Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 31.61 Billion |

| Market Size (2031) | USD 51.26 Billion |

| Growth Rate (2026 - 2031) | 10.15% CAGR |

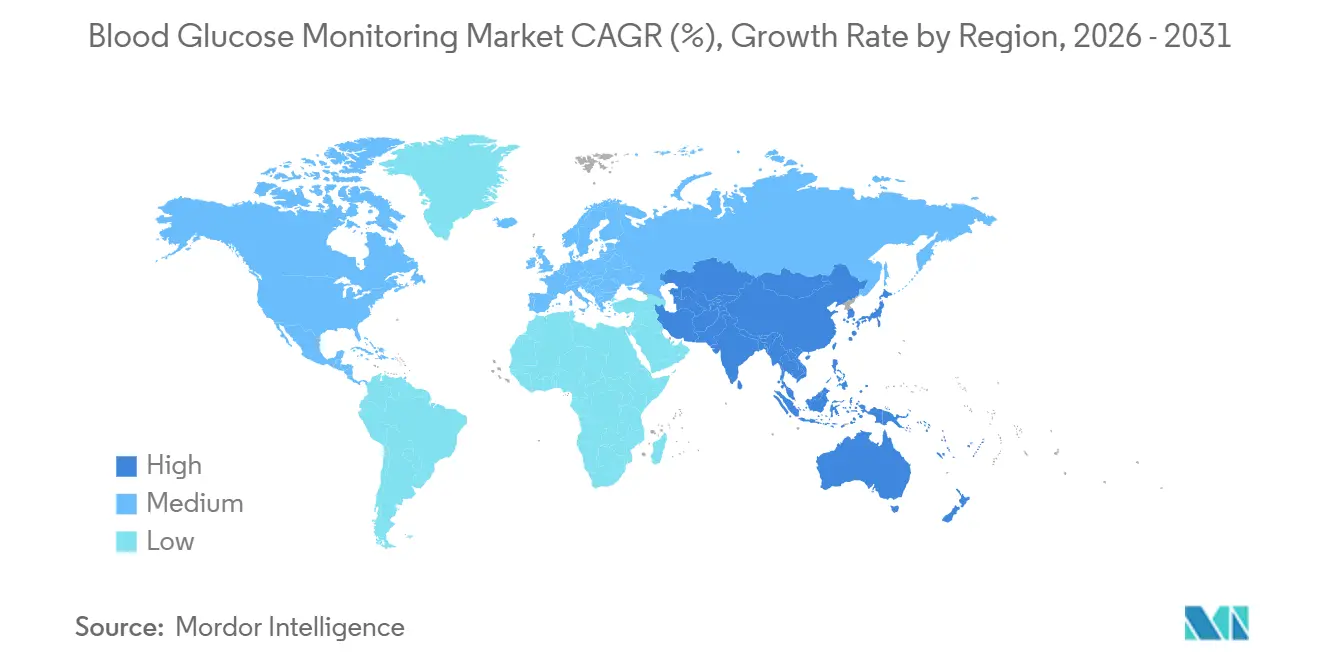

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Glucose Monitoring Market Analysis by Mordor Intelligence

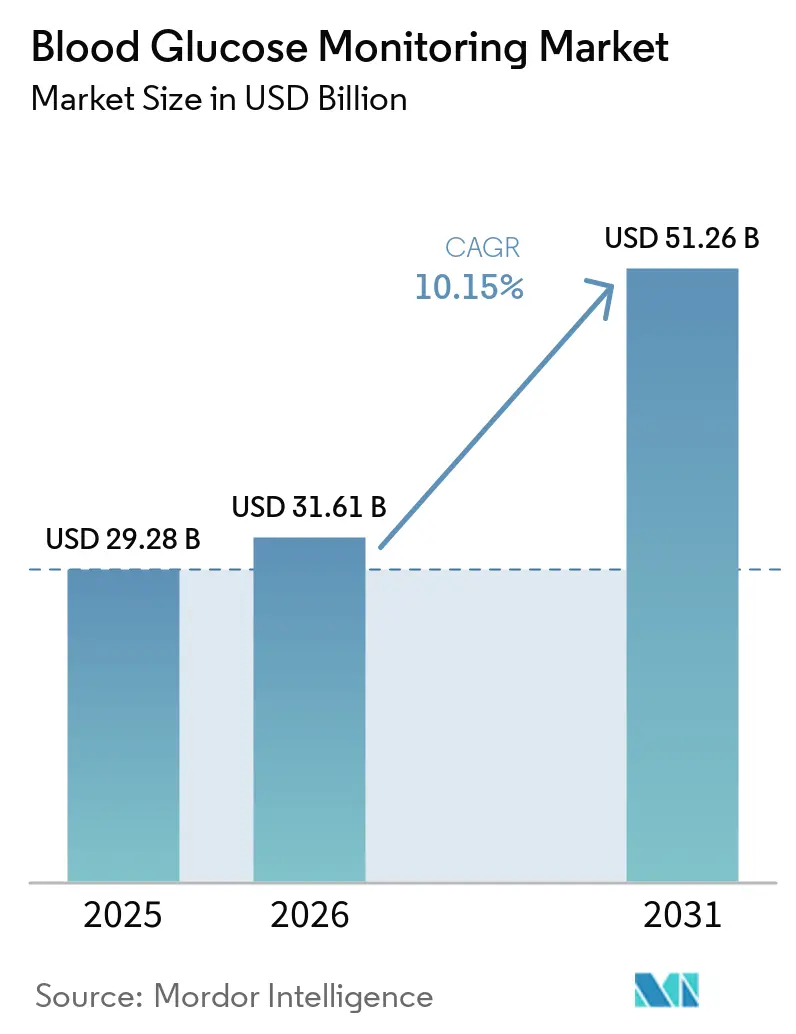

The Blood Glucose Monitoring Market size is projected to be USD 29.28 billion in 2025, USD 31.61 billion in 2026, and reach USD 51.26 billion by 2031, growing at a CAGR of 10.15% from 2026 to 2031.

Expanding reimbursement for continuous glucose monitoring (CGM), miniaturization of wearable sensors, and data integration with digital therapeutics underpin revenue acceleration even as self-monitoring blood glucose (SMBG) consumables face price compression. CGM adoption is rising fastest in North America and urban Asia-Pacific, helped by Medicare’s 2024 coverage expansion and national screening programs in China that enlarge the diagnosed patient pool. Home-care uptake benefits from remote patient monitoring codes that monetize connected devices and reduce follow-up clinic visits. Meanwhile, non-invasive platforms are still pre-commercial but attract outsized R&D spending because factory-calibrated sensors promise friction-free monitoring once regulatory hurdles are cleared. Competitive intensity continues to build as Abbott, Dexcom, and Medtronic layer glucose data into behavioral coaching engines that differentiate on actionable insights rather than mere accuracy.

Key Report Takeaways

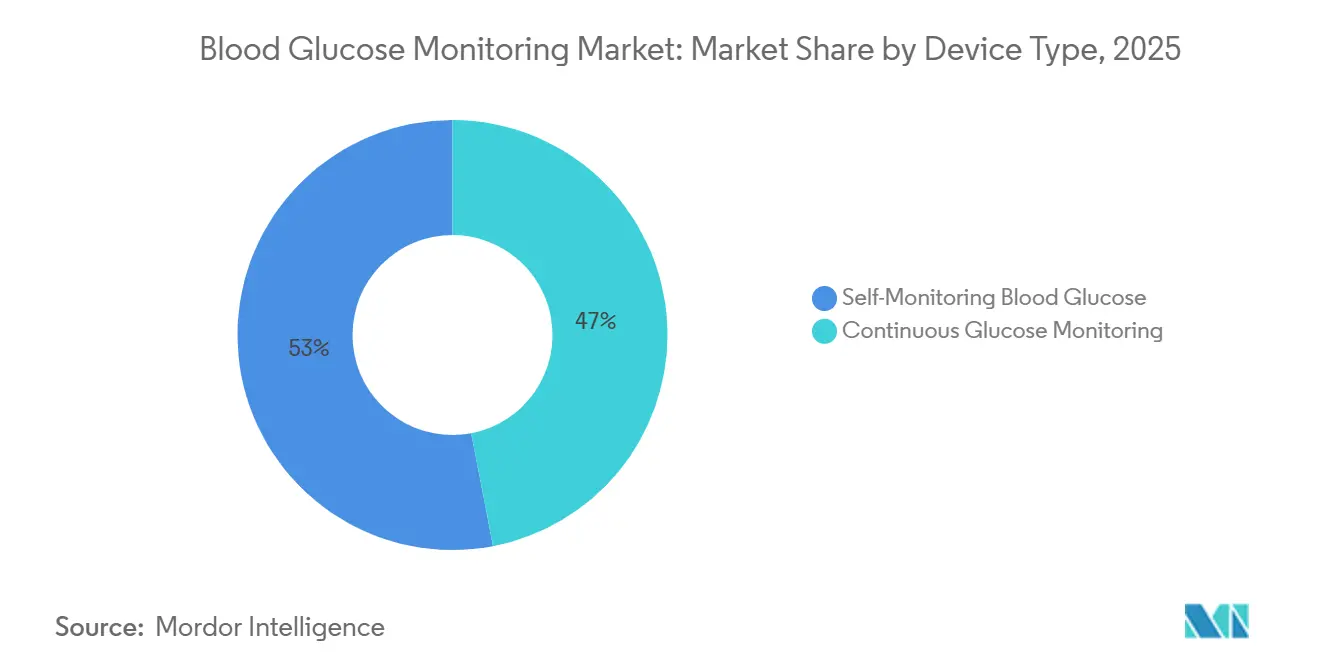

- By device, SMBG retained 53.01% revenue share in 2025, while CGM is expanding at a 15.09% CAGR to 2031.

- By end user, home-care settings commanded 59.10% of the blood glucose monitoring market share in 2025, and are advancing at a 11.21% CAGR through 2031.

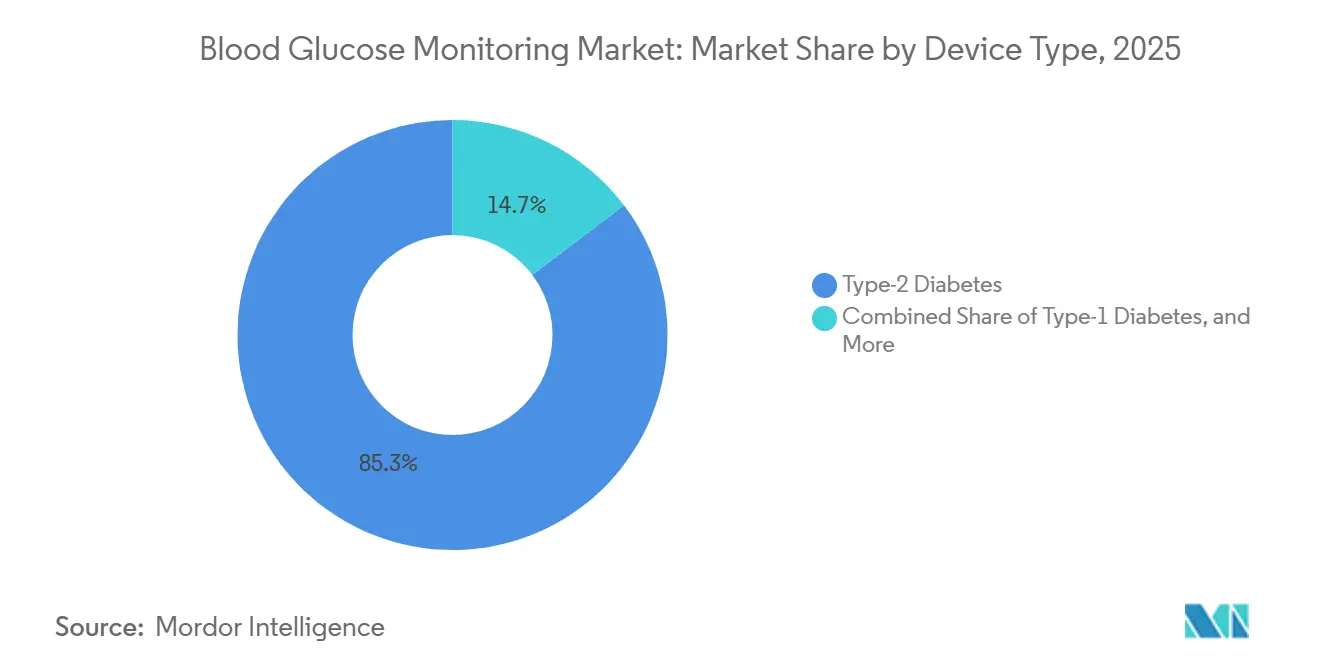

- By patient type, Type 2 diabetes accounted for 85.30% revenue share in 2025, and is projected to register a 10.34% CAGR to 2031.

- By distribution channel, retail pharmacies held 54.93% of 2025 revenue; online platforms are accelerating at a 11.71% CAGR as direct-to-consumer models displace pharmacies.

- By geography, North America captured 41.96% of revenue in 2025, and Asia-Pacific is anticipated to post the fastest regional growth at a 8.77% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Blood Glucose Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating shift from intermittent SMBG to continuous & connected glucose monitoring | +2.1% | Global, led by North America & Europe | Medium term (2-4 years) |

| Rapid expansion of diabetes prevalence and earlier screening in emerging economies | +1.8% | China, India, Middle East & Africa | Long term (≥ 4 years) |

| Miniaturization & wearable sensor innovations enhancing user convenience | +1.5% | Global, R&D hubs in U.S. & EU | Medium term (2-4 years) |

| Integration of glucose data into digital therapeutics & remote patient monitoring | +1.3% | U.S., EU, Japan, Australia | Short term (≤ 2 years) |

| Strategic pharma–med-tech–big-tech collaborations for end-to-end platforms | +0.9% | U.S. & Europe | Medium term (2-4 years) |

| Multi-payer alignment toward outcomes-based reimbursement | +0.8% | U.S., EU, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift From Intermittent SMBG to Continuous & Connected Glucose Monitoring

CGM adoption is accelerating because early initiation lowers long-term hypoglycemia events and streamlines insulin titration protocols. Pediatric Type 1 cohorts in the United Kingdom reached 95% CGM uptake within 36 months of diagnosis by 2024, illustrating how national guidelines can redefine standard of care[1]Addala et al., “Continuous Glucose Monitoring Access in Young Children,” BMJ Open Diabetes Research & Care, bmj.com. Dexcom’s 2024 direct integration with Apple Watch eliminates a separate receiver and delivers real-time alerts to 100 million users, embedding glucose insights into daily routines. Medicare’s 2024 decision to reimburse CGM for insulin-using Type 2 patients widened the U.S. addressable base by 3.5 million beneficiaries. However, SMBG incumbents face commoditization: generic strips priced below USD 0.20 now dominate tenders in Brazil and India, eroding branded margins. The migration therefore rewards firms with sensor portfolios and data-driven service layers while punishing legacy strip pure-plays.

Rapid Expansion of Diabetes Prevalence and Earlier Screening in Emerging Economies

Global diabetes prevalence hit 828 million adults in 2024, quadrupling since 1990 and leaving 445 million undiagnosed. China’s 140 million diagnosed cases and India’s 101 million patients galvanize community-based screening and create demand for affordable monitoring solutions[2]National Health Commission of China, “Diabetes Prevention and Control,” nhc.gov.cn. The Indian Council of Medical Research’s 2024 guidelines now advise glucose testing for all adults over 30 with one metabolic risk factor, bringing millions into the monitored population. Gulf Cooperation Council states show the world’s highest age-adjusted prevalence and are digitizing registries to track adherence, bolstering CGM volumes despite oil-linked budget swings. Still, affordability gaps persist: a Brazilian cost-effectiveness study found that FreeStyle Libre reduced severe hypoglycemia by 43% but cost more than annual per-capita health spending in 18 of 27 states.

Miniaturization & Wearable Sensor Innovations Enhancing User Convenience

Organic electrochemical transistors (OECTs) and microneedle arrays are shrinking sensor footprints and extending wear time. OECT-based prototypes delivered sub-5-second response times in 2024 with electrodes one-third the size of current enzymatic designs. Biolinq secured an FDA Investigational Device Exemption to study a 180-day intradermal microsensor that promises six-times longer wear versus today’s subcutaneous CGMs. Japan’s Diabetes Society created reimbursement codes for intermittently scanned CGM in 2024, signaling regulator comfort with non-continuous data streams for selected patients. A mid-infrared optoacoustic platform achieved clinical-grade accuracy without skin penetration in a 200-patient trial in 2024, yet commercialization awaits larger multicenter validations. These advances improve comfort and discretion but also fragment standards as proprietary algorithms proliferate.

Integration of Glucose Data Into Digital Therapeutics & Remote Patient Monitoring

CGM data now power behavioral coaching, insulin automation, and multi-biomarker analytics. Dexcom invested USD 75 million in Oura to correlate glucose excursions with sleep and stress metrics captured by the ring-based wearable, aiming to personalize lifestyle nudges. Glooko’s 2024 integration of Hedia’s insulin calculator delivers dose recommendations based on CGM trends, carb intake, and activity, thereby moving beyond retrospective dashboards. Medtronic’s MiniMed 780G adjusts basal insulin every five minutes and accounted for a growing share of its diabetes revenue in 2024 as European payers endorsed hybrid closed-loop systems. Updated FDA cybersecurity guidance in 2024 obliges vendors to patch vulnerabilities within 30 days, elevating the compliance hurdle for small entrants. CMS meanwhile pays physicians to review CGM data under new remote patient monitoring codes, underwriting permanent connectivity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persisting affordability gap for CGM devices in low-income segments | -1.2% | APAC, Latin America, Sub-Saharan Africa | Long term (≥ 4 years) |

| Competitive price compression in SMBG consumables from generic strip proliferation | -0.9% | Global, acute in APAC & Latin America | Short term (≤ 2 years) |

| Interoperability & cybersecurity concerns hindering device–app data exchange | -0.7% | U.S., EU, Japan | Medium term (2-4 years) |

| Stringent evidence requirements for factory-calibrated non-invasive sensors | -0.6% | U.S., EU, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persisting Affordability Gap for CGM Devices in Low-Income Segments

CGM systems typically cost USD 1,200–3,000 annually, well above median household incomes in India, Brazil, and much of Africa. Brazil’s Unified Health System pays only for strips, leaving Libre adoption to private-pay elites despite a 43% reduction in severe hypoglycemia demonstrated in a 2023 study. India’s public hospitals stock sensors in fewer than 2% of facilities, limiting access despite updated ICMR guidelines that endorse CGM for high-risk patients. China caps reimbursement at 50%, and rural uptake lags urban centers. Abbott introduced a lower-cost 10-day Libre at USD 30 in India in 2024, yet demand remains concentrated in metropolitan private clinics. These economics sustain SMBG strip demand priced below USD 0.30 and lock many patients into fingerstick routines.

Competitive Price Compression in SMBG Consumables From Generic Strip Proliferation

Generic strip makers in China and India have driven landed prices below USD 0.20, eroding Roche and LifeScan margins and forcing incumbents to add value through digital coaching bundles. Brazil’s procurement data show generics at 68% volume in 2024, underscoring price-first purchasing by budget-strained municipalities. In Africa and Southeast Asia, 90% of diabetes supplies are still paid out-of-pocket, so unit price dictates brand choice. Some generics sidestep ISO 15197:2013 certification, deepening the price gulf. The resulting squeeze cements a two-tier structure: value SMBG for cash-pay populations and premium CGM for insured cohorts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device: CGM Sensors Capture Innovation Premium

SMBG accounted for 53.01% of the blood glucose monitoring market in 2025, reflecting an installed base of more than 200 million glucometer users. However, CGM drives value creation; FreeStyle Libre 3 sensors retail for USD 70 per 14 days in the United States, and Dexcom G7 integrates directly with Apple Watch, justifying premium pricing through ecosystem synergies. Intellectual property now centers on algorithms, adhesives, and miniaturized electronics rather than strip chemistry, further tilting R&D budgets to CGM.

CGM’s 15.09% forecast CAGR raises its slice of blood glucose monitoring market size each year, while SMBG revenues flatten under generic pressure. Transmitters are disappearing as smartphone displays absorb that function, lowering hardware bills yet boosting app stickiness. Integrated pump-CGM loops like Medtronic’s MiniMed 780G automate insulin every five minutes and widen clinical distance from fingerstick-driven titration. Pre-commercial non-invasive prototypes garner venture funding but face an uncertain timeline to displace invasive incumbents entrenched behind strong reimbursement walls.

By End User: Home-Care Adoption Outpaces Institutional Growth

Hospitals and clinics held 31.45% revenue share in 2025 thanks to point-of-care testing mandates, but home-care settings held 59.10% revenue share and will post a 11.21% CAGR through 2031 as remote monitoring codes accelerate connected device deployment. The shift elevates blood glucose monitoring market share for consumer-centric brands and platforms that provide logistics, onboarding, and virtual coaching.

Hybrid closed-loop systems distributed by the U.K.’s NHS are reducing clinic visits, reinforcing the behavioral shift toward at-home management. Diagnostic laboratories lose relevance as CGM makes quarterly A1c draws less critical. China’s community health centers and India’s telemedicine rules further decentralize monitoring, favoring vendors with direct-to-consumer logistics capacity and cloud dashboards.

By Patient Type: Type 2 Dominance Masks Type 1 Innovation

Type 2 diabetes generated 85.30% of 2025 revenue but spends less per patient; many users opt for intermittent CGM or remain on strips, muting revenue per capita. Type 1 cohorts, though smaller, drive sensor innovation and premium pricing as hybrid closed loops become standard in pediatric populations.

Medicare’s 2024 decision doubled the addressable Type 2 CGM pool, yet manufacturers will still rely on Type 1 patients for early adoption of implantable and closed-loop solutions. Gestational diabetes, while a niche, is gaining CGM support after a 2024 Lancet trial showed 29% fewer neonatal hypoglycemia events versus SMBG.

By Distribution Channel: Online Platforms Disrupt Traditional Pharmacy Networks

Institutional sales represented 58.13% revenue in 2025, yet online channels are scaling at 17.51% CAGR as manufacturers capture full retail margins. Dexcom sells its OTC Stelo exclusively online, while Abbott India offers subscription deliveries that guarantee sensor continuity.

Pharmacies respond by bundling coaching or accepting margin erosion, and some payers steer patients to e-commerce for lower acquisition costs. In markets with limited internet penetration or counterfeit concerns, retail outlets remain critical, sustaining a hybrid channel mix.

Geography Analysis

North America retained 41.96% of global revenue in 2025 on the back of Medicare’s CGM expansion and high private-insurance penetration. U.S. uptake is approaching saturation in Type 1 cohorts, so incremental growth hinges on wider Type 2 coverage and employer wellness programs. Canada added Libre for all Type 1 patients in 2024, boosting sensor volumes in Ontario, Alberta, and British Columbia. Mexico’s 16% adult prevalence presents scale, yet affordability constrains CGM to private urban clinics.

Asia-Pacific is forecast to deliver a 12.75% CAGR, propelled by China’s 140 million diagnosed cases and India’s growing reimbursement pilots. China’s reimbursement covers only half the sensor cost, limiting rural penetration but driving urban growth. Japan formalized intermittently scanned CGM codes in 2024, sparking rapid uptake among elderly Type 2 patients. Australia’s Pharmaceutical Benefits Scheme now subsidizes CGM for intensive Type 2 regimens, trimming hospital days by 30%.

Europe shows mature penetration but keeps expanding as Germany funds CGM for insulin-intensive Type 2 cases and the United Kingdom mandates hybrid closed-loop systems. Prevalence in the Middle East is highest globally; Saudi Arabia’s digital registry seeks to improve adherence and capture outcomes. Latin America faces affordability hurdles: Brazil procures generic strips at USD 0.18 and CGM penetration remains under 5% outside private urban hospitals.

Competitive Landscape

Abbott, Dexcom, and Medtronic dominate CGM, while SMBG remains fragmented among Asian generic strip producers. FreeStyle Libre’s installed base topped 5 million by 2024, supported by factory calibration and direct-to-consumer logistics. Dexcom hinges its differentiation on real-time alerts and sleep-glucose analytics via its Oura partnership. Medtronic’s MiniMed 780G rides regulatory endorsements such as the NHS hybrid closed-loop rollout to cement pump-CGM leadership.

Roche and LifeScan combat strip commoditization with digital coaching bundles, yet generic prices undercut branded offerings by 30–40%[3]Roche, “Half-Year Report 2024,” roche.com. White-space innovations include implantable microsensors: Biolinq’s 180-day probe is in pivotal trials, while Senseonics’ Eversense seeks broader reimbursement. Tech majors add competitive heat; Apple’s HealthKit integration grants seamless user experience, intensifying lock-in risks for smaller app vendors. FDA cybersecurity rules favor well-resourced incumbents that can document software bill-of-materials and rapidly deploy patches.

Blood Glucose Monitoring Industry Leaders

Medtronic PLC

Dexcom Inc.

LifeScan Inc.

Abbott Laboratories (Diabetes Care)

F. Hoffmann-La Roche Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: IIT Madras researchers patented a minimally invasive, cost-effective glucose monitor aimed at long-term affordability for low-income populations.

- September 2025: Roche received CE Mark for Accu-Chek SmartGuide Continuous Glucose Monitoring and mySugr app integration, offering unified diabetes management.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the global blood glucose-monitoring market as all invasive self-monitoring blood glucose meters, test strips, lancets, and continuous glucose-monitoring (CGM) systems, including sensors, transmitters, and receivers that are sold for personal or clinical diabetes management. We treat standalone smartphone-enabled readers and integrated pump-CGM combos as part of the same revenue pool to keep a single, user-centric market view.

Scope Exclusions: Disposable syringes, insulin pumps, smart pens, and professional laboratory analyzers are left out, ensuring our numbers focus purely on monitoring devices.

Segmentation Overview

- By Device

- Self-Monitoring Blood Glucose

- Glucometers

- Test Strips

- Lancets & Lancing Devices

- Continuous Glucose Monitoring

- Sensors

- Transmitters & Receivers

- Self-Monitoring Blood Glucose

- By End User

- Hospitals & Clinics

- Homecare Settings

- Diagnostic Laboratories

- By Patient Type

- Type-1 Diabetes

- Type-2 Diabetes

- Gestational & Other Types

- By Distribution Channel

- Institutional Sales

- Retail Pharmacies

- Online Sales

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Our team interviews endocrinologists, diabetes nurses, procurement managers at hospital groups, and distributors across North America, Europe, and Asia-Pacific. Conversations clarify real-world sensor replacement rates, average selling prices, and uptake barriers that are rarely visible in public statistics.

Desk Research

Mordor analysts draw foundational figures from respected, open data sets such as the International Diabetes Federation Atlas, WHO Global Health Observatory, U.S. CDC National Diabetes Statistics, Eurostat trade codes for HS 902780, and filings from publicly listed device makers. Supplementary context comes from peer-reviewed journals, regional diabetes associations, and customs shipment trackers.

We also access paid databases, D&B Hoovers for company revenues and Dow Jones Factiva for deal flow, to confirm pricing shifts, channel mix, and regional launch timing. These sources, together with many others not exhaustively listed here, supply the building blocks for sizing and trend validation.

Market-Sizing & Forecasting

A top-down prevalence-to-treated pool assessment is first run using diagnosed diabetes numbers, test-strip usage norms, and CGM penetration ratios. Results are cross-checked with selective bottom-up roll-ups of manufacturer revenues and channel checks to fine-tune totals. Key variables include: a) diagnosed adult diabetes population, b) median daily strip tests per patient, c) CGM sensor wear days, d) average selling price erosion, e) regional reimbursement coverage, and f) unit shipment growth in emerging economies. Forecasts rely on multivariate regression linked to diabetes incidence, per-capita health spend, and sensor cost curves, producing a 2025-2030 CAGR that aligns with expert consensus. Assumption gaps in bottom-up data are bridged using weighted regional proxies and sensitivity ranges.

Data Validation & Update Cycle

Every quarter, analysts run variance checks between model outputs and fresh shipment, trade, and hospital-purchase signals; anomalies trigger re-contact with sources before sign-off. The report is fully refreshed each year, and clients receive interim updates after major regulatory or technology events.

Why Mordor's Blood Glucose Monitoring Baseline Commands Reliability

Published estimates often diverge because firms choose different device baskets, price assumptions, and refresh cadences.

That variety can confuse planners.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 24.56 B (2025) | Mordor Intelligence | - |

| USD 18.03 B (2025) | Global Consultancy A | Excludes lancets and combo pump-CGM units; applies flat ASPs |

| USD 17.20 B (2025) | Trade Journal B | Relies on 2022 diabetes prevalence and omits high-growth Asian markets |

The comparison shows that, while other publishers present useful snapshots, Mordor's disciplined scope definition, input breadth, and yearly update cadence give decision-makers a balanced, transparent baseline they can trace back to clearly stated variables and repeatable steps.

Key Questions Answered in the Report

How large is the blood glucose monitoring market in 2026 and what is its CAGR through 2031?

The blood glucose monitoring market size is USD 31.61 billion in 2026 and is projected to grow at a 10.15% CAGR to reach USD 51.26 billion by 2031.

Which device category is expanding fastest?

Continuous glucose monitoring is growing at a 15.09% CAGR, outpacing SMBG as reimbursement broadens and sensor prices fall.

What share do hospitals and clinics hold versus home care?

Hospitals and clinics held 31.45% of 2025 revenue, while home-care settings held 59.10% market share and are advancing at a 11.21% CAGR on the strength of remote monitoring codes.

Which region offers the highest growth potential?

Asia-Pacific is forecast to register a 12.75% CAGR through 2031, propelled by policy shifts in China, India, Japan, and Australia.

How are payers influencing CGM adoption?

Medicare and private insurers are tying payment to clinical outcomes, automatically approving CGM for high-risk patients and expanding coverage for insulin-using Type 2 cohorts.

What innovations could reshape monitoring over the next five years?

Implantable 180-day sensors and non-invasive optical platforms are in advanced trials and could reduce wear fatigue and eliminate fingersticks once regulatory approvals are secured.

Page last updated on: