United States Continuous Glucose Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

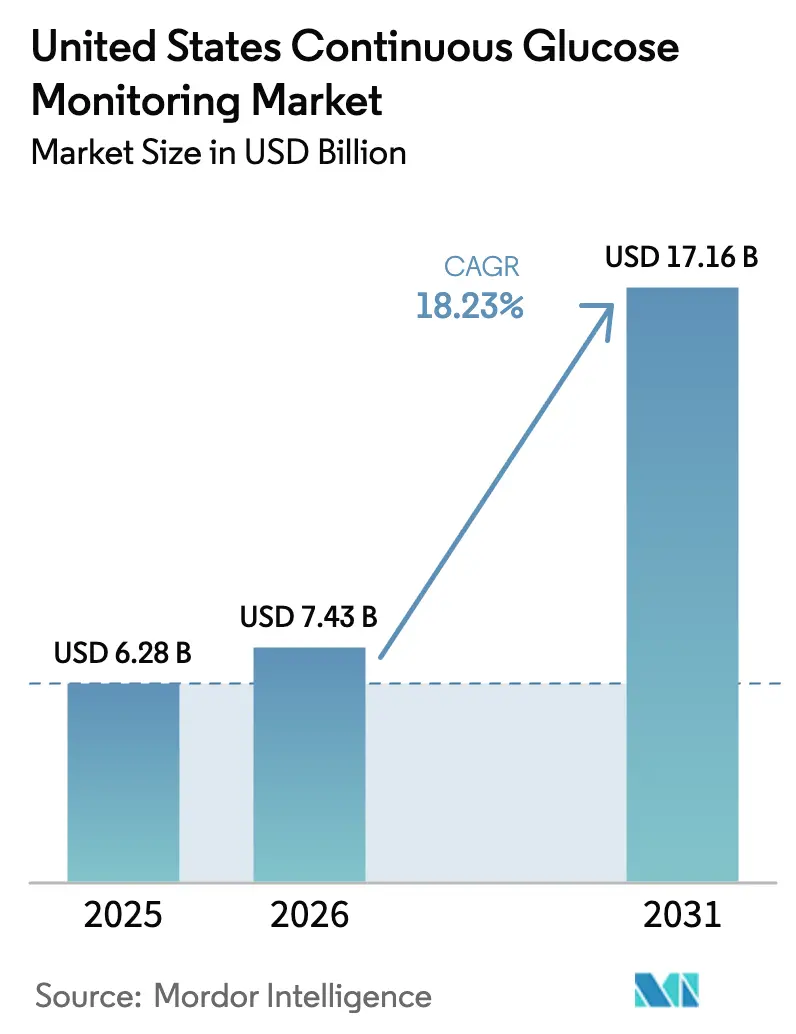

| Base Year Market Size (2025) | USD 6.28 Billion |

| Market Size (2026) | USD 7.43 Billion |

| Market Size (2031) | USD 17.16 Billion |

| Growth Rate (2026 - 2031) | 18.23% CAGR |

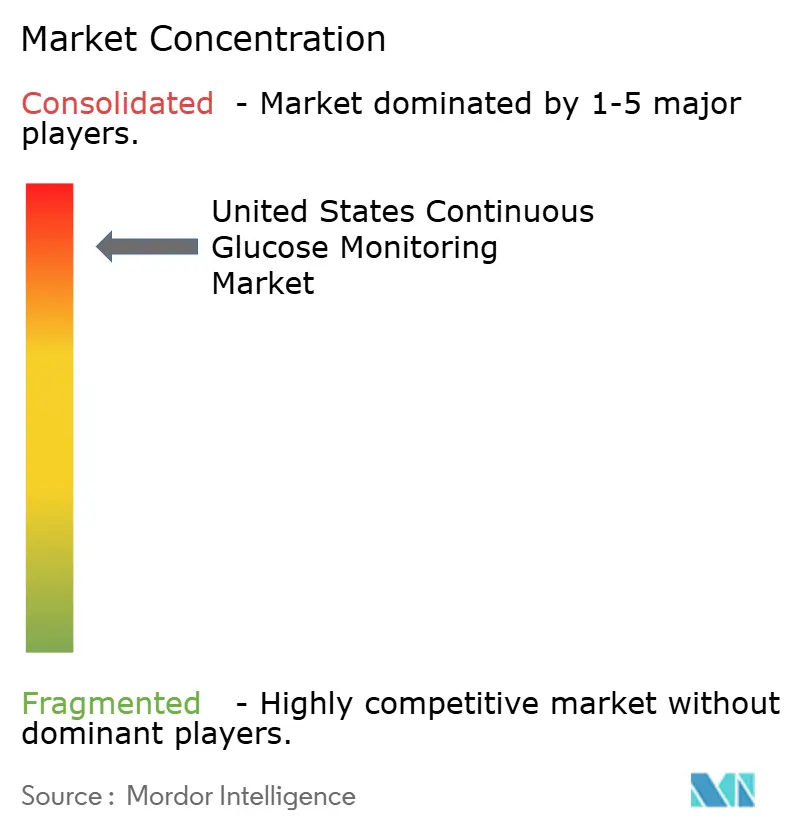

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Continuous Glucose Monitoring Market Analysis by Mordor Intelligence

The continuous glucose monitoring market size in 2026 is estimated at USD 7.43 billion, growing from 2025 value of USD 6.28 billion with 2031 projections showing USD 17.16 billion, growing at 18.23% CAGR over 2026-2031. The growth reflects expanded Medicare coverage for Type-2 basal-only patients, accelerating over-the-counter approvals, and steady sensor price erosion below USD 100 per 14-day wear period. Market momentum also comes from earlier diabetes diagnoses, hospital cost-saving pilots, and AI-enabled insulin dosing algorithms that embed CGM into routine clinical pathways. Alongside these medical drivers, wellness applications that let non-diabetic consumers track daily glucose trends continue to broaden the continuous glucose monitoring market beyond its historical insulin-dependent core.

Key Report Takeaways

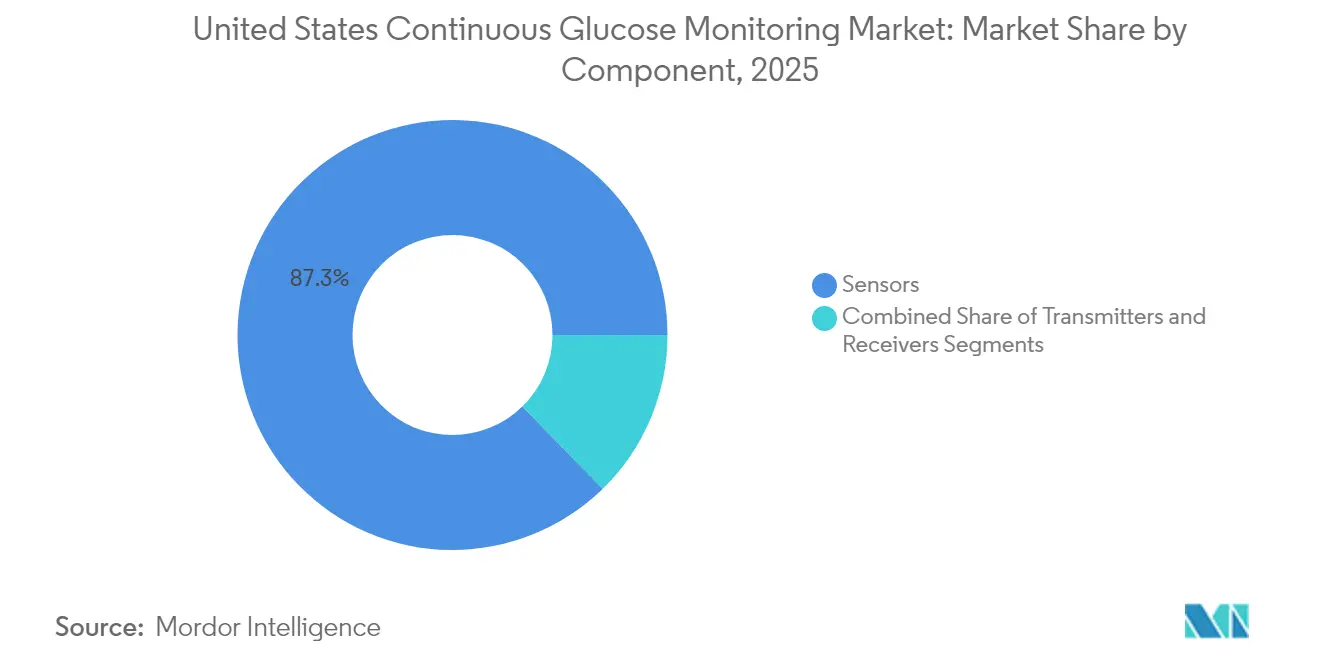

- By component, sensors held an 87.32% share of the continuous glucose monitoring market in 2025, while durable components recorded the fastest 19.35% CAGR between 2026 and 2031.

- By end user, home and personal use captured 67.10% of the continuous glucose monitoring market share in 2025; hospital and clinical settings are expanding at the leading 19.01% CAGR through 2031.

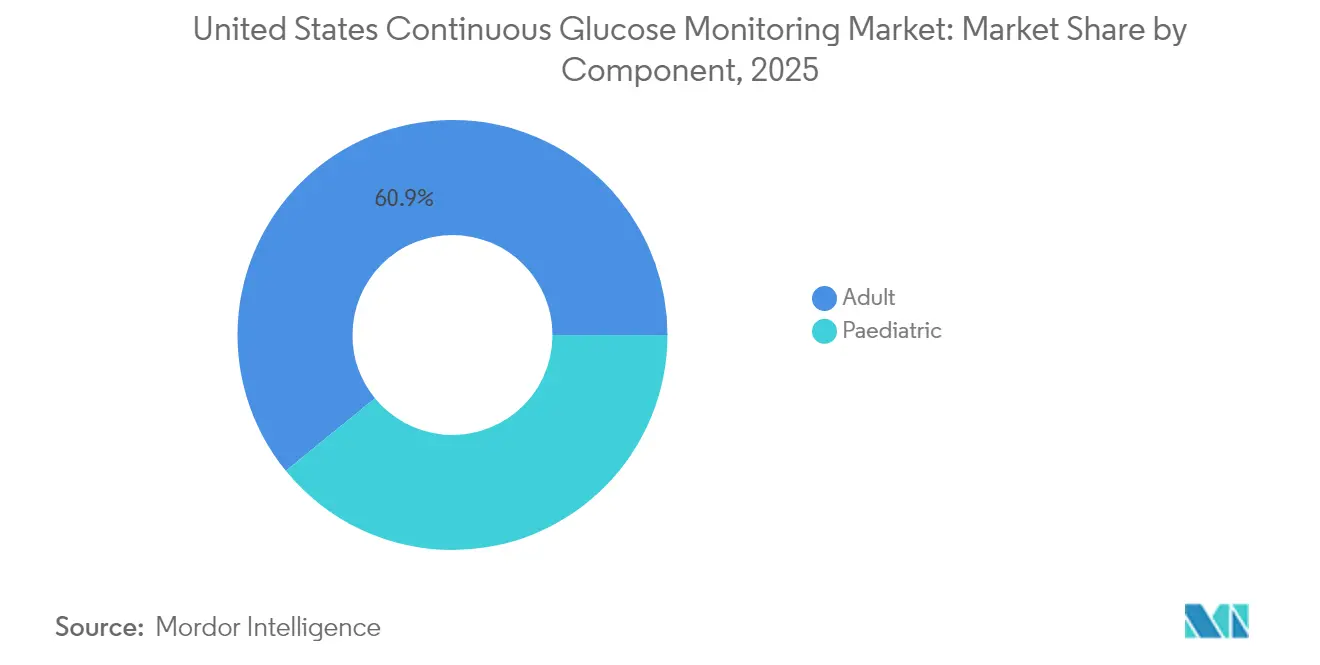

- By demography, adults accounted for 60.88% of the continuous glucose monitoring market size in 2025, whereas the pediatric segment posts the highest 19.12% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Continuous Glucose Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diabetes Prevalence and Earlier Diagnoses | +4.2% | National, highest in Southern and Midwest states | Long term (≥ 4 years) |

| Medicare/Medicaid Expansion For Type-2 Basal-Only Patients | +3.8% | National with state-level Medicaid variation | Medium term (2-4 years) |

| Price Erosion Of Sensors Below USD 60 Per 14-Day Wear Period | +2.9% | National, fastest in competitive metro areas | Short term (≤ 2 years) |

| Shift To OTC Wellness CGMs (Stelo, Lingo) Expands Addressable Base | +3.1% | National, early uptake in urban/suburban zones | Medium term (2-4 years) |

| AI-Driven Dosing Algorithms Boost Clinical Outcomes and Adoption | +2.4% | National, led by integrated health systems | Long term (≥ 4 years) |

| Hospital Ward Pilots Proving Cost-Savings Over POC Testing | +1.7% | National, concentrated in large hospital systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence and Earlier Diagnoses

CDC surveillance shows adult diabetes prevalence rising from 9.7% in 1999-2000 to 15.8% in 2021-2023, translating to 38.4 million Americans who potentially benefit from continuous glucose monitoring market solutions. Younger adults are being screened sooner, which pushes CGM adoption earlier in the disease course. Payers increasingly view CGM as a frontline therapy that prevents severe hypoglycemia and costly hospitalizations, making reimbursement justification easier. Providers treat CGM as a foundational self-management tool rather than an advanced add-on, a perception shift that enlarges the addressable base. As a result, the continuous glucose monitoring market gains sustained volume tailwinds from both Type-1 and Type-2 cohorts, whose treatment plans now anchor around real-time data feedback.

Medicare/Medicaid Expansion for Type-2 Basal-Only Patients

In April 2023, CMS broadened coverage to include Type-2 patients using basal insulin only, opening CGM eligibility to an extra 1.5 million beneficiaries. Adoption momentum varies by state Medicaid policy, yet progressive states already report higher authorization rates that speed volume uptake. The policy decision rests on evidence that CGM reduces emergency visits and inpatient costs, benefits that resonate with value-based care contracts. Pharmacy benefit pathways continue to evolve, so manufacturers are expanding distribution channels and patient support programs to navigate differing durable-equipment billing rules. The net effect is a medium-term surge in unit sales as both public and commercial payers harmonize benefit designs.

Sensor Price Erosion Below USD 60 per 14-Day Wear Period

Dexcom’s Stelo debut at USD 89-99 and Abbott’s similar OTC strategies indicate a broader slide toward sub-USD 60 sensor pricing over the next two years. Manufacturing automation, longer wear times, and simplified calibration have trimmed unit costs, allowing lower retail prices without eroding gross margins as steeply as feared. Affordable cash-pay options widen access for under-insured patients who previously rationed self-monitoring supplies. As prices fall, manufacturers pivot toward volume-based recurring revenue, favoring firms that already produce more than 10 million sensors annually. These economics could raise the entry barrier for smaller challengers, thereby reinforcing the high-volume leadership positions inside the continuous glucose monitoring market.

Shift to OTC Wellness CGMs Expands Addressable Base

The FDA cleared Dexcom’s Stelo as the first over-the-counter CGM in March 2024[1]U.S. Food and Drug Administration, “FDA Clears First Over-the-Counter Continuous Glucose Monitor,” fda.gov. Without prescription hurdles, marketing now targets health-conscious consumers who seek metabolic insight rather than strict diabetes control. Usage patterns differ; wellness buyers may use CGMs episodically alongside diet or fitness regimens, setting up demand spikes around seasonal initiatives like New Year resolutions. To cultivate recurring revenue, vendors bundle data analytics and lifestyle coaching subscriptions that deepen engagement beyond sensor hardware. Success in this arena could double the continuous glucose monitoring market’s reachable population by 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| GLP-1–Induced Glucose Normalization Reduces CGM Starts | -2.8% | National, strongest where GLP-1 use is high | Medium term (2-4 years) |

| Patch-Pump/CGM Bundles Limit Stand-Alone Sensor Sales | -1.9% | National, led by integrated tech adoption | Long term (≥ 4 years) |

| Data-Overload Fatigue Among Non-Insulin Users | -1.3% | National | Short term (≤ 2 years) |

| Uneven State-Level Medicaid Coverage Creates Access Gaps | -1.1% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

GLP-1 Induced Glucose Normalization Reduces CGM Starts

Rapid uptake of GLP-1 receptor agonists such as semaglutide brings many patients to normalized HbA1c levels, lowering perceived need for continuous monitoring. Studies show approximately 46% of non-diabetic users discontinue GLP-1 within a year, causing unpredictable sensor demand[2]Patricia J. Rodriguez et al., “Discontinuation and Reinitiation of GLP-1 Receptor Agonists Among US Adults,” medrxiv.org. Early discontinuation produces gaps in monitoring continuity, making it difficult for providers to justify CGM prescriptions. Nonetheless, emerging evidence supports CGM use during dose titration and to catch hypoglycemia in aggressively treated cohorts. Manufacturers now educate clinicians on complementary roles for CGM even when pharmacotherapy remains effective, which may soften this negative impact over time.

Patch-Pump and CGM Bundles Limit Stand-Alone Sensor Sales

Automated insulin delivery systems increasingly bundle proprietary sensors with pumps, locking users into specific ecosystems. Tandem’s Control-IQ platform requires Dexcom G6 sensors, and Abbott has exclusive supply deals with several pump makers. These arrangements create predictable high-margin revenue for participants yet reduce open-market sensor volumes. Closed-loop systems represent a large number of pump users today and grow 15-20% each year. If bundling becomes the norm, smaller or sensor-only companies may find access to the continuous glucose monitoring market more constrained, pushing them toward niche or wellness segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Sensors Anchor Recurring Revenue Streams

Sensors captured 87.32% of the continuous glucose monitoring market in 2025 and are forecast to compound at an 18.05% rate through 2031. This dominance stems from 14- to 15-day replacement cycles that create subscription-like revenue predictability. The continuous glucose monitoring market size for sensor hardware is on track to surpass USD 14.2 billion by 2031, underpinned by mass-production cost advantages and AI-ready data output. Dexcom’s G7 15-day sensor, cleared in April 2025, sustains 8.0% MARD accuracy, demonstrating how incremental performance gains support premium price points. Longer wear times and Bluetooth direct-to-phone links minimize the role of dedicated receivers, paving the way for consumer-scale adoption well beyond diabetes.

Durable components—receivers and transmitters—hold 12.68% share and grow at just 19.35% through the forecast. Their decelerating curve reflects smartphone ubiquity that makes proprietary displays obsolete. Transmitters lasting 90-180 days dampen replacement frequency, and regulatory scrutiny pushes manufacturers to extend life cycles further. Higher per-unit prices cushion revenue, yet overall share slips as sensors absorb much of the system’s value. Competitive focus, therefore, centers on transmitter miniaturization and waterproofing to simplify closed-loop pump pairing.

By End User: Home-Based Management Leads Adoption

Home and personal users represent 67.10% of the continuous glucose monitoring market share in 2025, a figure projected to climb with an 17.62% CAGR as self-management becomes standard care. COVID-19 accelerated remote monitoring norms, and these behaviors persist because patients value autonomy. Pharmacy benefit coverage and direct-ship logistics cut clinic dependency, while mobile apps translate glucose patterns into actionable guidance. Health coaches and telehealth consults reinforce proper usage, embedding CGM into everyday routines.

Hospitals and clinics account for 32.90% of 2025 revenue yet rise at a faster 19.01% CAGR from a smaller base. Value-based purchasing encourages inpatient systems to swap point-of-care finger sticks for continuous tracking, particularly on surgical floors and high-risk medical units. Integration with electronic medical records is improving, reducing nursing workload while elevating patient safety. Over time, many admitted patients already wearing CGM at home will stay on their own devices during hospitalization, bridging both end-user categories and deepening market entrenchment.

By Demography: Pediatric Uptake Surges on Early Intervention

Adults held the majority, 60.88% share of the continuous glucose monitoring market size in 2025, supported by Medicare expansions and employer wellness programs. Yet adoption rates vary within this age range. Younger adults under 50 embrace device ecosystems quickly, while older cohorts face smartphone literacy and cost hurdles even after coverage reforms. Education campaigns that pair CGM data with nutrition counseling show promise in improving long-term adherence.

The pediatric population, still smaller in absolute terms, grows fastest at 19.12% CAGR. Early use prevents long-term complications, making payers willing to absorb sensor costs. School nurses increasingly manage CGM alerts during class, an operational change that removes a prior barrier to classroom participation. Parents also leverage cloud portals to monitor children remotely, reducing fear of nocturnal hypoglycemia and driving strong word-of-mouth advocacy that furthers adoption.

Geography Analysis

The United States' continuous glucose monitoring market shows notable regional clusters. Medicare Advantage penetration above 40% in these areas provides richer benefits that quicken uptake. By contrast, Medicaid policies range widely; Washington state covers CGM broadly, while several Midwestern states still require prior authorizations that impede installation.

California stands out because both Dexcom and Abbott operate sizable development hubs there. Early employee trials often precede formal FDA submissions, seeding local physician familiarity. Meanwhile, employer-sponsored wellness plans in Silicon Valley offer CGM stipends that illustrate broader consumer possibilities. International sales success of U.S. brands feeds domestic R&D budgets, with European FreeStyle Libre volumes helping Abbott price competitively at home. Balancing foreign expansion and domestic defense remains a strategic tightrope for all major manufacturers.

Competitive Landscape

The continuous glucose monitoring market remains oligopolistic. Abbott, Medtronic, and Dexcom jointly command roughly 98% of unit sales, yet the pace of technology keeps rivalry intense. Abbott leverages its high-volume FreeStyle Libre platform to undercut on price and to branch into wellness under the Lingo brand. Medtronic focuses on fully integrated insulin delivery, strengthening stickiness through Simplera sensor approvals that align with its pump portfolio. Dexcom positions G7 as the accuracy leader and pushes deeper into Type-2 populations via pharmacy benefit deals that simplify prescription processes.

Partnerships exemplify the move from devices to ecosystems. Medtronic and Abbott now collaborate on transmitter protocols so hospitals can adopt hybrid device fleets without data silos. Start-ups develop AI coaches that interpret CGM data for weight-loss or athletic performance, broadening competitive dimensions beyond pure hardware.

United States Continuous Glucose Monitoring Industry Leaders

Dexcom Inc.

Medtronic plc

Abbott Laboratories

Senseonics Holdings Inc.

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: FDA cleared Dexcom’s G7 15-Day system, the longest approved wear duration with 8.0% MARD, setting the stage for a H2 2025 commercial launch.

- March 2025: FDA issued a warning letter to Dexcom citing manufacturing control concerns and requiring corrective actions within set timelines.

- August 2024: Abbott and Medtronic entered a global agreement to connect Abbott CGMs with Medtronic insulin pumps, signaling stronger ecosystem interoperability.

- August 2024: Dexcom rolled out Stelo, the first over-the-counter CGM priced at USD 89-99 to target non-insulin users and wellness consumers.

United States Continuous Glucose Monitoring Market Report Scope

Achieving optimal glycemic results can be very difficult without frequent monitoring of blood glucose levels. A continuous glucose monitor tracks blood sugar levels 24 hours a day. It collects readings automatically every five to 15 minutes and detects trends and patterns to provide a complete picture of diabetes. The United States continuous glucose monitoring market is segmented by components and end users. By components, the market is segmented into sensors and durables. The durables include receivers and transmitters. By end user, the market is segmented into hospitals/clinics and home/personal. The report offers the value (USD) for the above segments.

| Sensors |

| Transmitters |

| Receivers |

| Hospitals/Clinics |

| Home/Personal Use |

| Adult |

| Pediatric |

| By Component | Sensors |

| Transmitters | |

| Receivers | |

| By End User | Hospitals/Clinics |

| Home/Personal Use | |

| By Demography | Adult |

| Pediatric |

Key Questions Answered in the Report

How large is the U.S. continuous glucose monitoring market in 2026?

It sits at USD 7,430.15 million and is tracking an 18.23% CAGR toward USD 17,164.69 million by 2031.

Which component leads sales today?

Disposable sensors dominate with an 87.32% share and drive most recurring revenue.

What policy shift is boosting Type-2 patient adoption?

The April 2023 CMS rule that now reimburses CGM for basal-only insulin users expands eligibility to about 1.5 million beneficiaries.

Which demographic segment is growing fastest?

Children and adolescents post a 19.12% CAGR thanks to early intervention programs and improved pediatric insurance coverage.

Page last updated on: