Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

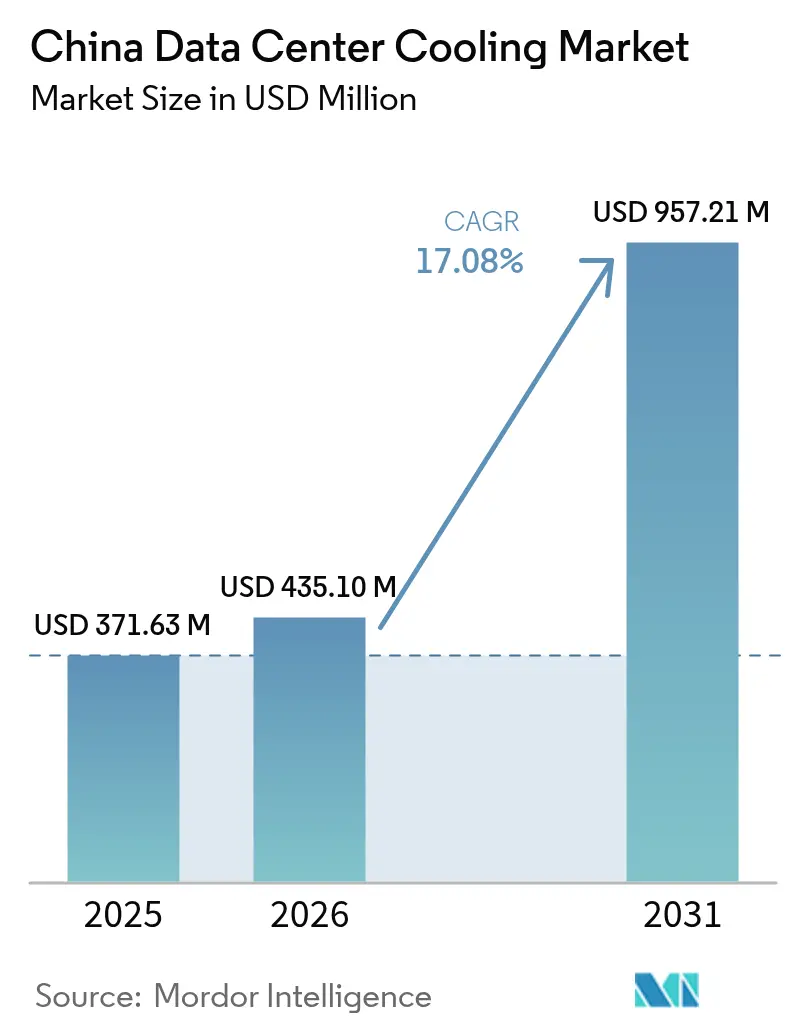

| Base Year Market Size (2025) | USD 371.63 Million |

| Market Size (2026) | USD 435.1 Million |

| Market Size (2031) | USD 957.21 Million |

| Growth Rate (2026 - 2031) | 17.08% CAGR |

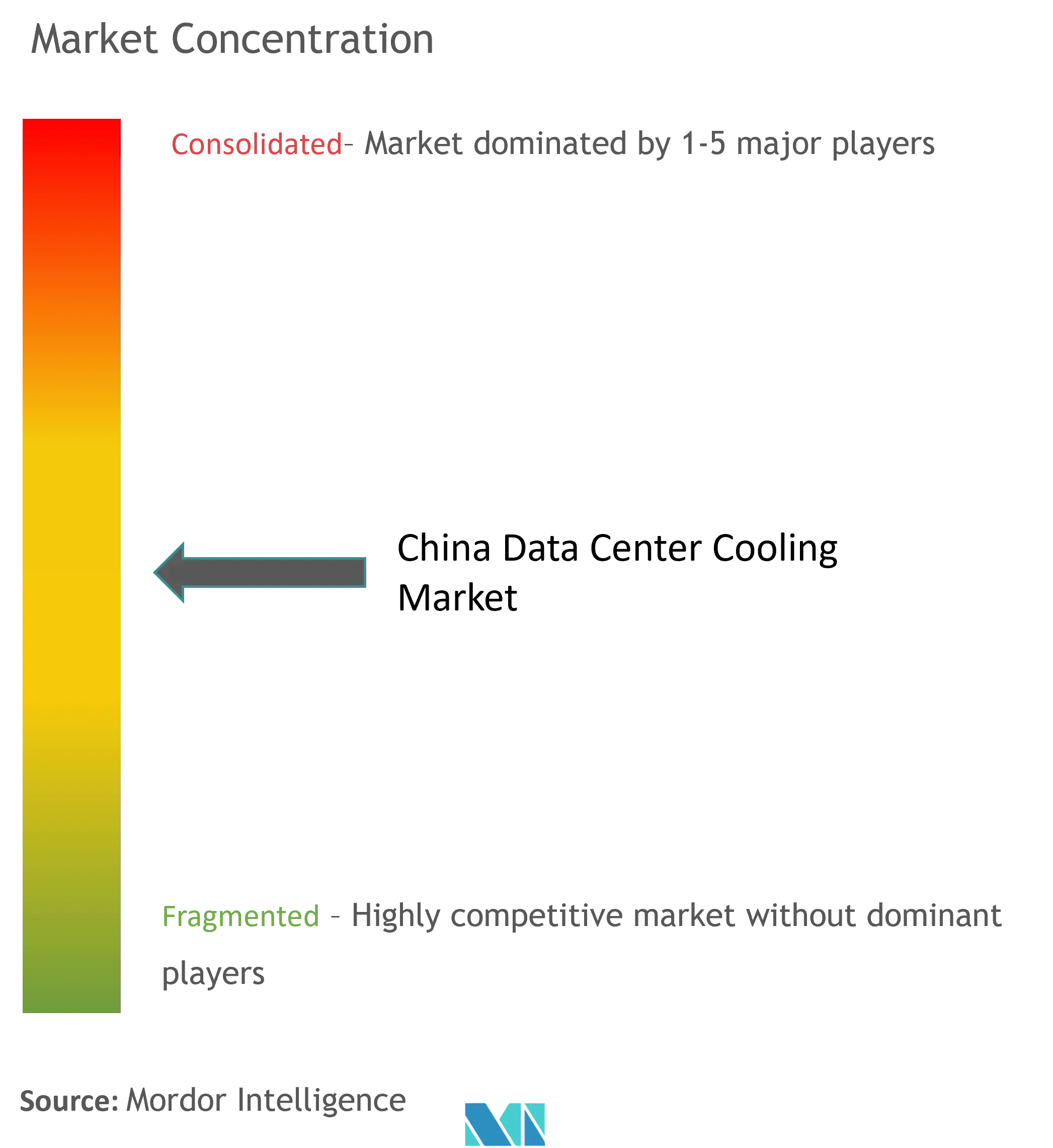

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Data Center Cooling Market Analysis by Mordor Intelligence

The China data center cooling market size is expected to grow from USD 371.63 million in 2025 to USD 435.1 million in 2026 and is forecast to reach USD 957.21 million by 2031 at 17.08% CAGR over 2026-2031. Mandatory Power Usage Effectiveness (PUE) caps, surging AI server rack densities that dissipate 6-8 times more heat than legacy workloads, and the government’s Eastern Data and Western Compute program are converging to accelerate capital outlays for liquid-based cooling. Operators are prioritizing technology that keeps PUE below 1.3 in Tier 1 cities, driving a pivot away from conventional air systems toward direct-to-chip, immersion, and rear-door liquid solutions. At the same time, water-stress regulations are pushing closed-loop designs that minimise consumption while maximising thermal efficiency. Although equipment sales still dominate spending, demand for specialised services is climbing fast as facility owners seek expertise to retrofit or green-field liquid deployments.

Key Report Takeaways

- By data center type, hyperscalers led with 46.02% of China data center cooling market share in 2025, while the segment is projected to expand at 17.62% CAGR through 2031.

- By tier type, Tier 3 facilities held 66.55% share of the China data center cooling market size in 2025; Tier 4 sites are forecast to grow the fastest at 18.83% CAGR to 2031.

- By cooling technology, air-based systems commanded 62.95% revenue share in 2025, whereas liquid-based solutions are advancing at an 17.92% CAGR through 2031.

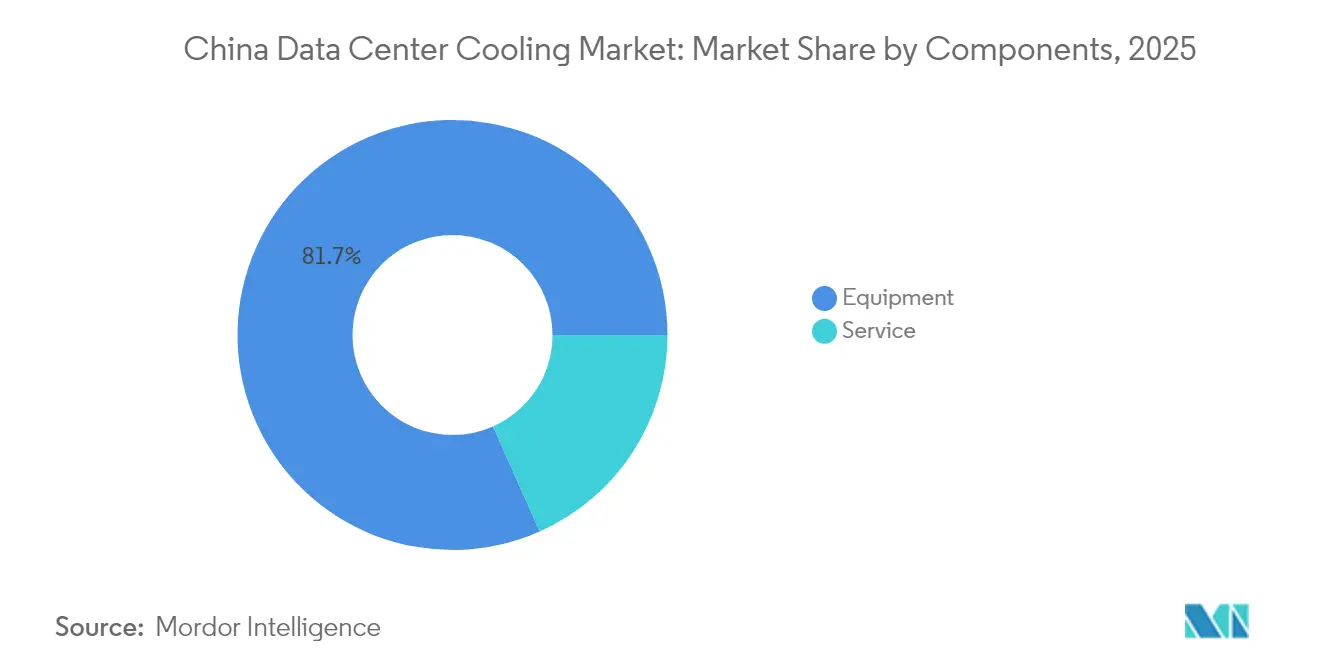

- By component, equipment accounted for 81.65% of the China data center cooling market size in 2025, while services are set to register an 18.21% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Data Center Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging hyperscale and AI-driven rack densities | +4.2% | National, concentrated in Beijing, Shanghai, Guangzhou | Short term (≤ 2 years) |

| Government-mandated PUE caps for new builds | +3.1% | National, strictest in Tier 1 cities | Medium term (2-4 years) |

| Rapid colocation expansion (+51.7% rack share YoY) | +2.8% | National, with early gains in Beijing, Shanghai, Shenzhen | Medium term (2-4 years) |

| Maturing liquid-cooling supply chain and local OEM scale-up | +2.3% | National, manufacturing hubs in Guangdong, Jiangsu | Long term (≥ 4 years) |

| Eastern Data and Western Compute programme exploiting cold-climate free-cooling zones | +1.9% | Western regions: Inner Mongolia, Xinjiang, Gansu | Long term (≥ 4 years) |

| Monetisation of server waste-heat into district-heating grids | +1.2% | Northern China: Beijing, Harbin, Hohhot | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging hyperscale and AI-driven rack densities

Modern AI cabinets consume 20-130 kW versus 5-10 kW for legacy servers, rendering air cooling insufficient and propelling mass adoption of liquid technologies. Huawei’s closed liquid-cooled cabinet cuts cooling power by 96% and lowers facility PUE to 1.1, proving viability at the hyperscale level.[1]Huawei Technologies, “Next-Generation Liquid-Cooled Cabinet Solution,” huawei.com National flagship AI compute clusters in Gui’an, Ulanqab, and Wuhu now specify liquid solutions at the build-out stage, underscoring a structural shift that places thermal design on par with chip performance in data-center planning.

Government-mandated PUE caps for new builds

Beijing’s 14th Five-Year plan requires all new data centers to operate below 1.5 PUE by 2025, while Shanghai tightens the threshold to 1.3. The 2023 Green Data Center standard expands compliance to water-consumption ratios and renewable-energy sourcing, cementing liquid cooling as the only practical route to meet efficiency targets at scale.[2] Ministry of Industry and Information Technology, “Guidelines for Data-Center Energy Efficiency,” gov.cn

Rapid colocation expansion

GDS Holdings booked a 17.7% YoY revenue increase to RMB 2.97 billion (USD 416 million) in Q3 2024, citing accelerated tenant migrations and multi-tenant AI clusters. Colocation providers leverage scale to amortise high-end liquid systems while offering differentiated cooling SLAs that attract hyperscaler tenants, reinforcing a virtuous cycle of density and efficiency gains.

Maturing liquid-cooling supply chain and local OEM scale-up

Chemours’ 2025 pact with Navin Fluorine localises production of Opteon two-phase fluids, mitigating tariff risk and lowering cost barriers for domestic adopters.[3]Chemours, “Chemours and Navin Fluorine to Produce Opteon™ Immersion Fluid in China,” chemours.com Parallel investments by firms such as Envicool and Yimikang are shortening lead times for pumps, manifolds, and heat exchangers, giving Chinese operators strategic autonomy in critical cooling components.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High electricity tariffs eroding TCO advantages | -2.1% | National, particularly acute in eastern coastal regions | Medium term (2-4 years) |

| Growing water-stress curbing evaporative-cooling permits | -1.8% | Northern and western China, Beijing-Tianjin-Hebei region | Long term (≥ 4 years) |

| Provincial power-quota caps delaying hyperscale projects | -1.5% | Eastern provinces: Jiangsu, Zhejiang, Guangdong | Short term (≤ 2 years) |

| Import dependency on fluorinated coolants facing tariff risk | -1.2% | National, supply chain concentrated in coastal ports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High electricity tariffs eroding TCO advantages

Data center power draw is expected to climb from 200 TWh in 2025 toward 400-600 TWh by 2030, with tariffs in Jiangsu and Zhejiang raising operating costs enough to negate savings from legacy equipment depreciation. The Eastern Data and Western Compute initiative counterbalances the burden by relocating load to renewable-rich provinces but requires operators to reconcile latency and fibre-backhaul constraints.

Growing water-stress curbing evaporative-cooling permits

Annual water demand from Chinese data centers could exceed 3 billion m³ by 2030, straining already dry river basins that host three-quarters of national rack capacity. Municipal authorities are therefore refusing new evaporative-tower permits and encouraging closed-loop or seawater solutions; China’s Hainan offshore data center demonstrates the shift, using natural seawater to cool high-density AI racks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Hyperscalers accelerate liquid upgrades

Hyperscalers accounted for 46.02% of 2025 revenue, and their contribution to the China data center cooling market size is forecast to expand at 17.62% CAGR through 2031. These firms build AI clusters that exceed 100 kW per rack, making liquid technology non-negotiable for thermal headroom and PUE compliance. Their scale also drives down per-rack cooling cost, creating a benchmark that enterprise and edge operators now emulate. Edge sites, however, favour compact rear-door heat exchangers due to space and maintenance limits. The hyperscaler wave ensures that liquid infrastructure will dominate new capacity additions, even though air systems retain a retrofit niche.

Colocation operators mirror this trajectory by bundling dedicated liquid zones as premium services, converting density into both margin and differentiated customer experience. Enterprise facilities lag on full immersion adoption but are piloting direct-to-chip loops to stretch existing chiller plants. Combined, these moves keep the China data center cooling market on a high-growth path as every operator segment advances toward AI-ready thermal architectures.

By Tier Type: Tier 4 construction gains share despite Tier 3 dominance

Tier 3 sites captured 66.55% of spending in 2025 thanks to their mature design frameworks and competitive balance of uptime vs. capex. Yet Tier 4 builds are growing at 18.83% CAGR because AI training workloads cannot afford even minutes of unplanned downtime. The China data center cooling market size for Tier 4 facilities will therefore rise swiftly as investors prioritise fault-tolerant, concurrently maintainable liquid systems that keep racks within 30 °C even during maintenance.

Tier 1 and Tier 2 footprints are steadily cannibalised as their power and cooling envelopes top out below 15 kW per rack. Meanwhile, Tier 3 specifications are being retrofitted with dual-loop liquid infrastructure so operators can satisfy new customer density requirements without a green-field Tier 4 budget. This tier evolution reinforces liquid technology as the baseline for any AI-centric build in China’s data center cooling market.

By Cooling Technology: Liquid systems close the gap on air incumbents

Air technologies still held 62.95% revenue share in 2025, but liquid methods are slated to capture the lion’s share of new capacity given their 17.92% CAGR forecast. Direct-to-chip loops remove up to 80% of server heat at the source, while immersion baths are driving PUE to near-1.0 levels in purpose-built AI pods. Rear-door heat exchangers, which require minimal floor reconfiguration, bridge legacy rooms into the liquid era and thus soften migration hurdles.

Within the remaining air segment, indirect evaporative and two-stage economisers maximise free-cooling hours in north-western provinces where annual mean temperatures stay below 10 °C. However, looming water-use limits underpin an inexorable shift toward sealed liquid circuits nationwide. Consequently, liquid adoption has become the central storyline shaping competitive dynamics and vendor R&D in the China data center cooling market.

By Component: Services boom alongside equipment leadership

Equipment purchases represented 81.65% of spend in 2025, reflecting the capital-intensive nature of chillers, CDUs, manifolds, and heat exchangers. As operators mature, however, services are climbing at an 18.21% CAGR, transforming the revenue mix. Consulting teams now blueprint fluid chemistry, fail-over logic, and future density headroom, while field engineers manage the precise commissioning that liquid networks demand.

Predictive maintenance contracts that utilise continuous coolant-quality monitoring and leak detection are becoming standard service upsells. Training programmes covering dielectric-fluid handling and emergency response have become mandatory for operating permits in Tier 1 cities. Together, these service layers lock in recurring revenue streams for vendors and reinforce customer reliance on specialised expertise, anchoring long-term growth within the China data center cooling market.

Geography Analysis

China’s cooling demand is undergoing a major east-to-west realignment. Ningxia, Gansu, and Inner Mongolia clusters leverage desert solar and sub-zero winters to achieve year-round free cooling, helping regional facilities post PUE readings near 1.2 without resorting to water-intensive towers. Inner Mongolia alone plans to triple rack counts to 720,000 by 2025, carving out a sizeable share of future China data center cooling market additions.

Nonetheless, Beijing, Shanghai, and Guangzhou still host the bulk of hyperscale footprint because of low-latency requirements. These cities suffer summer wet-bulb temperatures above 28 °C, forcing operators to adopt closed-loop liquid systems and invest in recycled water plants to respect municipal withdrawal caps. Shanghai’s sub-1.3 PUE mandate led multiple providers to retrofit direct-to-chip loops in 2024, pre-figuring a broader coastal transition that will amplify demand for advanced fluid technologies Tencent Cloud.

Coastal innovation continues with underwater data centers off Hainan, where seawater-based conduction cools AI racks processing 7,000 queries per second. Simultaneously, Tibet’s 3,600-metre-altitude facility in Lhasa exploits low ambient air to host disaster-recovery workloads for national banks. These geographic experiments underline the diversity of operating environments that vendors must address to win in the China data center cooling market.

Regulatory Landscape

China data center cooling requirements are being tightened through a mix of national policies led by MIIT, NDRC, the National Energy Administration, and the National Data Bureau, alongside a standards framework administered via SAMR/SAC. The Data Center Green Low-Carbon Development Special Action Plan (issued July 2024) prioritizes energy-saving retrofits and the adoption of high-efficiency equipment, which supports higher-density thermal designs aimed at lower PUE.

On the standards side, GB/T 44989-2024 (Evaluation for green data center) took effect on June 1, 2025, tying green evaluation to energy and resource performance and pushing operators toward higher-efficiency cooling architectures. In 2025, additional national standards were issued with 2026 implementation milestones, including GB/T 45837-2025 (issued June 30, 2025; implemented January 1, 2026) for comprehensive energy utilization evaluation and GB/T 46662-2025 (issued October 31, 2025; implemented May 1, 2026) for dynamic energy-efficiency measurement of IT systems. Together, these requirements shift attention from static facility metrics toward workload-aware efficiency measurement, which raises the value of monitoring, controls, and commissioning services alongside equipment.

Value Chain Analysis

The China data center cooling value chain runs from upstream materials and components (metals and alloys, electrical connectors, pumps, heat exchangers, valves, sensors, and controls) to midstream equipment and subsystem manufacturing (chillers, CRAH/CRAC, cooling towers where permitted, CDUs, manifolds, cold plates, rear-door heat exchangers, and dielectric fluids). Downstream, it extends into integration, commissioning, and lifecycle services delivered to hyperscalers, colocation providers, and enterprise/edge operators. China’s green data center push and AI-ready facility requirements are accelerating the shift toward integrated liquid-cooling stacks, where suppliers bundle CDUs, fluid distribution, intelligent controls, and monitoring to address PUE and water constraints.

Recent supply-side moves also point to deeper localization and vertical integration. Midea Group began construction of a Shunde liquid-cooling smart manufacturing base with investment exceeding RMB 1 billion (announced March 2026), targeting scaled production of chillers and CDUs. System integrators such as Shuguang Data Solutions are productizing MW-level phase-change immersion infrastructure (C8000 V3.0 launched April 2026). Standards are further shaping interoperability and acceptance across the chain, including YD/T 6358-2025 (Technical Requirements for Cold Plate Liquid Cooling Data Centers, implemented August 1, 2025) and GB/T 44989-2024 for green data center evaluation. These standards raise requirements for measurement, validation, and documentation, which expands demand for testing, commissioning, and maintenance service providers.

Competitive Landscape

Competition is intensifying as global incumbents clash with agile domestic challengers. Vertiv and Schneider Electric leverage long-standing channel networks, yet Chinese firms such as Huawei, Envicool, and Yimikang are closing technology gaps and winning on localisation, shorter lead times, and cost advantages. Schneider’s 2025 reference designs with NVIDIA that scale to 132 kW per rack illustrate how established brands are sharpening their AI value proposition.

Huawei’s liquid-cooled cabinet platforms show domestic R&D parity—achieving 1.1 PUE while slashing cooling power 96%—thereby redefining performance benchmarks. Envicool’s modular CDU lines, produced entirely in Guangdong, reduce delivery cycles to under four weeks for local customers, a speed advantage few foreign rivals can match. Meanwhile, Chemours’ immersion-fluid localisation deal signals multinationals’ willingness to partner rather than only export into the China data center cooling market.

China Data Center Cooling Industry Leaders

Schneider Electric SE

Johnson Controls International plc

GIGA-BYTE Technology Co. Ltd.

Vertiv Group Corp.

Carrier Global Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

An opportunity is forming around AI-oriented, high-density facilities that pair renewable power sourcing with advanced liquid cooling, supported by projects and programs connected to China’s east-to-west compute redistribution. In June 2026, China Telecom’s Ningxia branch launched an AI data center in Zhongwei, Ningxia, using wind-powered liquid-cooling technology and reporting PUE of 1.15. The announcement reinforces liquid-cooled architectures in energy-rich western provinces aligned with Eastern Data and Western Compute objectives.

A second whitespace is specialized cooling formats for constrained coastal environments, where efficiency needs overlap with water limits. This includes seawater-based and underwater concepts, along with sealed-loop liquid designs. In July 2026, HiCloud Technology commenced full commercial operations of a 24 MW offshore wind-powered underwater data center off the coast of Shanghai, using seawater for passive cooling and reporting PUE below 1.15. The project broadens the set of cooling reference architectures beyond conventional chiller and economizer plants. At the same time, tightening evaluation and measurement standards (for example, GB/T 44989-2024 for green data center evaluation, plus 2026-effective GB/T 45837-2025 and GB/T 46662-2025) increases demand for monitoring, validation, and service capability around dynamic efficiency, coolant management, and commissioning, especially for operators retrofitting Tier 3 footprints with direct-to-chip and rear-door liquid systems.

Recent Industry Developments

- June 2026: Schneider Electric unveiled a thermal management solutions innovation laboratory in Shanghai Zhangjiang focused on validating cooling approaches for high-density computing. The local test capability supports faster adaptation of liquid and hybrid cooling designs to China-specific PUE and deployment requirements, tightening the timeline for new reference architectures in the market.

- May 2026: Vertiv completed the acquisition of centrifugal chiller technology and related assets from BiXin Energy Technology Co. (BSE). The deal expands Vertiv’s chiller portfolio depth for data center applications and improves its ability to supply integrated thermal systems spanning both air-based and liquid-assisted configurations for AI-era loads.

- November 2024: GB/T 44989-2024, the national standard for green data center evaluation, was issued and later implemented from June 1, 2025. The standard raised the compliance baseline for energy and resource performance, supporting procurement of higher-efficiency cooling equipment and increasing the importance of measurable performance during commissioning and operations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the China data center cooling market covers the equipment, fluids, and related services used to remove heat from IT rooms and data halls in operating data centers, including air-based and liquid-based cooling used in new builds and retrofits.

Scope exclusions: We exclude portable spot coolers, building-wide HVAC that is not dedicated to IT spaces, and standalone aftermarket spare-parts sales.

Segmentation Overview

- By Data Center Type

- Hyperscalers (owned and Leased)

- Enterprise and Edge

- Colocation

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Cooling Technology

- Air-based Cooling

- Chiller and Economizer (DX Systems)

- CRAH

- Cooling Tower (covers direct, indirect and two-stage cooling)

- Others

- Liquid-based Cooling

- Immersion Cooling

- Direct-to-Chip Cooling

- Rear-Door Heat Exchanger

- Air-based Cooling

- By Component

- By Service

- Consulting and Training

- Installation and Deployment

- Maintenance and Support

- By Equipment

- By Service

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started by grounding the China-only market in public indicators that can be checked year over year, and then layering in commercial signals for cooling equipment and services. Public and official sources such as MIIT releases on data infrastructure, China Academy of Information and Communications Technology publications, National Bureau of Statistics energy and industrial series, China customs import and export statistics for relevant equipment categories, and International Energy Agency electricity data were used to anchor demand context.

We then reviewed company filings, investor presentations, and guidance from association and standards bodies such as ASHRAE and ISO, plus reputable press coverage on new data hall builds, rack density shifts, and liquid cooling deployments. A paid subscription focused on company financials and another subscription covering patent databases were used selectively to validate revenue exposure and technology direction for cooling solutions. The examples above are illustrative only, and many other public datasets and documents were also referenced for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work was used to test the assumptions that drive value the most in the China cooling spend model, including the pace of liquid-based cooling adoption, how pricing changes as rack density rises, and how much of total spend sits in equipment versus services for commissioning and retrofits. We spoke with a mix of data center operators, engineering and contracting teams, component suppliers, and maintenance providers across major China demand clusters so gaps from public information could be filled, then aligned back to the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 15% | |

| Mid tier: 45% | Functional/Unit leaders: 34% | |

| Smaller Players: 19% | Managers: 51% |

Market-Sizing & Forecasting

The core model uses top-down and bottom-up logic together, but it is anchored in a top-down reconstruction of cooling demand from China data center build and operations signals. We translated capacity additions and operating load proxies into a cooling demand pool, then applied realistic cooling architecture mixes to convert that pool into spend.

Key inputs that shaped sizing included the pace of new data hall commissioning, average rack density shifts that change the air-to-liquid mix, target PUE and cooling efficiency improvements, replacement cycles for major cooling assets, and typical services intensity for design, commissioning, and retrofit work. When public data did not separate IT-room cooling from general facility HVAC clearly, allocation factors were set using expert feedback so cooling totals stayed tied to IT heat removal.

For forecasting, scenario analysis was used so adoption curves for liquid cooling, containment, and economization could be tested without overfitting. The scenarios were anchored to interview-validated variables such as planned high-density deployments, expected pricing progression for liquid loops and coolant distribution units, and the timing of build-outs in key hubs.

Data Validation & Update Cycle

Validation was done in layers so the final totals did not depend on one assumption. We compared the modeled outcome with independent signals such as observed capacity additions, shifts toward higher-density computing, and reasonable cooling spend intensity per capacity band, then reviewed anomalies before sign-off.

If variance appeared in inputs like liquid cooling penetration or service attach rates, relevant respondents were re-contacted and assumptions were re-checked against newer public signals. Reports refresh annually, with interim updates when material events can move build activity, pricing, or deployment choices. Before delivery, a final analyst pass is completed so clients receive the latest updated view.

Mordor Intelligence's China Data Center Cooling Market Size Compared Against Other Published Estimates

Published market values for China data center cooling do not always match because what gets counted can shift even when the topic name looks identical. Differences usually come from whether the number includes services, how liquid cooling is treated, and how closely the definition sticks to IT heat removal rather than broader building cooling spend.

Evidence from capacity additions, rack density transition signals, and primary checks on cooling system mix keeps Mordor Intelligence's value tied to dedicated data hall cooling equipment, fluids, and supporting services, instead of blending in broader facility HVAC categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 371.63 M (2025) | |

| Industry Publisher A | USD 1.36 B (2025) | Uses a wider definition of cooling solutions that appears to include more facility mechanical scope beyond IT-room dedicated cooling, which increases the total versus an IT heat removal definition, and it also groups equipment under broader solution buckets. |

| Research Distributor B | USD 830.39 M (2030) | Reports a later-year value, so it is not directly comparable to a 2025 market size, and the uplift also depends on assumed multi-year adoption and pricing progression for liquid cooling and related services. |

The spread across sources is mainly driven by scope alignment and time alignment rather than arithmetic. When the market is kept China-only, centered on dedicated cooling for IT equipment, and tied back to capacity and density indicators, the final number becomes easier to replicate and update consistently.

Key Questions Answered in the Report

What is the current size of the China data center cooling market and how fast is it growing?

The market stands at USD 435.1 million in 2026 and is projected to climb to USD 957.21 million by 2031, reflecting a 17.08% CAGR over the forecast period.

Why are operators in China shifting from air-based to liquid-based cooling?

AI server cabinets now dissipate 6-8 times more heat than traditional workloads, pushing PUE targets below 1.3 in Tier 1 cities; liquid cooling handles these thermal loads far more efficiently than legacy air systems.

Which data-center segment is expanding the fastest?

Tier 4 facilities are growing at a 18.83% CAGR because fault-tolerant designs and liquid systems are essential for uninterrupted AI training workloads that can exceed 100 kW per rack.

What regional trend is reshaping demand for cooling solutions?

The Eastern Data and Western Compute program is relocating capacity to cooler, renewable-rich western provinces such as Ningxia and Inner Mongolia, where free-cooling hours are abundant and liquid systems can operate at even higher efficiency.

Page last updated on: