Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

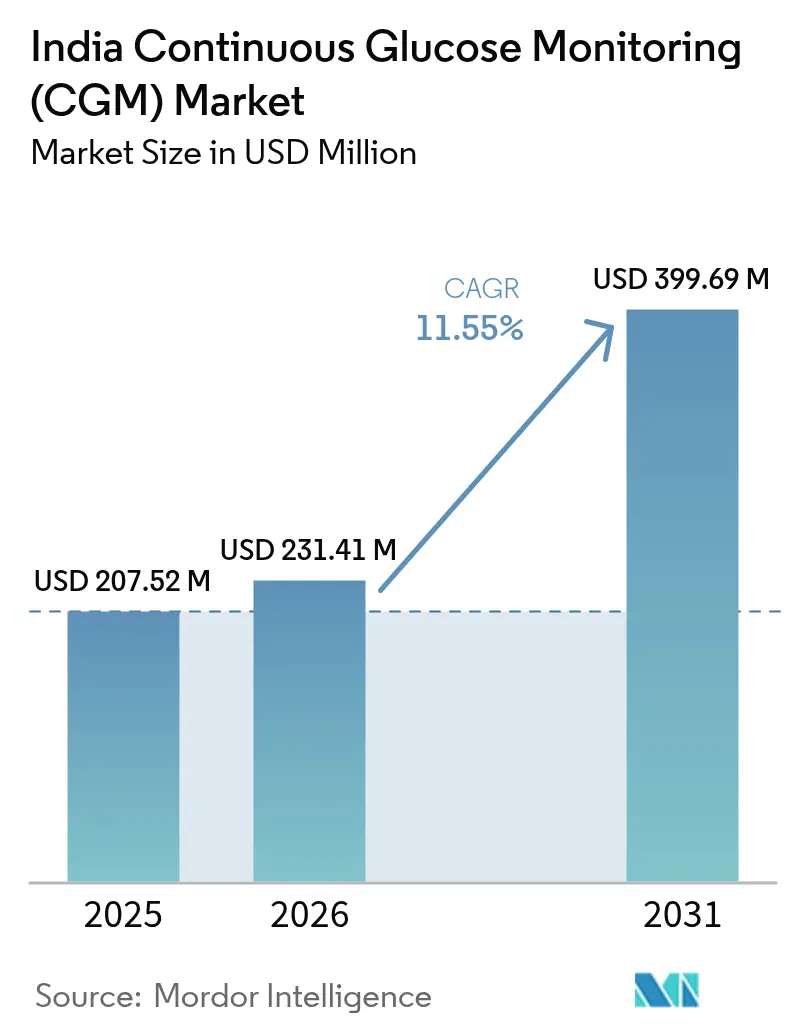

| Base Year Market Size (2025) | USD 207.52 Million |

| Market Size (2026) | USD 231.41 Million |

| Market Size (2031) | USD 399.69 Million |

| Growth Rate (2026 - 2031) | 11.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Continuous Glucose Monitoring (CGM) Market Analysis by Mordor Intelligence

The India Continuous Glucose Monitoring Market size was valued at USD 207.52 million in 2025 and is estimated to grow from USD 231.41 million in 2026 to reach USD 399.69 million by 2031, at a CAGR of 11.55% during the forecast period (2026-2031).

A structural transition toward proactive diabetes management underpins this expansion as 89.8 million Indian adults were already living with diabetes in 2024, and the number is forecast to reach 156.7 million by 2050. A structural transition toward proactive diabetes management underpins this expansion as 89.8 million Indian adults were already living with diabetes in 2024, and the number is forecast to reach 156.7 million by 2050 [1]International Diabetes Federation, “IDF Diabetes Atlas 11th Edition,” diabetesatlas.org. Three catalysts amplify demand: (1) the Ayushman Bharat Digital Mission’s 689 million ABHA accounts that enable seamless CGM data exchange (2) domestic sensor assembly subsidized by the Production Linked Incentive scheme that is lowering average selling prices by 10-30% and (3) integration with Indian wellness super-apps such as Ultrahuman and HealthifyMe that reposition CGM as a mainstream lifestyle tool. Together, these forces shorten adoption cycles, attract private insurers to remote-patient-monitoring contracts, and intensify competition between multinationals and venture-backed start-ups.

Key Report Takeaways

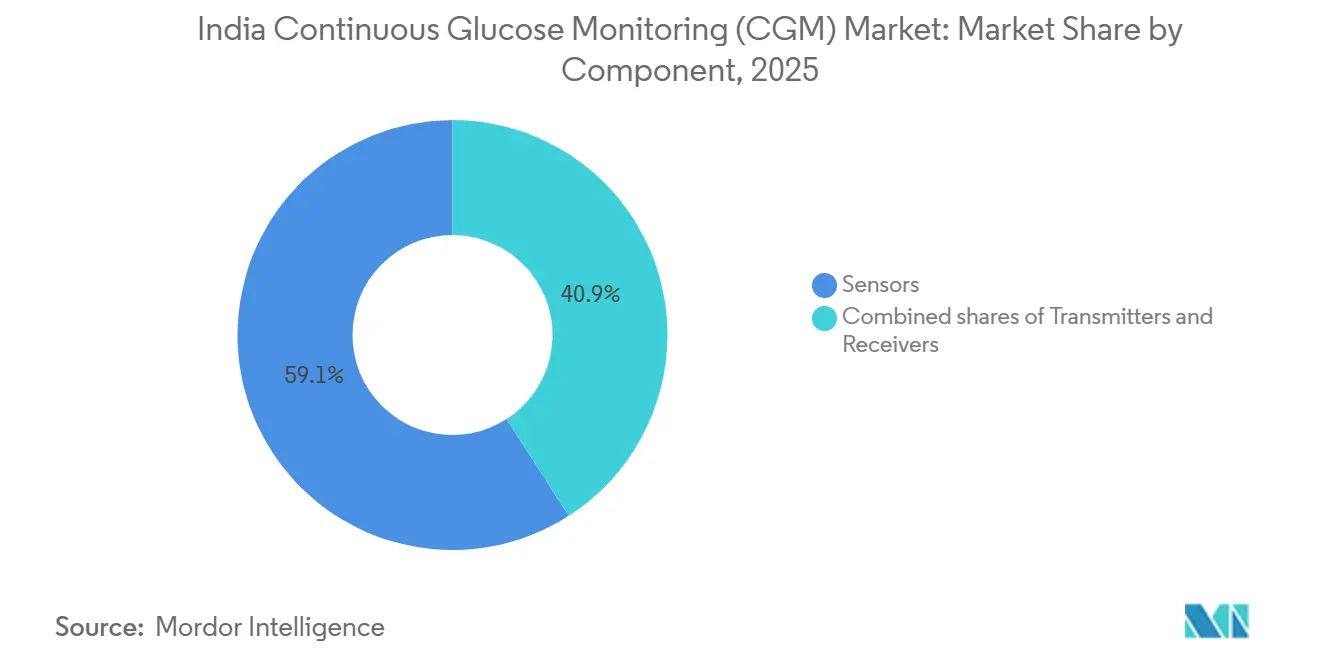

- By component, sensors led with 59.1% revenue share in 2025, while receivers are forecast to grow at a 12.34% CAGR to 2031.

- By device type, real-time systems commanded 60.2% of the 2025 market; intermittently-scanned systems are poised to expand at a 12.11% CAGR through 2031.

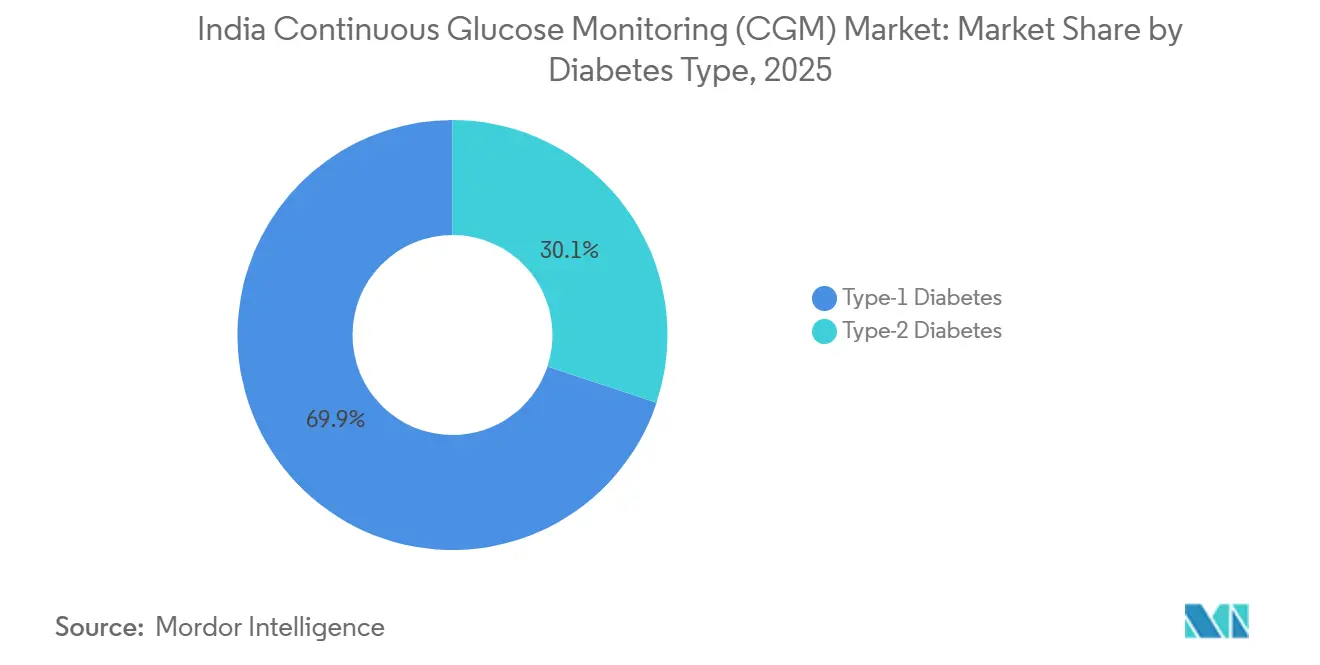

- By diabetes type, Type-1 accounted for 69.9% of 2025 revenue, whereas Type-2 is the fastest-growing segment at a 13.5% CAGR to 2031.

- By age group, adults dominated with 66.7% share in 2025; pediatrics is projected to climb at a 14.31% CAGR over 2026-2031.

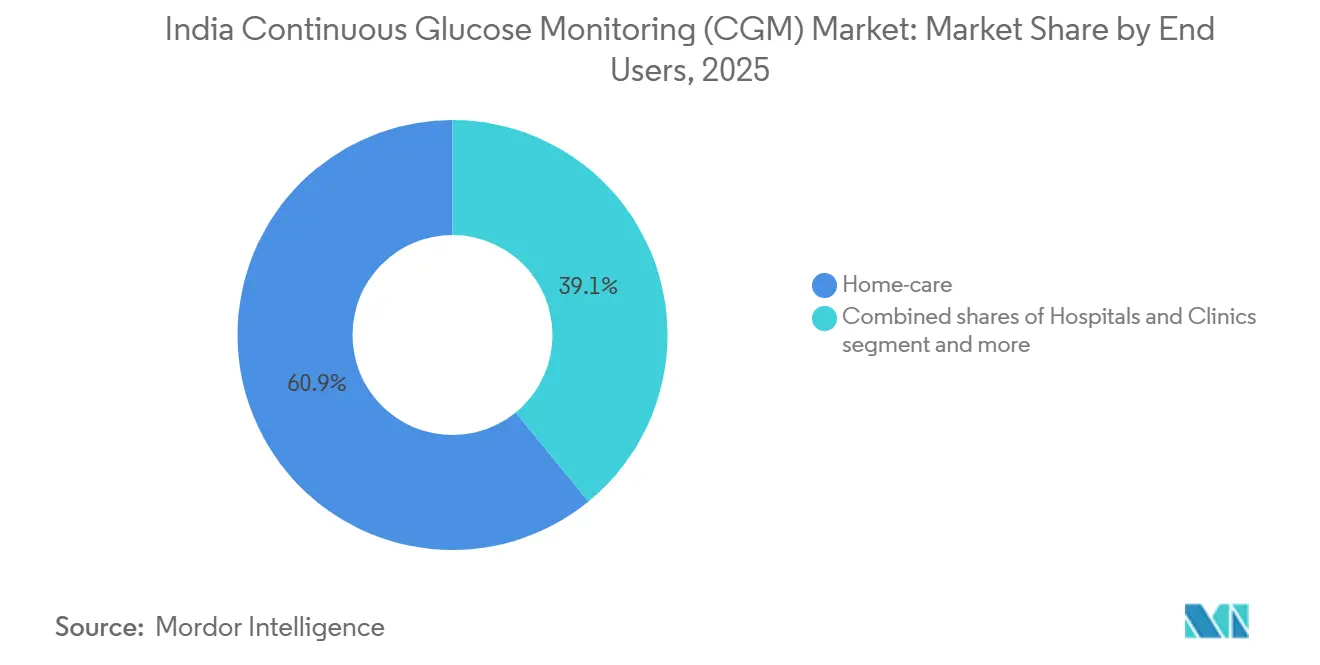

- By end-user, home-care settings captured 60.9% of 2025 revenue, while sports and fitness centers are set to accelerate at a 15.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Continuous Glucose Monitoring (CGM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soaring diabetes prevalence & earlier diagnosis | +3.2% | Urban India (Delhi, Mumbai, Bangalore, Chennai) | Medium term (2-4 years) |

| Rapid expansion of tele-consult & digital-health programs | +2.8% | Tier-1 cities; spillover to Tier-2/3 via e-Sanjeevani | Short term (≤2 years) |

| Growing penetration of insurance-led RPM contracts | +2.1% | Tier-1 metros and corporate hubs (Pune, Hyderabad, Ahmedabad) | Medium term (2-4 years) |

| Domestic sensor assembly lowering ASPs | +1.9% | National (Uttar Pradesh, Madhya Pradesh, Tamil Nadu) | Long term (≥4 years) |

| Integration with indigenous wellness super-apps | +1.6% | Metro and Tier-1 cities | Short term (≤2 years) |

| Rising clinical evidence for Type-2 diabetes CGM efficacy | +1.1% | National academic centers and corporate wellness programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Soaring Diabetes Prevalence & Earlier Diagnosis

India counted 89.8 million adults with diabetes in 2024, and 38.6 million remained undiagnosed, prompting the National NCD Program to scale 724 district clinics that will screen an additional 75 million citizens by March 2025 [2]Ministry of Health & Family Welfare, “National NCD Program,” mohfw.gov.in. Updated national guidelines elevate “time in range ≥ 70%” as a therapeutic goal, making continuous rather than episodic monitoring essential. Multicenter trials in 2025 showed FreeStyle Libre lifting TIR from 40.8% to 64.5% among non-insulin-dependent Type-2 patients. Payers face USD 8.5 billion in 2024 diabetes costs, accelerating a pivot toward preventive technologies that curb complications. As a result, new prescriptions for CGM in government and teaching hospitals climbed 22% in 2025, creating a pipeline for the India continuous glucose monitoring market.

Rapid Expansion of Tele-Consult & Digital-Health Programs

The Ayushman Bharat Digital Mission linked 45.38 crore health records by 2024, laying the technical rails for real-time CGM data sharing. Government telemedicine platform e-Sanjeevani logged 270 million sessions, yet only 2% incorporated glucose streams—an adoption gap that start-ups like BeatO are closing through insurer-bundled CGM services. Virtual endocrinology consults now authorize CGM within 4-6 weeks instead of the earlier 6-9 months cycle, compressing demand timelines. Informed-consent modules built into telemedicine workflows reduce prescription friction under the Telemedicine Practice Guidelines 2020. Overall, digitized care pathways increase addressable patients in the India continuous glucose monitoring market by an estimated 1.8 million annually.

Growing Penetration of Insurance-Led RPM Contracts

CGHS revised its insulin-pump ceiling to INR 300,000 and mandated CGM or ≥4 daily SMBG readings, producing a captive CGM population among 3.8 million government beneficiaries. Employer wellness deals account for 15-20% of current CGM volumes, especially in IT and pharma hubs of Bangalore, Hyderabad, and Ahmedabad. Sugar.fit’s RPM-as-a-service bundles secure sensors at a 25% discount and charge firms a monthly fee, bypassing individual reimbursement hurdles. The model is diffusing to Tier-2 cities where specialist density is low, but corporate parks proliferate, steering incremental growth toward the India continuous glucose monitoring market.

Domestic Sensor Assembly Lowering ASPs

Twenty-six manufacturers secured medical-device PLI incentives worth INR 3,420 crore in 2024, targeting 10-30% price cuts through localized sub-assemblies. Device parks in Uttar Pradesh and Tamil Nadu already produce transmitter housings and receivers, trimming FreeStyle Libre sensor prices from INR 6,000 in 2023 to INR 5,000 in 2025. Single-window licensure now clears new manufacturing lines in 6-9 months versus 18 months prior, hastening market entry. This cost trajectory enlarges the mid-income addressable pool and elevates volume elasticity in India continuous glucose monitoring market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront device cost vs SMBG | -2.7% | Tier-2/3 cities and rural areas nationwide | Medium term (2-4 years) |

| Patchy reimbursement outside Tier-1 cities | -1.8% | Semi-urban regions across all states | Long term (≥4 years) |

| Data-privacy compliance burden under DPDP Act 2023 | -0.9% | National start-ups and aggregators | Short term (≤2 years) |

| Limited endocrinologist networks outside metro cities | -1.0% | Tier-2/3 cities, rural belts, North-East region | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Upfront Device Cost vs SMBG

Abbott sensors cost INR 5,000 per 14 days versus INR 800-2,000 for a glucometer plus strips, making CGM up to 20 times dearer every month. Median annual health spend in Tier-3 cities is USD 60-70, far below the USD 720 needed for continuous isCGM use [3]National Health Systems Resource Centre, “National Health Accounts 2024,” nhsrcindia.org. EMI options are elusive outside large metros, and credit-card penetration among diabetics in small cities is less than 20%. Consequently, patients use CGM intermittently, dampening per-patient revenue in the India continuous glucose monitoring market.

Patchy Reimbursement Outside Tier-1 Cities

CGM lacks explicit inclusion in most private and state insurance schemes, except for CGHS pump-therapy coverage that benefits only 3.8 million employees and retirees. Insurance firms cite limited India-specific cost-effectiveness data to defend exclusions. Organized-sector workers represent only 10% of India’s labor force, leaving 80% of diabetics to self-finance devices. The reimbursement vacuum curtails mass adoption and caps upside for the India continuous glucose monitoring market

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Sensors Dominate, Receivers Gain Traction

Sensors delivered 59.1% of 2025 revenue thanks to their 7-14 day replacement cycle. Receiver demand will expand at 12.34% CAGR as privacy-minded or battery-constrained users choose standalone displays, lifting the India continuous glucose monitoring market size for hardware peripherals without eroding sensor sales. Transmitters face substitution pressure because new integrated designs fuse Bluetooth radio into sensors, eliminating a discrete SKU and trimming total device count.

Margins differ sharply: sensors yield 20-25% gross margins due to high output and discounting, whereas receivers secure 35-40% because of proprietary software tie-ins. Domestic assembly centers on receivers and transmitter shells, leaving high-value electrodes imported from Ireland and Malaysia, a pattern that constrains local value capture. Nonetheless, technology transfer arrangements under the PLI scheme are expected to localize at least 15% of sensor BOM value by 2028, gradually lifting the India continuous glucose monitoring market share of Made-in-India components.

By Device Type: Real-Time Leads, Intermittent-Scan Closes Gap

Real-time systems controlled 60.2% of revenue in 2025 because Type-1 insulin users require continuous alerts. Intermittently-scanned devices are projected to surge at 12.11% CAGR as FreeStyle Libre sensors, priced 30-40% lower, win adoption among Type-2 patients seeking lifestyle feedback rather than hypoglycemia warnings. HbA1c studies report a 0.5 point reduction in basal-insulin Type-2 cohorts using isCGM over 90 days, validating its clinical utility.

Pricing dynamics favor isCGM for volume expansion: a 14-day Libre sensor costs INR 5,000, translating to INR 10,700 monthly for continuous wear, 50-60% below monthly rtCGM outlay. Reimbursement pathways also tilt toward isCGM because insurers perceive lower per-member risk. Consequently, isCGM is cannibalizing SMBG far more than rtCGM, and its ascendancy is likely to raise the India continuous glucose monitoring market size for mid-tier offerings

By Diabetes Type: Type-1 Dominates Revenue, Type-2 Drives Growth

Type-1 diabetes accounted for 69.9% of 2025 revenue as insulin-pump protocols legally obligate continuous monitoring under CGHS reimbursement. Type-2 volumes, however, will expand at a 13.5% CAGR, widening the India continuous glucose monitoring market share of non-insulin therapies. Employer wellness contracts, OTC sensor pilots, and rising clinical evidence for basal-insulin optimization are catalyzing uptake.

Affordability remains the fulcrum: only urban households earning less than INR 1 million typically finance year-round CGM use. Short-cycle diagnostic deployments (2-4 weeks per quarter) are common among middle-income Type-2 patients, cutting per-user revenue by 50-60% but multiplying the installed base. Vendors that tailor subscription bundles and rental models for intermittent use will expand total addressable patients faster than those chasing full-time adherence.

By Age Group: Adults Lead, Pediatrics Accelerates

Adults held 66.7% share in 2025, reflecting the epidemiological weight of Type-2 cases in the 40-65 cohort. Pediatric sales, although smaller, will scale at 14.31% CAGR as Delhi, Mumbai, and Bangalore hospitals roll out CGM care paths that cut severe hypoglycemia by 36%. Improved school-based alert protocols and remote caregiver dashboards lower parental anxiety, widening adoption.

Geriatric growth is steadier because usability hurdles, such as small fonts, multi-step pairing, and adhesive discomfort, deter the 65+ segment. Yet India’s aging population (140 million by 2030) underpins a latent reservoir. User-interface simplification and caregiver-centric data sharing could unlock an incremental India continuous glucose monitoring market size in elderly care.

By End-User: Home-Care Dominates, Sports & Fitness Surges

Home-care captured 60.9% of 2025 revenue as smartphone penetration (760 million users) makes at-home insertion and monitoring feasible. Sports and fitness centers will grow fastest at 15.34% CAGR, propelled by Ultrahuman’s INR 7,000/month metabolic-score subscription and HealthifyMe’s 500,000 CGM sessions in 2025. These platforms position CGM as a biohacking utensil, enlarging demand beyond therapeutic confines.

Hospitals and clinics contribute to the balance but face decelerating growth as outpatient visits migrate online. Inpatient CGM remains limited to ICUs and perioperative wards; thus, their share may plateau, leaving consumer channels to anchor expansion in the India continuous glucose monitoring market.

Geography Analysis

North India records the highest absolute CGM uptake because Delhi houses 15 tier-one hospitals running advanced diabetes centers. Central-government employees clustered in the capital benefit from CGHS reimbursement, ensuring steady sensor volumes. Yet Tier-2 cities like Lucknow and Jaipur see slower penetration; annual health budgets of USD 70 struggle to fund INR 60,000 yearly sensor expenditure. Component assembly in the Uttar Pradesh device park is expected to trim prices further, potentially lifting India continuous glucose monitoring market share in northern heartlands post-2028.

South India shows the deepest per-capita adoption, led by Bangalore’s research ecosystem and Chennai’s medical-tourism inflows. Tamil Nadu’s PLI-backed facilities already churn out transmitter shells, injecting cost elasticity. Urban diabetes prevalence tops 17%, magnified by genetic susceptibility and lifestyle shifts, thus ensuring robust demand. High English literacy simplifies app usage, giving southern metros a sustained head-start in the India continuous glucose monitoring market.

West India balances prosperity in Mumbai and Pune against slower rural diffusion. Corporate wellness packages in Mumbai alone cover 200,000 executives, translating into bulk CGM orders. Gujarat’s pharma clusters lure component suppliers, yet full sensor production is nascent. East and North-East India trail on every metric: limited specialists, lower per-capita income, and nascent digital grids restrict adoption mostly to Kolkata’s private hospitals. Tribal regions with high impaired-glucose tolerance remain untapped because awareness campaigns have not prioritized continuous monitoring. Bridging these regional gaps holds the key to the next growth wave in the India continuous glucose monitoring market.

Regulatory Landscape

Continuous glucose monitoring (CGM) systems marketed in India are regulated as medical devices under the Medical Devices Rules, 2017 (MDR-2017), administered by the Central Drugs Standard Control Organization (CDSCO). Manufacturers and importers must align device quality and safety requirements with applicable Bureau of Indian Standards (BIS) specifications, or with recognized ISO/IEC or pharmacopoeial standards where BIS standards are not available. This affects technical documentation, QMS readiness, and time-to-license for multinational and domestic entrants.

Because CGM ecosystems are increasingly connected (Bluetooth/NFC-enabled sensors, transmitters, receivers, and companion apps), compliance also extends into wireless and software components that can increase pre-market work and change-management effort. CDSCO has further emphasized post-market surveillance capability building, including safety surveillance workshops conducted with international counterparts such as the Danish Medical Agency (DKMA) on April 8-9, 2026, reinforcing expectations for vigilance systems as CGM adoption broadens into home-care and consumer wellness channels.

Value Chain Analysis

India's CGM value chain combines import-heavy upstream inputs with growing domestic assembly and a distribution network centered on large metro procurement corridors. High-value electrochemical sensor elements and substrates remain largely sourced from outside India, while local activity has expanded in downstream sub-assemblies such as receiver units and transmitter housings, supported by medical device parks and incentive-led manufacturing programs referenced in the report context.

Downstream value capture is increasingly tied to software, data workflows, and service-layer integration rather than only device hardware. Platforms that bundle sensors with coaching, tele-consults, and analytics monetize adherence and outcomes while creating switching costs. Strategic supply arrangements between global leaders also influence product roadmaps, interoperability priorities, and channel strategies, which then play out in India through local partners, institutional accounts, and digital-health distributors. For instance, Abbott's sensor supply relationship with Medtronic for integrated offerings can shape how integrated systems are positioned in the market.

Competitive Landscape

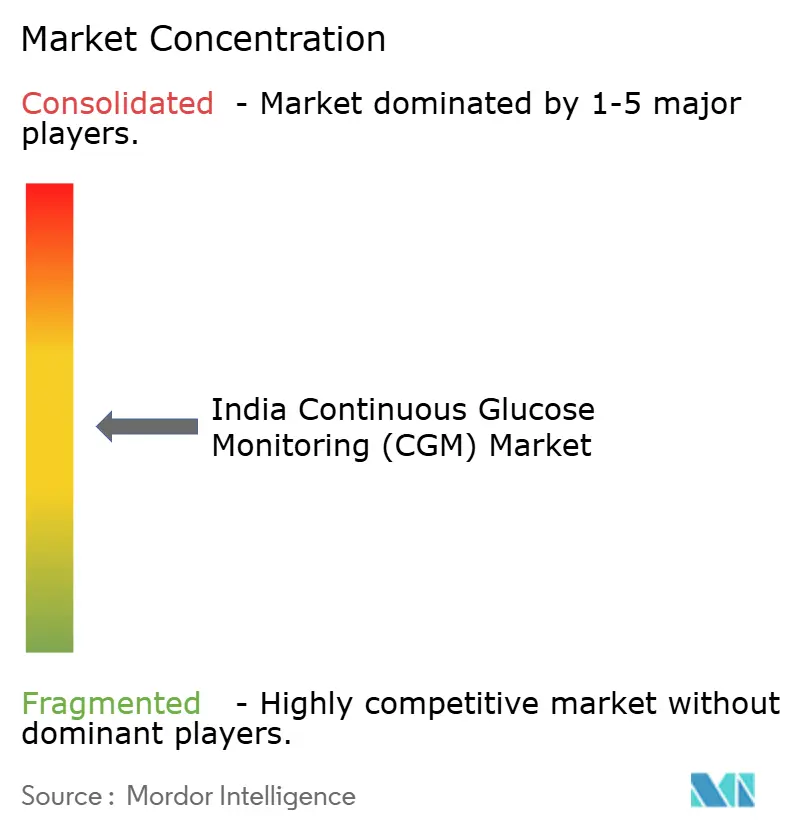

Abbott and Dexcom jointly hold the majority of sales, defining a moderately concentrated arena. Abbott pursues volume pricing, cutting sensor costs between 2023 and 2025, while Dexcom leverages a Cipla partnership to tap 5 million app users.

Domestic disruptors shape new battlegrounds. BeatO’s rental program offers sensors at INR 3,500 per fortnight in exchange for de-identified data, enlarging reach among price-sensitive Type-2 cohorts. Sugar. fit’s 25-clinic rollout melds CGM with on-site coaches, staking a claim in hybrid care. iSprit MedTech is the only indigenous sensor R&D pipeline; if its ImageriCGM gains CDSCO nod within nine months, as the new fast-track allows, the India continuous glucose monitoring market could shift toward local IP.

Technology vectors are converging on miniaturization and wear-time. Abbott’s Libre 3 shrank 70% versus Libre 2 yet preserved 14-day life, ideal for India’s humid climate, where skin irritation is common. Dexcom’s G7 fuses sensor and transmitter, lowering upfront outlay by 25% against the G6 baseline. Such innovations, alongside ISO 13485-mandated quality upgrades, incrementally reduce total cost of ownership, broadening market appeal even in semi-urban pockets.

India Continuous Glucose Monitoring (CGM) Industry Leaders

Dexcom Inc.

Medtronic PLC

Ascensia

Abbott Laboratories

Roche Diagnostics

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A whitespace remains between the scale of digital health infrastructure and how much CGM data is operationalized in routine care. In the report context, the Ayushman Bharat Digital Mission (ABDM) provides a foundation for data exchange through ABHA accounts and linked health records, while telemedicine usage remains high. The opportunity is to convert more diabetes encounters into continuous-data workflows, enabling CGM vendors and service providers to expand beyond device sales into remote patient monitoring packages, clinic dashboards, and consented data-sharing models that align with DPDP Act requirements.

Product and program signals also point to opportunity in differentiated use cases and tiered offerings rather than one-size-fits-all reimbursement. Published clinical evidence and 2026 study readouts strengthen the case for CGM in Type-2 cohorts beyond intensive insulin users, supporting uptake through employer-wellness and insurer-bundled deployments already visible in the market context. On technology, multi-analyte sensing is moving from concept to commercial regulatory milestones, including Abbott's Libre Duo dual glucose-ketone sensing cleared CE Mark in May 2026. This supports an upgrade cycle where Indian channels can segment premium clinical populations alongside lower-cost intermittent scanning options as local assembly reduces system-level costs.

Recent Industry Developments

- June 2026: Dexcom reports Reuters coverage of a CGM study showing benefits for non-insulin-using Type 2 diabetes patients (CONNECT trial). The global data on CGM performance supports pricing and adoption considerations in India and strengthens Dexcoms competitive positioning.

- May 2026: Abbott CE Mark for Libre Duo, dual glucose-ketone sensing technology. The addition of dual glucose-ketone sensing enhances CGM capabilities and creates further differentiation in the Indian market.

- May 2026: Dexcom targets entering Indian market (and Brazil/Mexico) within two years. The announced market entry timeline can reshape the Indian CGM competitive landscape by expanding Dexcom's global footprint and intensifying competition with Dexcoms G7.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the India continuous glucose monitoring market is defined as revenue earned in India from CGM systems and their core device components that enable continuous or near-continuous glucose tracking for personal or clinical use.

Scope exclusions: We exclude routine fingerstick blood glucose monitoring products (meters, strips, and lancets) and broader diabetes drugs and supplies that are not part of CGM device kits.

Segmentation Overview

- By Component

- Sensors

- Transmitters

- Receivers

- By Device Type

- Real-time CGM (rtCGM)

- Intermittently-Scanned CGM

- By Diabetes Type

- Type-1 Diabetes

- Type-2 Diabetes

- By Age Group

- Paediatrics

- Adults

- Geriatrics

- By End-user

- Hospitals & Clinics

- Home-care Settings

- Sports & Fitness Centres

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the market boundary, build the patient and care-setting context, and anchor assumptions that are later pressure-tested through interviews. We referred to public health statistics and clinical guidance that help interpret diabetes burden and monitoring adoption in India, plus device market signals around approvals, imports, and channel availability.

Sources used include public or official references such as National Health Mission and Ministry of Health publications, National Family Health Survey style health indicators, International Diabetes Federation diabetes estimates, World Health Organization diabetes and NCD dashboards, peer-reviewed clinical journals, and trade and customs statistics from Government of India portals. We also reviewed company annual reports, investor presentations, product labeling, and reputable press coverage, then supplemented missing financial context using paid subscriptions for company financials and intelligence and patent databases. The specific desk sources listed here are illustrative, and we used other public documents to collect data, validate assumptions, and clear up inconsistencies.

Primary Interviews and Surveys

Primary work focused on aligning the model to how CGM is actually bought and used in India, across hospitals and clinics, home-care settings, and emerging wellness use cases. We interviewed device distributors, clinicians, diabetes educators, procurement and channel managers, and product or commercial leaders to confirm pricing bands, replacement cycles, and adoption friction points across large metros and tier 2 cities.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 18% | |

| Mid tier: 44% | Functional/Unit leaders: 31% | |

| Smaller Players: 20% | Managers: 51% |

Market-Sizing & Forecasting

The core model is built using a top-down demand pool approach where diabetes prevalence, the addressable treated and monitored population, and CGM penetration are reconstructed for India, then translated into value using average selling price logic for key components. To keep totals realistic, we checked results against selective bottom-up approximations such as channel-level sell-in checks, sampled ASP by pack type, and sanity checks using import and distribution signals when available.

Inputs that matter in this market include the diagnosed diabetes population and care-seeking behavior, expected CGM wear duration and sensor replacement frequency, average device bundle pricing (sensor plus transmitter or receiver, depending on configuration), the share of rtCGM versus intermittently scanned CGM, and the end-user mix between hospitals and home-care. For forecasting, scenario analysis is used because pricing, reimbursement, and physician recommendation patterns can shift quickly, and these shifts are easier to express as base, conservative, and accelerated adoption paths. Where bottom-up pieces are incomplete, for example when channel coverage differs sharply by city, assumptions are filled using interview consensus and then re-tested against the overall demand pool so the model stays internally consistent.

Data Validation & Update Cycle

Outputs are validated through multiple checks, starting with consistency tests across patient pool, adoption, and implied unit volumes, followed by reviews of any jumps that do not match known policy, pricing, or supply signals. We also compare the final value series with independent indicators such as diabetes burden trend direction, observed product availability in key channels, and typical replacement behavior shared by practitioners and distributors.

Before sign-off, a second analyst reviews key assumptions, and any material variance triggers re-contact with respondents for clarification. Reports are refreshed annually, and interim updates are made when major events occur, such as important approvals, pricing moves, or channel shifts. Right before delivery, we run a final scan so clients receive the latest updated view.

Mordor Intelligence's India Continuous Glucose Monitoring Market Size Versus Other Published Estimates

Published market numbers for India CGM can look different across sources, even when they sound like they cover the same topic, because the counted products and the pricing and volume logic are not consistent. Differences can also come from the year used, the currency conversion timing, and whether the estimate is tied to realistic adoption and replacement behavior.

Some estimates fold in adjacent diabetes monitoring items or add broader digital health services linked to glucose data. Here, the value is counted only for CGM devices and their core components sold in India, then cross-checked with wear-duration based replacement cycles and interview-confirmed price bands so unit assumptions do not drift. This is where Mordor Intelligence makes the scope and adoption mechanics explicit in the estimate build.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 207.52 M (2025) | |

| Industry News Digest A | USD 231.28 M (2026) | This figure is commonly presented as a simple forward number without detailing the assumed sensor replacement frequency and the split between rtCGM and intermittently scanned CGM, which can shift implied unit volumes. |

| Healthcare Journal B | USD 397.32 M (2031) | The total is often quoted as a headline forecast, but the underlying base-case adoption path and pricing progression are not always shown, which can lead to aggressive uptake and steady ASP assumptions being applied together. |

The table shows that a one-year shift in the reference year and small differences in how replacement cycles and product mix are treated can move the market value meaningfully. By keeping the scope tight to CGM devices and then tying forecasts to observable demand indicators, the final numbers stay traceable to clear steps that can be repeated and re-checked over time.

Key Questions Answered in the Report

What is the current size of the India continuous glucose monitoring market?

The market is estimated at USD 231.41 million in 2026 and is projected to reach USD 399.69 million by 2031, expanding at an 11.55% CAGR over 2026-2031

Which diabetes-type segment dominates the India CGM market?

Type-1 diabetes captures 69.9% of 2025 revenue because CGHS insulin-pump reimbursement mandates CGM, but Type-2 is the fastest-growing at a 13.5% CAGR through 2031

Which component segment is growing fastest in the India CGM market?

Receivers are forecast to grow at a 12.34% CAGR through 2031 as privacy-minded users prefer dedicated displays; sensors still hold 59.1% share

How does real-time CGM compare with intermittently-scanned CGM?

Real-time systems hold 60.2% share in 2025; intermittently-scanned CGM is set to expand at 12.11% CAGR to 2031

Which age group is driving the fastest CGM growth?

Pediatric use will rise at 14.31% CAGR through 2031, with studies showing a 36% cut in severe hypoglycemia and a 12-point Time-in-Range improvement.

Page last updated on: