Precision Swine Farming Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

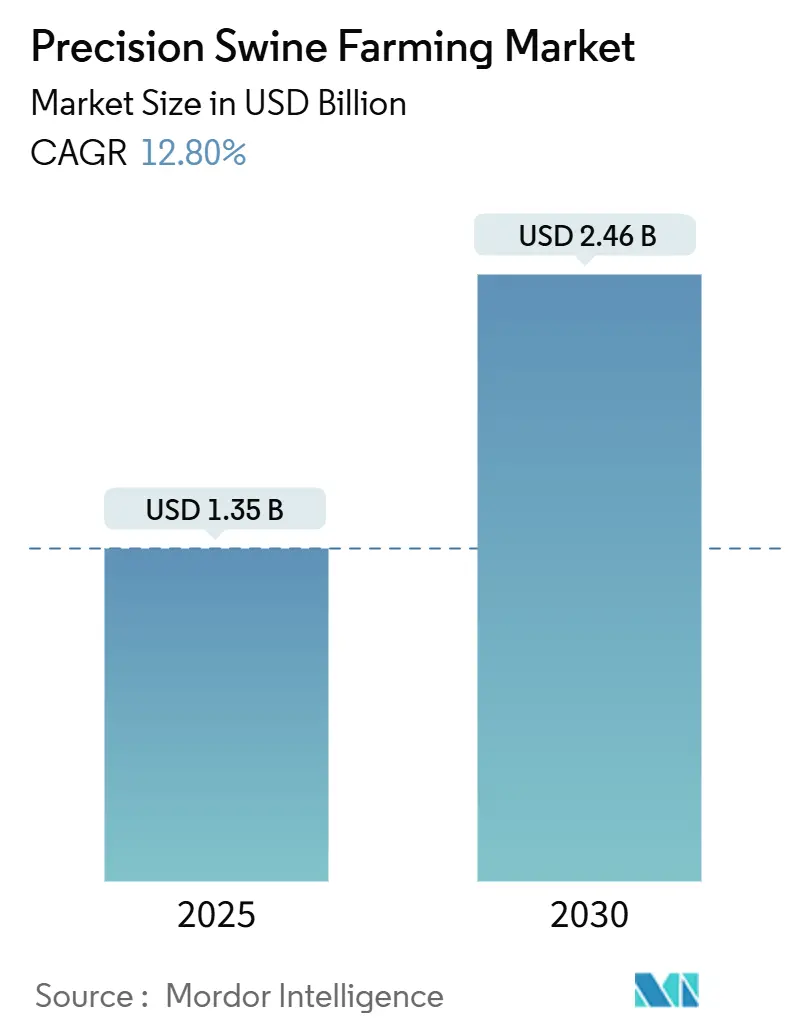

| Market Size (2025) | USD 1.35 Billion |

| Market Size (2030) | USD 2.46 Billion |

| Growth Rate (2025 - 2030) | 12.80% CAGR |

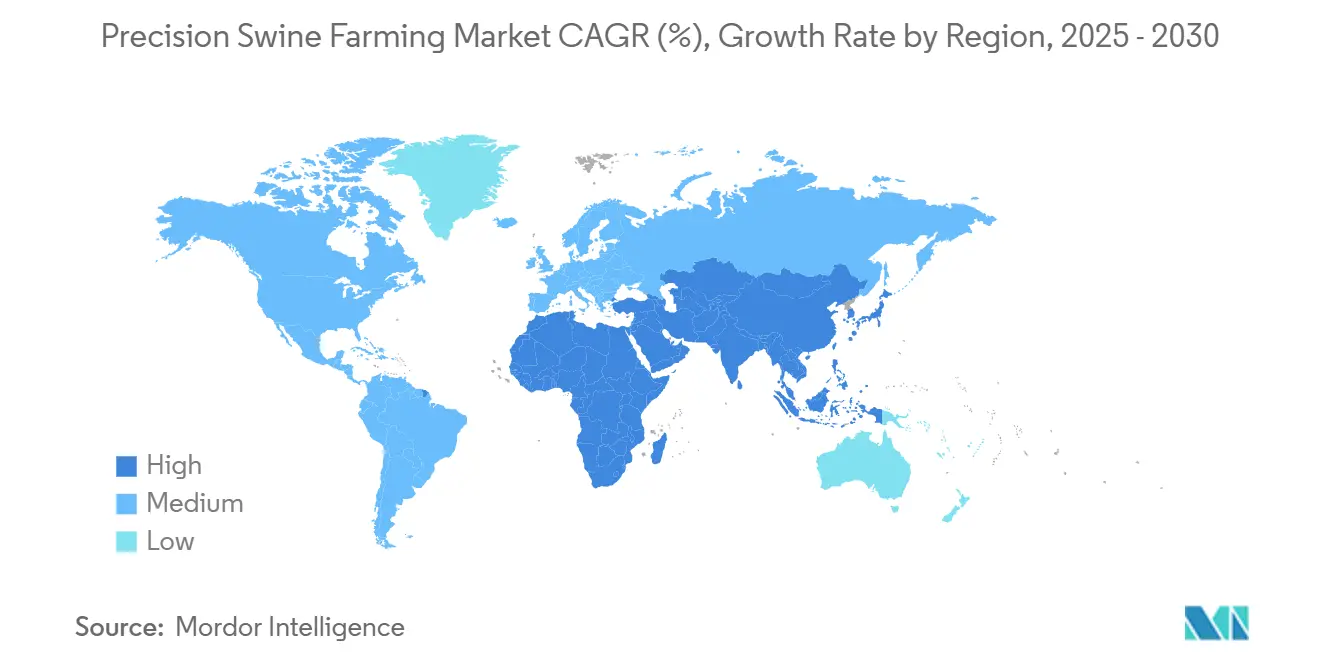

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Precision Swine Farming Market Analysis by Mordor Intelligence

The Precision Swine Farming Market size is estimated at USD 1.35 billion in 2025, and is expected to reach USD 2.46 billion by 2030, at a CAGR of 12.80% during the forecast period (2025-2030).

Expanding pork consumption, mounting regulatory pressure for antibiotic-free production, and rapid declines in sensor and connectivity costs are combining to reinforce steady capital deployment into precision livestock systems. Hardware remains the anchor purchase for most farms, yet software subscriptions and data-driven advisory services are beginning to compound revenue streams as producers pivot from one-off equipment buys to recurring analytics contracts. Strategic partnerships between feed, genetics, and pharmaceutical leaders with data analytics specialists are accelerating platform convergence, while rural 5G rollouts and low-earth-orbit satellite coverage are eliminating earlier connectivity constraints. Together, these forces position the precision swine farming market to record consistent double-digit growth through 2030.

Key Report Takeaways

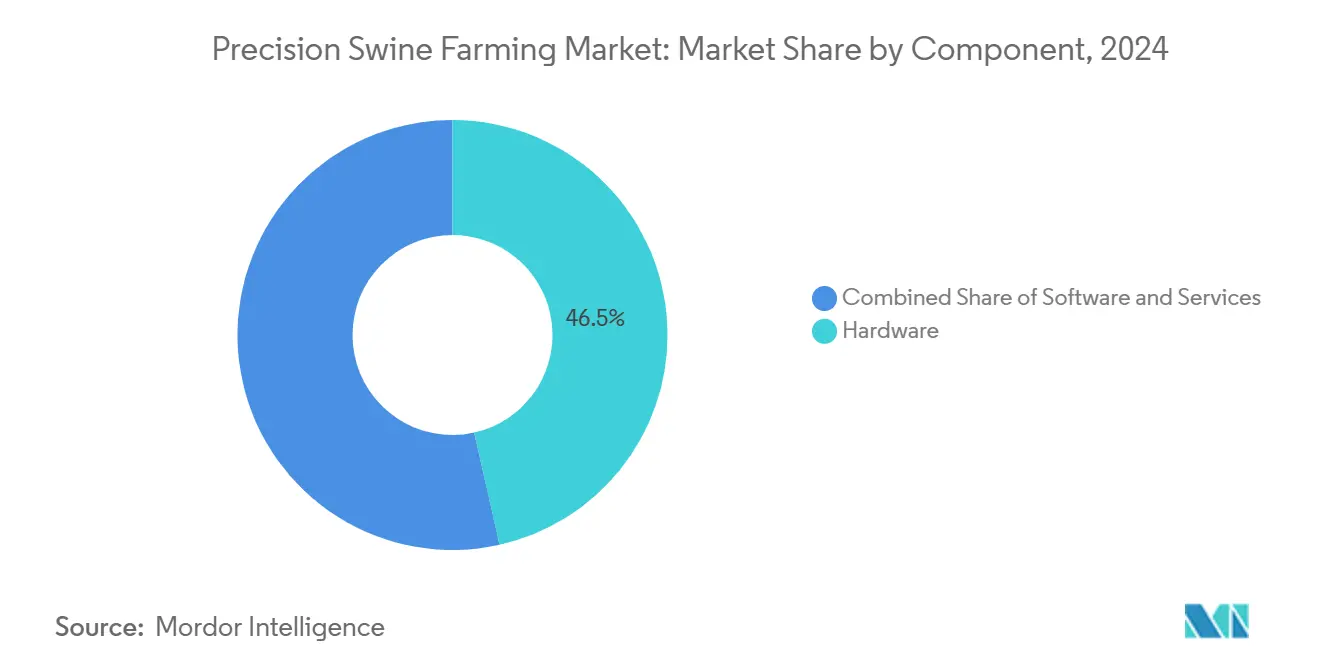

- By component, hardware led with 46.5% precision swine farming market share in 2024, while software is forecast to expand at a 15% CAGR through 2030.

- By technology, IoT and sensors accounted for 34.5% of the precision swine farming market size in 2024, and artificial intelligence is projected to advance at a 19% CAGR to 2030.

- By application, health monitoring captured 37% share of the precision swine farming market size in 2024 whereas waste management is anticipated to post an 18% CAGR during 2025-2030.

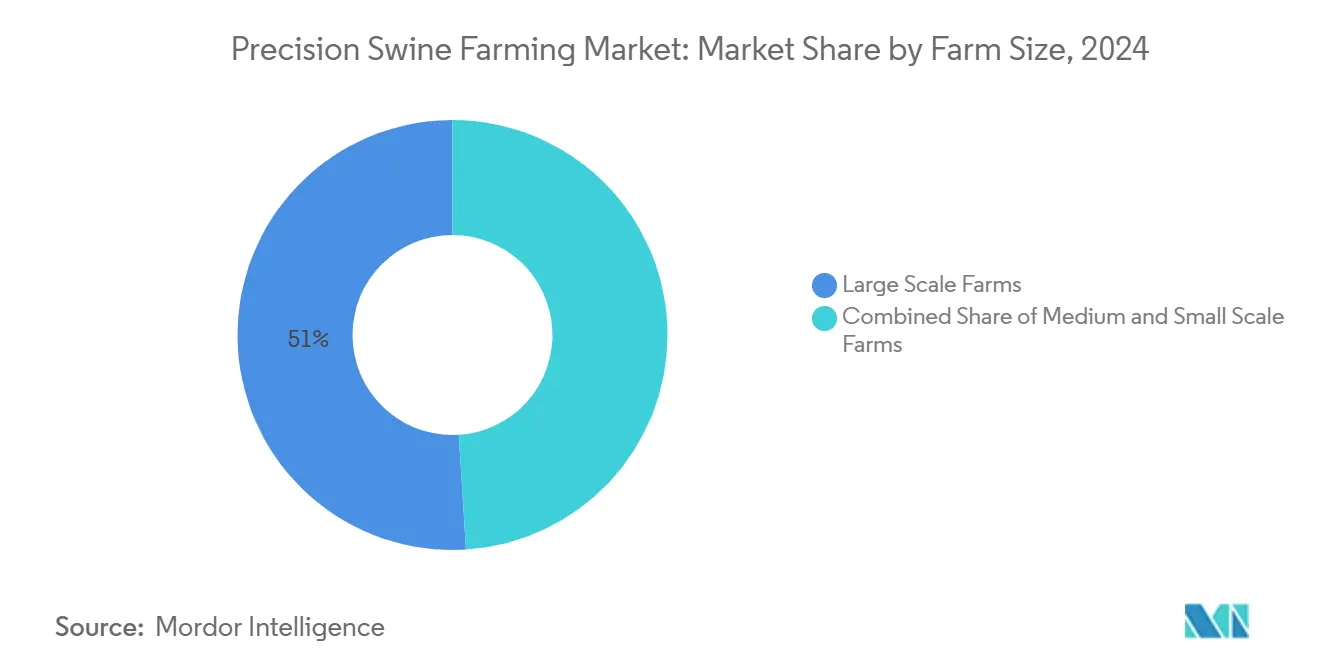

- By farm size, large-scale farms represented 51% precision swine farming market share in 2024, while medium-scale farms are likely to register a 14.5% CAGR through 2030.

- By geography, Europe held the largest regional share at 29% in 2024, and Asia-Pacific is set to exhibit the fastest growth at 16.5% CAGR over the forecast horizon.

Global Precision Swine Farming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in AI-enabled vision systems | +2.1% | Global, with Asia-Pacific leading adoption | Medium term (2-4 years) |

| Growing antibiotic-free pork demand | +2.8% | North America and Europe core markets | Short term (≤ 2 years) |

| IoT sensor price decline | +2.3% | Global, accelerated in Asia-Pacific | Short term (≤ 2 years) |

| Cloud connectivity in rural areas | +1.9% | North America and Europe infrastructure gains | Medium term (2-4 years) |

| ESG-linked agri-finance incentives | +1.7% | Europe and North America policy-driven | Long term (≥ 4 years) |

| Carbon-credit monetization for manure management | +1.4% | Global, with regulatory variations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in AI-enabled Vision Systems

Computer-vision platforms can now identify individual pigs and estimate real-time weight with error rates below 3%, cutting manual labor while lifting feed-conversion efficiency by up to 12%[1]Source: Shenzhen Stock Exchange, “Shenzhen Kingkey Smart Agriculture Annual Report 2024,” szse.cn. Funding momentum underscores the opportunity, with SwineTech securing USD 9.1 million Series A financing in December 2024 to commercialize piglet-safety analytics. Accelerating deployments in China and the United States demonstrate cross-regional viability, and new modules that detect lameness, aggression, and heat stress are already entering pilots.

Growing Antibiotic-Free Pork Demand

Retail and food-service multinationals have pledged to phase out routine antibiotics, compelling producers to adopt early-warning health systems capable of spotting illness 24-48 hours before visible symptoms. The European Union’s Veterinary Medicines Regulation, live since January 2024, further restricts prophylactic use, making data-driven diagnostics a commercial necessity. Real-time thermal imaging and behavior analytics help farms maintain animal welfare while retaining antibiotic-free certification, preserving premium price positions at retail.

IoT Sensor Price Decline

Average barn-environment sensors that cost USD 150 in 2022 now sell for USD 55, enabling holistic monitoring in medium-scale farms that manage 1,000-5,000 pigs [2]Source: IEEE Sensors Journal, “Cost Reduction Trends in Agricultural IoT Sensor Networks,” ieee.org. Suppliers in Shenzhen have engineered multi-parameter devices that track temperature, humidity, ammonia, and particulate matter for under USD 2,000 per building. This democratization of sensor technology is expanding the addressable market beyond large-scale industrial operations to include family-owned farms that represent major share of global swine production volume.

Cloud Connectivity in Rural Areas

The FCC 5G Fund and private-network deals such as John Deere and Verizon’s September 2024 agreement are delivering low-latency coverage to swine-heavy counties [3]Source: Federal Communications Commission, “5G Fund for Rural America Program Overview,” fcc.gov. Complementary satellite links from Starlink fill remaining gaps, allowing barns to stream continuous sensor feeds to cloud dashboards. The connectivity improvements enable cloud-based analytics platforms that can process data from thousands of sensors across multiple farm locations, providing insights that were previously impossible with on-premises computing limitations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for retrofitting legacy barns | -1.8% | Global, pronounced in Europe and North America | Short term (≤ 2 years) |

| Low digital literacy among smallholders | -1.4% | Asia-Pacific and Africa primarily | Medium term (2-4 years) |

| Cyber-biosecurity concerns | -0.9% | Global, regulatory focus in developed markets | Medium term (2-4 years) |

| Fragmented sensor interoperability standards | -0.7% | Global, industry standardization efforts ongoing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for Retrofitting Legacy Barns

Full precision upgrades can run USD 300,000 for a 1,000-head facility because many barns lack electrical, ventilation, and network backbones needed to support dense sensor arrays. Financing options remain limited, as traditional agricultural lenders often view precision farming technology as speculative rather than proven infrastructure investment. However, equipment leasing models are emerging as viable alternatives, with companies like Big Dutchman offering comprehensive technology packages. Government cost-share programs in Germany and the Netherlands have alleviated early outlays, but similar support is sparse elsewhere.

Low Digital Literacy Among Smallholders

Digital skills gaps among smallholder farmers represent a persistent adoption barrier, particularly in developing markets where 60-80% of swine producers operate facilities with fewer than 100 animals. Research conducted across Ghana, Nigeria, Kenya, and Uganda revealed that only 23% of smallholder farmers possess basic smartphone proficiency required for precision farming applications[4]Source: World Bank. "Digital Agriculture Report 2024: Bridging the Digital Divide in Rural Communities.", worldbank.org. Extension services and training programs are scaling to address these gaps, with organizations like the International Livestock Research Institute developing simplified user interfaces and local language support for precision farming platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Scale Sustains Leadership

Hardware contributed 46.5% precision swine farming market share in 2024, reflecting the physical infrastructure needed for data capture and automated control. The segment benefits from falling sensor prices and increased barn electrification, enabling wider deployment across finishing and farrowing units. Meanwhile, software revenues are forecast to advance 15% CAGR to 2030 as cloud analytics subscriptions expand. Services, including installation, calibration, and data interpretation, are also rising as producers seek external expertise to translate complex data streams into daily management actions.

Hardware maintains a central role because barns cannot exploit analytics without a dense device layer. Sensor clusters now integrate with automated feeders and climate control panels, creating closed-loop systems that adjust rations and ventilation on the fly. Software providers are layering machine-learning models atop these data flows, turning raw metrics into intuitive dashboards that flag anomaly conditions. Service partners routinely bundle quarterly on-farm audits, ensuring producers extract full value from connected equipment.

By Technology: AI Momentum Outpaces Foundational IoT

IoT and sensors accounted for 34.5% of the precision swine farming market size in 2024, yet artificial intelligence is on track for a 19% CAGR, making it the fastest technological riser. Initial deployments centered on simple environmental monitoring, but farms now demand predictive algorithms that transform historical records into actionable forecasts. Robotics is gaining traction for manure scraping and precision feeding, while blockchain pilots enhance traceability to satisfy export-market audits.

The precision swine farming market continues to shift from descriptive to prescriptive analytics. Vision-based AI models can pinpoint early lameness indicators, prompting treatment before performance drags. Feed suppliers integrate real-time growth curves into formulation software, automatically switching rations to match observed weight gain. Robotics platforms in Asia now perform routine barn sanitation, addressing labor shortages and biosecurity mandates. Although blockchain remains nascent, pilot programs in Denmark validate its potential to verify sustainability metrics from barn to retail shelf.

By Application: Health Monitoring Leads, Waste Management Gains Speed

Health monitoring dominated with 37% precision swine farming market share in 2024 because real-time disease detection underpins both welfare compliance and antibiotic-free positioning. Waste-management platforms are slated for an 18% CAGR through 2030, buoyed by monetization of manure-based carbon credits and tighter ammonia-emission caps in Europe. Nutrition optimization retains strong traction as feed remains roughly 65% of operating expenses, and environmental-control systems help mitigate climate-related heat stress episodes that erode average daily gain.

The precision swine farming industry is enlarging its scope from core health metrics toward holistic sustainability. Anaerobic digesters equipped with sensor suites now calibrate retention times to maximize biogas yield, offsetting electricity bills while trimming greenhouse gas releases. On the health front, infrared cameras detect fever spikes hours before caretakers notice clinical signs, enabling targeted treatment that maintains antibiotic-free status. Nutrition modules link genetic profiles with feed-intake data, personalizing diets to reduce feed conversion ratios below 2.3 in some finishing barns.

By Farm Size: Medium-Scale Operators Accelerate Catch-Up

Large-scale operations held a 51% precision swine farming market share in 2024, leveraging economies of scale to spread technology costs. Medium-scale farms are anticipated to grow 14.5% CAGR because falling device prices and simplified software interfaces make adoption feasible for herds between 1,000 and 4,999 pigs. Smallholders continue to face affordability barriers, though cooperatives that pool purchasing power are emerging in Southeast Asia.

Hardware vendors now offer modular kits calibrated to barn size, letting medium operators add capabilities in phases rather than commit to full retrofits immediately. Cloud dashboards feature a mobile-first design, suiting managers who handle chores directly rather than overseeing large staff counts. Over time, improved performance metrics could nudge consolidation, as digitized mid-scale barns demonstrate higher margins attractive to integrators.

Geography Analysis

Europe led the precision swine farming market with a 29% share in 2024. Adoption surged after the European Commission amended the Industrial Emissions Directive, mandating real-time environmental reporting for sites exceeding 2,000 pig places [5]Source: European Commission. "Industrial Emissions Directive Revision 2024." Environment and Climate Action, ec.europa.eu. Germany, Spain, and the Netherlands provide subsidies covering up to 40% of eligible hardware purchases, encouraging rapid modernization. Although the regional CAGR is moderately growing, as early-stage rollouts wane, replacement cycles for legacy sensors and software upgrades sustain demand.

Asia-Pacific is the fastest-growing region at 16.5% CAGR. China’s recovery from African swine fever spurred mega-farm construction that embeds IoT frameworks from inception. Public-private research hubs in Guangdong and Sichuan test AI algorithms on million-head complexes, accelerating technology diffusion. Japan applies precision breeding and waste heat-capture systems to raise premium pork, whereas Vietnam and Thailand emphasize affordable sensor bundles for family-run barns. Indigenous manufacturing capacity trims hardware costs, reinforcing domestic uptake.

North America is another key market. In the United States, chronic labor shortages heighten interest in robotics for feeding and cleaning tasks. The USDA’s revised precision-agriculture framework now clarifies data-ownership rules, encouraging producers to engage cloud vendors. Canada extends tax credits for emission-cutting investments, benefiting manure-to-energy projects. Mexico’s export ambitions for the Japanese market incentivize blockchain traceability pilots, even as industry groups lobby for customs harmonization. Collectively, advanced telecom networks, supportive policy, and established integrator structures sustain steady growth momentum.

Competitive Landscape

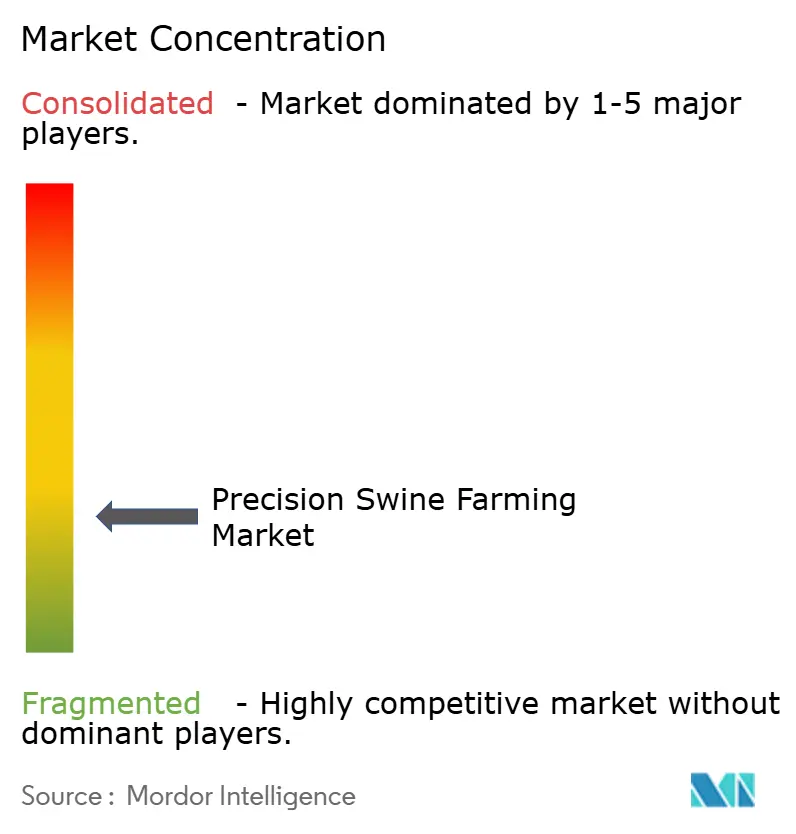

The precision swine farming market remains fragmented with the top five players being actively involved in strategic initiatives to strengthen their presence in the market. Nedap Livestock Management and Genus plc leverage end-to-end platforms that bundle feeding stations, weight-monitoring scales, and genetic analytics. Emerging firms such as SwineTech focus narrowly on high-value use cases like piglet survival, quickly scaling through software-as-a-service contracts. Hardware stalwarts including Big Dutchman partner with telecom and cloud providers to strengthen data-delivery guarantees, differentiating on service quality.

Mergers and minority-stake investments signify a race to assemble comprehensive ecosystems. Merck Animal Health’s January 2025 investment in LeeO Precision Farming merges pharmaceutical know-how with continuous monitoring capabilities, aiming to embed treatment protocols directly into farm dashboards. DSM-Firmenich integrates feed-formulation algorithms with barn sensors, allowing real-time ration adjustments that preserve growth targets while minimizing nitrogen excretion. Cyber-security specialists eye entry as insurers and regulators insist on hardened agricultural networks, presenting an underserved niche.

Barriers to entry hinge less on raw hardware IP than on data stewardship, algorithm performance, and multi-brand interoperability. Vendors that can simplify deployment, guarantee uptime, and translate terabytes of sensor output into actionable alerts will outpace equipment-only rivals. Opportunities also lie in mid-market bundling, where integrators curate curated kits of best-of-breed devices under single service contracts, shielding farmers from vendor-lock risks and steep learning curves while creating incremental recurring revenue.

Precision Swine Farming Industry Leaders

-

Nedap N.V.

-

TOPIGS NORSVIN

-

Genus plc.

-

Big Dutchman

-

Zoetis Services LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: The European Commission finalized Industrial Emissions Directive revisions requiring continuous emissions monitoring in large livestock sites. The new regulations mandate real-time emissions monitoring and data reporting, driving precision farming adoption across European swine operations.

- March 2024: DSM-Firmenich launched an adaptive nutrition concept for fattening pigs and a new Verax DBS Analytics service.

- September 2022: Merck Animal Health announced a strategic investment in LeeO Precision Farming to co-develop integrated swine health-management platforms.

- September 2021: SwineTech raised USD 9.1 million in Series A funding to scale its AI piglet-protection technology The technology addresses a critical problem that causes 15-20% mortality in newborn pigs across global swine operations.

Global Precision Swine Farming Market Report Scope

| Hardware |

| Software |

| Services |

| IoT and Sensors |

| Artificial Intelligence |

| Big Data Analytics |

| Robotics and Automation |

| Cloud Computing |

| Blockchain Traceability |

| Nutrition Optimization |

| Health Monitoring |

| Breeding Management |

| Environmental Control |

| Waste Management |

| Large-Scale Farms |

| Medium-Scale Farms |

| Small-Scale Farms |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Kenya | |

| Rest of Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Technology | IoT and Sensors | |

| Artificial Intelligence | ||

| Big Data Analytics | ||

| Robotics and Automation | ||

| Cloud Computing | ||

| Blockchain Traceability | ||

| By Application | Nutrition Optimization | |

| Health Monitoring | ||

| Breeding Management | ||

| Environmental Control | ||

| Waste Management | ||

| By Farm Size | Large-Scale Farms | |

| Medium-Scale Farms | ||

| Small-Scale Farms | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current global value of the precision swine farming market?

The market is valued at USD 1.35 billion in 2025.

How fast is the sector expected to grow through 2030?

It is projected to post a 12.8% CAGR and reach USD 2.46 billion by 2030.

Which component segment commands the largest revenue share?

Hardware leads with 46.5% share due to the foundational need for sensors and automation equipment.

Which application area is expanding the fastest?

Waste management systems are growing at an 18% CAGR on tighter environmental rules and carbon credit incentives

Why is Asia-Pacific considered the most dynamic regional opportunity?

China’s large-scale farm modernization, domestic manufacturing, and supportive policy combine to drive a 16.5% regional CAGR.

Page last updated on: