Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

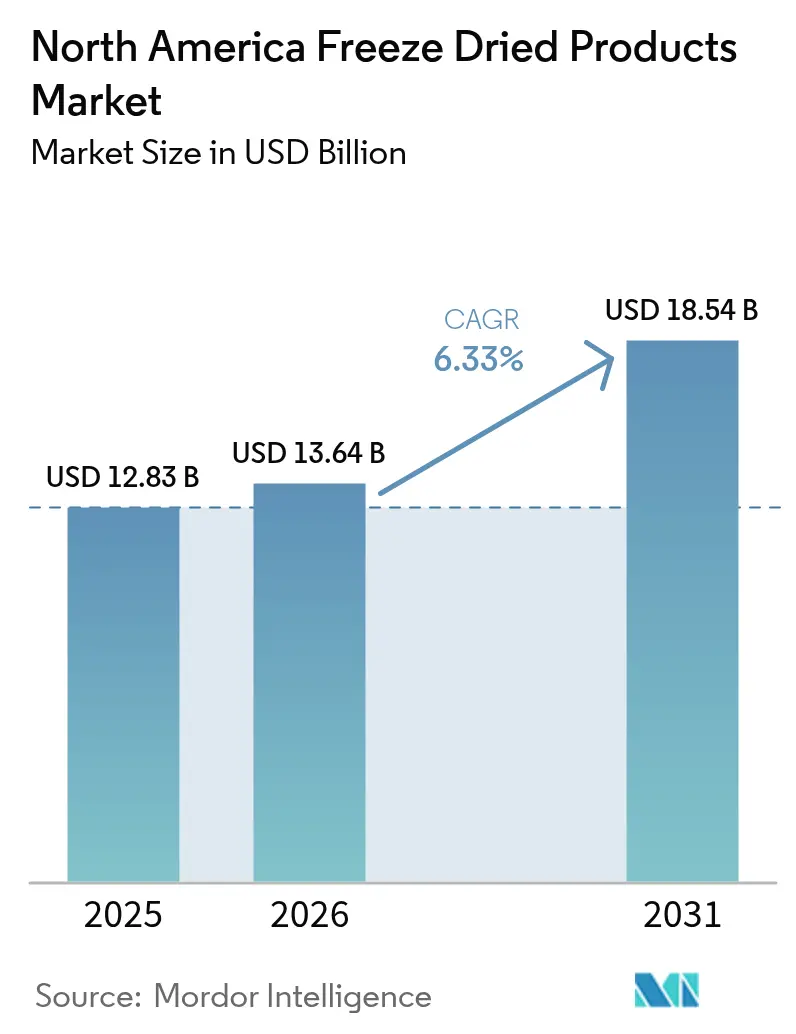

| Base Year Market Size (2025) | USD 12.83 Billion |

| Market Size (2026) | USD 13.64 Billion |

| Market Size (2031) | USD 18.54 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

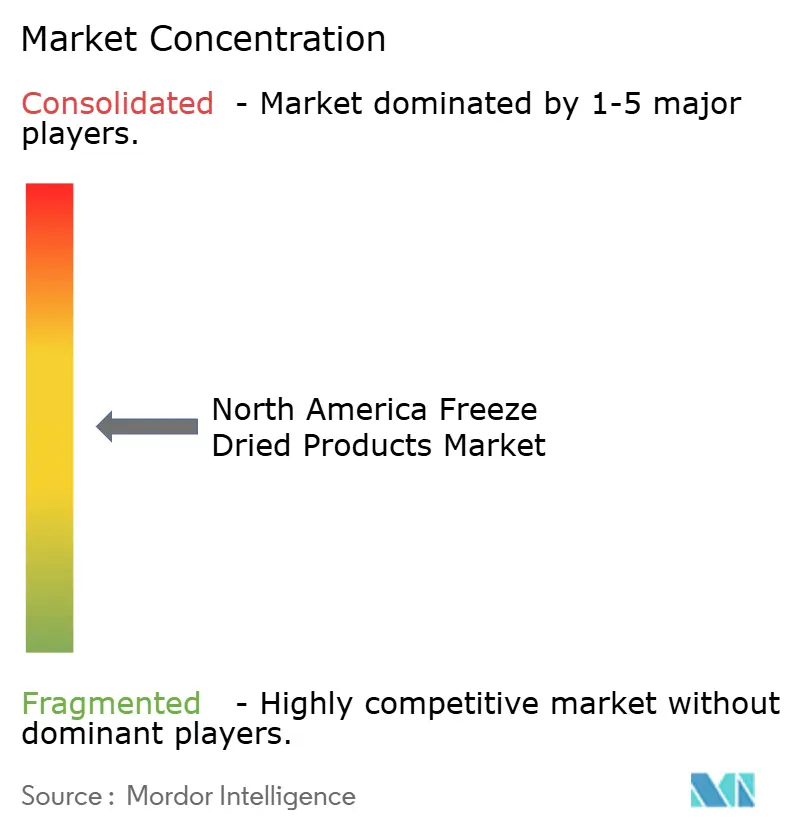

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Freeze Dried Products Market Analysis by Mordor Intelligence

The North America freeze-dried products market size in 2026 is estimated at USD 13.64 billion, growing from the 2025 value of USD 12.83 billion, with 2031 projections showing USD 18.54 billion, growing at 6.33% CAGR over 2026-2031. Robust defense provisioning, energy savings of 40% from continuous-process technology, and the premiumization of pet diets collectively set the growth tone. While the United States leads in volume and innovation, Mexico experiences the fastest expansion, driven by CUSMA's duty-free trade and NOM-051's clean-label regulations, which encourage domestic processors to adopt higher standards and expand their offerings. The momentum is further bolstered by the appeal of shelf-stable convenience, an organic crossover facilitated by the Canada-Mexico Organic Equivalency Arrangement, and a surge in online direct-to-consumer sales, which provide consumers with greater accessibility and variety. However, challenges arise as tariffs on machinery from China and Mexico elevate capital costs, impacting investment decisions for processors. Additionally, volatility in raw materials, particularly high-brix berries, tightens processor margins, creating pressure on profitability. These factors temper the market's growth, but don't halt its ascent.

Key Report Takeaways

- By product type, freeze-dried fruits led with 33.58% of north america freeze-dried products market share in 2025 and are projected to register a 5.98% CAGR through 2031, while pet foods are forecast to expand the fastest at an 10.62% CAGR over the same period.

- By nature, conventional offerings accounted for 86.55% of 2025 revenue; organic products are set to grow at an 8.44% CAGR between 2026-2031.

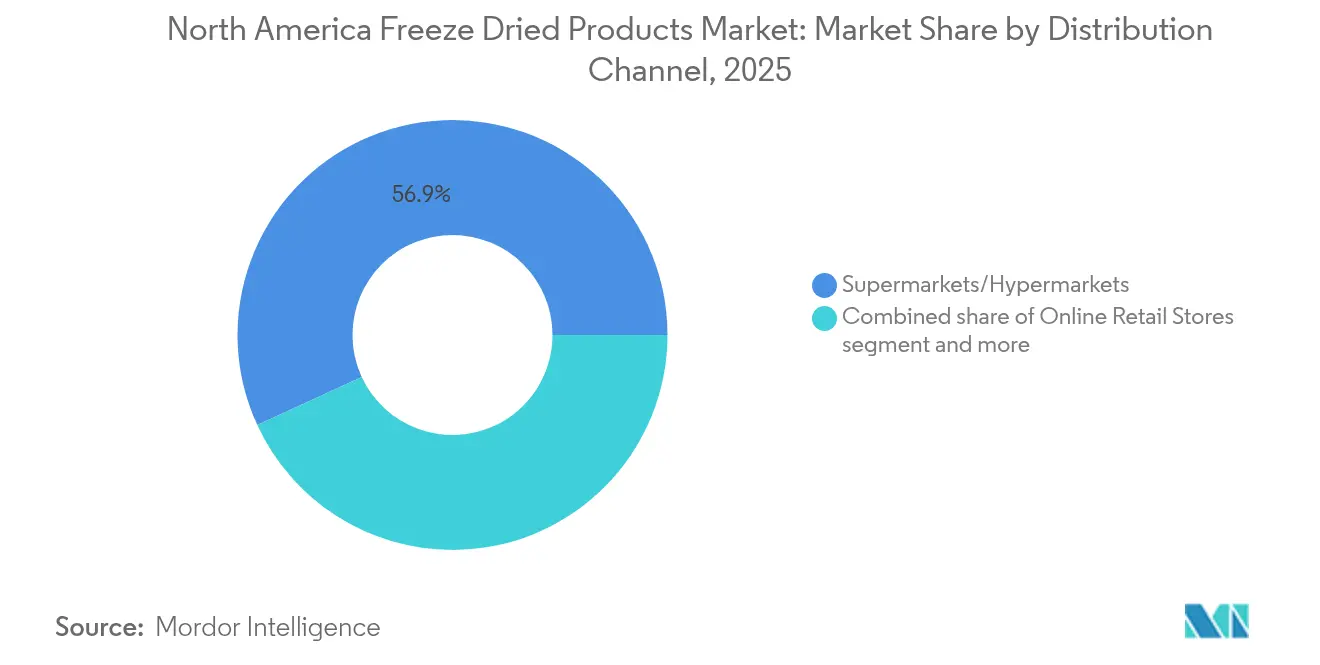

- By distribution channel, supermarkets and hypermarkets held 56.88% share in 2025, whereas online retail is expected to rise at a 8.96% CAGR through 2031.

- By geography, the United States commanded 79.55% of 2025 value; Mexico is anticipated to record a 6.78% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Freeze Dried Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenient shelf-stable food demand | +1.2% | United States, Canada, Mexico urban centers | Medium term (2-4 years) |

| Clean-label, nutrient-retaining preferences | +1.0% | Pan-regional | Long term (≥ 4 years) |

| E-commerce and direct-to-consumer growth | +0.9% | United States, Canada, selected Mexican metros | Short term (≤ 2 years) |

| Retail private-label premium SKUs | +0.7% | United States big-box, Canadian supermarket groups | Medium term (2-4 years) |

| Continuous freeze-drying energy savings | +0.8% | United States and Canadian production hubs | Long term (≥ 4 years) |

| United States military demand for lighter rations | +0.5% | United States defense clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient shelf-stable foods

Consumers are increasingly opting for ambient products that reduce spoilage and facilitate quick meal preparation, trading them for fresh and frozen items. Freeze-dried fruits and entrées boast a remarkable 25-30 year shelf life, help households cut food waste by up to 22%, and are 80-90% lighter than their hydrated counterparts, making them highly convenient for storage and transportation. Regions like the Gulf Coast and those prone to wildfires are purchasing 20-25% more per capita, underscoring the heightened emphasis on disaster preparedness, as these products provide a reliable food source during emergencies. The U.S. Army's endorsement of freeze-dried ration packs bolsters its credibility in civilian markets, as it highlights their practicality and durability under extreme conditions[1]Source: United States Army, "DEVCOM Soldier Center transitions new individual field ration for DoD-wide availability", army.mil. Retailers are weaving this "tactical nutrition" theme into their marketing strategies, ensuring that baseline demand remains resilient against the usual grocery market fluctuations while appealing to consumers' growing interest in long-term food security and convenience.

Growing preference for clean-label nutrient-retaining products

Freeze-drying, a method that preserves up to 98% of key micronutrients, stands out as superior to both air and spray-drying techniques due to its ability to retain nutritional value and extend shelf life[2]Source: National Center for Biotechnology Information, "Exploring Association Between Individuals’ Stature and Type 2 Diabetes Status: Propensity Score Analysis", pmc.ncbi.nlm.nih.gov. Starting in 2026, Canada’s new front-of-pack regulations will penalize products high in sugar and sodium, aiming to promote healthier food choices. This regulatory shift is steering formulators towards incorporating freeze-dried ingredients, which align with these health-focused standards. Research from Cornell University highlights the dairy industry's potential, suggesting brands can now substitute artificial electrolytes with natural minerals derived from whey permeate, enhancing product appeal and nutritional value. Additionally, the Canada-Mexico Organic Equivalency Arrangement's extension is reducing cross-border certification costs, simplifying trade processes, and leading to a surge in organic product adoption. Furthermore, younger, health-conscious consumers are increasingly associating freeze-dried products with wellness, recognizing their nutritional benefits and convenience. This trend is expanding their appeal beyond traditional emergency or camping uses, positioning freeze-dried products as a staple in everyday health-conscious lifestyles.

Expansion of e-commerce and D2C distribution

Online revenue sees an annual growth of nearly 10%, driven by the lightweight nature and extended shelf life of products, making parcel shipping cost-effective. With its direct-to-consumer (D2C) launch, Stella & Chewy not only captures the full margin but also gains valuable first-party data, enabling better customer insights and targeted marketing strategies. Their subscription bundles have elevated the lifetime value by almost 25%, offering consumers convenience and cost savings while fostering brand loyalty. Trends on TikTok, especially around freeze-dried candy, have led to a 340% year-over-year surge in category searches, highlighting the platform's influence on consumer behavior and product discovery. Amazon's inclusion of products in its Subscribe and Save program has further popularized pantry-stable SKUs, making them more accessible and appealing to a broader audience. Moreover, D2C channels are bridging the gap for rural households, contributing an estimated 12% boost to the total addressable demand by providing easier access to products that were previously less available in remote areas.

Retail private-label investment in premium freeze-dried SKUs

In 2024, big-box chains like Costco, Walmart, and Kroger flexed their shelf power, rolling out competitively priced fruits and vegetables. This strategic move not only attracted price-sensitive households but also significantly eroded the market share of established branded rivals. By leveraging their scale and supply chain efficiencies, these retailers were able to offer private-label products at lower prices without compromising on quality. Collaborating with ingredient specialists such as Van Drunen Farms and Mercer Foods further enabled them to enhance product offerings and meet consumer demand for fresh and affordable options. As a result, private-label penetration surged to 30% in 2024, marking a notable shift in consumer preferences. Meanwhile, branded players found themselves compelled to heavily invest in differentiation strategies such as introducing flavored yogurt bites or single-serve camp pouches to maintain their presence on the shelves and justify their premium pricing. Notably, these private-label lines boast gross margins of 30-40%, significantly outpacing the 20% margins of their branded counterparts, further solidifying their appeal to retailers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital- and energy-intensive production | -0.8% | United States, Canada greenfield builds | Short term (≤ 2 years) |

| Cheaper dehydrated or frozen substitutes | -0.6% | Region-wide, price-sensitive aisles | Medium term (2-4 years) |

| 2025 tariffs on machinery and barrier films | -0.4% | United States importers, packaging converters | Short term (≤ 2 years) |

| Volatile high-brix fruit prices | -0.3% | United States, Mexico sourcing belts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capital and energy costs inflate retail pricing

Starting at around USD 500,000 per chamber, equipment packages contribute significantly to total project costs, which can exceed USD 10 million for a mid-sized 10,000 sq ft plant. With electricity consumption ranging from 1.5 to 2 kWh per kilogram, power expenses account for approximately one-fifth of the finished goods cost, making energy efficiency a critical factor in operational profitability. Seasonal demand fluctuations result in capacity utilization dropping below 60%, which increases overhead costs per unit. This, in turn, keeps strawberry shelf prices between USD 18 and 24 per pound, three times the price of air-dried equivalents, thereby limiting affordability for consumers. Shepherd Boy Farms' USD 50 million investment in Indiana highlights the importance of achieving scale to reach breakeven. This requirement for substantial capital investment discourages new entrants and reinforces high barriers to entry in the market.

Competition from cheaper dehydrated/frozen substitutes

Budget-conscious consumers are gravitating towards dehydrated products, which retain 60-80% of their nutrients yet come at a cost that's 40-60% lower, making them an attractive option in the trail-mix and cereal aisles. Conagra’s Future of Frozen 2025 report highlights the dominance of frozen meals, valued at USD 28.9 billion, and vegetables, at USD 7.5 billion, overshadowing the freeze-dried segment in terms of market size and consumer preference. Techniques like IQF (Individually Quick Frozen) and cryogenic freezing, which maintain texture and color affordably, are blurring the lines of differentiation for freeze-dried products by offering similar quality at a lower cost. As a result, suppliers are pivoting their focus towards emergency, outdoor, and pet markets, where considerations of weight, portability, and product longevity take precedence over price, catering to niche consumer needs in these segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fruit Leadership, Pet-Food Momentum

In 2025, freeze-dried fruits captured a 33.58% share of North America's freeze-dried products market revenue, buoyed by robust demand from cereals, snack bars, and confectionery products. By 2031, this segment is set to contribute an additional USD 1.82 billion, thanks to rapid-cycle technology that narrows the cost gap with air-dried alternatives. Leading the SKU counts are strawberry, raspberry, and mango, while apple and pineapple take the lead in bulk orders for bakery mixes. This dominance underscores the familiar taste profiles and established processing methods of these fruits, with strawberries, raspberries, and pineapples particularly favored for their freeze-drying attributes.

While pet foods start from a smaller base, they are poised to outstrip all other segments with an impressive 10.62% CAGR. This surge is driven by pet owners' readiness to spend USD 3-5 per ounce on raw toppers that tout “ancestral nutrition.” In a testament to this burgeoning market, Shepherd Boy Farms and Petsource by Scoular poured in a combined USD 125 million for capacity expansions in 2024-2025. Such investments underscore a robust institutional confidence in the pet nutrition sector's growth. The market's diversification, bolstered by steady volumes from vegetables, meat, seafood, and dairy processing lines, ensures stability and mitigates over-reliance on any single end-use.

By Nature: Conventional Scale Meets Organic Acceleration

In 2025, conventional SKUs captured a dominant 86.55% share of North America's freeze-dried products market. This stronghold is bolstered by extensive grower networks and competitive farm-gate pricing, which allow manufacturers to offer products at attractive price points. Broad supply chains ensure consistent availability, particularly in military rations and budget supermarkets, where affordability remains a key driver of sales volume. Retailers adeptly dual-source from Baja California and California, bridging seasonal gaps and ensuring shelves remain stocked year-round. This dynamic highlights the entrenched position of conventional products in cost-sensitive markets, where price and availability are critical factors for consumer choice.

Organic products, starting from a modest 13.45% share in 2025, are projected to surge to nearly 17.60% by 2031, outpacing their conventional counterparts, thanks to a growing alignment with clean-label trends and increasing consumer awareness of health and sustainability. The Canada-Mexico Organic Equivalency Arrangement alleviates dual certification costs, making organic products more accessible to producers and consumers alike. Additionally, front-of-pack sugar and sodium warnings enhance the appeal of organic fruits, particularly among health-conscious buyers. Price premiums remain robust: organic strawberries fetch USD 24-32 per pound, outpacing the USD 18-24 for conventional. Yet, millennials willingly pay the premium for the promise of transparent sourcing and sustainable practices. Meanwhile, processors are locking in multi-year contracts with regenerative growers, ensuring stability in raw material costs and fostering long-term partnerships that support the organic supply chain.

By Distribution Channel: Supermarket Scale, Digital Velocity

In 2025, brick-and-mortar supermarkets and hypermarkets captured 56.88% of North America's freeze-dried products market turnover, to capitalize on high foot traffic and strategic in-aisle placements. These stores effectively attract consumers with visually as they shop for daily essentials, making them ideal for into which freeze-dried products can be integrated placed. Major players, including Costco, Walmart, and Kroger, boosted their private-label offerings by 15-20%, amplifying both visibility and sales volume. Convenience outlets, on the other hand, zero in on impulse snack purchases, promoting single-serve pouches. Meanwhile, outdoor specialists and military commissaries cater to specialized needs, offering premium, high-ticket kits.

Online retail emerges as the fastest-growing channel, set to achieve a 8.96% CAGR through 2031, fueled by subscription models and social-commerce tools. Stella & Chewy’s direct-to-consumer (D2C) push boasts repeat purchase rates 22-28% above brick-and-mortar, underscoring their digital retention prowess. This online shift broadens geographic reach, allowing efficient shipping of lightweight freeze-dried products to remote locales where fresh goods are costly to distribute. Such channel diversification shields the market from disruptions linked to any single distribution method.

Geography Analysis

In 2025, the U.S. accounted for a dominant 79.55% of the market value, buoyed by its deep-rooted outdoor culture, recurrent climate-related crises, and defense contracts. The entrenched outdoor culture fosters consistent demand for related products, while frequent climate emergencies drive the need for preparedness solutions. Additionally, defense provisioning contracts provide a steady revenue stream for key players. Private labels surged to claim 30% of the market, shifting power dynamics in favor of retailers as they leverage cost advantages and brand flexibility. While tariffs on machinery imports from China and Mexico have heightened expansion costs, established players, with their sunk assets and operational efficiencies, adeptly defend their market share. With household penetration stabilizing around 40%, suggesting a slowdown in incremental gains, upgrades in pet food and ongoing process enhancements are poised to sustain an overall growth trajectory of 5-7%.

Canada, accounting for about 13.25% of regional sales, is driven by regulations like Safe Food for Canadians licensing, bilingual packaging, and forthcoming nutrient flags on packaging. These regulations, particularly the French labeling requirement, pose challenges for smaller U.S. exporters, inadvertently bolstering domestic processors' market position. The Safe Food for Canadians licensing ensures stringent quality standards, while bilingual packaging mandates cater to the country's diverse population. Thanks to an equivalency agreement with Mexico, organic product line extensions are flourishing, reducing compliance costs and enabling Canadian producers to expand their offerings in the organic segment.

Mexico, though currently smaller in stature, is set to lead the region with a robust 6.78% CAGR through 2031, driven by clean-label regulations and urban consumers' time constraints. Clean-label rules align with growing consumer preferences for transparency and healthier options, while urban time poverty increases demand for convenient, ready-to-use products. While the CUSMA agreement facilitates duty-free trade, challenges arise from COFEPRIS documentation and new machinery tariffs, complicating capital investments. Yet, local assemblers are capitalizing on U.S. berry imports and cross-border e-commerce, especially in urban hubs where demand is concentrated. Meanwhile, while the Caribbean and Central American islands represent a niche market, they exhibit notable per-capita consumption, particularly for disaster preparedness, as these regions frequently face natural disasters, necessitating higher readiness levels.

Regulatory Landscape

In the United States, freeze-dried foods fall under FDA food safety and labeling requirements, with FSMA programs shaping processor and importer controls for higher-risk ingredients used in freeze-dried fruits and prepared foods. FDA set a uniform compliance date of January 1, 2028 for food labeling regulations published between January 1, 2025 and December 31, 2026, giving brand owners a defined window to align label artwork, inventory run-downs, and multi-SKU packaging refresh cycles.

Traceability compliance timelines also influence ingredient and co-manufacturing networks. FDA has indicated a proposed extension of the FSMA Food Traceability Rule compliance date to July 20, 2028, and 2026 draft guidance activity has reinforced the need to structure lot coding, event tracking, and recordkeeping across upstream produce supply, co-packers, and finished-goods distribution. In Canada, the Safe Food for Canadians Regulations (SFCR) and Canadian Food Inspection Agency preventive control plan expectations govern domestic and imported foods, with importers expected to demonstrate safety outcomes equivalent to Canadian preventive controls, increasing documentation and verification needs for cross-border shipments of freeze-dried products and ingredients.

Competitive Landscape

The North American freeze-dried Products Market exhibits moderate concentration. Nestlé, Kerry Group, and Conagra integrate freeze-dried inclusions across global research and development pipelines but do not exceed mid-single-digit shares individually. These companies focus on leveraging their extensive research capabilities to innovate and expand their product offerings, although their market shares remain relatively fragmented. Their efforts are directed toward enhancing product quality and meeting evolving consumer demands, particularly in the convenience and health-focused food segments.

Ingredient-first suppliers OFD Foods, Van Drunen Farms, and Mercer Foods dominate the market, working closely with co-packers and private-label clients. They adeptly balance volume and margin, catering to both military and retail sales. Their ability to manage large-scale operations while maintaining cost efficiency has positioned them as key players in the supply chain. These suppliers also invest in advanced technologies and strategic partnerships to strengthen their market presence. Meanwhile, Patent EP 4455590 A1 and microwave-assisted systems emerge as pivotal differentiators, granting early adopters a notable 20-25% advantage in unit costs. These technologies enable faster production cycles and reduced energy consumption, providing a competitive edge in terms of both cost and sustainability. Additionally, these innovations align with the growing demand for environmentally friendly production processes, further enhancing their appeal.

Pet-nutrition innovators like Stella & Chewy’s and Vital Essentials cultivate a loyal super-premium clientele, bolstered by endorsements from veterinarians. Their focus on high-quality, nutrient-rich products has resonated with consumers seeking premium options for their pets. These companies also emphasize transparency in sourcing and production, which has become a critical factor for pet owners. Firms that are vertically integrated and secure contracts for raw materials and renewable energy sources are reaping the benefits of continuous freeze-drying rollouts, enjoying both cost advantages and ESG appeal. This integration allows them to streamline operations, reduce dependency on external suppliers, and align with sustainability goals. As 2025 tariff schedules loom, market entry challenges intensify, positioning technology partnerships and asset-light D2C strategies as the most promising avenues for newcomers. These approaches enable new entrants to mitigate risks associated with high capital investments while leveraging established networks and innovative technologies to gain a foothold in the market. Furthermore, the rising consumer preference for sustainable and innovative products creates opportunities for new players to differentiate themselves through unique value propositions.

North America Freeze Dried Products Industry Leaders

-

Nestlé S.A

-

Kerry Group plc

-

Conagra Brands Inc.

-

OFD Foods LLC

-

Van Drunen Farms

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Mainstreaming of freeze-dried formats in impulse snacking and confectionery is creating white space beyond the category's traditional anchors in outdoor, emergency, and specialty nutrition. In January 2026, Mars rolled out M&M's POP'd (freeze-dried caramel chocolates) nationwide following a November 2025 soft-launch via TikTok Shop and MMS.com, indicating that large branded portfolios are allocating shelf and media support to freeze-dried textures rather than treating them as a niche novelty. This widens opportunities for ingredient suppliers and co-packers that can deliver consistent crunch, flavor delivery, and scalable particulate inclusions for bars, cereals, and confections.

On the supply and process side, cost and throughput constraints are pushing manufacturers to evaluate alternatives or complements to classic chamber freeze-drying, particularly where energy intensity and capex slow capacity additions. In May 2026, EnWave Corporation signed a technology evaluation and license option agreement with an unnamed multinational packaged food company (over USD 20 billion in annual revenue) to assess Radiant Energy Vacuum (REV) technology across multiple food categories, which points to active buyer interest in vacuum-based dehydration routes that can support commercial-scale launches. At the same time, regulatory time horizons, such as FDA's January 1, 2028 uniform labeling compliance date, set a practical cadence for reformulation and packaging upgrades, supporting programmatic rollouts of clean-label freeze-dried ingredients and portion-controlled SKUs through retail and D2C channels.

Recent Industry Developments

- June 2026: Chef Kitty launched freeze-dried quail egg yolks for cats and dogs in the United States. The product expands freeze-dried offerings into functional, single-ingredient animal nutrition, reinforcing premiumization in pet treats and toppers where nutrient density and portability support higher price points.

- April 2026: Mountain House (OFD Foods LLC) introduced two new meals, Cajun Style Jambalaya and Breakfast Fried Rice, produced in Albany, Oregon. The launch refreshes the prepared-meals assortment with higher-protein positioning and helps sustain brand relevance in outdoor and emergency channels that value long shelf life and lightweight convenience.

- April 2024: Oregon Freeze Dry (OFD Foods LLC) reorganized its business into two verticals, Food and Life Sciences. The realignment concentrates resources by end-market, strengthening commercialization focus for food programs while preserving specialized capabilities that can support higher-value applications and quality systems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of freeze-dried products sold in North America, where moisture is removed through freeze-drying to improve shelf life and usability across food and related end uses.

Scope exclusions: It does not count non-freeze drying methods (such as air-dried or spray-dried products) even if they are sold in similar channels.

Segmentation Overview

-

By Product Type

-

Freeze-Dried Fruits

- Strawberry

- Raspberry

- Pineapple

- Apple

- Mango

- Other Fruits

-

Freeze-Dried Vegetables

- Pea

- Corn

- Carrot

- Potato

- Mushroom

- Other Vegetables

- Freeze-Dried Meat and Seafood

- Freeze-Dried Dairy Products

- Freeze-Dried Beverages

- Prepared Meals

- Pet Foods

-

Freeze-Dried Fruits

-

By Nature

- Conventional

- Organic

-

By Distribution Channel

- Supermarket/Hypermarket

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

- United States

- Canada

- Mexico

- Rest of North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial market map and set practical guardrails for demand and pricing in North America. We reviewed public sources such as USDA data and reports, US Census and trade releases, Statistics Canada tables, the US International Trade Commission trade database, and Food and Drug Administration labeling guidance, which helps interpret category movement and compliance signals.

Along with these, we relied on company annual reports, investor presentations, and reputable press coverage to track changes in product mix and channel shifts like online retail. For pricing and company financial context, we also used paid subscriptions for company financials and news intelligence, plus import and export shipment-level data where it supported trade-linked volume validation. These desk sources are illustrative only, and other public references were used to collect, verify, and clarify data points.

Primary Interviews and Surveys

Primary work focused on talking with a mix of manufacturers, ingredient and packaging stakeholders, distributors, and large buyers across the United States, Canada, and Mexico, so desk research assumptions could be confirmed in operating terms. Interviews were used to sanity-check category splits, typical pricing movement, the share of organic offerings, and the pace of demand across applications such as snacking, ready meals, and pet food, before the totals were finalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | |

| Mid tier: 58% | Functional/Unit leaders: 28% | |

| Smaller Players: 16% | Managers: 58% |

Market-Sizing & Forecasting

Sizing started with a top-down build where North America food category demand was reconstructed into a freeze-dried value pool using product availability and adoption signals, followed by normalization for channel mix and typical price ladders. To keep the totals realistic, the outputs were then cross-checked with selective bottom-up approximations, such as sampled price per pack or per kilogram multiplied by implied consumption volume in key product groups.

Inputs that matter for this market include freeze-dried penetration in snacks and meal components, the share of pet food using freeze-dried inclusions, organic versus conventional mix, online retail contribution versus store-based sales, and the direction of unit pricing tied to raw material and energy cost pressure. Where direct bottom-up detail was missing for smaller niches, we filled gaps using proxy ratios from similar freeze-dried categories, then re-tested those ratios during primary calls.

For forecasting, scenario analysis was used so growth could be flexed based on how quickly adoption spreads across convenience-led categories and premium pet nutrition, and then the scenarios were anchored to what experts expect for pricing progression and channel expansion. Assumptions were kept simple enough to be repeated, and each step was tied back to a measurable signal that could be refreshed annually.

Data Validation & Update Cycle

Validation was done through multiple checks that compare modeled totals against independent indicators, such as trade direction, category momentum in retail and e-commerce, and the expected split of major product types. When a number looked out of range, we revisited the drivers, re-checked the conversion logic, and re-contacted sources if the variance could not be explained.

Before sign-off, the model and assumptions go through a step-by-step analyst review so calculation errors and inconsistent inputs are caught early. The report is refreshed every year, and interim updates are added when material events change prices, availability, or demand. Right before delivery, a final review pass is done so clients receive the most current view.

Mordor Intelligence's North America Freeze Dried Product Market Size Compared Against Other Published Estimates

Published market sizes for freeze-dried products in North America can look far apart, even when they appear to describe the same product set. The gaps usually come from how broadly products are defined, which years are treated as the base, how pricing is converted and updated, and how much interview validation is used to correct desk-driven assumptions.

Some estimates present a broader freeze-dried foods number that can drift toward adjacent preserved-food categories or use aggressive price growth across all applications. In Mordor Intelligence, only freeze-dried products are counted, and non-freeze drying formats are kept out even if they compete in the same retail aisle, which keeps the model tied to a cleaner demand pool and more consistent pricing checks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 12.83 B (2025) | |

| Global Consultancy A | USD 36.31 B (2024) | Uses a different base year and a wider freeze-dried foods framing, which likely pulls in more applications and a broader product sweep than freeze-dried products alone, and then applies faster value expansion assumptions. |

| Industry Publisher B | USD 16.24 B (2025) | Covers freeze-dried food for fewer countries and narrower end-use labeling, and the sizing approach appears more segment-led, which can shift totals depending on how channels and product forms are mapped into value. |

The table shows that the spread is mainly explained by scope width and base-year treatment, and then amplified by how prices and channel shares are projected forward. By keeping inclusions explicit and checking assumptions against real channel and application signals, the resulting number is easier to trace, re-run, and update as new information arrives.

Key Questions Answered in the Report

What is the 2026 valuation for freeze-dried foods in North America?

The north america freeze-dried food market size stands at USD 13.64 billion in 2026.

How fast will the category grow through 2031?

Revenue is projected to advance at a 6.33% CAGR between 2026 and 2031.

Which product line is expanding the quickest?

Pet-food applications are forecast to register an 10.62% CAGR over 2026-2031 as premium raw toppers gain traction.

Why is Mexico the fastest-growing geography?

CUSMA duty-free access and NOM-051 clean-label labeling rules push Mexico to a 6.78% CAGR through 2031.

Page last updated on: