Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

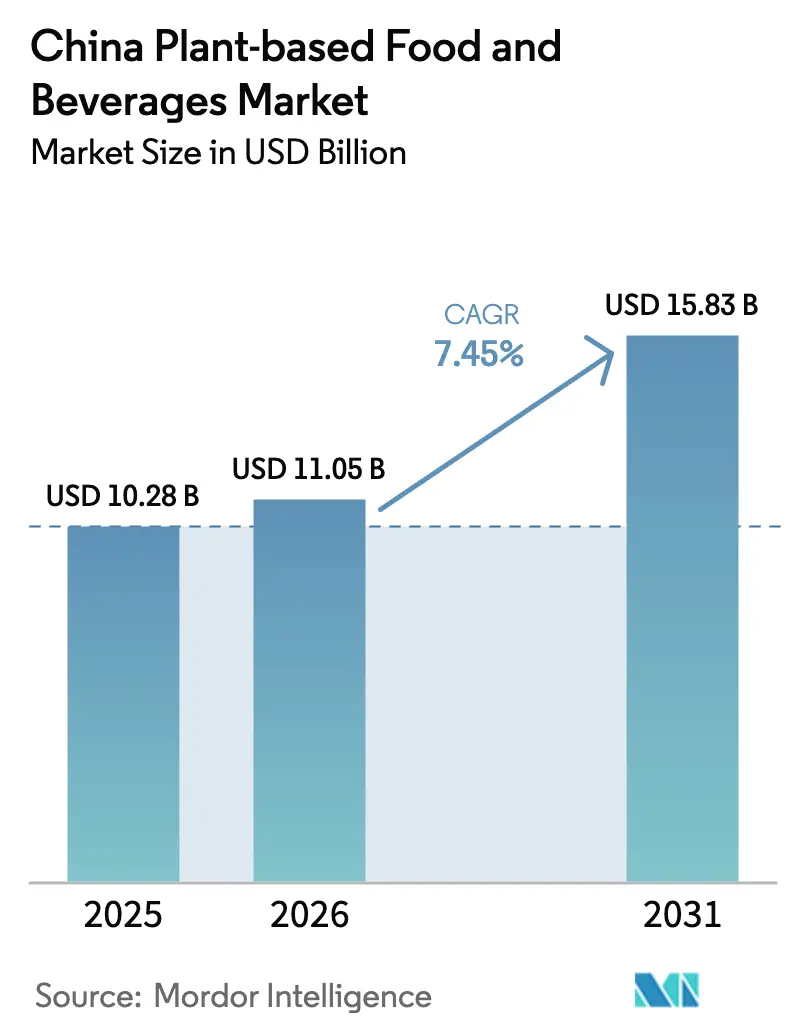

| Base Year Market Size (2025) | USD 10.28 Billion |

| Market Size (2026) | USD 11.05 Billion |

| Market Size (2031) | USD 15.83 Billion |

| Growth Rate (2026 - 2031) | 7.45% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Plant-based Food And Beverages Market Analysis by Mordor Intelligence

China plant-based food and beverages market size in 2026 is estimated at USD 11.05 billion, growing from 2025 value of USD 10.28 billion with 2031 projections showing USD 15.83 billion, growing at 7.45% CAGR over 2026-2031. Demand acceleration reflects rising health consciousness, supportive national policy under the 14th Five-Year Plan, and rapid progress in extrusion and fermentation technologies. Institutional endorsement from the State Council has normalized plant proteins in mainstream dietary guidance, while evolving e-commerce ecosystems shorten the path from product launch to mass trial. Domestic producers leverage scale advantages in soy processing and newly installed pea-protein lines to close the price gap with animal analogs. International entrants contribute advanced know-how, but price sensitivity and taste preferences reward companies that localize textures, seasonings, and cooking formats for Chinese cuisines.

Key Report Takeaways

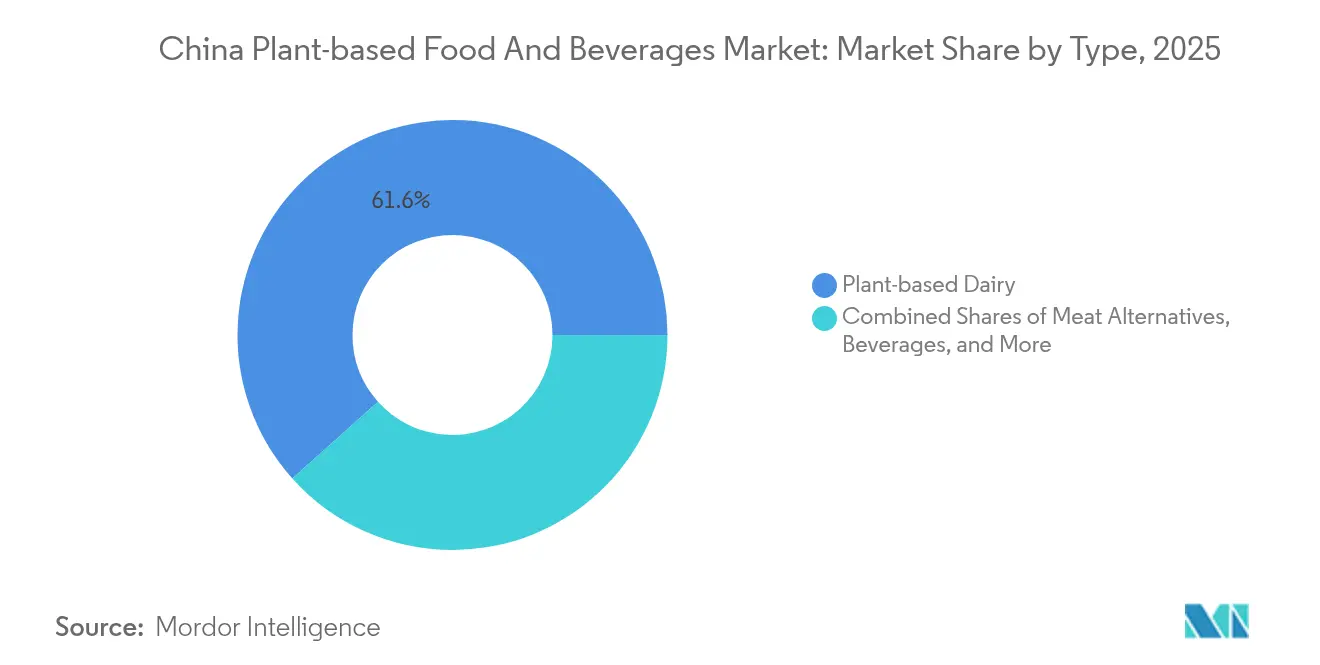

- By type, plant-based dairy led with a 61.62% China plant-based food and beverages market share in 2025. Meat substitutes are forecast to post the fastest 8.66% CAGR through 2031.

- By source, soy captured 53.92% of the Chinese plant-based food and beverages market size among source ingredients in 2025. Pea protein is projected to expand at an 8.41% CAGR between 2026-2031.

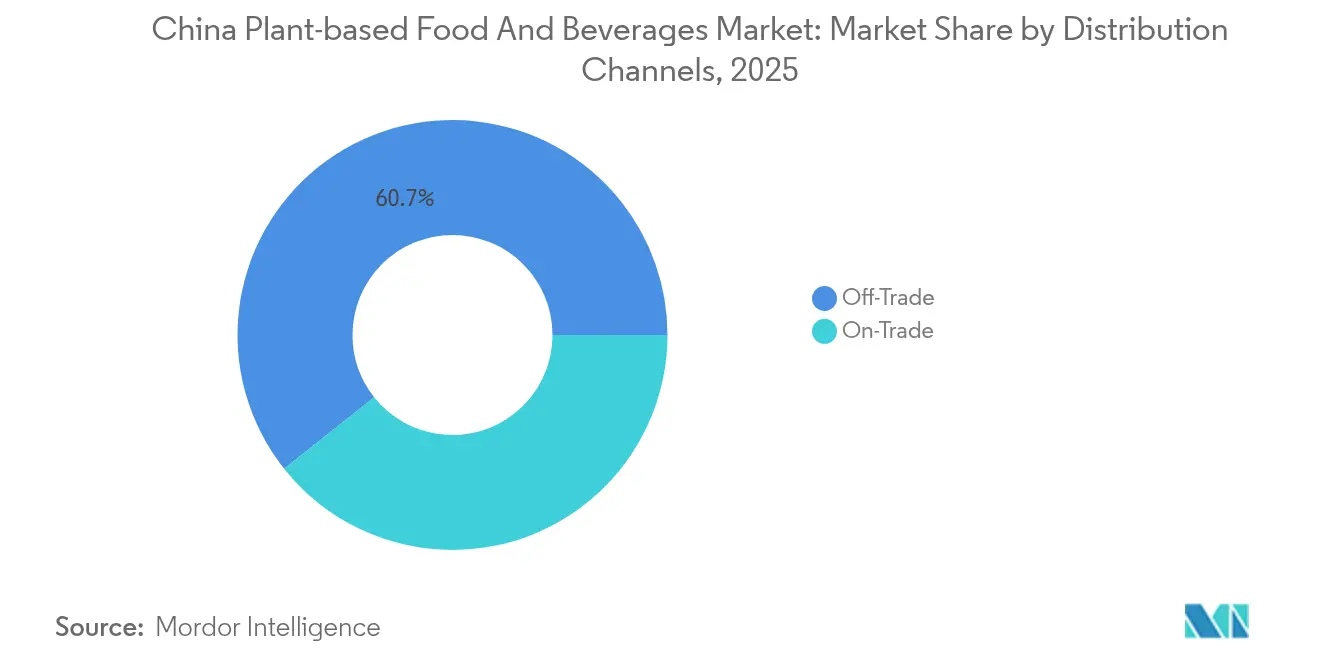

- By distribution Channels, off-trade channels commanded 60.68% revenue share in 2025, whereas on-trade is advancing at an 8.73% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Plant-based Food And Beverages Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Health and Wellness Trends | +1.2% | National, concentrated in tier 1-2 cities | Medium term (2-4 years) |

| Innovation in Product Development | +1.8% | Global, with research and development centers in Beijing, Shanghai | Long term (≥ 4 years) |

| Dietary Shifts and Flexitarianism | +1.0% | Urban areas, expanding to tier 3 cities | Medium term (2-4 years) |

| Increased Availability in Online Channels | +1.5% | National, strongest in tier 1-2 cities | Short term (≤ 2 years) |

| Growing Prevalence of Lactose Intolerance | +0.8% | National, higher impact in northern regions | Long term (≥ 4 years) |

| Influence of Western and Global Trends | +0.9% | Tier 1 cities, spreading to tier 2-3 | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Health and Wellness Trends

Following the pandemic, health consciousness among Chinese consumers has surged, fueling a growing preference for functional foods that combine nutritional benefits with convenience. To align with this trend, the China Food and Drug Administration implemented updated labeling standards, GB 7718-2025 and GB 28050-2025, which mandate clearer and more detailed nutritional information [1]Source: United States Department of Agriculture, “Prepackaged Food Labeling Standards Finalized” apps.fas.usda.gov. These regulations empower plant-based brands to emphasize their products' health advantages, such as zero cholesterol, higher fiber content, and reduced saturated fat levels when compared to animal-based products. This shift is particularly advantageous for the plant-based dairy alternatives market. China has the ability to play a significant role in advancing the global trend toward plant-based meat by boosting output and lowering costs. The country has an abundance of non-GMO soybeans locally and a large processing capacity for plant-based raw materials like soy and pea. According to ProVeg, 98% of Chinese consumers are likely to eat more plant-based foods when presented with scientific data on the benefits of such diets [2]Source: Proveg International, “Most people in China will eat more plant-based food when told of the benefits, survey finds,” proveg.org.

Innovation in Product Development

Chinese manufacturers leverage technological advances in high-moisture extrusion and fermentation processing to craft meat-like textures, addressing long-standing consumer concerns about plant-based alternatives. Research from Singapore's A*STAR highlights that multi-objective Bayesian optimization can fine-tune extrusion parameters, achieving chicken-breast-like hardness with just a 5-7% variance and a cutting force within 15% of targets. Jinan Xilang Machine, a domestic equipment manufacturer, offers production lines for textured vegetable protein, boasting capacities between 100-2,000 kg/hour, underscoring the infrastructure's readiness for scaled production. With China processing about 50% of the world's soy protein capacity, its fermentation capabilities not only reduce ingredient production costs but also position it competitively against imported alternatives.

Dietary Shifts and Flexitarianism

Chinese Generation Z consumers are showing a growing interest in plant-based diets, with environmental concerns (mean score 4.19 out of 5) being the leading motivation, followed by ethical considerations (3.76), according to a recent survey of tourists. Urban respondents, scoring 3.638, report higher perceived benefits compared to rural consumers, who scored 3.266, highlighting a concentration of early adopters in metropolitan areas. However, unlike Western consumers, Chinese consumers view plant-based products as complementary protein sources rather than full meat replacements. This behavioral difference has prompted brands like The Vegetarian Butcher to move away from burger-focused strategies and instead offer localized options, such as breakfast items, bakery fillings, and café applications, where plant proteins enhance rather than replace traditional meals.

Increased Availability in Online Channels

E-commerce platforms are enhancing market accessibility by addressing the limitations of traditional retail. Furthermore, increasing internet penetration is driving the growth of online shopping. According to World Bank data from 2023, China had an internet penetration rate of 78%. Similarly, plant-based brands are implementing strategies to broaden their market presence [3]Source: World Bank, "Internet Penetration Rate in China", data.worldbank.org. By utilizing cross-border e-commerce, these brands can navigate around the complexities of import registration processes while assessing market demand. Additionally, the integration of social commerce features enables collaboration with influencers and the dissemination of educational content. This approach helps bridge consumer knowledge gaps regarding plant-based nutrition and cooking methods. Such initiatives are particularly important for product categories that require significant behavioral changes, ensuring consumers are well-informed and more confident in adopting these alternatives. Moreover, the growing consumer preference for sustainable and health-conscious products is further driving the demand for plant-based alternatives, creating opportunities for brands to innovate and cater to evolving consumer needs.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain and Production Challenges | -1.1% | National, acute in western provinces | Short term (≤ 2 years) |

| Limited Awareness Beyond Major Cities | -0.9% | Tier 3-4 cities and rural areas | Medium term (2-4 years) |

| Regulatory and Standardization Complexities | -0.7% | National, affecting imports and novel ingredients | Long term (≥ 4 years) |

| Flavor and Texture Gaps | -1.3% | National, varying by product category | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain and Production Challenges

Fragmented raw material sourcing and rising costs for animal-free ingredients hinder production scalability and reduce profit margins. Chinese manufacturers in the plant-based sector face challenges with unstable ingredient supplies. Specialized proteins and functional additives require longer lead times and are more expensive compared to traditional food ingredients. Production cost analysis shows that plant-based products often cost 2-4 times more than conventional alternatives. This cost disparity is notable, with 21% of trial consumers identifying price as the main reason for not repurchasing, according to the Food Engineering Journal. Freight expenses further exacerbate these issues, as specialized ingredients need temperature-controlled logistics, and smaller batch sizes drive up per-unit transportation costs. To address these challenges, companies are adopting continuous processing automation and regional manufacturing strategies. Many are also developing integrated ingredient-processing facilities to optimize formulations with lower-cost proteins and simplify supply chains.

Flavor and Texture Gaps

Studies on consumer acceptance consistently identify taste and texture as major obstacles to repeat purchases. A 2020 survey found that 74% of Chinese consumers were unwilling to repurchase plant-based meat due to dissatisfaction with sensory attributes. Traditional Chinese mock meats, which are typically tofu-based and inexpensive, create negative perception benchmarks that next-generation plant proteins must overcome. Chinese culinary traditions emphasize specific textures and cooking techniques, such as high-heat stir-frying or braising, which plant-based alternatives often struggle to replicate. Research indicates that Chinese consumers exhibit greater resistance to meat substitutes compared to their Australian and UK counterparts, with food safety and concerns about over-processing outweighing environmental motivations. This resistance highlights the critical need for significant research and development investments in texture improvement and flavor localization to achieve market acceptance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Dairy Alternatives Drive Market Leadership

In 2025, plant-based dairy holds a dominant 61.62% market share, supported by a cultural preference for soy milk and rapid diversification across coffee shops and retail channels. This segment's leadership stems from consumer trust in established options like soy milk, which has facilitated the growth of oat, almond, and rice-based alternatives. Although meat substitutes currently account for a smaller market share, they exhibit the fastest growth, with an 8.66% CAGR projected from 2026 to 2031, driven by advancements in texture and flavor technologies. Meanwhile, plant-based beverages are leveraging China's growing café culture. Brands such as HEYTEA have achieved significant market presence by innovatively combining plant proteins with traditional tea formulations.

In addition, the food and beverage sector is experiencing growth in plant-based categories such as baking, snacks, and ready-to-eat meals, with companies like Zero Limits leading the way in animal-free bakery products. Regulatory developments also play a crucial role, as the China Food Safety Authority facilitates the approval of novel ingredients under the GB 2760-2024 food additive standards. However, extended approval timelines can delay product development. Furthermore, the Ministry of Agriculture and Rural Affairs influences category dynamics by providing subsidies to support domestic raw milk production, increasing competition and compelling plant-based dairy alternatives to establish clear value propositions beyond price.

By Source: Soy Dominance Faces Protein Diversification

In 2025, soy holds a commanding 53.92% market share, driven by China's role as a leading soy processor and the cultural acceptance of soy-based foods. At the same time, pea protein is experiencing the fastest growth, with an impressive 8.41% CAGR. This growth is supported by China's expanding processing capacity and the protein's superior functional properties, making it ideal for meat analog applications. Wheat protein is utilized in applications requiring gluten networks for texture, while rice and oat proteins appeal to consumers seeking hypoallergenic options or specific nutritional benefits. The diversification trend highlights both consumer demand for variety and manufacturers' efforts to balance cost and functionality across various product categories.

China's increasing processing capacity reflects its readiness for source diversification. Additionally, novel proteins, such as those derived from lion's mane mushrooms and various pulses, offer unique opportunities for differentiation. This is particularly relevant for water-scarce regions exploring alternative crops suitable for non-arable lands. China's agricultural modernization policies promote crop diversification, which could expand the raw material base for plant-based food production and reduce dependence on imported protein sources.

By Distribution Channels: Off-Trade Leadership with On-Trade Growth Acceleration

In 2025, off-trade channels, including supermarkets, hypermarkets, convenience stores, and online platforms, hold a dominant 60.68% market share, providing consumers with extensive access and price transparency. Online channels are experiencing significant growth, driven by platforms like Tmall and JD.com. Additionally, Douyin's social commerce is expanding into lower-tier cities. Convenience and specialty stores function as discovery points, introducing consumers to new products through sampling and promotional efforts. Supermarkets and hypermarkets remain key distribution channels but require substantial marketing investments to secure shelf visibility and encourage consumer trials.

On-trade channels, while currently accounting for a smaller share, are growing at an impressive 8.73% CAGR. This growth is fueled by strategic collaborations between plant-based brands and foodservice operators. Restaurant partnerships enable consumers to try products in prepared formats that enhance flavor while minimizing texture concerns. Examples include partnerships between plant-based suppliers and chains such as KFC, Haidilao, and independent cafés. The foodservice channel offers not only higher profit margins but also opportunities for brand building through chef endorsements and innovative menu designs. However, brands pursuing omnichannel strategies, particularly in cross-border e-commerce, must address regulatory challenges imposed by the Ministry of Commerce, especially regarding direct and distance selling.

Geography Analysis

China is the central focus of this market analysis, with regional differences influenced by economic development and consumer behavior across its tiered cities. Tier 1 cities such as Beijing, Shanghai, Shenzhen, and Guangzhou exhibit the highest levels of market penetration and consumer acceptance. This is driven by higher disposable incomes, greater international exposure, and increased availability of plant-based products through retail and foodservice channels. These urban hubs act as testing grounds for new product launches and brand strategies, with successful initiatives expanding into Tier 2 and Tier 3 markets.

Lower-tier cities offer substantial growth potential as young urbanites relocate from saturated first-tier markets, bringing preferences for premium and health-oriented products. Research shows that narrowing urban-rural income gaps and lower living costs in smaller cities enhance discretionary spending, creating emerging middle-class consumption trends outside major metropolitan areas. However, rural and Tier 3-4 consumers encounter significant barriers to adopting plant-based diets, including cultural and familial preferences for traditional meat, limited product availability, and a lack of awareness about plant-based nutrition and preparation.

Provinces like Shandong, Heilongjiang, and Guangdong, with well-established food processing infrastructures, dominate regional production capabilities. Their strengths lie in proximity to raw materials and efficient transportation networks. While provinces such as Inner Mongolia, Xinjiang, and Heilongjiang benefit from dairy industry subsidies that heighten competition for plant-based alternatives, coastal provinces focus on food technology innovation and export growth. The Ministry of Agriculture and Rural Affairs has allocated billions in subsidies for raw and spray-dried milk, illustrating how regional policies shape the competitive landscape between plant-based and conventional dairy products.

Competitive Landscape

The China plant-based food and beverages market exhibits moderate fragmentation with a concentration, creating space for both established players and emerging disruptors to capture market share through differentiated positioning and localized strategies. Domestic companies leverage cost advantages through integrated supply chains and cultural understanding, while international brands contribute technological expertise and premium positioning. Strategic patterns emphasize partnerships with foodservice operators, e-commerce platform optimization, and regional production to achieve price competitiveness against imported alternatives.

Technology deployment focuses on fermentation capabilities, extrusion processing, and flavor development to address texture and taste barriers that limit consumer adoption. Companies pursuing white-space opportunities target specific use cases like bakery applications, beverage formulations, and ready-to-eat formats where plant proteins complement rather than directly substitute animal products.

The suspension of Beyond Meat's China operations in 2025 illustrates the challenges facing international brands that fail to adapt formulations and pricing to local market conditions, creating opportunities for domestic players with localized product development capabilities and cost-competitive manufacturing. Regulatory compliance factors from the China Food Safety Authority regarding novel food approvals and labeling standards influence competitive positioning, particularly for companies introducing innovative ingredients or processing technologies.

China Plant-based Food And Beverages Industry Leaders

-

Green Monday Group

-

Qishan Foods

-

Oatly Group AB

-

Yili Group

-

The Livekindly Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Oatly launched three new vegan ice creams in China through strategic foodservice partnerships with the country's leading hotpot chain Haidilao and global fast-food brand KFC. Oatly introduced oat-based fruit popsicles at Haidilao in guava and grape flavors.

- March 2024: Marvelous Foods launched its Yeyo plant-based coconut yogurt in Ole, China’s largest premium supermarket chain. The launch began in Beijing, coinciding with Ole’s opening of a new low-carbon lifestyle concept store that enabled enhanced consumer education and better visibility for plant-based offerings.

- November 2023: Avonmore, Ireland’s leading milk brand, launched its Oat Drink Barista in China, marking its entry into the Chinese plant-based beverages sector. The oat drink, made from traceable Irish organic oats grown by Tirlán farmers, was specially formulated for a creamy, foamy texture suitable for lattes.

- July 2023: Veg of Lund, a Swedish potato milk brand, launched its DUG potato milk products in China, in collaboration with Haofood. The collaboration marked DUG's entry into the Chinese market, leveraging Haofood's established plant-based distribution network.

China Plant-based Food And Beverages Market Report Scope

The plant-based food and beverages include meat and dairy substitute products derived from plant products. The products include meat alternatives made from different plant-based ingredients like chickpea, soy and tofu, pea protein, and other such ingredients. The plant-based beverages include dairy alternatives like oats milk, almond milk, coconut milk, and other such beverages. By product type the market studied is segmented into meat substitutes, dairy alternative beverages, non-dairy ice cream, non-dairy cheese, non-dairy yogurt, and non-dairy spreads. Meat substitutes are bifurcated into Textured Vegetable Protein, Tofu, Tempeh, and others. Beverages are further segmented into soy milk, almond milk, and other beverages. By distribution channel, the market is segmented into hypermarkets/supermarkets, convenience stores, online retail channels, and other distribution channels. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Type

| Plant-based Dairy | Yogurt |

| Cheese | |

| Frozen Dessert and Ice Cream | |

| Other Dairy Products | |

| Meat Substitutes | Tofu |

| Tempeh | |

| Textured Vegetable Protein | |

| Other Meat Substitutes | |

| Beverages | Milk |

| Smoothies | |

| Tea | |

| Coffee | |

| Other Beverages | |

| Other Food and Beverages |

By Source

| Soy |

| Pea |

| Wheat |

| Rice |

| Oats |

| Other Sources |

By Distribution Channels

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Channels | |

| Other Distribution Channels |

| By Type | Plant-based Dairy | Yogurt |

| Cheese | ||

| Frozen Dessert and Ice Cream | ||

| Other Dairy Products | ||

| Meat Substitutes | Tofu | |

| Tempeh | ||

| Textured Vegetable Protein | ||

| Other Meat Substitutes | ||

| Beverages | Milk | |

| Smoothies | ||

| Tea | ||

| Coffee | ||

| Other Beverages | ||

| Other Food and Beverages | ||

| By Source | Soy | |

| Pea | ||

| Wheat | ||

| Rice | ||

| Oats | ||

| Other Sources | ||

| By Distribution Channels | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Channels | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

How large will China’s plant-based food and beverages sector be by 2031?

It is projected to reach USD 15.83 billion, reflecting a 7.45% CAGR from 2026.

Which product category leads sales in China’s plant-protein space?

Plant-based dairy accounts for 61.62% of revenue, supported by long-standing soy-milk consumption and café partnerships.

What ingredient is gaining share fastest after soy?

Pea protein is forecast to expand at an 8.41% CAGR thanks to domestic capacity expansion and favorable functionality for meat analogs.

Which sales channel shows the quickest growth?

On-trade foodservice, including cafés and restaurants, is advancing at an 8.73% CAGR as menu integrations boost trial.

Page last updated on: