Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

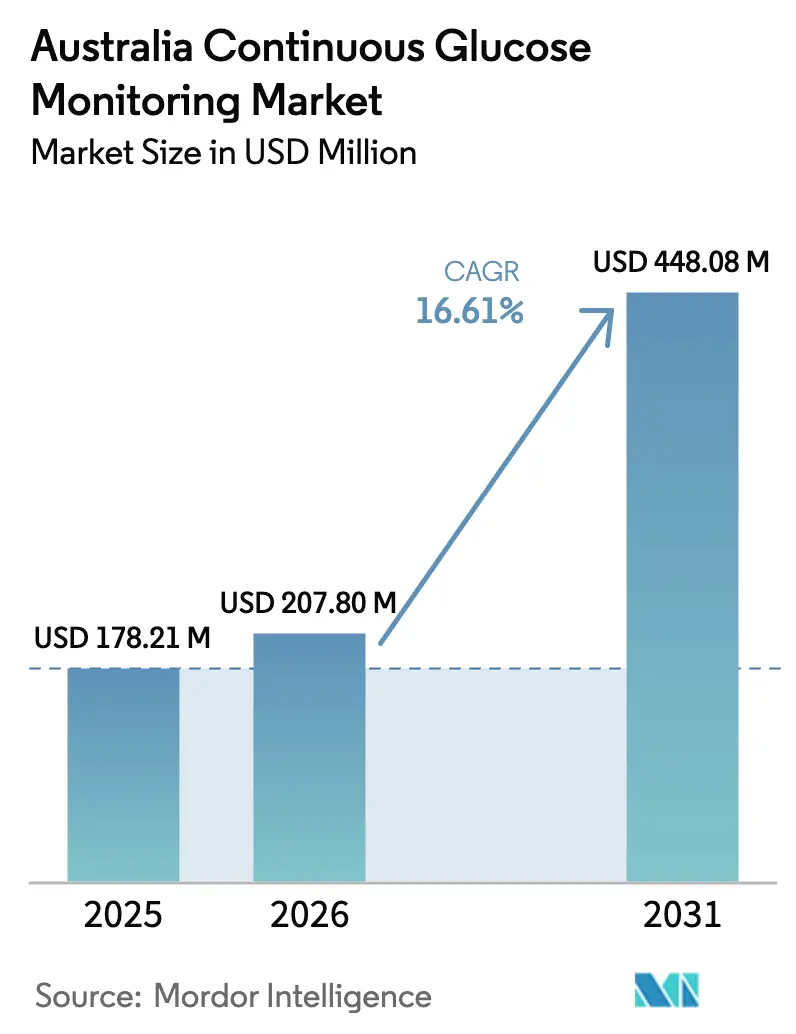

| Base Year Market Size (2025) | USD 178.21 Million |

| Market Size (2026) | USD 207.8 Million |

| Market Size (2031) | USD 448.08 Million |

| Growth Rate (2026 - 2031) | 16.61% CAGR |

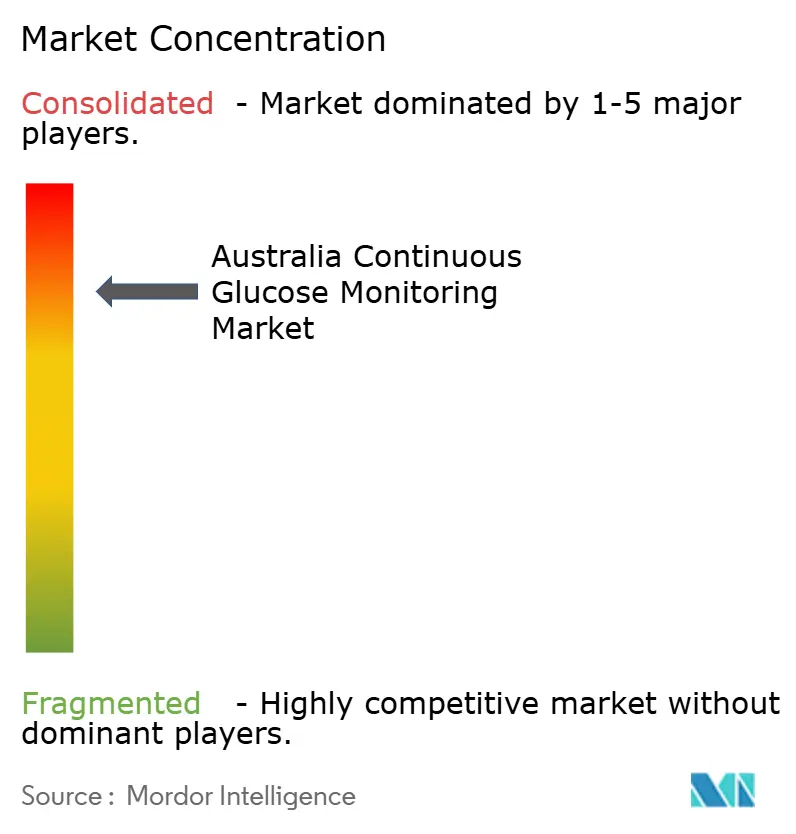

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Continuous Glucose Monitoring Market Analysis by Mordor Intelligence

Australia continuous glucose monitoring market size in 2026 is estimated at USD 207.8 million, growing from 2025 value of USD 178.21 million with 2031 projections showing USD 448.08 million, growing at 16.61% CAGR over 2026-2031. Consistent reimbursement expansion, factory-calibrated sensor innovation, and rising diabetes prevalence are accelerating adoption even faster than earlier forecasts. Larger adult cohorts that recently gained National Diabetes Services Scheme (NDSS) coverage are converting from finger-stick testing, while pediatric uptake remains brisk as caregivers prioritize remote monitoring[1]Source: Diabetes Australia, “CGM Subsidy Expansion,” diabetesaustralia.com.au. Hospital demand is climbing as endocrinology departments standardize inpatient glycemic management on CGM, and hybrid closed-loop insulin systems are creating fresh hardware refresh cycles that lift durable sales. Intensifying competition among Abbott, Dexcom, and Medtronic is encouraging price discipline yet widening device choice, positioning the Australia continuous glucose monitoring market for sustained double-digit growth.

Key Report Takeaways

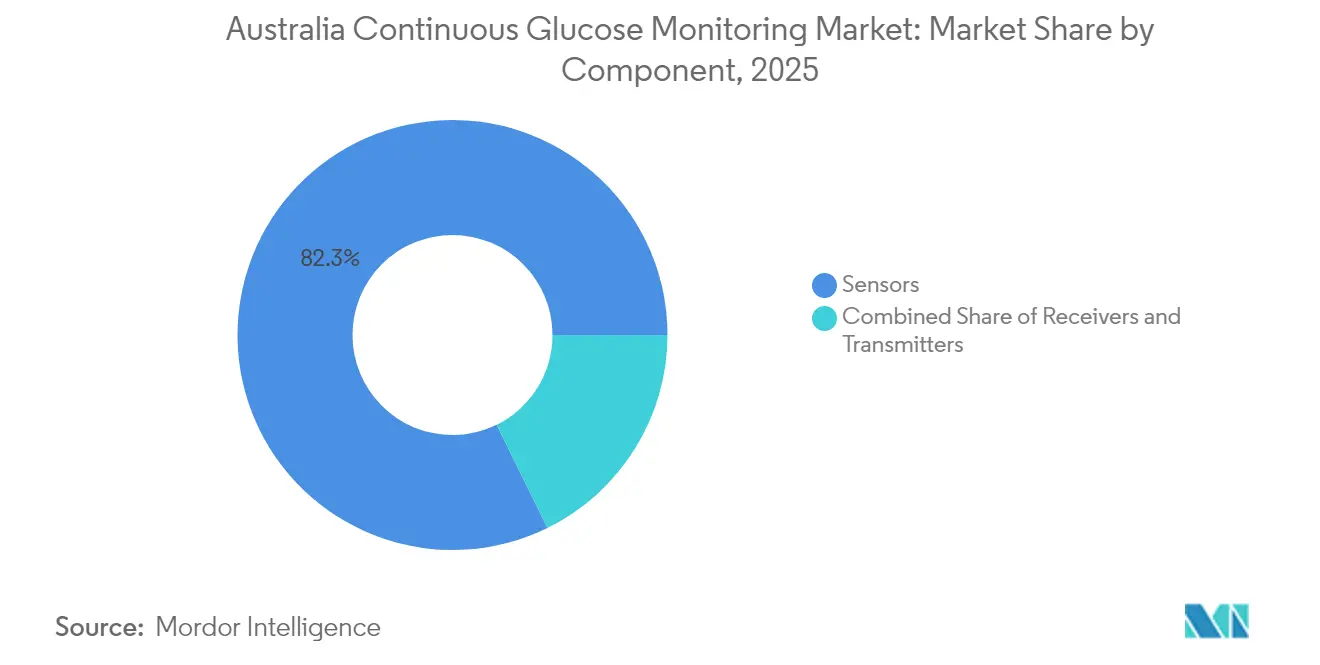

- By component, sensors captured 82.28% of the Australia continuous glucose monitoring market share in 2025, whereas durables are forecast to expand at a 17.05% CAGR to 2031.

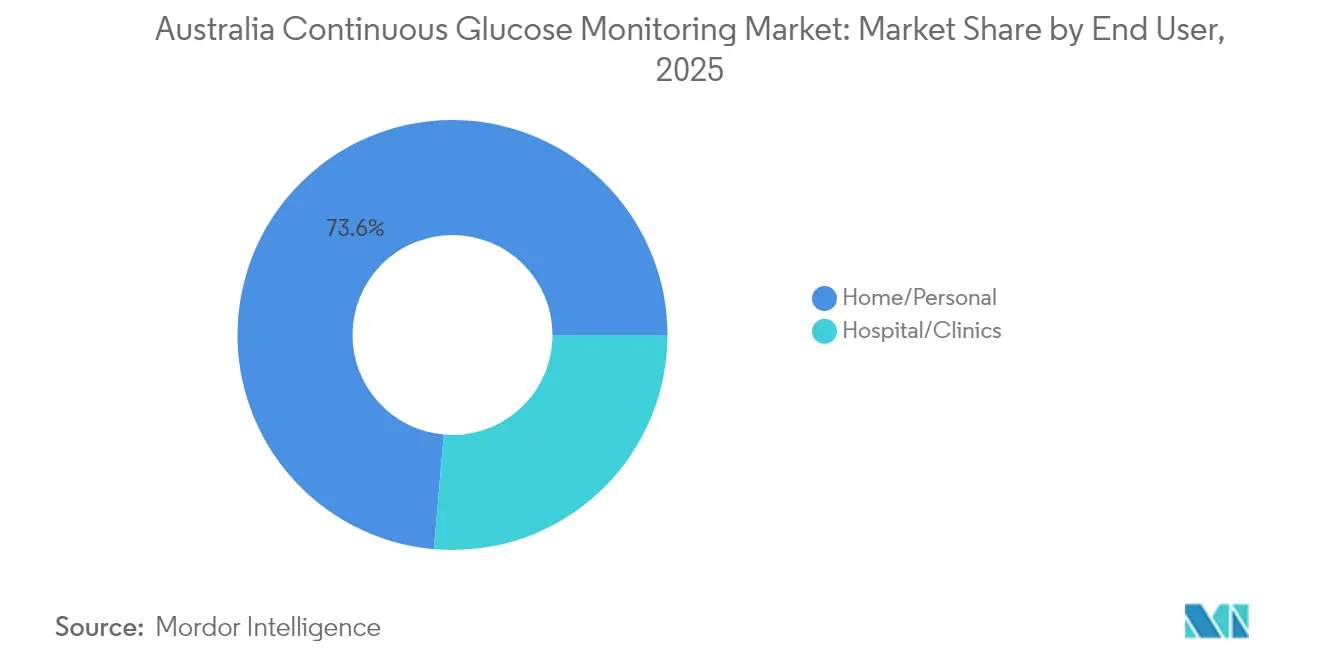

- By end user, home and personal use accounted for 73.62% share of the Australia continuous glucose monitoring market size in 2025, while hospital and clinic deployments are advancing at a 16.89% CAGR through 2031.

- By demography, adults held 64.38% of the installed base in 2025; the pediatric segment is growing fastest with a 16.73% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Continuous Glucose Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |

|---|---|---|---|---|

| Rapidly Increasing Diabetes Prevalence | 3.5% | National, higher in urban and remote Indigenous areas | Long term (≥ 4 years) | |

| Advances in CGM Sensor Technology | 2.8% | National, early use in metropolitan teaching centers | Medium term (2–4 years) | |

| Expansion of NDSS Reimbursement Policies | 4.5% | National, staged by diabetes type | Short term (≤ 2 years) | |

| Integration with Hybrid Closed-Loop Systems | 2.2% | National, urban endocrinology and pediatric clinics | Medium term (2–4 years) | |

| Employer-Sponsored Diabetes Programmes In Mining and Corporate Sector | 1.2% | National, higher in urban areas | Short term (≤ 2 years) | |

| Indigenous-Health Screening Initiatives In Remote Areas | 0.8% | National, increasing in remote areas | Medium term (2–4 years) | |

| Source: Mordor Intelligence | ||||

Rapidly Increasing Diabetes Prevalence

Australia’s diagnosed diabetes population rose to 1.5 million adults in 2024, equal to 6.6% of residents, up from 5.1% a decade earlier. Type 2 diabetes represents 1.2 million of these cases, yet full NDSS CGM subsidies still apply only to 130,000 Type 1 patients, creating a gap that policy makers are addressing. Indigenous Australians face diabetes rates three times the national average, and the Waminda pilot showed that 18 of 25 Aboriginal women achieved glycemic improvement using CGM plus group visits, with 7 attaining remission[2]Source: ABC News, “Aboriginal Women Reverse Type 2 Diabetes,” abc.net.au. Parliamentary committees are therefore recommending subsidy expansion to high-risk insulin-dependent Type 2 and gestational cohorts, a step that could double the eligible patient pool by 2027. Employers in mining and resources are also piloting on-site CGM programs that cut high-risk worker counts by more than half, indicating commercial willingness to fill coverage gaps.

Advances in CGM Sensor Technology

Factory-calibrated sensors with mean absolute relative difference (MARD) below 10% have become the country standard, removing the need for finger-stick confirmation. Abbott’s FreeStyle Libre 3 posts a 7.9% MARD, while Dexcom G7 records 8.2% overall and 8.6% in pediatric users, comfortably inside Therapeutic Goods Administration non-adjunctive dosing criteria. Wear time now extends to 14 days, halving annual sensor counts and supporting adherence. Real-time Bluetooth feeds to smartphones enable predictive alerts and caregiver sharing, features that drive uptake in children and older adults. Medtronic’s Simplera all-in-one disposable sensor, launched globally in 2024, promises easier insertion and lower cost once TGA approval is secured. These advances collectively keep Australia continuous glucose monitoring market growth on a steep trajectory.

Expansion of NDSS Reimbursement Policies

The NDSS expanded coverage in May 2024 to every Type 1 patient, eliminating prior age caps and unlocking roughly 80,000 adults who had self-funded or skipped CGM. Dexcom G7 gained listing in March 2025, followed by Abbott’s Libre 2 Plus in April 2025, increasing product choice and applying price pressure. A parliamentary inquiry has urged further extension to insulin-dependent Type 2, gestational, and pancreatogenic diabetes, potentially adding 200,000 users by 2027 if adopted. Pediatric experience shows that adoption can increase from 5% to 79% within two years once cost barriers are removed, indicating a similar surge in adult adoption is feasible. TGA accuracy standards filter entrants, ensuring that only four qualified platforms currently benefit from an NDSS listing, which sustains product quality but limits supply diversity.

Integration with Hybrid Closed-Loop Insulin Systems

Hybrid closed-loop platforms adjust basal insulin in real time, raising the performance bar for sensors and creating durable demand for compatible transmitters. Insulet’s tubeless Omnipod 5 gained Pharmaceutical Benefits Scheme subsidy in July 2024, targeting tech-savvy Type 1 adults who favor discretion. Medtronic’s MiniMed 780G and Tandem’s t:slim X2 with Control-IQ are widening footprints in urban centers as clinicians report 70–75% time-in-range versus 50–60% for conventional therapy. Despite only 9% of adults using automated delivery in 2024, falling hardware costs and broader reimbursement are expected to accelerate penetration. Each system relies on proprietary sensor-transmitter links, setting off refresh cycles that benefit device makers and underpin premium pricing.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device and Consumable Cost | -1.80% | National, greatest for unsubsidized Type 2 users | Short term (≤ 2 years) |

| Logistics Barriers to Serve Remote Regions | -1.20% | Remote Northern Territory, Western Australia, Far North QLD | Long term (≥ 4 years) |

| Data-Privacy Compliance Costs Under OAIC Regulations | -1.10% | National, greatest for unsubsidized Type 2 users | Short term (≤ 2 years) |

| Logistics Barriers to Serve Remote Regions | -0.80% | Remote Territory | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Device and Consumable Cost

Unsubsidized Australians face annual CGM bills of AUD 3,000–5,000 (USD 1,980–3,300), confining uptake among 1.2 million Type 2 patients to under 5%. Even with NDSS support, transmitters and app fees can top AUD 500 (USD 330) yearly, burdening pensioners and low-income households. Abbott, Dexcom, and Medtronic dominate supply, limiting price competition, while parallel-import rules block cheaper overseas sourcing. Some employers offset costs through wellness schemes, but coverage remains inconsistent. NDSS distribution tenders also force suppliers to maintain temperature-controlled networks across a vast continent, adding 15–20% to logistics expenses and constraining aggressive price cuts.

Logistics Barriers to Serve Remote Regions

Roughly 30% of Australia lies beyond next-day courier service, complicating cold-chain delivery for temperature-sensitive sensors. Shipments to Indigenous communities can take up to 10 days, risking accuracy loss from heat exposure. Limited mobile coverage hampers real-time data transmission, and digital-literacy gaps mean some users lack compatible smartphones. The NDSS tender now mandates 1800 technical helplines and end-to-end order tracking, but few carriers offer cost-effective depot coverage in remote areas. Scaling proven pilots such as Waminda requires trained community health workers and culturally tailored materials, which are still scarce outside major cities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Sensor Dominance Sustains Revenue Leadership

Sensors generated 82.28% of Australia continuous glucose monitoring market revenue in 2025, and the segment is projected to maintain a double-digit trajectory as NDSS eligibility expands and factory-calibrated 14-day wear becomes the norm. Abbott’s Libre 3 and Dexcom G7 both pair smaller footprints with rapid 30-minute warmup, encouraging upgrades that buoy average selling prices even as unit counts decline. Australia continuous glucose monitoring market size for sensors is forecast to climb to USD 365.9 million in 2031, implying a 16.02% CAGR alongside steady subsidy inflows.

Durables—transmitters and receivers—represented the remaining 17.72% in 2025, yet they are forecast to outpace sensors at 17.05% CAGR, reaching USD 82.18 million by 2031 as hybrid closed-loop systems create mandatory hardware refresh cycles. Transmitter evolution toward Bluetooth Low Energy now extends battery life to three months, while smartphone apps are cannibalizing standalone receivers, leaving a niche among seniors and remote users who lack smartphones. Medtronic’s Simplera could disrupt segment boundaries by integrating transmitter elements into the disposable sensor if TGA approval arrives in 2026, potentially reshaping Australia continuous glucose monitoring market share dynamics among incumbents.

By Demography: Pediatric Growth Outstrips Adult Base

Adults constituted 64.38% of the user base in 2025, largely because historical NDSS rules favored children under 21. Nevertheless, pediatric uptake is advancing at 16.73% through 2031, driven by caregiver demand for remote alerts and clinical evidence showing 0.5–0.8% HbA1c reductions and 40% fewer severe hypoglycemia events. Australia continuous glucose monitoring market size for pediatric patients is on track to reach USD 174.58 million by 2031, closing the gap with adult spending.

Adult adoption widened sharply after the 2024 subsidy extension, with smartphone-centric platforms such as Dexcom G7 and Libre 3 resonating among the 18–35 segment. Older adults remain partial to dedicated receivers due to lower smartphone use. Indigenous programs that pair CGM with culturally adapted coaching are demonstrating meaningful HbA1c cuts, hinting at further upside in both adult and pediatric Indigenous cohorts if reimbursements broaden.

By End User: Hospitals Accelerate from a Smaller Base

Home and personal settings produced 73.62% of revenue in 2025 as diabetes self-management dominated purchasing decisions. Australia continuous glucose monitoring market share for hospitals is, however, climbing off a low base, with 16.89% CAGR expected through 2031 as inpatient protocols mandate continuous monitoring for surgical candidates and steroid-treated patients. Royal Melbourne Hospital cut mean length of stay by 1.2 days after integrating CGM dashboards into electronic medical records, illustrating economic payback for institutions.

The home channel benefits from NDSS subsidies that reimburse personal devices but not hospital stock, yet clinics remain critical for onboarding and periodic retraining. Corporate wellness pilots among FIFO workforces represent an emerging hybrid category where employers finance devices but users manage them independently on site, adding nuance to end-user segmentation. As hybrid closed-loop pumps become mainstream, hospitals are expected to serve as initiation hubs even while long-term wear occurs at home, supporting parallel growth across both channels.

Geography Analysis

Eastern seaboard cities—Sydney, Melbourne, and Brisbane—house more than 50% of the nation’s 1.5 million diabetes cases and account for a similar share of CGM revenue thanks to dense endocrinology networks and same-day NDSS pharmacy fulfillment. Urban clinics report waiting lists of six to eight weeks for CGM starts, a backlog that underscores continuing demand momentum. Regional centers such as Newcastle, Wollongong, Geelong, and the Gold Coast leverage telehealth links to metropolitan specialists, sustaining mid-teen growth without proportional specialist headcount.

Remote and very remote areas, covering 30% of land but only 3% of residents, struggle with 5–10-day sensor delivery lags and patchy mobile coverage that compromise real-time alerts. Indigenous prevalence three times higher than the national norm magnifies the public-health imperative. Successful pilots like Waminda in Nowra are prompting state funding for scaled deployments in Alice Springs, Broome, and Cairns, although equipment transport and cultural-competency training remain bottlenecks

Competitive Landscape

Abbott and Dexcom jointly hold more than 60% of Australia continuous glucose monitoring market share, leveraging NDSS listings, broad pharmacy footprints, and aggressive direct-to-consumer education. Abbott emphasizes pharmacy convenience and longer 14-day wear, whereas Dexcom stresses real-time alerts, predictive analytics, and a smaller on-body footprint. Medtronic maintains 15–18% share within the hybrid closed-loop niche through its MiniMed 780G ecosystem paired with Guardian 4 sensors, appealing to tech-oriented Type 1s who value full automation.

Dexcom’s budget-oriented ONE+ launch in 2024 widens the addressable self-funded Type 2 segment and pressures Abbott to diversify beyond Libre 2 Plus and Libre 3. Technology battles focus on sensor accuracy (MARD < 8%), warmup time, smartphone integration, and data-sharing functionality.

Regulatory hurdles remain steep: TGA mandates ISO 15197:2013 accuracy compliance and NDSS tenders require nationwide logistics and call-center support, favoring incumbents with cash to maintain temperature-controlled depots. Medtronic’s Simplera, if listed in 2026, could shift price dynamics by merging transmitter and sensor into a single disposable, challenging the consumables revenue model of competitors.

Australia Continuous Glucose Monitoring Industry Leaders

Abbott Laboratories

Dexcom Inc.

Medtronic plc

Ascensia Diabetes Care Holdings AG

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: FreeStyle Libre 2 Plus Continuous Glucose Monitoring (CGM) sensors subsidised through the National Diabetes Services Scheme.

- March 2025: Dexcom G7 secured NDSS approval, introducing a 10-day wear sensor with 30-minute warmup and full smartphone integration.

- February 2025: Waminda trial reported 30% clinical remission among Aboriginal women using CGM plus group visits.

Australia Continuous Glucose Monitoring Market Report Scope

Continuous glucose monitoring automatically monitors blood sugar levels throughout the day and at night. One can quickly determine their blood sugar level at any moment. They can examine their glucose variations over several hours or days to spot trends. They can manage their diet, exercise, and medications better throughout the day if they can see their glucose levels in real-time. The Australian continuous glucose monitoring devices market is segmented by individual components, demography, and end users. The report offers the value (USD) for the above segments.

By Component

| Sensors |

| Transmitters |

| Receivers |

By End User

| Hospitals / Clinics |

| Home / Personal |

By Demography

| Adult |

| Pediatric |

| By Component | Sensors |

| Transmitters | |

| Receivers | |

| By End User | Hospitals / Clinics |

| Home / Personal | |

| By Demography | Adult |

| Pediatric |

Key Questions Answered in the Report

How fast is the Australia continuous glucose monitoring market expected to grow to 2031?

Value is projected to expand from USD 178.21 million in 2025 to USD 448.08 million by 2031, delivering a 16.61% CAGR.

Which component brings in the most revenue?

Sensors deliver 82.28% of current revenue because they are consumable items replaced every 14 days.

Why is pediatric adoption rising quicker than adult adoption?

Caregiver demand for real-time alerts and evidence of lower HbA1c and hypoglycemia drives a 16.73% pediatric CAGR versus 16.42% for adults.

What limits CGM penetration in remote Indigenous communities?

Delivery delays, temperature-controlled shipping, patchy mobile coverage, and limited digital literacy constrain uptake to below 2%.

Which hybrid closed-loop system is gaining reimbursed traction?

Insulet’s tubeless Omnipod 5, subsidized since July 2024, is popular among younger Type 1 adults seeking discreet wearables.

Page last updated on: