and on-farm advisory teams to lock in loyalty among fast-scaling integrators. SHV Holdings’ position was reinforced by the acquisition of Bigsal, granting it a foothold in northern Brazil’s grain-deficit zone, where the logistics premium favors local manufacturing.

Strategic playbooks revolve around vertical integration and digital solutions that blend formulation science with real-time farm data. Cargill’s minority stake in Agriness embeds its nutritional algorithms inside a software ecosystem monitoring over 2 million sows. ADM has partnered with upstream growers to secure low-mycotoxin corn streams, mitigating quality risk amid climate variability. Regional challenger CLADAN taps exclusive distribution of CBS Bio Platforms’ feed enzymes, providing middle-tier mills with advanced solutions without the capital burden of in-house R&D.

Barriers to entry include stringent product registration at the Ministry of Agriculture, Livestock and Supply (MAPA) and National Service of Agrifood Health and Quality (SENASA), capital-intensive micro-ingredient handling and the technical expertise required for modern antibiotic-free diets. Localized service networks, credit facilities and sustainability credentials further separate incumbents from aspirants, shaping future consolidation waves within the South America swine feed market.

South America Swine Feed Industry Leaders

Cargill, Inc.

ADM

SHV Holdings

BRF Global

De Heus Animal Nutrition

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Brazil's Ministry of Agriculture established a regionalization agreement with Singapore that allows pork trade to continue if African swine fever is detected. The agreement stipulates that trade can proceed if outbreaks remain contained within specific zones, in accordance with World Organization for Animal Health guidelines. This agreement reflects Brazil's efforts to maintain export market access.

- October 2024: DSM-Firmenich inaugurated a new animal nutrition factory in Sete Lagoas, Minas Gerais, Brazil, with 100,000 metric tons per year capacity for livestock supplements, targeting beef and dairy markets with potential expansion into swine applications as demand grows.

- February 2024: Cargill expanded its operations in Brazil by acquiring the Anhambi Animal Production Plant in Pato Branco. The facility has an annual production capacity of 60,000 metric tons of pelleted feed.

- January 2024: JBS invested USD 116.6 million to construct three feed factories in Seberi, Santo Inácio, and Itaiópolis in Southern Brazil. The investment aligns input supply with the production capacity of its Seara business unit, which has expanded significantly in recent years through the company's investment plan. The new factories incorporate automated systems and advanced technology for input production.

South America Swine Feed Market Report Scope

Swine feed consists of a nutrient blend derived from plant and animal sources, primarily including soy meal, corn, barley, wheat, and sorghum, supplemented with essential minerals, vitamins, micro-nutrients, and antibiotics.

This report analyzes the South American swine feed market share, segmented by ingredient (cereals, cereal by-products, oilseed meal, oils, molasses, supplements, and others) and supplements (antibiotics, vitamins, antioxidants, amino acids, enzymes, acidifiers, probiotics & prebiotics, and others). The geographical scope covers Brazil, Argentina, and the rest of South America. The report provides market estimations and forecasts in USD value for these segments.

By Feed Type

| Starter Feed |

| Grower Feed |

| Sow Feed |

| Rest of Feed Types |

By Additives

| Vitamins |

| Amino Acids |

| Enzymes |

| Organic Acids |

| Probiotics and Prebiotics |

| Antibiotics |

| Rest of Feed Additives |

By Country

| Brazil |

| Argentina |

| Chile |

| Peru |

| Colombia |

| Rest of South America |

| By Feed Type | Starter Feed |

| Grower Feed | |

| Sow Feed | |

| Rest of Feed Types | |

| By Additives | Vitamins |

| Amino Acids | |

| Enzymes | |

| Organic Acids | |

| Probiotics and Prebiotics | |

| Antibiotics | |

| Rest of Feed Additives | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

How big is the South America Swine Feed Market?

The South America Swine Feed Market size is expected to reach USD 13.11 billion in 2026 and grow at a CAGR of 4.84% to reach USD 16.59 billion by 2031.

Which country drives the most demand for compound swine feed in South America?

Brazil supplies 57.55% of regional value, leveraging integrated supply chains and strong export orientation.

What is the expected growth rate for Argentina’s swine feed sector?

Argentina’s feed demand is forecast to grow at a 6.05% CAGR through 2031 as consumers substitute pork for costlier beef.

Which additives are gaining traction as antibiotic replacements?

Bacillus-based probiotics, buffered organic acids and tailored enzyme complexes are showing rapid adoption across major herds.

Page last updated on: