Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

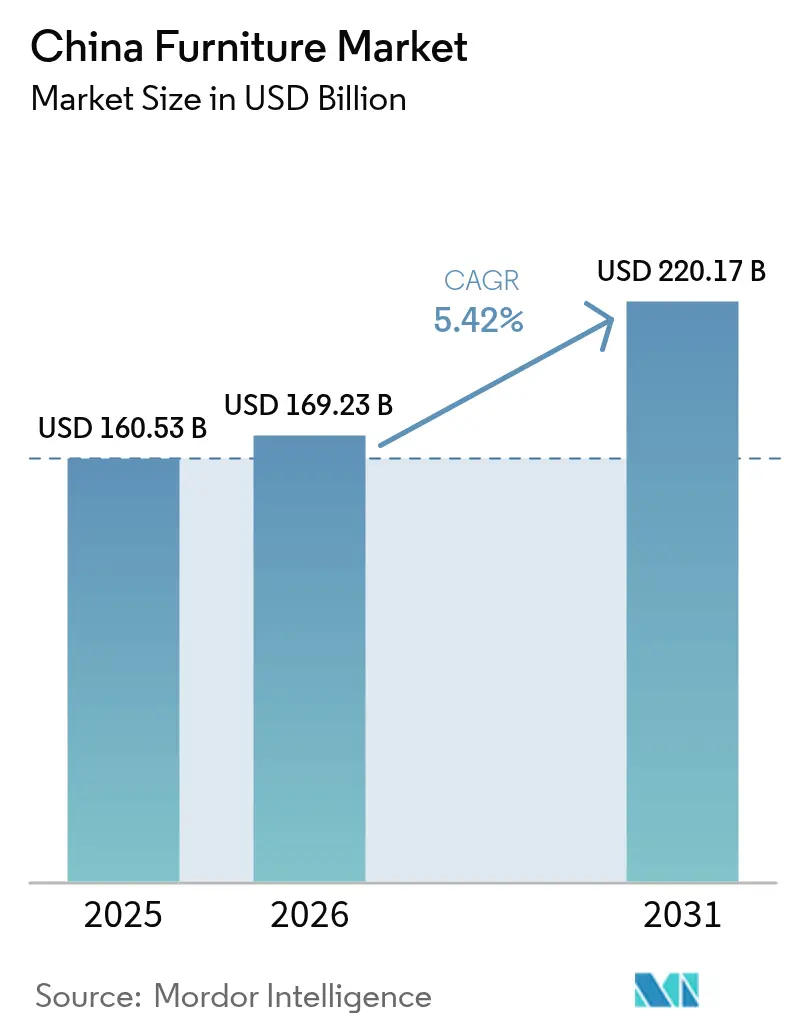

| Base Year Market Size (2025) | USD 160.53 Billion |

| Market Size (2026) | USD 169.23 Billion |

| Market Size (2031) | USD 220.17 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

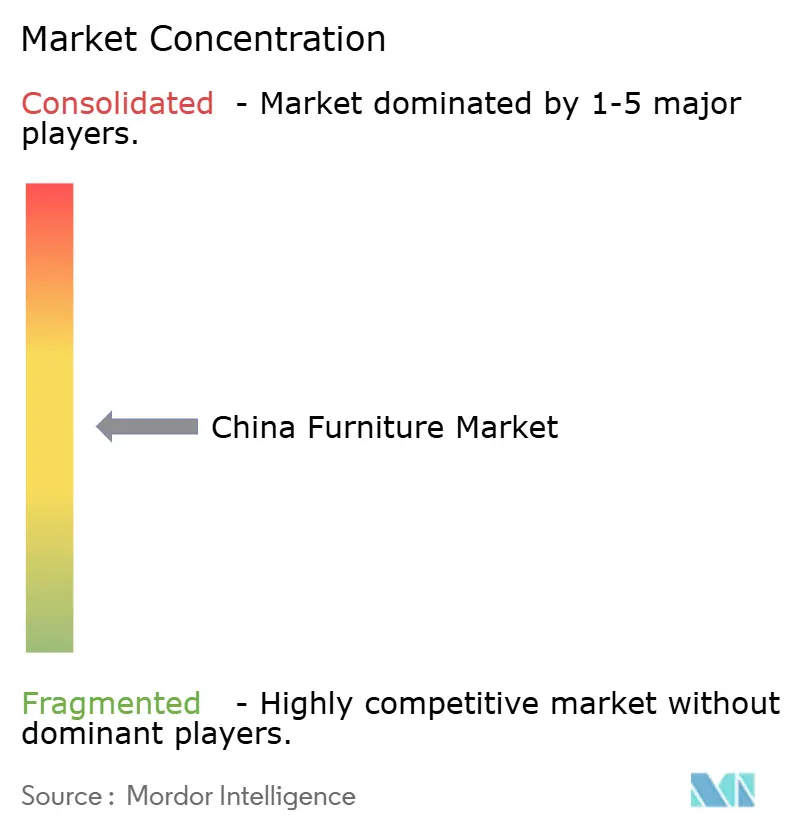

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Furniture Market Analysis by Mordor Intelligence

The China furniture market size was valued at USD 160.53 billion in 2025 and estimated to grow from USD 169.23 billion in 2026 to reach USD 220.17 billion by 2031, at a CAGR of 5.42% during the forecast period (2026-2031). Population migration toward lower-tier cities, sustained gains in disposable income, and the rapid adoption of omnichannel retail are steering revenue gains across the China furniture market. Demand patterns remain regionally unbalanced: eastern coastal provinces still account for the largest revenue pool, yet tier-2 and tier-3 urban clusters are generating the fastest incremental sales as housing completions and commercial fit-outs accelerate. Home furniture continues to dominate spending, while office furniture benefits from a renovation wave led by hybrid-work design mandates. On the supply side, export-oriented manufacturers are redirecting capacity to the domestic arena, increasing price competition, and speeding up product innovation. Government trade-in subsidies and a sharp rebound in domestic tourism are cushioning the negative impact of the property slowdown, keeping the China furniture market on a resilient growth trajectory through 2030 [1]International Monetary Fund, “People’s Republic of China: Staff Report for the 2025 Article IV Consultation,” imf.org.

Key Report Takeaways

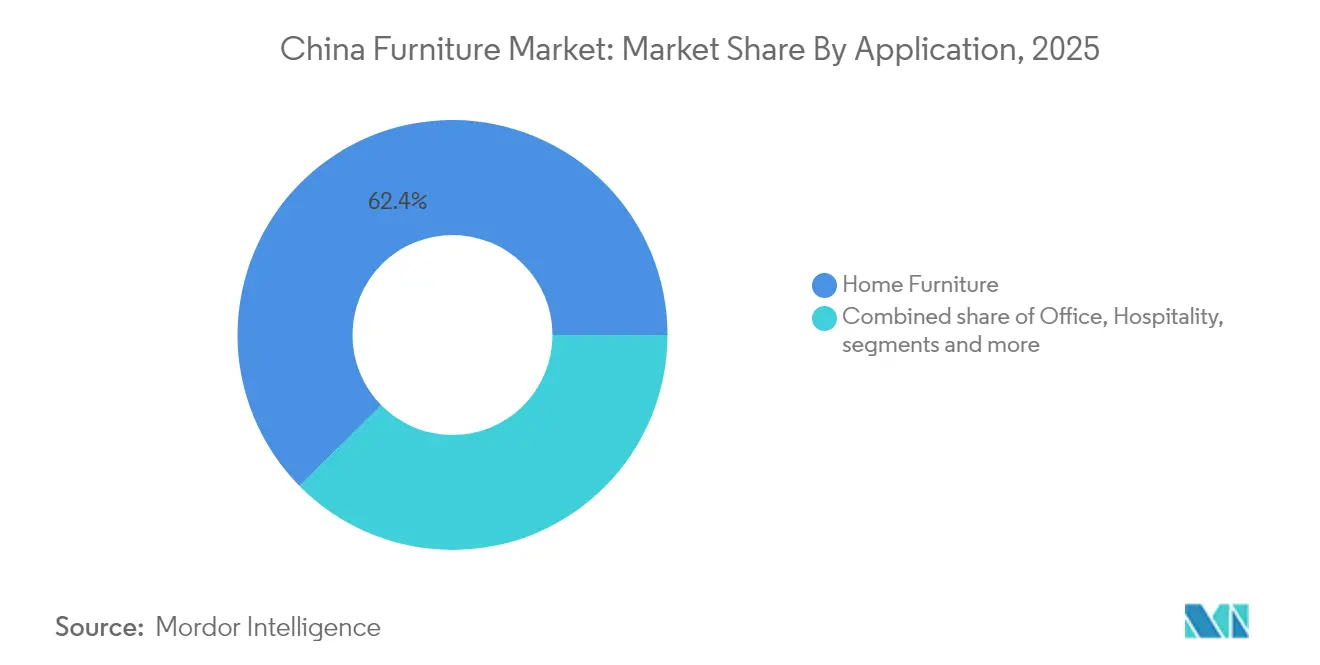

- By application, home furniture led with 62.40% of the China furniture market share in 2025, while office furniture is projected to post the highest 6.01% CAGR through 2031.

- By material, wood retained 56.60% revenue share of the China furniture market in 2025; polymers and plastics are set to expand at a 5.07% CAGR to 2031.

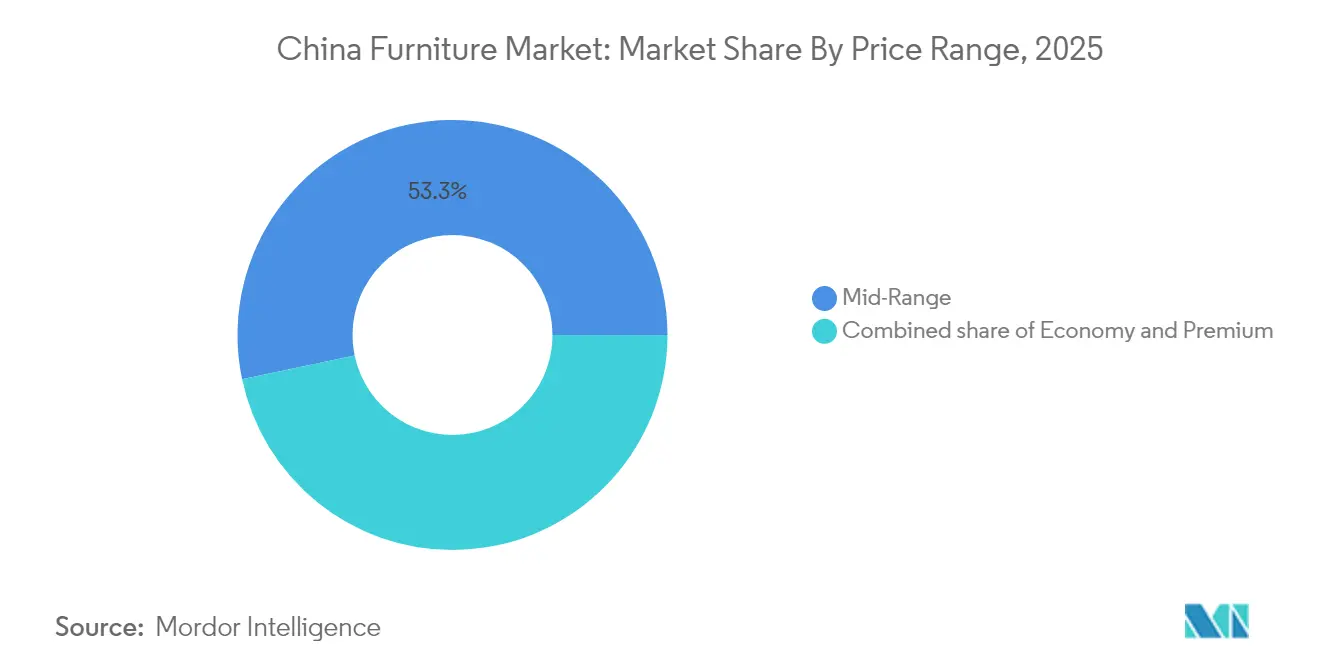

- By price range, mid-range products commanded 53.30% of the China furniture market size in 2025; the premium tier is forecast to grow at 6.18% CAGR between 2026-2031.

- By distribution channel, the B2C/retail segment captured 74.20% revenue share of the China furniture market in 2025, with the same channel advancing at a 5.69% CAGR through 2031.

- By geography, eastern China maintained the largest 37.60% revenue share of the China furniture market in 2025, whereas southwest China is expected to grow at 6.02% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Furniture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization in tier-2 & 3 cities | +1.2% | Nationwide; strongest in Chengdu, Hangzhou, Wuhan | Medium term (2–4 years) |

| Rise of e-commerce and omnichannel retail | +0.9% | Highest penetration in eastern China | Short term (≤ 2 years) |

| Expansion of commercial & hospitality projects | +0.7% | Tourism hubs and coastal metros | Medium term (2–4 years) |

| Office renovation cycle in metropolitan hubs | +0.6% | Beijing, Shanghai, Guangzhou, Shenzhen | Short term (≤ 2 years) |

| Export manufacturers pivoting to domestic demand | +0.4% | Guangdong, Zhejiang, Jiangsu | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization in Tier-2 & Tier-3 Cities

Urban residency climbed to 66.2% in 2024, a 0.9-point rise year on year. Chengdu and Wuhan together added 2 million new residents during the year [2]National Bureau of Statistics of China, “2024 National Economic and Social Development Statistical Bulletin,” stats.gov.cn. Government-backed city cluster programs continue to channel infrastructure capital toward inland urban centers, spurring new-home deliveries and stimulating furniture purchases. Local buyers in Chengdu, Wuhan and other growth hubs exhibit a stronger preference for design-oriented yet functional pieces, prompting suppliers to extend showrooms and last-mile distribution networks beyond the traditional coastal corridor. Manufacturers that diversify product lines for smaller living spaces find higher attachment rates for modular units and storage-optimized layouts, reinforcing volume gains across the China furniture market.

Rise of E-Commerce and Omnichannel Retail

The Ministry of Commerce tallied CNY 1.02 trillion in 2024 online sales of home-related goods—including furniture—up 15.4% year on year [3]National Bureau of Statistics of China, “2024 National Economic and Social Development Statistical Bulletin,” stats.gov.cn. Digitally led discovery journeys now dominate early-stage furniture research, and blended “click-to-brick” pathways are compressing the buying cycle. Leading platforms deploy augmented-reality visualization, boosting conversion and compressing return rates. Large store networks provide smaller urban showrooms, pick-up lockers, and same-day fulfilment to retain customer loyalty. These shifts lower geographic barriers, broadening the China furniture market and intensifying competitive pressures on product design and logistics agility.

Expansion of Commercial and Hospitality Projects

Domestic tourism recovered to near-pre-pandemic trip volumes in 2024, driving record room openings by national hotel chains. Shorter three-to-five-year replacement schedules for hospitality furniture compared with residential cycles sustain a reliable demand stream for customized case goods, lobby seating, and outdoor fixtures. Suppliers that couple design-build services with flexible manufacturing capacity capture a disproportionate share of high-margin projects across the China furniture market.

Export Manufacturers Pivoting to Domestic Demand

Heightened tariffs in key overseas markets have redirected capacity back home. Plants in Guangdong and Zhejiang fine-tune product aesthetics for local tastes, leveraging mature supply chains to compress lead times. This domestically focused output introduces more globally inspired styles at competitive ticket prices, intensifying margin pressure but enriching the variety and depth of the China furniture market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Property-sector slowdown | -1.3% | Most acute in tier-1 cities | Medium term (2–4 years) |

| Fragmented retail footprint & high rents | -0.7% | Tier-1 and tier-2 cities | Short term (≤ 2 years) |

| Timber import restrictions elevating costs | -0.5% | Guangdong, Zhejiang, Jiangsu | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Property-Sector Slowdown Curtailing New Residential Spending

Persistently weak residential starts in premium urban cores undermine demand for complete home furnishing packages. Consumers delay big-ticket purchases, raising promotional intensity across the China furniture market. Still, renovation spending partially offsets the decline as owners retrofit existing apartments, shifting product mix toward multifunctional and space-saving solutions.

Fragmented Retail Footprint & High Mall Rents Compressing Margins

Traditional chains face rent escalations that outpace same-store growth, especially in high-traffic malls. Many operators are moving to hub-and-spoke formats that combine flagship galleries with compact satellite units closer to residential districts. The resulting logistics complexity raises operating costs, pushing smaller dealers toward mergers or strategic alliances to remain viable within the China furniture market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Home Leadership and Office Momentum

Home furniture accounted for 62.40% of the China furniture market size in 2025 and continues to benefit from cultural emphasis on domestic comfort and aesthetics. Demand growth, however, is shifting toward upgradable modular units that fit compact apartments in dense cities. Beds and sofas remain volume anchors, yet kitchen cabinets and storage systems register faster growth as households optimize existing space amid slower property turnover.

Office furniture, gaining from a 6.01% CAGR outlook, is propelled by post-pandemic layout realignments, with smart desks, collaborative pods, and ergonomic seating securing order books. This evolution narrows the historical gap between residential and commercial categories, adding diversity to revenue streams across the China furniture market.

By Material: Wood Primacy and Plastic & Polymer Upswing

Wood held 56.60% of the China furniture market share in 2025, supported by consumer perceptions of durability and premium feel. Supply chain tension is prompting heavier use of certified plantations and mixed-wood veneers to stabilize costs.

Simultaneously, Plastic & Polymer posts the swiftest 5.07% CAGR as innovations enhance scratch resistance, color depth, and recyclability. Hybrid constructions that combine wooden frames with polymer accents create new mid-price offerings, extending appeal across broad consumer cohorts in the China furniture market.

By Price Range: Mid-Range Core, Premium Acceleration

Mid-range lines generated 53.30% of the China furniture market size in 2025, balancing design aspirations with value.

The premium tier’s 6.18% CAGR is anchored in affluent households in Beijing, Shanghai and Shenzhen that seek differentiated styling and brand pedigree. Domestic labels partner with European designers to up-level catalogs, while smart-home integration strengthens perceived value. Economy lines defend share in inland cities, though rising wages and raw-material costs compress margins, pushing makers to automation and leaner distribution in the China furniture market.

By Distribution Channel: B2C Dominance and Digital Integration

The B2C route captured 74.20% revenue share in 2025, due to specialist chains, home centers, and direct-to-consumer brands. Digital traffic influences over two-thirds of purchase journeys, and retailers embed augmented-reality visualization plus same-day pick-up to merge online discovery with showroom assurance.

Project-based B2B sales contribute the remaining quarter, buoyed by hotel, office, and institutional remodeling. Logistics and after-sales service excellence remain decisive factors in protecting loyalty across the China furniture market.

Geography Analysis

East China maintained the largest 37.60% revenue share of the China furniture market in 2025. East provinces—Guangdong, Zhejiang, Jiangsu—retain the lion’s share of consumption and production within the China furniture market, underpinned by dense retail networks, export-ready factories, and higher household incomes. Tier-1 cities feature elevated premium demand, yet slower population inflows temper growth relative to smaller urban clusters.

Central and western regions are emerging flashpoints for expansion as government infrastructure outlays lower logistics barriers. Urban clusters such as Chengdu-Chongqing record double-digit furniture revenue growth, fueled by rising home ownership and tourism-related hospitality projects. Manufacturers are allocating fresh capacity inland to capture labor cost savings, bolstering regional self-sufficiency in the China furniture market.

Distinct aesthetic preferences persist darker solid-wood motifs dominating northern styles, whereas southern consumers gravitate toward lighter hues and contemporary silhouettes. Retailers adjust assortments by city, supported by analytics that map demographic trends to design cues, enriching localization throughout the China furniture market.

Competitive Landscape

Competitive Landscape

Kuka Home, Suofeiya Home Collection, and Oppein Home Group exploit vertically integrated supply chains to compress production cycles and defend shelf space. IKEA continues to localize product dimensions and color schemes to suit Chinese apartments, retaining loyalty despite mounting local competition.

Strategic investment cycles emphasize plant automation, digital twins, and in-house logistics to counter wage inflation. Export specialists, pressed by tariffs abroad, accelerate domestic brand launches featuring globally inspired aesthetics at competitive prices, crowding mid-tier shelves across the China furniture market.

Digitally native challengers bypass legacy wholesale, leveraging data-driven configurators and regional micro-factories for three-week delivery of made-to-order pieces. Traditional players respond with omnichannel financing, white-glove assembly, and extended warranties, underscoring service as a key point of differentiation in the China furniture market.

China Furniture Industry Leaders

Kuka Home

Suofeiya Home Collection

Oppein Home Group

Red Star Macalline Group

IKEA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Long Bamboo Technology Group unveiled plans for a Romanian production plant to strengthen European supply lines.

- March 2025: ONLEAD Group presented sustainable commercial solutions at CIFF Guangzhou, underlining a patent portfolio exceeding 1,000 innovations.

- February 2025: IC3D acquired 3D-printed furniture pioneer Model No., preserving its micro-factory sustainability model.

- January 2025: JD.com and Alibaba activated nationwide rebate campaigns under the government’s furniture trade-in subsidy scheme.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we treat the China furniture market as the annual value of new household, office, hospitality, institutional, and contract furniture sold inside mainland China, measured at manufacturer gate prices before trade discounts and taxes. The estimate covers wood, metal, polymer, and hybrid pieces that are factory-built, assembled, or knock-down and intended for indoor use; outdoor, rental, and built-in cabinetry are counted only when they are sold as discrete furniture units.

Scope exclusion: custom interior fit-outs that are permanently fixed to the building structure remain outside our frame.

Segmentation Overview

- By Application

- Home Furniture

- Chairs

- Tables (side tables, coffee tables, dressing tables, etc.)

- Beds

- Wardrobes

- Sofas

- Dining Tables/Dining Sets

- Kitchen Cabinets

- Other Home Furniture (bathroom furniture, outdoor furniture, etc.)

- Office Furniture

- Chairs

- Tables

- Storage Cabinets

- Desks

- Sofas and Other Soft Seating

- Other Office Furniture

- Hospitality Furniture

- Educational Furniture

- Healthcare Furniture

- Other Applications (public places, retail malls, government offices, etc.)

- Home Furniture

- By Material

- Wood

- Metal

- Plastic & Polymer

- Other Materials

- By Price Range

- Economy

- Mid-Range

- Premium

- By Distribution Channel

- B2C/Retail

- Home Centers

- Specialty Furniture Stores

- Online

- Other Distribution Channels

- B2B /Project

- B2C/Retail

- By Geography

- East China

- South-Central China

- North China

- Southwest China

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with factory owners in Guangdong and Zhejiang, tier-one furniture chain buyers, e-commerce category managers, and interior design consultants across Beijing, Shanghai, Chengdu, and Chongqing. These conversations validated utilization rates, online price ladders, and discounting cadence, and helped us reconcile variance in provincial demand indicators highlighted by secondary sources.

Desk Research

Our desk work begins with macro-data from the National Bureau of Statistics, China Customs export files, and Ministry of Housing completion statistics, which anchor production, trade, and residential completions. Industry-specific inputs follow from bodies such as the China National Furniture Association, the China Construction Material Circulation Association, and provincial commerce bureaus. To refine price and mix shifts, we parse annual reports and 10-Ks of leading listed manufacturers, retail footfall disclosures, and credible news feeds accessed via Dow Jones Factiva. Paid intelligence from D&B Hoovers gives us audited company revenue splits, while Questel patent trends hint at material innovation that can swing cost curves. This list is illustrative; many more publicly available and proprietary documents were reviewed to cross-check figures and assumptions.

Market-Sizing & Forecasting

We reconstruct the 2024 baseline through a top-down "production-plus-net-imports" pool that is reconciled against retail sell-out indices and shipment-level export tallies. Supplier roll-ups and sampled average selling price times volume checks offer bottom-up guardrails that temper any overstatement from macro totals. Key model levers include urban new-home completions, disposable income per capita, plywood and steel price trends, e-commerce share of big-ticket categories, and office floor-space renovation starts. Forecasts to 2030 rely on multivariate regression blended with scenario analysis, allowing demand elasticity to raw-material inflation and housing policy shifts to surface. Gaps in provincial production data are bridged using three-year moving averages and peer ratios from contiguous provinces.

Data Validation & Update Cycle

Outputs undergo variance screening against independent retail sales, PMI new-orders sub-indices, and trade statistics before analyst review rounds. Reports are re-benchmarked each year, with mid-cycle revisions when policy shocks or material supply disruptions cross predefined thresholds.

Why Mordor's China Furniture Baseline Inspires Investor Confidence

Published figures seldom align because study scopes, price assumptions, and refresh timing differ.

We observe that many external estimates fold in custom joinery, soft furnishings, or rental streams, or convert revenues using spot exchange rates that distort local-currency growth narratives.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 160.53 B (2025) | Mordor Intelligence | - |

| USD 170.00 B (2024) | Global Consultancy A | Includes custom and modular installations and applies retail mark-ups to manufacturer values |

| USD 177.00 B (2024) | Research Boutique B | Combines furniture with home décor and uses export FOB prices without domestic back-adjustment |

The comparison shows that, by isolating furniture-only revenues, harmonizing currency at annual average rates, and refreshing models yearly, Mordor delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the China furniture market?

The China furniture market size is USD 169.23 billion in 2026, with a projected value of USD 220.17 billion by 2031.

Which application segment is expanding fastest?

Office furniture shows the highest growth, tracking a 6.01% CAGR for 2026-2031 due to renovation cycles and hybrid-work layouts.

How important is e-commerce to furniture sales in China?

Online discovery now drives most purchase journeys, and omnichannel strategies integrating showrooms with digital visualization tools are critical for growth.

What materials are gaining popularity beyond wood?

Engineered polymers and composite materials are registering the quickest gains as manufacturers seek cost stability and sustainability advantages.

How are global trade policies influencing the China furniture market?

Higher tariffs abroad have pushed export-oriented factories to focus on domestic consumers, intensifying competition and enriching product diversity.

Which regions inside China promise the highest growth potential?

Central and western urban clusters such as Chengdu-Chongqing are expanding rapidly, supported by infrastructure investment and rising home ownership.

Page last updated on: