Non-Invasive Glucose Monitoring Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

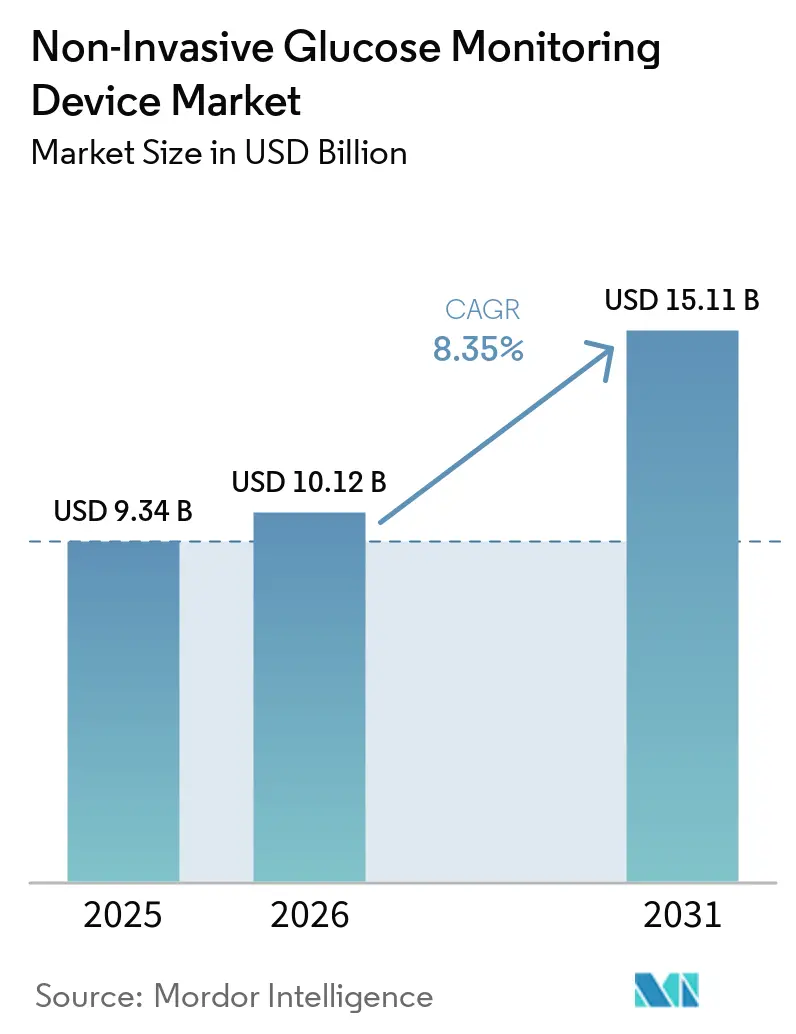

| Market Size (2026) | USD 10.12 Billion |

| Market Size (2031) | USD 15.11 Billion |

| Growth Rate (2026 - 2031) | 8.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

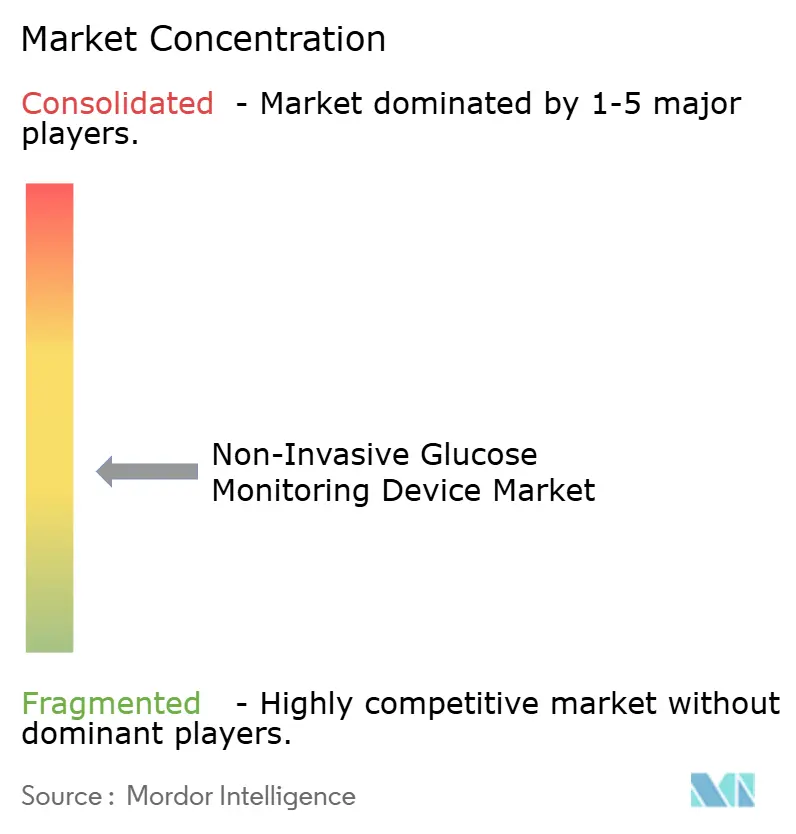

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Non-Invasive Glucose Monitoring Device Market Analysis by Mordor Intelligence

The non-invasive glucose monitoring device market size in 2026 is estimated at USD 10.12 billion, growing from 2025 value of USD 9.34 billion with 2031 projections showing USD 15.11 billion, growing at 8.35% CAGR over 2026-2031. Momentum stems from the collision of diabetes-prevalence pressures [1]International Diabetes Federation, “IDF Diabetes Atlas 10th Edition,” idf.org , rapid photonics miniaturization, and clear regulatory signals that favor needle-free monitoring. Public health spending tied to diabetes is set to top USD 1 trillion by 2030, creating strong economic rationale for payers and providers to shift toward less invasive technologies. Big-tech entrants drive consumer awareness through smartwatch pilots, while established diagnostic firms press ahead with optical accuracy improvements that approach single-digit MARD benchmarks. Capital flows remain robust, with venture rounds above USD 200 million in 2024 underpinning hardware-software convergence and integrated metabolic-data services.

Key Report Takeaways

- By device placement, arm and wrist options led with 39.74% of the non-invasive glucose monitoring device market share in 2025; forefinger solutions are poised for a 9.05% CAGR to 2031.

- By patient age group, adults accounted for 66.58% revenue in 2025, while geriatric demand is forecast to rise at a 9.38% CAGR through 2031.

- By end user, hospitals and clinics held 55.92% of the non-invasive glucose monitoring device market size in 2025; home and personal use is expanding at a 9.29% CAGR to 2031.

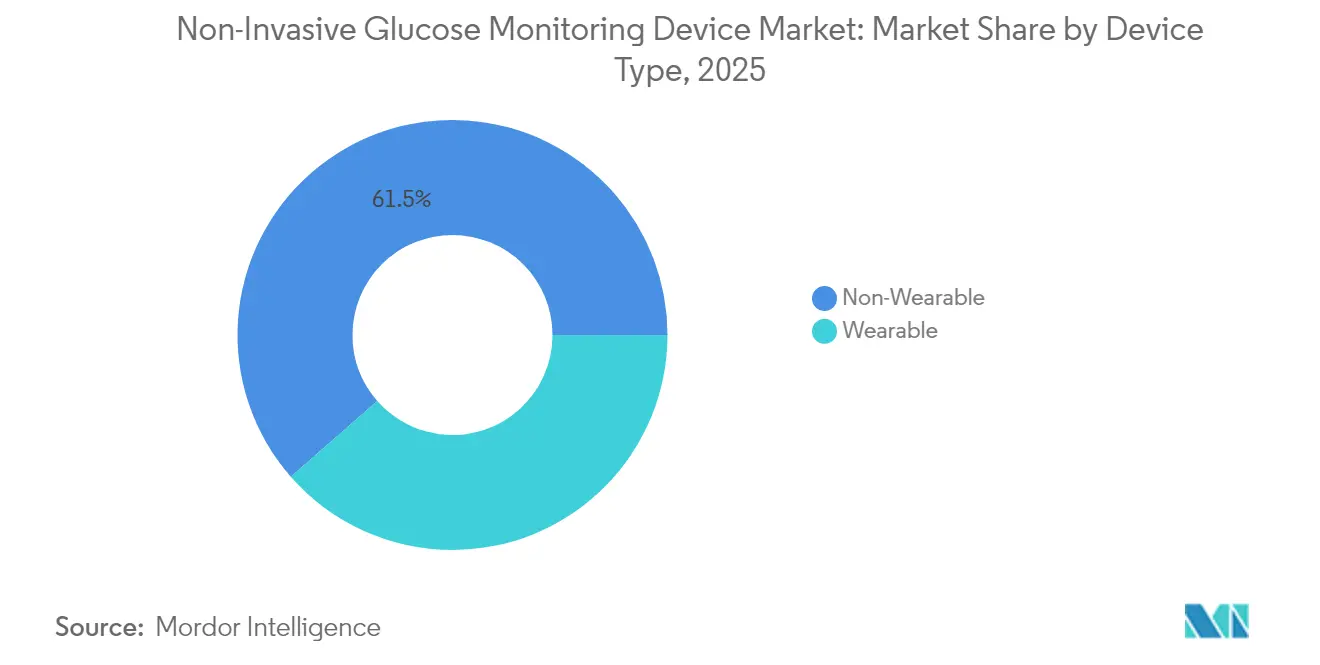

- By device type, non-wearables commanded 61.45% revenue in 2025, yet wearables exhibit the highest forward CAGR of 9.08% through 2031.

- By geography, North America captured 39.98% market share in 2025, whereas Asia-Pacific is tracking the fastest regional CAGR at 9.45% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Non-Invasive Glucose Monitoring Device Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diabetes prevalence & earlier diagnosis | +2.1% | Global with heightened impact in Asia-Pacific and the Middle East | Medium term (2-4 years) |

| Regulatory tailwinds for needle-free monitoring | +1.8% | North America & EU, expanding into Asia-Pacific | Short term (≤ 2 years) |

| Miniaturization of NIR/Raman photonics modules | +1.5% | Global, led by R&D hubs in the US, Germany, Japan | Long term (≥ 4 years) |

| Big-tech integration into smartwatch form factors | +1.3% | North America & EU with spillover to Asia-Pacific | Medium term (2-4 years) |

| Continuous metabolic-data monetisation models | +0.9% | Global, strongest in developed markets | Long term (≥ 4 years) |

| VC funding pivot to non-invasive biosensing start-ups | +0.7% | North America & EU venture ecosystems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence & Earlier Diagnosis

Diabetes cases climbed to 537 million adults in 2021 and are projected to surpass 783 million by 2045. The surge is most acute in emerging economies where lifestyle shifts converge with ageing populations. China’s prevalence alone rose from 7.53% in 2005 to 13.67% in 2023, underlining the urgency for scalable, painless monitoring options [2]Yu-Chang Zhou, "The national and provincial prevalence and non-fatal burdens of diabetes in China from 2005 to 2023 with projections of prevalence to 2050," Military Medical Research, mmrjournal.biomedcentral.com. Academic evidence from the University of Tokyo shows that continuous, non-invasive glucose trends reveal pre-diabetes risk earlier than fasting blood tests, encouraging proactive lifestyle interventions. As screening shifts beyond clinics to pharmacies and workplaces, the non-invasive glucose monitoring device market gains a broader addressable base. Payers view earlier detection as a cost buffer against downstream complications, reinforcing reimbursement prospects.

Regulatory Tailwinds for Needle-Free Monitoring

The US FDA cleared Dexcom’s Stelo as the first over-the-counter continuous glucose monitor in 2024, signalling a friendlier stance toward consumer-grade solutions. Parallel European CE-mark activity around optical systems such as Roche’s AI-enabled Accu-Chek SmartGuide illustrates a harmonising regulatory agenda [3] F. Hoffmann-La Roche Ltd, "Roche receives CE Mark for its AI-enabled continuous glucose monitoring solution," roche.com. Updated guidance on AI-enabled devices clarifies data transparency rules, lowering compliance risk for algorithms that refine optical accuracy. The integrated continuous glucose monitoring (iCGM) product code provides explicit performance targets that non-invasive vendors can benchmark. These frameworks shorten time-to-market and spur strategic alliances between diagnostics leaders and sensor start-ups.

Miniaturization of NIR/Raman Photonics Modules

Photonics laboratories have squeezed mid-infrared detectors to sub-centimetre footprints without active cooling, a technical leap documented by KAIST in 2024. Researchers demonstrated 5 mm sensors powered by coin batteries and Bluetooth, maintaining signal integrity for capillary glucose spectra. Multiple μ-spatially offset Raman spectroscopy trials across 230 participants yielded a 14.6% mean absolute relative difference, with 99.4% of readings inside clinically acceptable grids. Silicon CMOS fabrication brings down unit costs, positioning wearables for mainstream adoption by the decade’s close.

Big-Tech Integration into Smart-Watch Form Factors

Samsung publicly confirmed optical blood-glucose prototypes inside its Galaxy Watch roadmap, framing the feature as the next step in its health-suite expansion. Hamamatsu Photonics unveiled a reference smartwatch platform that exploits phase shifts between oxy- and de-oxyhemoglobin to infer glucose with promising trial data. Dexcom invested USD 75 million in Oura to blend glucose, sleep, and stress metrics, underscoring a shift from single-analyte gadgets to holistic metabolic dashboards. Such integrations broaden consumer appeal and lift recurring-service revenues from data analytics subscriptions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accuracy gaps vs. invasive CGMs | -1.9% | Global, strongest in tightly regulated markets | Medium term (2-4 years) |

| Lengthy multi-site clinical-validation cycles | -1.2% | Global, deepest in FDA/CE environments | Short term (≤ 2 years) |

| High component cost of mid-IR lasers | -0.8% | Global supply chains centred in Asia-Pacific | Long term (≥ 4 years) |

| Data-privacy backlash on cloud analytics | -0.6% | EU & North America, expanding to privacy-focused regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accuracy Gaps vs. Invasive CGMs

Leading invasive CGMs post MARD figures near 8.0%, whereas most non-invasive contenders still register between 11.1% and 18.2%. Comparative assessments place FreeStyle Libre 3 at 8.9% and Dexcom G7 at 8.0% MARD, setting a high bar for optical or radio-frequency solutions. Regulators and clinicians emphasise consensus error grid analysis over single-number MARD, yet payers remain cautious about therapy-adjustment decisions based on broader error margins. Bridging this gap requires enhanced spectral algorithms, multimodal sensing, and larger validation cohorts, all of which extend development timelines and burn rates.

Lengthy Multi-Site Clinical-Validation Cycles

The FDA’s iCGM classification compels extensive datasets that span paediatric, gestational, and hypoglycaemia scenarios. A typical pathway involves 12-18 months of multi-site trials plus up to a year of regulatory review. GlucoTrack’s Brazil study and Know Labs’ ongoing US programme illustrate the capital intensity of meeting these evidence thresholds. Start-ups often rely on bridge financing to navigate this window, granting an advantage to diversified med-tech incumbents with established CRO networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Wearables Rise on Consumer Pull

Non-wearable systems retained 61.45% revenue in 2025, rooted in hospital carts and clinic desktops that permit larger optics and vibration isolation. Yet wearables are racing ahead with a 9.08% CAGR, guided by smartwatch and patch designs that suit round-the-clock data capture. The non-invasive glucose monitoring device market is witnessing chipset integrations that shrink laser drivers to smartwatch motherboards without sacrificing battery life.

Samsung’s and Dexcom’s joint efforts epitomise convergence, while Biolinq channels its USD 100 million Series C into intradermal micro-array biosensors. Desktop platforms still claim premium pricing in endocrinology clinics, but unit growth is tilting decisively toward wrists and upper arms where consumer electronics firms wield distribution clout.

By Device Placement: Arm Dominates, Finger Surges

Arm and wrist deployments commanded 39.74% of the non-invasive glucose monitoring device market share in 2025, owing to prior CGM user familiarity and stable tissue characteristics. Finger-tip modalities are predicted to climb at a 9.05% CAGR, helped by rich capillary beds and seamless smartphone coupling.

Know Labs’ radio-frequency dielectric sensor reached 11.1% MARD on finger measurements across 200 volunteers, indicating progress toward single-digit accuracy. Ear-lobe and thumb sensors serve niche ergonomics, while corneal and breath analyses remain exploratory due to comfort and regulatory concerns. The diversification of sites grants suppliers more design latitude to optimise accuracy, comfort, and aesthetics across user cohorts.

By Patient Age Group: Adult Volume, Geriatric Velocity

Adults generated 66.58% of 2025 sales, reflecting higher diagnosis rates and disposable income, yet geriatric uptake is pacing at a 9.38% CAGR as longevity trends collide with polypharmacy risks. Continuous data streams cut hypoglycaemia episodes by 70% in elderly cohorts during recent trials, bolstering caregiver acceptance.

Voice-led interfaces and larger text displays mitigate dexterity and vision declines, while cloud dashboards allow family oversight of remote seniors. Paediatric adoption is constrained by sensor-size limits and incremental safety evidence requirements, but successful entrants stand to secure long lifecycle value as children transition to adult management programmes.

By End User: Clinical Anchor, Home Shift

Hospitals and clinics held 55.92% of 2025 revenue, underpinned by procurement cycles and EMR integrations. Nonetheless, the home-use channel is staging a structural shift with a 9.29% CAGR to 2031, catalysed by OTC labels and insurer subsidies for self-management. The non-invasive glucose monitoring device market is leveraging telehealth APIs that feed clinician dashboards while preserving patient ownership of raw data.

Ambulatory surgery centres seek non-invasive options to reduce infection risk during peri-operative glucose control. Long-term care homes are piloting optical wristbands to alert staff of nocturnal hypoglycaemia, confirming value beyond the acute care setting.

Geography Analysis

North America accounted for 39.98% of 2025 revenue thanks to favourable reimbursement codes, broad commercial insurance uptake, and early FDA guidance clarity. Device makers enjoy dense clinical-trial networks that accelerate evidence generation, while venture hubs in California and Massachusetts supply scale-up capital. Europe maintains steady adoption as CE-mark frameworks harmonise AI explainability and cybersecurity clauses. National health systems in Germany, France, and the Nordics finance integrated diabetes pathways that embrace needle-free modalities, though budget ceilings temper headline volumes.

Asia-Pacific is the breakout geography, clocking a 9.45% CAGR through 2031 on the back of surging diabetes incidence and manufacturing cost advantages. China’s diabetic population climbed from 92 million in 2010 to an estimated 149 million in 2024, creating a vast potential pool for consumer wearables. Local optical-component suppliers compress bill-of-materials cost structures, giving regional OEMs a pricing edge. South Korean firm i-SENS won European and Japanese approvals for its optical CGM system, exporting design credibility beyond domestic borders. Japan’s depth in photonics R&D, underscored by QCL ring-resonator breakthroughs, sustains technology leadership that suppliers then industrialise in neighbouring fabrication hubs.

Middle East and Africa show early-stage adoption, led by Gulf health-authority pilots that test remote monitoring for expatriate populations with type 2 diabetes. South American growth aligns with local manufacturing incentives in Brazil and Mexico, where regulatory pathways mirror CE-mark dossiers and shorten review cycles. Across these emerging markets, smartphone penetration serves as the distribution spine for app-based visualisations, lowering entry friction for consumers and easing clinician onboarding.

Competitive Landscape

The non-invasive glucose monitoring device market features moderate fragmentation, with legacy CGM giants countered by optical up-starts and big-tech arrivals. Abbott, Dexcom, and Medtronic wield distribution breadth and deep clinical data repositories. They reinforce positions through platform alliances, typified by Abbott’s pacts with Tandem Diabetes Care and Beta Bionics to embed Libre sensors into closed-loop pumps. Dexcom became the first to layer generative AI atop biosensing, promising personalised glucose forecasts as part of G7 enhancements. Such moves raise switching costs by bundling analytics, coaching, and device sales.

Optical specialists including Know Labs and Spiden pursue radio-frequency and multi-spectral Raman modalities respectively, each chasing single-digit MARD milestones. Know Labs amassed a patent trove exceeding 270 filings across dielectric measurement methods, aiming to ring-fence frequency domains for future wearables. Semiconductor houses pair with consumer electronics OEMs to enable native photonics in smartwatches, a path Samsung illustrates through advanced packaging deals with domestic chip foundries. Start-ups without manufacturing heft often elect fab-light models, licensing designs to contract manufacturers in Taiwan and Singapore.

VC confidence remains intact despite technical headwinds, as evidenced by USD 200 million plus deployed into Series B and C rounds in 2024 alone. Investors prize platforms that monetise recurring data services as much as hardware margin. Competitive intensity is expected to rise as AI augmentation blurs hardware differentiation, pushing suppliers to secure ecosystem lock-ins via API exclusivity, insurance partnerships, and cloud compliance badges.

Non-Invasive Glucose Monitoring Device Industry Leaders

-

Abbott

-

Dexcom

-

Medtronics

-

Eversence

-

Nemaura

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Tandem Diabetes Care agreed with Abbott to integrate an automated insulin-delivery platform with Abbott’s forthcoming dual glucose-ketone sensor, extending closed-loop functionality beyond glucose alone.

- May 2025: Sequel Med Tech and Abbott disclosed plans to pair the twist AID system with Abbott’s future glucose-ketone sensor for dual-analyte monitoring.

- May 2025: GlucoTrack secured Australian HREC approval for a clinical study of its continuous blood-glucose monitoring implant, moving the device toward first-in-human evaluation.

- April 2025: Dexcom G7 15 Day gained FDA clearance, lifting wear duration to 15.5 days while posting 8.0% MARD for the tightest accuracy standard in the segment.

Global Non-Invasive Glucose Monitoring Device Market Report Scope

Non-invasive blood glucose monitoring, as its name suggests, pertains to the identification of human blood glucose levels without inflicting harm on human tissues.

The non-invasive glucose monitoring device market is segmented by type (wearable and handled), by end-user (hospitals, clinics, and home care/personal), and by geography (North America, Europe, Asia-Pacific, the Middle East, Africa, and Latin America).

The report offers the value (in USD) and volume (in Units) for the above segments.

| Wearable |

| Non-Wearable |

| Arm and Wrist |

| Ear Lobe |

| Forefinger |

| Thumb |

| Cornea |

| Other Alternate Sites |

| Adults |

| Geriatric |

| Pediatric |

| Hospitals and Clinics |

| Home and Personal Use |

| Ambulatory Surgical Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Malaysia | |

| Indonesia | |

| Thailand | |

| Philippines | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Wearable | |

| Non-Wearable | ||

| By Device Placement | Arm and Wrist | |

| Ear Lobe | ||

| Forefinger | ||

| Thumb | ||

| Cornea | ||

| Other Alternate Sites | ||

| By Patient Age Group | Adults | |

| Geriatric | ||

| Pediatric | ||

| By End User | Hospitals and Clinics | |

| Home and Personal Use | ||

| Ambulatory Surgical Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Malaysia | ||

| Indonesia | ||

| Thailand | ||

| Philippines | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the non-invasive glucose monitoring device market?

The market stands at USD 10.12 billion in 2026 and is forecast to reach USD 15.11 billion by 2031.

Which region is growing the fastest for non-invasive devices?

Asia-Pacific is projected to post the highest CAGR at 9.45% through 2031, driven by rising diabetes prevalence and cost-effective manufacturing capacity.

How accurate are non-invasive monitors compared with invasive CGMs?

Leading non-invasive prototypes report mean absolute relative differences between 11.1% and 18.2%, whereas top invasive CGMs such as Dexcom G7 achieve about 8.0% MARD.

What regulatory developments support needle-free monitoring?

The FDA’s over-the-counter clearance of Dexcom’s Stelo and updated guidance on AI-enabled devices signal streamlined pathways for consumer-grade non-invasive monitors.

Which device type is expected to grow faster, wearables or non-wearables?

Wearables, including smartwatch-based sensors, are forecast to expand at a 9.08% CAGR as photonics miniaturisation and big-tech partnerships enhance usability.

Why are investors still funding non-invasive glucose start-ups despite accuracy hurdles?

Venture capital views the long-term revenue upside of integrated metabolic-data services and the large unmet need for painless monitoring as outweighing near-term technical risks.

Page last updated on: