China MCU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

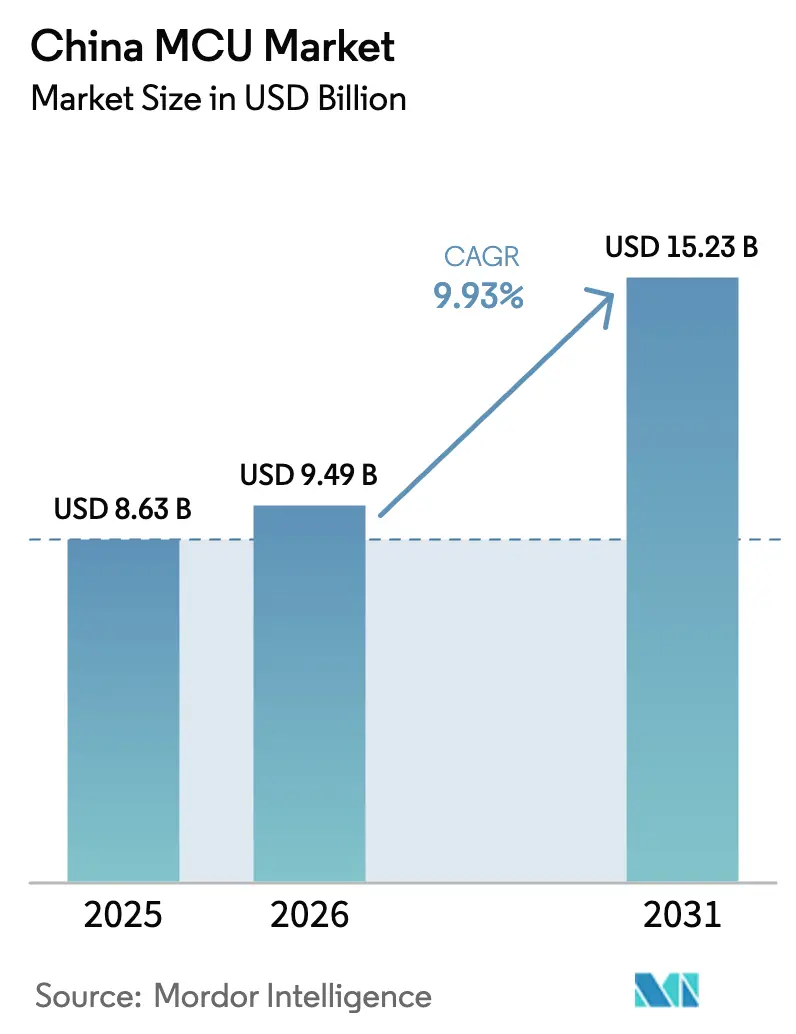

| Base Year Market Size (2025) | USD 8.63 Billion |

| Market Size (2026) | USD 9.49 Billion |

| Market Size (2031) | USD 15.23 Billion |

| Growth Rate (2026 - 2031) | 9.93% CAGR |

| Market Concentration | Medium |

Major Players_Market.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China MCU Market Analysis by Mordor Intelligence

The China MCU market size was valued at USD 8.63 billion in 2025 and estimated to grow from USD 9.49 billion in 2026 to reach USD 15.23 billion by 2031, at a CAGR of 9.93% during the forecast period (2026-2031). Persistent demand from electric vehicles, industrial automation, and AI-enabled IoT devices underpins this growth. Domestic fabs continue to scale mature-node capacity, allowing local suppliers to capitalize on Beijing’s drive for semiconductor self-reliance. At the same time, multinational vendors defend long-held design-wins through dependable quality, extensive toolchains, and automotive certifications. Edge-side AI inference, higher functional-safety requirements, and connectivity convergence are reshaping product roadmaps as system makers insist on one-chip solutions with security, wireless, and NPU blocks. Competitive dynamics increasingly reward firms that control both silicon and software ecosystems, while policy incentives accelerate the transition from foreign to indigenous MCUs across consumer, automotive, and industrial domains.

Key Report Takeaways

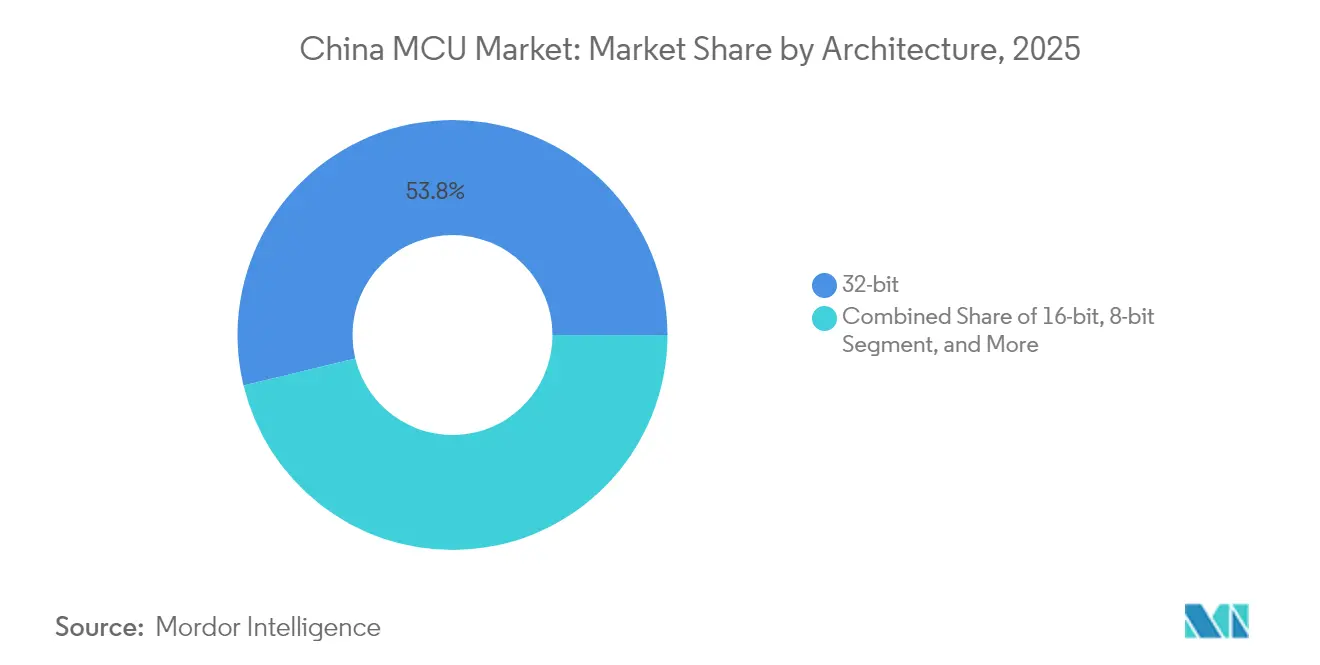

- By architecture, 32-bit devices held 53.78% revenue share in 2025 in the China MCU market; 64-bit units are forecast to expand at an 10.88% CAGR through 2031.

- By core IP, ARM Cortex-M devices captured 61.05% revenue in 2025 in the China MCU market; RISC-V implementations are advancing at a 10.49% CAGR to 2031.

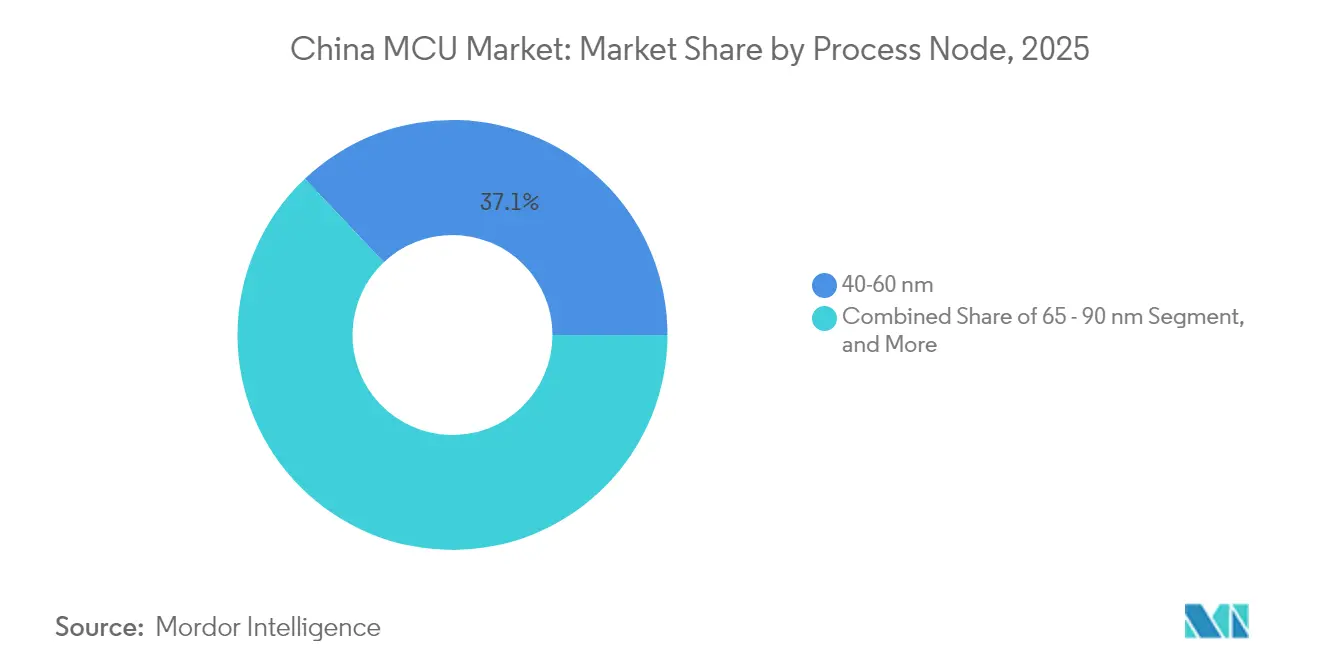

- By process node, 40-60 nm products accounted for 37.05% of the China MCU market share in 2025; sub-28 nm offerings are projected to grow at an 10.86% CAGR over the forecast period.

- By application, consumer electronics generated 28.40% of 2025 revenue in the China MCU market, while automotive deployments are rising at a 10.37% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China MCU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth in China's EV production triggering high-reliability automotive MCU demand | +2.8% | National, concentrated in Guangdong, Shanghai, Jiangsu automotive hubs | Medium term (2-4 years) |

| National "IoT +" strategy spurring connected-device MCU volumes | +2.1% | Global with spillover to Belt and Road markets | Long term (≥ 4 years) |

| Government subsidies to accelerate domestic MCU design-in (Made-in-China 2025) | +1.9% | National, with early gains in Beijing, Shanghai, Shenzhen tech corridors | Short term (≤ 2 years) |

| Industrial 4.0 retrofits in SMEs raising adoption of 32-bit industrial-grade MCUs | +1.6% | National manufacturing regions, particularly Yangtze River Delta | Medium term (2-4 years) |

| Emergence of RISC-V open ISA in Chinese MCUs lowering entry barriers | +1.4% | National with technology spillover to Southeast Asia | Long term (≥ 4 years) |

| Digital-yuan hardware wallet roll-out creating an all-new secure-MCU niche | +0.7% | National pilot cities expanding to full deployment | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Explosive Growth in China’s EV Production Triggering High-Reliability Automotive MCU Demand

New-energy vehicle production broke the 11 million-unit mark in 2024 and delivered over 40% domestic penetration, sharply lifting MCU content per car to USD 900-1,000. Level 2+ driver-assistance systems reached 62.5% penetration the same year, pushing demand for redundant domain controllers built on multiple high-performance MCUs for sensor fusion and braking logic. Chinese vendors such as Zhaoyi Innovation advanced toward ISO 26262 ASIL-D compliance, though most still focus on body ECUs rather than safety-critical powertrain blocks. Foreign suppliers maintain the lead in qualified 32-bit automotive controllers, yet rising domestic capacity and policy support are narrowing the gap. The China MCU market is therefore experiencing a rapid uptick in AEC-Q100-qualified parts, tighter cybersecurity requirements, and longer product lifecycles that favor suppliers with robust functional-safety toolchains.

National “IoT+” Strategy Spurring Connected-Device MCU Volumes

Beijing’s IoT+ blueprint underwrote more than 8,000 5G+Industrial-Internet projects by 2024, catapulting specialized 32-bit MCU demand for real-time machine control. China’s AIoT sector reached RMB 1.7 trillion in 2024, with AI-enabled terminals accounting for 55% of shipments and headed toward 80% by 2027. Bluetooth Low Energy modules, integral to TWS earbuds and wearables, are projected to top USD 1 billion worldwide by 2025, expanding at mid-teen CAGRs and anchoring MCU integration of wireless cores. Edge-side inferencing is permeating factory and consumer devices, forcing controller vendors to embed NPUs and secure elements into pin-compatible packages. This policy-driven proliferation of smart nodes cements the China MCU market as a volume engine for globally aligned IoT platforms.

Government Subsidies to Accelerate Domestic MCU Design-in (Made-in-China 2025)

Phase I and Phase II of the National IC Fund injected a combined 218 billion RMB into semiconductor ventures, granting MCU design houses access to low-cost capital and reinforcing an R&D intensity of 12%, nearly double the global average.[1]Arrian Ebrahimi, “China’s Mature Node Overcapacity: Unfounded Fears”, IFRI, ifri.org Tax deductions of up to 220% for qualified R&D outlays further cut breakeven points for fabless firms. Procurement guidelines issued in 2022 oblige state-owned buyers to favor indigenous chips if performance parity exists, accelerating qualification of domestic controllers. These incentives strengthen ecosystem depth, yet mission-critical markets still weigh track-record and ISO 26262 credentials, delaying full displacement of foreign suppliers. The China MCU market therefore balances immediate cost advantages against certainty of quality and long-term supply.

Industrial 4.0 Retrofits in SMEs Raising Adoption of 32-bit Industrial-Grade MCUs

China operates the world’s largest stock of industrial robots, and SME grants for digitalization are driving real-time control retrofits that need deterministic 32-bit MCUs. Factory-floor edge gateways require low-latency processing, multi-protocol fieldbus support, and extended temperature ranges. Domestic vendors gain early traction by bundling PLC libraries and reference designs tuned for local machine builders. Global players defend share through proven electromagnetic-compatibility performance and broad tool ecosystems. The China MCU market is thus seeing rising attach rates in servo drives, predictive-maintenance sensors, and machine-vision modules, reinforcing a medium-term growth runway for industrial-grade controllers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| U.S. export controls curbing access to advanced EDA and lithography tools | -1.8% | National, particularly affecting advanced node capabilities | Long term (≥ 4 years) |

| Persistent wafer-level supply bottlenecks in 40 nm, 28 nm nodes | -1.2% | Global supply chain with China-specific capacity constraints | Medium term (2-4 years) |

| Scarcity of functional-safety talent for ISO 26262-compliant MCU designs | -0.9% | National, concentrated in automotive hubs of Guangdong, Shanghai, Jiangsu | Medium term (2-4 years) |

| Reliability certification hurdles for domestic MCUs in Tier-1 auto OEMs | -0.7% | National automotive supply chain, early impact in Shanghai, Guangdong clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

U.S. Export Controls Curbing Access to Advanced EDA and Lithography Tools

Restrictions enacted by the United States hamper Chinese access to EUV scanners and advanced EDA suites, lifting projected 5 nm costs at SMIC by 40-50% versus TSMC peers while yields sit at roughly one-third of leading-edge benchmarks. Lack of EUV machinery forces DUV multi-patterning, inflating mask counts and cycle times. MCU designs targeting AI edge nodes or in-vehicle infotainment that need high logic density face performance-per-watt penalties. Domestic toolchains are progressing but still trail global incumbents in timing-closure and power-optimization depth. This technological drag tempers top-end growth of the China MCU market and slows adoption of sub-14 nm nodes.

Persistent Wafer-Level Supply Bottlenecks in 40 nm and 28 nm Nodes

Automotive and industrial MCUs rely heavily on 40-60 nm capacity, yet global shortages persist even as Chinese fabs enlarge footprint. SMIC and Hua Hong expansions must overcome equipment lead times and yield learning curves, keeping effective output below nameplate. These bottlenecks extend lead times, diluting the otherwise strong momentum of China MCU market shipments. Customers respond by dual-sourcing or redesigning boards around alternate package footprints, which stretches design cycles and inventory buffers. While additional fabs ramp through 2026, supply-demand equilibrium remains uneven across specialty processes such as BCD and eFlash.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Architecture: 64-bit Emergence Reshapes Performance Landscape

The China MCU market size for 32-bit devices reached USD 4.64 billion in 2025, equating to 53.78% revenue share. Edge AI workloads, surround-view stitching, and high-speed industrial vision accelerate 64-bit adoption, lifting that segment at an 10.88% CAGR. Sixteen-bit and eight-bit controllers linger in cost-sensitive appliances and small sensor nodes, yet their combined share slips yearly as 28 nm 32-bit pricing compresses. Suzhou Guoxin’s CCR4001S marries a 230 MHz RISC-V core with a 0.3 TOPS NPU, demonstrating domestic ambition to migrate control and inference onto one die. Automotive OEMs specify multicore lock-step 32-bit parts for body domain and dual-A76 64-bit SoCs for digital cockpit clusters, reinforcing a tiered architecture roadmap within the China MCU market.

Second-order effects include tighter alignment between memory density and compute throughput. As capacitive-touch HMIs enter appliances, firmware swells into the megabyte range, making on-chip flash a differentiation point. Vendors thus bundle 2–4 MB of eFlash in mid-range 32-bit MCUs. Concurrently, 64-bit controllers integrate LPDDR4 PHYs to stream neural-network weights. These advances collectively edge the China MCU market toward heterogeneous compute paradigms inside constrained power envelopes.

By Core IP: RISC-V Disruption Accelerates Domestic Innovation

ARM retained 61.05% of 2025 revenue, but royalty-free RISC-V cores chalked up double-digit growth, aided by government grants and open-source toolchains. Zhenhua Fengguang taped out its first fully indigenous 32-bit RISC-V MCU in January 2025, positioning for pilot production by year-end. Ultra-low-cost RISC-V parts priced near USD 0.10 invigorate entry-level IoT nodes. Design freedom enables domestic firms to add custom DSP blocks for motor control or crypto accelerators for digital-yuan wallets without paying license fees. However, migration hurdles include IDE maturity, middleware depth, and safety certification libraries, factors that still buttress ARM’s lead in the China MCU market.

Legacy 8051 cores persist in power meters and basic lighting controls, offering deterministic cycle timing and tiny die sizes on above 90 nm nodes. Yet new 8-bit sockets dwindle as ODMs standardize toolchains around 32-bit units with cost parity. The net result is an increasingly bifurcated China MCU market where premium performance leans toward 64-bit RISC-V and mass-market control consolidates on low-cost 32-bit ARM alternatives.

By Process Node: Advanced Nodes Gain Traction Despite Manufacturing Constraints

The 40-60 nm slice generated USD 3.19 billion in 2025 revenue, equal to 37.05% of the China MCU market size, due to its balanced cost-to-performance ratio. Sub-28 nm products, though just 8.35% of sales, post the quickest climb at an 10.86% CAGR as AIoT and advanced ADAS demand higher MIPS-per-milliwatt. Absence of EUV tools compels domestic fabs to rely on DUV tricks, raising mask counts yet still unlocking incremental leadership in energy efficiency. Triple-stack copper routing and refined eFlash IP help 28 nm controllers integrate SRAM, CAN-FD, and NPU blocks within automotive temperature envelopes.

Greater than 90 nm processes keep relevance for ultra-small code-storage MCUs and one-time-programmable chips embedded in white goods. Pricing advantage often outweighs die area penalties in such simple control loops. Nonetheless, gradual migration to 55 nm flash reduces BOM cost for high-growth wearables and smart-lighting segments, incrementally displacing older geometries inside the China MCU market.

By Application: Automotive Acceleration Outpaces Consumer Electronics Growth

Consumer devices retained 28.40% revenue share in 2025, fueled by brisk smartphone refreshes, smart-home hubs, and wearables that each require multiple low-power MCUs. Yet automotive deployments logged the highest forward momentum at a 10.37% CAGR, propelled by electrification, battery-management expansion, and ADAS penetration. A single battery-electric vehicle can host more than 100 discrete MCUs, spanning traction-inverter control to digital cockpit touchscreen management.

Industrial automation ranks third, driven by SME adoption of motion-control servos and predictive-maintenance nodes inside Industry 4.0 retrofits. Communications and IoT modules form the next tier, leveraging cellular Cat.1 bis SoCs such as XINYISEMI’s XY4100LC that fuse RISC-V cores with 4G modems. Medical devices are growing off a smaller base as NMPA tightens safety certification, but demographic shifts should lift unit demand for home diagnostics and portable therapy equipment.

Geography Analysis

The Yangtze River Delta anchors a significant share of national MCU consumption, due to its dense cluster of automotive plants, consumer-electronics giants, and embedded-system ODMs. Shanghai hosts Tesla’s Gigafactory, while nearby Suzhou and Wuxi concentrate board-level assembly, together absorbing large volumes from the China MCU market. Guangdong Province commands another 26.74% share through Shenzhen’s ODM ecosystem and Dongguan’s smartphone assembly lines, funneling high-mix low-cost orders toward flexible domestic fabs. Beijing-Tianjin draws design-centric demand for AI-enabled security cameras and smart-city infrastructures. Western hubs such as Chengdu and Xi’an cultivate fabless startups under provincial incentives, extending the geographic footprint of the China MCU market beyond the coast. Belt and Road export corridors in Southeast Asia and Latin America become natural outlets for Chinese controller vendors once domestic requirements reach scale, allowing product reuse in similar regulatory regimes. This inward-focused yet export-enabled geography supports robust, regionally diversified revenue streams.

Foundry proximity reduces logistics costs and trims lead-times, but over-concentration of 40-60 nm capacity in coastal metros leaves the China MCU market vulnerable to localized power or water disruptions. Policy planners are therefore nudging 12-inch expansions into inland cities to balance risk and stimulate local economies. Variations in environmental permitting and subsidy structures across provinces force MCU suppliers to adopt flexible production assignment to keep qualification time low and maintain AEC-Q100 continuity.

Competitive Landscape

Global incumbents, Microchip, NXP, STMicroelectronics, Texas Instruments, and Renesas, continue to ship high-reliability automotive and industrial MCUs backed by long-term supply contracts and ISO 26262 toolkits. Yet domestic challengers use cost-plus pricing, integrated connectivity, and local-language tech support to chip away at market share. Espressif Systems shipped more than 1 billion IoT MCUs cumulatively and logged 42.2% revenue growth during the first three quarters of 2024. GigaDevice leverages its own NOR flash lineage to bundle combo chips that shorten PCB space for smart speakers.

MindMotion targets motion-control with vector-engine extensions, while XINYISEMI rides cellular IoT modules into OEM design wins. Partnerships between fabless firms and assembly houses improve package variety, QFN, FC-QFN, and WCSP, to meet space-constrained wearable demands. International players defend share by launching application-specific variants; Texas Instruments’ MSPM0C1104 offers a 1.38 mm² die for wearable sensors.[3]“新品发布|德州仪器推出全球超小型MCU”, EET China, eet-china.com

M&A chatter revolves around smaller RISC-V startups seeking scale to fund tool-chain completion. Government watchdogs weigh antitrust clearance against domestic consolidation needs. The result is a moderately concentrated China MCU market where the top five suppliers account for roughly 55% of revenue, leaving meaningful whitespace for niche specialists.

China MCU Industry Leaders

Microchip Technology Inc.

Infineon Technologies AG

STMicroelectronics NV

Silicon Laboratories Inc.

NXP Semiconductors N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Texas Instruments launched the MSPM0C1104, the smallest ARM Cortex-M0+ MCU at 1.38 mm² die area, aimed at medical wearables.

- March 2025: XINYISEMI showcased the XY4100LC Cat.1 bis SoC and outlined a 5G RedCap roadmap, exceeding 150 million cumulative NB-IoT chip shipments.

- March 2025: Suzhou Guoxin Technology and Shenzhen Meidian Technology unveiled CCR4001S-based AI sensor modules, claiming 65% cost savings and 40% shorter design cycles for industrial and consumer AIoT nodes.

- March 2025: SMIC confirmed progress toward 5 nm yield ramp, despite 40-50% cost premium versus offshore peers, supporting Huawei Ascend 910C AI silicon.

China MCU Market Report Scope

A microcontroller is a compact, reasonably priced microprocessor that is made to carry out the particular functions of embedded systems, such as displaying microwave information and receiving distant signals, among others.

The China microcontroller (MCU) market is segmented by product (4 and 8-bit, 16-bit, 32-bit) and by application (aerospace and defense, consumer electronics and home appliances, automotive, industrial, healthcare, data processing and communication). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

| 8-bit |

| 16-bit |

| 32-bit |

| 64-bit |

| ARM Cortex-M Series |

| RISC-V Cores |

| 8051 / MCS-51 |

| MIPS and Others |

| above 90 nm |

| 65 – 90 nm |

| 40 – 60 nm |

| 28 – 40 nm |

| less than 28 nm |

| Consumer Electronics |

| Automotive |

| Industrial Automation |

| Communication and IoT |

| Healthcare and Medical Devices |

| Other Applications |

| By Architecture | 8-bit |

| 16-bit | |

| 32-bit | |

| 64-bit | |

| By Core IP | ARM Cortex-M Series |

| RISC-V Cores | |

| 8051 / MCS-51 | |

| MIPS and Others | |

| By Process Node | above 90 nm |

| 65 – 90 nm | |

| 40 – 60 nm | |

| 28 – 40 nm | |

| less than 28 nm | |

| By Application | Consumer Electronics |

| Automotive | |

| Industrial Automation | |

| Communication and IoT | |

| Healthcare and Medical Devices | |

| Other Applications |

Key Questions Answered in the Report

What is the growth outlook for the China MCU market to 2031?

Revenue is expected to climb from USD 9.49 billion in 2026 to USD 15.23 billion by 2031 at a 9.93% CAGR.

How many MCUs does an average electric vehicle in China now contain?

A typical battery-electric model integrates more than 100 controllers, lifting MCU content to USD 900-1,000 per car.

Which architecture is gaining share fastest within Chinese controllers?

64-bit devices are expanding at an 10.88% CAGR due to edge-AI and high-bandwidth automotive use cases.

Why is RISC-V important for Chinese semiconductor strategy?

The open ISA removes foreign royalty payments and allows domestic firms to tailor cores for specialized functions, accelerating self-reliance goals.

Which process node presently dominates MCU production in China?

The 40-60 nm bracket holds 37.05% revenue share, balancing cost, power, and maturity for high-volume applications.

Page last updated on: