Polystyrene Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

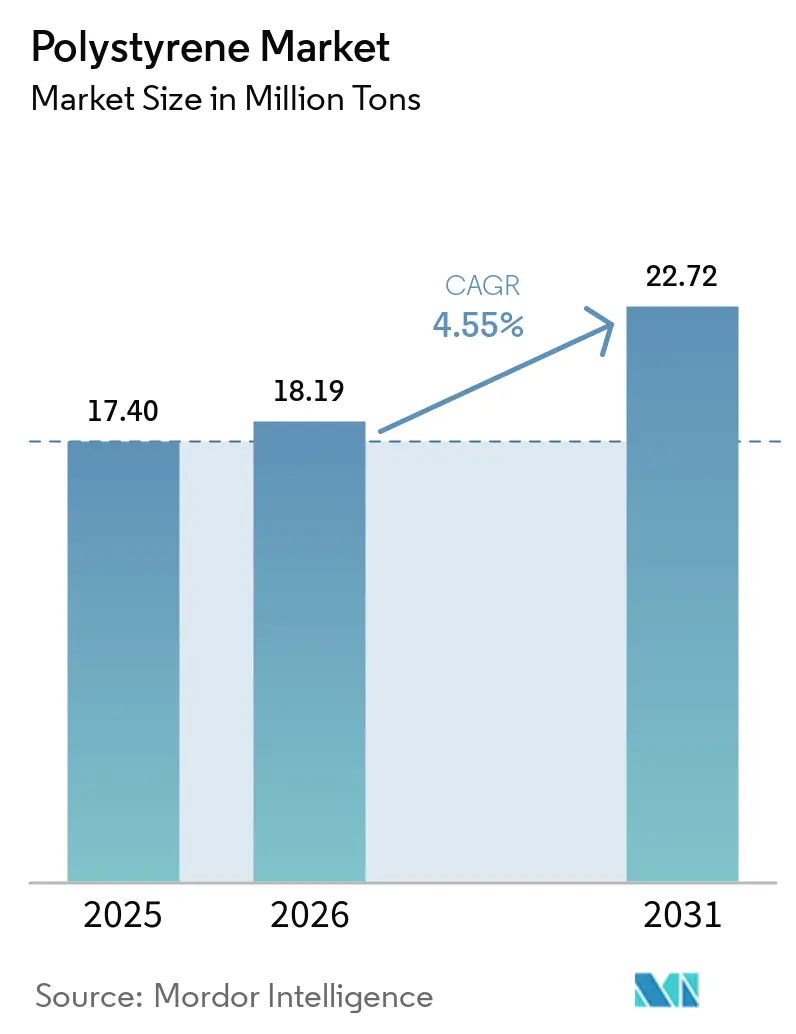

| Market Volume (2026) | 18.19 Million tons |

| Market Volume (2031) | 22.72 Million tons |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Polystyrene Market Analysis by Mordor Intelligence

The Polystyrene Market size is projected to expand from 17.40 million tons in 2025 and 18.19 million tons in 2026 to 22.72 million tons by 2031, registering a CAGR of 4.55% between 2026 to 2031. This expansion is being powered by stricter building-insulation codes, booming e-commerce logistics, and cold-chain pharmaceutical roll-outs, even as single-use plastic bans curb growth in food-service channels. Producers with access to low-cost ethane feedstock in North America continue to benefit from a 20-25% cost advantage, while Asia-Pacific suppliers leverage scale to dominate exports into neighboring emerging economies. Capital is flowing into chemical-recycling pilots that promise styrene monomer quality suitable for food contact, and the first commercial deliveries in 2025 have validated the business case. Simultaneously, equipment upgrades in injection molding and extrusion are broadening the addressable base for higher-value, performance-critical applications.

Key Report Takeaways

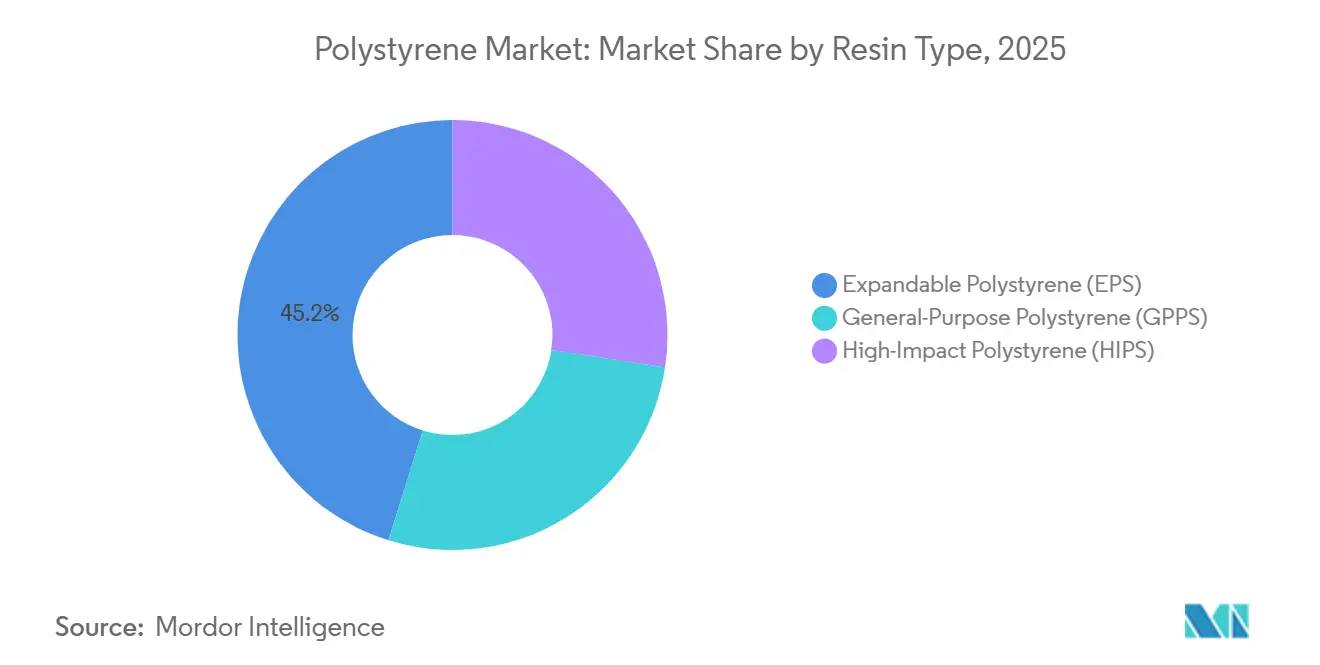

- By resin type, expandable polystyrene held 45.19% of the market share in 2025; general-purpose polystyrene is projected to post the fastest 5.51% CAGR through 2031.

- By form factor, foams captured 59.67% volume in 2025, while other form types are expected to grow at a 5.02% CAGR to 2031.

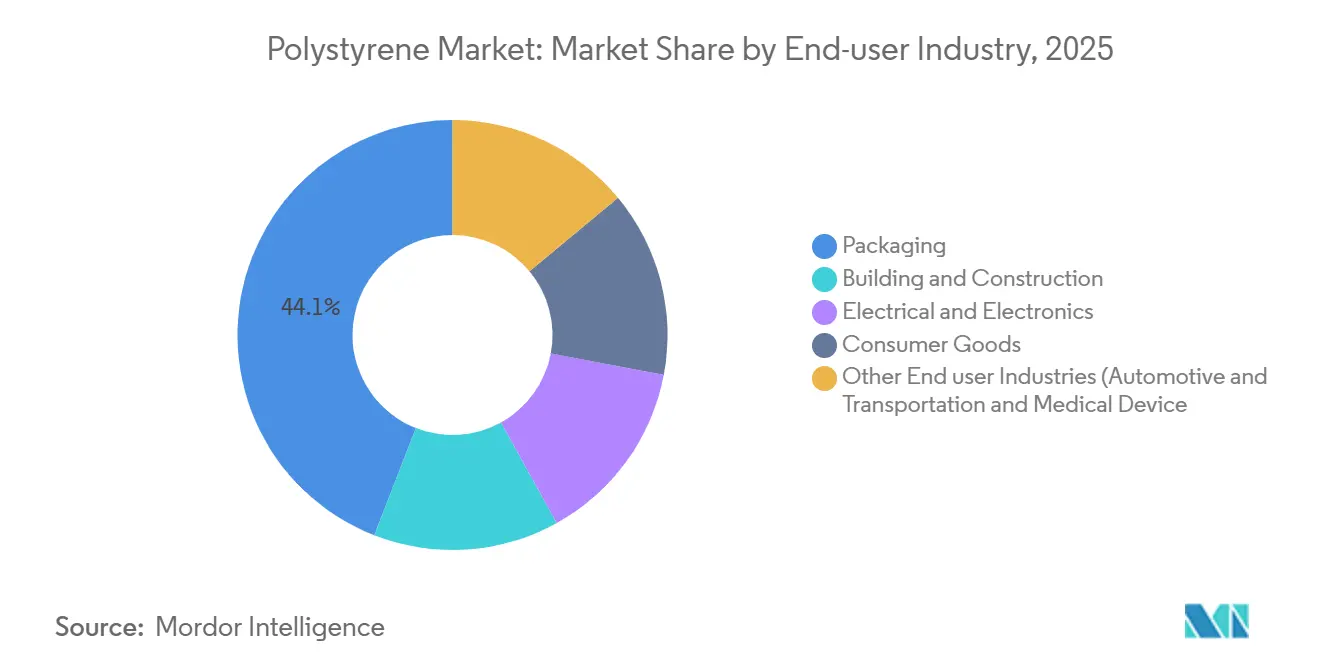

- By end-use industry, packaging accounted for 44.05% of the polystyrene market size in 2025, and other end-user industries, including automotive and medical devices, together represent the fastest 5.18% CAGR through 2031.

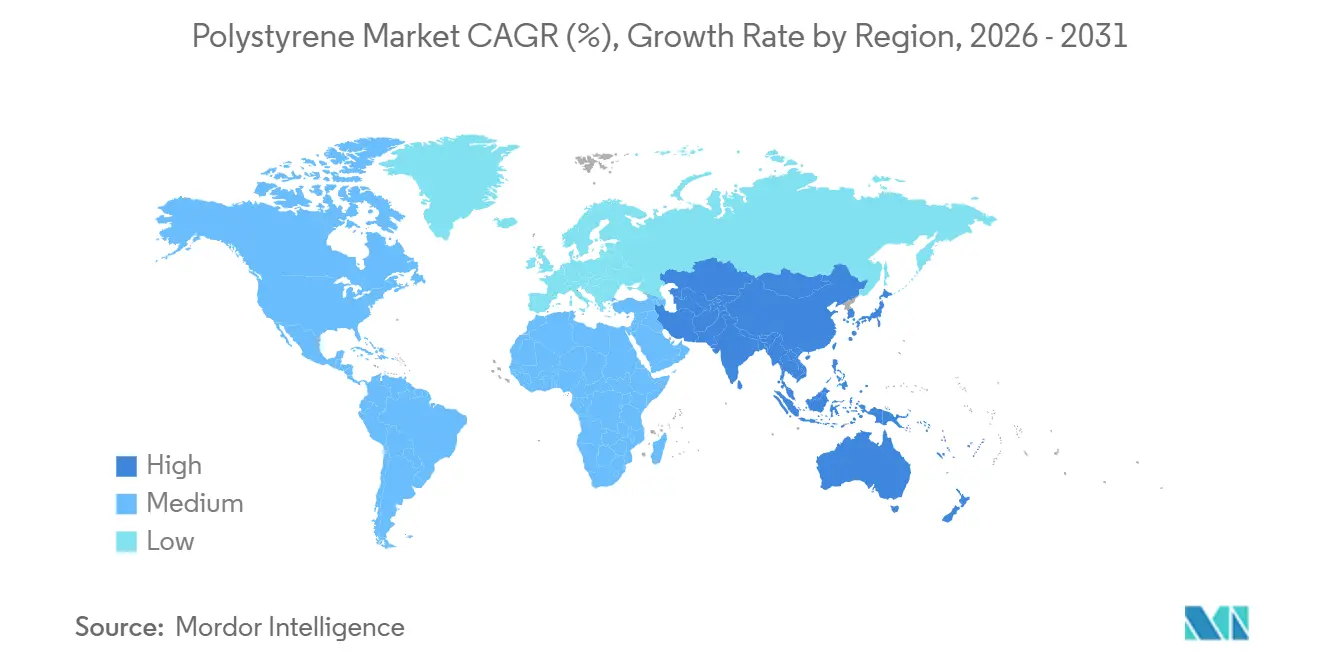

- By geography, Asia-Pacific commanded 56.88% of the polystyrene market share in 2025 and is expanding at a 5.66% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Polystyrene Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce and Food-service Packaging Boom | +0.9% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Energy-Efficiency Codes Lifting EPS/XPS Use | +1.2% | North America, Europe, spillover into Asia-Pacific urban centers | Long term (≥ 4 years) |

| Electronics and Appliance Output Growth | +0.8% | Asia-Pacific core—China, South Korea, Japan | Medium term (2-4 years) |

| Chemical-Recycling Breakthroughs | +0.7% | Early adoption in Europe and North America, scale-up in Asia-Pacific | Long term (≥ 4 years) |

| Cold-chain Pharma Logistics in Emerging Markets | +0.6% | Asia-Pacific, Middle East & Africa, Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce and Food-service Packaging Boom

Online retail and quick-service restaurant growth continue to lift protective packaging volumes, particularly in the Asia-Pacific where regulatory exemptions remain common. Lightweight EPS cushioning lowers dimensional-weight freight charges, securing its place versus corrugated inserts. Food-service operators in Latin America and Southeast Asia still rely on insulated beverage cups and clamshells because alternative compostable polymers remain cost-prohibitive. In North America, molded-fiber investments have started to displace foam in quick-service packaging, yet the sheer scale of e-commerce keeps the polystyrene market expanding. Brands balancing cost, cushioning performance, and consumer perceptions are therefore sustaining dual sourcing strategies[1]Huhtamaki Oyj, “Annual Report 2024,” huhtamaki.com.

Energy-Efficiency Codes Lifting EPS/XPS Insulation Demand

The 2024 International Energy Conservation Code and ASHRAE 90.1-2022 raised minimum R-values for walls and foundations, generating multi-year demand for thicker EPS and XPS boards in U.S. and European building envelopes[2]International Code Council, “IECC 2024 Highlights,” iccsafe.org. Europe’s Energy Performance of Buildings Directive, recast in 2024, stipulates near-zero-energy standards for new structures by 2030. Responding, BASF is adding 50,000 tons of Neopor EPS capacity at Ludwigshafen to come online in early 2027. China’s GB 55015-2021 mirrors these requirements for high-rise housing, entrenching EPS insulation as a structural growth pillar that is insulated from short-term cyclicality in packaging.

Electronics and Appliance Output Growth

High-impact polystyrene remains the preferred resin for television bezels, refrigerator liners, and small-appliance casings. China’s electronics production value climbed 11.77% year-on-year in the first half of 2025, pulling HIPS demand in step. South Korea and Japan add specialty grades for medical-equipment housings and automotive infotainment modules. OEM sustainability pledges are nudging procurement toward post-consumer recycled grades, prompting feedstock-loop projects such as LG Chem’s chemically recycled styrene integration at Yeosu.

Technology Break-throughs in Chemical Recycling

Commercial deliveries of styrene monomer produced via Sulzer’s EcoStyrene pyrolysis line in 2025 proved that recycled PS can meet food-contact purity thresholds at an industrial scale. The University of Bath’s tandem catalytic route delivered 90% monomer yields under mild conditions, cutting the energy penalty typical of pyrolysis. INEOS’s ResolVe program targets 50,000 tons of recycled PS output by 2027, creating a clear path to comply with European EPR levies. These advances position chemically recycled content as a differentiator that captures premiums in regulated markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Single-use PS Bans & EPR Fees | -1.1% | Europe, California, Taipei, Seoul | Short term (≤ 2 years) |

| High-performance Paper & Bio-polymer Substitutes | -0.6% | North America and Europe, early adoption in urban Asia-Pacific | Medium term (2-4 years) |

| Styrene Feedstock Tightness | -0.4% | Asia-Pacific and Europe naphtha/propane crackers; North America advantaged | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Single-use PS Bans and Extended Producer-Responsibility Fees

The EU Single-Use Plastics Directive, fully enforced in 2024, imposes EPR fees that lift polystyrene food-container costs by 15-25% across member states. California’s SB 54 mandates 25% recycled content by 2032 for single-use packaging, accelerating the shift toward fiber clamshells and compostable polymers. The UK plastic packaging tax of GBP 210.82 per tonne penalizes virgin PS imports lacking 30% recycled content, and Taipei plus Seoul have initiated phased bans on foam take-out ware. These measures are redirecting volume growth toward insulation, electronics, and other durable segments.

High-performance Paper and Bio-polymer Substitutes

Huhtamaki’s USD 60 million molded-fiber site in Arizona, operational since 2025, delivers 500 million units annually that compete head-on with EPS clamshells at a 20-30% cost premium acceptable to brands focused on sustainability. Pactiv Evergreen’s USD 235 million purchase of Fabri-Kal has consolidated paper-based alternatives that exceed 1 billion units in combined capacity, crowding the quick-service channel. NatureWorks ramped Ingeo PLA to 150,000 tons per year in 2025, with food-service ware representing 40% of output. Even though fiber lacks moisture resistance and PLA needs industrial composting, improving performance and tighter regulations are steadily eroding disposable PS volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: GPPS Gains on Food-contact Innovation

General-purpose polystyrene is set to outpace the broader market at 5.51% CAGR through 2031, despite expandable polystyrene's commanding 45.19% share in 2025. GPPS's acceleration stems from food-contact packaging innovations, particularly injection-molded yogurt cups, dessert containers, and portion-control trays that leverage its clarity, rigidity, and FDA-compliant formulations. High-impact polystyrene (HIPS), the second-largest resin type, serves durable-goods applications such as refrigerator liners, television bezels, and small-appliance housings, where its toughness and dimensional stability justify a price premium over commodity GPPS. HIPS demand correlates tightly with consumer electronics output; China's 11.77% year-over-year production growth in the first half of 2025 directly lifted HIPS consumption in injection-molding operations.

Expandable polystyrene remains the volume leader, driven by construction insulation and protective packaging, yet its growth rate lags GPPS due to regulatory headwinds in foodservice applications. EPS insulation demand is structural, tied to building energy codes such as IECC 2024 and ASHRAE 90.1-2022, which mandate higher R-values for commercial and residential envelopes. BASF's 50,000-tonne Neopor expansion at Ludwigshafen, targeting early 2027 commissioning, underscores confidence in long-term EPS insulation demand despite single-use packaging bans.

By Form Type: Specialty Films and 3D Filaments Disrupt Foam Dominance

Foams held 59.67% of total volume in 2025, primarily for protective packaging and insulation. Still, specialty films, thermoformed sheets, and 3D printing filaments are expanding at a 5.02% CAGR. Architectural model makers and education labs value the easy-to-print properties of polystyrene filament compared with ABS. Thermoformed barrier films for ready-to-eat meals and blister packs have gained traction on the back of e-commerce meal-kit services. Injection-molded parts maintain relevance in consumer appliances and automotive interiors, although price pressures from engineering plastics and biopolymers intensify as end-users seek sustainability credits.

Regulatory scrutiny on EPS clamshells and cups slows foam growth in high-income markets, but recycling breakthroughs such as Sulzer’s EcoStyrene process, which achieved 85% monomer yields in commercial trials, may mitigate demand erosion by cutting the embedded carbon of foam products. On balance, the foam share will drift marginally lower, yet still supply the volume backbone of the polystyrene market through 2031 thanks to insulation mandates and industrial-packaging resilience.

By End-user Industry: Automotive and Medical Devices Outpace Packaging

Packaging absorbed 44.05% of 2025 volume and will retain scale through the forecast, but the 5.18% CAGR logged by automotive, medical devices, and other specialized sectors will exceed packaging’s expansion rate. EPS and GPPS insulated shippers are entrenched in vaccine distribution, where WHO PQS compliance dictates material choices. Automotive interiors rely on HIPS for instrument panels and door inserts, benefiting from cost advantages over ABS while meeting impact and dimensional-stability requirements. Construction remains the second-largest consumer, driven by stricter insulation codes across developed and emerging markets.

Medical device casings made from sterilization-compatible GPPS and HIPS surged 12% year-on-year in 2025, propelled by hospital capacity expansion in India and Brazil. Cold-chain pharmaceutical packaging also rises in step, cementing EPS’s relevance even as single-use bans narrow food-service applications. Collectively, these higher-margin niches shield the polystyrene market from volatility endemic to commodity packaging channels.

Geography Analysis

Asia-Pacific commanded 56.88% of the 2025 volume and is forecast to deliver a 5.66% CAGR through 2031. In China, consumer electronics production, up 11.77% in the first half of 2025, underpins HIPS demand, while building-code GB 55015-2021 ensures steady EPS pull-through in residential high-rises. India’s pharma cold-chain subsidies continue to boost EPS shipper usage, and Styrenix’s acquisition of INEOS’s Thailand site adds 100,000 tons of capacity to serve Southeast Asia.

North America enjoys feedstock-cost leadership, with ethane-based styrene driving exports that rose 18% year-on-year during 2025. Energy-efficiency codes such as IECC 2024 sustain domestic insulation demand, even as single-use bans in California and municipal ordinances in Seattle and Portland trim food-service foam. Canada’s supply landscape is consolidating after INEOS decided to idle its Sarnia styrene plant by mid-2026, redirecting shipments to Gulf Coast hubs. Mexico gains from near-shoring as appliance assemblers add injection-molding lines in Monterrey and Querétaro industrial clusters.

The Europe expanded polystyrene (EPS) market faces a dual reality: rigorous Single-Use Plastics Directive levies reduce disposable food-ware volumes, yet the EPBD recast drives sustained EPS insulation growth. BASF’s Neopor expansion exemplifies the investment case tied to near-zero-energy building requirements. INEOS’s ResolVe program aligns with UK plastic-packaging-tax thresholds and EPR fee schedules, ensuring access to high-margin applications. Growth lags Asia-Pacific but remains durable in segments aligned with circular-economy mandates.

South America is anchored by Brazil, where e-commerce and residential construction lift GPPS and EPS usage. Argentina’s macro-economic headwinds limit building activity, but medical-device assembly in Córdoba offers a pocket of strength. Middle East and Africa volumes are nascent yet accelerating, led by Saudi Arabia’s Vision 2030 infrastructure pipeline and South Africa’s vaccine cold-chain expansions. Lack of local resin production keeps these regions tied to imports from Asia-Pacific and Europe, but rising insulation standards and healthcare investments signal long-term opportunity.

Competitive Landscape

The Polystyrene market is moderately concentrated. INEOS Styrolution and Trinseo are trimming assets in high-cost locales: INEOS will shutter its 455,000-tonne Sarnia styrene unit by June 2026 and sold its Map Ta Phut polystyrene site to Styrenix for USD 22.3 million in 2025 (ineos.com). Trinseo is paring low-margin sales and evaluating the divestiture of its Americas Styrenics stake to focus on higher-return specialties. Conversely, BASF, SABIC, and Styrenix are adding capacity or product extensions tied to circularity and insulation growth. BASF’s Neopor expansion deploys biomass-balanced and mechanically recycled grades to capture EPBD-driven demand.

Polystyrene Industry Leaders

INEOS

TotalEnergies

Trinseo

SABIC

BASF

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: INEOS Styrolution announced its decision to permanently shut down its polystyrene (PS) production facility in Wingles, France. This move aligns with the company's broader strategy to adapt to evolving market dynamics and bolster the competitiveness of its European operations in the long run.

- October 2025: Trinseo, in collaboration with its partner Indaver, commenced the receipt of chemically recycled styrene monomer (rSM) via depolymerization. Indaver's newly operational recycling plant, situated in Antwerp, Belgium, began production in August 2025. The facility specializes in utilizing polystyrene household packaging waste to extract the styrene monomer (SM).

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global polystyrene market as the aggregate production and first-sale trade of general-purpose, high-impact, and expandable polystyrene resins, measured in tonnage and, where price data allow, in equivalent revenue. End-use conversions such as finished foam cups or appliance housings are outside the scope, yet their resin uptake is captured through industry balance sheets.

Scope note: post-consumer recycled polystyrene, bio-based substitutes, and downstream fabrication services are excluded.

Segmentation Overview

- By Resin Type

- General-Purpose Polystyrene (GPPS)

- High-Impact Polystyrene (HIPS)

- Expandable Polystyrene (EPS)

- By Form Type

- Foams

- Films and Sheets

- Injection-Molded Parts

- Other Form Types (3-D Printing Filaments,etc.)

- By End-user Industry

- Packaging

- Building and Construction

- Electrical and Electronics

- Consumer Goods

- Other End user Industries (Automotive and Transportation,Medical Devices)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed polymer manufacturers, masterbatch suppliers, foam converters, and packaging buyers across Asia-Pacific, Europe, and the Americas. These discussions refined utilization factors, regional price spreads, and substitution intentions, letting us reconcile secondary patterns with on-ground sentiment.

Desk Research

We began with open statistics from UN Comtrade, USGS, Eurostat PRODCOM, and China's National Bureau of Statistics, which map styrene feedstock flows into primary resin. Trade association papers from PlasticsEurope, American Chemistry Council, and the Japan Styrene Industry Association helped benchmark regional operating rates and plant debottlenecking plans. Company 10-Ks, investor decks, and press releases supplied realized average selling prices and capacity changes, while patent analytics via Questel highlighted technology shifts toward graphite-enhanced EPS. D&B Hoovers gave us financial clues for privately held producers. This list is illustrative; many other publications informed our desk review.

Market-Sizing & Forecasting

A top-down demand pool built from styrene production, net trade, and inventory change sets the initial 2025 volume, which we corroborate with selective bottom-up checks such as sampled producer shipments and converter pull-through. Key variables include construction floor-space completions, e-commerce parcel growth, average EPS density, crude-derived feedstock prices, and announced capacity expansions. We forecast using multivariate regression that links resin demand to building starts, packaged-food output, and consumer electronics shipments, then scenario test against consensus from our primary interviews. Where bottom-up totals diverge, we adjust by the variance weighted to the more reliable input.

Data Validation & Update Cycle

Outputs flow through two-step analyst peer review; anomalous swings trigger re-contact with sources. Our models refresh each year, and we issue interim revisions when plant outages, policy bans, or mergers materially shift the baseline.

Why Mordor's Polystyrene Baseline Earns Trust Globally

Published figures often diverge because firms mix value and volume units, roll in fabricated goods, or apply uneven refresh cadences. By anchoring on resin tons and verifying price ladders quarterly, we, at Mordor Intelligence, minimize those distortions.

Key gap drivers include differing resin definitions (some fold in recycled blends), aggressive price escalation assumptions, and one-off COVID rebound adjustments that others still carry forward.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 17.40 mn tons (2025) | Mordor Intelligence | - |

| USD 50.99 bn (2025) | Global Consultancy A | Combines converted products and uses list prices, inflating value |

| USD 38.24 bn (2025) | Trade Journal B | Applies blended polymer basket and constant-currency uplift |

These contrasts show that our disciplined scope setting, dual-unit tracking, and annual update cadence deliver a balanced, transparent baseline clients can replicate and trust.

Key Questions Answered in the Report

What is the current polystyrene market size and its 2031 forecast?

The polystyrene market size stood at 18.19 million tons in 2026 and is forecast to reach 22.72 million tons by 2031.

Which region leads consumption and growth in polystyrene?

Asia-Pacific held 56.88% of 2025 volume and is projected to expand at a 5.66% CAGR through 2031.

Which resin type is growing fastest within polystyrene?

General-purpose polystyrene is projected to grow at a 5.51% CAGR owing to food-contact packaging innovation.

How are regulations affecting single-use polystyrene demand?

EU and California bans plus EPR fees are cutting disposables in high-income markets, redirecting growth to insulation and durable goods.

What technological shifts could reshape polystyrene supply?

Commercial chemical-recycling plants achieving 85-90% monomer yields are enabling recycled-content grades that satisfy circular-economy mandates.

Page last updated on: