UV Cured Printing Inks Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

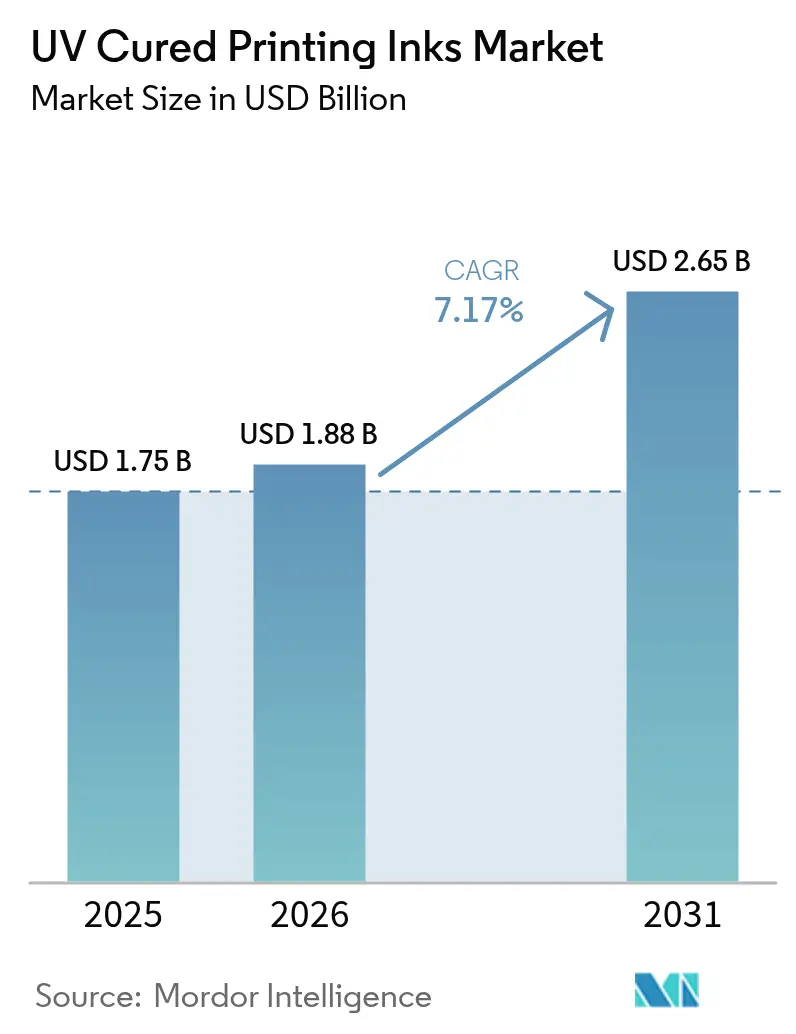

| Market Size (2026) | USD 1.88 Billion |

| Market Size (2031) | USD 2.65 Billion |

| Growth Rate (2026 - 2031) | 7.17% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

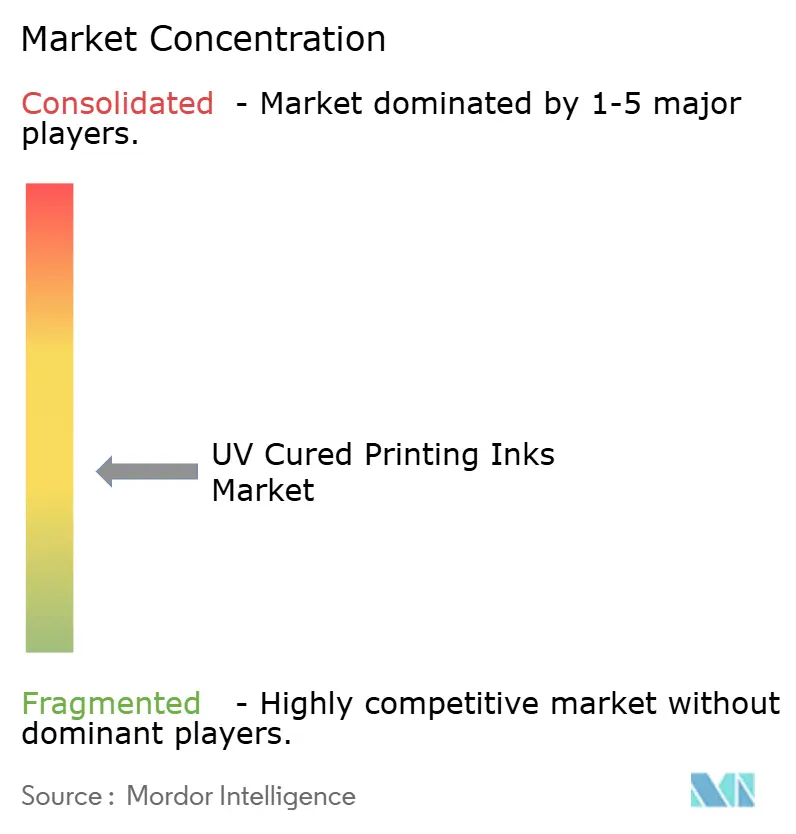

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UV Cured Printing Inks Market Analysis by Mordor Intelligence

The UV Cured Printing Inks Market size was valued at USD 1.75 billion in 2025 and estimated to grow from USD 1.88 billion in 2026 to reach USD 2.65 billion by 2031, at a CAGR of 7.17% during the forecast period (2026-2031). Energy-efficient LED curing, which lowers press power consumption by 60-65% while removing mercury lamp maintenance and VOC emissions, is the primary growth driver. Packaging converters are accelerating adoption because low-migration formulations meet tightening food-contact rules in Asia-Pacific, the European Union, and North America. As OEMs release retrofit LED systems that raise press speeds 30-50% without new capital outlay, the addressable installed base widens and barriers to entry fall. At the same time, photoinitiator supply risks and emerging water-based or EB-curable alternatives inject competitive pressure that suppliers must manage through innovation and sourcing agility.

Key Report Takeaways

- By curing process, LED technology captured 56.14% of UV-cured printing inks market share in 2025 and is projected to expand at a 9.13% CAGR through 2031.

- By ink type, UV flexo inks held 41.32% revenue share in 2025, while the “Other UV cured printing inks type” segment is forecast to grow at a 8.88% CAGR to 2031.

- By application, packaging accounted for 60.25% of the UV-cured printing inks market size in 2025, whereas the “Others” application group is advancing at a 10.24% CAGR through 2031.

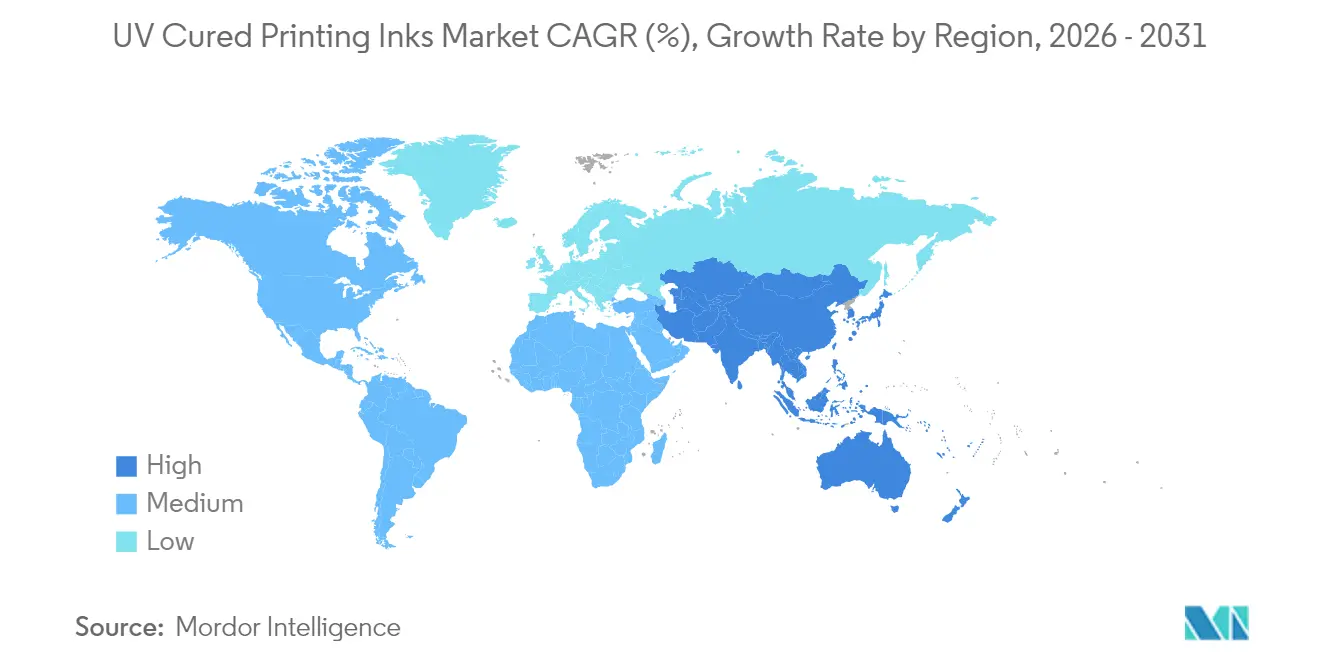

- By geography, Asia-Pacific led with 48.05% revenue share in 2025 and is on track for a 9.08% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global UV Cured Printing Inks Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital and inkjet printing growth | +1.8% | North America, Asia-Pacific | Medium term (2-4 years) |

| Packaging and label converter expansion | +2.1% | Asia-Pacific and other emerging markets | Long term (≥ 4 years) |

| Stricter VOC/sustainability regulations | +1.5% | EU, North America, spillover to Asia-Pacific | Short term (≤ 2 years) |

| Shift to energy-efficient LED UV systems | +2.3% | Early adoption in developed regions, global rollout | Medium term (2-4 years) |

| Low-migration inks in food and pharma packs | +1.2% | EU, North America, global compliance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Digital and Inkjet Printing

Print-on-demand adoption lets publishers slash warehousing expenses and meet rapid turnaround expectations, and UV-cured inks enable crisp imagery on coated and uncoated substrates without post-press drying delays[1]“Commercial Printing Trends 2024,” HP, hp.com. Direct mail volumes are rebounding as brands integrate tactile pieces with digital campaigns, reinforcing demand for durable, scuff-resistant UV impressions that withstand postal handling. Research and development momentum is visible in FUJIFILM’s patent covering surfactant-modified inkjet formulations that reduce inter-color bleeding and heighten gloss uniformity, an advance that strengthens UV compatibility with high-speed piezo heads. Commercial shops that add web-to-print storefronts tap short-run personalized jobs where instant curing shortens job queues. Although legacy publication volumes keep shrinking, the value shift to variable-data and specialty substrates produces a net positive pull on UV-cured printing inks market growth.

Expansion of Packaging and Label Converters

Converter capacity is rising across Indonesia, India, and Vietnam as regional FMCG demand climbs and global brands nearshore supply chains; each new press line typically specifies LED UV or hybrid curing to cut make-ready waste and satisfy factory ESG benchmarks. Flexographic press upgrades, exemplified by Miraclon’s FLEXCEL NX platform, let converters match gravure aesthetics while using thinner plates and lower ink laydowns that suit UV formulations. Brand-owner sustainability scorecards increasingly credit energy savings from UV LED curing, nudging converters toward technology refresh. The dual need to meet food-contact rules and lower total cost of ownership cements packaging’s pull on the UV-cured printing inks market.

Stricter VOC/Sustainability Regulations

The European Union’s designation of UV/EB technology as an environmentally preferable alternative, paired with the U.S. EPA’s “Super Clean Technology” status, removes regulatory ambiguity for printers evaluating investment payback. India’s FSSAI ban on toluene in food-grade inks accelerated substitution to non-aromatic UV systems, while China’s GB 4806.14-2023 tightens migration limits beginning 2026, compelling local converters to requalify ink sets. Chemical suppliers are proactively shifting additive portfolios to PFAS-free and bio-based inputs, such as Clariant’s rice-bran-derived waxes, further improving the environmental profile of UV formulations. These converging rules create an immediate compliance pull that magnifies the UV-cured printing inks market trajectory.

Rapid Shift to Energy-Efficient LED UV Systems

LED arrays emit in a narrow 365–405 nm band that polymerizes acrylate chains without radiant heat, allowing delicate films and shrink sleeves to run faster and flatter. Fujifilm’s Activ Hybrid retrofit kit boosts sheetfed speeds by 30-50% while letting operators toggle between LED and conventional UV, smoothing learning curves and capital amortization[2]Fujifilm Launches Activ Hybrid LED UV Retrofit System,” Large Format Review, largeformatreview.com. Baldwin Technology’s modular Unity LED™ platform extends lamp life past 25,000 hours, shrinking downtime and spare-part spend. With electricity costs rising and mercury disposal rules tightening, LED upgrades deliver quantifiable ROI, making this driver a pivotal lever in the UV-cured printing inks market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Decline of conventional commercial printing | -1.4% | Primarily developed economies | Long term (≥ 4 years) |

| Competition from water-based and EB systems | -0.8% | EU, North America | Medium term (2-4 years) |

| Photoinitiator supply-chain volatility | -1.1% | Global, China-centric sourcing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Decline of Conventional Commercial Printing

Newspaper and magazine pagination keeps sliding as advertisers channel budgets into digital platforms, eroding legacy UV offset ink demand. Commercial printers that fail to pivot toward packaging, labels, or value-added embellishments face press under-utilization that directly reduces ink consumption. While high-margin short runs temper revenue loss, volume attrition persists, marking this restraint as a structural headwind.

Competition from Water-Based and EB-Curable Systems

Brands with strict carbon accounting prefer water-based labels for chilled beverage and dairy packs where condensation resistance is less critical, narrowing UV’s addressable share in those niches. Electron-beam curing, which eliminates photoinitiators entirely, appeals to infant-formula can lines and retort pouches sensitive to potential migrants. Yet UV remains dominant where high-scuff resistance or dark-color holdout is mandatory, limiting the ceiling of this competitive threat.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Curing Process: LED Technology Reshapes Adoption Patterns

LED systems accounted for 56.14% of the UV-cured printing inks market size in 2025 and are forecast to post a 9.13% CAGR to 2031, underlining the technology’s broad acceptance among converters focused on energy metrics. The retrofit option lowers capital hurdles, letting operators preserve existing press platforms while sharply reducing downtime. Lower stack temperatures eliminate sheet distortion on thin films and enable higher nip pressures that maintain registration accuracy at press speeds above 18,000 sph. These attributes collectively sustain LED’s leadership in the UV-cured printing inks market.

Arc-lamp curing retains a toehold in certain wide-web and screen-printing applications that need broadband spectra to trigger cationic photochemistry. However, recent high-output LED diodes reaching 25 W/cm² narrow the former gap in cure depth, and hybrid lamp housings let users toggle modes mid-shift, hastening the migration curve. As government restrictions on mercury escalate, arc-lamp economics will further erode, reinforcing LED’s dominant trajectory.

By Ink Type: Flexographic Formulations Dominate Converter Demand

UV flexo inks delivered 41.32% of revenue in 2025 as package printers favor flexo’s quick changeovers and solvent-free cleanup that align with lean manufacturing goals. High-opacity whites and expanded-gamut seven-color sets let converters match gravure density without sacrificing throughput. Consequently, flexo commands the largest slice of UV-cured printing inks market share across corrugated, folding carton, and flexible film plants.

Offset UV inks continue serving premium commercial catalog and book jackets where precise dot fidelity matters, yet volume shifts toward packaging cap the segment’s growth. Screen-printing inks hold niche value for tactile varnish effects and industrial nameplates. The “Other UV cured printing inks type” bucket grows at 8.88% CAGR thanks to burgeoning single-pass inkjet presses for décor laminates and direct-to-shape beverage containers, expanding the functional footprint of the UV-cured printing inks industry.

By Application: Packaging Remains the Core Revenue Anchor

Packaging contributed 60.25% of total sales in 2025, reflecting relentless demand from food, beverage, personal-care, and pharma verticals that prioritize low-migration and high-opacity graphic standards. Instant cure speeds let form-fill-seal lines run without ink offset, while low-heat profiles preserve film shrink ratios. Consequently, packaging will continue dictating tonnage flows in the UV-cured printing inks market.

Commercial and publication work faces secular volume pressure, yet specialty brochures employing dimensional varnish and spot gloss effects still justify UV offset chemistry. The “Others” group, projected to rise 10.24% CAGR, spans electronic circuit printing, automotive dial decoration, and additive manufacturing supports that leverage UV’s rapid polymerization. This breadth of end-use anchors the resilience of the UV-cured printing inks market against segment-specific downturns.

Geography Analysis

Asia-Pacific generated 48.05% of 2025 revenue and is tracking a 9.08% CAGR to 2031, led by China’s nationwide GB 4806.14-2023 compliance deadline and India’s IS:15495 enforcement that restricts toluene in food packaging inks. Local leaders such as UFlex have introduced polyester acrylates that bond to metallized films, enabling converters to meet both barrier and migration goals in a single pass. Government incentives that refund up to 30% of energy-saving equipment costs further accelerate LED UV adoption across new gravure and flexo halls, cementing the region’s pull on the UV-cured printing inks market.

North America holds a technology-rich base where early adopters embraced LED units as early as 2016. The U.S. EPA’s endorsement and the Inflation Reduction Act’s clean-manufacturing credits financed numerous retrofits during 2024-25. Resin and additive capacity expansions, exemplified by Lubrizol’s doubling of Solsperse hyperdispersant output in Ohio, bolster supply assurance for domestic ink makers.

The Middle East and Africa, and South America contribute modest volume shares today, yet represent latent upside as packaging converters migrate from solvent lines to LED platforms to comply with export customer audits. Brazilian label printers installing hybrid UV-EB flexo lines attest to an emerging technology leapfrog that could compress adoption timelines once macroeconomic conditions stabilize.

Regulatory Landscape

Regulation for UV-cured printing inks is tightening around both food-contact compliance and the hazard profile of key photoinitiators. In the European Union, reclassification and labeling obligations for TPO (2,4,6-trimethylbenzoyl-diphenyl-phosphine oxide) hit compliance deadlines in 2025 (including an April 2025 deadline in the United Kingdom), which accelerated reformulation toward lower-migration and alternative photoinitiator systems for packaging inks. In February 2026, the European Chemicals Agency (ECHA) advanced its REACH Annex XIV pathway by publishing a draft recommendation that includes photoinitiator 379 (EC 438-340-0) and opened a public consultation through May 2, 2026, raising the compliance bar for suppliers serving EU packaging and label converters.

Food-contact governance is increasingly managed through documentation and positive-list alignment. The Swiss Ordinance on Printing Inks continues to serve as a global reference point for intentional and non-intentional substances in packaging inks, supported by updated 2026 interpretation guidance that reinforces Declaration of Compliance (DoC) expectations. EuPIA guidance and its voluntary Charter also provide an industry framework used by many European supply chains to screen hazardous raw materials beyond minimum legal requirements. Workplace safety obligations are evolving as well, including updated UK HSE COSHH guidance in January 2026 on ozone generation from UV-curing lamps in printing environments.

Value Chain Analysis

The UV-cured printing inks value chain begins with upstream chemical feedstocks (acrylate oligomers/monomers, pigments, additives, and stabilizers) and critical photoinitiators, then moves through formulation, dispersion, filtration/degassing, and packaging into press-ready products. Ink manufacturers qualify products with OEMs and converters, often at substrate and press-platform level, before distribution through regional warehouses and technical service teams to packaging, label, commercial, and industrial printers. Logistics and input availability, especially cleavage-type photoinitiators concentrated in Japanese and German production hubs, influence lead times and formulation continuity.

Value capture shifts downstream as applications move toward regulated packaging, where batch-level migration documentation and converter support for compliance testing become differentiators. Press OEM and ink supplier partnerships are strengthening as converters pursue system-level optimization (press settings, curing energy, and ink reactivity) alongside sustainability targets, including the June 2026 global alliance between Koenig and Bauer and INX International focused on LED-UV printing performance. Regionalization of manufacturing and sourcing is also more visible as tariff and import-cost pressures affect oligomers and pigments, while distribution networks continue to rely on major hubs such as the Port of Rotterdam and Shanghai Yangshan to serve multinational converter footprints.

Competitive Landscape

Competitive intensity remains moderately fragmented. DIC Corporation leverages two decades of UV-curable resin expertise from optical films to craft low-warpage inks for blister packs, underscoring cross-business synergies. Suppliers able to guarantee photoinitiator continuity gain an edge while the industry restructures around TPO replacements. Patent filings from Meta on multifunctional resins hint at future convergence between 3D additive processes and graphic inks, foreshadowing new arenas where incumbents will jostle for early mover advantage.

UV Cured Printing Inks Industry Leaders

artience Co. Ltd. (TOYO INK CO., LTD.)

DIC Corporation

Flint Group

Huber Group

Siegwerk Druckfarben AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A major opportunity sits at the intersection of LED-UV conversion and food-packaging compliance, where low-migration, low-energy ink sets can replace legacy UV systems while reducing power consumption and addressing tighter substance restrictions. The March 2026 launch of Toyo Ink Europe (artience Group) low-migration, low-energy UV ink portfolios, aligned to German Printing Ink Ordinance (GIO) benchmarks, shows how suppliers package regulatory readiness into commercially deployable product ranges for converters serving food-contact applications.

Capacity and localization investments point to gaps in supply assurance and regional service for packaging clusters, particularly where converters are installing or retrofitting UV LED systems and need stable ink families. In May 2026, Tritron GmbH started operating a 2,900 m2 Ink-Cube facility in Germany with a EUR 9.4 million investment to double UV and UV-LED ink manufacturing capacity, supporting shorter lead times for European customers. In China, HMD Inks received local approval in June 2026 to expand capacity from 5,000 to 20,000 tons, backed by a RMB 90 million investment, reflecting continued scale-up to serve high-volume packaging and industrial printing demand as suppliers manage photoinitiator scrutiny and migration documentation requirements.

Recent Industry Developments

- April 2026: artience Co., Ltd. announced a global price revision of 10% or more across UV-curable, oil-based offset, and screen inks, citing higher costs for crude oil and naphtha-derived solvents and resins. The change highlights feedstock-driven volatility in ink formulation economics and pushes printers and converters to tighten cost-of-ownership comparisons across curing platforms and ink chemistries.

- March 2026: Toyo Ink Europe (artience Group) rolled out a portfolio of low-migration, low-energy UV inks engineered to align with German Printing Ink Ordinance (GIO) safety benchmarks for food packaging. The company paired low-energy curing with migration-focused design to target converters upgrading to LED-UV or hybrid UV systems and to strengthen qualification pathways for regulated packaging accounts.

- December 2024: Flint Group opened a 9,000 m2 plant in Savli, India, adding water-based and UV-curable ink capacity for labels and narrow-web packaging. The expansion strengthens local supply to fast-growing converter hubs and improves responsiveness for customers balancing sustainability requirements with high-throughput packaging production.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of UV-cured printing inks used in printing processes where the ink film is cured by ultraviolet light (including LED and arc curing), creating an instant-dry finish on the substrate.

Scope exclusions: We exclude UV curing equipment, UV lamps, and service revenue related to press installation or maintenance because these do not represent ink sales.

Segmentation Overview

- By Curing Process

- Arc Curing

- LED Curing

- By Ink Type

- UV Flexo Inks

- UV Offset Inks

- UV Low Energy/LED Offset Inks (Except UV Offset Inks)

- UV Screen Printing Inks

- Other UV Cured Printing Inks Type

- By Application

- Packaging

- Commercial and Publication

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the starting structure of the market and to keep assumptions tied to public indicators that can be checked. We referred to sources such as the US Census Bureau manufacturing and trade data, USITC tariff and import statistics, Eurostat production indices, UN Comtrade shipment data, and publications from printing and packaging industry associations.

Along with these, we reviewed company annual reports, earnings notes, investor presentations, and press coverage to understand capacity moves, product launches, and changes in end-use demand such as packaging and commercial print. Patent databases were also used to track formulation activity around LED-curable and low-migration chemistries, and an import-export shipment-level database helped validate trade flows for key raw material and ink categories. These desk sources are not exhaustive, and many other public references were used to collect data, validate assumptions, and clarify the research.

Primary Interviews and Surveys

Primary work was used to pressure-test what desk sources cannot show clearly, mainly pricing movement, mix shifts between arc and LED curing, and how demand changes by printing process. We spoke with a mix of ink suppliers, raw material participants, converters and printers, and channel-side experts across major consuming regions so gaps could be closed and assumptions could be cross-checked.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 18% | APAC: 51% |

| Mid tier: 52% | Functional/Unit leaders: 26% | EMEA: 30% |

| Smaller Players: 21% | Managers: 56% | Americas: 19% |

Market-Sizing & Forecasting

Sizing started with a top-down build where printing activity and packaging output signals were translated into an addressable UV-ink demand pool, then filtered by where UV curing is actually used by process and application. To keep totals realistic, the model was corroborated with selective bottom-up approximations, mainly sampled volume by process multiplied by observed average selling prices, and then adjusted when channel checks showed mix differences.

A few practical inputs were used as market fingerprints, such as packaging print growth, commercial and publication print trends, adoption pace of LED curing systems, the share movement across UV flexo, UV offset, and UV screen usage, and raw material cost direction for photoinitiators and key resins that can push price resets. For forecasting, we relied on scenario analysis supported by a light multivariate regression view, where the demand outlook was linked to packaging volumes and industrial production, and then refined by interview consensus on UV penetration and price pass-through. Where bottom-up views were thin for smaller countries, per-capita print and trade proxies were used first and then aligned back to regional totals.

Data Validation & Update Cycle

Outputs were checked through more than one lens so single-source errors do not drive the final numbers. We compared modeled results against independent signals like trade flows, print production indicators, and observed pricing ranges, and then investigated any sharp variances before sign-off.

Reviews were done in steps, starting with model logic checks and followed by variance reviews across regions and end-use exposure, and then a final analyst review for consistency in units, currency conversion, and year mapping. Reports are refreshed annually, and interim updates are triggered when material events occur, such as major capacity additions, sudden raw material shocks, or regulation-linked formulation shifts tied to compliance needs. Before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Uv Cured Printing Inks Market Estimate Compared With Other Published Estimates

Published market sizes for UV-cured printing inks can look far apart even when everyone is discussing a similar product area, mainly because the math behind pricing, timing, and what is counted as UV-curable is not consistent. In practice, differences show up when one estimate uses a different base year, applies a single flat price trend, or blends adjacent ink categories into the total.

The biggest gap drivers here are usually the treatment of LED versus arc curing mix, whether low-migration formulations are priced and counted distinctly, and how packaging versus commercial print demand is weighted across regions. Currency timing matters as well because reported values can move when exchange rates are averaged differently across the year, and the spread widens when assumptions are not rechecked after raw material swings that change selling prices.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.88 B (2026) | |

| Industry Publisher A | USD 1.87 B (2025) | Uses a different base year and a longer forecast window, and the estimate appears to apply broad market averaging where LED and arc mix effects on ASP are not clearly separated. |

| Global Publisher B | USD 2.38 B (2025) | Starts from a larger 2024 base and may include a wider definition that blends additional UV-printing ink scope by substrate or application, which can inflate the value versus a stricter ink-only boundary. |

The table shows that year selection and pricing treatment are doing most of the work behind the spread. By refreshing the currency conversion window and the process-level ASP checks during each update cycle, Mordor Intelligence keeps the 2026 total tied to observable print demand and the UV adoption mix, rather than letting a single assumed price curve drive the whole forecast.

Key Questions Answered in the Report

What is the current value of the UV-cured printing inks market?

The UV-cured printing inks market size is USD 1.88 billion in 2026.

How fast is the market projected to grow?

It is set to expand at a 7.17% CAGR, reaching USD 2.65 billion by 2031.

Which curing technology leads today's installations?

LED curing accounts for 56.14% of 2025 revenue and continues to gain share due to 60-65% energy savings.

Why do packaging converters prefer UV-cured inks?

Instant curing, low VOC emissions, and compliance with food-contact regulations drive uptake in packaging, which holds 60.25% of revenue.

Which region offers the strongest growth outlook?

Asia-Pacific leads with 48.05% share in 2025 and the highest forecast CAGR at 9.08% through 2031.

What risks could slow market expansion?

Photoinitiator supply volatility, competition from water-based and EB systems, and the ongoing decline in traditional commercial printing volumes are notable restraints.

Page last updated on: