Road Marking Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 7.61 Billion |

| Market Size (2031) | USD 9.32 Billion |

| Growth Rate (2026 - 2031) | 4.14% CAGR |

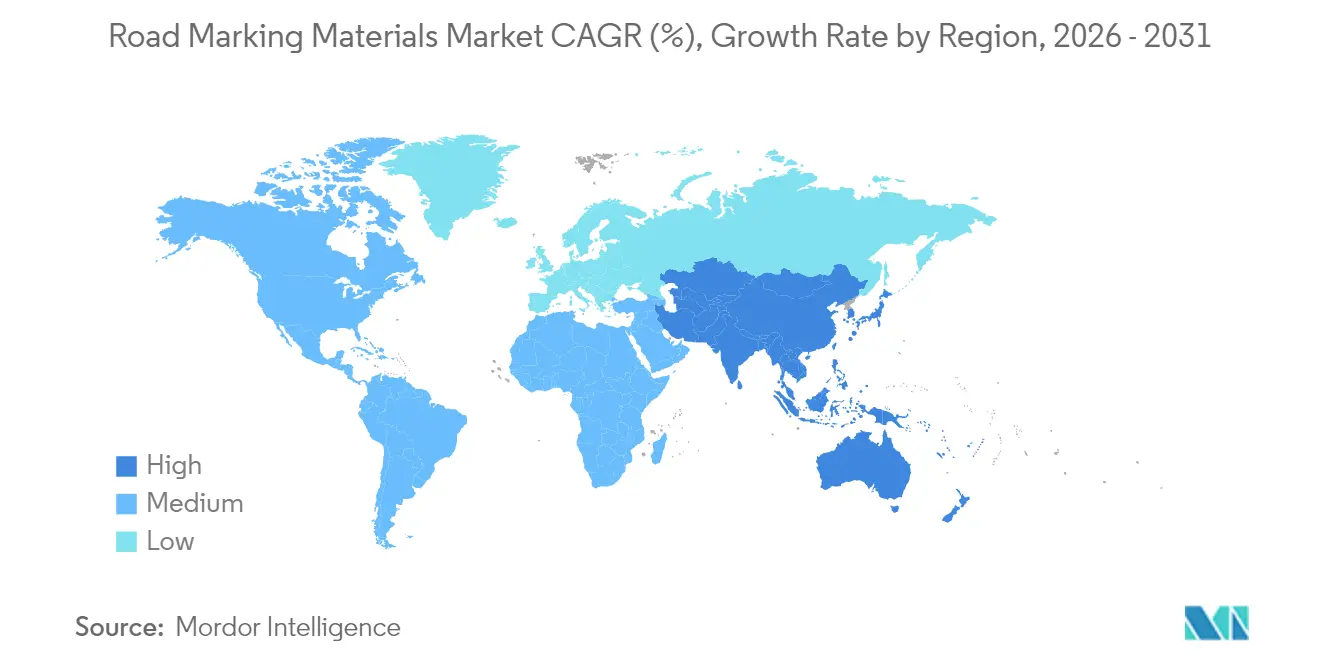

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Road Marking Materials Market Analysis by Mordor Intelligence

The Road Marking Materials market size is expected to grow from USD 7.31 billion in 2025 to USD 7.61 billion in 2026 and is forecast to reach USD 9.32 billion by 2031 at 4.14% CAGR over 2026-2031. The steady expansion is supported by surging infrastructure outlays, tightening safety mandates and rapid product innovation. Asia-Pacific remains the principal demand engine yet spending programs in North America and Europe sustain a broad global opportunity set. Material selection is evolving polymer systems are eroding the dominance of legacy paints, and machine-readable markings designed for autonomous vehicles are moving from pilot trials toward commercial roll-out. Environmental regulations now shape R&D priorities, pushing manufacturers toward low-VOC chemistries and recycled raw materials while retaining high visibility and durability. Competitive intensity is moderate, with established players relying on targeted acquisitions and technology licensing to protect share across high-growth regions.

Key Report Takeaways

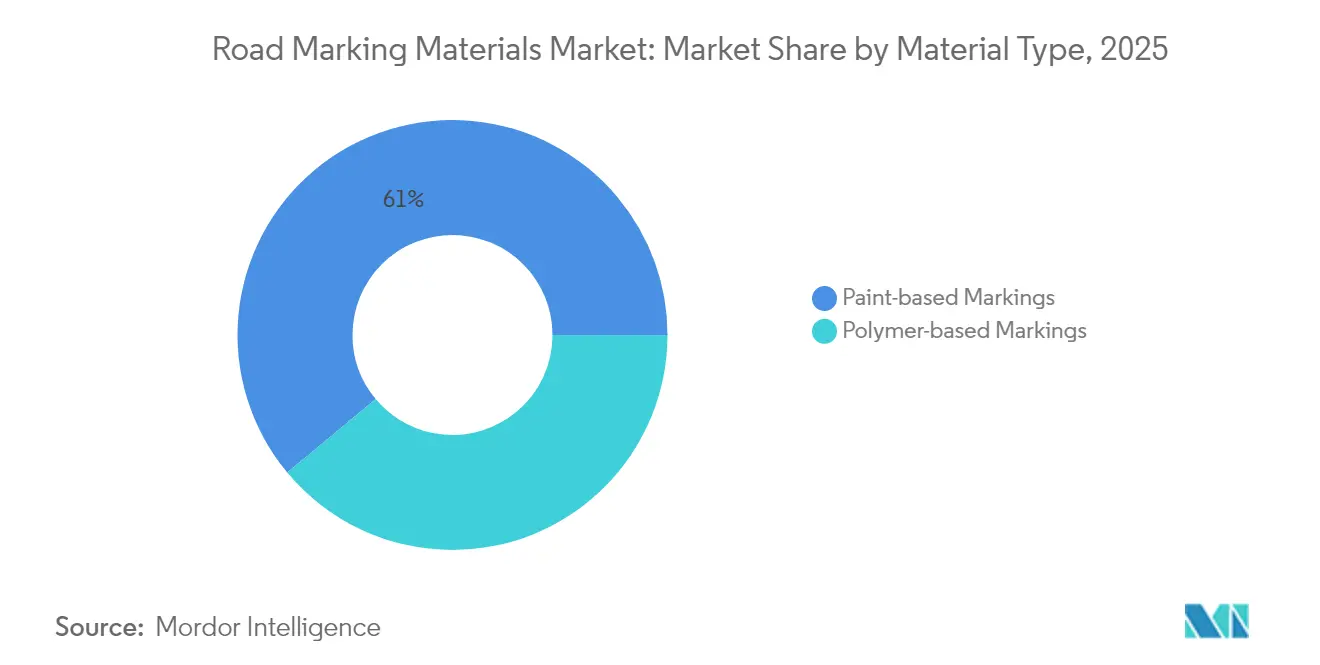

- By material, paint-based products captured 61.05% of the road marking materials market size in 2025, while polymer-based systems are projected to grow at a 4.52% CAGR to 2031.

- By application, highway and road projects accounted for a 68.20% share of the road marking materials market size in 2025 and are expanding at a 4.30% CAGR through 2031.

- By geography, Asia-Pacific held 40.20% of the road marking materials market share in 2025 and is advancing at a 4.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Road Marking Materials Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising road network expansion in developing economies | +1.2% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Escalating global road safety & visibility regulations | +0.8% | Global, with stricter enforcement in North America & EU | Short term (≤ 2 years) |

| Rapid urbanization boosting vehicle-density management | +0.9% | Asia-Pacific & MEA urban centers | Long term (≥ 4 years) |

| Machine-readable retro-reflective markings for AVs | +0.6% | North America & EU early adoption markets | Long term (≥ 4 years) |

| Photoluminescent / solar-charged line markings | +0.3% | Global pilot programs, concentrated in smart city initiatives | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Road Network Expansion in Developing Economies

Government-funded Road building drives much of the incremental demand in the road marking materials market. India’s transport blueprint earmarks USD 268.4 billion to add 30,600 km of new highways by 2032, with a wider goal of 200,000 km by 2037. Mega-projects of this scale require high-performance striping able to survive heavy axle loads, monsoon floods and desert heat. Similar funding surges across Southeast Asia and the Middle East channel multi-year volumes to suppliers capable of fast logistics and field technical support. Cross-border corridors also stimulate regional coordination on marking standards, nurturing opportunities for premium retro-reflective and thermoplastic lines that align with growing autonomous-vehicle readiness targets.

Escalating Global Road Safety & Visibility Regulations

Regulators continue to strengthen visibility criteria. The European Union Road Federation recommends 150 mm-wide lines with defined retro-reflection thresholds, while the US Federal Highway Administration enforces minimum retro-reflective values for centerlines and edgelines[1]European Union Road Federation, “Best Practice on Road Markings,” erf.be . Construction zones face even stricter orange marking rules that must remain conspicuous to LiDAR sensors. Parallel environmental statutes cap VOC content at 150 g/L in the United States, compelling manufacturers to migrate toward water-borne or high-solids chemistries. The combined safety-plus-sustainability pressure rewards suppliers with differentiated resin systems and advanced glass bead solutions that maintain night-time brightness without exceeding emission ceilings.

Rapid Urbanization Boosting Vehicle-Density Management

Cities add complex lane configurations, bus rapid-transit corridors and micro-mobility tracks that collectively elevate the frequency and sophistication of marking work. Photoluminescent lines reduce night-time accident rates on poorly lit arterials, as demonstrated in recent Dublin pilot projects. Thermochromic coatings mitigate the urban heat-island effect by reflecting infrared energy while keeping visual contrast high. Municipal agencies also deploy sensor-equipped pre-formed tapes to feed traffic analytics platforms, opening a fledgling niche for IoT-ready marking consumables.

Machine-Readable Retro-Reflective Markings for AVs

As automated and highly assisted vehicles proliferate, markings must be interpretable by cameras and LiDAR under rain, fog and worn-line scenarios. Contrast-optimized pigments, near-infrared receptive beads and modular maintenance guidelines now appear in tender documents for new freeway sections in California and Bavaria. Pigment developer DIC Corporation recently commercialized Spectrasense Black L 0082, which raises LiDAR return without compromising daytime color fidelity. Industry consortia are harmonizing global performance metrics, signaling a migration path toward ubiquitous AV-compatible striping after 2027.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC & micro-plastic emission norms | -0.7% | Global, with strictest enforcement in EU & California | Short term (≤ 2 years) |

| Petrochemical & Titanium dioxide price volatility | -0.4% | Global supply chain impact | Medium term (2-4 years) |

| Accelerated wear in extreme-climate zones | -0.3% | Desert regions, Arctic zones, tropical monsoon areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC & Micro-Plastic Emission Norms

The latest US amendments to aerosol-coating rules and Canada’s 2023 VOC statute compel continuous reformulation, adding R&D cost and elongating regulatory approvals[2]US Environmental Protection Agency, “National VOC Emission Standards for Aerosol Coatings—Final Rule,” epa.gov . Europe’s forthcoming micro-plastic directive identifies traffic paint abrasion as an emergent pollutant, prompting calls for particulate-shedding life-cycle audits. While studies suggest road markings contribute below 0.07% of total microplastics, compliance pathways—such as encapsulated bead systems and accelerated wear testing—divert capital from new-product marketing toward documentation and certification.

Petrochemical & Titanium Dioxide Price Volatility

Titanium dioxide spot prices posted double-digit swings during 2024, and polyethylene feedstock quotes rose 3 ¢/lb in early 2025, inflating polymer-based stripe margins. Exchange-rate turbulence amplifies costs for Asian converters that import TiO₂ denominated in EUR. Producers attempt hedging with long-term contracts and pigment substitution, yet smaller formulators face squeezed cash flows and occasional supply disruptions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Polymer Innovation Challenges Paint Dominance

Paints continue to anchor demand thanks to 61.05% share in 2025, especially in lower-traffic provincial roads where agencies prioritize first-cost savings. However, polymer systems are capturing incremental budgets, booking a 4.52% CAGR on the strength of methyl-methacrylate and durable pre-formed tapes. Water-borne acrylics see rising specification because they satisfy EPA’s 150 g/L VOC cap without sacrificing drying speed. Conversely, solvent-rich chlorinated rubber paints retreat in North America and Europe under emission scrutiny, yet retain beachhead demand in hot, humid equatorial projects that require rapid moisture resistance.

Thermoplastic—by far the largest polymer sub-class—wins where life-cycle cost is scrutinized. Pourable MMA technologies, curing at ambient temperatures, now permit night-time application even in 0 °C conditions, avoiding costly lane closures. The outlook suggests polymer formulations will approach half of the road marking materials market by the mid-2030s if durability targets continue to tighten.

By Application: Highway Dominance Drives Market Growth

Highways and arterial roads absorb 68.20% of 2025 volume and grow at 4.30% CAGR as governments place connectivity at the center of economic policy. These projects specify thicker film builds, high refractive-index glass beads and machine-readable contrast ratios to future-proof the asset. Car parks, while smaller in tonnage, demand rapid-drying paints free of odor due to proximity to occupied buildings, spawning niche blends of low-VOC epoxy. Factories and warehouses adopt ANSI Z535-compliant safety striping; raised markers and anti-skid ceramic inserts differentiate suppliers. Airport markings, although less than 2% of total tonnage, command premium pricing because FAA AC 150/5340-5D stipulates resistance to jet fuel and rubber deposits. Margins here offset commodity-road competition and justify specialized product lines.

Geography Analysis

Asia-Pacific’s 4.82% CAGR remains unchallenged through 2031. China’s continuing freeway additions and India’s 10% hike in highway budgets support multi-year procurement cycles. The climatic breadth—from Himalayan freeze zones to Thar Desert heat—incentivizes material diversification. North America, while mature, channels stimulus-funded resurfacing cash into compliant low-VOC lines and AV-ready patterns. EPA enforcement and Canada’s 2023 VOC rules demand dual-formulation inventories for cross-border suppliers. Europe’s micro-plastic debate pushes recyclate-rich paints and cradle-to-grave product passports; the region also advances AV lane trials in Germany and the Netherlands. Latin America and the Middle East post mid-single-digit growth anchored in urban ring-road builds and World Cup-driven stadium precinct upgrades, respectively.

Competitive Landscape

The road marking materials market shows moderate consolidation. 3M leverages micro-replication science to sell advanced beads, SWARCO bundles markings with traffic-management hardware, and PPG maintains scale advantages in alkyd and water-borne paints. Recent M&A underscores geographic ambition—Geveko Markings bought PPG’s Australian and New Zealand traffic-solutions arm to deepen Asia-Pacific presence, while SWARCO’s July 2024 purchase of Ireland’s Elmore Group expanded intelligent transport integration. Smaller innovators concentrate on photoluminescent and bio-based resins, using licensing agreements to access global distribution. Entry barriers stay moderate: raw-material access is commoditized, yet compliance testing, warranties and contractor relationships slow new entrant scale-up.

Road Marking Materials Industry Leaders

The Sherwin-Williams Company

Geveko Markings

PPG Industries, Inc.

3M

SWARCO

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Geveko Markings acquired Farby Maestria Polska Sp. z o.o., a road marking materials manufacturer, from Peintures Maestria and minority shareholders. It includes a production and distribution site in Płońsk, near Warsaw, and warehouse facilities in the Warsaw area, aligning with the company's growth strategy in key markets.

- October 2023: Geveko Markings has acquired PPG's Traffic Solutions business in Australia and New Zealand, formerly Ennis-Flint. It includes production facilities in Sydney and Melbourne, distribution centers in Brisbane and Perth, and a sales office in New Zealand.

Global Road Marking Materials Market Report Scope

Road marking is the application of paints or materials on road surfaces, pavements, concrete, or asphalt to communicate information to motorists and pedestrians. Road markings can be applied to various surfaces on roads and highways, pavements, airfields, car parks, racetracks, sports courts, and leisure complexes. Depending on the country, region, and purpose, road markings use a standard system of lines, colors, and marks to convey directions, lanes, zones, speed limits, parking, stopping, and safety. The road marking materials market is segmented by type, application, and geography. By type, the market is segmented into polymer-based markings and paint-based markings. By application, the market is segmented into road markings, factory and warehouse markings, car park markings, airport markings, and others. The report also covers the market size and forecasts for the road marking materials market in 15 countries across major regions. Each segment's market sizing and forecasts are based on revenue (USD).

| Polymer-based Markings | Thermoplastics |

| Cold Plastics | |

| Pre-formed Adhesive Tapes | |

| Raised Pavement Markers | |

| Paint-based Markings | Solvent-based |

| Water-based |

| Road Markings (Road and Highways) |

| Car Park Markings |

| Factory and Warehouse Markings |

| Airport Markings |

| Other Markings (Sports, Leisure, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Material Type | Polymer-based Markings | Thermoplastics |

| Cold Plastics | ||

| Pre-formed Adhesive Tapes | ||

| Raised Pavement Markers | ||

| Paint-based Markings | Solvent-based | |

| Water-based | ||

| By Application | Road Markings (Road and Highways) | |

| Car Park Markings | ||

| Factory and Warehouse Markings | ||

| Airport Markings | ||

| Other Markings (Sports, Leisure, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected size of the road marking materials market by 2031?

The road marking materials market size is expected to reach USD 9.32 billion by 2031, growing at a 4.14% CAGR.

Which region accounts for the largest share of the market?

Asia-Pacific holds the largest road marking materials market share at 40.20% in 2025, driven by extensive highway expansion across China and India.

Why are polymer-based markings gaining popularity?

Polymer systems such as methyl-methacrylate last up to 10 years versus 3-5 years for conventional thermoplastic, lowering life-cycle costs even though first costs are higher.

How are regulations influencing product development?

Stricter VOC caps and emerging micro-plastic limits compel manufacturers to shift toward water-borne or high-solids formulations while ensuring high retro-reflectivity for safety compliance.

Page last updated on: