Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

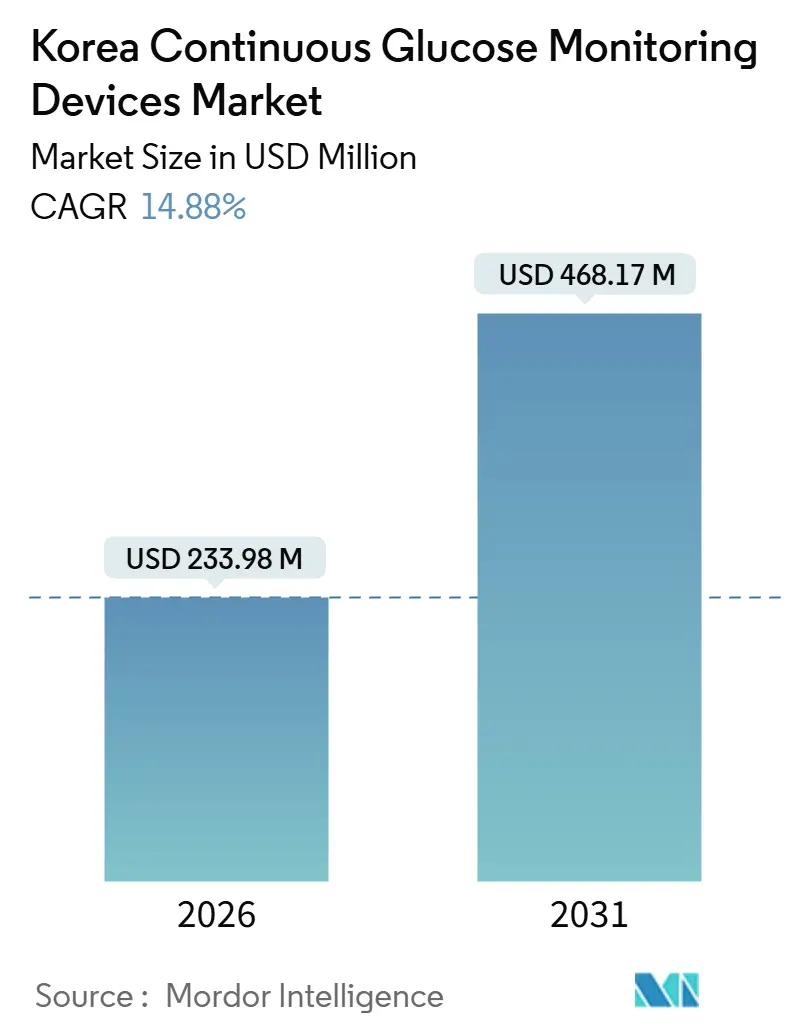

| Market Size (2026) | USD 233.98 Million |

| Market Size (2031) | USD 468.17 Million |

| Growth Rate (2026 - 2031) | 14.88% CAGR |

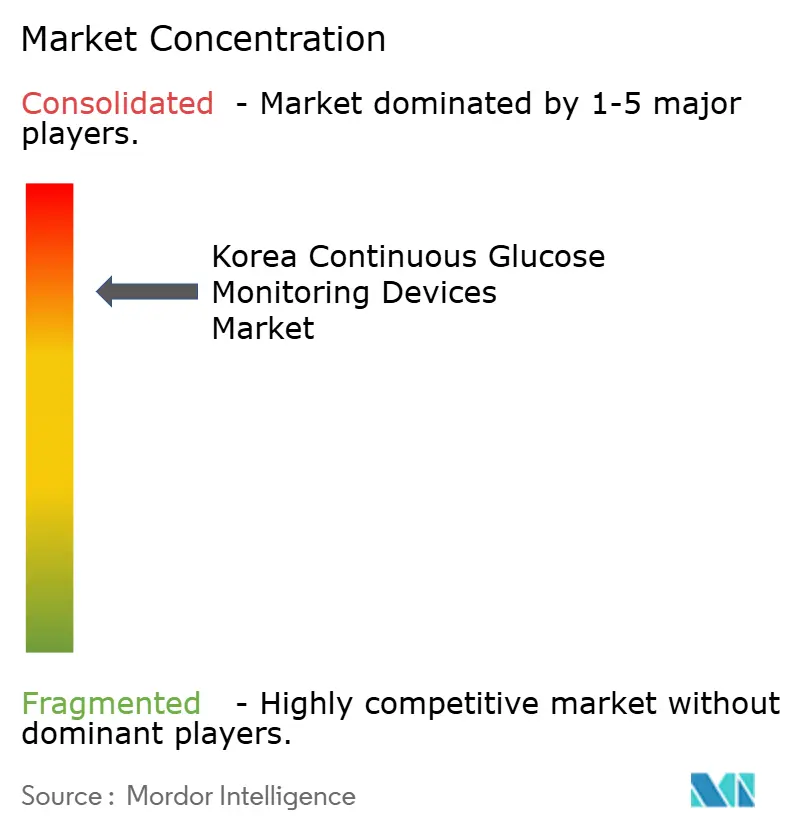

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Korea Continuous Glucose Monitoring Devices Market Analysis by Mordor Intelligence

The Korea continuous glucose monitoring market size reached USD 233.98 million in 2026 and is forecast to reach USD 468.17 million by 2031 at a 2026-2031 CAGR of 14.88%. Momentum reflects broadening NHIS coverage, tighter integration with automated insulin delivery systems, and domestic innovation that improves affordability and localization of supply. Clinician guidance has moved decisively toward real-time CGM for adults with Type 1 diabetes and for insulin-intensive Type 2 regimens, which strengthens device demand in both home and hospital settings. Telemonitoring pilots have established workable legal and operational pathways for remote diabetes care, which sustains CGM use outside the clinic. Evidence from local cost-utility studies has also been favorable, supporting ongoing reimbursement alignment for advanced indications.

Key Report Takeaways

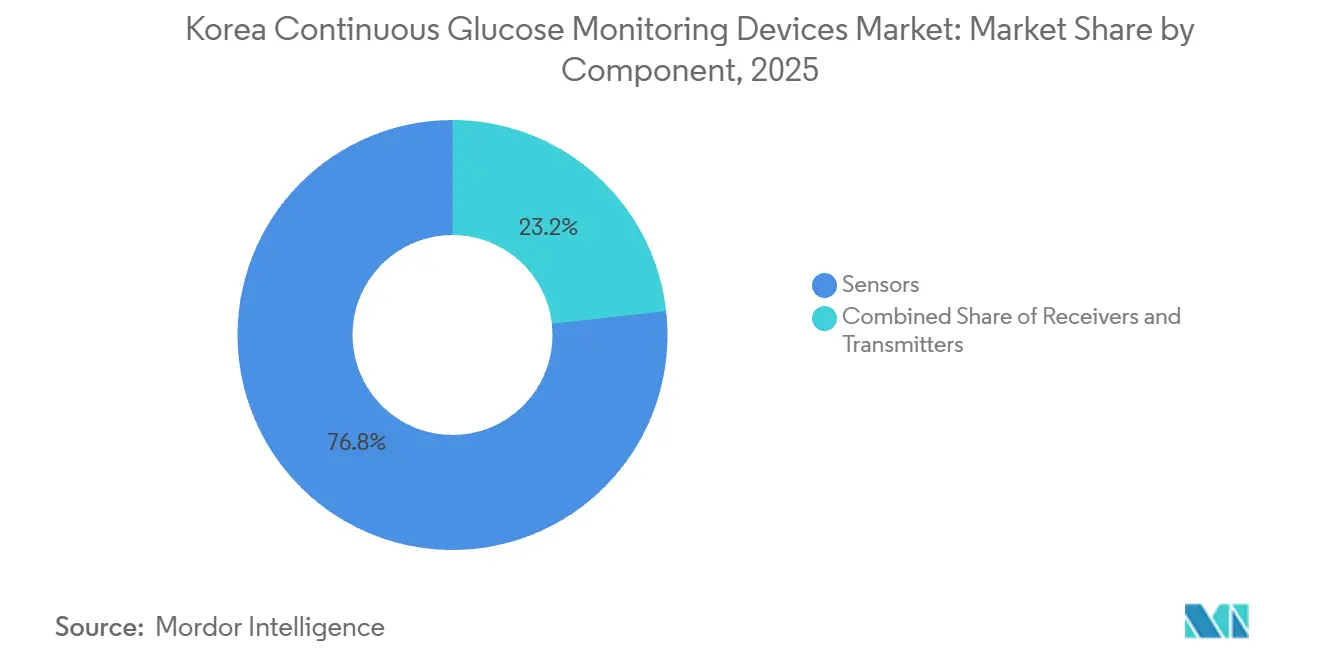

- By component, sensors led with 76.78% share in 2025, while durables recorded the fastest growth at a 16.86% CAGR through 2031.

- By end user, the home or personal segment held 75.97% share in 2025, and hospitals or clinics posted the highest growth at a 15.63% CAGR through 2031.

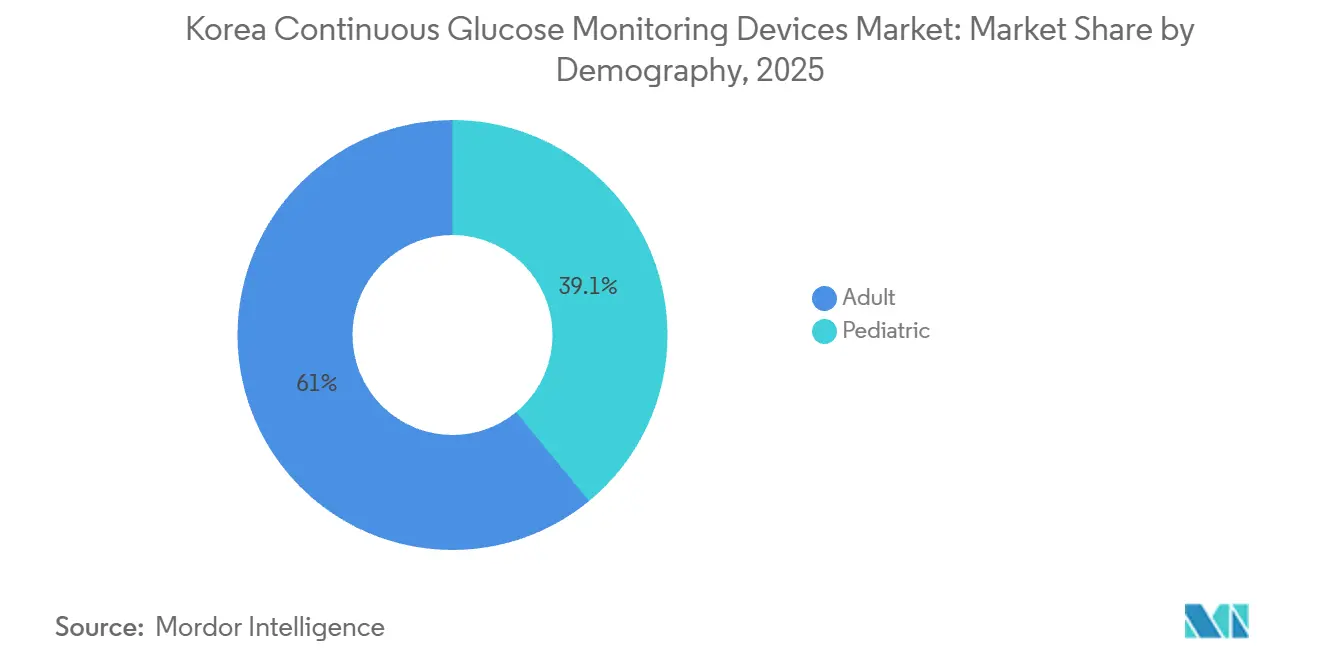

- By demography, adults accounted for a 60.95% share in 2025, while pediatrics advanced at a 15.49% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Korea Continuous Glucose Monitoring Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reimbursement Expansion Under Korea's National Health Insurance (NHIS) | +4.2% | National, concentrated in Seoul metropolitan area and pediatric populations | Medium term (2-4 years) |

| Rapid Uptake of CGM-Enabled Artificial-Pancreas Research Programs | +2.8% | National, with early gains in tertiary hospitals (Seoul, Busan) | Long term (≥ 4 years) |

| Growing Demand From Type 2 Diabetics on GLP-1 Therapy | +3.5% | Global trend spilling into APAC; highest uptake in affluent urban zones | Medium term (2-4 years) |

| Next-Gen Multi-Analyte (Glucose + Ketone) Sensors Entering KMFDS Trials | +1.4% | National, initially targeting T1D cohort with SGLT2i therapy | Long term (≥ 4 years) |

| Post-COVID-19 Telemonitoring Incentives From MOHW | +2.1% | National, with spill-over to medically underserved rural areas | Short term (≤ 2 years) |

| Start-Up-Driven Non-Invasive CGM Prototypes (e.g., Photonic Wristbands) | +1.2% | National R&D hubs (Seoul, Incheon, Seongnam); international commercialization potential | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Expansion Under Korea's National Health Insurance (NHIS)

Policy support serves as an immediate catalyst, reducing out-of-pocket costs for priority groups and encouraging continuous sensor use. Coverage improvements have coincided with a marked age gradient in uptake, with national cohort data showing higher continuous use among younger individuals and lower use among older adults who face more barriers to adoption. Clinical societies have updated guidance in favor of real-time CGM for all adults with Type 1 diabetes and for those with Type 2 diabetes who require intensified insulin therapy, which aligns clinical practice with payer objectives to prevent severe hypoglycemia and improve time in range[1]Source: Korean Diabetes Association, “2025 Clinical Practice Guidelines for Diabetes Management in Korea,” Diabetes & Metabolism Journal, pmc.ncbi.nlm.nih.gov. Economic evaluations conducted in South Korea find that real-time CGM is cost-effective in insulin-intensive Type 2 diabetes, which informs coverage evaluations and underscores the budget impact of fewer acute complications. The reimbursement review process also emphasizes device quality and safety, which means vendors need to provide robust clinical evidence and comply with local submission standards to sustain funding. Over time, streamlined implementation and education will remain essential so that policy improvements translate into continuous real-world usage among eligible patients.

Rapid Uptake Of CGM-Enabled Artificial‐Pancreas Research Programs

Automated insulin delivery systems are bringing CGM into more care pathways by linking sensors, pumps, and algorithms into closed-loop operation. Standards of care for 2026 recommend AID for adults with Type 1 diabetes and recognize the role of CGM within comprehensive insulin management, which supports clinical and payer alignment around these platforms. Korean guidelines also elevate real-time CGM in Type 1 diabetes and define best practices for integrating sensor data into dose titration, which underpins training protocols in tertiary hospitals. Domestic R&D programs continue to explore device integration and data-driven dose guidance, which may widen AID benefits beyond pump users to multiple daily injection cohorts. As algorithms mature, hospital adoption and home use reinforce each other because the same sensor platforms support both inpatient and outpatient workflows.

Growing Demand From Type-2 Diabetics On GLP-1 Therapy

Behavioral and pharmacologic synergies are shifting attention to non-insulin Type 2 diabetes care pathways. Clinical guidance emphasizes that CGM feedback helps adjust meal timing and activity patterns, which complements the appetite and gastric-emptying effects of GLP-1 receptor agonists for glycemic control. Korean guidelines recognize real-time CGM in patient groups that benefit from continuous data, and this creates a foundation for combination approaches where therapy adjustments require near-real-time feedback. The broader clinical community also highlights how CGM can support medication optimization through improved time in range and fewer hypoglycemia events, which is particularly relevant when intensifying or de-intensifying therapy. As digital tools evolve, data sharing between patients and care teams enables targeted interventions that fit into routine care, rather than frequent clinic visits. Together, these changes expand the addressable user base for the South Korea Continuous Glucose Monitoring market in early-stage Type 2 management, where lifestyle feedback can shape outcomes.

Next-Gen Multi-Analyte (Glucose + Ketone) Sensors Entering KMFDS Trials

Platform innovation aims to deliver more analytes, longer wear, and simpler workflows. Clinical reviews describe progress toward achieving reduced calibration, sub-10% MARD accuracy, and app-based analytics that make sensor data more actionable for clinicians and users. The addition of ketone monitoring has clear relevance for patients at risk of euglycemic diabetic ketoacidosis in certain therapy combinations, and clinical guidance continues to emphasize risk mitigation for these regimens. Improvements in sensor chemistry and signal processing enable longer wear windows, which can increase adherence and reduce replacement burden without compromising accuracy. As vendors validate multi-analyte designs under local submission standards, clinical utility will center on the earlier detection of acute risk and the provision of finer-grained guidance for therapy adjustments. These features broaden the role of CGM and support further adoption in the South Korea continuous glucose monitoring market, as clinical teams target both long-term outcomes and near-term safety.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Monopolized Import Channel & High Device ASPs | -3.8% | National, disproportionate impact on low-income and rural populations | Medium term (2-4 years) |

| Physician Scepticism Over Non-Adjunctive Use In Primary Care | -1.6% | National, concentrated in community clinics vs. tertiary hospitals | Short term (≤ 2 years) |

| Stricter KMFDS Data-Privacy Mandates For Cloud Platforms | -0.9% | National, heightened scrutiny in Seoul/Incheon digital health hubs | Medium term (2-4 years) |

| Competition From Low-Cost SMBG & CGM Rental Models | -2.1% | National, most acute in price-sensitive T2D non-insulin cohort | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Monopolized Import Channel & High Device ASPs

Device affordability remains a barrier for users who do not qualify for higher reimbursement or who face budget constraints. Domestic manufacturing capacity is expanding, which can lower landed costs and shorten supply lines for sensors and receivers. Cost-utility research in South Korea supports funding for intensive insulin users, yet patients outside prioritized groups still weigh ongoing sensor costs against limited budgets. Uptake patterns confirm that continuous use is higher among younger and more digitally engaged cohorts, and lower among older adults who are more sensitive to recurring expenses and required device training. As local vendors improve scale and as reimbursements evolve, price dispersion can narrow and help the South Korea continuous glucose monitoring market reach new patient segments. In the meantime, clinicians and payers continue to target groups that derive the greatest clinical and economic benefits from continuous use.

Physician Scepticism Over Non-Adjunctive Use In Primary Care

Training, liability, and workflow gaps can reduce prescription rates outside tertiary centers. National cohort data show that only a minority of eligible adults with Type 1 diabetes used CGM continuously, and utilization was highest among pediatric users who benefit from caregiver support and structured education. Clinical guidance endorses real-time CGM for Type 1 diabetes and for insulin-intensive Type 2 diabetes, yet adoption in community clinics can lag due to limited time for data interpretation and fewer resources for structured onboarding. As standard operating procedures for ambulatory glucose profile interpretation and dose titration expand, familiarity rises, and inertia declines. Hospital centers and endocrinology clinics also anchor early use of automated insulin delivery, which then diffuses to broader practice as training models mature. Over the forecast period, structured education and clear clinical governance will be essential to unlock primary care uptake in the South Korea continuous glucose monitoring market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Sensors Anchor Recurring Revenue, Durables Surge on Pump Integration

Sensors account for the largest component share, with 76.78% in 2025, driven by recurring replacement cycles and widespread clinical endorsement for real-time monitoring. Advances in accuracy and reduced calibration have raised patient confidence, while app-based analytics improve visibility into trends that inform therapy adjustments. Clinical guidance has clarified how to use time-in-range metrics to guide treatment, which further legitimizes the role of sensors in standardized care pathways. Domestic vendors have launched calibration-free platforms with competitive MARD and faster warm-up, which strengthen local value propositions and support broader uptake across age groups. As these features consolidate into baseline expectations, competition moves toward wear comfort, seamless data sharing, and compatibility with clinical dashboards that fit into hospital and clinic workflows.

Durable components, including receivers and transmitters, are expanding at the fastest clip with a 16.86% CAGR. User preferences vary by age and setting because some cohorts favor smartphone-native monitoring while others need dedicated displays for simplicity and accessibility. Closed-loop systems validate the role of reliable communication hardware that can sustain high-frequency data exchange for algorithmic control, which helps define performance benchmarks for the category. Domestic offerings of receivers and app updates also reflect attention to localization, language, and user-interface design, which encourages adoption in older adults who need straightforward displays. As platforms converge on accuracy, the South Korea continuous glucose monitoring industry is differentiating on ecosystem depth, app usability, and the quality of integration with hospital systems.

By End User: Homecare Primacy Masks Hospital Surge Driven by Inpatient Hypoglycemia Protocols

Home or personal settings represent 75.97% of end-user share in 2025 as patients prioritize convenience, real-time alerts, and fewer clinic visits for routine glucose management. Telemedicine pilots and remote monitoring workflows allow clinicians to review CGM data asynchronously, which reduces friction for therapy adjustments between in-person visits. Clinical guidelines support the use of real-time sensor data to drive time-in-range improvements, which strengthens physician confidence in virtual follow-up for eligible patients. As a result, the South Korean continuous glucose monitoring market has a strong home care foundation that reflects both user preference and evolving clinical workflows.

Hospitals and clinics are growing faster at 15.63% CAGR as inpatient protocols adopt CGM for insulin titration, perioperative control, and high-risk monitoring. Closed-loop systems validated in specialty centers help create templates for broader rollouts across tertiary networks, which then standardize training and interpretation. As data flows into care teams earlier in the patient journey, hospitals can use the same sensor platforms for both inpatient and discharge planning, which increases continuity and adherence at home. These patterns reinforce South Korea's continuous glucose monitoring industry’s shift toward integrated care that spans settings instead of siloed device use.

By Demography: Adult Dominance Masks Pediatric Surge Fueled by Coverage and Adherence

Adults represent 60.95% share in 2025, reflecting the burden of Type 2 diabetes in older cohorts and their need for structured glycemic control strategies. National cohort evidence shows that continuous use has been higher in younger groups and lower in older adults, which signals the importance of education, simplified apps, and caregiver features in raising adherence among seniors. Clinical guidance details how to translate sensor data into dose changes for insulin-intensive patients and when to rely on alarm features to avoid severe hypoglycemia, which supports adult-focused therapy intensification. Over time, adult adoption should benefit from easier onboarding and broader coverage for groups with the greatest gains in time in range and complication risk reduction[2]Source: Ministry of Health and Welfare, “Pilot Program for Tele-medical Service Kicks Off,” Ministry of Health and Welfare, mohw.go.kr.

Pediatrics is the fastest-growing demographic with a 15.49% CAGR because caregiver support, high alert utility, and improved access encourage continuous use. National data show that pediatric users adopt CGM more consistently than older adults, and predictive alerts are especially valued in school and nighttime settings. Korean guidance supports universal real-time CGM for Type 1 diabetes in children, which directs training and resource allocation toward effective long-term control in youth. As capabilities migrate into everyday devices and caregiver apps, the South Korea continuous glucose monitoring market will capture sustained pediatric growth supported by strong clinical consensus.

Geography Analysis

Regional adoption varies with provider density, digital readiness, and logistics. Uptake concentrates around tertiary centers where endocrinology teams and device training programs are established, and this concentration raises visibility for continuous use among local clinics that share care pathways with those centers. Younger cohorts that are more comfortable with apps and wearables also cluster in metropolitan areas, which supports a higher baseline of continuous use relative to rural settings. These dynamics help the market build a larger installed base in urban areas that can diffuse out as training and access expand.

Telemonitoring pilots reduce geographic barriers by allowing data review without travel. Government pilots and legal clarifications support remote interpretation of physiological data, which is central to CGM-led diabetes management plans outside major cities[3]Source: Ji Yoon Kim et al., “Real-time continuous glucose monitoring vs. self-monitoring of blood glucose: cost-utility in South Korean type 2 diabetes patients on intensive insulin,” Journal of Medical Economics, tandfonline.com. As those programs mature, standard protocols for consent, security, and clinical action can help smaller clinics integrate CGM into routine follow-up, which lifts adoption in underserved regions. Over the medium term, continued investment in digital literacy and education should reinforce steady expansion of the market beyond metropolitan hubs.

Referral patterns also shape regional access. Hospitals that deploy closed-loop systems become centers for training and device onboarding, which then influence how nearby clinics prescribe and monitor CGM. As these networks share protocols and data templates, clinicians across regions can apply uniform standards in dose adjustment and hypoglycemia prevention. In parallel, domestic vendors provide localized support, language-specific interfaces, and supply capacity that reduce friction for clinics and pharmacies outside major cities, thereby contributing to increased market access.

Competitive Landscape

The competitive set comprises multinational leaders and a growing domestic challenger, with competition shifting from headline accuracy to ecosystem performance. Clinical reviews document a convergence around sub-10% MARD with reduced calibration and faster warm-up, which makes alerts, sharing, and integration key differentiators. Domestic platforms have achieved calibration-free operation with competitive MARD and a shorter warm-up, which resonates in both home and clinic environments, where simpler setups reduce drop-off. As devices reach standard accuracy thresholds, integrated decision support and smoother hospital workflows will define market leadership.

Automated insulin delivery validates higher-value use cases that depend on dependable CGM streams. The MiniMed 780G with Simplera Sync shows how disposable sensors with seamless connectivity can power closed-loop control for pediatric and adult users, and this strengthens the role of CGM in complex therapy. Standards of care for 2026 highlight AID for adults with Type 1 diabetes and recognize real-time CGM as essential in intensive insulin management, which boosts the platform logic for algorithm-enabled care. Hospital adoption can anchor future home uptake because the same sensor streams support both inpatient treatment and remote follow-up planning in the market.

Localization and supply depth now significantly influence a company's competitive posture. Domestic manufacturing with multi-million unit capacity underpins cost competitiveness and can shorten lead times for sensors and receivers, which helps clinics avoid stockouts and reduces friction in reimbursement processes. Product updates that remove manual calibration and reduce warm-up simplify starts for new users, which aligns with clinician priorities to reduce onboarding time. Over the forecast period, leadership will hinge on combining sensor accuracy with high-reliability connectivity, human-centered apps, and robust integration with clinical systems that fit hospital and clinic workflows in the South Korea Continuous Glucose Monitoring market.

Korea Continuous Glucose Monitoring Devices Industry Leaders

Abbott

Dexcom, Inc.

i-SENS Inc.

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: i-SENS Inc. announced the global launch of the CareSens Air Receiver, a dedicated display device designed to support reimbursement and tender eligibility in European markets.

- May 2025: i-SENS Inc. received approval from Korea’s Ministry of Food and Drug Safety for an upgraded CareSens Air CGM that eliminates manual calibration and shortens warm-up to 30 minutes, achieving an 8.7% MARD and aligning performance with leading platforms.

- June 2023: Dexcom Inc. and Kakao Healthcare Corp. announced a strategic partnership to integrate the Dexcom G7 CGM system with Kakao Healthcare's digital health platform, enabling real-time glucose data transmission via KakaoTalk messaging, Korea's dominant communication application with 95% smartphone penetration, to facilitate remote patient monitoring and asynchronous physician consultations.

Korea Continuous Glucose Monitoring Devices Market Report Scope

According to the report's scope, patients with type 1 or type 2 diabetes can manage their condition with the use of continuous glucose monitoring (CGM) devices by performing fewer fingerstick tests. Blood sugar levels are continuously monitored by a sensor located just under the skin. Results are sent via a transmitter to a cell phone or wearable technology. The Korea continuous glucose monitoring devices market is segmented into components, end user, and demography. The report offers the value (in USD) for the above segments.

By Component

| Sensors |

| Transmitters |

| Receivers |

By End User

| Hospitals / Clinics |

| Home / Personal |

By Demography

| Adult |

| Pediatric |

| By Component | Sensors |

| Transmitters | |

| Receivers | |

| By End User | Hospitals / Clinics |

| Home / Personal | |

| By Demography | Adult |

| Pediatric |

Key Questions Answered in the Report

What is the current size and forecast for the South Korea Continuous Glucose Monitoring market?

The South Korea continuous glucose monitoring market reached USD 233.98 million in 2026 and is projected to reach USD 468.17 million by 2031 at a 2026-2031 CAGR of 14.88%.

Which components are leading growth in the South Korea Continuous Glucose Monitoring market?

Sensors lead by share, while durables, including receivers and transmitters, post the fastest growth due to integration with automated insulin delivery and diversified user preferences.

How do clinical guidelines affect adoption in the South Korea Continuous Glucose Monitoring market?

National and international guidance endorses real-time CGM for Type 1 diabetes and for insulin-intensive Type 2 diabetes, which supports prescription and reimbursement alignment across settings.

What end-user settings are most important in the South Korea Continuous Glucose Monitoring market?

Home or personal use holds the largest share, while hospitals and clinics are growing quickly as inpatient protocols and discharge planning incorporate continuous data.

What demographic trends shape demand in the South Korea Continuous Glucose Monitoring market?

Adults hold the largest share due to the burden of Type 2 diabetes, while pediatric use is growing fastest because of strong caregiver support, alert utility, and improved access.

Which innovations will shape the South Korea Continuous Glucose Monitoring market over the next few years?

Closed-loop systems, calibration-free sensors with faster warm-up, multi-analyte capabilities, and stronger integration with telemonitoring workflows are expected to define product differentiation.

Page last updated on: