China Continuous Glucose Monitoring Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

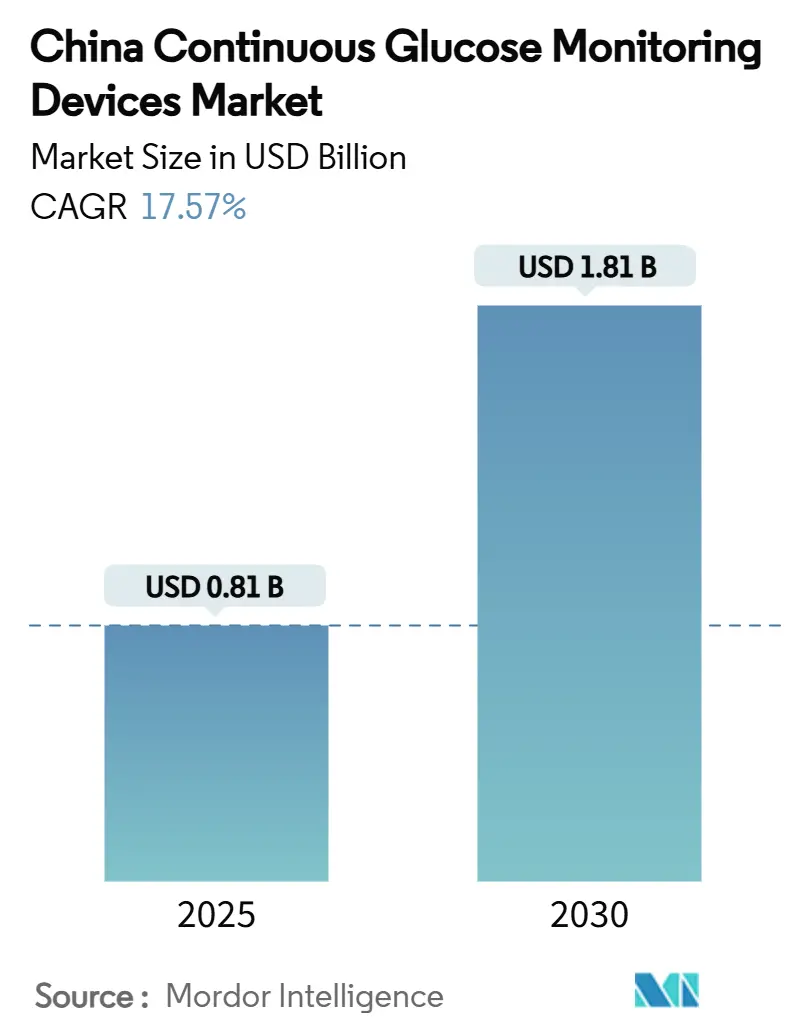

| Market Size (2025) | USD 0.81 Billion |

| Market Size (2030) | USD 1.81 Billion |

| Growth Rate (2025 - 2030) | 17.57% CAGR |

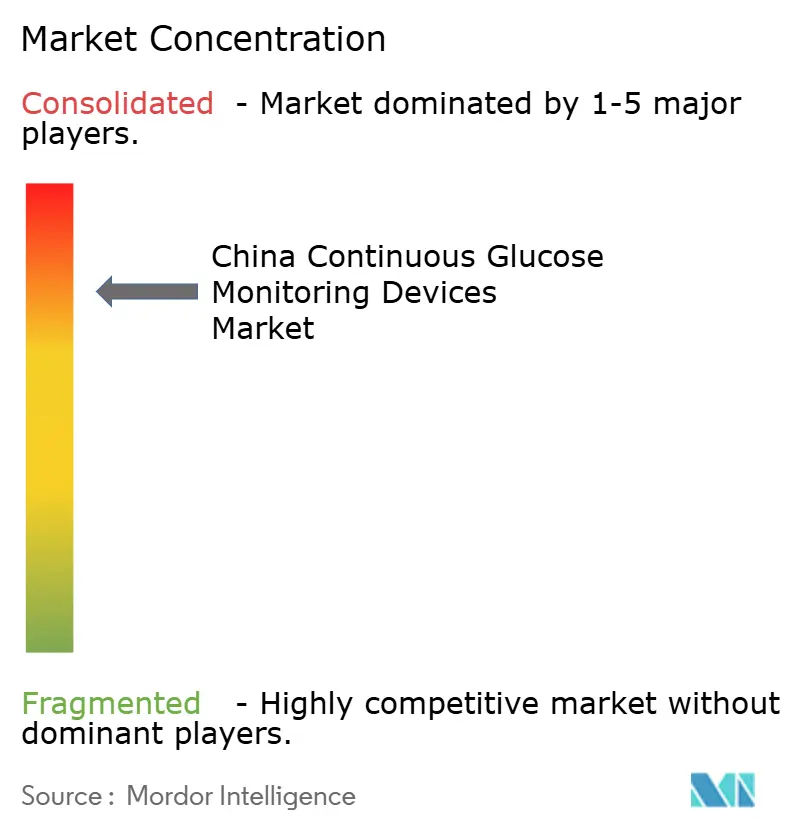

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Continuous Glucose Monitoring Devices Market Analysis by Mordor Intelligence

The China continuous glucose monitoring devices market size stands at USD 806.76 million in 2025 and is forecast to reach USD 1,812.27 million by 2030, advancing at a 17.57% CAGR. This trajectory rests on the confluence of a soaring diabetes burden, policy-backed price rationalization, sensor miniaturization, and widespread uptake of smartphone-enabled health platforms. Provincial volume-based procurement (VBP) continues to shrink device prices, while extended-wear sensors and non-invasive prototypes raise adoption among both clinical and wellness users. Foreign incumbents leverage ecosystem partnerships to defend their share, whereas cost-competitive domestic innovators aim to penetrate value-conscious rural segments. In parallel, the regulatory fast-track for “innovative devices” accelerates time-to-market, giving China's continuous glucose monitoring devices market a clear runway for double-digit expansion.

Key Report Takeaways

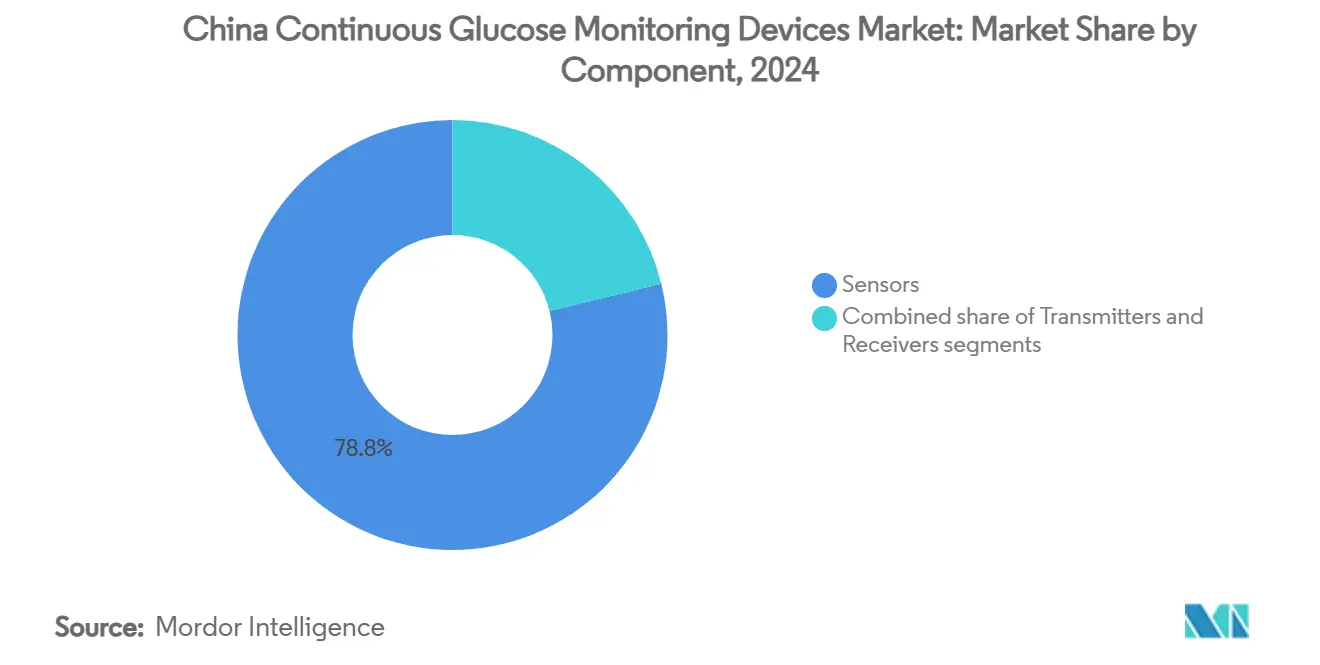

- By component, sensors commanded 78.84% of the China continuous glucose monitoring devices market share in 2024.

- Transmitters and receivers are projected to post an 11.79% CAGR through 2030, the slowest growth among components.

- Home and personal use captured 67.92% revenue in 2024, while hospital and clinic settings are projected to log the fastest 19.27% CAGR to 2030.

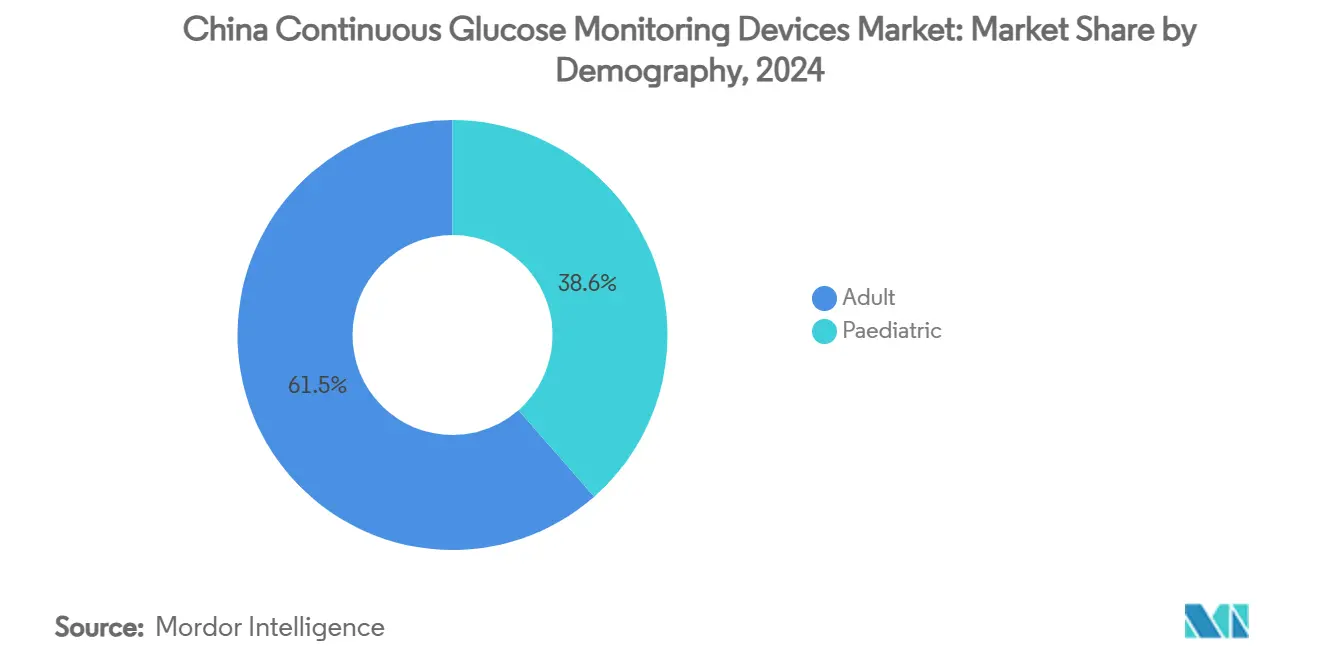

- Adult users contributed 61.45% to 2024 revenue, whereas the pediatric cohort is forecast to climb at 19.61% CAGR, the highest among demographic groups.

China Continuous Glucose Monitoring Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Rise In Diabetes Prevalence | 4.20% | National; highest in Beijing, Tianjin, Shanghai | Long term (≥ 4 years) |

| Technological Miniaturisation and Extended-Wear Sensors | 3.80% | National; early adoption in tier-1 cities | Medium term (2-4 years) |

| Lifestyle-Wellness Adoption Beyond Diabetics | 2.10% | Urban centers; expanding to tier-2 cities | Medium term (2-4 years) |

| Provincial Volume-Based Procurement (VBP) Price Resets | 1.90% | National; provincial implementation variations | Short term (≤ 2 years) |

| Domestic AI-Powered Non-Invasive R&D Clusters | 2.30% | Beijing, Shanghai, Shenzhen innovation hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Rise in Diabetes Prevalence

China documented 233 million adults with diabetes in 2023, equal to 15.88% of the adult population. Urban hubs, including Beijing, Tianjin, and Shanghai, have breached 20% prevalence, intensifying demand for real-time glycemic surveillance[1]Yiming Chen, “Urban Diabetes Prevalence Trends,” Military Medical Research, bmc.org. Government models warn that untreated diabetes could cost USD 460 billion by 2030, positioning CGM as a cost-containment lever. Ageing demographics add further strain, with type 2 cases climbing from 98 million in 2013 to 125 million in 2023 and tracking toward 127 million in 2024. These dynamics ensure sustained volume expansion for the China continuous glucose monitoring devices market.

Technological Miniaturization and Extended-Wear Sensors

University-led prototypes have produced coin-sized organic electrochemical transistor sensors matching Dexcom G6 accuracy, underscoring domestic engineering prowess. The Glunovo real-time system posted an 8.89% mean absolute relative difference (MARD) in multicenter trials, surpassing flash monitoring comparators. Engineers focus on 14-day wear cycles that lower patient burden and boost adherence. Non-invasive Raman spectroscopy platforms have achieved 14.6% MARD without personalized calibration, signaling disruptive potential. Collectively, these breakthroughs anchor China’s ascent as an affordable CGM manufacturing base.

Lifestyle-Wellness Adoption Beyond Diabetics

A three-year national weight-management plan targets metabolic health after projecting that 70.5% of adults will be overweight or obese by 2030[2]Shu Zhang, “Adult Obesity Forecasts,” NutraIngredients-Asia, nutraingredients-asia.com. Abbott’s China strategy markets CGMs for general wellness, pitching real-time glucose insights to fitness-minded consumers. Smartphone-synced wearables now relay glucose trends for diet and exercise optimization, widening the addressable pool far beyond diagnosed diabetics. Government “Three Reductions and Three Health” messaging further links sugar moderation with continuous monitoring, fostering mainstream acceptance.

Provincial Volume-Based Procurement (VBP) Price Resets

National VBP drove a 42% median price decline for insulin, setting a precedent that medical device tenders quickly emulate. Provinces that finalize CGM tender rounds grant instant formulary preference, accelerating penetration where reimbursement hurdles once prevailed. The reform rewards manufacturers that couple quality with cost agility, nudging the China continuous glucose monitoring devices market toward broader access without sacrificing margins for efficient players.

Domestic AI-Powered Non-Invasive R&D Clusters

Federated-learning algorithms reached root-mean-square errors of 19.1 mg/dL with 99.31% clinical acceptability, all while preserving data privacy. Innovation hubs in Beijing, Shanghai, and Shenzhen blend university research with technology-firm capital to refine photoplethysmography and spectroscopy solutions. The National Medical Products Administration (NMPA) offers accelerated reviews for devices addressing urgent clinical needs, shortening the path from lab to bedside. Local AI breakthroughs reduce dependence on foreign algorithms and meet domestic data-sovereignty rules.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-Of-Pocket Cost Versus SMBG | -2.8% | National; stronger in rural areas | Short term (≤ 2 years) |

| Limited CGM Awareness In Primary-Care Tier | -1.7% | Rural and tier-3 cities | Medium term (2-4 years) |

| GLP-1 Drug Boom Reducing Glucose Testing Frequency | -2.2% | Urban centers with higher GLP-1 adoption | Medium term (2-4 years) |

| Data-Privacy Compliance Burden For Cloud Platforms | -1.4% | National; affecting international providers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Cost Versus SMBG

Despite falling tender prices, CGM remains costlier than finger-stick systems, with patients paying 49% of innovative-device costs in 2023. Commercial insurance covers only 7.7% of CGM expenses, and rural capitation models often discourage higher-ticket technologies even when clinically justified. Point-of-care HbA1c testing costs USD 185.10 per quality-adjusted life year in rural trials, underscoring acute price sensitivity. Until broader reimbursement arrives, affordability curbs the China continuous glucose monitoring devices market’s rural reach.

Limited CGM Awareness in Primary-Care Tier

Primary-care physicians in tier-3 cities and rural townships prioritize acute symptom treatment over preventive monitoring, leaving CGM under-prescribed. Training deficits and scarce demonstration units impede clinical confidence. Provincial medical alliances have begun deploying tele-education modules, yet broad-based literacy remains a multi-year endeavor. As VBP lowers prices, parallel clinician education must progress to convert demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Sensors Drive Innovation Leadership

Sensors represented USD 636.4 million of 2024 revenue, or 78.84% of the China continuous glucose monitoring devices market. Backing that dominance, the segment is projected to register an 18.87% CAGR to 2030, outpacing the overall China continuous glucose monitoring devices market size growth. Bench-top accuracy leaps—such as Glunovo’s 8.89% MARD—are turning sensors into the prime competitive battlefield. Domestic labs advance organic electrochemical transistor designs that lower bill-of-materials cost, boosting export potential while consolidating local price-performance leadership.

Transmitters and receivers accounted for USD 147 million in 2024, equal to 21.16% of the China continuous glucose monitoring devices market share. As Bluetooth and smartphone integration absorb receiver functionality, unit growth slows to an 11.79% CAGR. Over time, back-end software scalability rather than hardware shipments will drive revenue. Combined, these shifts reposition sensors as the chief value generator, reshaping procurement negotiations and product-development pipelines.

By End User: Home Adoption Accelerates Digital Health

Home and personal settings have 67.92% of the market share in China continuous glucose monitoring devices industry. The segment is forecast to climb at 18.14% CAGR, powered by app-linked self-management culture. Digital health platforms effectively improved fasting glucose by 1.68% and HbA1c by 0.45% points in controlled studies[3]Wang, “Digital Diabetes Management via Digital Platforms,” BMC Health Services Research, bmchealthservres.biomedcentral.com. Consumers prioritize discreet, needle-free wearables and pay for continuous metabolic insights, making home use the anchor of volume scalability.

Hospitals and clinics have a 32.08% share, yet they will outpace at a 19.27% CAGR by 2030. Inpatient glycemic management protocols and ER triage increasingly require real-time monitoring, placing CGM on formularies. Government capitation models reward standardized care, prompting institutional bulk purchases that amplify China's continuous glucose monitoring devices market share for clinical channels.

By Demography: Pediatric Segment Shows Highest Growth Potential

Adults generated 61.45% of 2024 turnover and track a 17.79% CAGR aligned with escalating type 2 diabetes prevalence. Early diagnosis initiatives target working-age populations, cementing adult demand for daily trend graphs and insulin-dose calculators.

Pediatrics has a 38.55% market share, but the cohort leads with a 19.61% CAGR through 2030. Type 1 diabetes management and parental safety concerns underpin uptake. Sensor designs now feature hypoallergenic adhesives and flexible substrates, boosting wear compliance during sports and school activities as prevalence spreads into younger age brackets, lifetime user value expands, creating a durable revenue pillar for the China continuous glucose monitoring devices market.

Geography Analysis

Beijing, Tianjin, and Shanghai, where prevalence tops 20%, generated a significant portion of the 2024 revenue for the China continuous glucose monitoring devices market. High insurance penetration and specialist density fuel willingness to adopt premium CGM services. NMPA’s 2023 issuance of 12,213 medical-device approvals ensures new entrants can quickly access these urban centers, holding demand velocity steady.

Coastal provinces such as Guangdong, Zhejiang, and Jiangsu are also key regions for the market, propelled by manufacturing clusters and employer-sponsored insurance schemes. Regional AI hubs in Shenzhen and Hangzhou expedite pilot deployments of non-invasive prototypes, giving local patient populations early exposure to next-gen devices. Provincial governments align Healthy China 2030 targets with diabetes screening drives, looping CGM into chronic-disease toolkits.

Rural community health centers integrate CGM readings into electronic medical record rollouts, improving continuity of care. However, patient co-payment rates stay high, muting penetration. Remote-monitoring programs funded by poverty-alleviation budgets are beginning to close that gap, signaling a multiyear climb toward equitable access across all Chinese geographies.

Competitive Landscape

The China continuous glucose monitoring devices market features a moderate concentration of global titans Abbott and Dexcom, and agile domestic peers Medtrum, Zhejiang POCTech, and MicroTech Medical. Abbott shifted its China strategy in January 2025, pledging a pipeline of localized sensor SKUs to sidestep currency headwinds and meet VBP price ceilings. Dexcom invests in bilingual app interfaces and hospital data-integration modules to cement specialist loyalty.

Domestic innovators wield cost advantages. Medtrum’s patch pumps and CGMs bundle into hybrid closed-loop kits, while POCTech’s distributed manufacturing cuts lead times to provincial tenders. MicroTech Medical leverages Beijing-funded AI labs to refine non-invasive spectroscopy, positioning for first-mover status once accuracy thresholds clear regulatory bars. Domestic telecom giants furnish 5G data backbones, integrating CGM with tele-consultation and cloud analytics to sustain elevated switching costs for installed user bases.

China Continuous Glucose Monitoring Devices Industry Leaders

Abbott Laboratories

Medtronic plc

Dexcom Inc.

A. Menarini Diagnostics S.r.l.

MicroTech Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Abbott announced a strategic focus on glucose-monitoring products, unveiling new sensor lines tailored to VBP pricing brackets.

- September 2024: A consortium of Chinese universities disclosed a coin-sized organic electrochemical transistor CGM sensor equaling Dexcom G6 performance, signaling home-grown miniaturization capabilities.

- June 2024: The National Medical Products Administration issued revised registration provisions that streamline CGM dossier reviews and define fast-track criteria for breakthrough devices.

China Continuous Glucose Monitoring Devices Market Report Scope

Continuous glucose monitoring devices are used to diagnose both hyperglycemic and hypoglycemic conditions in diabetic patients throughout the day. The Chinese continuous glucose monitoring device market is segmented into components (sensors and durables).

The report offers the value (in USD) and volume (in units) for the above segments.

| Sensors |

| Transmitters |

| Receivers |

| Hospitals / Clinics |

| Home / Personal |

| Adult |

| Pediatric |

| By Component | Sensors |

| Transmitters | |

| Receivers | |

| By End User | Hospitals / Clinics |

| Home / Personal | |

| By Demography | Adult |

| Pediatric |

Key Questions Answered in the Report

What growth rate is forecast for the China CGM space through 2030?

The China continuous glucose monitoring devices market is projected to advance at a 17.57% CAGR to 2030.

Which product category dominates sales?

Sensors constituted 78.84% of 2024 revenue, making them the leading component.

How fast is pediatric adoption rising?

Pediatric revenue is projected to grow at 19.61% CAGR, the quickest among demographic groups.

Who are the key domestic CGM manufacturers?

Medtrum Technologies, Zhejiang POCTech, and MicroTech Medical are the principal home-grown competitors.

Do GLP-1 drugs threaten CGM demand?

GLP-1 therapies reduce daily testing frequency but still require periodic monitoring, positioning CGM as a complementary tool rather than a substitute.

Page last updated on: