Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

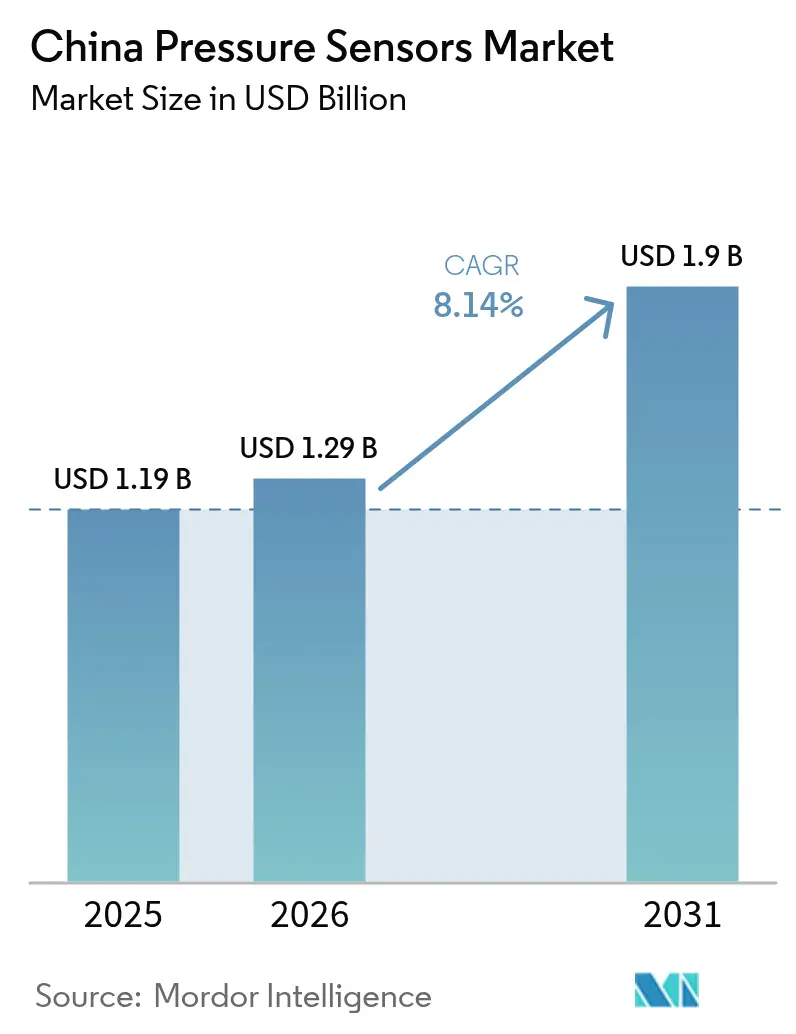

| Base Year Market Size (2025) | USD 1.19 Billion |

| Market Size (2026) | USD 1.29 Billion |

| Market Size (2031) | USD 1.9 Billion |

| Growth Rate (2026 - 2031) | 8.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Pressure Sensors Market Analysis by Mordor Intelligence

The China pressure sensors market size was valued at USD 1.19 billion in 2025 and estimated to grow from USD 1.29 billion in 2026 to reach USD 1.9 billion by 2031, at a CAGR of 8.14% during the forecast period (2026-2031). Rising semiconductor self-sufficiency goals, rapid vehicle electrification, and factory digitization collectively underpin expansion. MEMS miniaturization breakthroughs enable battery-powered and space-constrained designs, while supportive funding policies accelerate domestic fabs. Demand intensifies from electric vehicles, industrial automation, and medical wearables, each requiring precise, low-power sensing. International suppliers still lead niche high-reliability categories, yet local champions scale aggressively, narrowing technology gaps and shortening lead times.

Key Report Takeaways

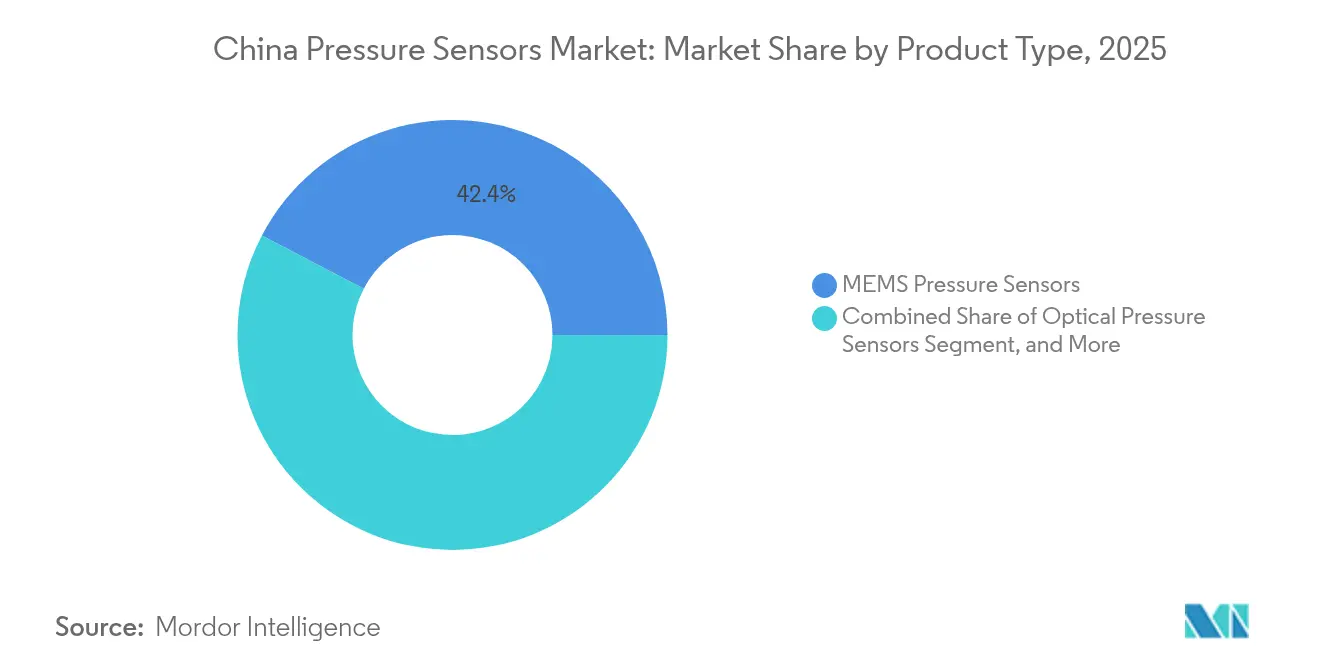

- By product type, MEMS pressure sensors held 42.35% of the China pressure sensors market share in 2025.

- By pressure measurement, gauge pressure sensors led with 48.25% revenue share in 2025 in the China pressure sensors market; differential pressure sensors will expand at a 9.68% CAGR through 2031.

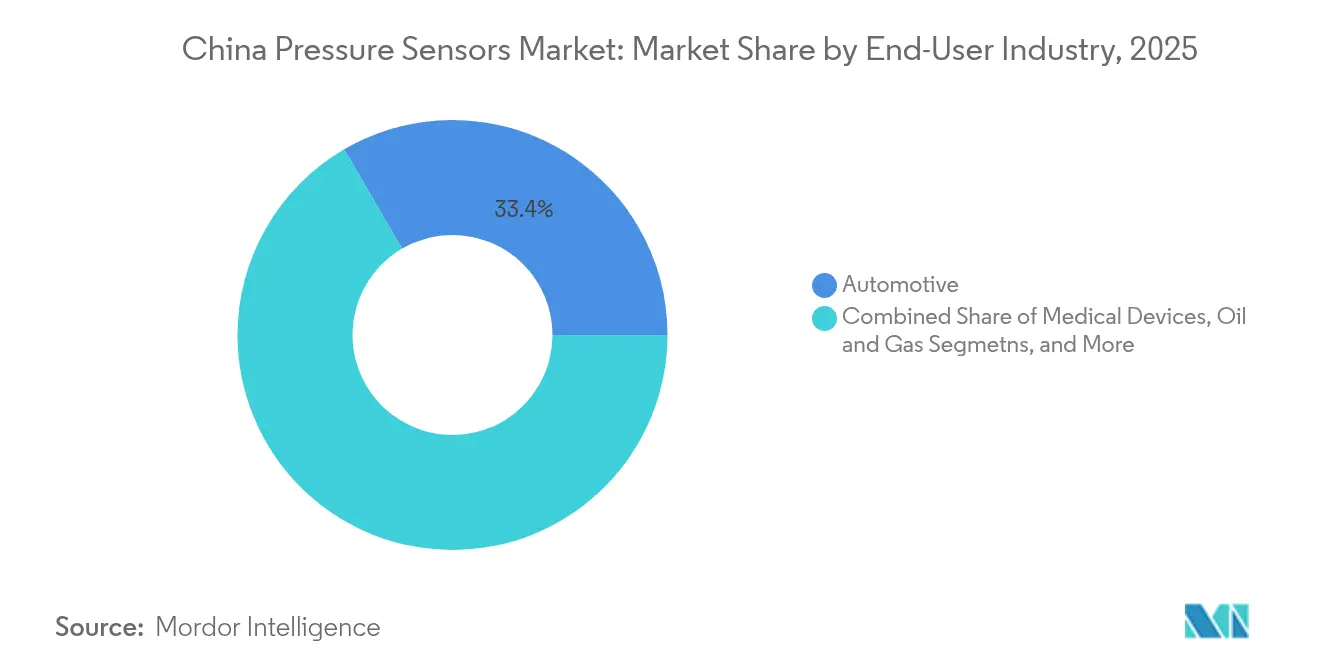

- By end-user industry, automotive accounted for 33.40% of the China pressure sensors market size in 2025, while medical devices record the highest projected CAGR at 9.25% to 2031.

- By technology platform, piezoresistive sensors retained 37.10% share in 2025 in the China pressure sensors market; capacitive MEMS is projected to grow at 9.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Pressure Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating adoption of MEMS-based miniaturized sensors in electric vehicles | +2.1% | National, with concentration in East and South China manufacturing hubs | Medium term (2-4 years) |

| Government incentives for domestic semiconductor self-sufficiency and sensor localization | +1.8% | National, with priority zones in Xiong'an, Wuxi, and Shenzhen | Long term (≥ 4 years) |

| Expansion of Industry 4.0 smart manufacturing across Chinese industrial parks | +1.5% | East China, South China, with spillover to Central and North China | Medium term (2-4 years) |

| Rising demand for high-precision medical devices and wearable health monitoring | +1.3% | National, with early adoption in tier-1 cities | Short term (≤ 2 years) |

| HVAC and smart-building retrofits boosting demand for wireless pressure sensors | +0.9% | Urban centers nationwide, concentrated in East and South China | Medium term (2-4 years) |

| Digital oil and gas field development requiring harsh-environment pressure sensing | +0.8% | West China, Northeast China, with offshore applications in South China Sea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of MEMS-Based Miniaturized Sensors in Electric Vehicles

China’s electric-vehicle leadership pushes unprecedented volumes for compact, automotive-qualified pressure sensors. Domestic fabs now deliver millions of MEMS units annually, lowering import dependence and ensuring supply resilience.[1]China Electronics Technology Corporation, “Automotive MEMS Production Expansion,” cetc.com.cn Each EV integrates 15–20 sensing points for thermal management, braking, and ADAS functions, and the convergence of autonomy with electrification multiplies sensor content per car. Robust designs withstand −40 °C to 150 °C temperature swings and high vibration, meeting AEC-Q103 reliability demands. Rapid battery-pack innovation further fuels demand for high-accuracy differential sensors that monitor cell pressure for safety. As automakers localize component sourcing, price-performance dynamics favor homegrown MEMS that match global specifications at lower landed cost.

Government Incentives for Domestic Semiconductor Self-Sufficiency and Sensor Localization

National and provincial programs earmark substantial grants, tax incentives, and low-interest loans for sensor fabs and R&D centers.[2]National Development and Reform Commission, “Sensor Localization Policies,” ndrc.gov.cn Wuxi High-tech Zone alone raised several hundred million RMB for four pressure-sensor start-ups in 2024, funding cleanroom expansion and backend packaging lines. Sensor pilot lines now benefit from shared metrology labs, lowering entry barriers for small firms. The 14th Five-Year Plan prioritizes core process equipment, aiming to lift domestic content above 70% by 2030. Strategic clusters in Xiong’an and Shenzhen offer expedited permitting, discounted land, and workforce subsidies, accelerating time-to-market for qualified devices.

Expansion of Industry 4.0 Smart Manufacturing Across Chinese Industrial Parks

Smart-factory rollouts heighten demand for networked, self-diagnosing pressure nodes that feed MES and cloud analytics platforms. Wireless variants cut cabling costs on retrofit lines and facilitate quick re-layout for short production runs. High-accuracy sensors enable closed-loop adaptive control, reducing scrap and unplanned downtime. Precision industries, semiconductor, pharmaceutical, and precision machining, require ±0.05 %FS accuracy under thermal cycling, spurring uptake of capacitive MEMS. The coupling of 5G and edge AI supports ultra-low-latency monitoring across sprawling industrial estates, while cybersecurity requirements drive adoption of encrypted sensor buses.

Rising Demand for High-Precision Medical Devices and Wearable Health Monitoring

An aging population and post-pandemic digital-health push fuel multi-parameter wearables that incorporate tiny barometric elements for blood-pressure trends and sleep-apnea alerts. Domestic R&D teams leverage proprietary algorithms for greater accuracy, shortening the feedback loop between sensor output and patient insights. NMPA reforms streamline device approvals, cutting review cycles by up to 30 %. Hospital procurement shifts toward localized suppliers, citing faster service and custom firmware upgrades. Home ventilators and infusion pumps adopt redundant pressure lines to meet stringent patient-safety norms, further increasing unit counts per device.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in silicon-wafer and rare-earth material prices | -1.2% | Global supply chains affecting all Chinese manufacturing regions | Short term (≤ 2 years) |

| High reliability-certification barriers for automotive-grade sensors | -0.8% | National, with particular impact on automotive manufacturing clusters | Medium term (2-4 years) |

| Intellectual-property disputes limiting export opportunities | -0.7% | National, affecting export-oriented manufacturers | Long term (≥ 4 years) |

| Short product lifecycles causing rapid obsolescence for consumer-grade sensors | -0.5% | Consumer electronics hubs in South and East China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Silicon-Wafer and Rare-Earth Material Prices

Global wafer-fab cycles create sharp price swings; 2024 spot silicon rose 38% before softening in late Q4. China’s dominance in rare-earth processing introduces additional uncertainty, as export-quota adjustments and geopolitical tensions influence Nd- and Pr-based compound pricing.[3]International Energy Agency, “Global Critical Minerals Outlook 2024,” iea.org Manufacturers hedge by multi-sourcing and holding higher safety stocks, tying up working capital and pressuring gross margins. Larger fabs leverage forward contracts, but smaller houses face squeezed book-to-bill ratios, delaying capacity upgrades. Accelerated recycling programs may partly ease supply-chain risk after 2026.

High Reliability-Certification Barriers for Automotive-Grade Sensors

ISO 26262 ASIL D validation demands over 18 months of design-for-safety audits, failure-mode analysis, and traceability. China’s GB/T 34590.1-2022 harmonizes local requirements, yet extensive documentation and test tooling remain cost-intensive. Early movers such as Axera Semiconductor secured full ASIL D process approval in 2024, but many peers still progress through lower readiness levels. Automakers consequently dual-source with incumbent global suppliers, limiting near-term share gains for local challengers. Joint ventures offering shared qualification labs emerge to reduce per-company burden.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: MEMS technology accelerates miniaturization leadership

MEMS devices accounted for 42.35% of the China pressure sensors market share in 2025, and this category is projected to grow at a 9.34% CAGR to 2031. MEMS dies fabricated on 8-inch CMOS lines leverage mature tooling, delivering high yield and low unit cost. Simultaneous integration of ADCs and temperature compensation logic enables plug-and-play modules, supporting drop-in replacement across industries. Capacitive sensors maintain a loyal base in industrial pneumatics thanks to superior overload tolerance, whereas piezoelectric variants meet aerospace vibration needs. Strain-gauge sensors serve heavy machinery requiring rugged mechanical bonding. Optical pressure sensors occupy small niches in high-EMI zones such as power-generation switchyards. Hybrid smart modules that pair MEMS cores with BLE or Wi-Fi microcontrollers illustrate an evolution from single-parameter measurement toward holistic condition monitoring.

The China pressure sensors market size for MEMS designs benefits from automotive and medical synergies, where miniaturization, low power, and fast response converge. Domestic IDMs invest in wafer-level chip-scale packaging to shrink Z-height for smartwatches and hearables. Strategic partnerships with ASIC design houses reduce BOM cost, quickening competitive cycles. As fabs qualify 12-inch MEMS tooling after 2027, die output per wafer will rise, further lowering cost curves and widening adoption into price-sensitive appliances.

By Pressure Measurement: Differential sensing drives precision growth

Gauge variants led the China pressure sensors market with 48.25% revenue in 2025, serving air-brake, HVAC, and hydraulic circuits. However, differential devices will record the highest 9.68% CAGR, propelled by flow metering, filter monitoring, and smart-building VAV control. Vacuum and sealed-reference devices supply semiconductor tools and laboratory instrumentation where absolute accuracy below 10 mTorr is mandatory. Wireless differential modules achieve sub-Pascal resolution at 1 µA sleep currents, aligning with battery-powered retrofit projects.

China pressure sensors market size gains in differential configurations mirror expanding digital oilfield programs and high-rise energy audits. As construction codes tighten envelope-leakage limits, air-flow balancing becomes mandatory, lifting sensor attach rates per floor. Manufacturers improve long-term stability via silicon-on-insulator diaphragms and proprietary micro-porous reference cavities, curbing drift below 0.1% per year. Emerging micro-fluidic dosing lines in biotech plants adopt millibar-range differential sensing to assure dosing accuracy.

By End-User Industry: Medical devices outpace automotive expansion

Automotive retained 33.40% share of the China pressure sensors market size in 2025, driven by ICE manifold absolute pressure monitoring, EV battery stress detection, and tire-pressure systems. Still, medical devices are forecast to grow fastest at a 9.25% CAGR, supported by aging demographics, tele-health uptake, and NMPA fast-track routes. Home dialysis, infusion pumps, and CPAP units deploy miniature absolute and differential sensors, often in redundant arrays for fail-safe design. Aerospace, chemical, and oil-and-gas verticals demand high-temperature hermetic packages in low volumes yet high ASPs.

China pressure sensors market adoption in medical settings benefits from government reimbursements for remote patient monitoring, bolstering hospital procurement of wearable patches. Domestic OEMs leverage flexible sensor membranes to conform to skin curvature, improving comfort and signal fidelity. Automotive, while mature, injects new demand through hydrogen-fuel cell pressure stacks and advanced thermal management for 800 V architectures. Consumer electronics remain volume leaders yet face ASP compression and rapid design churn.

By Technology Platform: Capacitive MEMS sets innovation pace

Piezoresistive silicon continues to command 37.10% share thanks to well-established processes and linear output. Capacitive MEMS, however, is projected at a 9.32% CAGR, favored for energy-harvesting IoT nodes where sub-microamp quiescent current matters. Optical fiber sensors cater to high-voltage substations and downhole wells where EMI resilience is critical. Resonant solid-state devices provide ppm-level accuracy for national standards labs and aerospace IMUs, albeit at premium pricing.

The China pressure sensors market now witnesses hybrid assemblies merging capacitive MEMS cores with resonant reference cavities, delivering digital outputs immune to aging drift. Nano-structured graphene diaphragms under pilot production showcase mbar sensitivity with flexure under 100 Pa, opening pathways for soft-robotics and e-skin. Flexible printed sensors on polyimide films enable disposable medical patches, supporting mass screening campaigns without sterilization overhead.

Geography Analysis

East China, led by Jiangsu and Shanghai, commanded the largest regional slice of the China pressure sensors market in 2025. Dense clusters of semiconductor fabs, automotive assembly plants, and consumer-electronics EMS providers anchor demand. Provincial grants subsidize ISO 17025 calibration labs, encouraging in-region qualifying cycles. Shanghai’s free-trade zone eases the import of photolithography tools, while local universities supply MEMS design talent.

South China will post the fastest regional CAGR through 2031 as Shenzhen’s electronics corridor and Guangzhou’s EV plants expand output. Abundant surface-mount lines and rapid prototyping hubs shorten design-win cycles. Guangdong’s “Advanced Manufacturing 2025” blueprint sets subsidies for Industry 4.0 sensors deployed in SMEs, stimulating adoption among parts suppliers. Export proximity to ASEAN markets further elevates volumes.

North and Central China grow steadily, supported by state-owned heavy-industry modernization. Retrofit mandates for steel mills and coal-to-chemicals complexes in Hebei and Shanxi drive rugged, high-pressure sensor installations. West China’s oil and gas basins adopt downhole sensors resistant to sour environments, while Northeast China’s revitalization policies encourage automotive component relocation, boosting local sensor attach rates. Combined inland gains diversify the overall China pressure sensors market base beyond coastal megahubs.

Competitive Landscape

Global leaders Honeywell, Bosch, and Infineon retain technological edges in high-reliability and safety-critical segments. Honeywell’s Nanjing plant, its largest sensor site worldwide, ships roughly 300 million units annually, leveraging economies of scale. Bosch maintains dual fab lines for piezoresistive dies and ASICs, ensuring vertical integration and strict defect-density control. Infineon exploits 300 mm MEMS lines for cost leadership in tire-pressure sensors.

Local vendors accelerate catch-up. CETC scales automotive MEMS production to two million ASIL-D certified units yearly, targeting domestic EV makers. Shanghai Zhaohui invests in EU lithography to upgrade critical dimensions, narrowing gap in diaphragm uniformity. Xi’an UTOP partners with German test-rig suppliers to build GB/T 34590 labs, expediting qualification cycles. Tier-2 challengers pursue application niches, oilfield, medical, or wearable, where bespoke design and proximity support beat generic imports.

Platform strategies gain favor: several Chinese groups bundle pressure, temperature, and humidity sensors with common digital ASICs and firmware, cutting BOM costs and unifying API calls for IoT gateways. Software ecosystems become differentiators as predictive-maintenance dashboards deliver higher margins than standalone hardware. Consolidation looms; capital-constrained micro-fabs may merge to achieve wafer volumes needed for 12-inch migration.

China Pressure Sensors Industry Leaders

Shanghai Zhaohui Pressure Apparatus Co.,Ltd

Ericco International Limited

TM Automation Instruments Co., Ltd.

All Sensors Corporation

Xi'an UTOP Measurement Instrument Co., Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: China Electronics Technology Corporation doubled automotive pressure-sensor capacity to 2 million units, supplying ASIL D-qualified EV modules.

- December 2024: Wuxi High-tech Zone raised several hundred million RMB for four pressure-sensor start-ups focusing on Industry 4.0 and IoT.

- November 2024: Shanghai Zhaohui procured advanced MEMS lithography tools from Europe to enhance automotive-grade yield.

- October 2024: Xi’an UTOP partnered with a German tester supplier to establish GB/T 34590 certification lines for automotive sensors.

China Pressure Sensors Market Report Scope

The report studies the relation of market drivers like emphasis on miniaturization of equipment and robust designing with enhanced performance in rugged environment of various components on Pressure Sensor development and production in China along with the effect of technical issues associated with the involvement of smaller components. The study's sope includes the segmentation of pressure sensors by Product (Capacitive, MEMS, Strain gauge, Bourdon, Vacuum Pressure), and by End-user Vertical (Automotive, Aerospace & Military, Chemical & Petrochemical, Medical, HVAC, Power Generation). The study also tracks the impact of COVID-19 on the industry landscape in the country.

By Product Type

| MEMS Pressure Sensors |

| Capacitive Pressure Sensors |

| Piezoelectric Pressure Sensors |

| Strain Gauge Pressure Sensors |

| Optical Pressure Sensors |

| Other Product Types |

By Pressure Measurement

| Gauge Pressure Sensors |

| Absolute Pressure Sensors |

| Differential Pressure Sensors |

| Vacuum Pressure Sensors |

| Sealed Reference Pressure Sensors |

By End-user Industry

| Automotive |

| Aerospace and Defense |

| Chemical and Petrochemical |

| Medical Devices |

| HVAC and Building Automation |

| Power Generation |

| Industrial Manufacturing |

| Oil and Gas |

| Consumer Electronics |

| Other Industries |

By Technology Platform

| Piezoresistive |

| Capacitive MEMS |

| Optical Fiber |

| Resonant Solid State |

| Electromagnetic |

| Nano and Flexible |

| By Product Type | MEMS Pressure Sensors |

| Capacitive Pressure Sensors | |

| Piezoelectric Pressure Sensors | |

| Strain Gauge Pressure Sensors | |

| Optical Pressure Sensors | |

| Other Product Types | |

| By Pressure Measurement | Gauge Pressure Sensors |

| Absolute Pressure Sensors | |

| Differential Pressure Sensors | |

| Vacuum Pressure Sensors | |

| Sealed Reference Pressure Sensors | |

| By End-user Industry | Automotive |

| Aerospace and Defense | |

| Chemical and Petrochemical | |

| Medical Devices | |

| HVAC and Building Automation | |

| Power Generation | |

| Industrial Manufacturing | |

| Oil and Gas | |

| Consumer Electronics | |

| Other Industries | |

| By Technology Platform | Piezoresistive |

| Capacitive MEMS | |

| Optical Fiber | |

| Resonant Solid State | |

| Electromagnetic | |

| Nano and Flexible |

Key Questions Answered in the Report

What is the size of the China pressure sensors sector in 2026?

Sales reach USD 1.29 billion in 2026 and are projected to rise to USD 1.9 billion by 2031.

What CAGR is forecast for China pressure sensor sales through 2031?

Revenue is expected to expand at an 8.14% CAGR over the 2026-2031 period.

Which product type currently holds the largest share in China pressure sensors?

MEMS pressure sensors led with 42.35% share in 2025 and are also the fastest-growing category.

Which end-user segment is predicted to grow fastest through 2031?

Medical devices post the highest forecast CAGR at 9.25%, driven by wearables and remote-care equipment.

Who are the leading companies producing pressure sensors in China?

Global players Honeywell, Bosch, and Infineon maintain technological leadership, while CETC and Shanghai Zhaohui are fast-scaling domestic challengers.

Page last updated on: