Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.29 Billion |

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 1.79 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

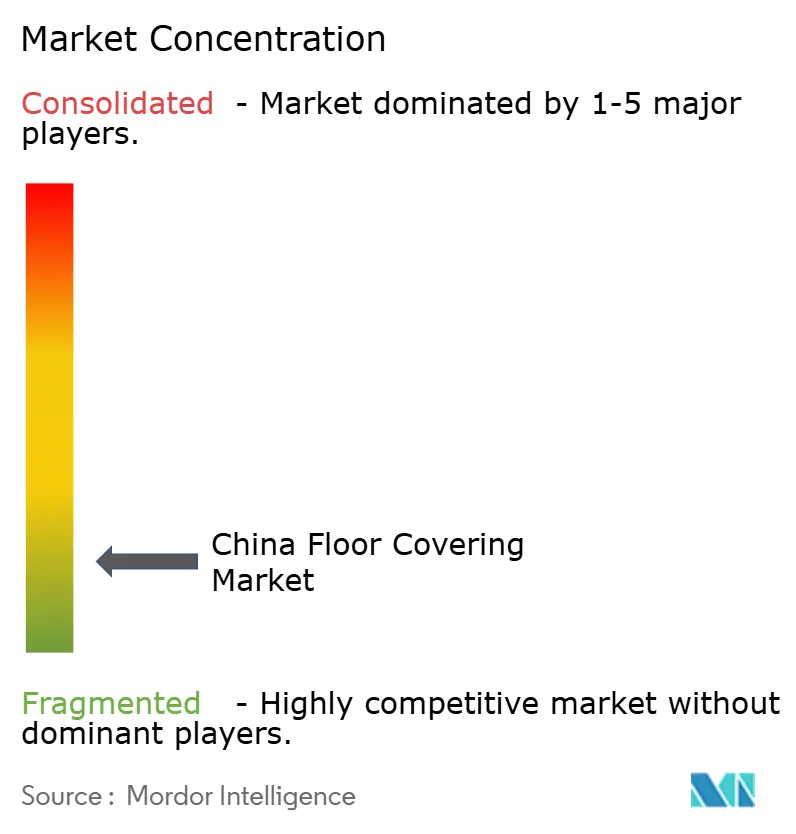

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Floor Covering Market Analysis by Mordor Intelligence

The China floor covering market size is expected to grow from USD 1.29 billion in 2025 to USD 1.36 billion in 2026 and is forecast to reach USD 1.79 billion by 2031 at 5.58% CAGR over 2026-2031. Market expansion aligns with the government’s urban renewal program, covering more than 60,000 projects and a total investment of CNY 2.9 trillion in 2024. Heightened residential standards effective May 2025 mandate 3-meter ceiling heights and stricter acoustic rules, prompting higher-specification flooring demand [1]Source: Government of China, “Residential Building Standards GB XXX-2024,” gov.cn. . Resilient products built on PVC-free technology record double-digit growth, helped by GB 18584-2024 limits on volatile organic compounds that take effect in July 2025. East China continues to anchor production and distribution, yet South-Central China leads incremental volume on the back of Guangdong’s CNY 9.2 trillion project pipeline for 2025. Meanwhile, 34% tariffs on Chinese luxury vinyl plank exports to the United States redirect capacity toward the domestic opportunity, pushing brands to accelerate omnichannel penetration and invest in low-carbon manufacturing footprints.

Key Report Takeaways

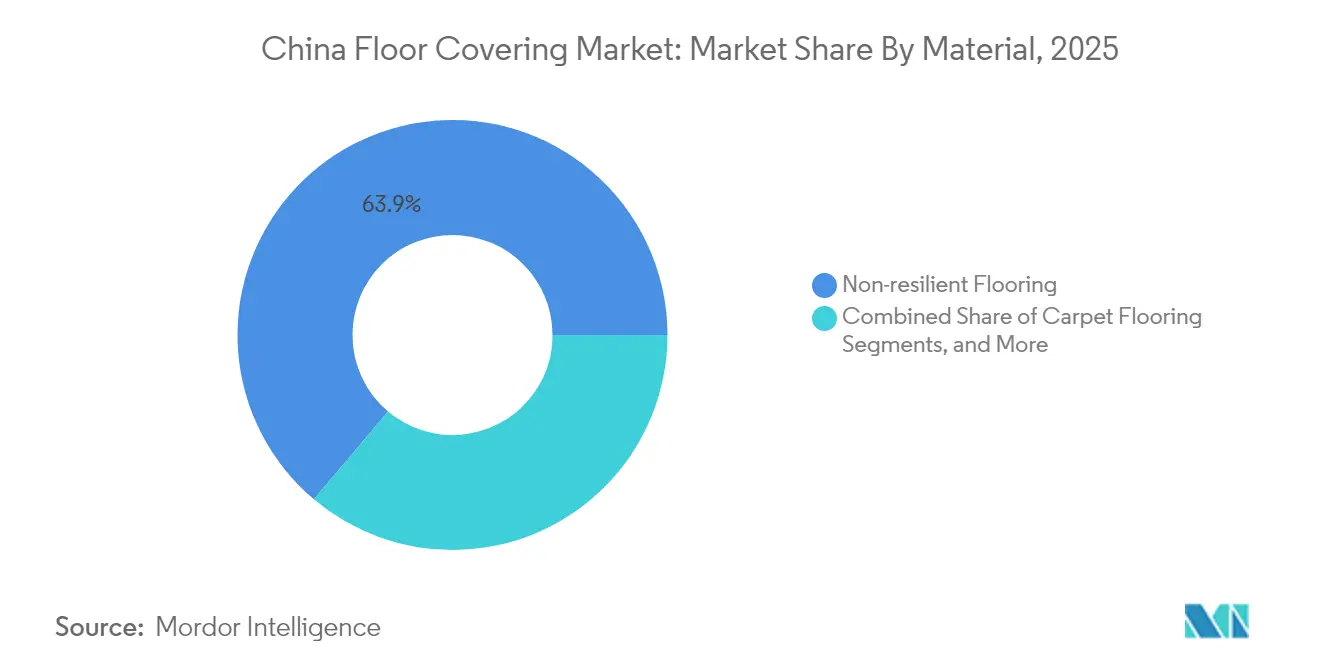

- By material, non-resilient flooring led with 63.85% revenue share in 2025, while resilient flooring is projected to register the fastest 9.85% CAGR to 2031 in the China floor covering market.

- By end use, residential applications held 55.95% share in 2025, whereas healthcare facilities are forecast to expand at the quickest 8.31% CAGR through 2031 in the China floor covering market.

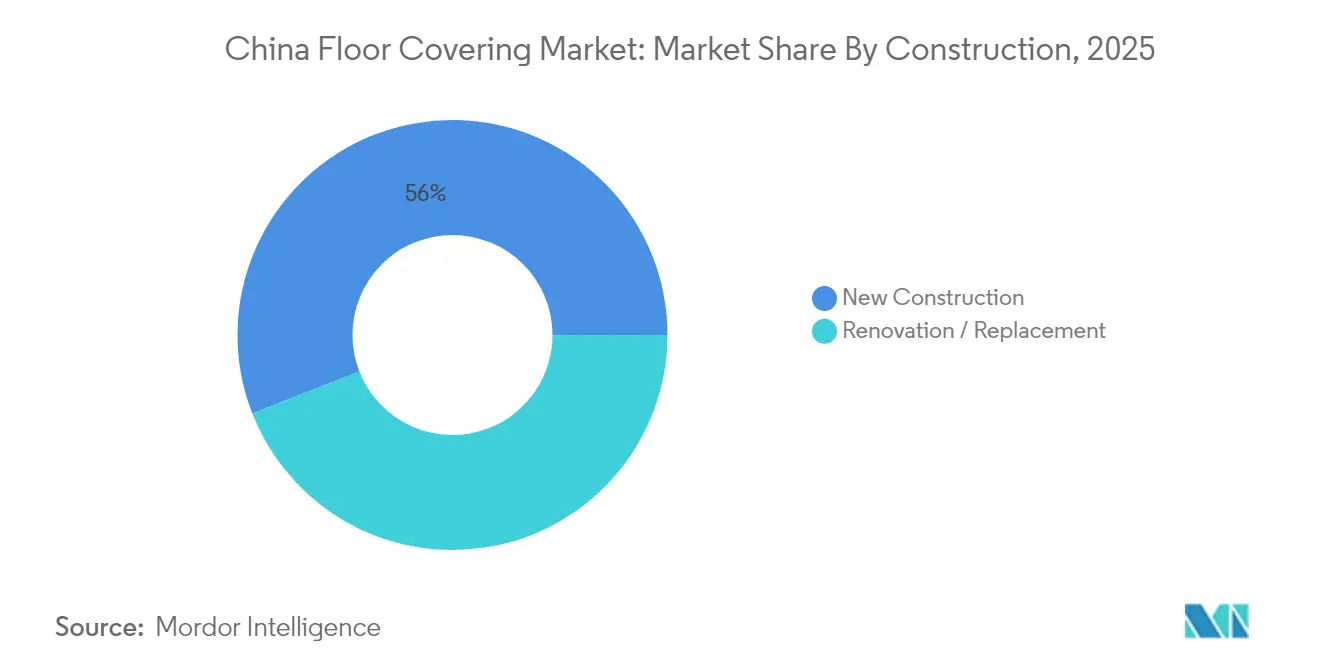

- By construction type, renovation captured a 44.05% share in 2025, yet new construction is poised for the highest 8.02% CAGR over the same period in the China floor covering market.

- By distribution channel, specialty stores dominated with 86.10% share in 2025, as online direct-to-consumer sales anticipate an 8.23% CAGR to 2031 in the China floor covering market.

- By region, East China seized 37.05% revenue share in 2025, while South-Central China is expected to post the sharpest 6.92% CAGR to 2031 in the China floor covering market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Floor Covering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urban renewal and affordable housing push | +1.8% | National, with concentration in tier-1 and tier-2 cities | Medium term (2-4 years) |

| Rising demand for green-certified buildings | +1.2% | East China and South-Central China leading adoption | Long term (≥ 4 years) |

| Growth of PVC-free resilient flooring technologies | +0.9% | Global with China manufacturing focus | Medium term (2-4 years) |

| E-commerce-enabled customized design services | +0.6% | National, with urban centers driving adoption | Short term (≤ 2 years) |

| Modular and prefabricated construction uptake | +0.5% | National, with tier-2 cities showing rapid adoption | Medium term (2-4 years) |

| Export pull from Belt-and-Road infrastructure | +0.4% | Global with focus on Southeast Asia and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urban Renewal and Affordable Housing Push

Continuous city-level renewal across 300 municipalities, backed by policy funding and the first-time “quality homes” pledge in the 2025 government work report, underpins demand for acoustically engineered and moisture-resistant surfaces [2]Source: National Development and Reform Commission, “2025 Urban Renewal and Affordable Housing Work Report,” ndrc.gov.cn. . National per-capita housing floor area surpasses 40 m², underscoring a substantial retrofit pool now shifting from basic price points to specification-driven orders.

Rising Demand for Green-Certified Buildings

Guangzhou’s Green Building Regulations mandate certified materials for all public projects, while GB 55037-2022 enhances fire-safety thresholds for commercial and residential structures [3]Source: Guangzhou Municipal People’s Government, “Green Building and Energy Efficiency Regulations,” gz.gov.cn. . These frameworks link certification status to preferential land-use ratios and loan terms, positioning low-VOC flooring as a compliance prerequisite for developers.

Growth of PVC-Free Resilient Flooring Technologies

Suppliers introduce magnesium oxide and bio-polymer cores that remove conventional PVC yet sustain dent resistance and waterproof performance. PureTech and SolidTech R series incorporate over 70% recycled feedstock, dovetailing with corporate carbon goals and upcoming VOC caps. Manufacturing partnerships with organizations like Plastic Bank demonstrate industry commitment to ocean plastic reduction while securing recycled material supply chains for next-generation flooring products

E-commerce-Enabled Customized Design Services

Visualisation tools embedded in marketplaces such as DHgate let buyers preview pattern, plank width, and color in real scale, compressing the specification cycle from weeks to hours. The system supports just-in-time manufacturing, thereby lowering inventory risk for both factory and customer.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile PVC, wood and petro-chemical feedstock prices | -1.4% | Global with China manufacturing concentration | Short term (≤ 2 years) |

| Stricter national VOC and carbon limits on flooring | -0.8% | National implementation with regional enforcement variations | Medium term (2-4 years) |

| EU-DR deforestation rules threatening wood exports | -0.5% | Europe-focused with global supply chain implications | Medium term (2-4 years) |

| Anti-dumping tariffs on Chinese vinyl and tile abroad | -0.7% | North America and Europe primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile PVC, Wood and Petro-Chemical Feedstock Prices

The March 2025 ban on U.S. log imports and resin price swings force multi-sourcing strategies and trigger producer price adjustments passed downstream within one quarter. Petrochemical feedstock fluctuations directly impact vinyl and synthetic flooring production costs, particularly affecting luxury vinyl tile manufacturing that relies on stable resin pricing for competitive positioning.

Stricter National VOC and Carbon Limits on Flooring

GB 18584-2024 formalizes emission caps effective July 2025, compelling investment in alternative binders, in-house test chambers, and longer product-approval lead times, thereby elevating compliance costs. Regional enforcement variations create compliance complexity for national distributors, while international suppliers face additional certification requirements that may limit market access for non-compliant products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Resilient Technologies Challenge Traditional Dominance

Non-resilient lines contributed 63.85% of China flooring market share in 2025. Ceramic, stone, and solid wood remain staples, yet resilient formats are accelerating at a 9.85% CAGR through 2031, closing the gap via rigid-core and SPC upgrades. The China flooring market continues to see rigid core adoption in high-rise residential projects because floating installation shortens project schedules. Pioneer magnesium-oxide cores address stricter fire codes, while PVC-free planks help builders achieve green certification benchmarks.

Manufacturers leverage digital inkjet printing for hyper-realistic textures that erode the aesthetic premium long enjoyed by parquet and marble. In parallel, ceramic producers win orders for heavy-traffic metro station concourses, capitalizing on large-format slabs that lower grout maintenance. The cross-learning across segments fosters hybrid innovations—stone-plastic composite tile that offers the look of porcelain and the thermal comfort of vinyl. Over the forecast span, resilience, recyclability, and quick-lay formats underpin the substitution trend.

By End Use: Healthcare Facilities Drive Premium Segment Expansion

Healthcare flooring logged an 8.31% CAGR, the fastest among end uses, as provincial health-commission budgets fund tier-2 and tier-3 hospital upgrades. The segment absorbs weld-seamless homogenous sheet and conductive vinyl designed to withstand daily disinfection cycles. In contrast, residential holds 55.95% share of China flooring market size, reflecting the magnitude of urban renewal. Developers of large-scale housing now differentiate via acoustic underlayment packages bundled at the presale stage. Commercial offices recover steadily; tenants prioritize low-VOC warranties and rapid replacement options compatible with raised-floor cabling.

Schools and universities align with smart-campus programs and prefer loose-lay formats that permit future tech retrofits without demolition debris. Logistics warehouses and e-commerce fulfillment centers demand high-compressive-strength rigid vinyl capable of tolerating autonomous mobile robot traffic.

By Construction: New Projects Accelerate Despite Renovation Dominance

Renovation controlled 44.05% China flooring market share in 2025 and remains the volume bedrock, yet new construction is forecast to outgrow at 8.02% CAGR to 2031. High-speed rail station pipelines in the Yangtze River Delta and Pearl River Delta spur contract wins for stone and porcelain tile. Parallel mixed-use developments capitalize on integrated design-build contracts that specify resilient floors meeting both retail and residential criteria. Renovation, meanwhile, benefits from provincial subsidies for old residential block upgrades, often requiring thin-profile, self-adhesive planks that avoid door re-trimming.

By Distribution Channel: Digital Transformation Challenges Traditional Retail

Specialty dealers own 86.10% share of channel sales owing to entrenched installer relationships and sample libraries. However, direct-to-consumer online portals are climbing at 8.23% CAGR as mobile apps offer visualization, AI-driven color matching, and one-click logistics. The shift forces showrooms to add AR kiosks and subscription-based design services. Manufacturers roll out last-mile installation certification programs to retain service standards within an omnichannel model.

Geography Analysis

East China anchored 37.05% revenue in 2025, supported by cluster efficiencies around Shanghai, Suzhou, and Ningbo ports that compress inbound raw-material lead times. The Yangtze River Delta intercity rail expansion to 16,700 km by 2025 forms one-to-three-hour economic circles, lifting demand for commercial renovation in satellite cities. Government pilot projects using low-carbon building codes in Suzhou further amplify resilient-flooring penetration.

South-Central China posts the highest 6.92% CAGR, propelled by Guangdong’s CNY 9.2 trillion project roster for 2025. The Shenzhen-Zhongshan Bridge, operational since June 2024, slashes cross-bay transit to under 30 minutes and unlocks industrial land for smart-factory campuses. Flooring suppliers gain via proximity to thriving electronics and appliance sectors that adopt anti-static vinyl in cleanroom extensions.

North China’s mix of public housing retrofits and winter-proof linoleum demand supports steady growth around Beijing-Tianjin rail corridors. Northeast China receives state-owned enterprise investment incentives, translating to hospital modernization and education infrastructure orders. Southwest and Northwest China benefit from Belt and Road logistics hubs; resilient floors tolerant to desert temperature swings gain traction in distribution centers near new freight rail terminals.

Competitive Landscape

Competition is moderate, with no single firm exceeding a double-digit share. Domestic groups such as Nature Home, Power Dekor, and Der International co-exist with multinational brands Mohawk, Tarkett, and LG. Firms diversify by setting up Vietnamese and Cambodian plants to hedge tariff exposure, as seen in CFL Flooring’s 750,000 ft² North Vietnam site scheduled for Q4 2025 start-up. Technology leadership centers on PVC-free chemistry, rigid-core durability, and AI-bus visualization. Sustainability credentials become the new battleground; Mohawk’s SolidTech R leverages reclaimed polymer streams and offers a lifetime waterproof warranty.

Omnichannel models integrate flagship digital storefronts with curated showrooms, while installers receive micro-learning modules on VOC compliance to ensure final-mile adherence. Market entry for premium healthcare grades remains attractive given rising hospital cap-ex and limited domestic formulation know-how. Conversely, mainstream residential sub-segments endure price pressure, pushing scale players to automate in-line digital printing and robotic stacking to curb unit costs.

China Floor Covering Industry Leaders

Nature Home

Der International

Power Dekor

Shanghai Cimic Tiles

CFL Flooring

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: CFL Flooring announced construction of a 750,000 ft² SPC and hybrid-flooring plant in North Vietnam, scheduled to begin operations in Q4 2025 and aimed at diversifying regional capacity

- February 2024: Mohawk Industries introduced PureTech technology, employing renewable polymer cores made with 70% recycled content to meet rising low-VOC and sustainability requirements

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the China floor covering market as all finished materials, carpet, resilient vinyl/LVT/SPC, and non-resilient wood, laminate, stone, and ceramic tile installed over a structural floor in residential or commercial buildings and priced to the first point of domestic sale. The value base is factory-gate or landed import price expressed in constant 2024 US dollars.

Scope note: temporary rugs, unfinished lumber planks, and raised access flooring are outside this assessment.

Segmentation Overview

- By Material

- Carpet Flooring

- Non-resilient Flooring

- Wood

- Laminate

- Stone

- Ceramic Floor and Wall Tile

- Resilient Flooring

- Vinyl Sheet

- Luxury Vinyl Tile (LVT)

- Stone-Plastic Composite (SPC)

- By End Use

- Residential

- Commercial

- Office

- Retail

- Hospitality

- Healthcare

- Institutional/Education

- Industrial and Logistics

- By Construction

- New Construction

- Renovation / Replacement

- By Distribution Channel

- Manufacturer-Owned Stores

- Speciality Stores

- Online Direct-to-Consumer

- Wholesale / Distributors

- By Region (China)

- East China

- South-Central China

- North China

- Northeast China

- Southwest China

- Northwest China

Detailed Research Methodology and Data Validation

Desk Research

We began by mapping demand fundamentals from tier-1 public sources such as the National Bureau of Statistics of China, General Administration of Customs, China Building Materials Federation, and China Construction Industry Association. Construction floor-space completions, building permit issuances, tile and PVC resin output, and import-export tonnage created the primary demand pool. To enrich company, price, and project intelligence, analysts sourced filings on D&B Hoovers, news archives on Dow Jones Factiva, patent cues from Questel, and trade journals like AsiaFloorGuide. Macro indicators, urban disposable income, mortgage approvals, and renovation subsidy allocations were tracked through the People's Bank of China and IMF data portals. The list above is illustrative; many additional open datasets and industry periodicals informed validation.

Primary Research

Structured interviews with architects, flooring installers, bulk distributors, and procurement heads across eight provinces helped us calibrate material mix, average selling prices, and installation share between newbuild and retrofit segments. Follow-up surveys with vinyl and ceramic producers tested supply utilization, margin trends, and export realignment, giving our team fresh viewpoints that desk sources could not offer.

Market-Sizing & Forecasting

A top-down build starts with gross floor-space put-in-place by end use; penetration rates for each material family convert area into volumes, which are then multiplied by weighted ASPs captured from price sheets and on-ground checks.

Supplier roll-ups and sampled channel invoices serve as bottom-up guardrails to reconcile totals.

Key variables feeding the model include: - Urban housing completions (million m2) - Average renovation cycle length (years) - Ceramic and PVC production indices - Provincial real-estate investment growth (%) - Import share of premium wood flooring (%)

A multivariate regression with ARIMA overlay forecasts each driver to 2030; scenario analysis adjusts for policy stimulus or commodity shocks.

Gaps in bottom-up evidence are bridged with regional proxies vetted during expert calls.

Data Validation & Update Cycle

Outputs pass two-stage variance checks against historical ratios and independent trade statistics before senior analyst sign-off. Reports refresh annually, and mid-cycle updates are triggered if material events shift any driver by +/-5 %.

Why Mordor's China Floor Covering Baseline Commands Confidence

Published estimates often diverge because firms apply different material scopes, convert currencies on disparate dates, or project using single-factor growth curves.

Key gap drivers identified: some studies fold soft furnishings and wall tiles into floor coverings, others extrapolate manufacturer shipment values without installation mark-ups, while a few assume uniform ASP escalation nationwide. Mordor's disciplined segmentation, dual price capture, and yearly driver refresh narrow such variances, giving decision-makers a balanced anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.29 B (2025) | Mordor Intelligence | - |

| USD 27.1 B (2024) | Global Consultancy A | Treats all flooring materials, includes wholesale margins, limited primary validation |

| USD 46.4 B (2023) | Trade Journal B | Aggregates construction spend proxies, excludes currency normalization, infrequent update cadence |

In sum, Mordor's model ties every yuan of flooring spend back to transparent area, price, and replacement-cycle assumptions that can be retraced and replicated by clients, ensuring dependable guidance for strategic planning.

Key Questions Answered in the Report

What is the current value of the China flooring market?

The China flooring market size stands at USD 1.36 billion in 2026.

How fast will the market grow?

It is forecast to advance at a 5.58% CAGR over 2026-2031, reaching USD 1.79 billion by 2031.

Which region is the fastest growing?

South-Central China is expected to post the highest 6.92% CAGR through 2031 thanks to Guangdong’s large infrastructure pipeline.

Why are PVC-free floors gaining traction?

Upcoming GB 18584-2024 emission caps and corporate sustainability targets favor PVC-free resilient flooring that meets low-VOC thresholds.

How are tariffs influencing the market?

The 34% U.S. tariff on Chinese luxury vinyl pushes manufacturers to pivot toward domestic sales and invest in overseas capacity to bypass duties.

Which segment is expanding quickest?

Healthcare facilities lead end-use growth with an 8.31% CAGR due to stringent hygiene and durability demands in new hospital projects.

Page last updated on: